In Building Wireless Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.33 Billion |

| Market Size (2031) | USD 46.54 Billion |

| Growth Rate (2026 - 2031) | 12.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In Building Wireless Market Analysis by Mordor Intelligence

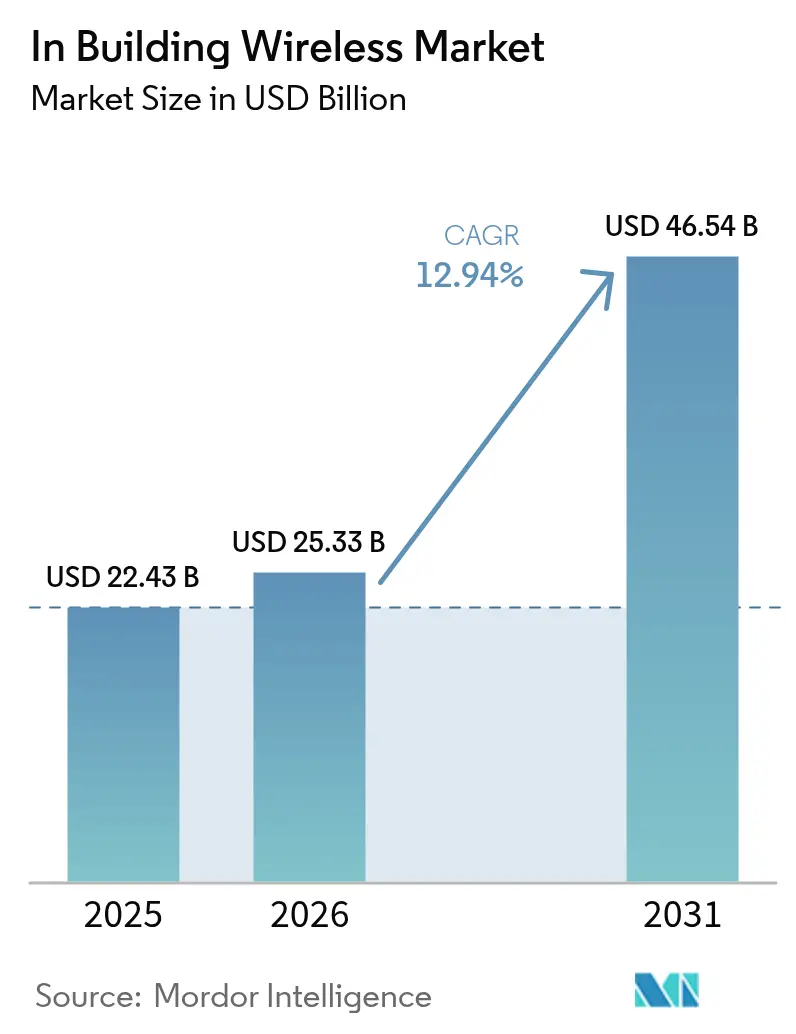

The In Building Wireless market size is expected to grow from USD 22.43 billion in 2025 to USD 25.33 billion in 2026 and is forecast to reach USD 46.54 billion by 2031 at 12.94% CAGR over 2026-2031.

Sustained demand for always-available indoor connectivity, the transition to 5G-ready buildings, and rising smart-facility mandates are driving this momentum. Enterprises now treat indoor coverage as core infrastructure, investing in cellular-first architectures that pair private 5G with next-generation Wi-Fi to guarantee application uptime. Supply-chain inflation has nudged deployment costs higher, yet cost pressures are partially offset by neutral-host designs and AI-based optimisation that lower life-cycle expenses. Vendor consolidation is reshaping the In-Building Wireless market as equipment makers pursue end-to-end solution portfolios capable of spanning radio, transport, and cloud management layers.

Key Report Takeaways

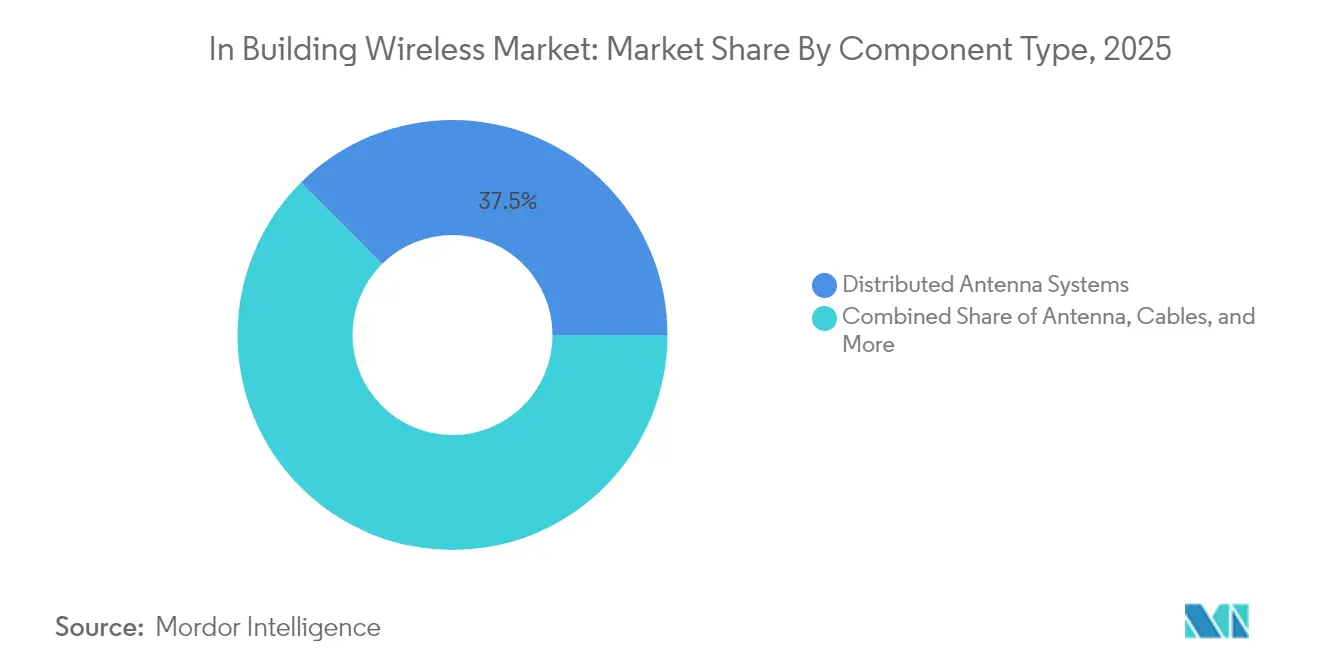

- By component type, Distributed Antenna Systems led with 37.45% revenue share in 2025, while Private-5G small cells are projected to expand at a 13.52% CAGR to 2031.

- By technology, 4G/LTE held 64.20% of the In-Building Wireless market share in 2025, and 5G NR is the fastest-growing segment at a 14.10% CAGR through 2031.

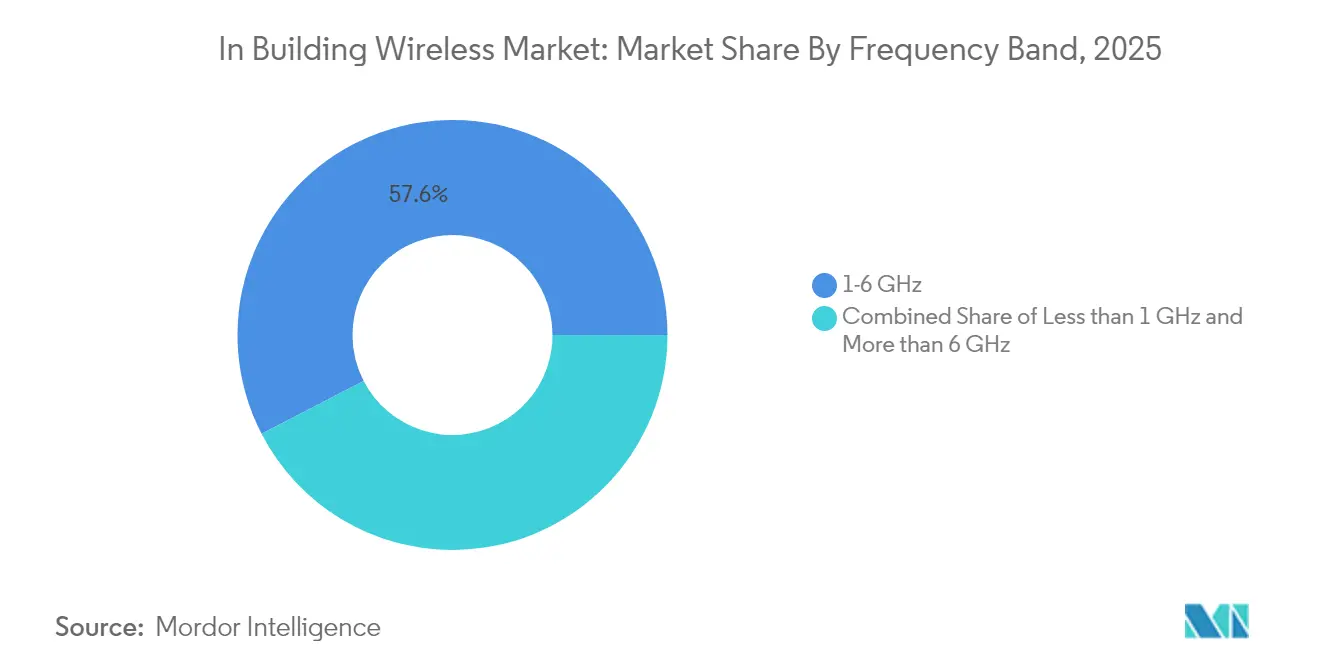

- By frequency band, mid-band spectrum accounted for 57.60% share of the In-Building Wireless market size in 2025; mmWave is advancing at a 14.18% CAGR through 2031.

- By end-user industry, commercial facilities captured 44.55% revenue share in 2025, whereas industrial deployments are forecast to grow at a 13.05% CAGR through 2031.

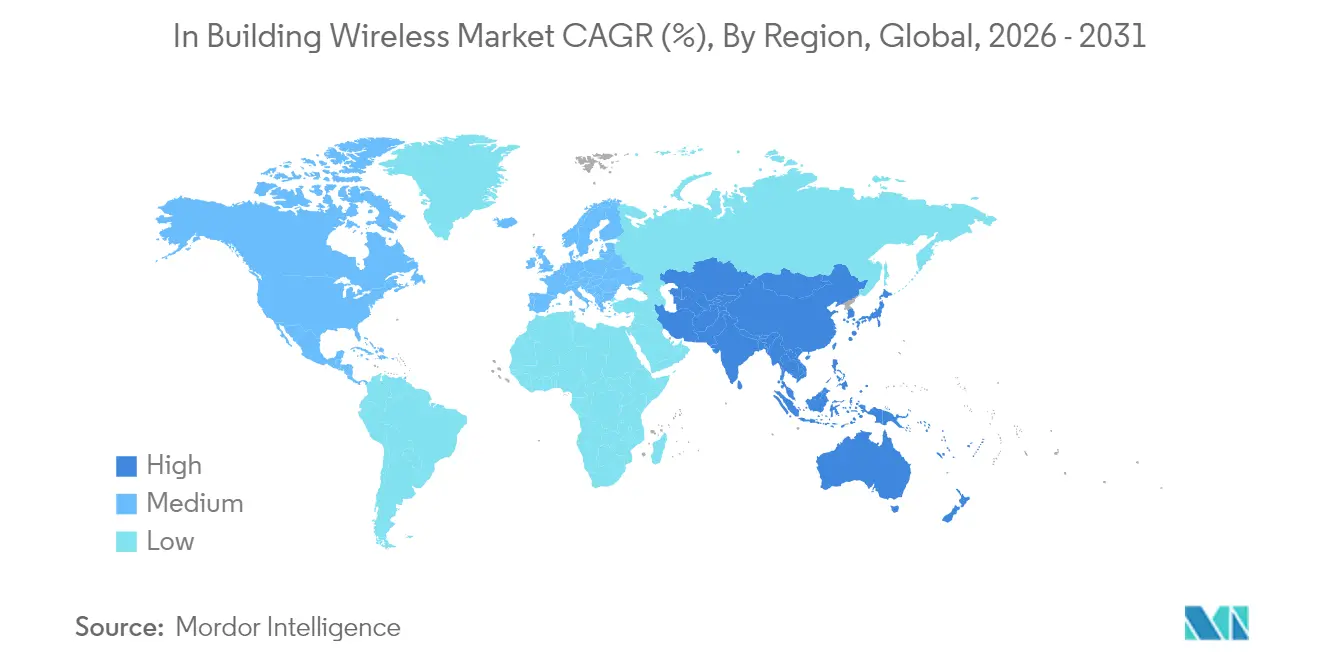

- By geography, North America commanded a 33.60% share in 2025; Asia-Pacific is the fastest-growing region at a 14.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of In Building Wireless Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mobile-data consumption indoors | 2.80% | Global; highest in North America & Asia-Pacific | Medium term (2–4 years) |

| 5G spectrum allocations for indoor use | 2.10% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Demand for uninterrupted enterprise connectivity | 1.90% | Global; concentrated in developed markets | Short term (≤2 years) |

| Smart-building mandates for gigabit-grade Wi-Fi | 1.40% | North America & EU; expanding to APAC urban centres | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising mobile-data consumption indoors

Roughly 80% of all mobile traffic now originates inside buildings, overwhelming legacy Wi-Fi whenever video, AR training, or high-density IoT workloads spike. Retail chains such as Tractor Supply adopted 5G across more than 2,000 outlets after Wi-Fi could not support real-time inventory and customer-engagement applications. In healthcare, a single children’s hospital installed 900 tri-radio APs to safeguard tele-medicine and imaging traffic without patient disruption, underscoring the capacity gap that indoor 5G plus Wi-Fi 6E is filling. Growing video collaboration and edge analytics workloads will intensify the demand curve, reinforcing the revenue outlook for the In-Building Wireless market.

5G spectrum allocations for indoor use

Regulators are carving out dedicated indoor spectrum, shifting enterprise design from outdoor-to-indoor overlay to private cellular from day one. In the United States, the CBRS auction channelled USD 4.6 billion into 3.5 GHz licences aimed at enterprise and venue deployments, with one Tier-1 carrier alone spending USD 1.89 billion[1]Federal Communications Commission, “CBRS Auction Results,” fcc.gov. Europe authorised 480-500 MHz in the 6 GHz band, enabling 320 MHz-wide channels critical for stadiums, airports, and universities. China Mobile earmarked USD 416 million for 5G-Advanced rollouts across 300 cities to accelerate factory automation at scale. Such allocations ensure long-term spectrum certainty, lifting confidence and capex commitment across the In-Building Wireless market.

Demand for uninterrupted enterprise connectivity

Digital-first operations demand carrier-grade resilience. Automotive plants replaced Wi-Fi with private 5G to guarantee connectivity for automated guided vehicles and real-time quality control, as shown by Toyota Material Handling’s engagement with Ericsson. Semiconductor fabs validate every wireless node against strict uptime and latency tolerances to protect high-value processes. Hospitals upgrading to WPA3-certified access points illustrate how mission-critical networks must also satisfy evolving security baselines. Service-level agreements now reference 99.9% uptime for wireless segments, making redundancy and automated failover central to new indoor architectures.

Smart-building mandates for gigabit Wi-Fi

Sustainability and occupancy-efficiency schemes push property owners to embed multi-gigabit wireless that supports energy dashboards, smart HVAC, and AI-driven space utilisation. A full-service resort in California rebuilt its campus network around a 1 Gb minimum throughput target to serve guests and IoT workloads seamlessly. Wi-Fi 7 access points from Cisco feature 320 MHz channels and multi-link operation that together exceed 40 Gbps theoretical speeds, laying the foundation for immersive services. Certification frameworks such as LEED now factor connectivity, forcing developers to specify robust In-Building Wireless solutions during the design phase.

Restraints Impact Analysis of In Building Wireless Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns | -1.80% | EU, North America, APAC | Short term (≤2 years) |

| High capex of multi-operator DAS deployments | -2.30% | Global; most acute in emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and cybersecurity concerns

Enterprises remain cautious about exposing operational traffic to broader cellular ecosystems. GDPR compliance elevates scrutiny of location-tracking functions in Europe, prolonging procurement cycles for smart-office projects. Healthcare providers mandate Protected Management Frames and advanced encryption before approving new radios because patient data moves over the same air interface. The US “rip-and-replace” rules for insecure equipment add unexpected swap-out costs but ultimately harden the security posture of the In-Building Wireless market.

High capex of multi-operator DAS deployments

Traditional neutral-host systems can cost USD 18.25 per underground foot of fibre, and labour still equals 60-80% of the bill of materials. Economic returns are therefore thin outside marquee venues, causing some tower operators to cancel thousands of nodes. Semiconductor shortages extend lead times for mmWave and Wi-Fi 7 chipsets, deferring revenue recognition for integrators. Enterprises counter these economics by adopting small-cell and private-network models that shift spend from shared DAS to targeted cellular footprints capable of supporting multiple tenants on a single RAN instance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

In Building Wireless Market Segment Analysis

By Component Type:

DAS dominance faces Private-5G disruptionDistributed Antenna Systems held 37.45% of 2025 revenue, anchoring the In-Building Wireless market through deep penetration in stadiums, airports, and Class-A offices. Private-5G small cells, however, are advancing at a 13.52% CAGR, signaling a pivot toward agile cellular networks that enterprises can own and manage. Rising fibre and coax prices push integrators to favour active DAS or small-cell architectures that minimise cabling runs and facilitate remote software upgrades.

Antenna innovation now prioritises multi-band, multi-operator designs that collapse Wi-Fi and cellular coverage into one form factor, trimming roof-space requirements. Repeater use is declining as small-cell clusters deliver stronger uplinks without RF noise penalties. Vendor consolidation, illustrated by Amphenol’s USD 2.1 billion acquisition of CommScope’s mobility assets, bundles cabling, connectors, and radio components to streamline procurement. As neutral-host demand grows, single backbone infrastructures capable of carrying public and private slices simultaneously will reshape capital-allocation patterns across the In-Building Wireless market.

By Technology:

5G NR acceleration challenges 4G/LTE incumbency4G/LTE retained 64.20% share in 2025, underpinned by a mature device ecosystem and proven stability for voice and data. Yet 5G NR is expanding at a 14.10% CAGR, driven by industrial automation projects that need deterministic latency below 10 ms. Wi-Fi 6E is also scaling, but Wi-Fi 7 introduces 320 MHz channels, multi-link operation, and 4K-QAM, giving enterprises a non-cellular path to ultra-high throughput.

Hybrid deployments blending 5G and Wi-Fi 7 are emerging as the reference architecture in hospitals, smart factories, and higher-education campuses. Manufacturing plants use 5G for mobile robotics and safety-critical telemetry, while Wi-Fi handles bulk data offload for tablets and laptops. China’s 5G-Advanced roll-out validates the technology’s readiness for indoor broadband, fuelling component demand from active DAS and small-cell vendors. With each additional private licence granted, the In-Building Wireless market deepens its shift from operator-led to enterprise-controlled networks.

By Frequency Band:

Mid-band dominance amid mmWave emergenceMid-band spectrum between 1 GHz and 6 GHz supplied 57.60% of 2025 revenue, balancing penetration and capacity for multi-floor buildings. The CBRS band stands out, converting shared spectrum rules into fast-tracked private-network pilots at Fortune 500 campuses. In contrast, mmWave is growing 14.18% annually as airports, arenas, and convention centres embrace 24 GHz+ channels to support 8K video streaming and XR experiences in dense crowds.

Regulators in Europe released 6 GHz for Wi-Fi, enabling 320 MHz channels that greatly boost per-user throughput. Japan combines Sub-6 for blanket coverage with mmWave overlays to lift uplink capacity for machine-vision cameras on production lines. Power-level debates within the FCC could raise indoor CBRS output, further blurring lines between mid-band and low-power macro coverage. These moves collectively sustain frequency diversity, ensuring the In-Building Wireless market can match performance tiers to each application.

By End-User Industry:

Commercial leadership amid industrial accelerationCommercial properties delivered 44.55% of 2025 sales, demonstrating enduring demand for seamless guest and staff connectivity across offices, retail chains, healthcare campuses, and hospitality venues. Office landlords refit networks to accommodate hybrid work, while stores weave analytics, loyalty apps, and frictionless checkout into their wireless footprint. Hospitals replace ageing access points with WPA3-ready gear to maintain accreditation for electronic health records. Resorts invest in estate-wide Wi-Fi 7 to elevate guest satisfaction metrics and support IoT-enabled energy management.

Industrial projects are the fastest-growing opportunity at 13.05% CAGR. Automotive OEMs such as BMW and Tesla leverage private 5G to synchronise robotics and automate in-line quality inspection. Oil and gas operators deploy cellular links for remote-area asset monitoring, avoiding fibre trenching costs. Warehouses rely on low-latency wireless to orchestrate autonomous forklifts and real-time inventory systems, while government agencies adopt FirstNet Band 14 coverage to underpin next-generation public-safety workflows. Industrial appetite for secure, deterministic networks will keep capital flowing toward the In-Building Wireless market.

Geography Analysis

North America In Building Wireless Market

North America led the In-Building Wireless market with 33.60% revenue share in 2025, aided by CBRS spectrum liberalisation and FirstNet’s USD 8 billion public-safety investment that funded 1,000 new cell sites. Enterprises in the United States adopt neutral-host architectures to consolidate carrier relationships and future-proof private-network ambitions. Wi-Fi 7 launches from multiple vendors accelerate refresh cycles, while Canada and Mexico leverage their automotive and aerospace clusters to justify private cellular rollouts inside plants.

APAC In Building Wireless Market

Asia-Pacific is expanding at a 14.12% CAGR to 2031. China already hosts 4.4 million 5G base stations and plans to exceed 4.5 million within the forecast horizon as it digitalises manufacturing and logistics. Japan’s licence regime supports sub-6 and mmWave hybrids in smart factories, and South Korea channels state incentives into campus networks at semiconductor fabs. India’s electronic-manufacturing drive is supported by antenna localisation partnerships that trim import costs and shorten deployment lead times.

Europe In Building Wireless Market

Europe shows steady uptake influenced by regulatory stringency around data privacy and building emissions. The 6 GHz allocation enlarges Wi-Fi capacity for dense venues, and French cities demonstrate the cost advantage of private 5G for municipal camera backhaul. German, British, and French enterprises lead adoption, while Central-Eastern manufacturers pilot private 5G to support Industry 4.0. Strict GDPR compliance requirements nudge buyers toward on-premises core networks and secure device-identity frameworks, shaping a security-first approach within the In-Building Wireless market.

Regulatory Landscape

In-building wireless deployments are shaped by spectrum governance and indoor infrastructure approval processes that affect private cellular, neutral-host DAS, and next-generation Wi-Fi. From 1 January 2025, the 2024 edition of the ITU Radio Regulations entered into force, setting a global baseline for radio-frequency use and coordination that underpins national indoor allocations across low-, mid-, and high-band spectrum.

In major markets, policymakers are also targeting permitting and authorization friction that can delay indoor and campus buildouts. In December 2025, the US FCC issued an NPRM under the Build America Agenda aimed at removing barriers to wireless deployments, while the European Commission in 2026 proposed the Digital Networks Act to consolidate connectivity legislation and simplify authorization and access rules. At the multilateral level, regulators at the ITU Global Symposium for Regulators in May 2026 endorsed Best Practice Guidelines on regulatory governance for resilience and emerging technologies, and ITU-R work on IMT-2030 (6G) technical evaluation requirements advanced in March 2026, indicating a longer-term standardization track that is already influencing indoor equipment roadmaps.

Value Chain Analysis

The in-building wireless value chain starts with silicon and RF components (baseband/RF SoCs, ASICs, power modules, timing, and memory), then moves into radio and Wi-Fi access equipment (small cells, active/passive DAS headends and remotes, Wi-Fi 6E/7 APs), antennas, and structured cabling (fiber/coax). Optical transport and edge/core software (private 5G core, cloud management, analytics/assurance, security) sit upstream of system integration, venue construction, and commissioning. Delivery then occurs through OEM direct sales and channel partners, and through neutral-host providers, telecom operators, and specialist integrators that handle design, RF engineering, installation, and managed services.

Supply-side constraints and sourcing strategy can materially affect project timing and BOM cost. Industry procurement has shifted toward just-in-case models, with electronic-parts inventory buffers falling below 8 weeks in Q4 2025 versus 31 weeks in Q4 2024. Late-2025 bottlenecks highlighted long lead times for DRAM (exceeding 40 weeks) and custom ASICs, while early-2026 reporting indicated some radio-unit component lead times slipping from 14 to 32 weeks. Geopolitical and tariff exposure, along with difficulty relocating specialized component manufacturing away from China for certain inductors and semiconductors, continues to push OEMs and integrators toward vendor diversification, longer-term allocations, and modular architectures that reduce dependence on a single radio supply chain where feasible.

Competitive Landscape

The In-Building Wireless market is moderately fragmented but trending toward consolidation. Amphenol absorbed CommScope’s mobility portfolio for USD 2.1 billion, combining cabling, connectors, and active equipment under one roof. Nokia secured EU clearance to acquire Infinera for USD 2.3 billion, vaulting it to the number two slot in optical networking and bolstering its end-to-end 5G proposition. These moves illustrate a push for vertical integration that captures radio through optical transport to cloud-managed orchestration.

Strategic alliances complement M&A. Nokia joined forces with Cisco, HPE, and Microsoft to embed cloud RAN inside enterprise data centres, delivering turnkey private 5G plus Wi-Fi 7 bundles that suit campuses lacking telco expertise. Extreme Networks leveraged AI-driven cloud software to deliver double-digit revenue growth for six straight years, earning Gartner leadership accolades that differentiate its subscription model. Patent filings in antenna design surge as players race to perfect multi-link and extended-reality support, with Meta, Samsung, and Qualcomm among the most active applicants.

Price pressure persists because fibre, power, and skilled labour inflate installation budgets; however, software-defined architectures allow vendors to pivot toward recurring revenue. Neutral-host providers experiment with marketplace pricing where building owners sell wholesale capacity to carriers and private tenants. Edge compute integration opens new revenue streams, letting integrators bundle analytics, computer vision, and localised AI into their radio footprint. In the next five years, competitive intensity will hinge on the ability to couple radio hardware with cloud-native control to meet the evolving expectations of the In-Building Wireless market.

In Building Wireless Industry Leaders

CommScope Holding Co.

Cisco Systems Inc.

Corning Inc.

Ericsson AB

Pierson Wireless Corp.

- *Disclaimer: Major Players sorted in no particular order

In Building Wireless Market Companies Covered in this Report

- CommScope Holding Co.

- Cisco Systems Inc.

- Corning Inc.

- Ericsson AB

- Nokia Corp.

- ATandT Inc.

- Verizon Communications Inc.

- Pierson Wireless Corp.

- Cobham PLC

- Cambium Networks

- TE Connectivity Ltd.

- Dali Wireless Inc.

- Airspan Networks

- American Tower Corp.

- Boingo Wireless Inc.

- Extreme Networks Inc.

- Juniper Networks Inc.

- HPE (Aruba Networks)

- Samsung Electronics (Co. Networks)

- Huawei Technologies Co. Ltd.

Market Opportunities and Future Outlook

Neutral-host and shared-spectrum architectures create whitespace in mid-sized commercial sites and multi-tenant venues where traditional multi-operator DAS economics can be restrictive. In the United States, CBRS continues to function as an enterprise and venue enabler, and the ecosystem is expanding beyond small cells into active DAS: Federated Wireless launched CBRS active DAS support in January 2026 to add indoor 5G capacity using shared spectrum, while InfiniG partnered with Nokia in April 2026 to integrate Nokia AirScale radios into a cloud-managed neutral-host service aimed at carrier-grade indoor coverage. Together, these moves support deployment models where property owners and venue operators procure indoor coverage as a building service and onboard carriers as tenants.

Platform upgrades in active DAS and Wi-Fi 7 also create opportunities tied to building modernization, sustainability targets, and operational automation. SOLiD introduced the nGENESIS active DAS platform in May 2026, positioning digital connectivity across 4G and 5G bands alongside an energy-efficient architecture that aligns with smart-building mandates and life-cycle cost focus in large facilities. On the financing and delivery side, Andorix secured a USD 10 million strategic equity investment in May 2026 to scale converged smart-building and in-building connectivity projects, reflecting a pickup in activity around bundled design, deployment, and managed operations for indoor networks where fiber availability, route-miles, and construction logistics are primary gating factors.

Recent Industry Developments in In Building Wireless Market

- February 2026: Cisco disclosed continued infrastructure upgrades at Capital One Arena as part of an USD 800 million venue transformation, including Wi-Fi 7 alongside Cisco Spaces and ThousandEyes. The program shows how large venues are pairing high-capacity indoor access with experience analytics and performance assurance, increasing the software and services content of in-building wireless projects.

- November 2025: CommScope RUCKUS introduced an MDU-focused suite that combines AI capabilities with Wi-Fi 7 to help multi-dwelling unit stakeholders manage resident connectivity and operating costs. The launch brings Wi-Fi 7 further into residential and multi-tenant buildings, extending refresh cycles from access points into cloud management and automation features.

- May 2024: Tesla activated a private 5G network at its Berlin Gigafactory to support automated manufacturing workflows. The deployment reinforces private cellular as a production-network option for mission-critical indoor environments where deterministic performance and control drive the business case.

In Building Wireless Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the in-building wireless market is treated as the revenue generated from indoor connectivity infrastructure installed to improve wireless coverage and capacity inside buildings and large venues, across cellular use cases (including in-building DAS and small cells) and enterprise Wi-Fi use cases.

Scope exclusions: We exclude temporary event-only rentals and outdoor small-cell street furniture that is not primarily deployed for indoor coverage.

Segments Covered in This Report

- By Component Type

- Antenna

- Distributed Antenna Systems (Active DAS, Passive DAS)

- Cables (Coax, Fiber)

- Repeaters

- Small Cells (Femtocell, Picocell, Microcell)

- By Technology

- 4G/LTE

- 5G NR

- Wi-Fi 6/6E

- Wi-Fi 7

- By Frequency Band

- Less than 1 GHz (Low-band)

- 1 - 6 GHz (Mid-band incl. CBRS)

- More than 6 GHz (mmWave)

- By End-user Industry

- Commercial

- Offices

- Retail

- Healthcare

- Hospitality

- Residential

- MDU

- Single-family

- Industrial

- Manufacturing

- Warehousing

- Oil and Gas

- Public-Safety and Government

- Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by collecting the market building blocks that explain demand for indoor coverage and the ability to supply it. We mainly use public references such as spectrum and wireless policy releases from regulators (for example, the FCC and similar bodies), telecommunications statistics from the ITU, and technical guidance documents from 3GPP and the Wi-Fi Alliance. For context on where indoor systems are being deployed, we also review materials such as CTIA resources, OECD digital and infrastructure indicators, and peer-reviewed articles covering indoor propagation and enterprise network planning.

Alongside these sources, we review company filings, investor presentations, and reputable trade press to understand pricing direction, typical deployment patterns, and the channel structure for in-building projects. Where it helps, paid subscriptions are used for company financials and news, patent scanning, and shipment-level import and export signals tied to key indoor-radio components. The desk research sources listed here are illustrative, and we also used additional public and paid sources for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to verify what the desk data cannot reliably show, specifically how indoor systems are specified, priced, and refreshed across venue types. We speak with a mix of network operators, neutral-host style integrators, OEM channel partners, and enterprise IT and facilities stakeholders across APAC, EMEA, and the Americas. We then align responses to common units such as number of nodes, coverage targets, and typical service attachment. When differences show up by building type or technology, we run follow-up discussions so assumptions can be tightened before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 18% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where telecom and enterprise connectivity spending signals are reconstructed into an indoor coverage demand pool, then filtered using adoption rates for DAS, small cells, repeaters, and in-building Wi-Fi upgrades by venue intensity. To keep this grounded, we corroborate the totals with selective bottom-up approximations, including sampled bill-of-material checks, typical node counts per building category, and installed base expansion patterns described by interviewees.

Key model inputs include (as examples) the share of 5G and private LTE/5G indoor deployments, public safety coverage requirements for larger venues, enterprise Wi-Fi refresh cycles, average nodes per 10,000 square feet for different building types, and the mix shift between DAS and small cells as traffic grows. ASP logic is handled by separating hardware value from design, integration, and managed services, then applying realistic price progression ranges based on recent quotes, component cost trends, and contract structures. For forecasting, we rely on scenario analysis supported by expert consensus. Each scenario tests different timelines for 5G densification, enterprise modernization, and venue investment pace, and gaps in partial bottom-up data are bridged using conservative penetration assumptions that are rechecked during validation.

Data Validation & Update Cycle

Outputs are checked through multiple passes so obvious overcounts and undercounts are reduced early. We compare model totals against independent signals such as operator capex direction, indoor-node shipment momentum, and venue rollout announcements, and then investigate variances that exceed expected ranges for a given region or technology. When a number looks off, assumptions are revisited, and respondents can be re-contacted to confirm whether the issue is pricing, service attachment, or a scope boundary.

Before sign-off, another analyst reviews the chain of assumptions and the arithmetic so the steps are repeatable. Reports are refreshed annually, and interim updates are made when material events occur, such as major spectrum changes or sudden pricing shifts. Right before delivery, the model is rechecked so the published view reflects the latest available data.

Mordor Intelligence's In Building Wireless Market Estimate Compared With Other Published Estimates

Published market sizes for in-building wireless often do not align because the underlying counting rules vary, even when the market name sounds the same. Differences usually come from what is treated as in-scope, how service revenue is handled, and whether pricing is updated to match current contract reality.

A refresh-led gap shows up most when exchange rates and ASPs are not updated at the same time, or when older price points are carried forward even though the mix is shifting from legacy DAS to newer small-cell and private network builds. By refreshing currency timing and separating hardware-only ASPs from implementation and managed services during each annual update, Mordor Intelligence reduces drift that can build up when older assumptions are reused for fast-moving indoor deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.33 B (2026) | |

| Global Consultancy A | USD 21.05 B (2024) | Uses an earlier base year and can understate newer 5G and private network deployment value if the indoor node mix shift and attached services are not fully reflected in ASP updates. |

| Industry Research Group B | USD 12.70 B (2024) | Often applies a tighter definition focused on core equipment, which can exclude parts of integration, optimization, and managed services that are frequently bundled into indoor coverage projects. |

The spread in the table is mostly explained by timing and scope choices rather than arithmetic. When currency timing, service attachment, and technology mix are refreshed together, the resulting market size stays traceable to practical deployment drivers and can be reproduced with clear steps.

Key Questions Answered in the Report

What is the current size of the In-Building Wireless market?

The In-Building Wireless market size stands at USD 25.33 billion in 2026.

How fast will the In-Building Wireless market grow through 2031?

Revenue is forecast to reach USD 46.54 billion by 2031, reflecting a 12.94% CAGR during 2026-2031.

Which component is growing the quickest inside buildings?

Private-5G small cells are advancing the fastest at a 13.52% CAGR as enterprises seek dedicated cellular capacity.

Why is Asia-Pacific considered the most dynamic region?

Massive 5G investments, including China’s 4.4 million base-station footprint, drive a 14.12% regional CAGR and rapid industrial adoption.

How are enterprises justifying the cost of new indoor networks?

AI-managed neutral-host architectures and private-network models cut operating expenses and unlock monetisation of shared infrastructure.

What security steps are critical for healthcare or GDPR-sensitive deployments?

Deployments typically specify WPA3 encryption, Protected Management Frames, and on-premise cores to preserve data sovereignty while assuring 99.9% uptime.

Page last updated on: