Racing Simulator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

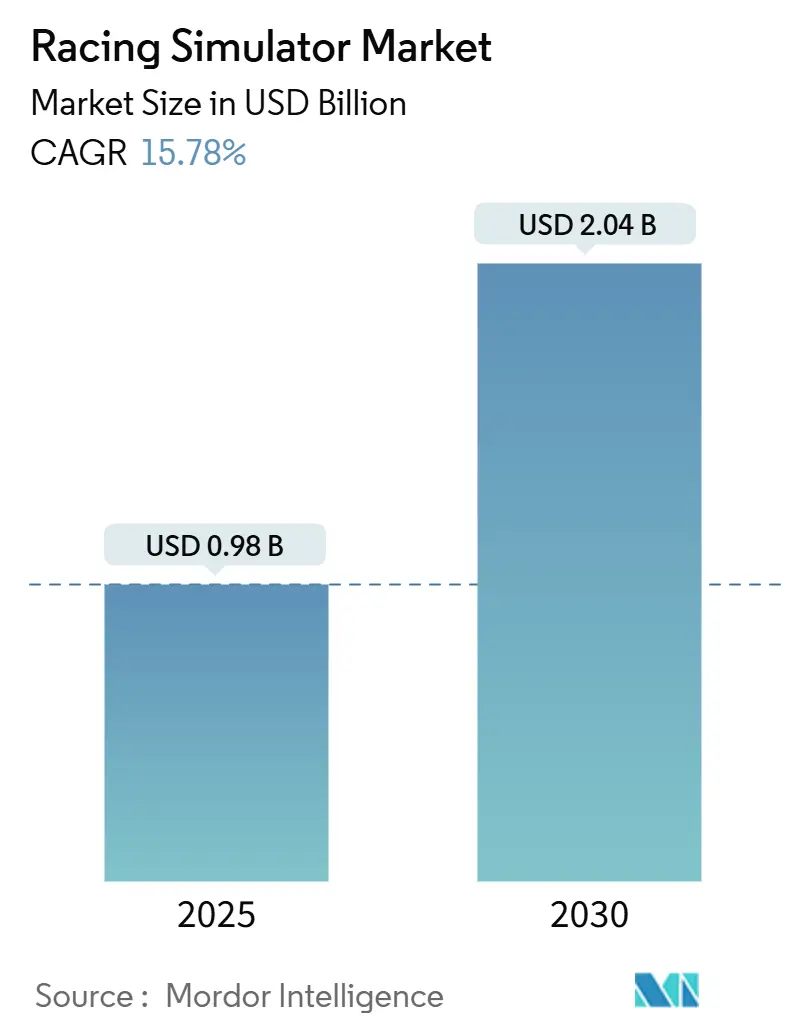

| Market Size (2025) | USD 0.98 Billion |

| Market Size (2030) | USD 2.04 Billion |

| Growth Rate (2025 - 2030) | 15.78% CAGR |

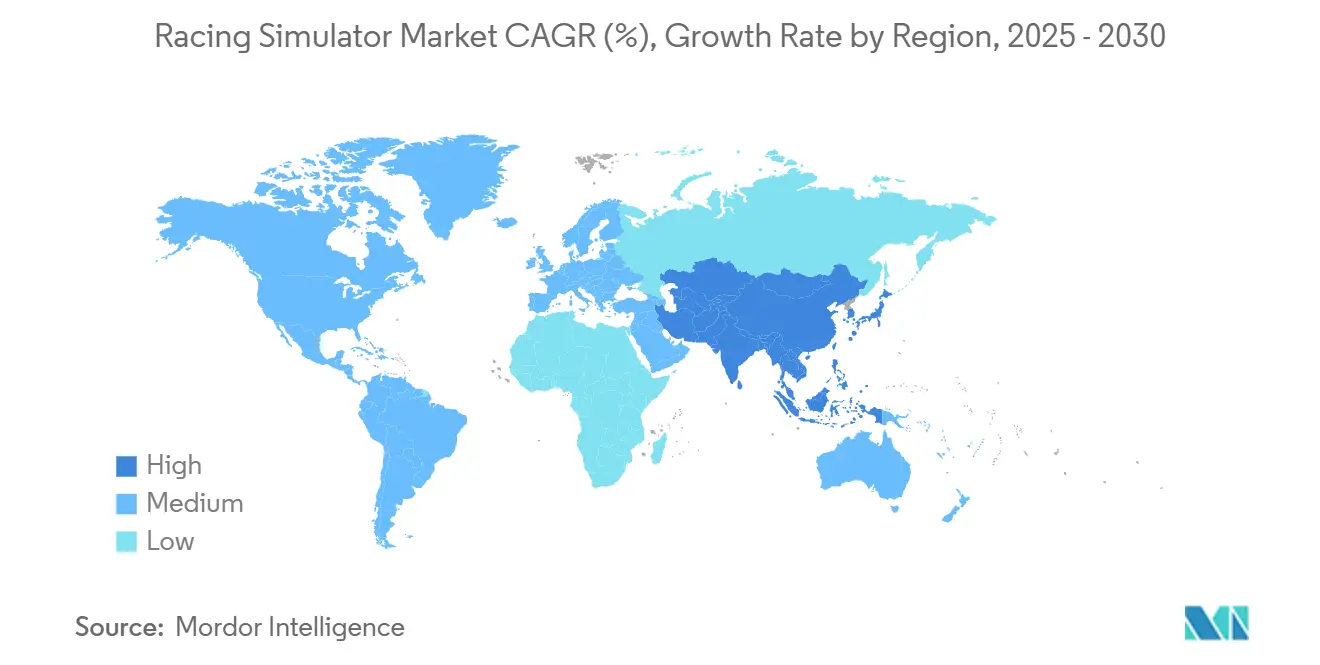

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Racing Simulator Market Analysis by Mordor Intelligence

The racing simulator market size is USD 0.98 billion in 2025 and is projected to reach USD 2.04 billion by 2030, registering a 15.78% CAGR. Growing tournament prize pools, professional motorsport adoption, and declining hardware prices together fuel expansion in both consumer and commercial segments. Esports organizers now stipulate uniform equipment, converting competition specifications into mass-market demand. Automotive original equipment manufacturers embed simulators in driver development programs, shifting the technology’s image from hobbyist pastime to indispensable training asset. Meanwhile, online channels simplify configuration and global delivery, helping mid-level rigs reach gamers in price-sensitive regions.

Key Report Takeaways

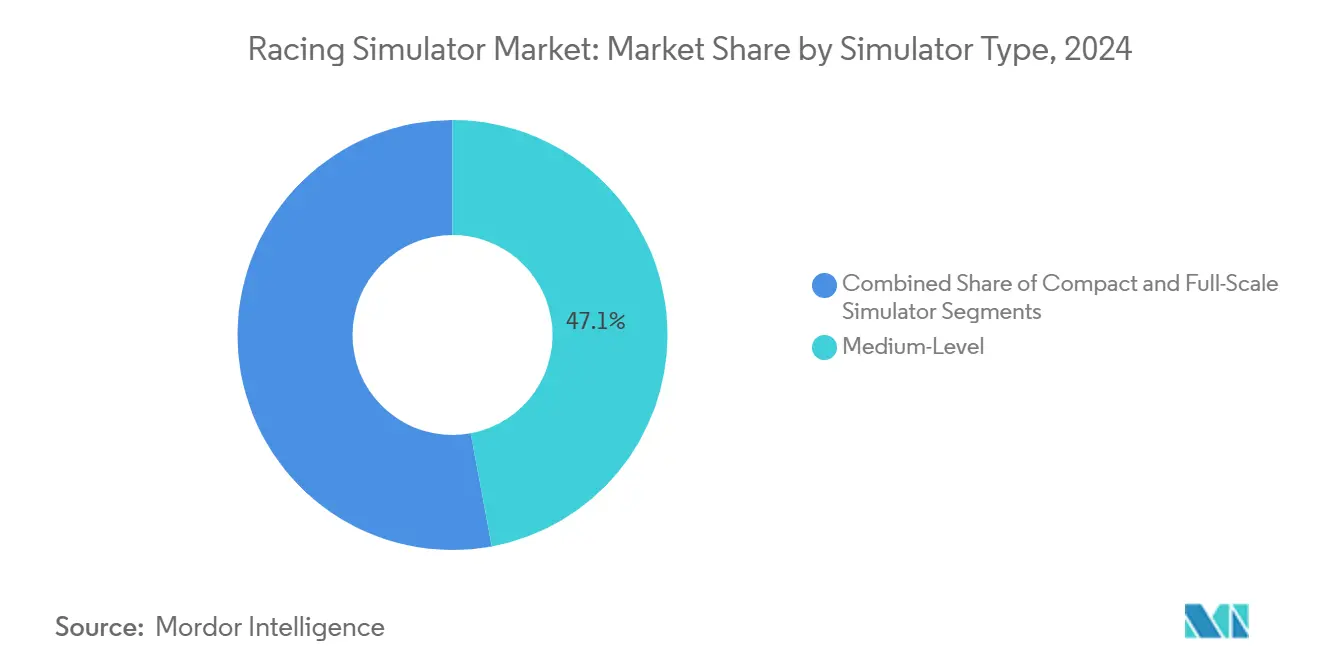

- By simulator type, medium-level systems held 47.08% of the racing simulator market share in 2024, whereas full-scale rigs are forecast to grow at an 18.52% CAGR through 2030.

- By offering, hardware maintained 73.69% of the racing simulator market size in 2024, while software is set to expand at a 17.81% CAGR to 2030.

- By component, steering wheels accounted for a 33.77% share of the racing simulator market size in 2024, yet cockpits will advance at a 21.65% CAGR over the same horizon.

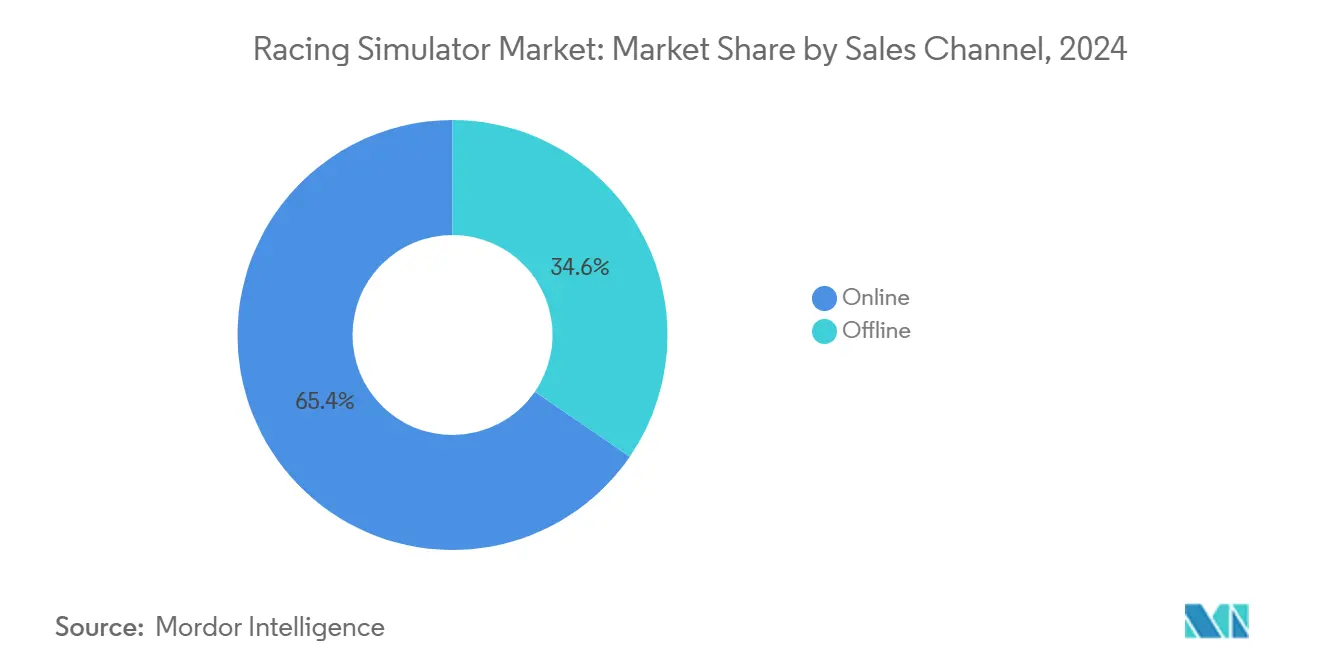

- By sales channel, online platforms commanded 65.41% revenue in 2024, whereas offline outlets are poised for a 16.95% CAGR through 2030.

- By application, home use dominated with 59.36% revenue in 2024, and commercial venues will accelerate at a 19.96% CAGR toward 2030.

- By geography, Europe captured 31.73% market share in 2024, while Asia-Pacific is projected to be the fastest growing at a 16.58% CAGR.

Global Racing Simulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sim-Racing Esports Tournaments | +4.2% | Global, with concentration in Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| VR and Haptic Technologies | +3.8% | North America & Europe leading, Asia-Pacific adoption accelerating | Long term (≥ 4 years) |

| Declining Price Points | +3.5% | Global, particularly benefiting emerging markets in APAC, South America | Short term (≤ 2 years) |

| Experiential Marketing Tie-Ups | +3.1% | Europe, North America core markets, expanding to Asia-Pacific | Medium term (2-4 years) |

| Telemetry-Linked Driver Training Programs | +2.4% | Europe, North America professional motorsport hubs | Long term (≥ 4 years) |

| AI Coaching and Real-Time Analytics | +2.2% | Global, led by North America and Europe technology centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Global Sim-Racing Esports Tournaments

International events legitimize the racing simulator market by mirroring traditional motorsport structures. Hardware suppliers partner with leagues to standardize wheelbases, pedals, and cockpits, creating predictable upgrade cycles. Teams such as Williams Racing field dedicated rosters and training facilities that blur lines between virtual and real pit lanes[1]“Esports World Cup 2024,” Liquipedia, liquipedia.net. Audience reach grows through streaming platforms, driving sponsorship interest and inflows that subsidize tournament operations. This ecosystem turns competitive play into a consumer adoption funnel.

Advances in VR and Haptic Technologies

Premium rigs increasingly bundle haptic actuators that relay tire slip and engine vibrations directly to the driver. D-BOX actuators enable micro-feedback at each wheel to cultivate muscle memory for professional racers[2]“Three Biggest Myths About Haptics in Sim Racing,” D-BOX, d-box.com. When combined with high-resolution VR headsets, the sensory package approximates track realism without multi-monitor costs. Consumer models now inherit scaled-down haptic modules, widening access. Developers overlay adaptive AI that reads telemetry in real time, dynamically adjusting resistance curves inside the wheelbase. The result is a progressively personalized experience that retains users through ongoing software updates.

Declining Price Points for Mid-Level Hardware

Supply-chain efficiencies and motor standardization push direct-drive wheelbase entry prices below USD 500. Bundled cockpit kits retail near USD 2,000, lowering barriers for casual gamers. Asian contract manufacturers raise production volumes, pushing cost curves down and enabling white-label imports. Established brands answer with value-oriented product lines, protecting share while growing the overall racing simulator market. Modular architecture allows incremental upgrades, spreading expenditure over multiple years and encouraging platform loyalty.

Automotive OEM Experiential Marketing Tie-Ups

Vehicle makers integrate simulators into showrooms and brand centers to showcase handling and performance data. Partnerships with simulator studios yield bespoke rigs equipped with official steering wheels and dashboards. These activations generate telemetry that funnels into customer relationship management systems, translating driving skill metrics into engagement scores. As luxury marques co-sponsor esports teams, the racing simulator industry receives cross-promotion at car launches and motorsport weekends. Co-developed hardware sometimes appears in retail catalogs, carrying manufacturer badges that signal quality assurance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Full-Scale Rig Cost | 3.2% | Global, particularly constraining in price-sensitive emerging markets | Short term (≤ 2 years) |

| Supply-Chain Shortages | 2.8% | Global, with acute impact in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Software Ecosystem and Compatibility Gaps | 1.8% | Global, affecting cross-platform integration and user experience | Medium term (2-4 years) |

| Limited Space for Simulator Rigs | 1.5% | Urban centers globally, particularly acute in Asia-Pacific dense housing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Full-Scale Rigs

Professional motion platforms retail between USD 25,000 and USD 50,000, constraining demand outside well-funded teams and entertainment venues. Financing options remain limited, unlike automotive leasing, forcing operators to allocate significant capital. Annual maintenance, covering actuators, bearings, and firmware, adds another USD 1,000-5,000 to ownership costs. This pricing gap leaves a middle-market vacuum that current mid-level products attempt to fill but cannot replicate the full immersion of six-degree motion systems. Consequently, adoption skews toward businesses with multi-seat throughput.

Supply-Chain Shortages of Force-Feedback Motors and Electronics

The global semiconductor crunch lengthens lead times for brushless motors and control boards central to direct-drive wheelbases. Force-feedback manufacturers stockpile components, tying up working capital and pressuring margins. Higher input costs filter down to retail pricing, risking demand elasticity effects. While new fabrication plants in North America promise resilience, capacity expansion projects require multi-year timelines. Brands that diversify supplier bases or redesign products for alternative controllers mitigate exposure but incur engineering costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Simulator Type: Full-Scale Systems Drive Premium Growth

Medium-level setups captured 47.08% revenue in 2024 as they balance cost and performance for hobbyists and small businesses. Full-scale rigs, while niche, are projected to deliver an 18.52% CAGR and will broaden the racing simulator market through professional training demand. Entry-level frames stay relevant for casual gamers seeking affordable immersion without dedicated room space. This layered hierarchy addresses distinct user personas and preserves upgrade ladders that elongate customer lifecycles.

Professional teams such as Mercedes-AMG actively deploy full-motion pods for driver development programs, validating premium segment value propositions. Commercial venues like newly funded racing arcades prioritize full-scale hardware to maximize throughput and spectacle. Manufacturing advances in aluminum extrusion have lowered chassis costs, encouraging suppliers to bundle motion actuators into previously static models. As the racing simulator market integrates more AI-based telemetry, premium rigs will further differentiate through data accuracy, attracting both esports franchises and engineering departments.

By Offering: Software Innovation Accelerates Beyond Hardware

In 2024, hardware accounted for 73.69% revenue, reflecting the physical essentials of wheelbases, pedals, and cockpits. Software subscriptions are on pace for a 17.81% CAGR, signaling a pivot where recurring digital services outgrow one-time equipment sales. Track-analysis platforms generate fresh datasets each lap, turning every session into an opportunity for upsell. This recurring income aligns incentives for continual feature releases that enrich the racing simulator market.

Developers embed cloud telemetry, AI coaching, and dynamic weather engines, extending lifespan for existing rigs. Hardware makers now release companion dashboards that integrate firmware updates, storefronts, and social leaderboards, blurring lines between physical and digital. As user bases mature, software communities drive mod ecosystems, raising switching costs and cementing brand loyalty. The racing simulator industry thus transitions toward experience-centric economics, propelled by cross-platform content libraries.

By Component: Cockpits Emerge as Fastest-Growing Category

Steering wheels held 33.77% of revenue in 2024 owing to their indispensable role as control interfaces. Cockpits will achieve a 21.65% CAGR through 2030, becoming the growth engine within the racing simulator market. Integrated chassis packages unify seat ergonomics, monitor mounts, and cable management, simplifying setup for novices. Modular rail systems allow professional upgrades such as motion actuators and tactile transducers without replacing the entire frame.

New cockpit designs fold or disassemble quickly, addressing urban space limitations. Manufacturers secure licensing from governing bodies, ensuring geometry that mimics real racing seating positions. Aluminum profile and carbon-fiber composites reduce flex and support heavier direct-drive loads, enhancing feedback fidelity. These innovations turn cockpits from passive frames into active components that shape driving realism, elevating perceived value and justifying premium pricing tiers.

By Sales Channel: Online Dominance Reflects Technical Complexity

Digital storefronts generated 65.41% revenue in 2024, as enthusiasts rely on product configurators, community reviews, and firmware resources hosted online. Offline retail will still rise at a 16.95% CAGR, encouraged by experiential showrooms where customers evaluate force-feedback strength and pedal modulation firsthand. Cross-channel strategies include click-and-collect services and local service centers offering assembly support.

Manufacturers leverage direct-to-consumer models to capture margin and collect usage telemetry, feeding iterative design cycles. Brick-and-mortar chains counter by bundling in-person tech consultations and financing packages for high-ticket full-scale rigs. Hybrid strategies emerge where physical venues double as marketing outposts and esports arenas, converting foot traffic into sales funnel entries. The racing simulator market thus maintains online primacy while nurturing tactile sales environments to expand addressable demographics.

By Application: Commercial Segment Accelerates Through Entertainment Venues

Home use sustained 59.36% share in 2024, backed by falling component prices and expanding game libraries. Commercial operators, including themed bars and corporate experience centers, will lift application revenue at a 19.96% CAGR, widening the racing simulator market beyond residential settings. High-throughput venues demand robust rigs capable of continuous multi-hour sessions, steering design priorities toward durability and quick-swap components.

Arcade chains secure venture funding to roll out multi-seat arenas with leaderboard integrations and live broadcasting, creating social spectacles that amplify brand exposure. Corporate events adopt simulators for team-building and customer engagement, booking portable rigs with branded liveries. Training academies for aspiring racers allocate simulator hours as mandatory curriculum elements, elevating commercial demand for realistic physics engines and FIA-approved cockpits. This institutional uptake diversifies revenue streams, buffering the industry against consumer spending cycles.

Geography Analysis

Europe controlled 31.73% revenue in 2024, anchored by dense motorsport calendars and a regulatory framework that certifies esports competitions. Racing hubs such as Germany, the United Kingdom, and France house both automotive giants and championship circuits, fostering a culture that values simulation accuracy. Local manufacturers produce premium direct-drive wheelbases, keeping technological leadership inside the region. European governing bodies continuously refine technical regulations, pushing simulator makers to innovate and maintain compliance. These factors collectively sustain a stable user base and encourage professional training adoption.

Asia-Pacific will post the highest regional CAGR at 16.58% through 2030, driven by government investment in digital entertainment and robust consumer electronics supply chains. Mainland China offers price-competitive components, enabling budget tiers that attract first-time buyers. Meanwhile, Japan and South Korea contribute software and network infrastructure that underpin large-scale esports tournaments. Urban density challenges physical installation, spurring compact, foldable cockpit designs tailored to apartments. Regional operators expand simulator cafés, converting leisure tastes into recurring revenue and steadily enlarging the racing simulator market.

North America follows with an 11.48% CAGR, supported by high discretionary spending and mainstream console gaming culture. Major streaming services amplify tournament reach, offering advertisers premium inventory during live events. Local semiconductor fabrication projects promise medium-term relief for electronic component shortages, providing supply-chain resilience for hardware assemblers. Motorsport institutions such as NASCAR integrate virtual racing into fan engagement, reinforcing simulator legitimacy. Although smaller in absolute unit shipments than Asia-Pacific, the region commands some of the highest average selling prices, underpinning profit margins.

Competitive Landscape

The racing simulator market features moderate fragmentation, with top brands holding meaningful yet non-dominant shares. This creates opportunities for specialized competitors to capture niche segments through technological differentiation. Midsize challengers like MOZA Racing leverage direct-drive innovations to secure footholds in premium segments. Hardware specialists increasingly offer full ecosystem ranges, wheelbases, pedals, cockpits, and software dashboards, to solidify switching costs and harvest data insights.

Strategic partnerships drive differentiation. Next Level Racing’s licensing agreement with the Fédération Internationale de l’Automobile authenticates its cockpits for official competition use. D-BOX collaborates with esports leagues to embed haptic profiles that replicate specific race cars, showcasing the cross-pollination of hardware and content. Larger consumer-electronics firms deploy global logistics and marketing clout, while boutique players court enthusiast communities with rapid firmware iterations and open-source mod support.

Consolidation remains a future possibility, demonstrated by recent acquisitions where peripheral conglomerates absorb niche simulator brands. Financial investors eye subscription analytics platforms that offer predictable cash flows compared with hardware cycles. Sustainability themes enter competitive dialogue as manufacturers announce recyclable aluminum frames and energy-efficient motor drivers. Overall, firms that harmonize reliable mechanics, immersive software, and community ecosystems stand to outperform peers in the evolving racing simulator market.

Racing Simulator Industry Leaders

Fanatec (Endor AG)

Logitech G

Thrustmaster (Guillemot)

MOZA Racing

SimXperience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Harness Racing NSW launched a mobile driving simulator that lets participants experience standardbred racing.

- September 2025: Caterham partnered with FPZERO Simulators to release the Clubsport Simulator featuring bespoke components.

- June 2025: Racing Unleashed and McLaren Racing unveiled a carbon-fiber motion simulator built on a three-degree-of-freedom platform.

- April 2025: GIANTS Software opened pre-orders for Project Motor Racing, a new title using the Hadron 720 Hz physics engine with full mod support.

Global Racing Simulator Market Report Scope

| Compact / Entry-Level Simulator |

| Medium-Level Simulator |

| Full-Scale Simulator |

| Hardware |

| Software |

| Steering Wheel |

| Pedal Sets |

| Gearbox Shifters |

| Seats |

| Monitor Stand |

| Cockpits |

| Others |

| Online |

| Offline |

| Home / Personal Use |

| Commercial (Arcades, Training Centers) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Simulator Type | Compact / Entry-Level Simulator | |

| Medium-Level Simulator | ||

| Full-Scale Simulator | ||

| By Offering | Hardware | |

| Software | ||

| By Component | Steering Wheel | |

| Pedal Sets | ||

| Gearbox Shifters | ||

| Seats | ||

| Monitor Stand | ||

| Cockpits | ||

| Others | ||

| By Sales Channel | Online | |

| Offline | ||

| By Application | Home / Personal Use | |

| Commercial (Arcades, Training Centers) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for the racing simulator market in 2030?

The racing simulator market size is projected to reach USD 2.04 billion by 2030.

Which simulator type is growing fastest toward 2030?

Full-scale rigs lead growth with an expected 18.52% CAGR owing to commercial venue and professional team demand.

Why are software subscriptions gaining traction within racing simulation?

AI coaching, real-time telemetry, and continuous content updates create recurring value that outpaces one-time hardware sales.

Which region will expand the market most rapidly?

Asia-Pacific is slated to record a 16.58% CAGR thanks to esports infrastructure investment and cost-effective hardware sourcing.

How do haptic technologies enhance training effectiveness?

Actuators transmit nuanced vibrations such as tire grip changes, enabling drivers to react sooner and develop muscle memory for real-world racing.

Are online channels expected to remain dominant for simulator purchases?

Yes, online platforms will keep the largest share because they provide detailed configuration tools and global reach, though experiential retail will grow quickly.

Page last updated on: