Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

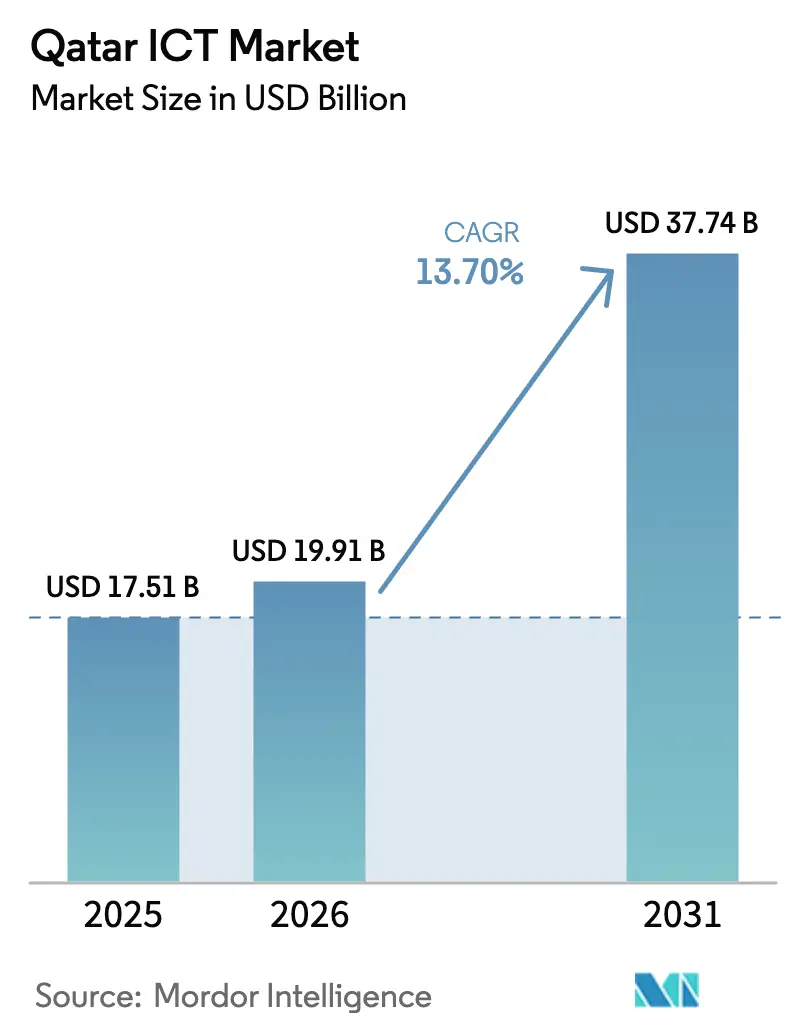

| Base Year Market Size (2025) | USD 17.51 Billion |

| Market Size (2026) | USD 19.91 Billion |

| Market Size (2031) | USD 37.74 Billion |

| Growth Rate (2026 - 2031) | 13.70% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Qatar ICT Market Analysis by Mordor Intelligence

The Qatar ICT market size was valued at USD 17.51 billion in 2025 and estimated to grow from USD 19.91 billion in 2026 to reach USD 37.74 billion by 2031, at a CAGR of 13.7% during the forecast period (2026-2031). Rapid 5G roll-out, sovereign cloud investments, and mandatory Arabic large-language-model (LLM) development are accelerating enterprise digitization, while the National Digital Agenda 2030 channels more than USD 2.47 billion of public funds into next-generation infrastructure [1]International Trade Administration, “Qatar - Digital Economy,” trade.gov. Communication Services remain the revenue backbone as telecom operators densify networks ahead of the Asian Games 2030, yet Cloud Services post the steepest growth thanks to data-sovereignty-compliant hyperscale launches by Microsoft and regional carriers. Intensifying competition among Ooredoo, Vodafone Qatar, and global hyperscalers is spurring price innovation in managed security, edge, and GPU hosting, opening fresh opportunities for domestic software firms that localize Arabic applications. On the demand side, banking, energy, and public administration projects dominate contract value, but esports venues and smart-manufacturing pilots signal emerging pockets of high-margin spend.

Key Report Takeaways

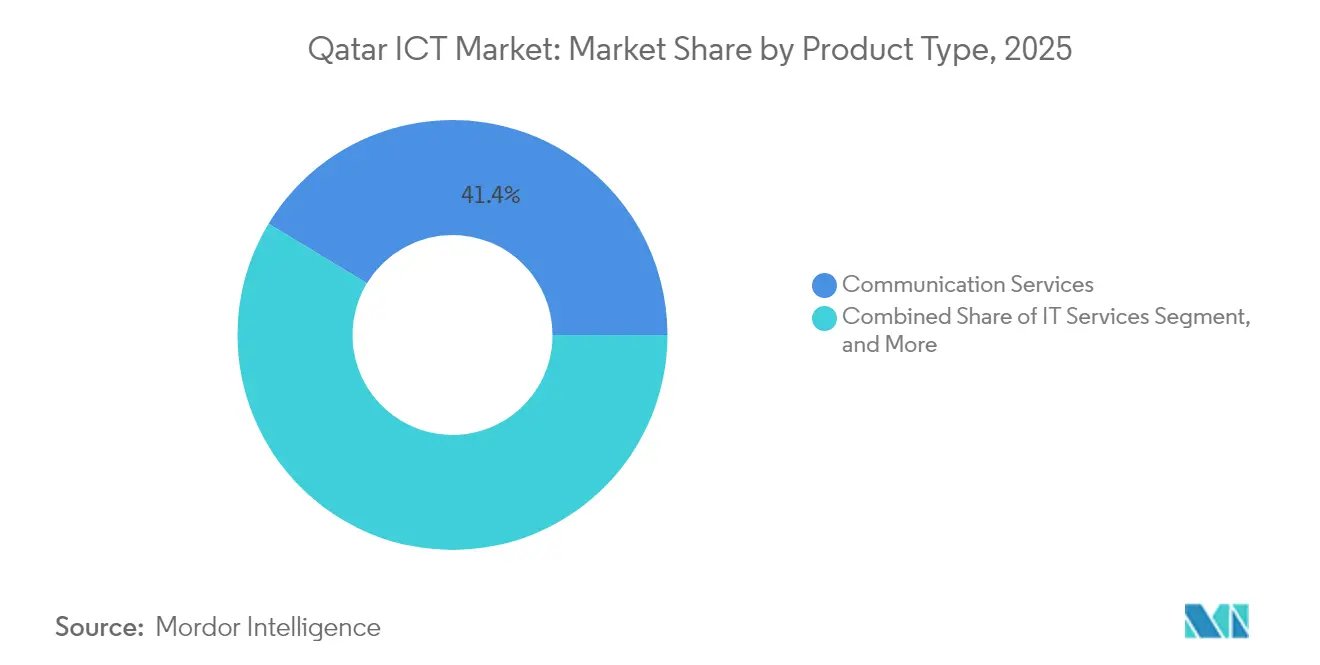

- By product type, Communication Services led with 41.35% revenue share in 2025, while Cloud Services are projected to expand at a 21.7% CAGR through 2031.

- By enterprise size, large enterprises commanded 71.30% of the Qatar ICT market share in 2025; SMEs record the fastest 12.3% CAGR to 2031.

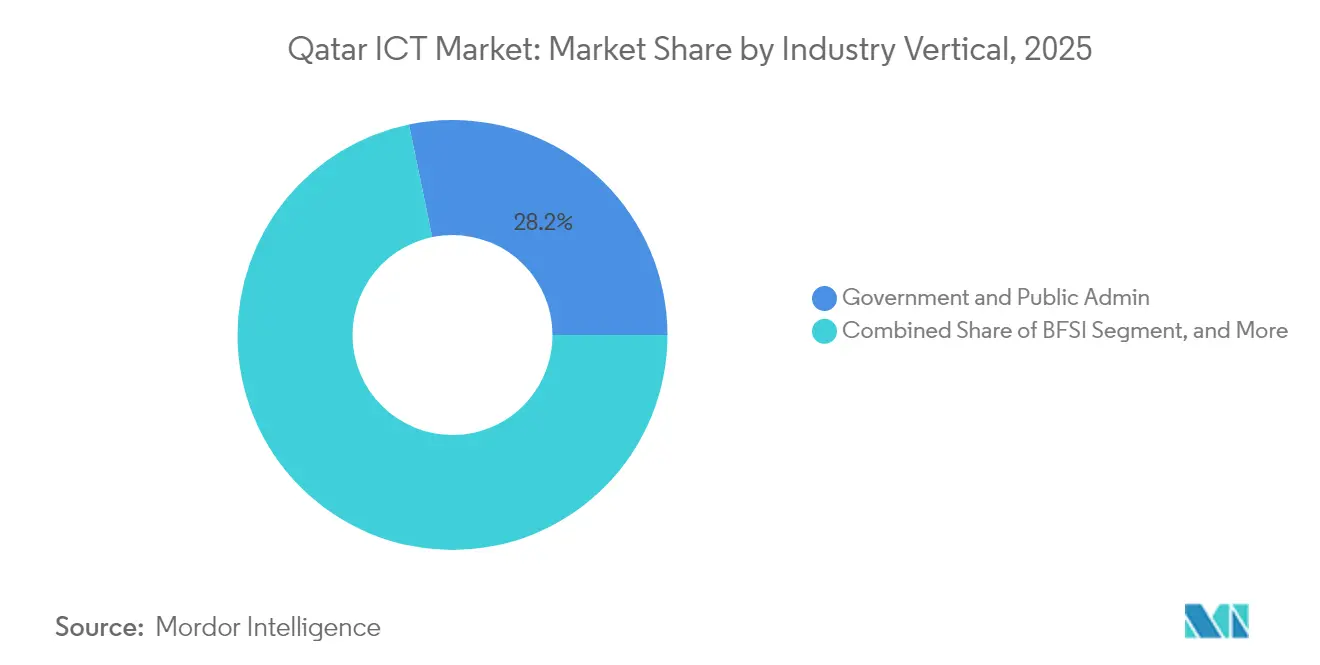

- By industry vertical, Government and Public Administration held 28.25% of 2025 revenue, whereas Gaming and Esports is advancing at 17.3% CAGR to 2031.

- By deployment mode, on-premises solutions represented 63.55% of 2025 spend; cloud-only deployments show a 21.4% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G roll-out and network densification | +2.8% | Doha, Al Rayyan, Lusail | Medium term (2-4 years) |

| Government Digital Agenda 2030 capital spending | +3.2% | National smart-city corridors | Long term (≥ 4 years) |

| Rapid cloud take-up within the BFSI sector | +2.1% | Doha Financial District | Short term (≤ 2 years) |

| Mega-events pipeline (Asian Games 2030, Expo 2033) | +1.9% | Doha metro area | Medium term (2-4 years) |

| Mandated Arabic-LLM build-out | +1.6% | Doha tech parks | Medium term (2-4 years) |

| Compulsory critical-infrastructure cyber audits | +1.4% | Energy and finance hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G roll-out and network densification

Vodafone Qatar’s 2025 agreement with Nokia is modernizing the nationwide radio and core layers to support low-latency 5G slicing for industrial IoT and 8 K streaming, aligning with the regulator’s December 2025 3G sunset that frees up spectrum for enhanced mobile broadband. Parallel trials by Ooredoo using Wi-Fi 7 over fiber deliver four-fold throughput gains, reinforcing Qatar’s ambition to provide 10 Gbps residential access and bolster enterprise edge computing . These upgrades enable smart-stadium analytics and autonomous shuttle pilots for the Asian Games 2030, reinforcing Qatar ICT market growth prospects.

Government Digital Agenda 2030 capital spending

The Third National Development Strategy allocates multi-year funds so that digital public services account for at least 90% of citizen transactions by 2030. Key programs include a five-year partnership with Scale AI covering more than 50 AI use cases, and the launch of a National Cyber Security Academy to train local talent[2]Digital Watch Observatory, “Five-year agreement to bring AI-driven improvements to Qatar,” dig.watch . Spending commitments extend to quantum-ready research and new sovereign-cloud regions, anchoring long-run demand for consulting, integration and secure hosting capacities within the Qatar ICT market.

Rapid cloud take-up within the BFSI sector

Commercial Bank and Meeza’s secure cloud platform supports instant payments and analytics, illustrating the sector’s pivot toward hybrid architectures that satisfy Qatar Central Bank compliance rules. Microsoft’s hyperscale region, operating under local data-privacy law 13-2016, now hosts core banking workloads for leading lenders, cutting disaster-recovery RPOs from hours to minutes. As financial institutions chase real-time risk management, the Qatar ICT market size attached to BFSI workloads is set to expand steadily through the forecast horizon.

Mega-events pipeline boosting ICT demand

Building on World Cup infrastructure, organizers of the Asian Games 2030 and Expo 2033 are issuing tenders for 8 K broadcast, crowd-analytics and ticketless entry systems. These projects combine edge compute, private 5G and IoT sensors, injecting multi-year capex into the Qatar ICT market while leaving a post-event smart-city legacy that underpins e-government and tourism apps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cyber-skills shortage inflating wage bills | -1.8% | National | Long term (≥ 4 years) |

| Heavy reliance on foreign OEMs raising lifecycle TCO | -1.2% | National | Medium term (2-4 years) |

| New data-localization decree limiting cross-border SaaS uptake | -0.9% | Multinational corporates | Short term (≤ 2 years) |

| Higher water and power tariffs squeezing data-center P&L | -0.7% | Data-center clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute cyber-skills shortage inflating wage bills

Despite the National Cyber Security Agency’s training academy, demand for qualified analysts outstrips local supply, forcing enterprises to import talent at wage premiums above regional norms. The situation is acute in energy and banking, where critical-infrastructure audit deadlines create time-sensitive hiring spikes. Elevated labor costs erode margins for managed security providers and could temper Qatar ICT market expansion if unaddressed.

Heavy reliance on foreign OEMs raising lifecycle TCO

Core routers, GPU clusters and storage arrays are sourced almost entirely from U.S., European and East-Asian vendors. Currency swings and extended spares lead-times inflate total cost of ownership, particularly for data-center operators locked into proprietary architectures. Government-backed localization rules now offer tariff rebates for assemblies completed in Qatar, yet supplier diversification remains a medium-term necessity for cost-efficient growth of the Qatar ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Communication Services retain scale, cloud accelerates

Communication Services generated the largest share of Qatar ICT market revenue at 41.35% in 2025, reflecting sustained mobile-data demand, fiber roll-outs and wholesale transit fees. The segment benefits from mandatory VoLTE migration and 5G enterprise slicing, providing steady cash flow for network operators. Conversely, Cloud Services exhibit the fastest 21.7% CAGR as hyperscale regions and local sovereign-cloud zones allow banks and ministries to comply with data-residency law 13-2016. Robust GPU demand for Arabic LLMs and AI-driven customer interaction further boosts cloud uptake. IT Hardware sales track densification cycles across mobile and data-center footprints, while Software growth is propelled by low-code platforms that local firms adapt for Arabic interfaces.

Historical spending showed Communication Services navigating margin compression through bundle innovations, whereas present momentum clearly favors cloud elasticity. Market players are increasingly combining managed security with unified communications to defend share. Local system integrators align with the sovereign-cloud push, creating cross-sell opportunities into analytics and workflow software. The sector’s shift aligns with National Digital Agenda targets that prioritize cloud-delivered public services, lifting the Qatar ICT market size for XaaS offerings more sharply than for legacy hardware.

By Enterprise Size: Large enterprises dominate, SME digitization catches up

Large enterprises controlled 71.30% of 2025 spend, fueled by mega-project budgets within government, energy and aviation. Their roadmaps encompass ERP cloud migration, zero-trust security and AI-augmented workflows worth tens of millions of USD per contract. However, SME digital programs backed by Qatar Development Bank subsidies propel a 12.3% CAGR, signaling a gradual re-balancing of the Qatar ICT market. Lower entry costs for SaaS, simplified e-invoice mandates and marketplace access entice micro-firms to adopt accounting and CRM clouds.

For incumbents, hybrid-cloud governance and localized data-lake architectures are key procurement criteria. SMEs, in contrast, prioritize pay-as-you-go platforms bundled with cybersecurity baselines, narrowing the digital divide. Channel partners offering turnkey e-commerce and payment APIs capitalize on this wave. Over time, SME digital maturity is expected to unlock indigenous app-development talent, reinforcing the government’s ambition to generate 26,000 ICT jobs and broadening the Qatar ICT market addressable base.

By Industry Vertical: Public sector leads, esports surges

Government and Public Administration contributed 28.25% of 2025 turnover due to massive e-services re-platforming and AI chatbots that reduce citizen touch-points. Mandatory LLM training datasets amplify compute demand, sustaining public-sector outlays. In parallel, Gaming and Esports post a 17.3% CAGR as purpose-built arenas, streaming studios and regional tournaments draw sponsorships and media rights. The Qatar ICT market share commanded by public-sector buyers remains high, but esports monetization of cloud gaming, VR and influencer analytics injects new revenue paths for service providers.

Banks exploit sovereign cloud and ISO 27001 alignment to roll out instant payments and anti-fraud AI, while energy utilities deploy IoT sensors for predictive maintenance of LNG terminals. Manufacturing pilots under Factory One showcase 5G-connected robotics, signaling future diversification. Healthcare taps AI imaging tools hosted locally. This vertical mix underscores policy goals of diversifying non-hydrocarbon GDP by 4% annually, translating into broad-based demand for secure, low-latency digital infrastructure within the Qatar ICT market.

By Deployment Mode: On-premises still majority, cloud-only scales rapidly

On-premises solutions accounted for 63.55% of 2025 spend, reflecting risk aversion and data-sovereignty obligations across defense, finance and energy. Nevertheless, cloud-only environments achieve a 21.4% CAGR as hyperscale and sovereign regions achieve ISO 27001 and local privacy compliance, mitigating earlier regulatory hurdles. Hybrid deployments emerge as a middle path, combining on-prem workloads with low-latency cloud analytics and disaster recovery replicas.

Initial migrations focus on customer-facing portals and dev-test workloads; later waves encompass core ERP and data lakes. Vendors differentiate on transparent residency controls and in-country support. As more ministries receive clearance for confidential-workload hosting, the Qatar ICT market size attributable to off-premises consumption is set to rise steadily, narrowing the on-prem share by the decade’s close.

Geography Analysis

Qatar’s compact landmass enables near-universal fiber coverage, with national broadband reaching major municipalities and industrial zones. International subsea cables land directly in Doha, creating single-digit-millisecond round-trip latency to Europe and India, a decisive factor for cloud and trading workloads. The presence of LNG-powered generation ensures resilient electricity supply for Tier III+ data centers, although planned tariff revisions could weigh on operator margins.

Doha remains the nexus of the Qatar ICT market owing to the concentration of ministries, banks and headquarters. Smart districts such as Msheireb deploy integrated IoT platforms, open-access fiber and autonomous shuttles that serve as living laboratories for local tech start-ups. Lusail’s stadiums and Expo site extend digital infrastructure northwards, while Al Rayyan hosts edge nodes that offload metro traffic. The clustering effect underpins an ecosystem where telcos, hyperscalers and academia co-locate, accelerating innovation cycles.

Regionally, Qatar leverages GCC collaborations to aggregate content delivery and cross-border cloud recovery. Ooredoo’s memorandum with stc Group synchronizes network APIs across markets, giving multinationals consistent SLAs. The country’s visa-light policies and 100% foreign ownership zones attract regional headquarters of U.S. and Asian software firms, deepening the skills pool and broadening solution portfolios available in the Qatar ICT market.

Competitive Landscape

Market leadership is shared by Ooredoo, Vodafone Qatar and global hyperscalers that jointly shape service bundles and price points. Ooredoo’s 15% normalized net-profit jump in Q3-2024 reflects upselling of 5G-enabled managed services and GPU rentals for Arabic-LLM training [3]Ooredoo Group, “Ooredoo Group Q3 2024 – Normalized Net Profit Rises 15%,” ooredoo.com. Vodafone’s network-modernization pact with Nokia positions it for enterprise 5G slicing as it leverages its 8.1% Q1-2025 net-profit increase to fund digital-service innovation . Microsoft’s in-country region offers confidential computing and multi-zone resilience, attracting banks, airlines and ministries seeking cloud certification under national privacy law.

Strategic alliances dominate go-to-market models. Ooredoo-NVIDIA GPU clusters, Microsoft-MCIT AI sandboxes and SAP’s RISE partnerships provide turnkey stacks that de-risk transformation projects. Local ISVs focus on Arabic UX and compliance wrappers, enhancing vendor stickiness in the Qatar ICT market. White-space opportunities lie in SME cybersecurity platforms and Industry 4.0 edge appliances, segments where global players still lack localized offerings[4]Investment Opportunities in Qatar's Manufacturing Sector." April 13, 2025. https://www.invest.qa/en/sectors-and-opportunities/manufacturing..

Emergent challengers include Snoonu, which leverages a five-year Web Summit collaboration to scale logistics software, and Meeza, whose sovereign-cloud services anchor sensitive government and BFSI workloads. Barriers to entry rise as the National Cyber Security Agency tightens compliance audits, giving incumbents with mature governance frameworks a defensible edge.

Qatar ICT Industry Leaders

-

Ooredoo Q.P.S.C.

-

Vodafone Qatar P.Q.S.C.

-

Microsoft Corporation

-

Amazon Web Services

-

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Qatar signed a five-year agreement with Scale AI to deploy more than 50 AI use cases across government services.

- February 2025: e& posted AED 59.2 billion consolidated revenue for FY-2024 and expanded its AWS collaboration to 38 countries.

- January 2025: Power International Holding acquired 100% of Mobile Telecom-Service LLP from Kazakhtelecom, strengthening regional telecom assets.

- December 2024: Qatar Computing Research Institute launched Fanar, the national Arabic LLM, at the Global AI Summit.

Qatar ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services. It enables users to digitally store, access, transmit, retrieve, and manipulate information.

The Qatar ICT market is segmented by type (Hardware, Software, IT Services, and Telecommunication Services), by the size of the enterprise (Small and Medium Enterprise and Large Enterprises), and by industry vertical (BFSI, IT and Telecom, Government, Retail and E-commerce, Manufacturing, and Energy and Utilities). The market sizes and forecasts are in terms of value (USD million) for all the above segments.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

By Deployment Mode

| On-Premises |

| Cloud-only |

| Hybrid |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming and Esports | ||

| Other Verticals | ||

| By Deployment Mode | On-Premises | |

| Cloud-only | ||

| Hybrid | ||

Key Questions Answered in the Report

How large is the Qatar ICT market in 2026 and what growth is expected by 2031?

The market is valued at USD 19.91 billion in 2026 and is projected to reach USD 37.74 billion by 2031, reflecting a 13.7% CAGR.

Which segment shows the fastest growth in Qatar’s technology spending?

Cloud Services post the steepest 21.7% CAGR as sovereign and hyperscale regions satisfy data-residency rules.

Why do on-premises deployments still dominate spending?

Critical data-sovereignty mandates and sector-specific compliance keep 63.55% of 2025 budgets on-prem, though hybrid models are gaining traction.

What is driving the surge in Qatar’s gaming and esports sector?

Purpose-built venues, government sponsorship and regional tournaments lift gaming and esports ICT outlays at a 17.3% CAGR.

Page last updated on: