Radial Artery Compression Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

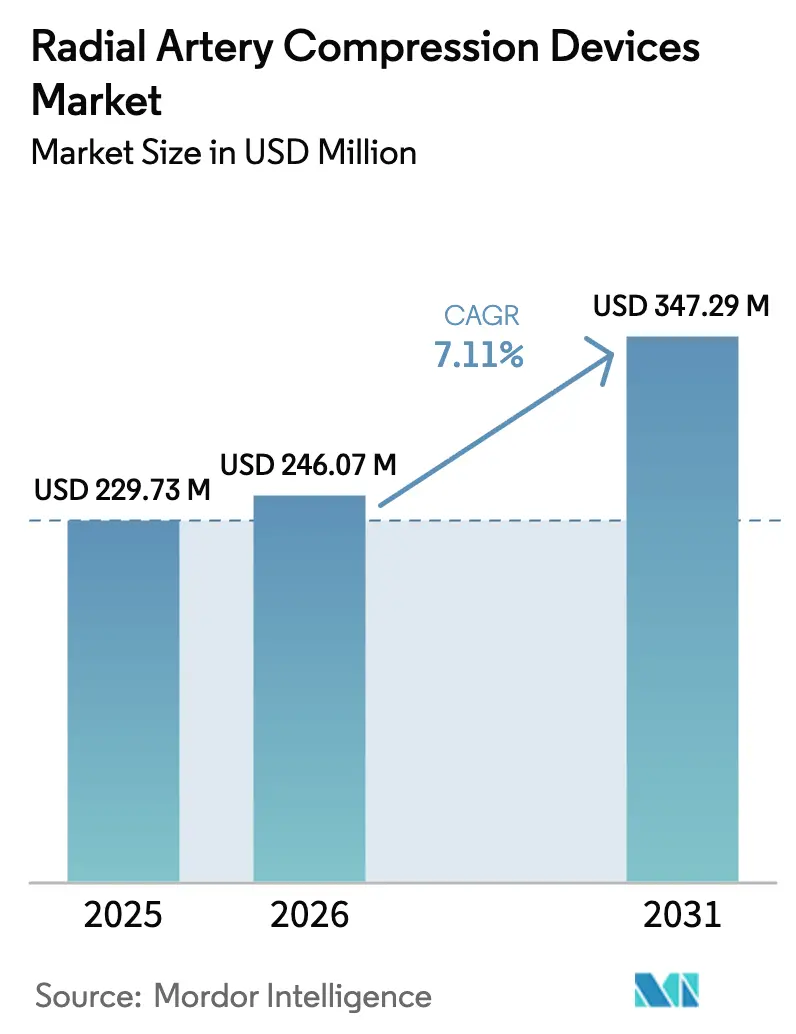

| Market Size (2026) | USD 246.07 Million |

| Market Size (2031) | USD 347.29 Million |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

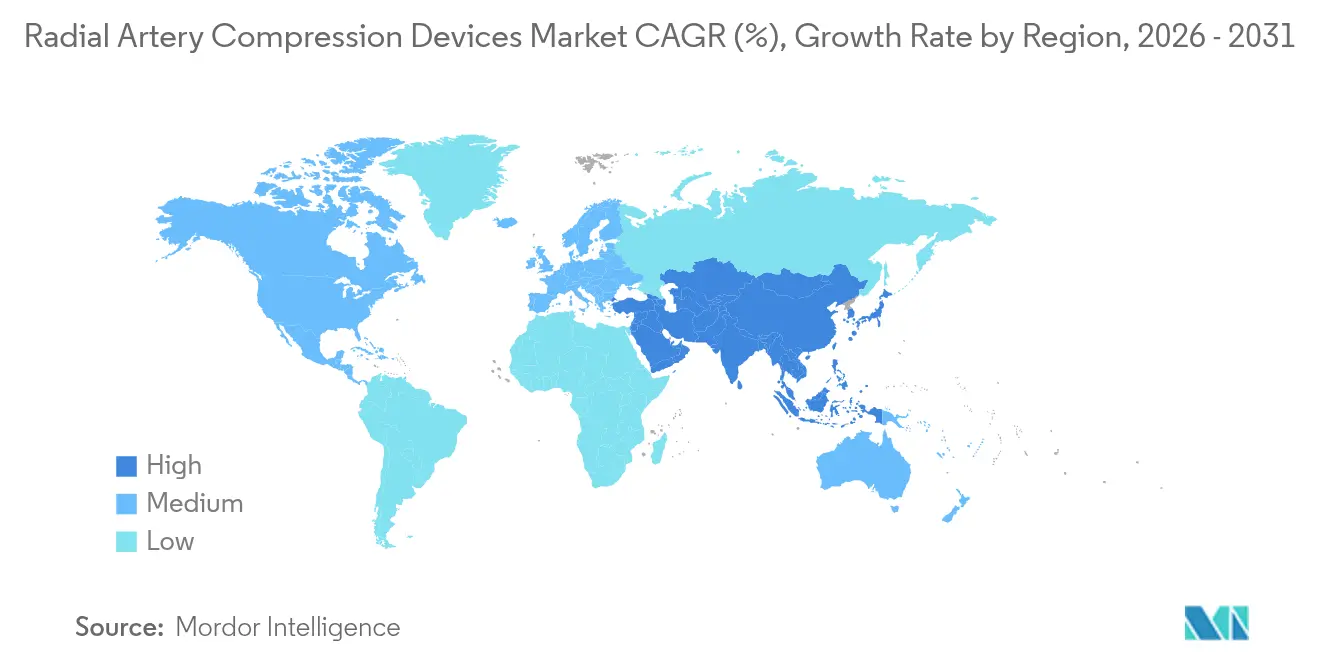

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radial Artery Compression Devices Market Analysis by Mordor Intelligence

The radial artery compression device market size is expected to grow from USD 229.73 million in 2025 to USD 246.07 million in 2026 and is forecast to reach USD 347.29 million by 2031 at 7.11% CAGR over 2026-2031. Growth is anchored in the rapid clinical migration from femoral to transradial access, which reduces bleeding events, shortens recovery times, and supports same-day discharge protocols. The radial artery compression device market also benefits from hospital cost-containment goals because radial procedures cut recovery room occupancy by up to four hours, freeing capacity for higher patient turnover. North America and Europe remain revenue leaders, yet Asia-Pacific registers the highest volume acceleration as training programs scale and reimbursement systems align with radial-first guidelines. Technological advances in pressure-controlled and hybrid devices, alongside patent-hemostasis protocols that keep radial artery occlusion below 2%, further stimulate purchasing activity across high-volume centers.

Key Report Takeaways

- By product type, band or strap systems held 46.82% of the radial artery compression device market share in 2025 and knob-based devices are on course for a 7.64% CAGR to 2031.

- By mechanism, pneumatic units accounted for 59.35% of the radial artery compression device market size in 2025 and hybrid or automatic systems are expanding at a 7.75% CAGR through 2031.

- By usage, disposable cuffs captured 76.55% revenue in 2025 and reusable alternatives are forecast to grow at an 7.88% CAGR between 2026 and 2031.

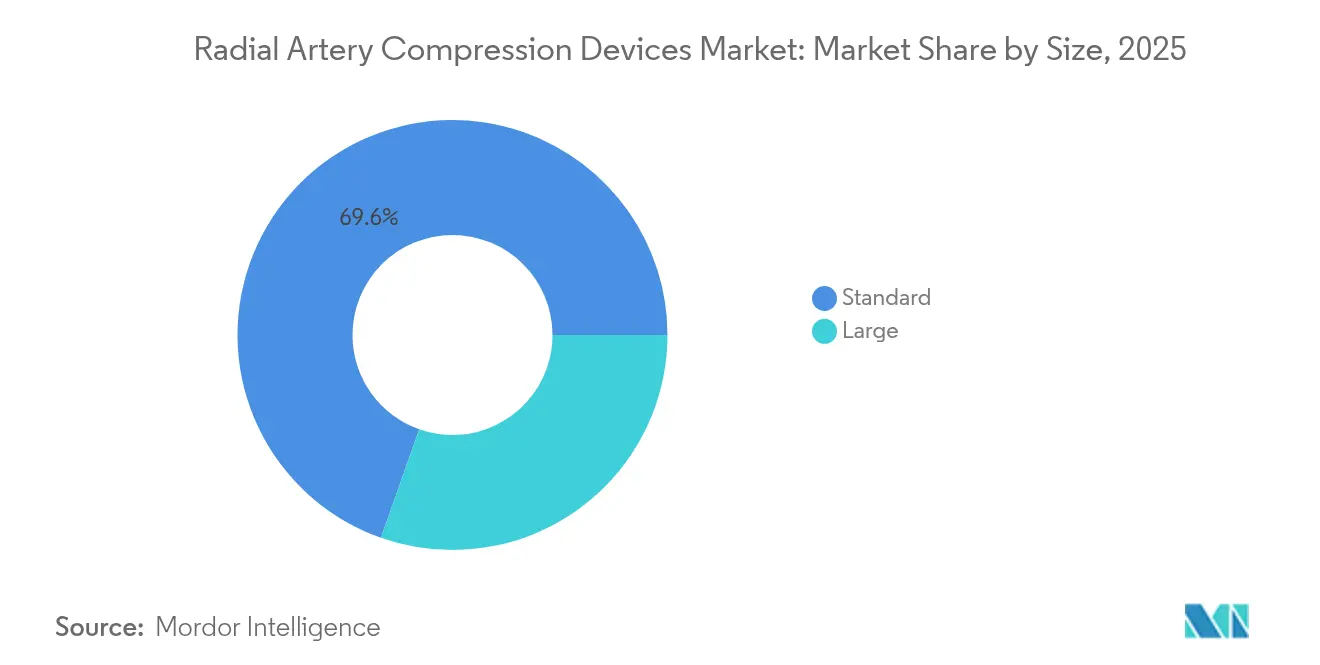

- By size, standard variants represented 69.60% of the radial artery compression device market size in 2025 and large cuffs are rising at an 8.05% CAGR toward 2031.

- By end user, hospitals led with 64.32% share in 2025 and ambulatory surgical centers are advancing at an 8.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radial Artery Compression Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of transradial access for PCI | +2.1% | Global, with strongest impact in North America & Asia-Pacific | Medium term (2-4 years) |

| Rising global cardiovascular disease burden | +1.8% | Global, with pronounced effects in aging populations of developed markets | Long term (≥ 4 years) |

| Cost-savings vs. femoral access in cath labs | +1.4% | North America & Europe, expanding to emerging markets | Short term (≤ 2 years) |

| Emergence of patent-hemostasis protocols | +1.2% | Global, with early adoption in academic medical centers | Medium term (2-4 years) |

| Automation & pressure-controlled devices cut turnover time | +0.9% | Developed markets initially, scaling to high-volume centers globally | Medium term (2-4 years) |

| Outpatient reimbursement shifts favouring radial approach | +0.8% | North America primarily, with EU following regulatory alignment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Transradial Access for PCI

Professional guidelines now recommend a radial-first strategy for acute coronary syndrome, cutting major bleeding events by up to 60% and doubling same-day discharge rates. This institutional endorsement fuels steady procedure growth that anchors recurring demand within the radial artery compression device market. Hospitals favor compression cuffs with transparent windows and color-coded markers that simplify nursing workflows and align with patent-hemostasis protocols. Supplier training programs now certify thousands of clinicians annually, reducing the residual learning curve and locking in product loyalty. Continuous innovation in pressure feedback sensors is expected to lift adoption further across late-adopter community centers.

Rising Global Cardiovascular Disease Burden

Population aging and heightened metabolic risk factors sustain a climb in cardiovascular admissions, ensuring a growing addressable pool for radial procedures. A nationwide study in Japan calculated average savings of USD 387 per PCI when radial access replaced femoral techniques, primarily through shorter admissions and lower transfusion rates. These economic advantages reinforce procurement decisions in both public and private hospitals. Disposable cuffs remain the workhorse in high-volume units that prioritize infection control and swift turnover. Meanwhile, emerging health-policy frameworks in India and China include radial benchmarks within quality dashboards, broadening the base for compression device purchases. As disease prevalence rises, device unit sales are expected to outpace GDP growth in most regions.

Rising Global Cardiovascular Disease Burden

Population aging and heightened metabolic risk factors sustain a climb in cardiovascular admissions, ensuring a growing addressable pool for radial procedures. A nationwide study in Japan calculated average savings of USD 387 per PCI when radial access replaced femoral techniques, primarily through shorter admissions and lower transfusion rates. These economic advantages reinforce procurement decisions in both public and private hospitals. Disposable cuffs remain the workhorse in high-volume units that prioritize infection control and swift turnover. Meanwhile, emerging health-policy frameworks in India and China include radial benchmarks within quality dashboards, broadening the base for compression device purchases. As disease prevalence rises, device unit sales are expected to outpace GDP growth in most regions.

Cost Savings versus Femoral Access in Cath Labs

New evidence from 2024-2025 confirms that transradial arterial access delivers measurable economic value for cardiac catheterization programs. A multicenter analysis presented at the 2024 SCAI Scientific Sessions showed that radial access lowered in-hospital mortality by 0.15%, cut major access-site bleeding by 0.64%, and reduced major vascular complications by 0.21% relative to femoral approaches. Beyond direct procedural savings, hospitals document lower nursing utilization, shorter recovery windows, and fewer high-cost interventions to manage complications, all of which widen operating margins. Ambulatory surgical centers—which treated 3.4 million Medicare beneficiaries last year and are growing procedures at 5.7% annually—describe radial access as a key lever for safeguarding profitability in price-sensitive settings[1]Source: Medicare Payment Advisory Commission, “Report to the Congress. These compounding benefits become more pronounced as facilities gain scale and operator proficiency, creating a reinforcing cycle that accelerates radial adoption even in budget-constrained markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High use of manual gauze/tape in low-resource settings | -1.3% | Emerging markets, rural healthcare facilities globally | Long term (≥ 4 years) |

| Risk of radial artery occlusion (RAO) & medico-legal exposure | -0.9% | Global, with heightened concerns in litigation-prone markets | Medium term (2-4 years) |

| EU-MDR compliance costs elevating device prices | -0.7% | Europe primarily, with spillover effects on global pricing | Short term (≤ 2 years) |

| Medical-grade TPU & PU supply chain constraints | -0.5% | Global manufacturing hubs, affecting all markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Use of Manual Gauze or Tape in Low-Resource Facilities

Many community hospitals in emerging economies still rely on adhesive dressings because unit costs are a fraction of disposable cuffs. Yet randomized trials show compression devices halve hematoma incidence and shorten hemostasis by up to 12 minutes. International donors and public-private partnerships now highlight these downstream savings to justify subsidized device procurement. Manufacturers respond with value-tier bands priced below USD 5 to unlock latent demand without compromising quality control. Conversion from manual methods therefore represents a long-tail growth opportunity for the radial artery compression device market.

Radial Artery Occlusion Risk and Medico-Legal Anxiety

Reported occlusion rates vary from 0.8% in expert centers to 30% in low-volume labs, fueling practitioner apprehension. A 2024 FDA Class I recall involving 334,995 radial kits heightened scrutiny of closure safety and sparked temporary purchasing pauses[2]Source: Center for Devices and Radiological Health, “Recall of ARROW QuickFlash Kits,” fda.gov . Hospitals increasingly restrict product approval to cuffs that support patent-hemostasis and provide post-market surveillance data. Vendors address liability concerns by offering simulation-based credentialing that documents operator proficiency. As clinical variation narrows through training and technology, legal exposure is expected to moderate, yet it remains a near-term drag on universal adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bands Retain Leadership, Knobs Accelerate Adoption

Band or strap devices continued to dominate the radial artery compression device market with 46.82% share in 2025, reflecting long-standing clinical trust and straightforward nurse training. Hospitals value transparent windows that allow visual bleed checks, while color-coded inflation syringes guide novice operators through patent-hemostasis steps. Disposable construction eliminates reprocessing labor, aligning perfectly with cardiac units that average 15–20 percutaneous interventions daily. Manufacturers now enhance existing bands with antimicrobial linings that deter cuff-site dermatitis, an increasingly scrutinized quality metric. Digital printing of QR codes on band tabs links staff to short training videos, reducing onboarding time by 40% in multicenter pilots. Clinical educators stress that correct strap tensioning prevents venous congestion without compromising radial flow, a nuance easier to demonstrate with the familiar band format. Even as premium hybrids emerge, volume purchasing agreements keep bands embedded in formulary lists across multi-hospital systems. The radial artery compression device market therefore shows stable baseline demand for bands, particularly in secondary hospitals that lack capital budgets for automated alternatives.

Knob-based devices are expanding at a 7.64% CAGR to 2031 because their incremental tightening offers finer pressure control suited to distal radial and pediatric cases. A dual-dial architecture lets clinicians set baseline compression then micro-adjust every 15 minutes without cuff removal, a workflow that fits patent-hemostasis protocols endorsed by leading societies. Early adopters report 22% lower nurse intervention counts per patient compared with straps, freeing staff for turnover tasks in high-volume cath suites. Vendors ship pre-calibrated dials with tactile clicks at 25 mmHg intervals, ensuring reproducible settings even in noisy labs. Product brochures emphasize compatibility with ultrasound-guided distal access where wrist articulation demands smaller footprints. Several European buyers bundle knobs with handheld Doppler probes, creating turnkey distal-radial kits that command premium reimbursements. Although unit prices exceed bands by 35–50%, purchasing managers justify spend through fewer post-procedure bleed alarms and shorter recovery chair occupancy. Continued physician fellowship exposure to distal radial techniques is expected to enlarge the addressable pool for knob solutions, cementing their role as the fastest-growing product line within the radial artery compression device market.

By Mechanism: Pneumatic Dominance Faces Hybrid Momentum

Pneumatic cuffs held 59.35% of 2025 revenue, leveraging decades of proven reliability and low part counts that simplify global service logistics. Simple balloon bladders distribute uniform pressure, minimizing hot spots that could induce skin ischemia in frail patients. Quick-release valves permit immediate deflation if bleeding restarts, an essential safety requirement embedded in most cath-lab checklists. Hospitals appreciate that pneumatic syringes cost pennies and integrate with existing arterial sheath kits, keeping supply chains lean. Training time remains minimal because pressure targets rely on straightforward volume markings rather than electronic displays. Yet the radial artery compression device market increasingly values objective pressure readouts, a limitation of purely pneumatic designs in data-driven quality programs.

Hybrid or automatic pressure-controlled devices are projected to rise 7.75% annually as they merge pneumatic bladders with microprocessor feedback loops that measure pulse perfusion beneath the cuff. Optical or piezoelectric sensors transmit flow signals to an LED panel, guiding staged deflation without continuous bedside attendance. Clinical audits at two U.S. academic centers recorded a 34% reduction in radial artery occlusion when hybrid devices replaced manual syringes, tipping committee votes toward capital purchase approvals. Manufacturers preload evidence dashboards on USB drives, allowing quality teams to import RAO trend graphs directly into electronic records. Disposable sensor pads attach via low-cost peel-and-stick connectors, ensuring the core electronics module is reused for 100 cycles before factory recalibration. While acquisition prices challenge smaller hospitals, group purchasing organizations are negotiating lease-to-own models that align monthly fees with procedural volumes. As outcome-based reimbursement spreads, hybrids are positioned to erode pneumatic share steadily, reshaping mechanism preferences within the radial artery compression device market.

By Usage: Disposables Dominate, Reusables Gain Sustainability Traction

Disposable cuffs captured 76.55% share in 2025 because infection-control leaders prefer single-use pathways that remove sterilization variability. One-and-done workflows fit cath-lab turnover targets where 20-minute room flips are routine. Regulatory trendlines reinforce disposables; several U.S. states now require documented high-level disinfection logs for patient-contact equipment, paperwork eliminated when cuffs are discarded. Vendors answer environmental critiques with bio-based TPU films that degrade 60% faster in commercial landfills, meeting rising sustainability targets without altering clinical practice. Barcode integration on each cuff automates lot tracking, enabling rapid recall compliance, a critical feature after recent high-profile device alerts. Contract price per unit continues to fall as manufacturing shifts to high-speed insert-molding facilities in Southeast Asia, supporting volume expansion even in cost-sensitive emerging markets.

Reusable cuffs are enlarging at an 7.88% CAGR as green-procurement committees recalibrate purchasing criteria to include waste-reduction metrics. Autoclavable silicone bladders now withstand 50 steam cycles without pressure drift, validated by bench tests that exceed ISO 10555 burst-pressure thresholds. Several European university hospitals publish life-cycle analyses showing total ownership savings once weekly procedure counts exceed 120, capturing administrator attention. RFID tags embedded into buckle housings record sterilization counts and flag end-of-life thresholds on central dashboards, ensuring patient safety. Vendors provide stainless-steel drying racks and calibration pumps as part of starter bundles, lowering operational hurdles for sterile services teams. Although up-front capital outlays run 3–4 times the price of disposables, amortization over a single fiscal year is feasible in centers performing 3,500 radial cases annually. Rising landfill surcharges and forthcoming EU waste directives bolster the economic case, suggesting reusable penetration will keep climbing, particularly inside the radial artery compression device industry’s high-volume European customer base.

By Size: Standard Options Prevail, Large Cuffs Grow with Obesity Trend

Standard-size cuffs generated 69.60% of the radial artery compression device market size in 2025, covering adult wrist circumferences from 14 cm to 20 cm. Distributors prefer stocking fewer SKUs to streamline par-level management, and clinical educators design in-service modules around the universal fit. Studies show under-sizing inflates RAO risk by 18%, making correct fit critical to outcomes; standard cuffs meet anatomical profiles for most patients in Asia and Europe. Packaging now carries wrist-circumference pictograms, helping technicians choose quickly under time pressure.

Large cuffs, forecast to expand 8.05% per year, address growing obesity prevalence that pushes average wrist size beyond 20 cm in North America and parts of the Middle East. Underscoring the need, bariatric PCI centers report up-sizing rates approaching 35% of all radial cases, more than double the 2019 figure. Vendors engineer larger bladders from three-layer TPU films that maintain even pressure without edge curling. Adjustable Velcro extensions flex around edema-prone wrists, ensuring secure placement. Promotional literature highlights that proper large-cuff usage cuts post-procedure hematoma by 27% compared with stretching a standard cuff across the same patient cohort. Hospitals track size utilization in inventory systems, informing quarterly restocking models that prevent critical gaps. Manufacturers anticipate launching extra-large versions beyond 24 cm circumference by 2026, keeping pace with demographic shifts and safeguarding the radial artery compression device market from performance complaints in high-BMI populations.

By End User: Hospitals Lead, ASCs Accelerate on Outpatient Shift

Hospitals held 64.32% share in 2025, reflecting established cardiology programs, round-the-clock cath-lab staffing and immediate surgical backup. Academic centers average 4,500 radial interventions annually and standardize product choice across affiliated networks, producing high volume for preferred suppliers. Electronic purchasing systems tie cuff requisitions to catheter counts, helping materials managers keep par levels that minimize expiry write-offs. Capital committees favor devices with published peer-review data, reinforcing incumbent brand grip. Hospitals with Magnet nursing status cite reduced nurse workload as a staff-retention tactic, positioning advanced hybrid cuffs as recruitment assets.

Ambulatory surgical centers report the fastest growth at 8.17% CAGR because same-day discharge harmonizes with Medicare outpatient payment schedules. Travel-time statistics show 70% of U.S. residents live within 30 minutes of an ASC, supporting decentralized cardiac care. Centers leverage compact radial procedures that avoid general anesthesia, fitting business models centered on high throughput and limited overnight staff. Device makers court ASC chains with consignment cabinets prepaid on usage, relieving inventory cash flow. Upper Midwest centers piloting hybrid cuffs record five-minute shorter recovery-bay occupancy, enabling an extra case per session and validating premium pricing. Catheterization laboratories embedded within large hospital systems occupy a middle ground, typically employing both disposable bands for diagnostic angiograms and reusable hybrids for complex PCI, underlining the varied procurement logic across the radial artery compression device market.

Geography Analysis

North America remained the largest regional contributor to the radial artery compression device market in 2024, yet procedure penetration still trails international benchmarks. Federal reimbursement is neutral between access routes, but private payers increasingly tie bonus payments to bleeding-avoidance metrics that favor radial protocols. Growth prospects rest on expanding fellowship curricula that embed radial skills early, thereby raising baseline competence among new interventionalists. Canada mirrors U.S. trends yet faces distinct logistical challenges in remote provinces where cath-lab staffing is limited; disposable bands dominate these sites due to simplified logistics.

Europe generated robust revenue anchored by Germany, France and the United Kingdom, despite EU-MDR hurdles that inflate compliance costs per stock-keeping unit. National audits capturing RAO rates now form part of hospital accreditation renewals, compelling administrators to choose devices with proven patent-hemostasis performance. Scandinavian systems integrate cuff SKU consumption data into nationwide quality registries, providing real-time benchmarking that influences tenders. Spain experienced a temporary dip in supply after smaller distributors failed MDR recertification, illustrating how regulation reshapes competitive dynamics. Vendors that invested early in notified-body capacity maintained uninterrupted shipments and gained share during transition periods.

Asia-Pacific delivered the highest procedural growth, led by South Korea’s 82.4% radial adoption and Japan’s documented USD 387 cost savings per PCI. China’s Healthy China 2030 plan funded over 1,800 cath labs since 2022, many staffed by returnee cardiologists trained in radial techniques abroad. Domestic manufacturers supply cost-optimized mechanical cuffs, but tertiary centers still import premium hybrids that conform with international trial protocols. India’s private hospital chains negotiate multi-year master agreements bundling arterial sheaths and cuffs, leveraging volume for 15% price discounts. Southeast Asian ministries now accept radial competency hours toward cardiology board certification, expanding practitioner pools. Together these initiatives accelerate the radial artery compression device market across Asia-Pacific, with procedural volumes forecast to grow at double the global average through 2030.

Competitive Landscape

The radial artery compression device market shows moderate concentration. Terumo maintains leadership through its TR Band series combined with intensive clinician-training programs that certify over 5,000 operators each year. Merit Medical capitalizes on cross-selling opportunities within its vascular access line, integrating WRAPSODY stent-graft data into closure-device proposals to present an end-to-end solution. Teleflex completed a EUR 760 million acquisition of BIOTRONIK’s vascular intervention business in July 2025, adding European production capacity and broadening its physician-education footprint.

Technology differentiation now centers on sensor-guided pressure modulation. Abbott pilots Bluetooth-enabled cuffs that stream deflation profiles to cloud dashboards, assisting quality teams in benchmarking RAO outcomes across campuses. Japanese start-up FlowGuard gained CE mark for an algorithm-driven device that halts deflation if pulse amplitude falls below preset thresholds, though commercial rollout awaits reimbursement approval. Chinese firms pursue price leadership by integrating cuffs into sheath kits, shaving logistics costs for provincial hospitals.

Strategic moves include Terumo’s USD 30 million plant in Puerto Rico that localizes supply to the Americas and mitigates maritime disruption risks. Cardinal Health launched a new compression system in November 2024, targeting GPO contracts with bundled disposables. Competitive tender documents increasingly request evidence of environmental stewardship; reusable portfolio owners highlight waste-tonnage reductions, while disposable specialists tout recyclable materials. Over the next five years, consolidation is expected among mid-tier European firms struggling with MDR overheads, potentially increasing share for multinational incumbents within the radial artery compression device market.

Radial Artery Compression Devices Industry Leaders

TERUMO CORPORATION

Abbott

Teleflex Incorporated

Lepu Medical Technology(Beijing)Co.,Ltd.

TZ Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed its EUR 760 million acquisition of BIOTRONIK’s vascular intervention business Teleflex completed its EUR 760 million acquisition of BIOTRONIK’s vascular intervention business

- February 2024: Terumo broke ground on a USD 30 million manufacturing facility in Puerto Rico

Global Radial Artery Compression Devices Market Report Scope

As per the report's scope, a radial artery compression device is designed to assist in hemostasis of the radial artery after specific medical procedures, particularly cardiac catheterization or coronary angiography. The device reduces bleeding complications and provides functionality and consistent performance after surgical procedures.

The radial artery compression devices market is segmented into products, usage, applications, end-user, and geography. By product type, the market is segmented into band/strap-based, knob-based, and plate-based. By usage, the market is segmented into replaceable devices and reusable devices. By application, the market is segmented into surgical intervention and diagnostics. By end-user, the market is segmented into hospitals, ambulatory surgical centers, and others (research institutes and cath labs, among others). By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Band/Strap-based Devices |

| Knob-based Devices |

| Plate-based Devices |

| Others |

| Pneumatic |

| Mechanical |

| Hybrid / Automatic Pressure-Controlled |

| Disposable |

| Reusable |

| Standard |

| Large |

| Hospitals |

| Ambulatory Surgical Centers |

| Catheterization Laboratories |

| Others |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Band/Strap-based Devices | |

| Knob-based Devices | ||

| Plate-based Devices | ||

| Others | ||

| By Mechanism | Pneumatic | |

| Mechanical | ||

| Hybrid / Automatic Pressure-Controlled | ||

| By Usage | Disposable | |

| Reusable | ||

| By Size | Standard | |

| Large | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Catheterization Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What total revenue will the radial artery compression device market likely achieve by 2031?

Forecasts indicate USD 347.29 million by 2031, reflecting a 7.11% CAGR over 2026-2031.

Which device format is most widely used in hospitals today?

Band or strap-based cuffs remain the most common, accounting for 46.82% of 2025 global sales.

Why are ambulatory surgical centers increasing their use of radial compression devices?

ASCs favor radial access for same-day discharge and have recorded 8.17% annual growth in device adoption through 2031.

How do hybrid automatic cuffs improve safety compared with pneumatic models?

Hybrids use sensors to adjust pressure automatically, supporting patent-hemostasis and lowering radial artery occlusion incidence to below 2% in leading programs.

What regulatory issue most affects device pricing in Europe?

EU-MDR certification costs of EUR 5,000100,000 per product elevate production expenses and influence final pricing across European hospitals.

Which region is expected to record the fastest procedural growth during the forecast period?

Asia-Pacific is poised for the highest growth as co

Page last updated on: