Contact Center Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

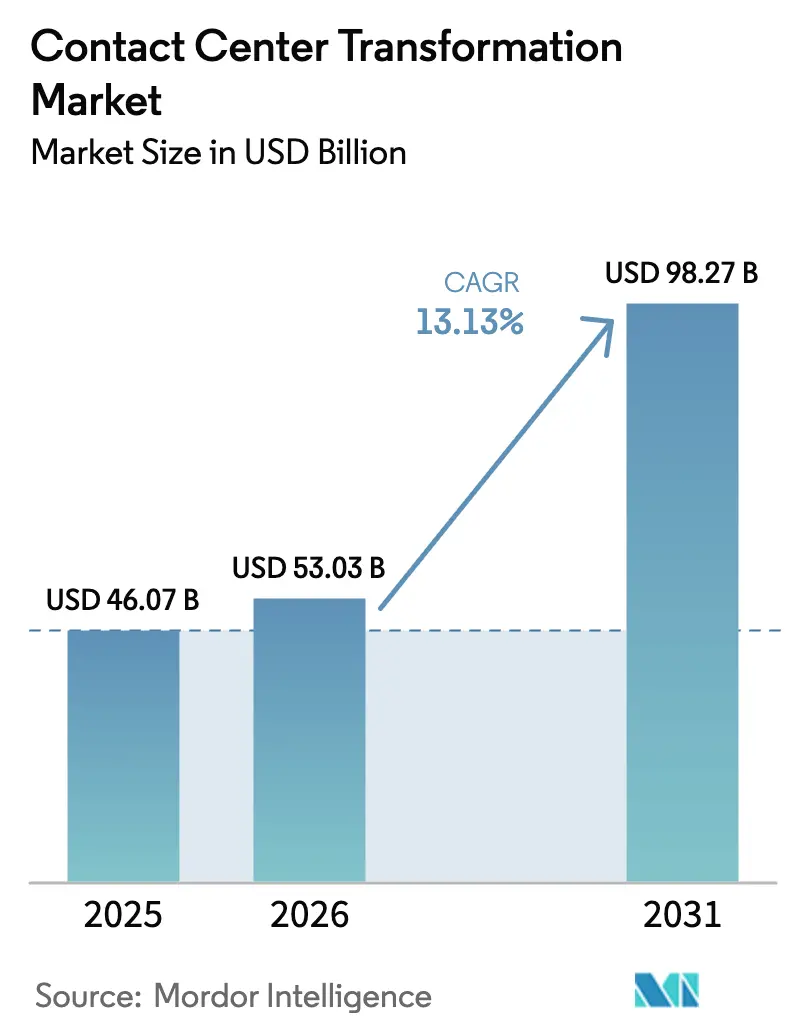

| Market Size (2026) | USD 53.03 Billion |

| Market Size (2031) | USD 98.27 Billion |

| Growth Rate (2026 - 2031) | 13.13% CAGR |

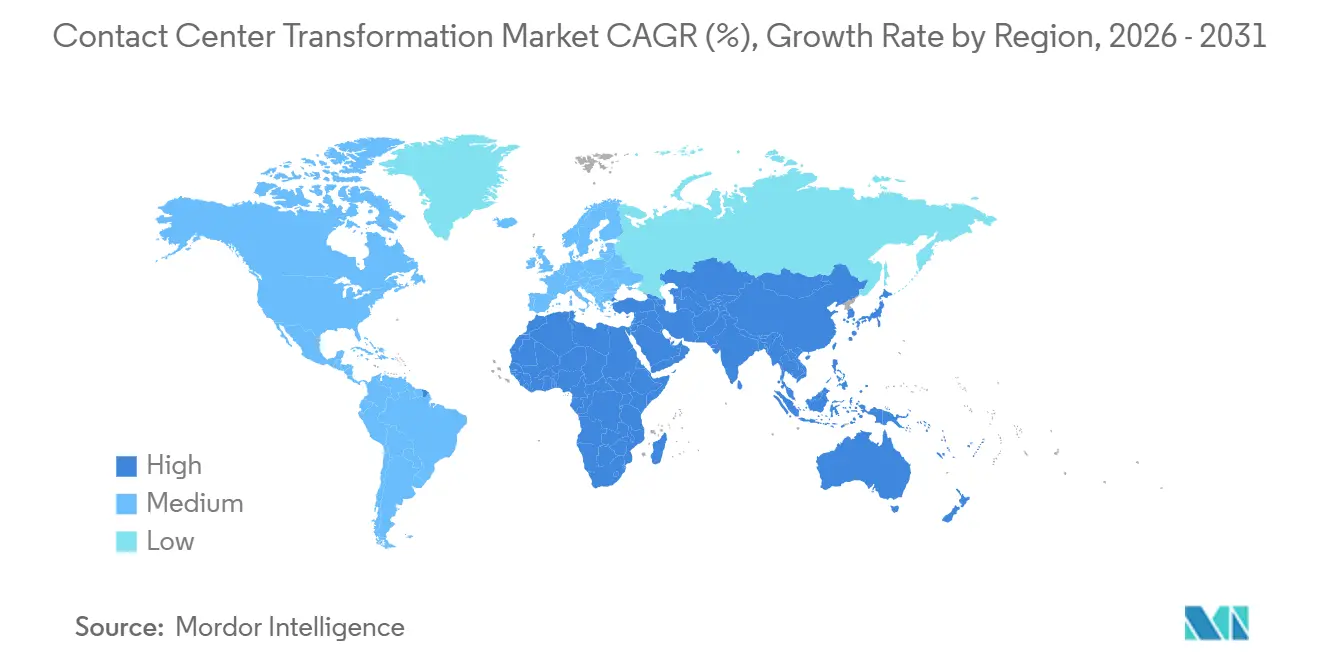

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Contact Center Transformation Market Analysis by Mordor Intelligence

The Contact Center Transformation Market size is expected to grow from USD 46.07 billion in 2025 to USD 53.03 billion in 2026 and is forecast to reach USD 98.27 billion by 2031 at 13.13% CAGR over 2026-2031.

Real-time analytics, artificial intelligence, and omnichannel orchestration are replacing legacy private branch exchange systems, enabling faster issue resolution and richer customer insights. Demand intensifies as subscription-based cloud deployments convert fixed costs to operating expenses, while automation trims labour, which still represents 60% to 70% of operating outlays. Financial-services providers are early adopters because fraud detection, voice biometrics, and audit-grade recording are now table stakes, and telehealth growth positions healthcare as the next large wave of adopters. Competitive pressure is increasing as hyperscale cloud providers bundle compute, storage, and machine learning with contact center software, offering aggressive unit pricing and rapid feature velocity. Regionally, privacy regulations and data-localization rules are shaping vendor roadmaps, forcing multi-tenant platforms to deliver country-specific instances without compromising latency or uptime.

Key Report Takeaways

- By end-user industry, banking, financial services, and insurance held 27.59% of the contact center transformation market share in 2025, whereas healthcare is expanding at a 13.96% CAGR through 2031.

- By deployment, on-premises architectures commanded 61.58% of the contact center transformation market size in 2025, yet hosted solutions are advancing at 13.68% CAGR.

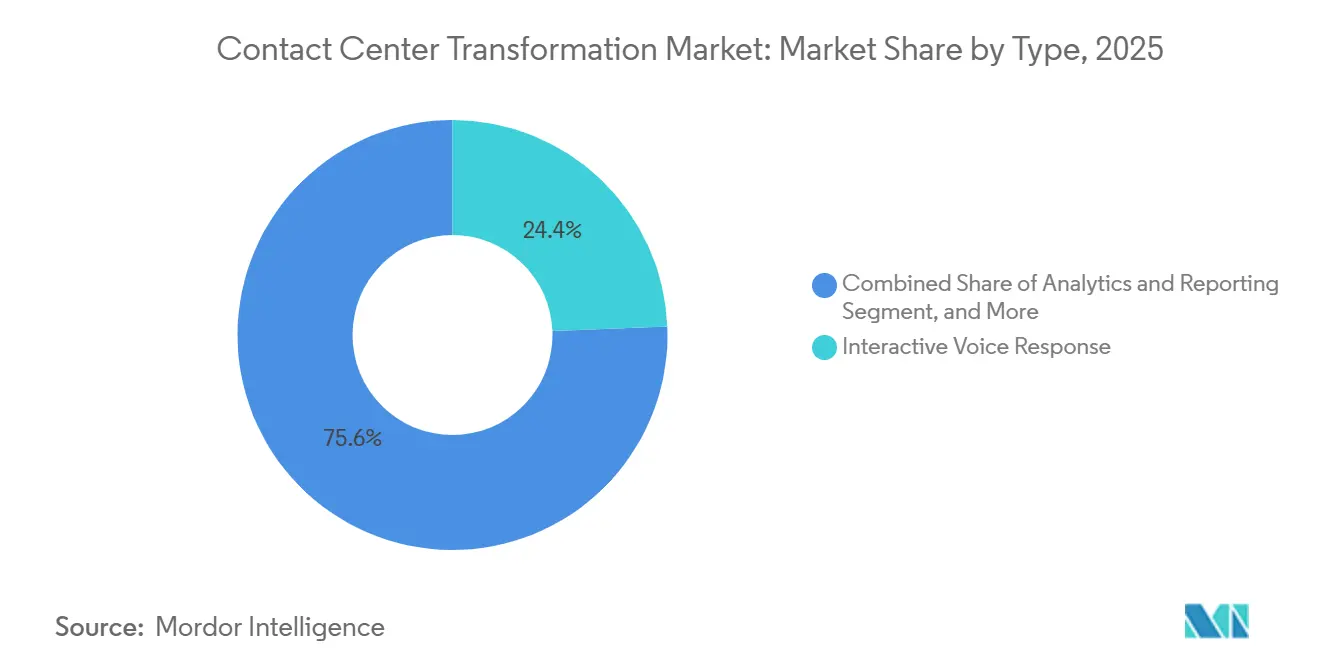

- By type, interactive voice response held 24.37% share in 2025, while analytics and reporting platforms are pacing the field at a 14.83% CAGR through 2031.

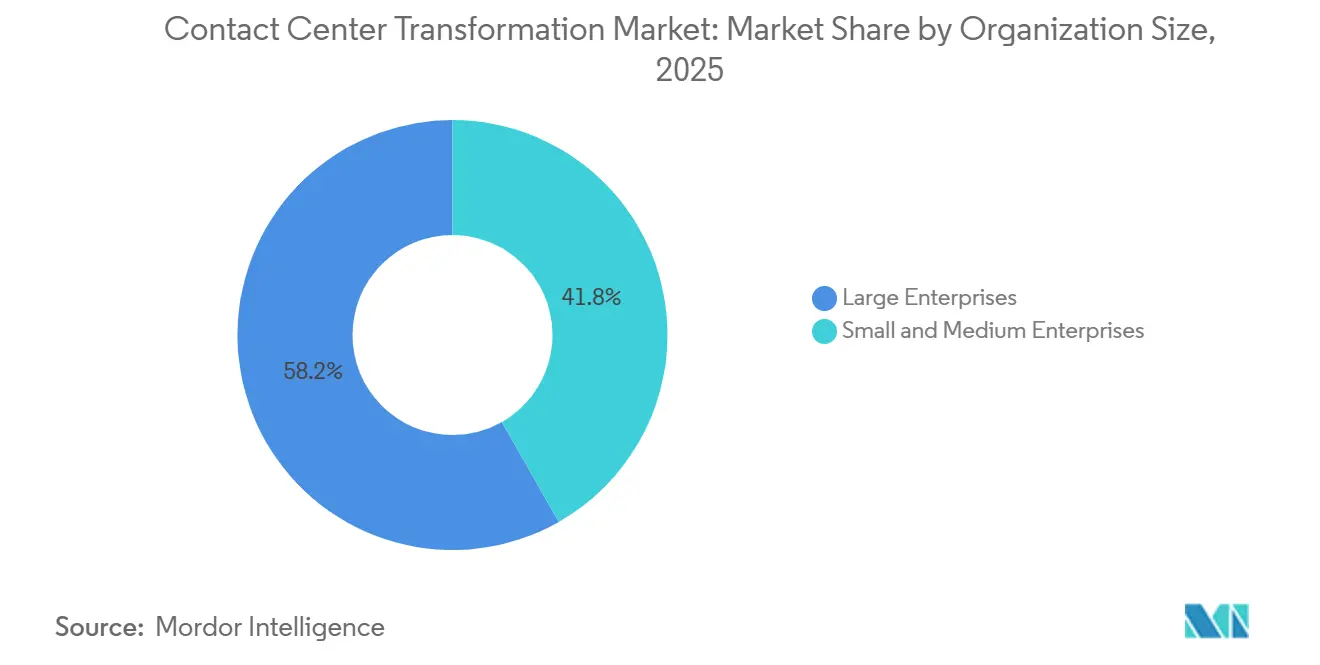

- By organization size, large enterprises led with 58.23% of global revenue in 2025, but small and medium enterprises are scaling at a 14.12% CAGR because subscription pricing cuts total cost of ownership 30% to 40%.

- By geography, North America captured 36.49% revenue in 2025, but Asia Pacific records the fastest regional CAGR at 14.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contact Center Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Omnichannel Customer Engagement | +2.10% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Shift Toward Subscription-Based Cloud Contact Centers | +2.40% | Global, led by North America and Asia Pacific | Short term (≤ 2 years) |

| Cost Reduction Imperative Through Automation | +2.80% | Global, particularly strong in Asia Pacific and Latin America | Short term (≤ 2 years) |

| Compliance Pressures In Regulated Industries | +1.60% | North America, Europe, with emerging impact in Asia Pacific | Long term (≥ 4 years) |

| Growing Use Of Real-Time Speech Analytics | +1.40% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Customer-Owned Data Lake Integration Needs | +1.20% | North America and Europe, early adoption in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Omnichannel Customer Engagement

Customers shift fluidly between voice, email, chat, social media, and messaging, and they expect context to travel with them. Three-quarters of service journeys now involve more than one touchpoint, yet fewer than one-third of enterprises maintain unified profiles, which elevates churn and repeat contact rates. Retailers, e-commerce platforms, and subscription media brands therefore invest in channel-agnostic routing engines that map sentiment, customer value, and agent skill in real time to cut average handle time by one-fifth. Cloud platforms embed unified desktops, so agents immediately see prior conversation threads, improving first-contact resolution and net promoter scores. The impact is most pronounced in consumer-facing industries where brand perception hinges on friction-free interactions.[1]“Amazon Web Services Annual Report 2025,” Amazon Web Services, aws.amazon.com

Shift Toward Subscription-Based Cloud Contact Centers

Chief financial officers favour operating-expense models that remove hardware refresh cycles and shrink deployment from months to weeks. Large-scale migrations show total cost of ownership reductions north of one-third over five-year horizons because upkeep, patching, and capacity planning shift to the vendor. Annual recurring revenue for leading providers is rising more than 40% on new cloud subscriptions, underscoring demand elasticity when upfront capital barriers fall. Hosted licenses also let enterprises launch greenfield operations in emerging markets by spinning up agent seats in hours instead of procuring rack space. Adoption is particularly swift among Asian small and medium enterprises that lack the resources for on-premises builds yet still need enterprise-grade uptime and compliance.

Cost Reduction Imperative Through Automation

Voice and chatbots now close roughly 70% of tier-one tickets, freeing human agents for complex problem-solving. Large enterprises report labour savings of up to one-quarter, with payback periods under 18 months when virtual assistants, predictive dialers, and robotic process automation handle repetitive tasks. Workforce management algorithms forecast interaction peaks and adjust staffing, trimming idle time 15% to 20%. Automating after-call documentation alone recovers thousands of productive hours annually in business-process-outsourcing hubs facing double-digit wage inflation. The capex-to-labour substitution effect is strongest in India, the Philippines, and Latin America where attrition tops 40% and wage pressures squeeze operator margins.

Compliance Pressures in Regulated Industries

Financial institutions must encrypt payment data end to end, health systems must log every access to protected health information, and European banks must deploy voice biometrics that authenticate callers within seconds. These mandates require modern call recording, audit trails, and AI-driven redaction that legacy PBX gear cannot supply. Vendors able to certify against the Payment Card Industry Data Security Standard, the Health Insurance Portability and Accountability Act, and regional data residency laws secure premium contract values, sometimes 50% higher than unregulated verticals. Diverging statutes mean global organizations now architect region-specific cloud instances, a complexity that favours platforms with granular policy engines and elastic multi-region footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexities With Legacy PBX | -1.80% | Global, particularly acute in Europe and mature North American enterprises | Medium term (2-4 years) |

| Data-Privacy And Sovereignty Concerns | -1.50% | Europe, China, India, with spillover to multinational deployments | Long term (≥ 4 years) |

| Agent Skill Gaps For AI-Augmented Workflows | -0.90% | Global, most pronounced in Asia Pacific and Latin America BPO hubs | Medium term (2-4 years) |

| Uncertain ROI For Edge-Deployed Contact Centers | -0.70% | North America and Europe, limited adoption in other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexities with Legacy PBX

Enterprises often operate 10-year-old switching infrastructure custom-wired to billing, order management, and customer-relationship-management systems. Undocumented call flows, home-grown IVR scripts, and mixed vendor hardware extend migrations up to 18 months, raising consulting bills beyond annual run-rate spend for mid-market firms. Professional-services engagements average several million United States dollars, and overruns are common when data conversion or compliance gaps surface late in the project. European organizations face additional hurdles because multi-vendor estates complicate retention of call recordings for statutory periods, stretching timelines and undermining internal business cases.

Data-Privacy and Sovereignty Concerns

The European Union’s General Data Protection Regulation levied EUR 1.6 billion in fines during 2024, stoking board-level anxiety about cross-border data flows. China’s Cybersecurity Law blocks outbound transfers unless operators obtain government approval, and India is debating localization that would raise infrastructure costs by one-quarter. Multinationals must therefore deploy country-specific cloud footprints, fracturing global agent pools, reducing scale efficiencies, and inflating compliance audits. The resulting operational drag slows cloud conversion rates for risk-averse enterprises that cannot reconcile cost-savings targets with jurisdictional rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Analytics Platforms Outpace Legacy IVR

Analytics and reporting tools, expanding at a 14.83% CAGR, are eclipsing legacy IVR’s 24.37% 2025 share as executives demand sentiment tracking and predictive churn alerts rooted in natural-language processing. This slice of the contact center transformation market size is fuelled by attach rates that now exceed three-quarters of net-new platform sales, reflecting recognition that voice and text interactions are strategic data assets. Intelligent call routing and workforce optimization modules ride the same trend, leveraging machine learning to pair customers with agents based on skill, language, and lifetime value, trimming average handle time by up to 20%.

Dialers, CTI connectors, and service engagements hold steady but slower growth, constrained by tightening rules on unsolicited calls and by cloud platforms embedding middleware natively. Yet services revenue remains important because enterprises outsource complex migrations and continuous optimization. The pivot toward analytics signals that competitive advantage now lies in converting call recordings and chat logs into actionable insight, rather than merely handling volume.

By Deployment: Hosted Solutions Gain Despite On-Premises Dominance

On-premises systems held 61.58% of the contact center transformation market share in 2025, but hosted deployments are advancing at 13.68% CAGR as organizations chase elastic capacity, automatic upgrades, and subscription pricing that converts capex to opex. Financial institutions and hospitals increasingly prefer hybrid configurations, keeping authentication or payment modules in-house while placing agent desktops, workforce management, and analytics in the vendor cloud. Hyperscalers intensify the shift by offering bundled contact center software alongside compute and storage at discounts that legacy vendors struggle to match.

Hosted deployments also speed geographic expansion, letting enterprises spin up thousands of seats across continents in weeks rather than procuring local data-center space. Latency-sensitive use cases, such as emergency dispatch or trading floors, and jurisdictions with patchy internet still favour on-premises or edge nodes. Consequently, the deployment mix will likely stabilize in a barbell shape, with greenfield and mid-market adopters defaulting to cloud while specialized workloads cling to dedicated hardware.

By Organization Size: SMEs Embrace Cloud-First Strategies

Large enterprises captured 58.23% of 2025 revenue, leveraging scale for volume discounts and integrated hybrid estates that span on-premises, private, and public clouds. They average thousands of agent seats across multiple countries and demand customized security, language support, and open APIs, lengthening sales cycles but yielding high contract values.

Small and medium enterprises, however, are the fastest risers, posting a 14.12% CAGR through 2031 as subscription tiers drop entry costs. Cloud-first platforms deliver pre-configured templates that activate in eight weeks, letting startups and mid-tier firms launch high-quality service with minimal IT staff. This dynamic is visible across Asia Pacific, where digital-native e-commerce and fintech companies scale from zero to hundreds of agents without touching a data center. Price sensitivity remains a constraint, so vendors rely on usage-based billing and automated onboarding to prevent churn.

By End-User Industry: Healthcare Adoption Accelerates Post-Pandemic

Banking, financial services, and insurance held 27.59% share in 2025, sustained by regulatory mandates for secure call recording, fraud detection, and voice authentication. Contract values here continue to exceed average deal sizes because compliance add-ons, redundancy zones, and encryption are compulsory.

Healthcare, expanding at 13.96% CAGR, is converting contact centers into telehealth and patient-engagement hubs that integrate electronic health records, appointment scheduling, and secure messaging. Hospitals report administrative cost savings north of 30% when agents and clinicians share unified desktops, and full audit trails ensure Health Insurance Portability and Accountability Act compliance. Media, retail, and telecommunications firms follow, emphasizing omnichannel orchestration that ties billing, subscription management, and in-store experiences to contact center workflows. Government and utilities adopt more slowly but provide multiyear contracts once platforms pass procurement and cybersecurity reviews.

Geography Analysis

Asia Pacific delivers the fastest growth trajectory at 14.55% CAGR because India’s business-process-outsourcing ecosystem employs 1.4 million agents and domestic enterprises now shift to cloud platforms to remain competitive. China’s data-residency mandates drive local infrastructure buildouts, benefitting indigenous vendors while raising entry costs for multinationals that must invest in local zones to comply. Southeast Asia’s e-commerce boom drives 24-hour service demand, and domestic small and medium enterprises gravitate toward pay-as-you-go models that minimize upfront costs.

North America remains the largest regional contributor at 36.49% revenue share in 2025, buoyed by early cloud adoption, sophisticated analytics use cases, and a mature ecosystem of system integrators and vendors. Privacy-shield successor agreements facilitate cross-border data flows, enabling consolidated operations that exploit labour arbitrage. United States enterprises lead adoption of AI-driven sentiment analysis and workforce automation to contain rising wage pressures and elevate customer-experience metrics.[2]“India BPO Industry Report 2025,” NASSCOM, nasscom.in

Europe follows, propelled by demand from financial services, retail, and government agencies. Strict General Data Protection Regulation enforcement stretches procurement cycles and adds professional-services cost, yet it simultaneously accelerates platform refresh as older systems cannot satisfy consent logging or data-erasure mandates. Southern European outsourcing hubs in Portugal and Greece attract foreign investment because multilingual talent pools lower cost per seat while staying inside the regulatory perimeter.

South America registers moderate expansion, with Brazil accounting for three-fifths of regional deployments. Currency volatility and political uncertainty temper long-range capex, so enterprises favour cloud subscription contracts that can scale down if economic conditions tighten. The Middle East and Africa remain nascent, though Saudi Arabia and the United Arab Emirates invest heavily under economic-diversification programs, funding government and telecom projects that require Arabic-language support and onshore hosting. South Africa leads African adoption but poor connectivity in rural zones sustains on-premises demand that tolerates intermittent bandwidth.

Competitive Landscape

The top 10 vendors command roughly 55% of global revenue, making the contact center transformation market moderately concentrated. Genesys, NICE, and Avaya leverage decades-long customer bases, extensive integrations, and compliance certifications to defend share. Cloud-native rivals, Five9, Talkdesk, and RingCentral differentiate through consumption pricing, rapid feature releases, and AI modules that reduce time to value. Amazon Web Services and Microsoft Azure disrupt margins by bundling contact center software with broader cloud consumption agreements, offering discounts of 30% to 40% for consolidated workloads.

Vertical specialization is emerging as a new frontier. Vendors that embed electronic health record connectors, voice biometrics certified for banking, or language packs optimized for regional dialects gain traction in regulated or underserved niches. Smaller players focus on real-time analytics, workforce optimization, or conversational AI, often entering technology-transfer partnerships or positioning for acquisition. Incumbents reinforce portfolios through intellectual-property filings, such as Cisco’s predictive routing algorithms that consider nearly 50 variables per interaction, signalling an arms race in applied data science rather than core telephony.

Competitive intensity is expected to escalate through 2031 as artificial intelligence commoditizes baseline features. Differentiation will hinge on regulatory depth, ecosystem breadth, and total cost of ownership rather than call-handling capacity alone. Vendors that balance global footprint with localized compliance, transparent pricing, and vertical accelerators will outpace peers that rely solely on legacy maintenance contracts.[3]"Cisco Webex Contact Center Patent Filing,” United States Patent and Trademark Office, uspto.gov

Contact Center Transformation Industry Leaders

-

RingCentral Inc.

-

NICE Systems Inc.

-

8x8 Inc.

-

Genesys Telecommunications Laboratories Inc.

-

Five9 Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Genesys committed USD 500 million to expand cloud data centers in Singapore, Mumbai, and Sydney to satisfy data-localization laws and cut latency.

- November 2025: NICE acquired a workforce-management provider for USD 1.2 billion, integrating AI scheduling and performance analytics into its CXone suite.

- October 2025: Amazon Web Services introduced Amazon Connect Forecasting, offering 95%-accurate volume and staffing predictions at no additional cost.

Global Contact Center Transformation Market Report Scope

The study analyses the demand and adoption of contact center software and services solutions across key industry verticals. The study provides a detailed assessment of the transformation of contact centers over the last decade from single-channel (call) entities to omnichannel-based centers with advanced capabilities, mainly driven by the growing adoption of cloud-based solutions and technological advancements. The impact of COVID-19 on the overall contact center industry and its effect on the various deployment types are comprehensively analyzed in the study. Segmentation by deployment considers on-premise and hosted sub-segments, where hosted also realizes cloud based-deployments.

The contact center transformation market is segmented by type (intelligent call routing, workforce performance optimization, dialers, interactive voice response, computer telephony integration, analytics, and reporting, services (consulting and managed services), by deployment (on-premise, hosted), organization size ( small and medium enterprises, large enterprises), by end-user industry ( banking, financial services, and insurance (BFSI), IT and telecom, media and entertainment, retail and consumer, healthcare), and by geography (North America, Europe, Asia-pacific, Middle East & Africa, and Latin America). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

The Contact Center Transformation Market Report is Segmented by Type (Intelligent Call Routing, Workforce Performance Optimization, Dialers, Interactive Voice Response, Computer Telephony Integration, Analytics and Reporting, Services), Deployment (On-Premise, Hosted), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (BFSI, IT and Telecom, Media and Entertainment, Retail and Consumer, Healthcare, Others), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa, Oceania). Market Forecasts are Provided in Terms of Value (USD).

| Intelligent Call Routing |

| Workforce Performance Optimization |

| Dialers |

| Interactive Voice Response |

| Computer Telephony Integration |

| Analytics and Reporting |

| Consulting and Managed Services |

| On-Premise |

| Hosted |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| IT and Telecom |

| Media and Entertainment |

| Retail and Consumer |

| Healthcare |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Intelligent Call Routing | |

| Workforce Performance Optimization | ||

| Dialers | ||

| Interactive Voice Response | ||

| Computer Telephony Integration | ||

| Analytics and Reporting | ||

| Consulting and Managed Services | ||

| By Deployment | On-Premise | |

| Hosted | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| IT and Telecom | ||

| Media and Entertainment | ||

| Retail and Consumer | ||

| Healthcare | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the contact center transformation market in 2026?

The market size is USD 53.03 billion in 2026, with a projected rise to USD 98.27 billion by 2031.

What is the expected CAGR through 2031?

The forecast CAGR is 13.13%.

Which region is growing fastest?

Asia Pacific leads with a 14.55% CAGR driven by BPO scale-up and data-localization mandates.

Which deployment model is gaining ground?

Hosted cloud solutions are advancing at a 13.68% CAGR as enterprises favor subscription pricing and rapid rollout.

Why is healthcare a high-growth vertical?

Telehealth expansion and stringent data-security requirements push healthcare to a 13.96% CAGR, integrating electronic health records with contact center workflows.

What drives platform selection among large enterprises?

Compliance depth, global data-center footprint, and embedded analytics heavily influence vendor choice for multi-country rollouts.

Page last updated on: