Coding And Marking Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

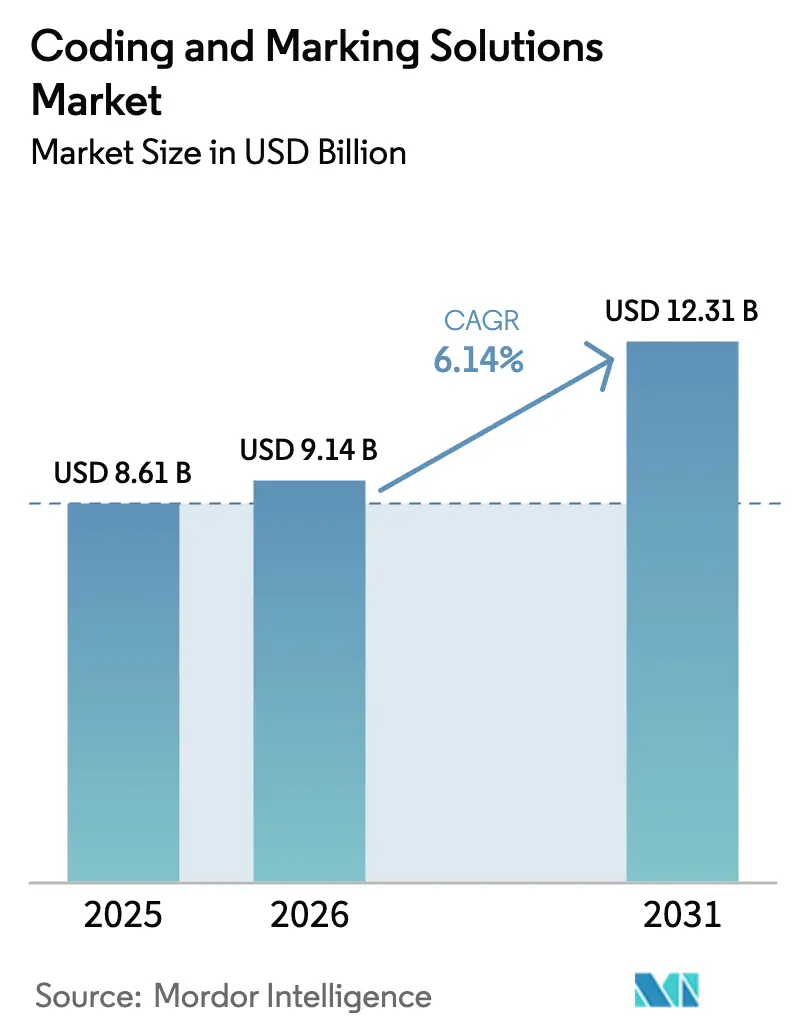

| Market Size (2026) | USD 9.14 Billion |

| Market Size (2031) | USD 12.31 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coding And Marking Solutions Market Analysis by Mordor Intelligence

The coding and marking solutions market size is expected to increase from USD 8.61 billion in 2025 to USD 9.14 billion in 2026 and reach USD 12.31 billion by 2031, growing at a CAGR of 6.14% over 2026-2031. Smart-factory investments, track-and-trace mandates, and the steady pivot from capital sales to service contracts are widening the addressable base for equipment, consumables, and cloud monitoring. End-to-end serialization across food and pharmaceuticals is tightening technical specifications for print quality, code readability, and data connectivity, boosting demand for laser coders and connected continuous inkjet systems. Vendors are responding with pay-per-mark pricing and predictive-maintenance subscriptions that monetize uptime while lowering up-front costs for small and mid-size manufacturers. Regional VOC limits, especially in Europe, are accelerating a transition from solvent-based inks to fiber-laser technology that eliminates consumables and ensures regulatory compliance. Competitive differentiation hinges on embedded vision verification, standards-based data exchange, and the ability to bundle service, software, and consumables into multi-year lifecycle contracts that shield customers from unplanned downtime.

Key Report Takeaways

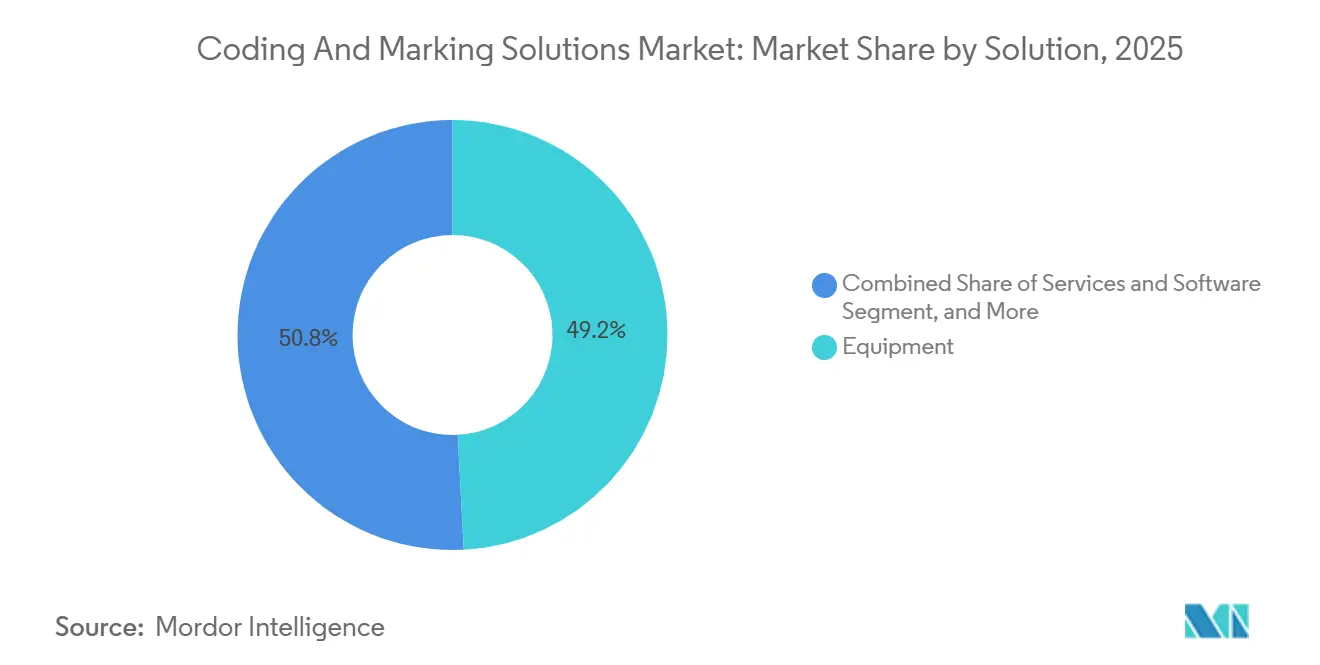

- By solution, equipment led with 49.16% revenue share in 2025, while services and software are advancing at a 6.92% CAGR through 2031.

- By equipment technology, continuous inkjet held 36.87% of the coding and marking solutions market share in 2025, whereas laser coders are projected to grow at a 7.11% CAGR between 2026 and 2031.

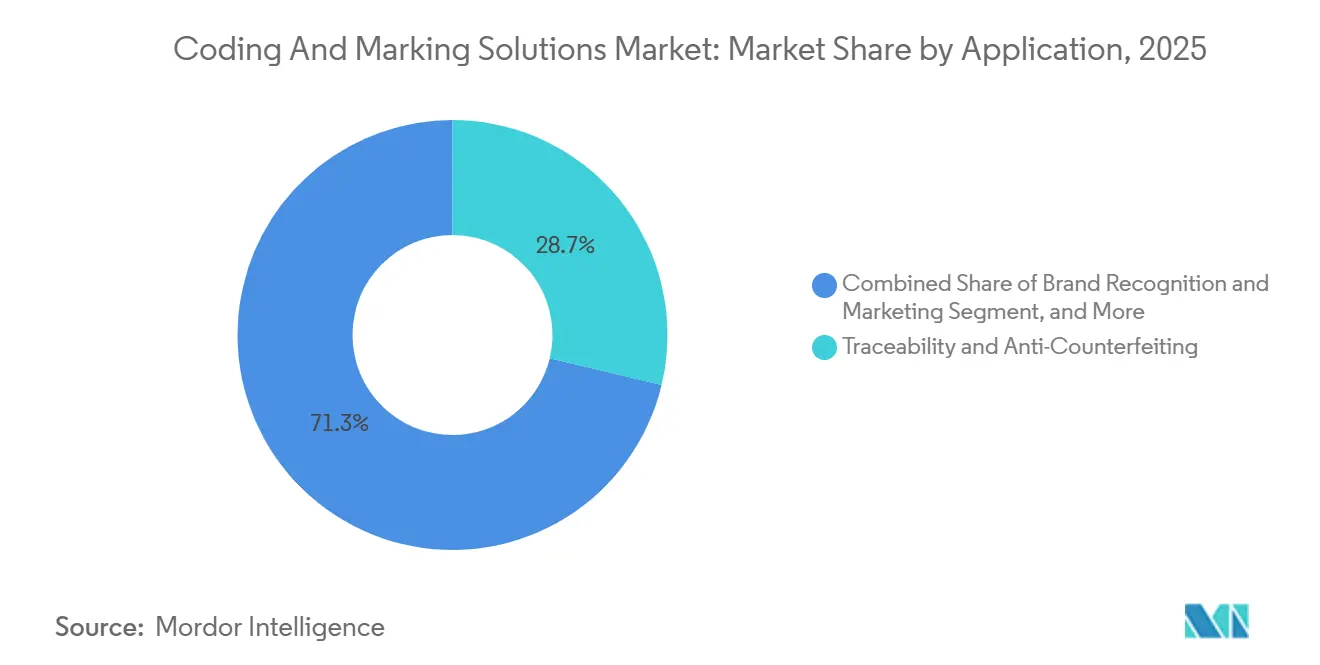

- By application, traceability and anti-counterfeiting accounted for 28.73% of the coding and marking solutions market in 2025, and brand recognition and marketing is forecast to expand at a 6.96% CAGR through 2031.

- By end-user industry, food and beverages accounted for 38.91% of revenue share in 2025, while the pharmaceutical sector is set to record the highest projected CAGR of 7.16% over 2026-2031.

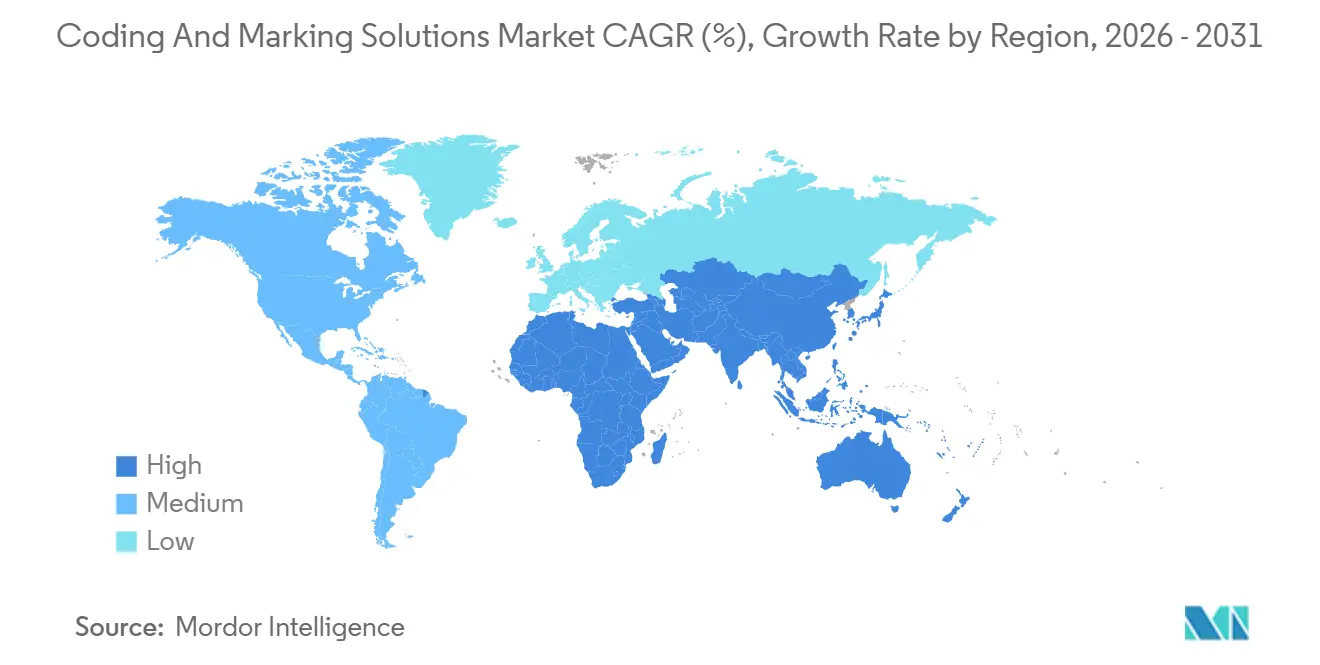

- By geography, Asia-Pacific captured 37.39% of global revenue in 2025, and the Middle East is expected to post the fastest growth at a 7.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coding And Marking Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Production and Packaging Industries | +1.8% | Global, with concentration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Demand for End-to-End Traceability | +1.5% | North America and Europe core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Mandates for Batch Coding | +1.3% | North America, Europe, emerging in Middle East and South America | Short term (≤ 2 years) |

| Industry 4.0-Enabled Predictive Maintenance | +0.9% | Europe and North America early adopters, Asia-Pacific following | Medium term (2-4 years) |

| Shift to Solvent-Free Fiber-Laser Coding | +0.7% | Europe leading due to VOC regulations, global diffusion | Long term (≥ 4 years) |

| AI-Assisted Inline Vision Verification | +0.6% | North America and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Production and Packaging Industries

Manufacturing growth in Asia-Pacific and the Middle East is lifting baseline demand for inline coders across food, beverage, and pharmaceutical lines. China’s industrial production index rose 5.6% year-on-year in December 2025, while India’s manufacturing sector expanded 6.2%, both outpacing global averages.[1]National Bureau of Statistics of China, “Industrial Production Statistics,” stats.gov.cn North American packaging machinery shipments reached USD 9.8 billion in 2025, a 4.3% increase that signals sustained investment in additional capacity. Vietnam’s emergence as an electronics contract-manufacturing hub requires component-identification printing that supports just-in-time workflows. Saudi Arabia’s Public Investment Fund allocated USD 20 billion in 2025 to build food-processing clusters that will each install serialization-ready coding lines.

Demand for End-to-End Traceability

Food-safety and pharmaceutical laws now obligate manufacturers to link every unit to a digital record, forcing coders to interface with enterprise resource planning and blockchain platforms. The FDA Food Traceability Rule, effective January 2026, mandates lot-level coding for leafy greens, finfish, and other high-risk foods.[2]U.S. Food and Drug Administration, “Drug Supply Chain Security Act,” fda.gov Europe’s Farm-to-Fork strategy, which targets 25% organic production by 2030, drives demand for coders that print origin data and sustainability seals directly on packs. GS1 Digital Link adoption by a dozen global food brands in 2025 shows how serialized QR codes blend compliance with consumer engagement. Pharmaceutical serialization under the Drug Supply Chain Security Act remains active, with ongoing aggregation challenges sustaining demand for high-speed vision verification.

Regulatory Mandates for Batch Coding

Governments worldwide keep tightening batch-coding rules to accelerate recalls and curb counterfeiting. Full enforcement of the EU Falsified Medicines Directive requires that every prescription package carry a verifiable, unique identifier. Brazil’s regulator extended serialization requirements to over-the-counter drugs in 2024, creating a backlog of line upgrades that will stretch into 2027. ISO 22742:2024 now specifies contrast, modulation, and decode rates, pushing factories to add inline vision systems that certify code quality before shipment. Cosmetics producers in the European Union face mounting pressure to adopt similar coding that supports safety assessments, although enforcement remains uneven.

Industry 4.0-Enabled Predictive Maintenance

Connected coders stream performance data to cloud platforms, allowing maintenance teams to address nozzle wear or laser drift before print defects appear. Deloitte’s 2025 Smart Factory Survey found 68% of North American and European plants have already deployed IoT sensors on packaging lines, achieving a median 15% gain in overall equipment effectiveness. Domino introduced closed-loop automation in April 2025 that automatically adjusts print speed and ink viscosity in response to substrate changes, cutting material waste. Videojet’s remote-diagnostics platform alerts operators to emerging faults and has documented 12% savings in consumables on high-speed beverage lines. The 6.92% CAGR for services and software reflects how subscription models monetize these predictive insights.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Running Costs | -0.8% | Global, acute in South America and Africa | Short term (≤ 2 years) |

| Growth of Pre-Printed Packaging Alternatives | -0.5% | North America and Europe, limited in Asia-Pacific | Medium term (2-4 years) |

| Regional Bans on MEK-Based Inks | -0.3% | Europe core, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Geopolitical Constraints on High-Power Diode Lasers | -0.2% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Running Costs

Entry-level continuous-inkjet systems start at around USD 15,000, while fiber-laser coders exceed USD 50,000 and require annual consumables outlays of up to 30% of the initial price. Such costs deter small food processors in South America and Africa, who often default to manual date stamping that lacks serialization capability. Pharmaceutical contract packagers pass the burden of USD 100,000 vision-verification systems to brand owners, inflating per-unit fees. Equipment-as-a-service models ease the capex hurdle but remain concentrated in mature credit markets across North America and Europe.

Growth of Pre-Printed Packaging Alternatives

Digital and flexographic presses now imprint variable data during primary graphics runs, reducing the need for secondary inline coders on filling lines. HP and Koenig and Bauer machines can print serialized codes at speeds close to 200 meters per minute, directly challenging thermal transfer overprinting on labels. Brand owners in North America and Europe embrace pre-printing for short-run SKUs because unified artwork and code management cut changeover time.[3]HP Inc., “Digital Printing Solutions,” hp.com The model is less prevalent in Asia-Pacific, where long batch lengths and lower labor costs keep inline coding attractive. Regulatory agencies still require point-of-fill printing for most pharmaceutical products, limiting the spread of pre-printed solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Services Monetize Uptime Over Hardware

Services and software are expanding at 6.92% annually through 2031, steadily eroding the 49.16% equipment benchmark recorded in 2025. The coding and marking solutions market for services is projected to expand faster than the hardware market because predictive analytics, remote diagnostics, and pay-per-mark billing align with customer demand for outcome-based contracts. Vendors bundle consumables, spare parts, and guaranteed uptime in multiyear agreements that shift capex to opex, appealing to finance departments aiming to preserve cash. Cloud portals consolidate code-quality metrics from global plants, providing quality managers with a real-time audit trail that meets pharmaceutical inspection requirements. Consumables remain a resilient annuity stream, but margin pressure from third-party ink suppliers is prompting OEMs to defend their proprietary fluids through formulation patents. Equipment sales still dominate absolute revenue because greenfield factories in the Middle East and Asia-Pacific specify dozens of coders per line, yet volume-driven hardware profits are thinning as customers expect lower prices in return for long-term service commitments.

Capital replacement in North America and Europe is now primarily technology-driven, with factories upgrading from solvent-heavy inkjet to solvent-free laser solutions when legacy assets reach the end of life. These mature regions, therefore, provide fertile ground for service innovations such as uptime-guarantee SLAs pegged to production volume. Pharmaceutical contract packagers value service wraparounds that include validation documentation, since regulatory authorities require proof that every print head maintains code legibility throughout the batch. Across all geographies, the coding and marking solutions market consistently rewards suppliers that deliver rapid response times, embedded analytics, and transparent total cost of ownership.

By Equipment Technology: Laser Coders Capture Environmental Mandates

Laser coders are forecast to lead growth at 7.11% through 2031 as European VOC regulations push manufacturers toward solvent-free alternatives. The coding and marking solutions market share for continuous inkjet remains significant at 36.87% in 2025, but fiber-laser devices now penetrate beverage, dairy, and life-science segments that previously defaulted to ink. Upgraded fiber sources enable crisp, high-contrast marks on both flexible and rigid plastics without consumables, making lifetime costs attractive despite higher acquisition prices. Thermal inkjet continues to gain traction in blister and sachet formats where interchangeable cartridges reduce downtime. Drop-on-demand systems play a supporting role in large-character case coding, while thermal transfer overprinting holds niche leadership on flexible film applications that require high-resolution graphics and barcodes.

Vendors racing to differentiate their lasers emphasize integrated vision verification, enhanced beam steering, and modular cooling to ensure installations fit tight OEM machinery footprints. European Printing Ink Association exclusions and corporate sustainability dashboards collectively accelerate the shift, but continuous inkjet retains dominance on ultra-high-speed lines above 1,000 containers per minute, especially in carbonated beverage plants. The coding and marking solutions market will therefore remain a multimodal technology landscape, with few one-size-fits-all printers.

By Application: Brand Engagement Drives QR-Code Adoption

Compliance and regulatory coding remain the baseline across every industry, but brand recognition and marketing are advancing at a 6.96% CAGR as manufacturers harness QR codes for consumer engagement. The coding and marking solutions market for traceability and anti-counterfeiting accounted for a 28.73% share in 2025, driven by serialized pharmaceuticals and fresh food. Now, GS1 Digital Link enables a single QR symbol to carry product data for supply-chain partners while redirecting shoppers to campaign microsites. Consumer goods giants piloting interactive codes report higher scan rates when variable text ties into loyalty programs and sustainability disclosures. Electronics and automotive firms integrate part IDs with digital-twin software so maintenance crews can retrieve component histories via handheld readers, thereby shrinking repair times. Cosmetics brands, meanwhile, experiment with blockchain registries to authenticate products at the point of sale, a use case that relies on secure, tamper-evident batch codes.

As information density in symbols increases, there's a growing preference for laser and high-resolution thermal inkjet printers over older valve-jet units due to their ability to handle complex coding requirements. Ensuring readability, particularly on glossy or uneven substrates, underscores the critical role of vision-system integration in modern printing solutions. These heightened technical demands not only enhance operational efficiency but also justify the premium pricing for printers adept at upholding code integrity on a large scale, meeting the evolving needs of industries reliant on precise and reliable coding.

By End-User Industry: Pharmaceutical Serialization Sustains Premium Pricing

The pharmaceutical sector is projected to expand at a 7.16% CAGR, while maintaining premium pricing, as validation, audit trails, and tamper-evident specifications raise performance thresholds. Contract manufacturers in India and China have upgraded multiple packaging lines to maintain export eligibility in regulated markets, thereby boosting recurring revenue from service and software subscriptions tied to remote compliance reporting. Food and beverages accounted for 38.91% of revenue in 2025 and remain volume-heavy, yet their fragmented structure slows technology migration relative to pharma. Dairy and beverage plants rely on high-speed continuous inkjet, while bakeries favor thermal inkjet, which can handle dusty environments without clogging.

Cosmetics and personal care vendors accelerate code adoption to address rising consumer scrutiny over ingredient transparency. Construction and industrial materials remain underpenetrated, creating whitespace where regulatory lag and manual marking methods intersect. Vendors that package hardware with ruggedized heads and dust-resistant seals could unlock new volume in cement, plywood, and steel rebars once traceability norms tighten.

Geography Analysis

Asia-Pacific dominated the coding and marking solutions market with 37.39% of global revenue in 2025 and will maintain leadership through 2031, as China, India, and Vietnam continue to outpace global manufacturing growth. High-speed food and beverage filling lines across the region require continuous operation, prompting strong adoption of connected continuous inkjet systems supported by local service networks. Japan and South Korea maintain high penetration of laser coders in automotive, electronics, and medical devices, where permanent, abrasion-resistant marks are mandatory for warranty tracking. Southeast Asia offers growth upside as multinationals diversify supply chains, installing component-identification printers that integrate with digital-twin factories.

The Middle East leads regional growth at a projected 7.19% CAGR through 2031. Saudi Vision 2030 investments in food processing and the United Arab Emirates' push into pharmaceuticals are embedding serialization capability in every new line, effectively “baking in” demand for laser and thermal inkjet units. Greenfield megaprojects specify redundancy and remote monitoring from the outset, favoring vendors with robust service footprints. Africa remains nascent, yet multinational food and beverage groups deploy compliant coding to align regional plants with global quality policies, creating a beachhead for future expansion once local regulations catch up.

North America and Europe present mature but lucrative upgrade cycles. The European Printing Ink Association's ban on MEK spurs reinvestment in fiber-laser technology, and corporate ESG goals reinforce solvent-free conversion. In North America, line-aggregation challenges under the Drug Supply Chain Security Act sustain demand for vision-verified printers even after serialization deadlines passed. South America’s outlook depends on regulatory follow-through, especially in Brazil, where over-the-counter drug serialization is phasing in and could trigger extended hardware orders if enforcement proves rigorous.

Competitive Landscape

The coding and marking solutions market remains moderately concentrated, with Videojet Technologies, Domino Printing Sciences, and Markem-Imaje together accounting for about 36% of global revenue through bundled hardware, fluids, and service contracts. Hitachi Industrial Equipment and Linx Printing Technologies form the next tier, capturing roughly 24% by focusing on high-speed beverage, electronics, and pharmaceutical lines that reward rapid service response. The remaining 40% is fragmented among regional producers and cloud-native start-ups that promote pay-per-mark pricing to convert capex into opex for small and mid-size manufacturers.

Service-led innovation dominated 2025 strategies. Domino expanded equipment-as-a-service packages in India, bundling printers, consumables, and predictive maintenance under volume-based fees that shift financial risk from packagers to the vendor. Videojet filed patents for MEK-free continuous-inkjet inks compliant with European volatile organic compound rules, safeguarding consumables margins as solvent restrictions tighten. Keyence released fiber-laser models optimized for automotive and electronics substrates, using higher beam quality to mark metals and ceramics without post-treatment.

Technology differentiation now centers on integrated vision verification, cloud analytics, and open data protocols that enable printers to feed quality metrics into manufacturing execution systems. ISO 22742:2024, which mandates inline code-quality checks on pharmaceutical packs, raises entry barriers that favor vendors with validated vision subsystems. Danaher, the parent of Videojet, cross-sells motion-control and inspection hardware alongside coders, offering turnkey packaging lines that smaller rivals struggle to match. Whitespace opportunities persist in construction materials and cosmetics anti-counterfeiting, segments where regulatory standards are still being defined, and incumbents have yet to lock in market share.

Coding And Marking Solutions Industry Leaders

Videojet Technologies Inc.

Domino Printing Sciences plc

Markem-Imaje Corporation

Hitachi, Ltd.

REA Elektronik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA Food Safety Modernization Act Food Traceability Rule took effect, requiring lot-level coding for high-risk foods and accelerating coder integration with cloud traceability platforms.

- December 2025: Domino Printing Sciences appointed a new managing director for India and expanded its equipment-as-a-service model, shifting capital risk from packagers to the vendor.

- June 2025: Domino launched the K300 piezo inkjet printer and extended its Dx-Series fiber-laser portfolio for life-science serialization lines that demand vision-verified code quality.

- April 2025: Domino introduced closed-loop automation solutions that adjust print speed and ink viscosity based on substrate variation, reducing waste and boosting equipment effectiveness.

Global Coding And Marking Solutions Market Report Scope

The Coding And Marking Solutions Market Report is Segmented by Solution (Equipment, Fluids and Ribbons, Spares, Services and Software), Equipment Technology (Continuous Inkjet, Thermal Inkjet, Laser Coders, Drop-on-Demand and Valve Jet, Thermal Transfer Overprinting), Application (Component Identification, Brand Recognition and Marketing, Traceability and Anti-Counterfeiting, Compliance and Regulatory Coding), End-User Industry (Food and Beverages, Pharmaceutical, Cosmetics and Personal Care, Construction and Industrial, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Equipment |

| Fluids and Ribbons |

| Spares |

| Services and Software |

| Continuous Inkjet |

| Thermal Inkjet |

| Laser Coders |

| Drop-on-Demand and Valve Jet |

| Thermal Transfer Overprinting |

| Component Identification |

| Brand Recognition and Marketing |

| Traceability and Anti-Counterfeiting |

| Compliance and Regulatory Coding |

| Food and Beverages |

| Pharmaceutical |

| Cosmetics and Personal Care |

| Construction and Industrial |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution | Equipment | ||

| Fluids and Ribbons | |||

| Spares | |||

| Services and Software | |||

| By Equipment Technology | Continuous Inkjet | ||

| Thermal Inkjet | |||

| Laser Coders | |||

| Drop-on-Demand and Valve Jet | |||

| Thermal Transfer Overprinting | |||

| By Application | Component Identification | ||

| Brand Recognition and Marketing | |||

| Traceability and Anti-Counterfeiting | |||

| Compliance and Regulatory Coding | |||

| By End-User Industry | Food and Beverages | ||

| Pharmaceutical | |||

| Cosmetics and Personal Care | |||

| Construction and Industrial | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the coding and marking solutions market be by 2031?

It is projected to reach USD 12.31 billion by 2031, increasing from USD 9.14 billion in 2026.

Which equipment technology is growing the fastest?

Laser coders lead with a forecast 7.11% CAGR between 2026 and 2031, helped by solvent-free operations and regulatory drivers.

Why are services gaining share over hardware sales?

Manufacturers prefer outcome-based contracts that bundle printers, consumables, predictive maintenance, and uptime guarantees into monthly fees, shifting capex to opex.

Which industry will add the most revenue through 2031?

Pharmaceuticals are expected to register the strongest growth at a 7.16% CAGR as serialization compliance deepens worldwide.

What region shows the highest growth potential?

The Middle East is forecast to expand at 7.19% CAGR, supported by Vision 2030 industrialization and new pharmaceutical investments.

How are sustainability rules shaping technology choice?

European VOC limits and corporate ESG goals favor fiber-laser printers that eliminate solvent inks and reduce life-cycle emissions.

Page last updated on: