Push To Talk Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 47.45 Billion |

| Market Size (2031) | USD 77.53 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Push To Talk Market Analysis by Mordor Intelligence

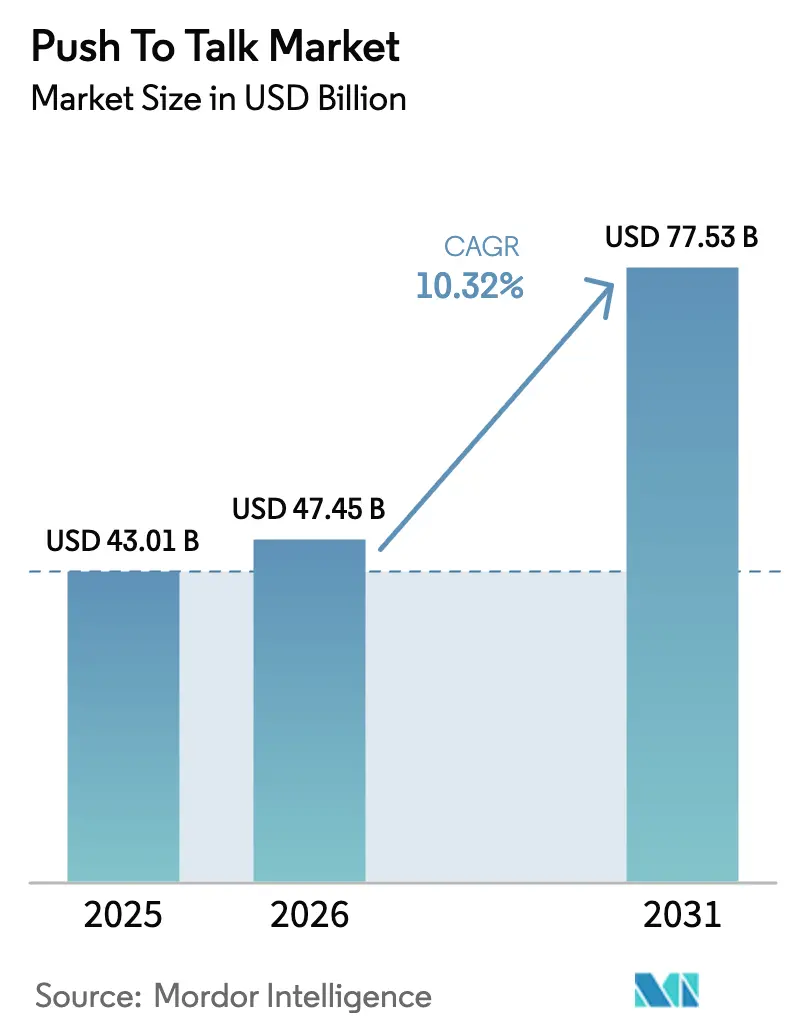

The Push To Talk Market size was valued at USD 43.01 billion in 2025 and estimated to grow from USD 47.45 billion in 2026 to reach USD 77.53 billion by 2031, at a CAGR of 10.32% during the forecast period (2026-2031).

The Push to Talk market is valued at USD 43.01 billion in 2025 and is on course to reach USD 70.82 billion by 2030, translating to a compound annual growth rate of 10.49%. Sustained demand for instant voice services in public safety, oil and gas, utilities, and logistics environments continues to pull investments toward broadband-based solutions that complement or replace Land Mobile Radio (LMR). The widening availability of carrier-integrated Mission Critical Push to Talk (MCPTT) on 5G networks, the integration of artificial intelligence in dispatch centers, and the proliferation of rugged smart devices are reinforcing the commercial case for next-generation services. At the same time, operators have to navigate fragmented spectrum allocation, semiconductor shortages, and heightened cyber-risk, factors that collectively shape procurement choices and deployment timelines. Competitive pressure is rising as traditional radio vendors, telecom infrastructure suppliers, and cloud-native software companies jostle for a larger position in the Push to Talk market.[1]European Telecommunications Standards Institute, “ETSI Announces 9th MCX Plugtests,” etsi.org

Key Report Takeaways

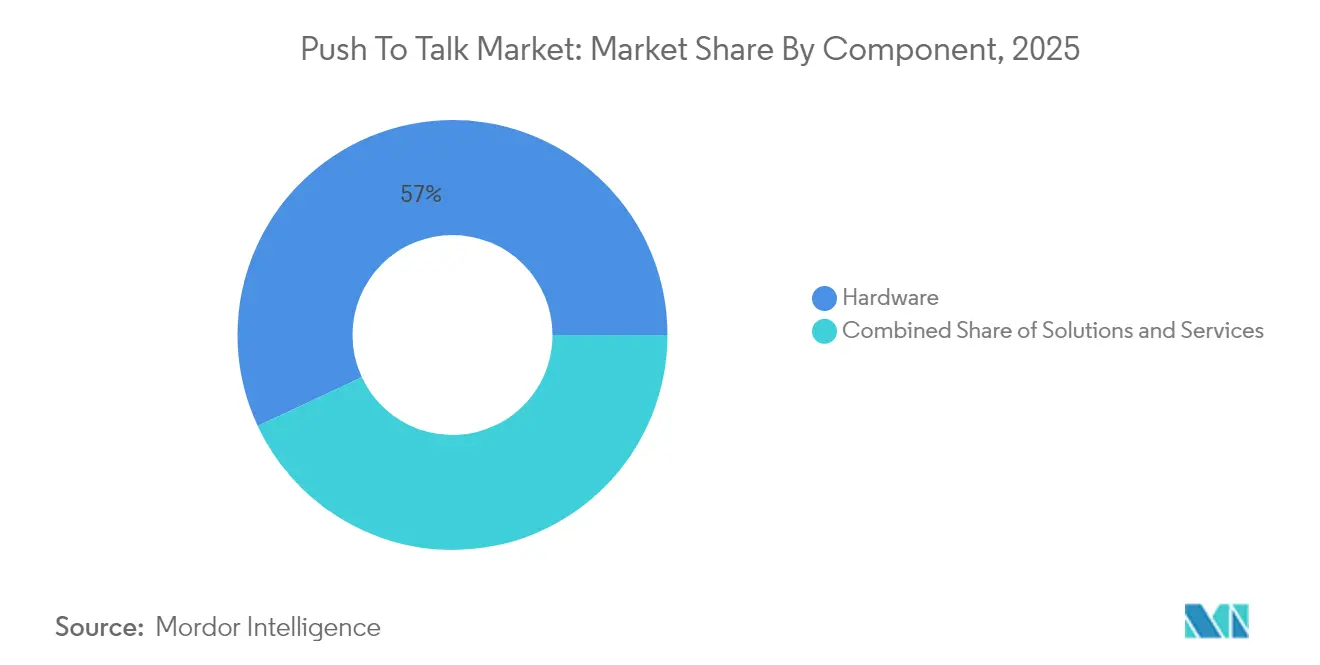

- By component, hardware led with 56.95% revenue share in 2025, while services are projected to grow at a 12.18% CAGR through 2031.

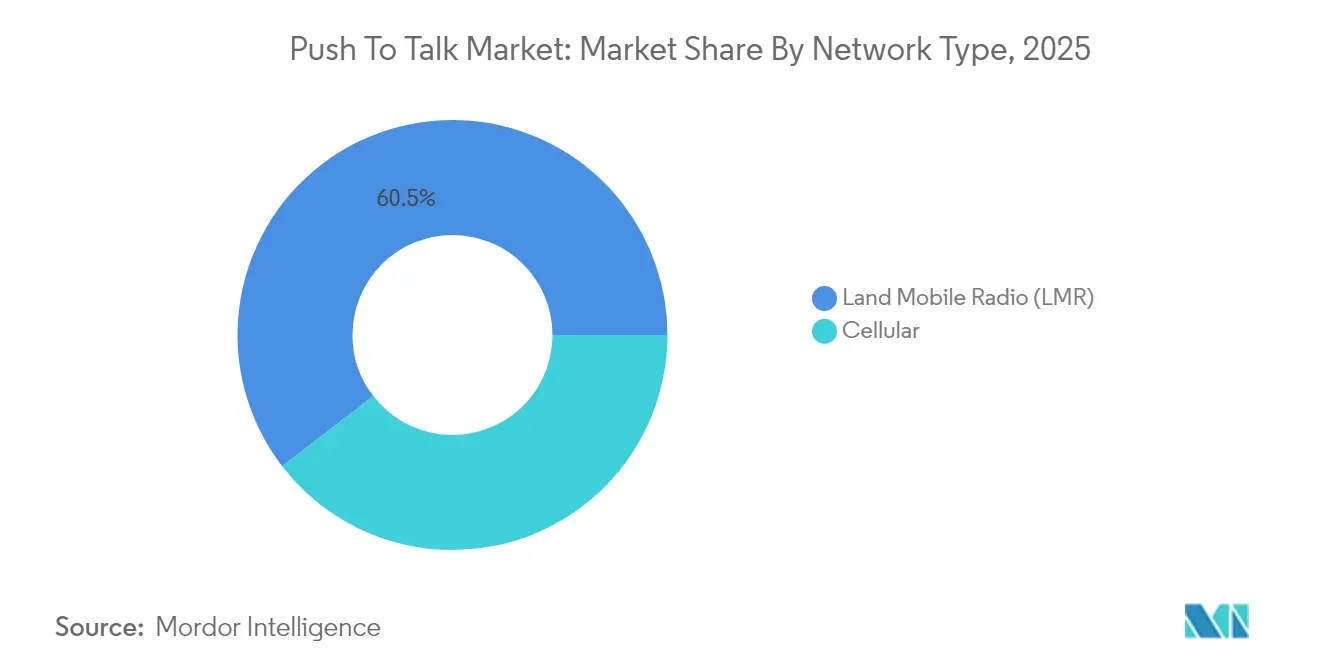

- By network type, Land Mobile Radio retained 60.45% of Push-to-Talk market share in 2025; 5G cellular networks are advancing at a 15.18% CAGR to 2031.

- By vertical, public safety accounted for 45.95% of the Push-to-Talk market size in 2025, whereas oil and gas and utilities are expected to expand at a 13.22% CAGR through 2031.

- By geography, North America held 36.35% revenue share in 2025, while Asia-Pacific is forecast to post the fastest regional growth at an 11.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Push To Talk Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration from legacy LMR to LTE/5G PoC solutions | +2.8% | Global; North America and Europe lead | Medium term (2-4 years) |

| Growing mission-critical communications demand in public safety | +2.1% | Global; strongest in developed markets | Long term (≥ 4 years) |

| Proliferation of rugged smart devices with integrated PTT | +1.9% | Asia Pacific core; spill-over to MEA and Latin America | Short term (≤ 2 years) |

| AI-driven dispatch analytics and situational awareness | +1.4% | North America and Europe first; APAC next | Medium term (2-4 years) |

| Carrier-integrated MCPTT standards (3GPP Release 18+) | +1.2% | Global; deployment paced by carriers | Long term (≥ 4 years) |

| Industrial private-5G campus networks | +0.8% | Industrial hubs in Germany, Japan, South Korea, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Migration from Legacy LMR to LTE/5G PoC Solutions

Analog and early digital LMR systems are approaching end-of-life, and agencies are turning to broadband Push to Talk over Cellular (PoC) to address voice, video, and data in one service. The United Kingdom’s Emergency Services Network provides a prominent illustration of how public safety organizations are prioritizing broadband capability while preserving mission-critical availability standards. In North America, FirstNet allows agencies to phase out P25 equipment gradually without jeopardizing coverage. Private 5G networks inside factories and offshore platforms remove the line-of-sight constraints that previously complicated LMR roll-outs. Together, these use cases continue to accelerate the Push to Talk market shift toward cellular architectures.[2]Federal Communications Commission, “4.9 GHz Band Proposals,” fcc.gov

Growing Mission-Critical Communications Demand in Public Safety

Police, fire, and emergency medical teams have moved beyond voice-only communication. Today’s frontline personnel expect broadband Push to Talk services that seamlessly stream body-worn camera feeds, drone footage, and sensor data back to command centers. NATO field exercises in 2025 validated how 5G can maintain secure communications across multiple agencies operating jointly, highlighting the need for interoperable, low-latency services. Despite tight municipal budgets, federal grants motivate system upgrades that bring predictive analytics and location awareness into routine operations. These requirements ensure that public safety will remain the anchor vertical within the Push to Talk market.[3]GovCon Wire, “DoD Completes NATO 5G Exercises,” govconwire.com

Proliferation of Rugged Smart Devices with Integrated PTT

Rugged Android handsets now combine Push to Talk buttons, high-resolution cameras, and barcode scanners, displacing single-purpose radios for many industrial and logistics users. Cost inflation tied to chipset shortages has pushed device makers to emphasize value-added software subscriptions to preserve margins. Leasing and device-as-a-service offerings reduce customer capital outlay and shorten refresh cycles, expanding the addressable base. As enterprises evaluate total cost of ownership, device convergence is driving additional momentum into the Push to Talk market.

AI-Driven Dispatch Analytics and Situational Awareness

Artificial intelligence engines incorporated into dispatch consoles automatically analyze voice traffic, background noise, and caller sentiment. They sequence incidents based on severity and available resources, shaving critical seconds off deployment times. Real-time language translation promotes cross-border cooperation, while transcription services preserve evidentiary records without human intervention. Early adopters cite measurable reductions in false alarms and overtime costs, reinforcing the growth potential for AI-enhanced Push to Talk market solutions.

Restraints Impact Analysis of Push To Talk Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented spectrum allocation and regulatory delays | −1.8% | Global; severity varies by region | Long term (≥ 4 years) |

| Security vulnerabilities in PoC over public networks | −1.3% | Global; heightened for defense and utilities | Medium term (2-4 years) |

| Interoperability gaps between LMR and broadband PTT platforms | −0.9% | North America and Europe | Medium term (2-4 years) |

| Budgetary capital-expenditure constraints in public sector agencies | −0.7% | Developing markets mainly | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Spectrum Allocation and Regulatory Delays

Conflicting national priorities complicate the hunt for harmonized mission-critical spectrum. In the United States, protracted debates around 4.9 GHz sidelink usage have slowed statewide deployments. Europe’s reliance on 380–470 MHz TETRA channels poses integration challenges with 700 MHz broadband allocations. Certification cycles can stretch past two years, deterring smaller vendors from entering new territories and delaying revenue realization for the Push to Talk market.[4]Federal Communications Commission, “4.9 GHz Band Proposals,” fcc.gov

Security Vulnerabilities in PoC over Public Networks

Cellular Push to Talk traffic traverses shared infrastructure, increasing exposure to denial-of-service and eavesdropping threats. Operators report that 76% of attempted breaches now target signaling planes to disrupt priority services. End-to-end encryption is improving, yet multi-agency interoperability often forces temporary downgrades in cipher strength. These vulnerabilities make risk-averse buyers reluctant to abandon closed LMR networks, slowing certain Push to Talk market conversions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Push To Talk Market Segment Analysis

By Component:

Services Extend MonetizationHardware still generated USD 24.5 billion in 2025, representing the largest single slice of the Push to Talk market. Strong demand for intrinsically safe radios in petrochemical sites and for rugged smartphones in construction has kept device revenues steady. Nevertheless, managed service contracts that wrap device management, cybersecurity, and 24/7 network monitoring are outpacing unit sales growth. Service providers now bundle predictive maintenance and analytics dashboards, which elevate switching costs and lengthen customer lifecycles. The evolution aligns with enterprise procurement teams that favor operational expenditure over lump-sum capital purchases.

The services category, growing at 12.18% annually, increasingly includes regulatory advisory, grant-writing assistance, and user-training subscriptions. Software vendors monetize artificial-intelligence modules on a per-seat basis, delivering customizable incident-command features without fresh hardware purchases. As a result, the Push to Talk market size for services is projected to exceed USD 35.7 billion by 2031, indicating a substantial shift in revenue mix away from physical equipment. Deployment complexity, particularly in hybrid LMR-cellular environments, guarantees a multi-year runway for professional services revenue.

By Network Type:

Cellular Transformation AcceleratesLMR retained a commanding foothold with 60.45% Push to Talk market share in 2025, showing that proven reliability still matters to mission-critical users. However, 5G deployments are expanding at a 15.18% CAGR on the back of network slicing and enhanced mobile broadband. Multi-operator core networks, pioneered in the European public safety community, allow first responders to roam across carriers without manual intervention, directly challenging LMR’s historical advantage in coverage continuity.

Private industrial 5G has unlocked new pockets of demand. Automotive assembly lines use sub-20-millisecond latency channels to synchronize autonomous guided vehicles, with real-time voice overlays for maintenance alerts. Hybrid architectures are the norm: agencies keep LMR for fallback while shifting day-to-day traffic to broadband. Over the forecast horizon, the Push to Talk market size for cellular solutions is set to eclipse USD 40.6 billion, driven by cap-and-grow migration strategies.

By Vertical:

Industrial Uptake Gains PacePublic safety dominated revenue with USD 19.8 billion in 2025, reflecting federal mandates for interoperable voice platforms and continuing FirstNet expansion. Police command centers integrate body-worn video feeds and geofencing, which pushes users toward broadband. Fire and emergency medical services rely on biometric tracking to protect personnel in hazardous zones, a feature absent in legacy radios.

The oil and gas and utilities vertical is projected to post the quickest gains, with 13.22% annual growth as operators roll out private 5G in refineries and transmission corridors. Cellular Push to Talk supports direct-transfer-trip schemes that halt equipment instantly if communication links fail, satisfying stringent safety regulations. Transportation and manufacturing segments follow similar logic, merging plant controls with real-time voice. By 2030, industrial users are expected to contribute more than one-third of incremental Push to Talk market revenue.

Geography Analysis

North America Push To Talk Market

North America generated the largest regional revenue in 2024, underpinned by extended FirstNet coverage, federal grant incentives, and a sizable installed base of P25 networks needing upgrades. Canada’s public safety agencies prioritize interoperability across vast territories, while Mexico’s maquiladora factories seek unified communication channels to support lean workflows.

Europe Push To Talk Market

Europe’s modernization programs focus on seamless roaming across borders. Pilot projects in Scandinavia demonstrate cross-carrier MCPTT hand-offs that preserve push-to-talk sessions during high-speed rail travel. Regulatory clarity on 700 MHz narrowband spectrum has accelerated tender activity, though supply-chain constraints occasionally disrupt device deliveries.

APAC Push To Talk Market

Asia Pacific, the fastest-growing region at 11.12%, benefits from large-scale 5G roll-outs and industrial automation drives in China, Japan, and India. Local vendors supply purpose-built terminals at lower price points, encouraging small- and mid-size enterprises to adopt broadband Push to Talk. Australia and New Zealand remain niche markets that emphasize mining safety applications, yet their stringent equipment standards create attractive margins for premium device makers.

MEA Push To Talk Market

The Middle East and Africa trail on absolute revenue yet show momentum in verticals such as energy and smart city public safety. Gulf Cooperation Council members invest in network slicing to support megaproject security, while South Africa leans on broadband PTT to monitor deep-level mine operations. As coverage gaps close, cellular-first deployments may let new entrants bypass legacy LMR entirely, broadening the Push to Talk market addressable base.

Competitive Landscape

Competition centers on who can deliver mission-critical latency and reliability while keeping total cost-of-ownership low. Incumbent LMR suppliers protect their franchises through large patent portfolios and decades-long relationships with government agencies. Telecom infrastructure giants partner with carriers to layer MCPTT directly onto 5G cores, providing nationwide reach without dedicated repeaters. Cloud-native entrants differentiate through AI-powered dispatch analytics and subscription pricing.

Consolidation has intensified: several regional two-way radio distributors merged in 2024 to build scale in managed services, and a handful of software vendors acquired smaller AI start-ups to embed real-time transcription inside mobile apps. Meanwhile, chipset shortages forced device makers to prioritize high-margin rugged handsets, indirectly squeezing budget buyers. The drive toward open APIs has also widened the playing field— integrators can mix and match radios, smartphones, and dispatch consoles from multiple brands without forfeiting support contracts.

Strategic moves underline vertical specialization. One radio vendor partnered with a turbine manufacturer to certify explosion-proof handsets for floating LNG terminals. A telecom operator bundled cloud-hosted MCPTT together with 5G smart-meter connectivity for European utilities, locking in multi-decade contracts. Another supplier launched a device-as-a-service offer that rolls hardware, software, and 24-hour replacement into a single monthly fee. Such tactics underscore a broader migration from hardware margins to recurring revenue inside the Push to Talk market.

Push To Talk Industry Leaders

Qualcomm Technologies, Incorporation

Nokia

Samsung Electronics

Ericsson

Verizon Communications

- *Disclaimer: Major Players sorted in no particular order

Push To Talk Market Companies Covered in this Report

- Motorola Solutions

- AT&T (FirstNet)

- Verizon Communications

- Hytera Communications

- Tait Communications

- Iridium Communications

- Telstra

- Qualcomm Technologies

- Zebra Technologies

- Samsung Electronics

- Airbus Defence and Space

- Cisco Systems

- Nokia

- Ericsson

- L3Harris Technologies

- Sonim Technologies

- Sepura

- ESChat

- RugGear

- Siyata Mobile

Recent Industry Developments in Push To Talk Market

- March 2025: Turkcell and Huawei signed an MoU covering sustainable 5G Advanced networks with tunnel antennas to extend Push to Talk coverage under challenging topographies.

- March 2025: O2 Telefónica Germany chose AWS for 5G core and IMS workloads, supporting MCPTT growth plans.

- February 2025: ETSI scheduled the 9th MCX Plugtests at Texas A&M University to certify multi-vendor Push to Talk interoperability across 4G, 5G, TETRA, and P25

- February 2025: O2 Telefónica began live tests of 5G RedCap for German power utilities, ensuring reliable low-bandwidth connectivity for smart meters.

Push To Talk Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global push-to-talk market as all revenue earned from hardware, software, and allied services that enable half-duplex, press-to-transmit voice on land-mobile-radio or broadband (3G, 4G, 5G) networks, including mission-critical PTT and over-the-top PoC solutions. The scope spans rugged radios, PTT-enabled smartphones, dispatch consoles, and cloud cores used across public safety, government, and industrial settings.

Scope exclusion: Devices offering only full-duplex VoIP or text messaging with no push-button voice trigger are outside coverage.

Segments Covered in This Report

- By Component (Value)

- Hardware

- PTT Radios

- Rugged / Ultra-rugged Smart Devices

- Gateways and Repeaters

- Audio Accessories

- Solutions

- PoC Software (MCPTT, PoC, iPTT)

- Dispatch and Command-Centre Consoles

- Application-Integration Middleware

- Services

- Professional Services

- Managed Services

- Training and Support

- Hardware

- By Network Type (Value)

- Land Mobile Radio (LMR)

- Analog LMR

- Digital LMR (DMR, TETRA, P25, dPMR, NXDN)

- Cellular

- 3G

- 4G / LTE

- 5G

- Land Mobile Radio (LMR)

- By Vertical (Value)

- Public Safety

- Police

- Fire and Rescue

- Emergency Medical Services

- Government and Defense

- Commercial

- Transportation and Logistics

- Manufacturing

- Construction

- Oil and Gas and Utilities

- Hospitality and Retail

- Public Safety

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with carrier product leads, government procurement officers, and system integrators across North America, Europe, Asia-Pacific, and the Gulf. Interviews verified P25-to-LTE churn rates, typical device lifespans, and service fee ranges, closing gaps left by documents and anchoring key assumptions.

Desk Research

We extracted spectrum, subscriber, and traffic series from the International Telecommunication Union, the US FCC, the GSMA, and TCCA, while FirstNet Authority releases clarified public safety migration timelines. Company 10-Ks, investor decks, and shipment filings gave us shipment counts and realistic average selling prices. D&B Hoovers and Dow Jones Factiva supplied component-level revenue for leading vendors. These inputs formed the first demand curve for each country. The sources named are illustrative; many additional databases and open records were reviewed.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins our model. National wireless service revenue is apportioned to PTT using penetration ratios from interviews, then reconciled against sampled hardware shipments multiplied by realized ASPs. Inputs such as active LMR subscribers, 5G coverage above 80 percent, public safety capital budgets, rugged phone ASP drift, and TETRA-to-LTE migration speed feed a multivariate regression that projects values to 2030.

Data Validation & Update Cycle

Outputs pass anomaly checks against customs imports and quarterly carrier disclosures before senior review. Models refresh annually, with interim updates after spectrum awards, large-scale tenders, or major technology launches, and a final validation pass precedes each report release.

How Mordor Intelligence's Push To Talk Market Size Compares to Other Published Estimates

Published estimates often diverge. Differences stem from whether service fees are counted, how quickly LMR users are assumed to switch to broadband, and if refurbished radios are folded into totals. Our disciplined scope, interview-tested variables, and yearly refresh make Mordor Intelligence numbers a dependable baseline.

These contrasts show that our scope-aligned, interview-validated approach delivers a transparent, reproducible baseline that mirrors real procurement flows and avoids hidden inflators.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 43.01 bn (2025) | Mordor Intelligence | - |

| USD 33.18 bn (2023) | Global Consultancy A | Excludes carrier service revenue and slow 5G migration |

| USD 35.30 bn (2023) | Industry Journal B | Includes refurbished radios and list-price ASP uplift |

These contrasts show that our scope-aligned, interview-validated approach delivers a transparent, reproducible baseline that mirrors real procurement flows and avoids hidden inflators.

Key Questions Answered in the Report

What is the projected size of the Push to Talk market in 2031?

The Push to Talk market is expected to reach USD 77.53 billion by 2031 on a CAGR of 10.32%.

Which component segment is growing the fastest?

Services, comprising integration, managed support, and training, are advancing at a 12.18% CAGR through 2031.

Why are public safety agencies moving toward broadband Push to Talk?

They need low-latency voice along with real-time video, location tracking, and analytics that traditional LMR cannot deliver.

How does 5G benefit Push to Talk applications?

5G provides network slicing and sub-20-millisecond latency, matching mission-critical voice standards while adding high-bandwidth data.

What regions show the highest growth potential?

Asia Pacific leads with an 11.12% CAGR because of large-scale 5G deployments and industrial digitalization programs.

Are LMR systems becoming obsolete?

Not immediately; many users run hybrid deployments that leverage existing LMR for fallback and broadband for enhanced data features.

Page last updated on: