Microbiome Modulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

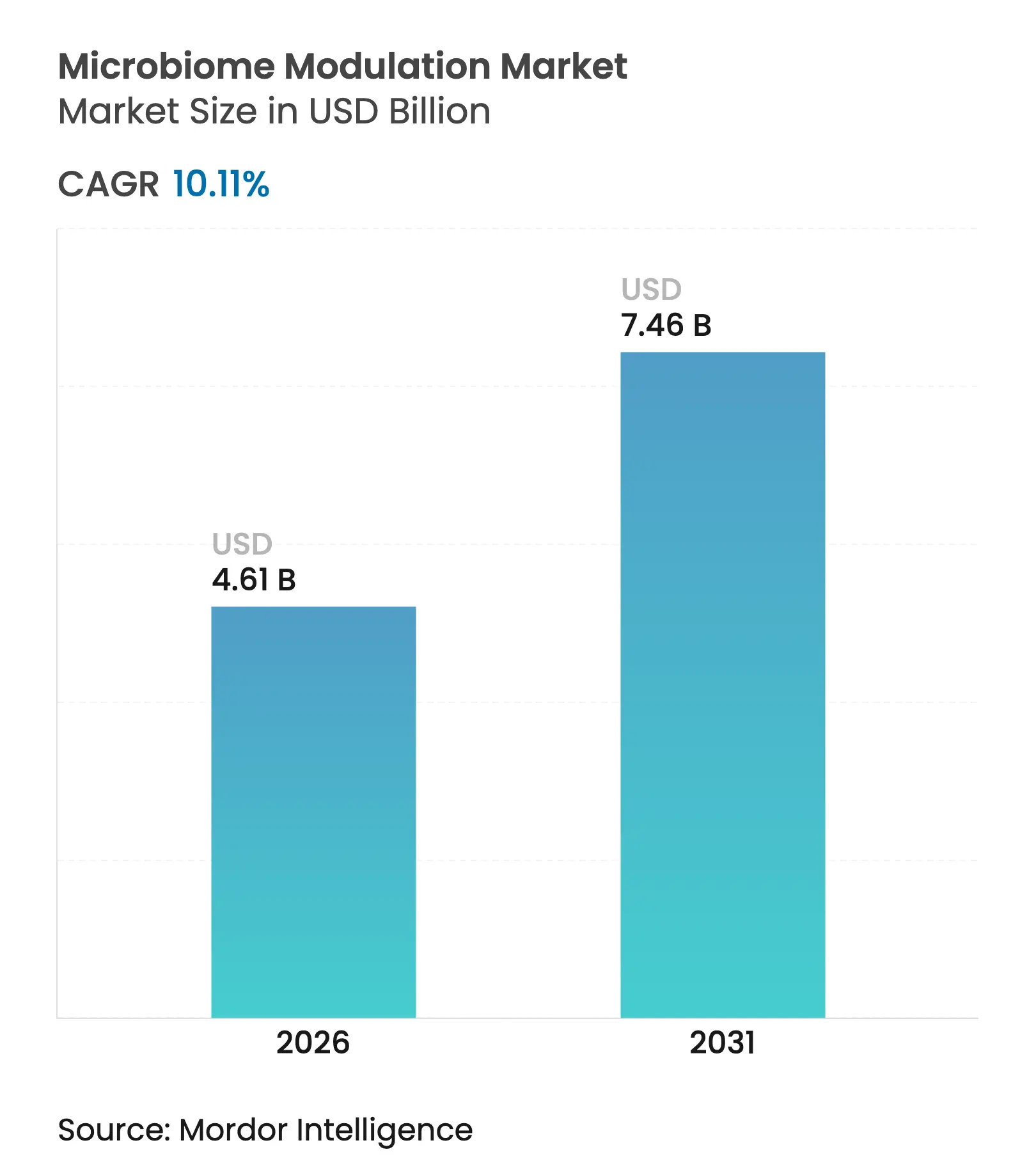

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 10.11 % CAGR |

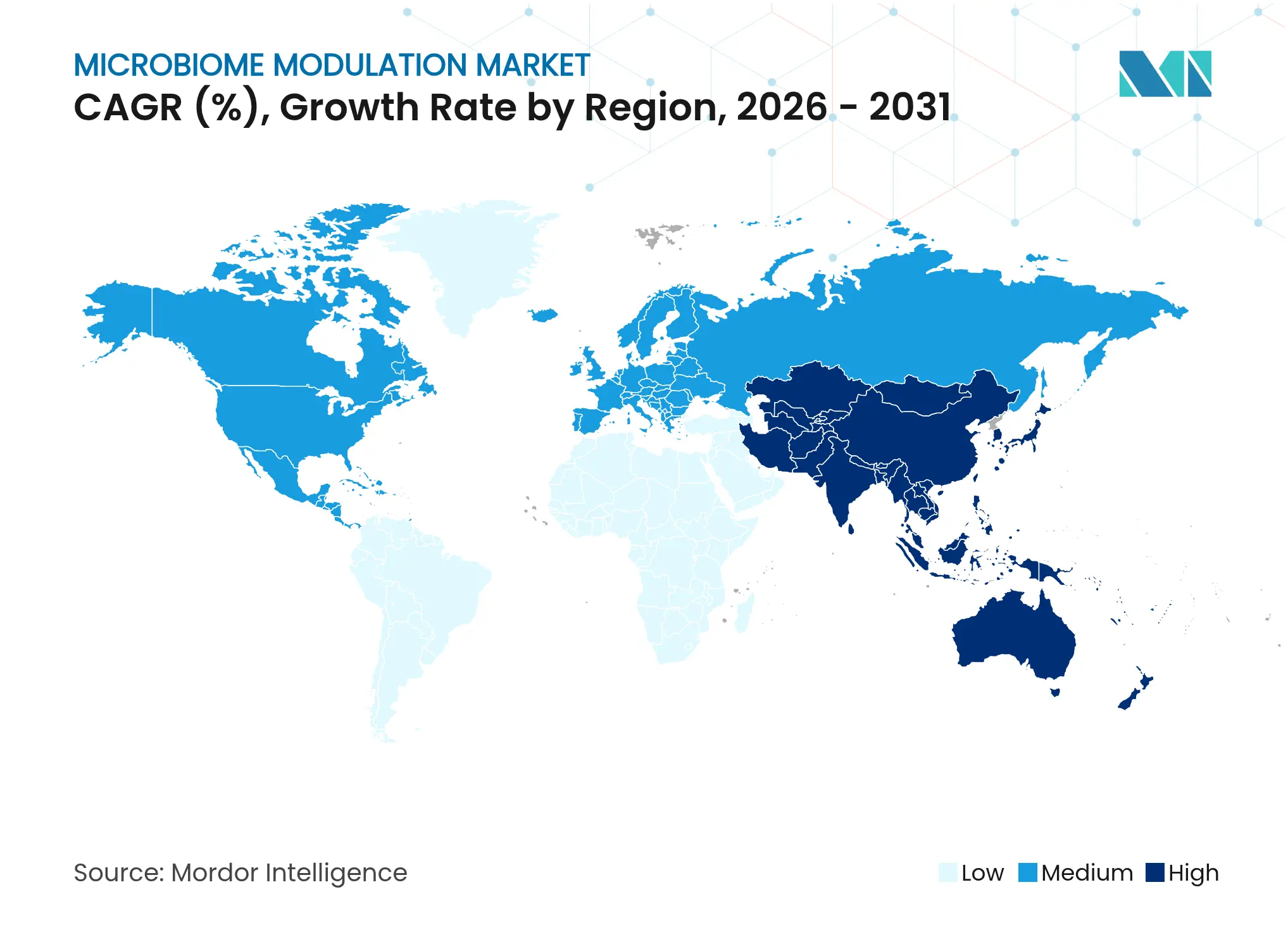

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

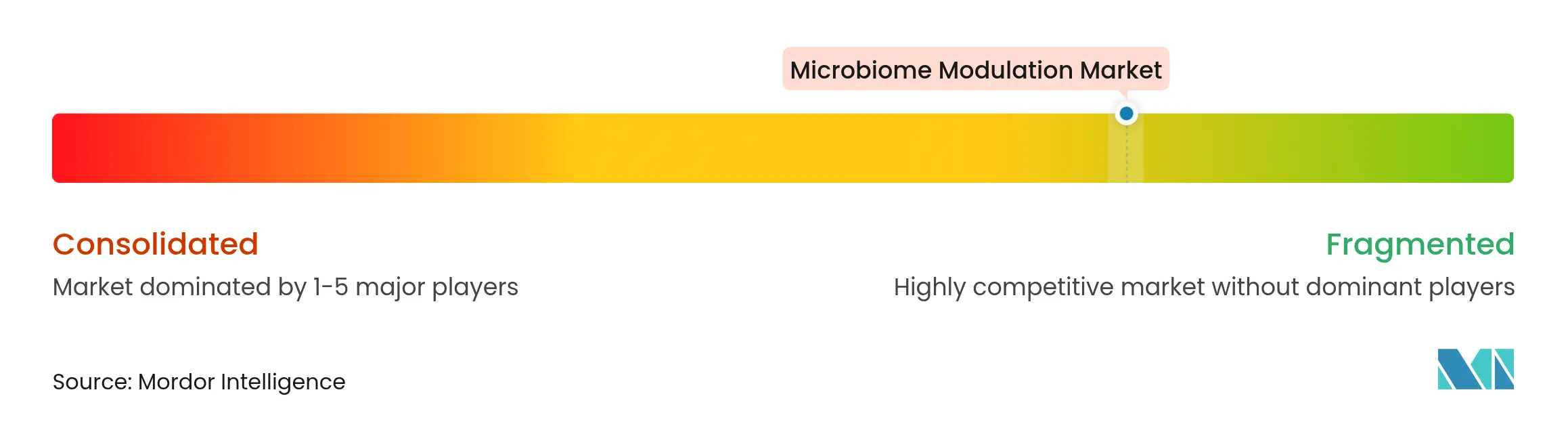

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Microbiome Modulation Market Analysis by Mordor Intelligence

The microbiome modulation market size is expected to grow from USD 4.19 billion in 2025 to USD 4.61 billion in 2026 and is forecast to reach USD 7.46 billion by 2031 at 10.11% CAGR over 2026-2031. Growth is reinforced by regulatory fast-track designations for live biotherapeutic products, steady precision-microbiome research outputs, and widening consumer demand for preventive gut-health nutrition. The 2024 FDA approvals of VOWST and REBYOTA created an essential precedent for microbiome therapeutics, while contract manufacturing scale-up now enables commercial viability for complex live biotherapeutic formulations. Competitive strategies increasingly focus on proprietary strain libraries, cold-chain logistics, and regulatory expertise, with consolidation accelerating as pharmaceutical and food majors acquire specialized biotechnology capabilities. Regionally, North America leads on account of regulatory maturity, but Asia-Pacific is the fastest-growing geography as national regulators formalise microbiome guidance and disposable income rises. Consumer migration toward functional foods, coupled with precision-medicine approaches for severe infections and chronic inflammatory diseases, preserves a broad opportunity spectrum for both wellness-oriented and prescription-grade offerings across the microbiome modulation market.

Key Report Takeaways

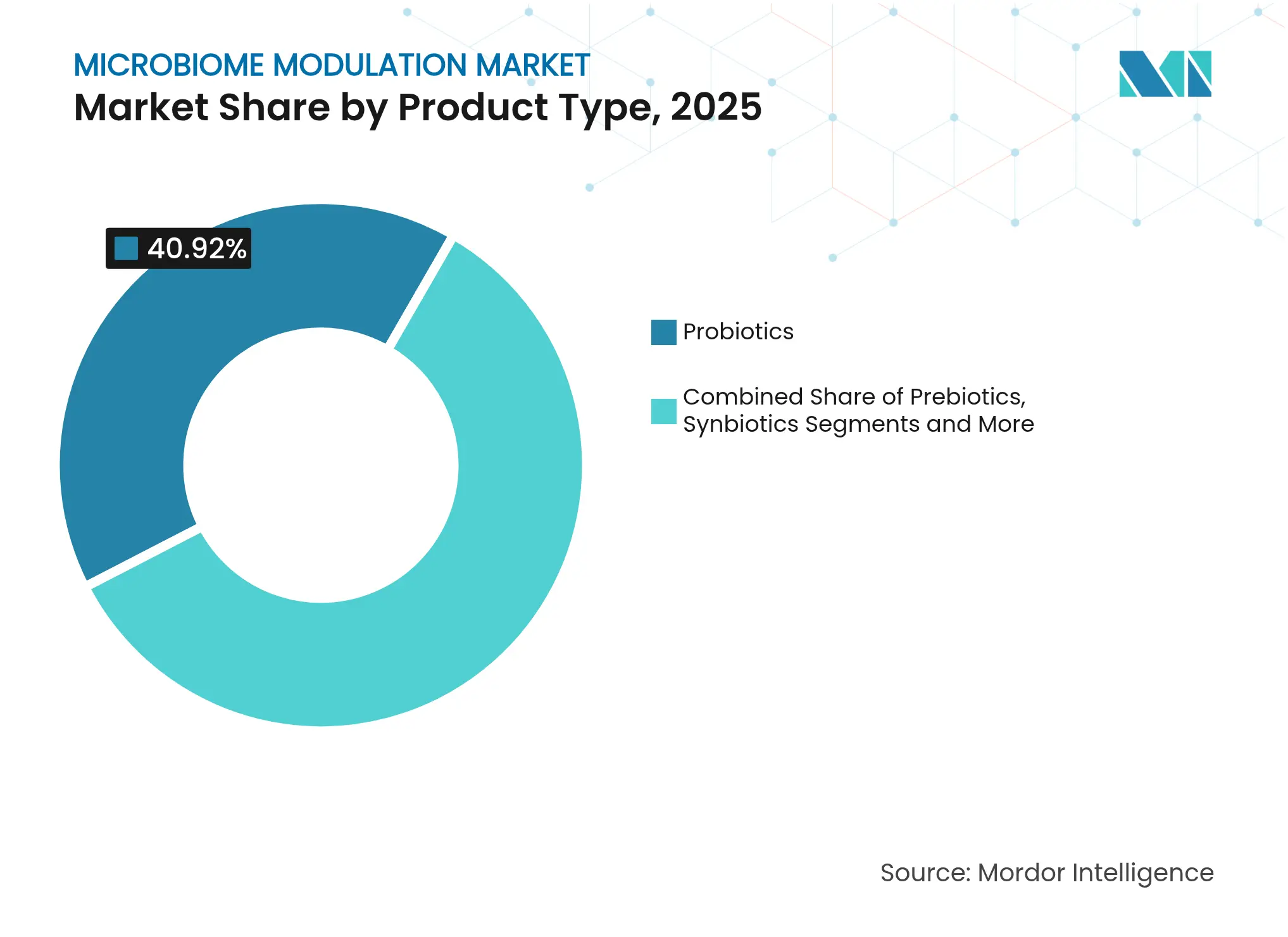

- By product category, probiotics led with 40.92% revenue share in 2025, whereas live biotherapeutic products are projected to expand at a 24.62% CAGR through 2031.

- By application, gastrointestinal disorders accounted for 32.14% of the microbiome modulation market size in 2025, while infectious disease applications are advancing at a 25.78% CAGR through 2031.

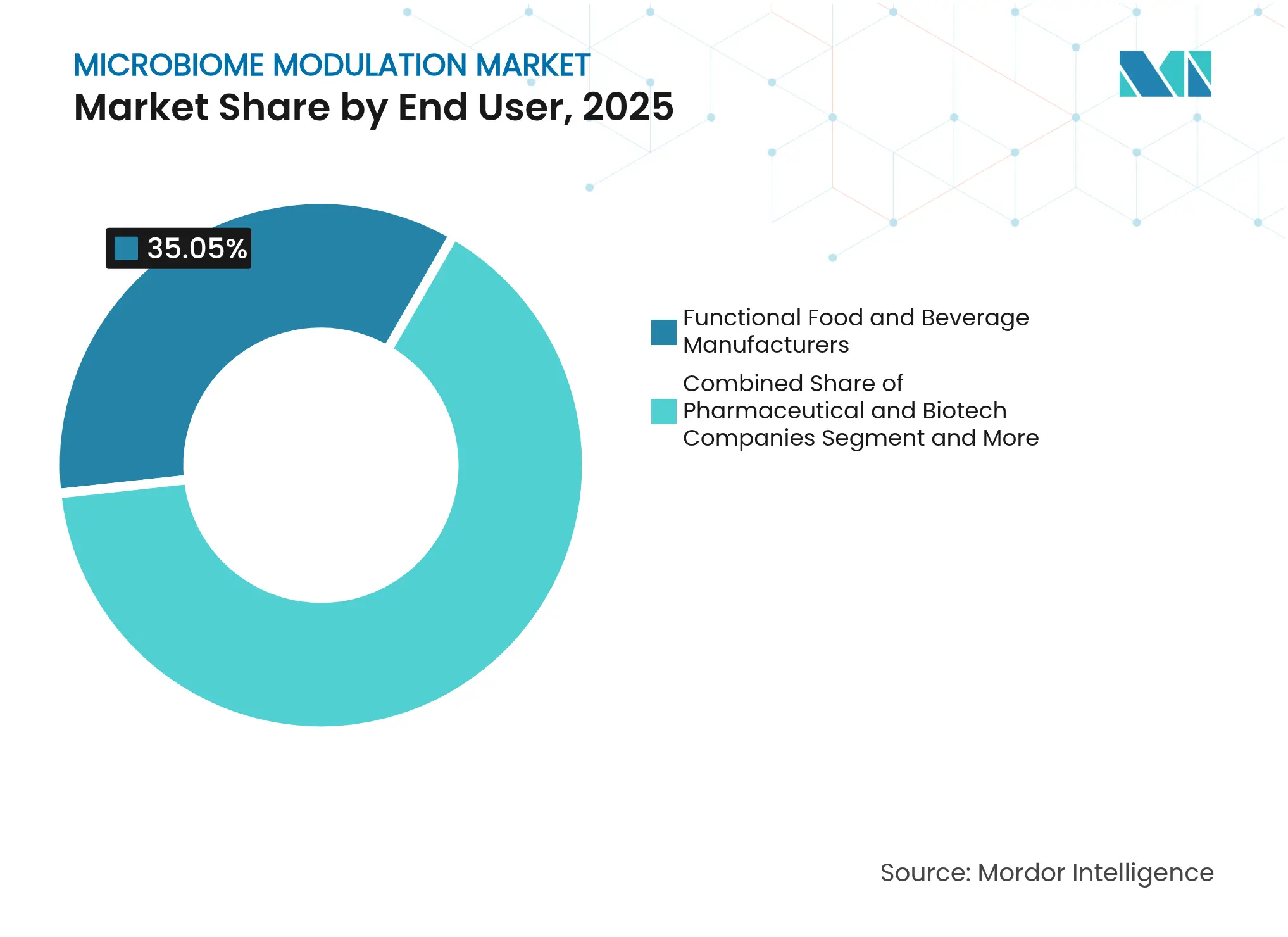

- By end-user group, functional food and beverage manufacturers held 35.05% of the microbiome modulation market share in 2025; pharmaceutical and biotechnology companies record the highest projected CAGR at 24.38% to 2031.

- By formulation, powders and sachets commanded 34.74% share of the microbiome modulation market size in 2025 and liquids and drinks are rising at a 19.22% CAGR over the same period.

- By geography, North America contributed 36.78% of 2025 revenue, whereas Asia-Pacific is advancing at a 12.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microbiome Modulation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of gastrointestinal disorders

Rising prevalence of gastrointestinal disorders

| +2.5% | North America, Europe, global spread | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.5%

| Geographic Relevance:

North America, Europe, global spread

| Impact Timeline:

Medium term (2-4 years)

|

Advances in microbiome research & new applications

Advances in microbiome research & new applications

| +1.8% | North America lead, Asia-Pacific catch-up | Long term (≥ 4 years) | |||

Consumer shift toward preventive gut-health habits

Consumer shift toward preventive gut-health habits

| +2.1% | Early adoption in North America & Europe; global diffusion | Short term (≤ 2 years) | |||

Contract-manufacturing scale-up for live products

Contract-manufacturing scale-up for live products

| +1.2% | North America & Europe, spreading to Asia-Pacific | Medium term (2-4 years) | |||

Regulatory fast-track pathways for C. difficile LBPs

Regulatory fast-track pathways for C. difficile LBPs

| +0.9% | North America & Europe; harmonisation under discussion | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence Of Gastrointestinal Disorders

Escalating incidence of inflammatory bowel disease, irritable bowel syndrome, and antibiotic-associated diarrhea has elevated digestive-health expenditures to USD 51.62 billion in 2025, tracking an 8.3% CAGR[1]EnteroBiotix, “EBX-102-02 Phase 2 IBS Trial,” enterobiotix.com. Conventional pharmaceuticals often fail to correct underlying dysbiosis, positioning microbiome-targeted interventions as first-line therapy for recurrent or refractory cases. Phase 2 data from EnteroBiotix’s EBX-102-02 trial showed clinically meaningful symptom relief for IBS, confirming the therapeutic value of full-spectrum bacterial consortia over single-strain products. Clinical protocols are shifting toward precision medicine that tailors interventions to individual microbiome profiles, allowing root-cause correction rather than symptomatic control. Investment in diagnostic tools that characterise patient-specific microbial signatures supports this personalised model, which in turn broadens adoption prospects for the microbiome modulation market.

Advances In Microbiome Research & Expanding Therapeutic Applications

Validated gut-brain axis mechanisms now connect the intestinal microbiome with neurological, dermatological, and metabolic pathologies, thereby enlarging total addressable revenue pools. Systematic reviews reported measurable improvements in depression and anxiety with Lactobacillus and Bifidobacterium supplementation. In autism spectrum disorder trials, precision microbial interventions improved social behaviours, demonstrating the feasibility of targeted windows even when core severity scores held steady. Inhaled probiotics delivered via dry powder formulations improved asthma control, indicating the promise of airway microbiome modulation. Each new disease domain advanced by robust clinical evidence reduces market dependence on gastrointestinal indications, though regulatory pathways remain intricate when translating basic science into licenced therapeutic products.

Consumer Shift Toward Preventive Gut-Health Nutrition

Rising public awareness of how gut microbiota influence systemic immunity and metabolic balance has propelled demand for functional foods, dietary supplements, and next-generation postbiotic ingredients. Reviews in 2025 highlighted immune-modulating, anti-inflammatory, and glycaemic benefits from prebiotic inulin, multi-strain probiotics, synbiotic combinations, and heat-treated postbiotics. Postbiotics, being non-viable yet biologically active, deliver stability advantages for manufacturers unequipped to maintain cold chains. Microencapsulation of synbiotics achieved log 8 CFU mL-1 survival through the gastrointestinal tract, removing viability concerns in mainstream food matrices. Preventive consumption translates into recurring purchase cycles, thus generating steady revenue for companies across the microbiome modulation market, but education campaigns and product labelling standards remain essential to reinforce consumer trust.

Contract-Manufacturing Scale-Up Of Live Biotherapeutic Products

High-grade manufacturing facilities are critical to bridge the transition from clinical proof-of-concept to commercial availability. The University of Chicago opened the first academic cGMP suite dedicated to live biotherapeutics in 2024, enabling production of therapeutically defined bacterial consortia for investigator-initiated trials. Spray-drying and encapsulation upgrades enhance shelf-life, while specialised cold-chain logistics mitigate viability losses en route to end users. Small biotech enterprises leverage contract manufacturing organisations to avoid capital-intensive facility build-outs, shortening time-to-market for novel formulations. Nevertheless, stringent procedural compliance and batch-to-batch consistency requirements create high entry barriers that favour players with established quality systems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lack of product standardisation vs traditional drugs

Lack of product standardisation vs traditional drugs

| -1.5% | Global; regulatory divergence pronounced | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-1.5%

| Geographic Relevance:

Global; regulatory divergence pronounced

| Impact Timeline:

Long term (≥ 4 years)

|

High development & clinical-trial costs for LBPs

High development & clinical-trial costs for LBPs

| -0.8% | North America & Europe funding hubs | Medium term (2-4 years) | |||

Cold-chain bottlenecks in last-mile distribution

Cold-chain bottlenecks in last-mile distribution

| -0.7% | Emerging markets most affected | Short term (≤ 2 years) | |||

Microbiome IP-patent thickets slowing licensing

Microbiome IP-patent thickets slowing licensing

| -0.3% | North America & Europe dominating filings | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lack Of Product Standardisation Vs. Traditional Therapies

Traditional pharmaceuticals enjoy rigorous and universally recognised quality benchmarks, whereas microbiome therapies still lack harmonised potency, purity, and identity metrics. The National Institute for Biological Standards and Control has begun issuing reference reagents to calibrate analytical assays, but cross-manufacturer consistency in viable cell counts and metabolite profiles remains variable. Physicians hesitate to prescribe products when dose-response relationships are ambiguous, delaying mainstream adoption even in markets with regulatory approvals. Inconsistent labelling and over-the-counter probiotic variability further erode clinician confidence, keeping prescription volumes below potential despite demonstrated efficacy[2]FDA, “Early Clinical Development of Live Biotherapeutic Products,” fda.gov. Harmonisation of manufacturing standards, validated biomarkers, and clinical endpoints will be pivotal in unlocking the full growth curve of the microbiome modulation market.

High Development & Clinical-Trial Costs For LBPs

Live biotherapeutic product programmes require extensive safety datasets and complex manufacturing comparability protocols, elevating development budgets beyond those for small molecules. Trials often need larger cohorts and longer follow-up to prove durable microbiome reconstitution, obliging sponsors to raise sizeable capital rounds in competitive funding environments. FDA guidance clarifies investigational requirements but still mandates meticulous documentation of strain provenance, genomic stability, and contaminant controls, raising baseline spend on CMC activities. Venture capitalists scrutinise time-to-exit prospects, tempering deal flow toward early-stage innovators. Moreover, reimbursement frameworks lag in defining value metrics for microbiome products outside narrowly approved indications, compounding uncertainty for investors and slowing product pipelines.

Segment Analysis

By Product Type: Live Biotherapeutics Catalyse Therapeutic Transformation

Live biotherapeutic products accounted for USD 1.07 billion in 2025, yet they are forecast to climb at a 24.62% CAGR to 2031, reflecting the sector’s shift from commodity probiotics toward precisely characterised bacterial consortia. Vedanta Biosciences’ global Phase 3 RESTORATiVE303 study of VE303 across 22 countries illustrates the widened clinical infrastructure backing these modalities. Defined consortia satisfy regulatory preference for exact strain composition, contrasting with historical reliance on undefined faecal transplants. Conversely, probiotics remain the volume leader, holding 40.92% of 2025 revenue because of entrenched consumer familiarity and looser regulatory oversight. Synbiotics gain visibility after 2024 expert consensus guidance clarified usage definitions, paving the way for combination products that integrate both prebiotic substrates and probiotic organisms.

Manufacturing complexity for viable multi-strain formulations poses high barriers, but also underwrites premium pricing models that improve profitability per dose. Postbiotics, being metabolite-based rather than live, offer ambient-temperature stability and easier scalability, attracting food and beverage innovators with fewer cold-chain capabilities. Acurx Pharmaceuticals’ ibezapolstat patent, protecting an antibiotic that preserves microbiome balance while delivering 96% clinical cure, underscores convergence between traditional antimicrobials and microbiome-sparing design. Across the continuum, the microbiome modulation market size for defined bacterial consortia is projected to outpace legacy categories, driven by payer willingness to reimburse products supported by randomised controlled evidence.

Note: Segment shares of all individual segments available upon report purchase

By Application: Infectious Disease Use Cases Accelerate Beyond GI Focus

Gastrointestinal disorders kept a dominant 32.14% share in 2025 because regulators and clinicians have built the most robust evidence base here, yet infectious-disease applications are accelerating at a forecast 25.78% CAGR to 2031. Meta-analyses of probiotic prophylaxis show 28–38% relative risk reduction for ventilator-associated pneumonia, highlighting tangible clinical value outside the gut. Oropharyngeal probiotic lozenges such as Bactoblis reduce recurrent respiratory infections in paediatric populations, thereby curbing antibiotic utilisation and healthcare costs. Urinary-tract infection prevention trials demonstrate statistically significant recurrence reductions with combined oral and vaginal probiotic courses, tackling rising antimicrobial resistance without relying on new small molecules.

Neurological, dermatological, and metabolic conditions progressively enter late-stage pipelines as mechanistic understanding of the microbiome–immune–endocrine nexus deepens. Still, regulatory frameworks insist on disease-specific clinical endpoints and post-marketing surveillance, delaying commercial deployments relative to gastrointestinal indications. Companies that establish modular development platforms—capable of rotating strain sets for different organs—stand to capture multiple addressable segments and expand the microbiome modulation market share across therapeutic domains.

By End User: Pharmaceutical Companies Lead Therapeutic Shift

Functional food and beverage companies captured 35.05% of revenue in 2025 on the strength of mass-retail distribution, brand loyalty, and consumer education campaigns. However, pharmaceutical and biotechnology firms are projected to post the fastest 24.38% CAGR through 2031 as prescription-grade live biotherapeutics secure regulatory approvals. Nestlé Health Science’s USD 175 million acquisition of VOWST and PepsiCo’s USD 1.95 billion purchase of Poppi signal food and beverage giants’ entry into the regulated therapeutic arena, aligning consumer-facing and clinical-grade capabilities. Academic institutions also comprise a notable end-user block, driving early-stage discovery and clinical validation through public-private partnerships, which often licence out intellectual property once proof-of-concept is achieved.

Reimbursement negotiations remain a pivotal hurdle for biopharmaceutical entrants because payers demand pharmacoeconomic evidence beyond microbial readouts. Contract manufacturing organisations allow smaller biotechs to comply with GMP while avoiding construction of bespoke facilities, but long-term value capture may shift toward firms that vertically integrate manufacturing and distribution. Ultimately, therapeutic-oriented entities capable of demonstrating clear clinical benefit in randomised trials will steer the microbiome modulation market toward higher-margin prescription revenue streams.

Note: Segment shares of all individual segments available upon report purchase

By Formulation: Liquids Match Convenience With Technological Viability

Powders and sachets maintained a 34.74% revenue lead in 2025 because stability at room temperature simplifies global distribution. Nonetheless, liquids and drinks are forecast to grow at 19.22% CAGR as consumers gravitate to ready-to-consume formats that integrate easily into daily routines. Encapsulated synbiotics embedded in beverages preserve log 8 CFU mL-1 counts during transit through simulated gastrointestinal conditions, demonstrating technological feasibility for mass-market products. Capsules and tablets offer dosing precision for prescription regimens, whereas topical creams exploit skin-microbiome science to address chronic dermatitis and acne without systemic exposure.

Inhalable dry-powder formulations of Lactobacillus rhamnosus GG achieve 86% aerosolisation efficiency, enabling targeted respiratory-tract delivery for bronchiectasis maintenance. Yet liquid formats demand robust cold-chain infrastructure to maintain viability, thereby privileging companies with established refrigeration logistics. Emerging shelf-stable postbiotic liquids could balance convenience with manufacturing pragmatism, opening an attractive avenue for new entrants to penetrate the microbiome modulation market without encumbering cold-chain constraints.

Geography Analysis

North America held 36.78% of 2025 revenue due to the FDA’s clear regulatory framework for live biotherapeutic products, a deep bench of clinical trial centres, and substantial venture capital pools. Successful completion of enrolment in Seres Therapeutics’ SER-155 Phase 1b trial illustrates the region’s capacity to fast-track complex microbiome studies across transplant recipients. Strategic acquisitions, such as the Nestlé–Seres VOWST deal, validate exit pathways for innovators and draw additional investment into the microbiome modulation market. However, high R&D and compliance costs elevate entry thresholds, limiting participation to well-funded startups or large incumbents.

Europe combines progressive novel-food legislation for probiotic foods with advanced academic research programmes, resulting in high product diversity and robust clinical pipelines. Positive Phase 3 results for MaaT 013 in acute graft-versus-host disease underscore European prowess in niche, high-value indications. The European Medicines Agency collaborates with national authorities to harmonise dossier expectations, but variations in health-claim rules necessitate tailored launch strategies. Long-standing cold-chain networks across the continent ease distribution of viable therapeutics, supporting gradual uptake in hospitals and specialist clinics.

Asia-Pacific emerges as the fastest-growing zone at a projected 12.21% CAGR through 2031, propelled by increasing healthcare expenditure, rising middle-class incomes, and widespread cultural acceptance of fermented foods that align with probiotic narratives. Governments in Japan, South Korea, and Singapore are drafting explicit guidelines for microbiome therapies, signalling policy support and lowering regulatory ambiguity. Large population bases offer scale benefits for consumer-facing products, though fragmented regulation across developing countries requires local partner collaborations. Infrastructure deficiencies in rural zones challenge cold-chain continuity, favouring shelf-stable postbiotic and spore-forming probiotic formats. Cumulatively, these drivers underpin the expansion of the microbiome modulation market across Asia-Pacific as companies adapt portfolios to diverse regulatory and logistical environments.

Competitive Landscape

Market Concentration

The microbiome modulation market remains fragmented, with numerous research-stage biotechs, ingredient suppliers, and traditional food conglomerates vying for positioning. Consolidation is accelerating as deep-capital players acquire niche innovators to access specialised strain libraries and manufacturing know-how. Nestlé Health Science’s acquisition of VOWST epitomises this strategy, granting immediate entry to an FDA-approved asset while providing Seres Therapeutics with non-dilutive capital to advance pipeline programmes. PepsiCo’s purchase of functional-soda brand Poppi demonstrates parallel interest from beverage groups seeking microbiome credentials in consumer portfolios.

Intellectual-property portfolios centred on proprietary strains, genomic editing techniques, and encapsulation materials act as competitive moats. Patent thickets complicate cross-licensing negotiations, occasionally slowing multi-strain product development but reinforcing the value of robust legal strategies. Manufacturing scale represents a second differentiation layer; companies controlling cGMP facilities that handle strict anaerobic processes command higher margins and are attractive contract-service partners. Cold-chain distribution capabilities, although costly, further distinguish multinationals equipped to maintain viability from factory to point of sale.

Competitive intensity has also risen around data analytics and personalised nutrition platforms that translate metagenomic sequencing outputs into tailored supplement recommendations. Firms integrating AI-enabled strain selection and CRISPR-guided gene editing can iterate candidate consortia faster than traditional culture-based approaches, compressing development timelines. Meanwhile, traditional pharmaceutical companies are exploring microbiome-sparing antibiotics like ibezapolstat to extend franchise life without triggering dysbiosis-related side effects. Overall, the market landscape balances opportunity for scientific innovation against the resource demands of manufacturing, regulatory navigation, and global distribution.

Microbiome Modulation Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MaaT Pharma announced positive results from its pivotal Phase 3 ARES study evaluating MaaT 013 for acute graft-versus-host disease, paving the way for regulatory submissions.

- August 2024: Seres Therapeutics completed a USD 175 million asset purchase agreement with Nestlé Health Science for VOWST, the first FDA-approved oral microbiome therapy for recurrent C. difficile infection.

Table of Contents for Microbiome Modulation Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Gastrointestinal (GI) Disorders

- 4.2.2Advances In Microbiome Research & Expanding Therapeutic Applications

- 4.2.3Consumer Shift Toward Preventive Gut-Health Nutrition

- 4.2.4Contract-Manufacturing Scale-Up Of Live Biotherapeutic Products

- 4.2.5Regulatory Fast-Track Pathways For Recurrent C-Difficile LBPs

- 4.3Market Restraints

- 4.3.1Lack Of Product Standardisation Vs. Traditional Therapies

- 4.3.2High Development & Clinical-Trial Costs For LBPs

- 4.3.3Cold-Chain Bottlenecks In Last-Mile Distribution

- 4.3.4Microbiome IP-Patent Thickets Slowing Cross-Licensing

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Prebiotics

- 5.1.2Probiotics

- 5.1.3Synbiotics

- 5.1.4Postbiotics

- 5.1.5Live Biotherapeutic Products (LBPs)

- 5.1.6Others

- 5.2By Application

- 5.2.1Infectious Diseases

- 5.2.2Gastrointestinal Diseases

- 5.2.3Endocrine & Metabolic Disorders

- 5.2.4Dermatological Conditions

- 5.2.5Neurological & Mental Health

- 5.2.6Others

- 5.3By End User

- 5.3.1Pharmaceutical & Biotech Companies

- 5.3.2Functional Food & Beverage Manufacturers

- 5.3.3Dietary Supplement Brands

- 5.3.4Cosmetic & Personal-care Companies

- 5.3.5Academic & Research Institutes

- 5.4By Formulation

- 5.4.1Capsules & Tablets

- 5.4.2Powders & Sachets

- 5.4.3Liquids & Drinks

- 5.4.4Topicals & Creams

- 5.4.5Others

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Seres Therapeutics

- 6.3.2Nestle Health Science

- 6.3.3Yakult Honsha Co.

- 6.3.4DuPont (IFF Health)

- 6.3.5Chr. Hansen Holding A/S

- 6.3.6Danone

- 6.3.7Rebiotix / Ferring

- 6.3.8Vedanta Biosciences

- 6.3.9Second Genome

- 6.3.10Microbiotica

- 6.3.114D pharma

- 6.3.12Siolta Therapeutics

- 6.3.13Finch Therapeutics

- 6.3.14Azitra

- 6.3.15Symrise

- 6.3.16ADM

- 6.3.17BioGaia AB

- 6.3.18Seed Health

- 6.3.19Kanvas Biosciences

- 6.3.20Synlogic

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Microbiome Modulation Market Report Scope

As per the scope of the report, microbiome modulation is the practice of manipulating the microbiome in order to improve gut health and well-being. The microbiome modulation market is segmented into product, application, end-user, and geography. By product, the market is segmented into prebiotics, probiotics, synbiotics, and others. By application, the market is segmented into infectious diseases, gastrointestinal diseases, endocrine and metabolic disorders, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.