Pseudomonas Aeruginosa Infection Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

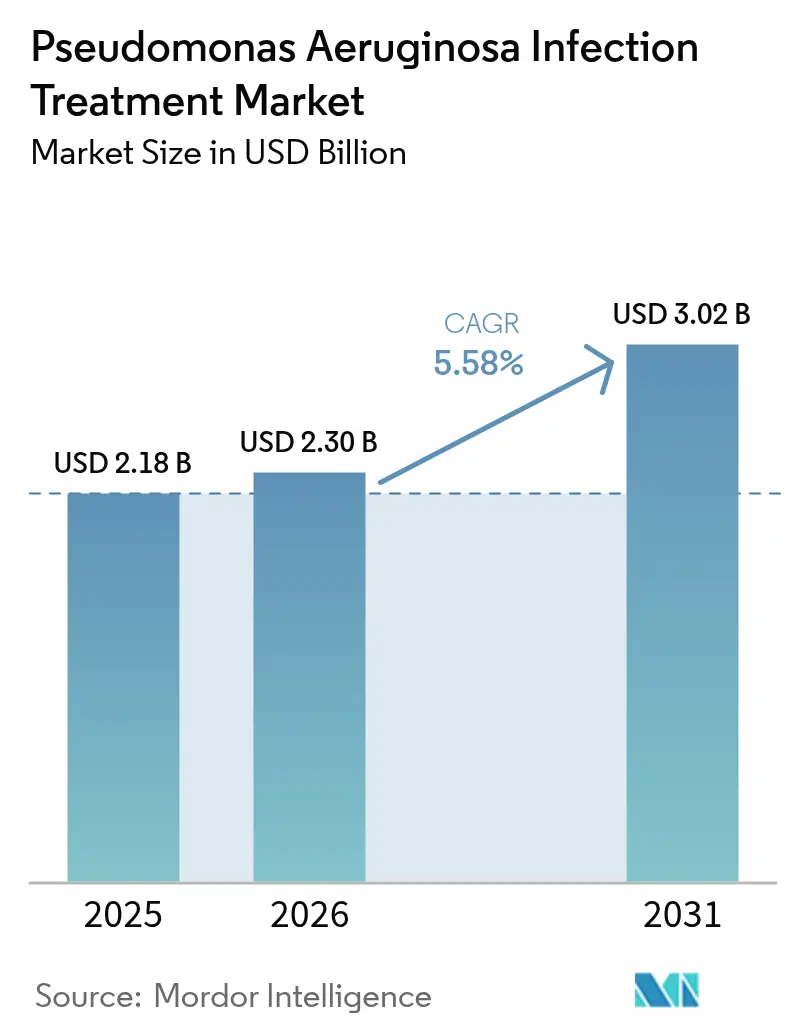

| Market Size (2026) | USD 2.3 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pseudomonas Aeruginosa Infection Treatment Market Analysis by Mordor Intelligence

The pseudomonas aeruginosa infection treatment market size in 2026 is estimated at USD 2.3 billion, growing from 2025 value of USD 2.18 billion with 2031 projections showing USD 3.02 billion, growing at 5.58% CAGR over 2026-2031. This growth trajectory underscores how healthcare systems are racing to contain hospital-acquired infections, particularly those caused by carbapenem-resistant strains that now account for 29.7% of Pseudomonas cases in European hospitals.[1]European Centre for Disease Prevention and Control, “Point Prevalence Survey of Healthcare-Associated Infections and Antimicrobial Use in European Acute Care Hospitals 2022-2023,” ecdc.europa.eu A widening pipeline of β-lactam/β-lactamase inhibitor combinations, rising investments in phage therapies, and the spread of rapid molecular diagnostics collectively boost demand for advanced therapeutics. North America continues to shape clinical protocols through robust stewardship programs, while Asia-Pacific gains momentum on the back of accelerating healthcare expenditure and molecular surveillance networks. Innovation intensity is further stoked by FDA fast-track pathways and CARB-X grants, both of which shorten time-to-market for next-generation agents.

Key Report Takeaways

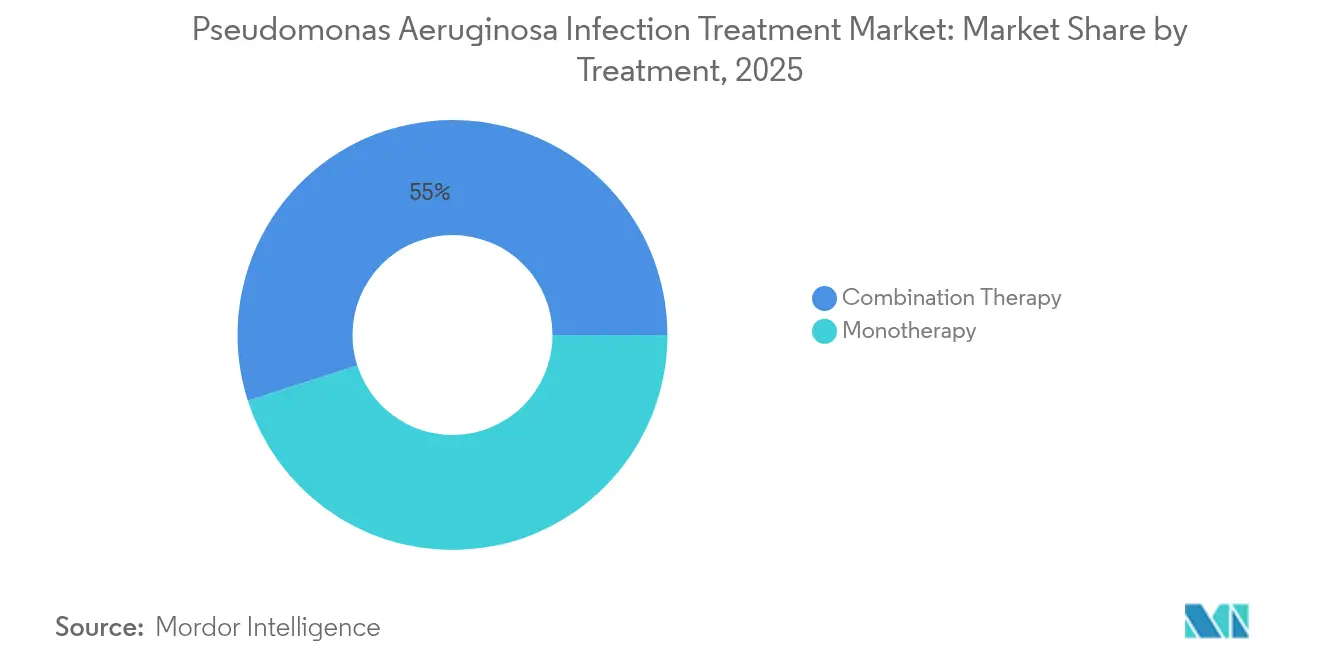

- By treatment type, combination therapy led with 54.95% of the Pseudomonas aeruginosa infection treatment market share in 2025, and the segment is projected to post a 9.58% CAGR through 2031.

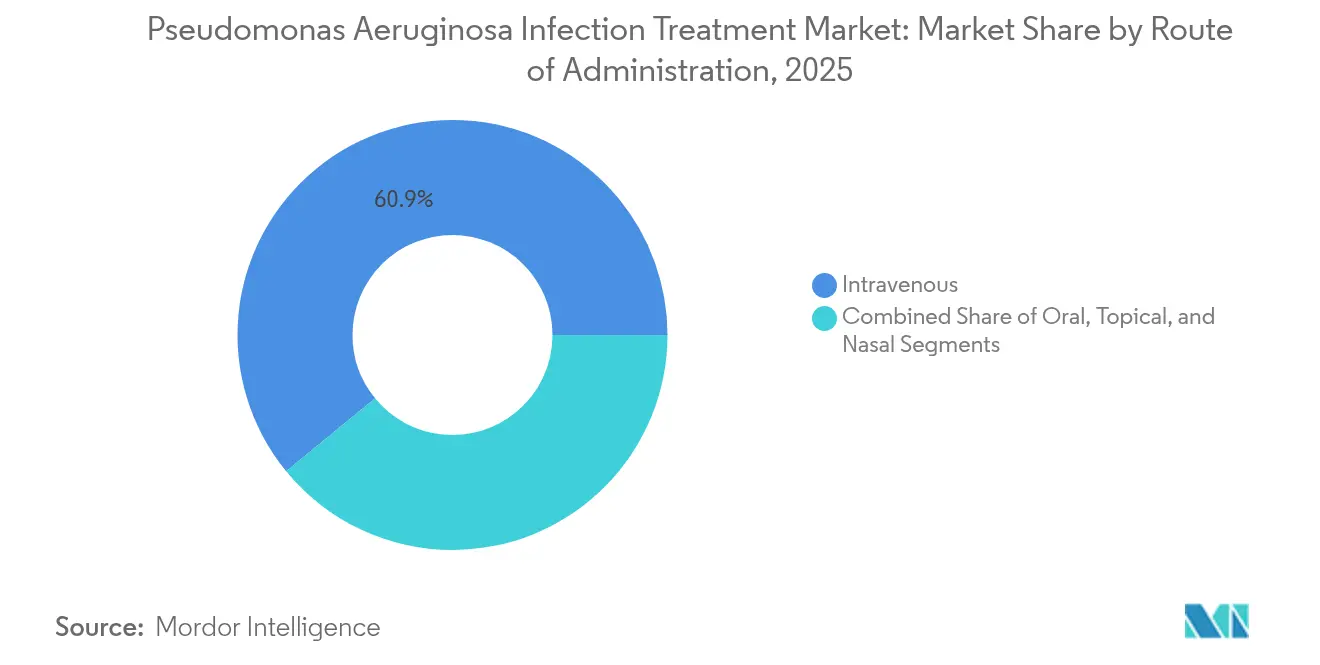

- By route of administration, intravenous products accounted for 60.92% of the Pseudomonas aeruginosa infection treatment market size in 2025, while inhalation therapies are poised to grow at an 7.95% CAGR.

- By distributional channel, hospital pharmacies contributed 63.98% revenue in 2025; Online/ Mail order pharmacies is forecast to register the fastest 8.89% CAGR to 2031

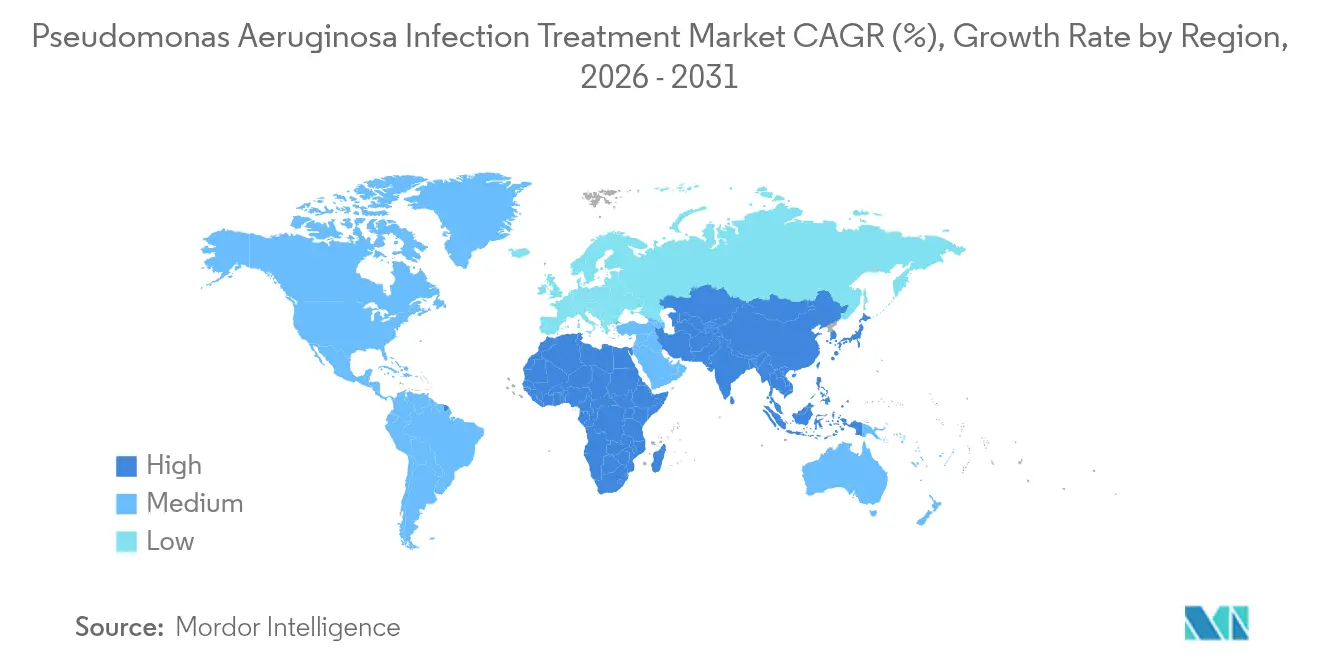

- By region, North America contributed 34.02% revenue in 2025; Asia-Pacific is forecast to register the fastest 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pseudomonas Aeruginosa Infection Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Hospital-Acquired Infections | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing R&D Investment In Antipseudomonal Drugs | +0.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Increasing Chronic Lung Disease Burden (CF, COPD) | +1.0% | Global, with concentrated impact in developed markets | Long term (≥ 4 years) |

| Regulatory Incentives For Phage & Novel Antibiotic Platforms | +0.6% | North America & EU regulatory frameworks | Medium term (2-4 years) |

| Adoption Of Inhaled Nano-Formulations Improving Adherence | +0.9% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Expansion Of Rapid Molecular Diagnostics | +0.7% | APAC core, expanding to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hospital-Acquired Infections

Hospital environments create a near-ideal reservoir for Pseudomonas aeruginosa, especially where intensive care units rely on mechanical ventilation and invasive catheters. European surveillance indicates more than 3.5 million healthcare-associated infections yearly, leading to over 90,000 deaths, of which 71% involve antibiotic-resistant organisms. Ventilator-associated pneumonia remains a critical subset, with mortality climbing to 35.1% in extensively drug-resistant episodes.[2]Diogo Mendes Pedro, “Extensively Drug-Resistant Pseudomonas aeruginosa: Clinical Features and Treatment with Ceftazidime/Avibactam and Ceftolozane/Tazobactam in a Tertiary Care University Hospital Centre in Portugal,” Frontiers in Microbiology, frontiersin.orgThese statistics spur hospitals to favor dual-agent protocols able to break through biofilms and tackle adaptive resistance.

Growing R&D Investment in Antipseudomonal Drugs

Funding consortia such as CARB-X have channelled significant capital toward novel mechanisms, exemplified by support for Forge Therapeutics’ metallo-enzyme inhibitors and Phico Therapeutics’ engineered phage platform. The GAIN Act has granted 147 qualified infectious disease product designations, accelerating review cycles for breakthrough agents.[3]U.S. Food and Drug Administration, “Generating Antibiotic Incentives Now Required by Section 805 of the Food and Drug Administration Safety and Innovation Act,” U.S. Department of Health and Human Services, fda.govPartnerships such as Eli Lilly–OpenAI illustrate how artificial intelligence now underpins lead-compound discovery pipelines.

Increasing Chronic Lung Disease Burden (CF, COPD)

Persistent colonization is commonplace in cystic fibrosis airways, where dense biofilms blunt systemic antibiotic penetration. Microbiome research shows Bacteroides species moderating inflammatory cascades, hinting at adjunct probiotic interventions. COPD animal models demonstrate that nanoparticle-borne antibiotics drop pulmonary bacterial loads and dampen inflammation more effectively than standard formulations.[4]Bob Yirka, “Antibacterial Agent Carried by Nanoparticles Used to Treat COPD in Mice,” Phys.org, phys.org As CFTR modulators extend life expectancy, therapy algorithms must reconcile chronic inhaled regimens with systemic tolerance thresholds.

Regulatory Incentives for Phage & Novel Antibiotic Platforms

The FDA’s QIDP pathway reduces review times and awards 5-year exclusivity extensions, while Europe’s Innovative Medicines Initiative nurtures adaptive trial designs that fit microbiology-specific endpoints. Such frameworks helped advance EMBLAVEO from submission to approval in under 12 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Emergence Of Multidrug Resistance | -1.8% | Global, with highest impact in Asia-Pacific & MEA | Short term (≤ 2 years) |

| High Cost Of Next-Generation Antibiotics | -1.1% | Global, disproportionate impact in LMICs | Medium term (2-4 years) |

| Cold-Chain Gaps For Liposomal Inhaled Products In LICs | -0.7% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Tighter Antimicrobial-Stewardship Protocols In High-Income Health Systems | -0.9% | North America & EU core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Emergence of Multidrug Resistance

Genetic plasticity fuels swift adaptation, with Portuguese tertiary centers reporting 3.7% extensively drug-resistant prevalence and 35.1% mortality. OprD porin loss confers carbapenem resistance, yet complete multidrug resistance requires intertwined efflux and β-lactamase pathways that force clinicians toward dual agents.

High Cost of Next-Generation Antibiotics

Premium pricing collides with limited reimbursement windows, especially in public hospitals across low- and middle-income regions where essential antibiotic availability can drop to 23.76%. Pharmaceutical company exits from emerging markets, exemplified by GSK and Sanofi departures from Nigeria, further constrain access to quality antimicrobials and increase reliance on substandard medications that accelerate resistance development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment: Combination Protocols Drive Resistance Management

Combination regimens commanded 54.95% of the Pseudomonas aeruginosa infection treatment market in 2025 and are advancing at a 9.58% CAGR through 2031. This dominance is anchored in robust Phase 3 evidence showing ceftolozane-tazobactam plus amikacin outperforming monotherapy for carbapenem-resistant infections. The Pseudomonas aeruginosa infection treatment market size for combination therapy is expected to reach USD 2.07 billion by 2031 on the back of synergistic mechanisms that block efflux, disable β-lactamases, and disrupt biofilm matrices. Even as monotherapies remain pivotal for fully susceptible isolates and select outpatient indications, next-generation hybrids such as aztreonam/avibactam or cefepime/enmetazobactam are redefining clinical thresholds for adequate coverage. Phage-antibiotic cocktails further expand the clinical toolkit, leveraging bacteriophages to perforate biofilms and ferry antibiotics into protected micro-colonies.

A deeper examination reveals how dual-agent protocols also mitigate supply-chain disruptions. Hospitals cushion against single-drug shortages by stocking versatile combinations spanning multiple mechanisms, thereby tempering the 42% higher shortage rate seen with antimicrobials. Meanwhile, stewardship committees favor combinations that deliver rapid bactericidal activity, shorten hospital stays, and cut downstream costs associated with prolonged ICU support. These clinical and economic advantages explain why the Pseudomonas aeruginosa infection treatment market continues to gravitate toward dual-agent strategies.

By Route of Administration: Inhalation Gains Momentum Through Innovation

Intravenous formulations retained 60.92% revenue in 2025, driven by their indispensability in sepsis management and surgical prophylaxis. Nevertheless, inhalation products are outpacing every other route with an 7.95% CAGR. The inhaled segment’s Pseudomonas aeruginosa infection treatment market size is forecast to cross USD 0.67 billion by 2031, buoyed by nano-enabled dry-powder systems achieving a 40% fine-particle fraction ideal for deep-lung deposition. Chronic bronchiectasis and cystic fibrosis cohorts champion inhaled delivery because localized doses reach 50-fold higher airway concentrations than systemic infusions, all while lowering nephrotoxicity risk.

Technological leaps include silver-nanoparticle adjuncts that slash required antibiotic doses and hyaluronic-acid complexes designed for viscous CF mucus. Regulatory confidence builds in parallel: the PROMIS trials confirmed that inhaled colistimethate sodium significantly reduces exacerbation frequency over 12 months. As device portability improves and dosing regimens shrink from thrice daily to once daily, patient adherence is set to climb, reinforcing the inhaled route’s role within the broader Pseudomonas aeruginosa infection treatment market.

By Distribution Channel: Digital Transformation Reshapes Access Patterns

Hospital pharmacies accounted for 63.98% of the Pseudomonas aeruginosa infection treatment market share in 2025, reflecting the need for on-site access to broad-spectrum and combination agents in critical‐care settings. These outlets integrate clinical pharmacists with stewardship teams and maintain real-time inventory controls that keep newly approved drugs such as EXBLIFEP and EMBLAVEO immediately available. Their embedded role inside hospitals also supports rapid dose adjustments for septic patients and minimizes treatment delays. Retail pharmacies play a complementary role by dispensing inhaled and oral follow-up therapies that allow earlier discharge and reduce inpatient costs.

Online and mail-order pharmacies are the fastest-growing channel, advancing at a 8.89% CAGR through 2031 as digital health platforms expand remote prescribing and adherence tracking . These distributors offer temperature-controlled logistics that protect liposomal or nanoparticle inhaled products, a capability that is increasingly valuable given the 42% higher shortage rate facing antimicrobials compared with other medicines. Automated refill reminders and connected inhaler data help clinicians monitor dosing fidelity in chronic cases, especially cystic fibrosis and bronchiectasis patients. As hybrid care models spread, the Pseudomonas aeruginosa infection treatment market increasingly relies on digital channels to close last-mile gaps and safeguard uninterrupted therapy.

Geography Analysis

North America holds firm at a 34.02% revenue share thanks to well-funded hospitals, aggressive stewardship mandates, and early uptake of QIDP-designated drugs. The region’s Veterans Health Administration surveillance shows shifting resistance profiles across 14 years, prompting continuous protocol updates and shifting formulary priorities. The United States accelerated approvals for EXBLIFEP and EMBLAVEO in less than a year, reinforcing a pragmatic regulatory environment that accelerates innovation. Canada’s provincial health reforms emphasize rapid diagnostic reimbursement, while Mexico increasingly codifies stewardship into national accreditation programs, giving the Pseudomonas aeruginosa infection treatment market strong regional headroom.

Asia-Pacific is the fastest riser, clocking an 8.55% CAGR as health ministries expand universal coverage and molecular labs. Carbapenem resistance reaches a mean 31.3% across the region, necessitating robust investment in rapid diagnostics and phage research. Japan exemplifies best-practice alignment, with 78.8% adherence to febrile neutropenia guidelines that pivot toward β-lactamase inhibitor combinations. China’s national surveillance network now integrates real-time genomic tracking, while India balances its role as the world’s antibiotic supplier with quality-control initiatives to curb substandard exports.

Europe demonstrates stable but sizable opportunity. Coordinated ECDC surveillance links antimicrobial use to resistance, informing guideline updates that favor rapid switch-to-oral strategies and high-dose prolonged infusions. Regulatory alignment enabled the European Commission to green-light EMBLAVEO for pathogen-limited options, illustrating responsive policy to clinical evidence. Southern Europe’s higher resistance burden drives combination therapy uptake, while Scandinavian countries leverage low antibiotic consumption to maintain comparatively lower resistance levels. Overall, the Pseudomonas aeruginosa infection treatment market remains primed for steady gains within western European strongholds and accelerated growth in central and eastern transition economies.

Competitive Landscape

The Pseudomonas aeruginosa infection treatment market is moderately fragmented, with top players competing across β-lactam/β-lactamase inhibitor platforms, inhaled formulations, and bacteriophage pipelines. Shionogi’s acquisition of Qpex Biopharma underscores a consolidation trend aimed at marrying discovery-stage assets with global commercialization muscle. AbbVie, Pfizer, and Roche pursue differentiated β-lactamase inhibitors tailored to Metallo-β-lactamases and difficult-to-treat intra-abdominal infections.

Competitive intensity also plays out in delivery-system innovation. Armata and BiomX both advance inhaled phage cocktails targeting chronic bronchiectasis and cystic fibrosis, each armed with orphan-drug incentives that grant seven-year exclusivity in the United States. In parallel, B. Braun’s DUPLEX system simplifies hospital compounding logistics by co-packing piperacillin-tazobactam in ready-to-use infusors, mitigating nurse workload and contamination risk.

Geographic reach remains pivotal. GSK’s return to the antibiotic arena via gepotidacin highlights a renewed pipeline that blends novel topoisomerase inhibition with existing distribution strength. Meanwhile, Allecra’s FDA nod for cefepime/enmetazobactam broadens U.S. hospital formularies just as European rollouts commence. Strategic partnerships, orphan-drug designations, and AI-enabled discovery collectively push competitors to sharpen differentiation, suggesting the Pseudomonas aeruginosa infection treatment market will see continued pipeline breadth rather than a winner-takes-all scenario.

Pseudomonas Aeruginosa Infection Treatment Industry Leaders

Teva Pharmaceutical Industries Ltd

Johnson & Johnson

Pfizer Inc

Merck & Co Inc

AbbVie Inc. (Allergan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Armata Pharmaceuticals reported positive Phase 2 “Tailwind” topline data for inhaled AP-PA02 in non-cystic-fibrosis bronchiectasis patients.

- January 2024: Armata Pharmaceuticals reported positive Phase 2 “Tailwind” topline data for inhaled AP-PA02 in non-cystic-fibrosis bronchiectasis patients.

Global Pseudomonas Aeruginosa Infection Treatment Market Report Scope

As per the scope of the report, pseudomonas aeruginosa is a rod-shaped, encapsulated, Gram-negative bacteria that causes diseases in humans. It infects people with weakened immune systems causing 'blue-green pus bacteria' associated with hospital-acquired infections such as ventilator-associated pneumonia and sepsis. Pseudomonas aeruginosa infection treatment drugs inhibit the growth of Pseudomonas aeruginosa or completely eliminate the bacterium. The Pseudomonas Aeruginosa Infection Treatment Market is Segmented by Treatment (Monotherapy and Combination Therapy), Route of Administration (Nasal, Oral, and Intravenous), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for all the above segments.

| Monotherapy |

| Combination Therapy |

| Intravenous |

| Oral |

| Inhalation / Nasal |

| Topical |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online / Mail-Order Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment | Monotherapy | |

| Combination Therapy | ||

| By Route of Administration | Intravenous | |

| Oral | ||

| Inhalation / Nasal | ||

| Topical | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online / Mail-Order Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Pseudomonas aeruginosa infection treatment market?

The market stands at USD 2.3 billion in 2026 and is projected to reach USD 3.02 billion by 2031 at a 5.58% CAGR over 2026-2031.

Which treatment modality leads global sales?

Combination regimens dominate with 54.95% 2025 revenue and are expanding at a 9.58% CAGR through 2031 due to superior performance against multidrug-resistant strains.

Why is Asia-Pacific the fastest-growing region?

High carbapenem resistance prevalence, rising healthcare expenditure, and rapid diagnostic adoption collectively drive an 8.55% regional CAGR.

How are inhalation therapies changing the treatment landscape?

Nano-enabled dry powders and liposomal aerosols deliver high local drug concentrations with fewer systemic effects, underpinning an 7.95% CAGR for inhaled products.

What hurdles limit broader access to new antibiotics?

High drug acquisition costs and cold-chain requirements create access gaps, especially across low- and middle-income countries where essential medicines availability is already constrained.

Page last updated on: