Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

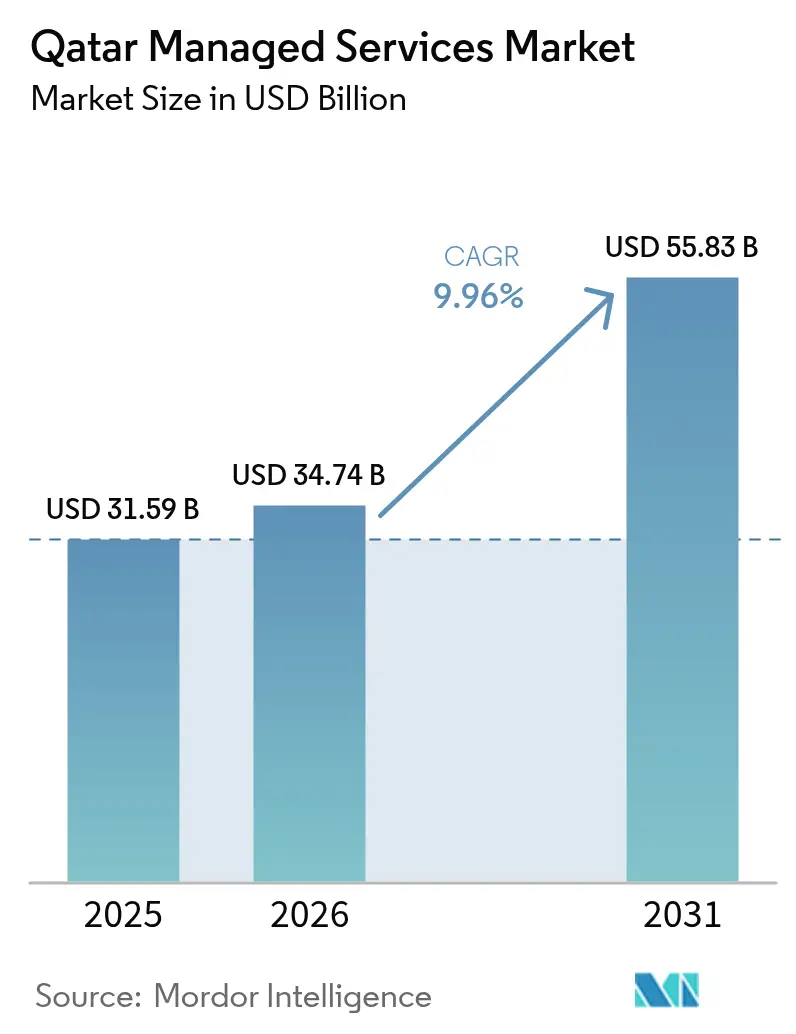

| Base Year Market Size (2025) | USD 31.59 Billion |

| Market Size (2026) | USD 34.74 Billion |

| Market Size (2031) | USD 55.83 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Managed Services Market Analysis by Mordor Intelligence

The Qatar managed services market size was valued at USD 31.59 billion in 2025 and estimated to grow from USD 34.74 billion in 2026 to reach USD 55.83 billion by 2031, at a CAGR of 9.96% during the forecast period (2026-2031).

The growth trajectory is powered by state-led digitization programs, rising cloud adoption, and heightened cybersecurity spending that together turn the nation into a regional digital hub[1]International Trade Administration, “Qatar Artificial Intelligence,” trade.gov. Substantial allocations under the National Digital Agenda 2030, including USD 2.5 billion for AI deployment, spur demand for managed cloud, security, and infrastructure services. The Qatar managed services market benefits further from the energy sector’s reinvestment of LNG revenues into large-scale IT modernization, while a new Personal Data Protection Law accelerates outsourcing for compliant data-hosting solutions. Intensifying cyber-threats, 23 million attempted attacks were logged in 2022, anchor spending on managed security, and international hyperscalers deepen competition by launching in-country data centers.

Key Report Takeaways

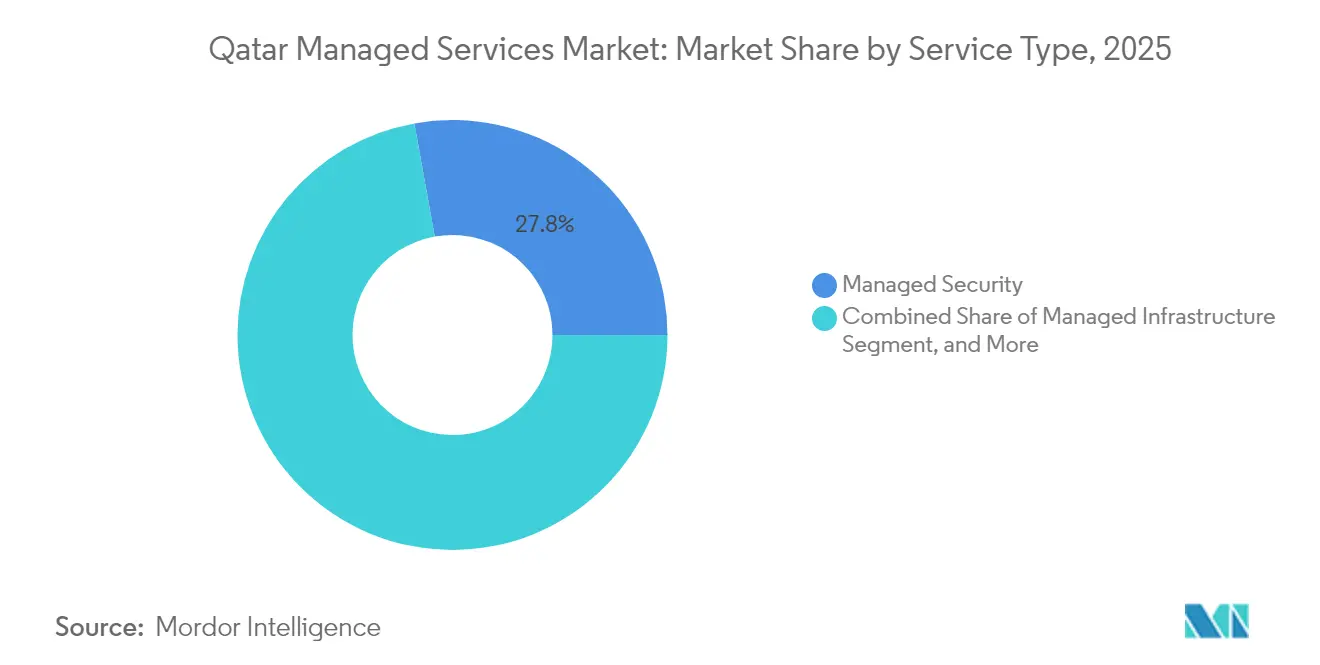

- By service type, managed security led with 27.84% of the Qatar managed services market share in 2025; managed cloud services are projected to expand at a 11.72% CAGR to 2031.

- By deployment model, public cloud accounted for 42.78% of the Qatar managed services market size in 2025, while hybrid cloud records the fastest 16.05% CAGR through 2031.

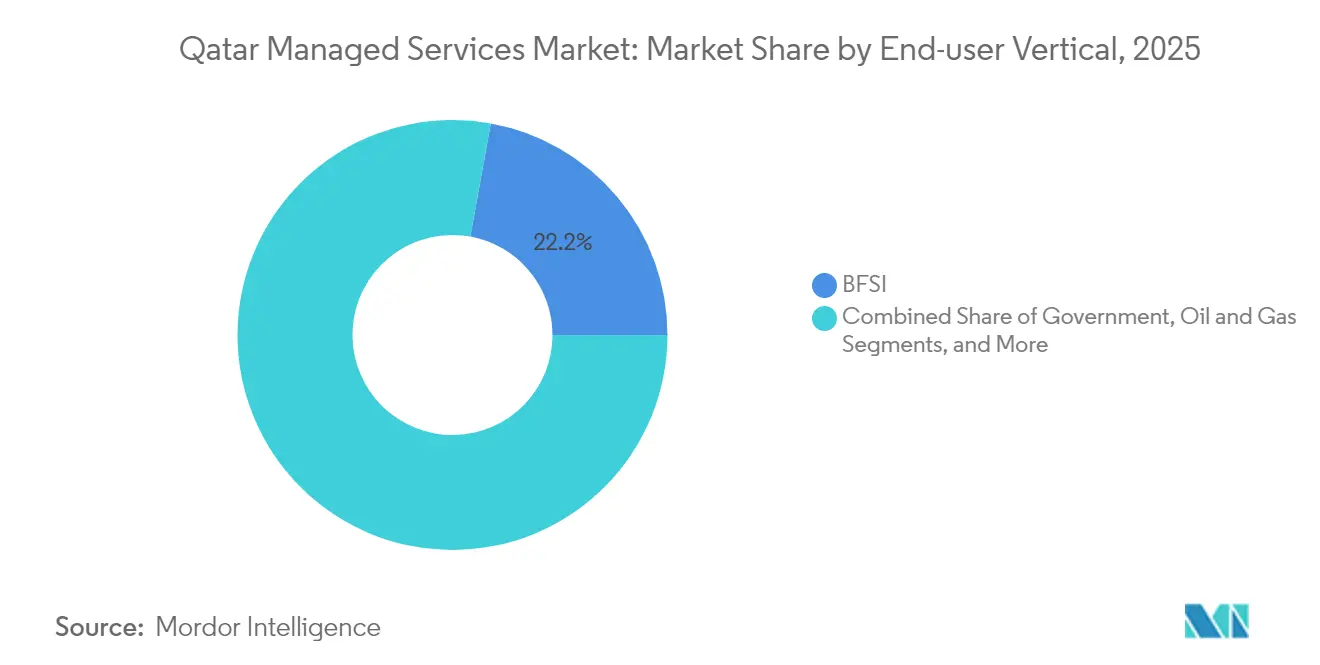

- By end-user vertical, BFSI secured 22.15% revenue share in 2025; healthcare is advancing at a 12.86% CAGR through 2031.

- By enterprise size, large enterprises held 50.62% share of the Qatar managed services market size in 2025, yet SMEs post the strongest 14.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for outsourcing of non-core IT operations | +2.1% | National, concentrated in Doha and industrial cities | Medium term (2-4 years) |

| Government-led digital-transformation programmes (NDS3, NDA2030) | +3.2% | National, with spillover to GCC region | Long term (≥ 4 years) |

| Escalating cyber-threat landscape across critical sectors | +1.8% | National, with focus on energy and financial sectors | Short term (≤ 2 years) |

| New Personal Data Protection Law driving data-residency outsourcing | +1.4% | National, affecting multinational enterprises | Medium term (2-4 years) |

| National tech mega-events (Web Summit, World Summit AI) boosting MSP uptake | +0.9% | National, with regional demonstration effects | Short term (≤ 2 years) |

| AI-skills deficit encouraging AIOps-as-a-Service adoption | +1.7% | National, particularly in government and large enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Outsourcing of Non-Core IT Operations

Enterprises increasingly redirect capital toward core revenue streams by engaging managed service providers for complex IT tasks. QatarEnergy’s 2023 revenue of USD 43.8 billion enabled large investments in digital twins and operational automation that require specialist partners, illustrating how scale and complexity justify external support[2]QatarEnergy, “Annual Review 2023,” qatarenergy.qa Source: Data Center Knowledge, “Qatar Takes Steps to a More Sustainable Future,” datacenterknowledge.com . CEO surveys show 84% of business leaders plan to boost technology spending, a sentiment reinforced by the Third National Development Strategy’s efficiency mandate. High-value contracts in energy and banking cascade into mid-market adoption, accelerating the Qatar managed services market. Provider engagements typically bundle infrastructure monitoring, security hardening, and application management, creating long-term recurring revenue streams.

Government-led digital-transformation programs (NDS3 and NDA 2030)

The Ministry of Communications and Information Technology partners with Scale AI to embed over 50 AI applications across public services, underpinning USD 2.5 billion in tech funding. E-government expansion to 1,400 services forces ministries to seek external expertise for cloud migration, managed security, and continuous operations. Public-sector proof-of-concepts set adoption benchmarks that private firms replicate, lifting overall managed services penetration. Long-term program roadmaps assure visibility to providers, encouraging multiyear investments in skills and data-center capacity that strengthen the Qatar managed services market.

Escalating cyber-threat landscape across critical sectors

Twenty-three million attempted attacks in 2022 prompted the National Cybersecurity Strategy 2024-2030 with a USD 1.64 billion budget earmarked for workforce development and infrastructure protection. Mandatory breach reporting and rising regulatory fines, such as the Qatar Financial Centre’s USD 150,000 penalty, raise the cost of non-compliance. Energy, finance, and healthcare organizations increasingly outsource security monitoring, threat intelligence, and incident response to certified providers. Salary premiums for in-house security talent make outsourcing economically attractive, further boosting the Qatar managed services market.

New Personal Data Protection Law driving data-residency outsourcing

The law introduces strict consent, localization, and breach-notification rules. Multinationals must reconcile GDPR with Qatar-specific mandates, making compliant hosting a critical differentiator. Partnerships like Ooredoo–Google Cloud guarantee local data storage while offering global analytics capabilities. Managed providers bundle data-governance, encryption, and audit services, securing steady demand among banking, telecom, and e-commerce players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign MSP licensing and local-ownership rules | -1.9% | National | Medium term (2-4 years) |

| Senior cloud/security talent scarcity and wage inflation | -2.3% | Doha and industrial zones | Long term (≥ 4 years) |

| Limited hyperscale data-center capacity | -1.1% | National | Medium term (2-4 years) |

| LNG-linked budget cyclicality | -1.6% | Government and energy sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of senior cloud/security talent and high wage inflation

Monthly salaries reach QAR 45,000 for cloud architects and QAR 15,119 for security consultants, straining provider cost structures[3]EDOXI, “2025 Cybersecurity Job Trends in Doha,” edoxi.com . The government’s ambition to create 13,000 AI jobs by 2030 intensifies competition. Skill shortages cap project throughput, elongate deployment timelines, and reduce profit margins, especially for SME-focused providers. Although the National Cyber Security Academy opened in 2024, near-term supply–demand gaps persist, constraining segment growth across the Qatar managed services market.

LNG-linked budget cyclicality dampening long-term IT contracts

Hydrocarbon revenues still fund most public spending; a 30% capital-expenditure cut by QatarEnergy in 2020 exemplifies the volatility. When commodity prices dip, ministries and state-owned enterprises freeze or shorten managed-services contracts, weakening providers’ revenue visibility. The North Field expansion offers some insulation, yet CIOs remain cautious, often favoring flexible, consumption-based agreements over multi-year commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Dominate While Cloud Accelerates

Managed security contributed 27.84% of the Qatar managed services market share in 2025 as enterprises prioritized threat intelligence, endpoint detection, and compliance services. Spending gains momentum from the USD 1.64 billion National Cybersecurity Strategy that directs funds toward 24×7 monitoring and incident-response platforms. Qatar's managed services market size for security is projected to climb steadily as energy and transport operators adopt zero-trust frameworks to mitigate geopolitical risk. Asset-management modules protect OT environments, whereas risk-and-compliance services surge after enforcement fines in the financial district.

Managed cloud services, growing at 11.72% CAGR, reflect organizations’ pivot to hybrid architectures that satisfy data-residency mandates and scalability needs. Large contracts, such as Qatar Airways’ shift of analytics workloads to Google Cloud, highlight demand for migration, optimization, and FinOps capabilities. Infrastructure and hosting remain relevant for legacy workloads, yet their share gradually declines as containerization and serverless patterns mature. Disaster-recovery subscriptions rise alongside telemedicine uptake, ensuring continuity for 1.5 million virtual consultations processed in 2024.

By Deployment Model: Hybrid Architectures Gain Ground

Public-cloud environments retained the largest footprint in 2025, capturing 42.78% of the Qatar managed services market. The presence of Microsoft’s Qatar cloud region and MEEZA’s expanding facilities shortens latency and satisfies sovereignty requirements. Banks, insurers, and e-commerce platforms host front-end applications in public regions while encrypting sensitive databases locally, sustaining demand for cloud governance and interconnect services.

Hybrid cloud, forecast to post a 16.05% CAGR, resolves conflicting needs for sovereignty, performance, and global reach. Ooredoo’s managed-hybrid offering, underpinned by local Google Cloud infrastructure, exemplifies how providers bundle compliance, orchestration, and managed Kubernetes stacks into turnkey packages. On-premise deployments persist in defense and upstream energy, but lifecycle refresh cycles increasingly include edge gateways that integrate with central cloud control planes, subtly shifting workloads toward hybrid models and expanding the Qatar managed services market.

By End-User Vertical: BFSI Leads, Healthcare Surges

BFSI retained a 22.15% share of the Qatar managed services market size in 2025 as banks modernized mobile channels and payment rails. The Qatar Central Bank’s digital-currency sandbox stimulates blockchain infrastructure projects, further elevating managed security and compliance tasks. Conversely, the healthcare sector grows the fastest at 12.86% CAGR, propelled by 300 digital-health projects within the National Health Strategy 2024-2030. Tele-ICU, e-pharmacy, and AI-diagnostics platforms necessitate resilient hosting, interoperability layers, and HIPAA-aligned security controls, all sourced via managed-service contracts.

Oil and gas companies remain heavy consumers, funding digital twins, predictive maintenance, and 5G private networks in Ras Laffan. Retail and logistics tap IoT and smart-city platforms to optimize fulfillment cycles, supporting uptake of AIOps and managed analytics. Education accelerates classroom digitalization initiatives that rely on secure, cloud-delivered collaboration suites, broadening the Qatar managed services industry footprint.

By Enterprise Size: Large Enterprises Anchor Spend; SMEs Accelerate

Large enterprises generated 50.62% of 2025 revenue, leveraging deep budgets to secure multi-domain support that covers infrastructure, security, and application stacks. Qatar Airways’ partnership with Thales to deploy the FlytEDGE cloud-native inflight entertainment suite illustrates such complex engagements that require on-site and remote managed services. Long procurement cycles and stringent SLAs continue to favor established MSPs with ISO 27001 certifications.

SMEs, aided by Qatar Development Bank grants and a regulatory handbook on cloud adoption, are forecast to expand at a 14.78% CAGR. Consumption-based pricing, bundled cybersecurity, and quick-start migration kits lower entry barriers. As digital commerce booms among homegrown brands, managed service providers introduce tiered packages that include storefront hosting, DevSecOps, and 24×7 SOC coverage, broadening the Qatar managed services market’s reach beyond the enterprise segment.

Geography Analysis

Doha remains the epicenter of the Qatar-managed services market, hosting Microsoft’s cloud region, MEEZA’s five data centers, and the Qatar Science and Technology Park’s innovation campus. Proximity to ministerial headquarters streamlines government migration projects, while telecom carriers deploy metro fiber loops that reduce latency for financial-trading and video-streaming workloads.

Industrial cities such as Ras Laffan, Mesaieed, and Dukhan drive vertical-specific demand. LNG facilities integrate real-time analytics and OT-security monitoring, prompting on-site managed-edge nodes hardened against harsh environments. Managed service providers position satellite offices nearby to comply with safety briefings and maintenance windows specified by QatarEnergy, whose 126 million-ton North Field expansion secures long-term IT budgets.

Qatar’s compact geography fosters rapid response SLAs, a competitive advantage over neighboring GCC states. International subsea cables and zero-income-tax policies attract hyperscalers and talent alike, reinforcing the nation’s role as a managed-services hub for enterprises pursuing regional headquarters. Mega-events like Web Summit Qatar expose local MSPs to foreign buyers, widening cross-border contract opportunities and enhancing the strategic relevance of the Qatar managed services market.

Regulatory Landscape

Qatar’s ICT and managed services activity sits under a multi-agency framework led by the Ministry of Communications and Information Technology (MCIT) for national digital programs and government ICT standards, the Communications Regulatory Authority (CRA) for telecom and ICT market regulation, and the National Cyber Security Agency (NCSA) for cybersecurity and privacy oversight. Public-sector engagements are shaped by MCIT’s government-wide internal IT policy requirements, while sector regulators (for example, in financial services) add compliance expectations that increase demand for certified managed security and governance providers.

Cloud adoption is increasingly policy driven. Qatar’s government Cloud First Policy requires government entities to consider cloud options ahead of on-premise deployments, and CRA’s Cloud Policy Framework plus its regulation for cloud data interoperability and portability introduce obligations that affect how managed cloud contracts are structured, including migration support and portability. In parallel, the Personal Data Privacy Protection Law (PDPPL), enforced through the National Data Privacy Office under the NCSA, tightens requirements around consent, security controls, and third-party processor supervision, reinforcing demand for locally compliant hosting, managed security, and audit-ready operations.

Value Chain Analysis

The value chain starts with national policy and procurement direction from MCIT and related government bodies under the National Digital Agenda 2030 and the Third National Development Strategy (2024-2030), which set priorities for cloud-first adoption, cybersecurity, and sector digitization. Infrastructure foundations are provided by telecom and backbone connectivity players such as Ooredoo, Vodafone Qatar, and Qatar National Broadband Network (QNBN), alongside local data center operators (notably MEEZA) and in-country cloud regions operated by hyperscalers (Microsoft, AWS, and Google Cloud), supporting low-latency managed hosting and cloud operations.

Service delivery is carried out by domestic systems integrators and managed service providers (including MEEZA and Gulf Business Machines Qatar), typically bundling advisory, migration, integration, 24x7 operations, and managed security capabilities for government and regulated verticals. Upstream inputs include OEM and software vendor ecosystems spanning security, observability, and cloud platforms, while downstream demand is concentrated in government, BFSI, and oil and gas programs that require stringent SLAs and compliance. Talent availability in cloud and security, along with the pace of hyperscaler-grade capacity additions, remains a bottleneck that affects delivery timelines, cost structures, and the feasibility of high-availability and disaster recovery offerings.

Competitive Landscape

Innovation and Specialization Drive Future Success

Success in the Qatar managed services market increasingly depends on providers' ability to deliver innovative, industry-specific solutions while maintaining service excellence and cost competitiveness. Incumbent players need to continue investing in emerging technologies like AI, IoT, and cloud while developing deep vertical expertise in key sectors like government, financial services, and oil and gas. Building strong cybersecurity capabilities, achieving relevant certifications, and maintaining compliance with evolving regulations are critical for maintaining market leadership. Companies must also focus on talent development and retention while optimizing their delivery models to improve operational efficiency.

For new entrants and challenger firms, the path to success lies in identifying and focusing on underserved market segments or specialized service areas where they can build distinctive capabilities. Developing strong partnerships with global technology providers while maintaining local market understanding and relationships is essential. Companies need to carefully evaluate customer concentration risks and build diversified client portfolios across industries. The ability to demonstrate a clear value proposition, maintain service quality, and build long-term client relationships while managing competitive pressures on pricing will be crucial for gaining market share. Regulatory compliance and data sovereignty requirements will continue to influence service delivery models and market entry strategies.

Qatar Managed Services Industry Leaders

MEEZA QSTP LLC

Gulf Business Machines Qatar W.L.L.

Diyar Group

Paramount Computer Systems FZ-LLC

Ooredoo Q.P.S.C

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Government platform consolidation and cloud resiliency programs are creating clear whitespace for managed cloud operations, integration, and security services. In February 2026, MCIT and Oracle signed a three-year renewal for government technical support and established a new dedicated Oracle cloud region aimed at backup and operational resilience for government digital services. That move expands opportunities for managed migration, hybrid operations, and continuity management for sovereign workloads. In June 2026, MCIT launched the enhanced Hukoomi platform as the first product of the Digital Factory initiative, which increases the need for managed integration, API management, application operations, and security monitoring across centralized citizen and business services.

Capacity and connectivity upgrades are also changing what providers can deliver locally, which supports higher-value managed services such as disaster recovery, high-availability architectures, and latency-sensitive cloud management. In July 2026, MEEZA completed a 4 MW data center expansion delivered to a global hyperscaler under a long-term agreement, improving local hosting options for regulated and data-resident workloads. Separately, Doha IX operated by Ooredoo, integrated with DE-CIX Marseille, improves access to global internet exchanges and hyperscaler platforms, creating room for managed network, cloud interconnect, and cross-border SaaS performance management services. SME digitization programs such as MCIT’s SMEs Go Digital, supported by matchmaking involving 59 service providers, further open a scalable route for packaged managed services across endpoint, security, and cloud adoption for smaller customers.

Recent Industry Developments

- July 2026: MEEZA completed a 4 MW data center expansion that was delivered to a global hyperscaler under a long-term agreement (delivered on 21 June 2026). The added hyperscaler-grade capacity supports in-country hosting for data-resident workloads and increases the ceiling for managed cloud, security, and business continuity services delivered from Qatar.

- December 2025: MEEZA and Huawei signed two strategic MoUs during MWC25 Doha to collaborate across digital infrastructure, AI, and talent development initiatives. The collaboration supports broader solution packaging for enterprise and government customers that want managed infrastructure combined with AI-ready platforms and local capability building.

- October 2024: Gulf Business Machines (GBM) and Splunk formed a strategic partnership during GITEX Global 2024 to deliver cybersecurity and observability solutions across the Gulf region. This strengthens managed security and monitoring propositions available to Qatar customers that need SOC integration, threat detection, and service assurance across hybrid environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We size the Qatar managed services market as the revenue earned from outsourced, ongoing IT operations delivered to customers in Qatar, where a provider runs, monitors, and improves defined IT functions under a service contract.

Scope exclusions: The sizing excludes one-off implementation only work that does not include continued management, and also excludes pure hardware resale without an attached managed service.

Segmentation Overview

- By Service Type

- Managed Infrastructure (Network, Desktop)

- Managed Hosting (Application, Data Center)

- Managed Security

- Asset Management and Monitoring

- Threat Intelligence and Management

- Risk and Compliance

- Other Managed Security

- Managed Cloud Services

- Disaster Recovery and Business Continuity

- By Deployment Model

- On-premise

- Cloud-based

- Hybrid

- By End-user Vertical

- Government

- BFSI

- Oil and Gas

- IT andTelecom

- Healthcare

- Retail and E-commerce

- Education

- Logistics and Transportation

- By End-user Enterprise Size

- Large Enterprises

- SMEs

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding the Qatar demand environment and the spend pools that typically feed managed services. We rely on public signals such as ICT and cloud policy releases, telecom regulator updates, and national digital program announcements, which help clarify what types of managed delivery are being prioritized.

We also review non paywalled sources such as ministry portals and national strategy documents, International Telecommunication Union indicators, World Bank macro series, and WTO trade and services data, followed by company filings, investor presentations, and reputable press coverage for Qatar deals and contract movement. Where it helps validate scale, we selectively cross-check company financials and news intelligence through a paid subscription, and we also scan public patent databases to understand security and automation direction. These sources are illustrative only, and many other references were used to collect data points, validate assumptions, and clarify scope questions.

Primary Interviews and Surveys

Primary work is used to turn desk signals into usable sizing inputs, such as service attach rates, contract tenures, and typical pricing movement for infrastructure, hosting, security, cloud operations, and DR and business continuity. We speak with provider-side leaders and delivery managers, and we also include customer-side IT and security owners across government, BFSI, oil and gas, and telecom so demand patterns are not assumed from supply only. For this country market, feedback is focused on Qatar buying behavior and on-the-ground contract structures.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | |

| Mid tier: 50% | Functional/Unit leaders: 28% | |

| Smaller Players: 18% | Managers: 58% |

Market-Sizing & Forecasting

Sizing begins from a top-down build that reconstructs the addressable managed services spend inside Qatar by mapping enterprise IT and telecom service outlays into the portions typically contracted as run and operate services. Once that demand pool is shaped, we corroborate it using selective bottom-up checks, such as sampled contract values by service line, channel feedback on managed security and cloud operations uptake, and sanity checks on revenue ranges for active providers.

Inputs used in the model include cloud adoption pace in large accounts, cybersecurity compliance push in regulated sectors, outsourcing penetration by vertical, average contract length and renewal behavior, and service scope mix shifts between infrastructure, hosting, security, managed cloud, and DR and business continuity. When a data gap shows up for a smaller service area, ranges are applied based on interview medians and then tightened using observed deal patterns. Forecasting is run using scenario analysis, where drivers like public sector digital projects, security spending intensity, and cloud workload migration are stress-tested, and the final trajectory is aligned to expert consensus on what is realistic over the next cycle.

Data Validation & Update Cycle

Validation is done through several passes that check whether totals and service splits behave like the real market. We compare outputs against independent signals such as major contract announcements, macro ICT spend direction, and security and cloud adoption narratives, then we re-check any sharp jumps that do not match customer procurement cycles.

Before sign-off, assumptions are reviewed by another analyst and large variances trigger re-contact with selected interviewees so the reason is clearly understood. Reports are refreshed each year, and interim updates are made when material events occur, such as regulatory shifts or large multi-year outsourcing awards. Before delivery, we do a fresh scan so clients receive the latest updated view.

Mordor Intelligence's Qatar Managed Services Market Size Versus Other Published Estimates

Published market numbers for Qatar managed services can differ a lot, even when they look like they are talking about the same topic. The differences usually come from what is counted as managed services versus broader IT services, which year is treated as the base, and how pricing and renewals are handled in the model.

A second driver is the treatment of managed security and managed cloud operations, since some estimates only capture a narrow IT outsourcing slice or mix in adjacent consulting and integration revenue. Another source of spread is currency timing and how multi-year contracts are annualized, which can inflate a single year if backlog is pulled forward. The approach here keeps service scope tied to run and operate revenue recognized in-year, including infrastructure, hosting, security, managed cloud, and DR and business continuity, and this inclusion choice explains much of the gap, a modeling decision applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.59 B (2025) | |

| Trade Journal A | USD 0.59 B (2024) | Uses a smaller near-term spend view that reads like a narrower outsourcing or managed security slice, and it reports a different base year and forecast window, which reduces the counted revenue pool. |

| Industry Platform B | USD 0.95 B (2024) | Anchored to IT services revenue and an outsourcing sub-segment framing, which can exclude managed infrastructure and ongoing cloud operations, and it may apply different contract annualization and pricing assumptions. |

The table shows that the biggest spread is not only about growth expectations, it is mainly about what revenue lines are included and how contracts are converted into an annual market value. By keeping the steps traceable to service scope, in-year revenue recognition, and a small set of practical demand drivers, we can explain the number and update it consistently when market conditions change.

Key Questions Answered in the Report

What is the 2026 value of the Qatar managed services market?

The sector is valued at USD 34.74 billion in 2026.

How fast is the market expected to grow?

It is forecast to post a 9.96% CAGR between 2026 and 2031.

Which service type currently dominates spending?

Managed security leads with 27.84% revenue share in 2025.

Why are hybrid cloud models gaining popularity?

Hybrid deployments balance data-residency compliance with global scalability, pushing 16.05% CAGR.

Which vertical shows the fastest growth?

Healthcare is expanding at 12.86% CAGR through 2031 due to telemedicine and AI diagnostics initiatives.

Page last updated on: