Women Active Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 98.52 Billion |

| Market Size (2031) | USD 142.69 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Women Active Wear Market Analysis by Mordor Intelligence

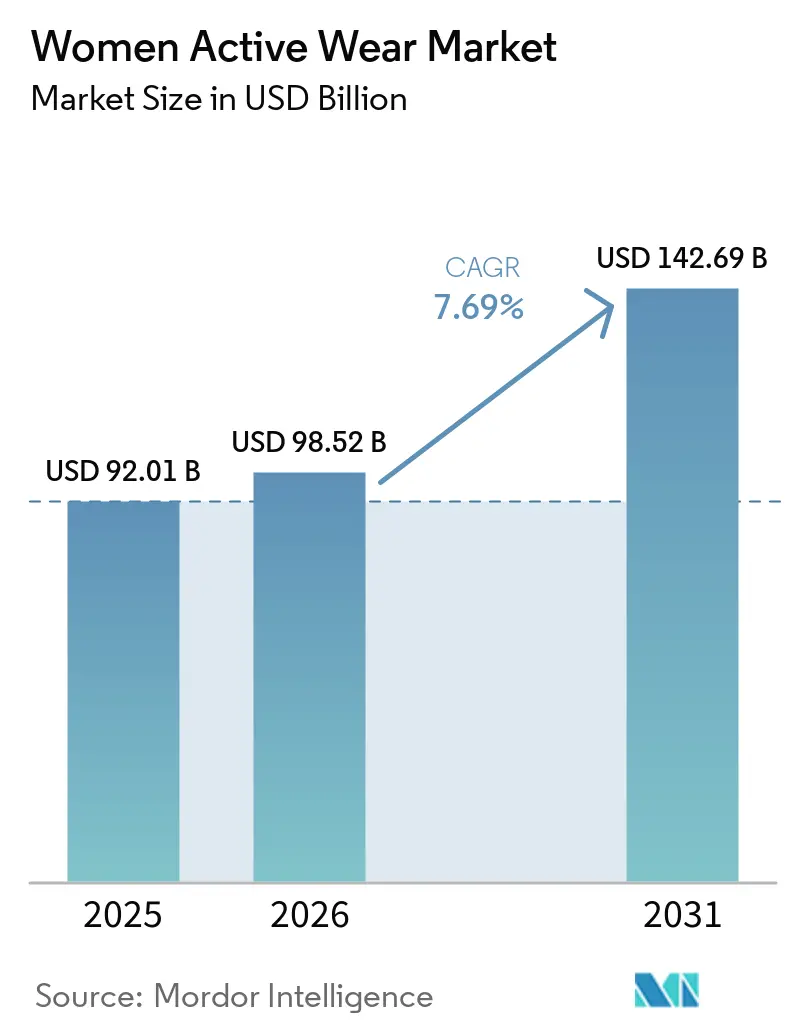

The women's active wear market size was USD 92.01 billion in 2025, and is projected to reach USD 98.52 billion in 2026, and USD 142.69 billion by 2031, growing at a CAGR of 7.69% from 2026 to 2031. Greater female participation in organized sports, expanding gym and boutique-fitness memberships, and brand investments in body-inclusive sizing keep demand on an upward trajectory. Quick adoption of performance fabrics that regulate temperature, repel odor, and enhance compression supports premium price realization. Visibility of athleisure looks across social platforms normalizes leggings and sports bras as everyday apparel, adding non-sport occasions to the purchase funnel. Leading brands incorporate recycled polyester and plant-based elastane to satisfy eco-conscious shoppers, while start-ups test biodegradable dyes as an emerging differentiator. Retailers deepen omnichannel models so shoppers can buy online, pick up in store, or return curbside, limiting friction and reducing basket abandonment.

Key Report Takeaways

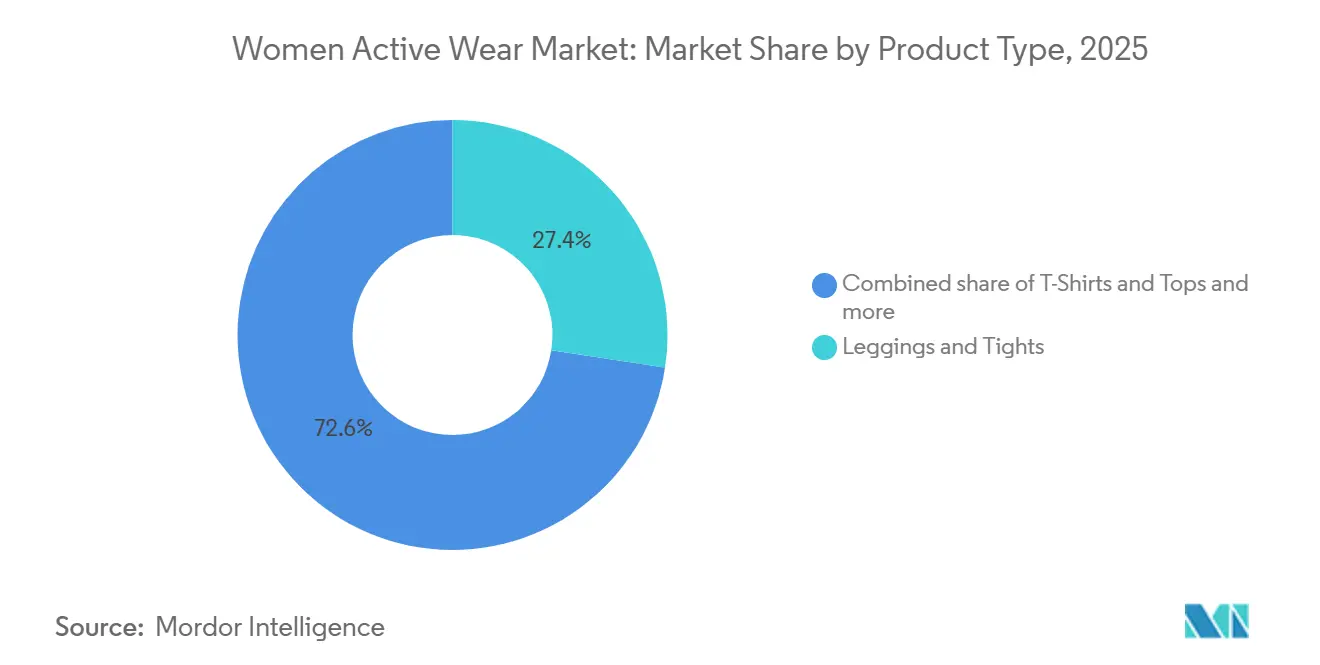

- By product type, leggings and tights held 27.42% of the women active wear market share in 2025, while sports bra is forecast to expand at a 7.92% CAGR between 2026 and 2031.

- By category, conventional/synthetic accounted for 85.25% revenue share of the women active wear market size in 2025, and sustainable/organic are projected to grow at a 8.75% CAGR through 2031.

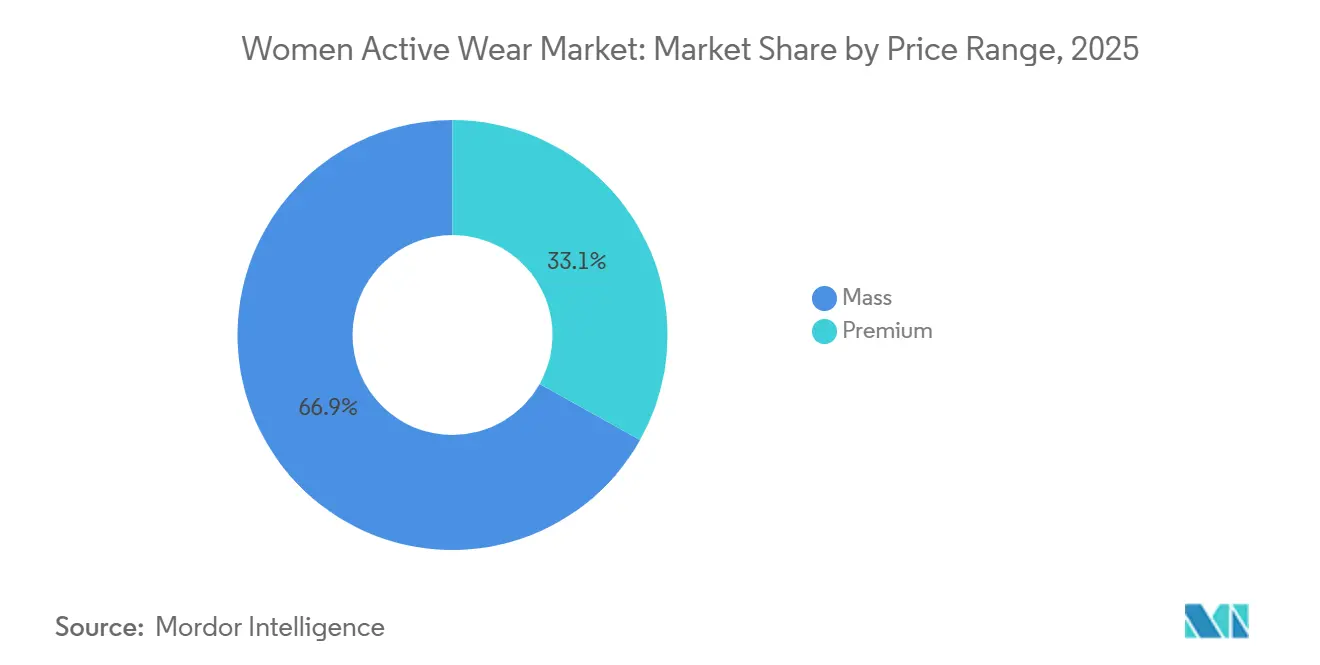

- By price range, mass labels commanded 66.87% of 2025 sales, whereas premium collections are set to register a 9.06% CAGR over 2026 - 2031.

- By distribution channel, specialty stores captured 52.68% of the 2025 value, and online retail stores are poised for a 8.59% CAGR to 2031.

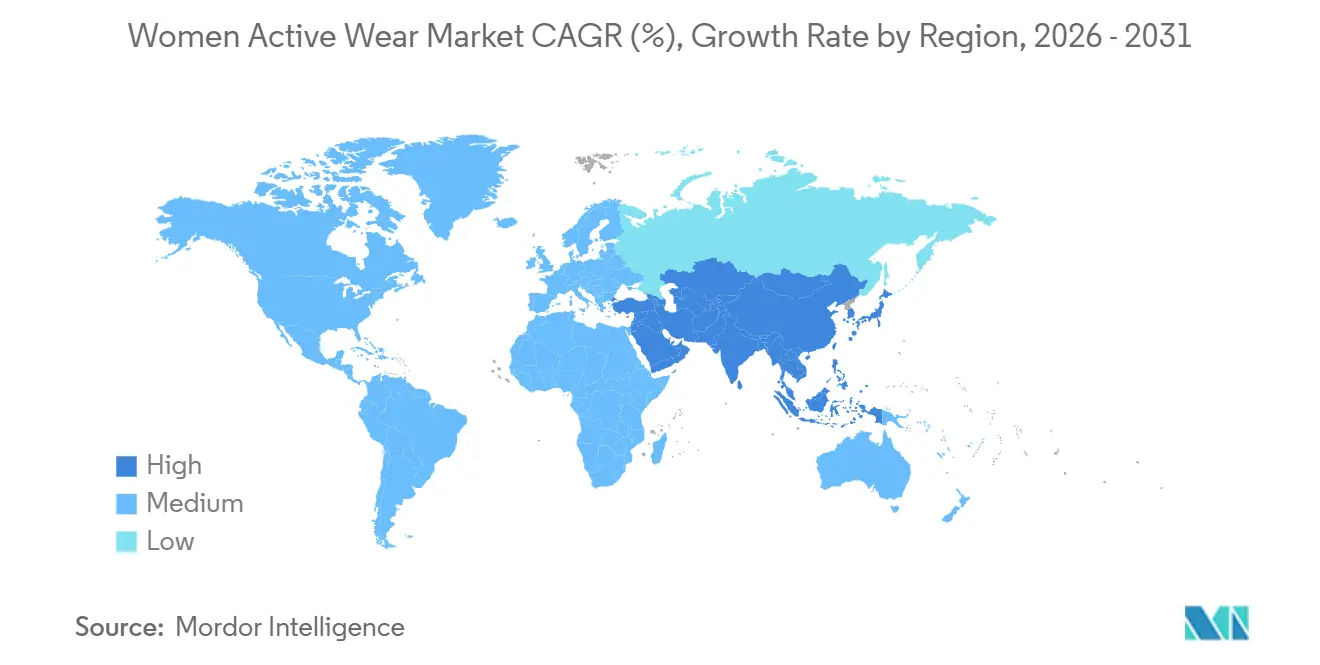

- By geography, North America contributed 46.91% to 2025 revenue, while Asia-Pacific is anticipated to post a 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Women Active Wear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing female involvement in sports and fitness | +2.1% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growing awareness and focus on health and wellness | +1.8% | Global, particularly pronounced in developed markets | Long term (≥ 4 years) |

| Rising demand for sustainable, eco-friendly materials | +1.4% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Social media trends and influencer/celebrity impact | +1.2% | Global, with highest penetration in North America and Europe | Short term (≤ 2 years) |

| Trend-driven designs and body-positive styling | +0.9% | North America and Europe primarily, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Advancements in performance fabrics and smart textiles | +1.1% | Global, led by technology-advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing female involvement in sports and fitness

Participation in amateur leagues, school athletics, and community running clubs continues to widen the women’s active wear market consumer base. National federations report record enrollment for women’s soccer and cricket in 2026, opening more on-field uniform contracts. Large gym chains allocate additional floor space for female-only training zones, signaling that equipment makers and apparel brands can customize lines for those spaces. Manufacturers promote inclusive sizing up to 6XL, reinforcing the notion that every body type is welcome in sport. According to the Sport England survey (2023-2024), 76% of women in England actively engaged in sports or physical activities, demonstrating a fundamental shift toward health-conscious, active lifestyles [1]Source: Sport England, "Sports participation rate among women in England", sportengland.org. This widespread participation drives continuous market expansion and product innovation as women seek specialized apparel for diverse athletic pursuits. Collectively, these shifts elevate volume demand and premium mix in the women’s active wear market

Growing awareness and focus on health and wellness

Health-tracker adoption doubled in the United States between 2024 and 2026, nudging wearers toward daily activity goals that call for comfortable attire. This surge in health-conscious behavior has led to a noticeable uptick in sales for fitness-related apparel. As more Americans prioritize their health, the demand for stylish yet functional active wear has never been higher. Governments in Germany, Japan, and Australia subsidize community fitness programs, indirectly boosting equipment and attire purchases. These subsidies not only promote healthier lifestyles but also stimulate local economies through increased retail activity. Such initiatives underscore the global recognition of fitness as a cornerstone of public health. Medical journals highlight physical-activity benefits for mental wellness, encouraging physicians to prescribe exercise, which translates into retail store visits. This endorsement from the medical community lends credibility to the fitness movement, further driving consumer interest. Brands collaborate with nutrition and mindfulness apps to bundle apparel discounts with membership subscriptions, integrating the women’s active wear market into broader wellness ecosystems. These partnerships signify a shift in how brands view their role in consumers' lives, moving beyond mere transactions to holistic wellness contributors.

Rising demand for sustainable, eco-friendly materials

As consumers become more environmentally conscious, they're scrutinizing the ecological footprint of their fashion choices. This heightened awareness is compelling brands to be more transparent, with many now publishing detailed life-cycle assessments for each garment. In a notable move towards sustainability, Patagonia and Adidas unveiled leggings crafted from 70% recycled ocean plastics in 2025, showcasing a commitment to commercial-scale circularity. Meanwhile, European Union directives set to take effect in 2027 mandate producers to finance recycling schemes, offering a regulatory advantage to early adopters. Start-ups are making waves by sourcing biosynthetic elastane from sugarcane, a move that significantly curtails dependence on traditional petrochemical feedstocks. Retailers are also jumping on the bandwagon, dedicating "conscious collection" sections in stores that boast a higher full-price sell-through rate compared to standard racks. These trends underscore the growing importance of sustainability as a key differentiator in the competitive women's active wear market.

Social media trends and influencer/celebrity impact

Influencers with micro-followings under 50,000 achieve higher engagement rates than mega-celebrities, prompting brands to ink thousands of modest-value deals that collectively shape fashion narratives. This shift underscores the evolving landscape of brand partnerships, where authenticity often trumps sheer reach. Viral treadmill-walking challenges on TikTok popularized matching pastel sets, sending search spikes for “buttery soft leggings.” Such trends highlight the platform's power in dictating fashion fads, with users eagerly chasing the latest viral sensations. Celebrity trainers launch co-branded capsules that sell out within hours when livestreamed, fusing entertainment with commerce. This phenomenon showcases the blurring lines between fitness, celebrity culture, and retail, captivating audiences in real-time. Platforms integrate one-click checkout within reels, shrinking the path to purchase to under 30 seconds. This innovation not only streamlines the shopping experience but also capitalizes on the fleeting nature of online trends. These dynamics propel immediate sell-through and frequent style refreshes within the women’s active wear market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising production costs and raw material expenses | -1.6% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Counterfeiting issues and intellectual property concerns | -0.8% | Global, concentrated in regions with weak IP enforcement | Medium term (2-4 years) |

| Fierce competition and brand oversaturation in the market | -1.1% | Mature markets primarily, spreading to emerging economies | Medium term (2-4 years) |

| Global supply chains: navigating complexity and risks | -0.9% | Global, with highest impact on brands with concentrated sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising production costs and raw material expenses

Raw material cost fluctuations significantly impact profit margins, compelling brands to implement strategic pricing approaches while maintaining profitability targets, especially in mass-market segments where consumer price sensitivity limits the ability to transfer costs. The volatility in polyester and nylon prices, driven by dynamic petroleum market conditions and ongoing supply chain disruptions, directly influences the production costs of essential performance fabrics in modern active wear manufacturing. These cost pressures intensify substantially as brands transition to sustainable materials and implement advanced manufacturing processes, which demand premium input costs and require extensive research and development investments. The escalating labor costs across major manufacturing regions further amplify these challenges, prompting brands to explore comprehensive supply chain diversification strategies that effectively balance cost optimization with stringent quality standards and consistent delivery performance.

Counterfeiting issues and intellectual property concerns

Counterfeiting and intellectual property violations significantly constrain the global women's active wear market by undermining brand integrity, diminishing revenue streams, and eroding consumer trust. The market faces substantial challenges from counterfeit products across multiple categories, including leggings, tops, and performance wear. These unauthorized replicas consistently use substandard materials and poor manufacturing processes, creating serious health risks and severely diminishing customer satisfaction. The widespread presence of counterfeit products deeply affects consumer confidence, with a growing number of customers expressing strong hesitation to purchase or recommend brands that have been targeted by counterfeiters. The rapidly increasing sophistication of counterfeit operations, particularly in producing high-quality replicas that meticulously mimic authentic products, makes detection increasingly complex and resource-intensive. The implementation of comprehensive anti-counterfeiting measures substantially increases operational costs, particularly affecting small and medium-sized brands in their competitive market positions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sports Bras Drive Innovation Leadership

Leggings and Tights accounted for 27.42% of global women active wear market revenue in 2025, making them the leading product category. Their dominance is driven by the growing convergence of performance wear and athleisure, with consumers seeking versatile apparel for workouts and casual wear. Innovations in moisture-wicking, compression, seamless, and sculpting fabrics have strengthened demand, while premium features such as pockets and high-waist designs enhance appeal. T-shirts and tops remain a major segment, while joggers, sweatpants, and track pants, jackets, hoodies, and sweatshirts, and shorts and skirts benefit from increasing demand for comfortable and seasonally adaptable activewear.

Sports Bras are projected to be the fastest-growing product segment, registering a CAGR of 7.92% during 2026–2031. Rising participation in sports, running, yoga, and gym activities, along with increasing emphasis on comfort and support, is driving demand. Brands are introducing seamless designs, moisture-management fabrics, adjustable support levels, and inclusive sizing to meet evolving preferences. Meanwhile, other product types, including niche apparel categories, continue to support market growth by addressing specialized requirements and expanding product portfolios.

By Category: Sustainable/Organic Segment Accelerates Beyond Conventional/Synthetic Products

Conventional/Synthetic products accounted for 85.25% of global women active wear market revenue in 2025, making them the dominant category. Their leadership is supported by the widespread use of polyester, nylon, elastane, and conventional cotton, which offer durability, stretch, moisture management, and cost efficiency. These materials enable manufacturers to deliver high-performance apparel at competitive price points across various activities and price tiers. Their established supply chains and broad consumer acceptance continue to underpin demand across key product segments, including leggings, tops, sports bras, and outerwear.

Sustainable/Organic products are projected to be the fastest-growing category, registering a CAGR of 8.75% during 2026–2031. Rising consumer awareness regarding environmental impact, coupled with increasing adoption of recycled polyester, recycled nylon, and organic cotton, is driving growth. Brands are investing in eco-friendly materials, circular fashion initiatives, and low-impact production processes to strengthen sustainability credentials. Although representing a smaller share of the market, sustainable and organic activewear is gaining traction among environmentally conscious consumers and supporting portfolio diversification across premium and mainstream offerings.

By Price Range: Premium Segment Outpaces Market Growth

Mass brands, leveraging their extensive retail footprints and price-sensitive strategies, accounted for a significant 66.87% of the 2025 revenue, particularly appealing to first-time buyers. Supermarket chains, recognizing the trend, have expanded their private-label collections, now bundling sports bras and leggings for under USD 35. Yet, it's the premium ranges that are projected to enjoy a notable 9.06% CAGR, driven by advanced materials, compelling ethical sourcing narratives, and the allure of limited runs. Shoppers, increasingly discerning, justify their willingness to pay a premium by emphasizing garment durability and alignment with their personal status.

Premium players, keen to avoid the pitfalls of overproduction, are turning to made-to-order micro-drops, ensuring a full-margin sell-through. Meanwhile, influencer-co-designed capsules are not just trendy; they create halo effects, boosting the appeal of adjacent core collections. Mass retailers, in a bid to innovate, are experimenting with “bridge” sub-labels. These labels incorporate select premium features, like bonded seams or recycled yarns, yet cleverly maintain a value-centric messaging. This strategic tiering not only caters to price-sensitive segments but also gently nudges them towards upgrades, crafting a multi-layered offer structure within the women's active wear market.

By Distribution Channel: Digital Transformation Accelerates

Specialty stores represented 52.68% of 2025 sales, showcasing technical fits under expert guidance that online mock-ups cannot yet replicate. Store staff employs 3D-scanning kiosks to recommend precise sizes, driving lower return rates. Physical locations double as community hubs for running clubs and wellness talks, deepening customer stickiness. These initiatives not only enhance customer loyalty but also foster a sense of belonging among patrons. As a result, specialty stores are carving out a unique niche in an increasingly digital world.

Online retail stores are increasing with a CAGR of 8.59% from 2026 to 2031. Direct-to-consumer platforms personalize landing pages based on browsing history, elevating conversion. Hybrid models such as “reserve online, fit in store” neutralize hesitation around sizing. Marketplaces invest in authenticity badges, reassuring shoppers wary of counterfeits. Social-commerce integrations allow in-feed checkouts, shrinking the path to purchase. With the rise of influencer marketing, brands are leveraging social media personalities to further boost their visibility and credibility. As bandwidth costs fall, livestream shopping exposes global audiences to niche capsule drops, extending geographical reach for emerging designers within the women’s active wear market.

Geography Analysis

North America led the women’s active wear market in 2025 with 46.91% revenue share, propelled by high disposable incomes and gym penetration of the adult population. U.S. collegiate athletics allocate increasing budgets for female team uniforms, sparking contracts that guarantee baseline volumes for suppliers. Canada witnesses strong demand for cold-weather performance tights with brushed interiors as winter sports participation grows. Mexico’s middle-class expansion creates a rising pool of urban fitness enthusiasts, motivating global brands to localize sizing and marketing messages. Local governments fund fitness-centric urban redevelopment, embedding jogging tracks into city parks and sustaining apparel sales.

Europe remains a mature yet innovation-focused cluster, contributing notable sustainability momentum to the women’s active wear market size. Germany pioneers biodegradable elastane research through joint university-industry grants. The United Kingdom’s athleisure penetration surges as hybrid work supports all-day leggings. Italian mills leverage design heritage to craft premium compressive fabrics, bolstering the regional luxury segment. French consumers embrace inclusive sizing campaigns, while Spain’s seaside running events push UV-protective tops. Across the bloc, repair and resale programs extend garment life, aligning with EU circular-economy policies.

Asia-Pacific is projected to post the fastest 8.33% CAGR through 2031, underpinned by burgeoning female sports leagues in China and India. E-commerce festivals such as Singles’ Day move millions of units in minutes, reflecting digital savviness. Japan’s demographic aging paradoxically boosts demand, as seniors adopt low-impact yoga routines that still require flexible attire. Australia’s surf culture migrates inland via athleisure-inspired board-short leggings. Southeast Asian influencers localize Western trends, customizing modest silhouettes for cultural fit. This region’s factory base also positions it as both major consumer and supplier, intertwining domestic demand with export opportunity in the women’s active wear market.

Competitive Landscape

The women's active wear market, while moderately concentrated, sees established global players leveraging brand equity, expansive distribution networks, and innovative prowess to carve out competitive advantages. However, these industry stalwarts are increasingly challenged by the rise of direct-to-consumer brands and those prioritizing sustainability. Through athlete endorsements, tech collaborations, and a lifestyle-centric approach, market leaders fortify their positions. In contrast, emerging brands are carving their niche, focusing on community engagement and swiftly adapting product cycles to resonate with consumer tastes. Key players shaping the landscape include Adidas AG, Nike, Inc., Puma SE, Under Armour, Inc., and Lululemon Athletica Inc.

In the global women's active wear market, companies are forging partnerships centered on technological innovations to carve out strategic differentiations. By channeling investments into research and development, these companies are seamlessly integrating advanced fabric technologies. These include moisture-wicking capabilities, temperature regulation, four-way stretch features, and a commitment to sustainable materials. Such innovations not only bolster the performance, comfort, and functionality of active wear but also arm companies with a competitive edge, adeptly catering to a spectrum of consumer needs.

Both new entrants and established players are eyeing significant opportunities in segments that remain underserved. For instance, adaptive active wear tailored for women with disabilities not only fills a market gap but also champions an essential consumer base. This segment emphasizes inclusive design features and user-friendly elements. Furthermore, there's a burgeoning demand for maternity and postpartum fitness wear. This niche caters to women keen on fitness, offering apparel that adapts to their evolving body shapes and prioritizes comfort.

Women Active Wear Industry Leaders

-

Adidas AG

-

Nike, Inc.

-

Puma SE

-

Under Armour, Inc.

-

Lululemon Athletica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Crew Clothing has introduced a new technical active wear collection for men and women. The collection features styles designed for various activities, ranging from low-impact yoga and reformer Pilates to higher-intensity Hyrox workouts, padel games, and running.

- March 2025: Old Navy launched a comprehensive new active wear collection featuring versatile leggings, performance tops, and figure-flattering jackets in Regular, Tall, and Petite sizes.

- February 2025: Nike has partnered with Skims to introduce an innovative active wear line. The strategic collaboration, named NikeSKIMS, will offer a comprehensive range of apparel, footwear, and accessories.

- June 2024: SOIE launched a new active wear collection designed for various physical activities and sports, ranging from low to high impact. The products focus on performance enhancement while maintaining style.

Global Women Active Wear Market Report Scope

Active wear is utility clothing for athletes engaged in sports and fitness activities. It helps enhance the performance of athletes, owing to its various advantages, such as enhanced grip, wicking function, and bi-stretchable characteristics. The Women's Active Wear Market is Segmented by Product Type (Topwear, Bottomwear, Outerwear, and Accessories), Activity (Running and Cycling, Gym and Fitness, and More), Category (Mass and Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, and Other Distribution Channels), and Geography (Europe, North America and More). The Market Forecasts are Provided in Terms of Value (USD).

| T-Shirts and Tops |

| Leggings and Tights |

| Sports Bras |

| Shorts and Skirts |

| Joggers, Sweatpants, and Track Pants |

| Jackets, Hoodies, and Sweatshirts |

| Other Product Types |

| Conventional/Synthetic |

| Sustainable/Organic |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | T-Shirts and Tops | |

| Leggings and Tights | ||

| Sports Bras | ||

| Shorts and Skirts | ||

| Joggers, Sweatpants, and Track Pants | ||

| Jackets, Hoodies, and Sweatshirts | ||

| Other Product Types | ||

| By Category | Conventional/Synthetic | |

| Sustainable/Organic | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the women’s active wear category in 2026?

The women’s active wear market size reached USD 98.52 billion in 2026, reflecting sustained global demand.

Which region is expanding fastest for women’s athletic apparel?

Asia-Pacific is forecast to grow at a 8.33% CAGR through 2031, fueled by urbanization, rising incomes, and social-commerce uptake.

Which product sub-segment shows the highest future growth?

Outerwear leads with a projected 7.92% CAGR as consumers seek weather-adaptive pieces that transition beyond gyms.

Why are premium active wear lines outperforming mass options?

Consumers pay for advanced fabrics, certified sustainability, and recovery-oriented functionality, driving a 9.06% CAGR for premium collections.

Page last updated on: