Protein Purification And Isolation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

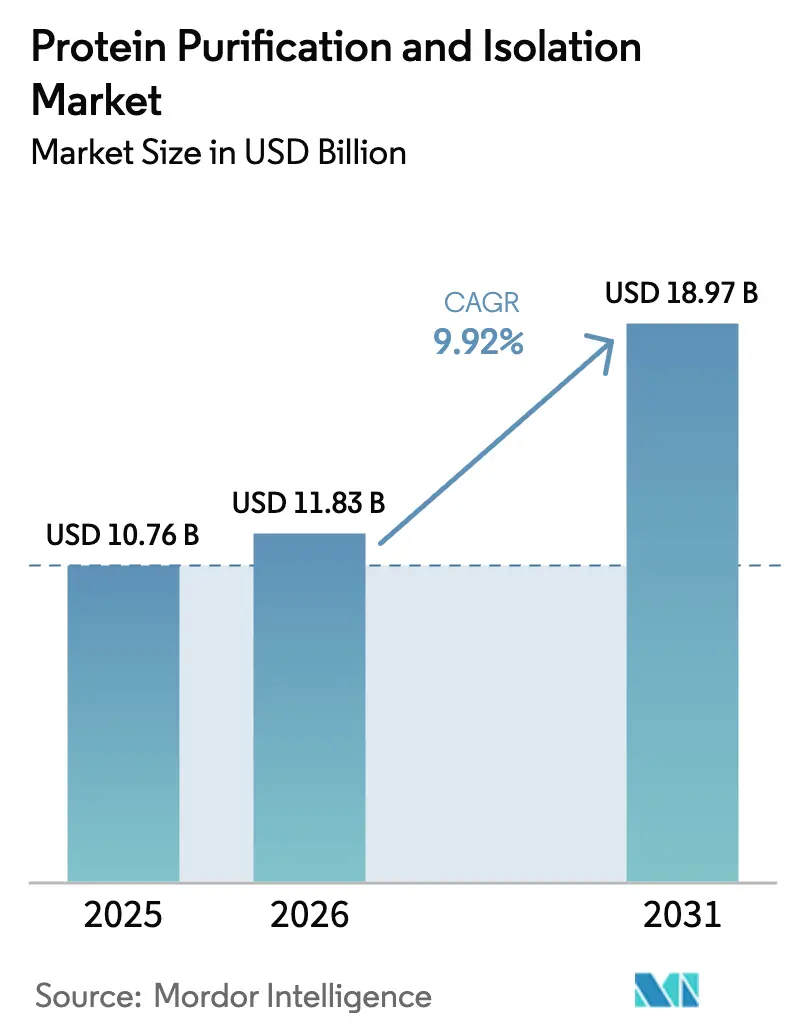

| Market Size (2026) | USD 11.83 Billion |

| Market Size (2031) | USD 18.97 Billion |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

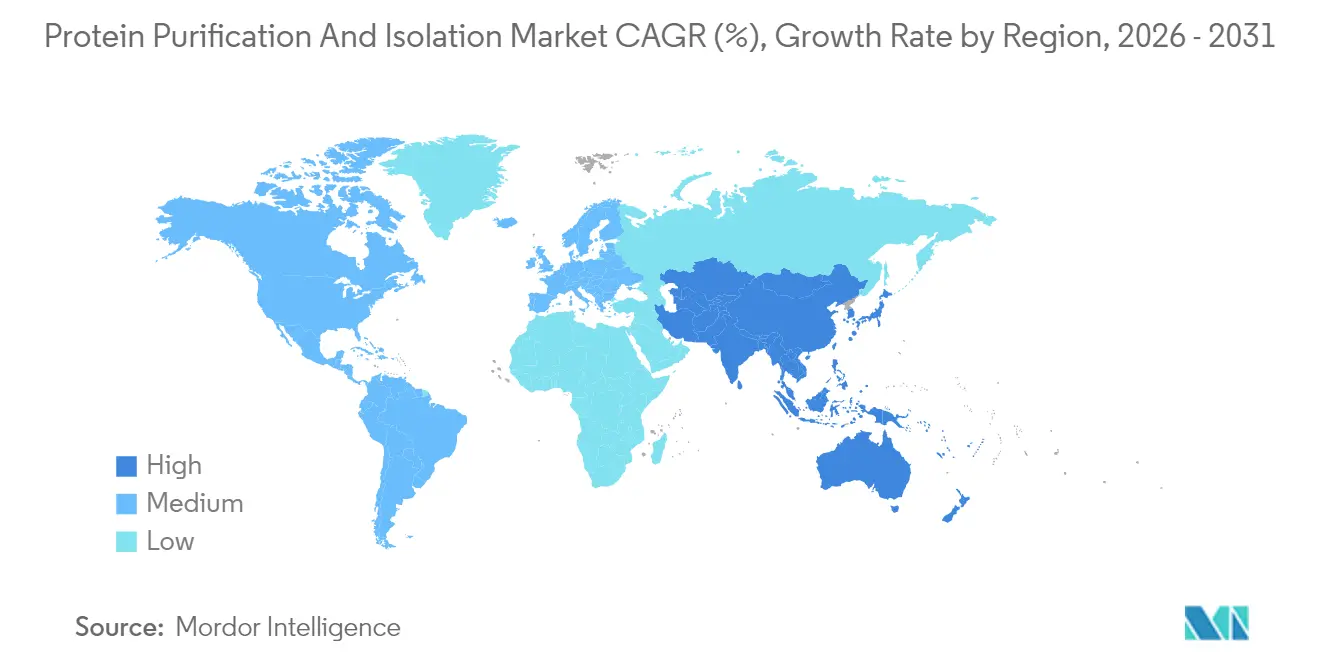

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

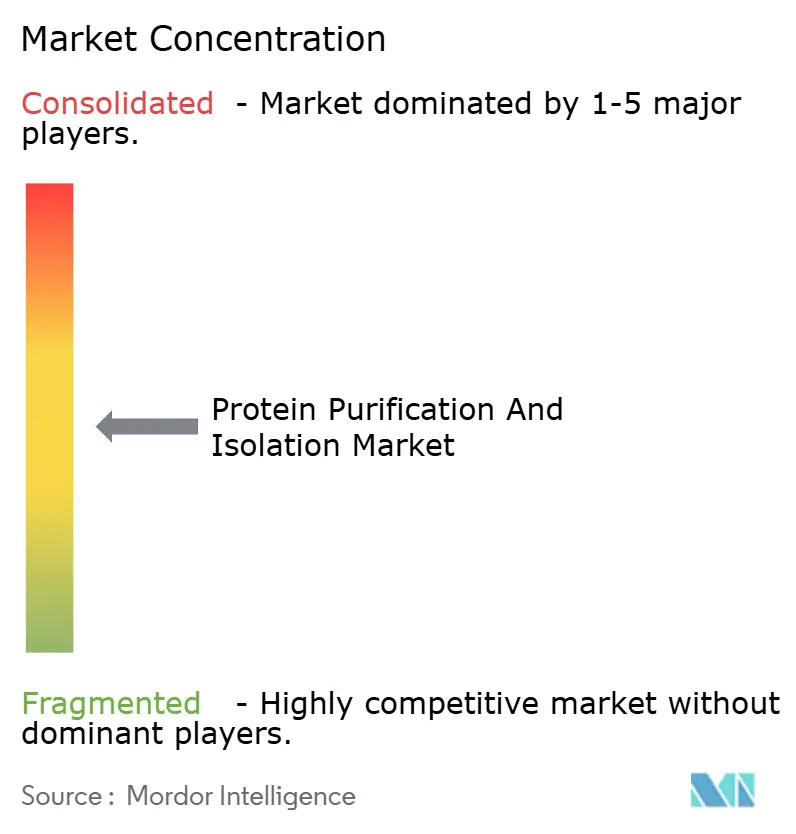

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protein Purification And Isolation Market Analysis by Mordor Intelligence

Protein Purification And Isolation market size in 2026 is estimated at USD 11.83 billion, growing from 2025 value of USD 10.76 billion with 2031 projections showing USD 18.97 billion, growing at 9.92% CAGR over 2026-2031. Continuous biologics pipeline expansion, accelerating cell- and gene-therapy commercialization, and rapid integration of artificial intelligence into downstream processing jointly underpin this trajectory. Intensifying competition among contract development and manufacturing organizations (CDMOs), rising deployment of single-use consumables that curb cross-contamination, and government-backed structural proteomics initiatives further enrich demand. Vendors that align equipment portfolios with continuous processing and data-driven automation gain an edge as quality-by-design approaches become the regulatory norm. At the same time, cost‐efficient manufacturing hubs in Asia-Pacific are changing global capacity allocation, prompting multinational suppliers to localize production footprints and after-sales service.

Key Report Takeaways

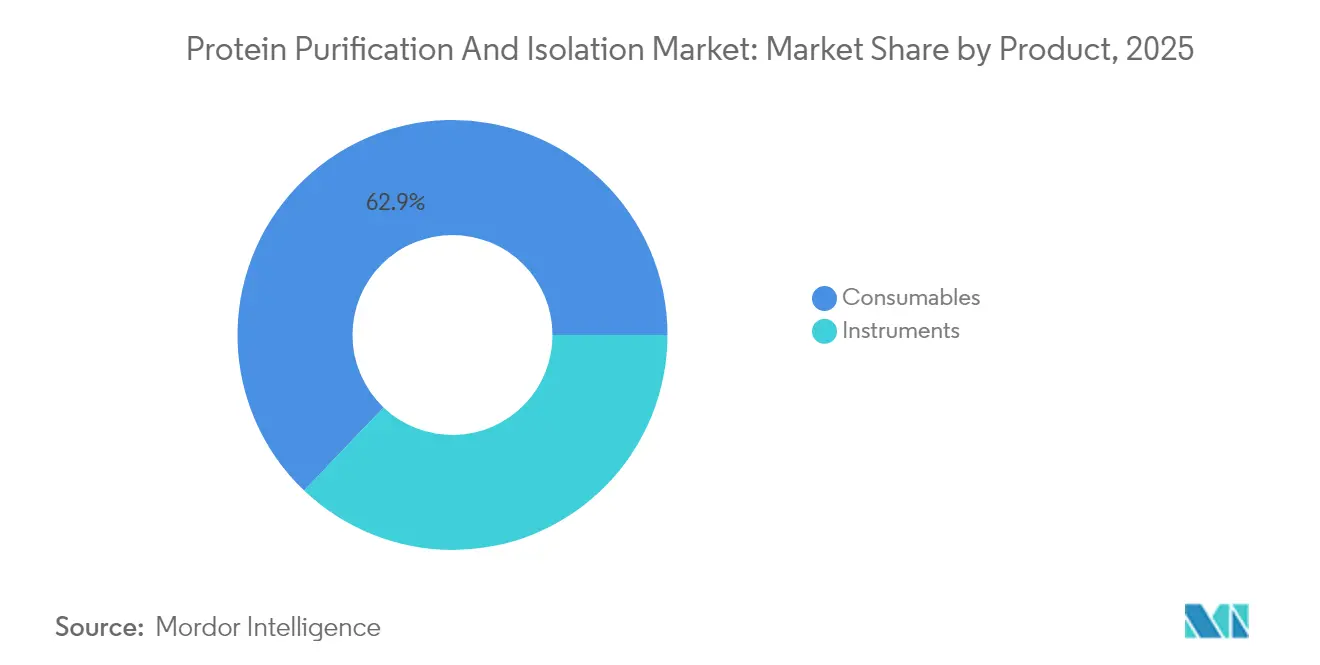

- By product, consumables led with 62.88% revenue share in 2025, while instruments recorded the highest projected CAGR at 11.37% through 2031.

- By technology, chromatography held 32.10% of the protein purification and isolation market share in 2025; ultrafiltration and diafiltration are projected to expand at an 10.90% CAGR to 2031.

- By end-user, academic and research institutes accounted for 42.55% of the protein purification and isolation market size in 2025, whereas CROs/CMOs show the fastest outlook at a 10.75% CAGR.

- By geography, North America commanded 41.95% of 2025 revenue, but Asia-Pacific is forecast to accelerate at an 11.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Purification And Isolation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Monoclonal Antibody and Recombinant Biologics Pipeline | +2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Surge in Cell- & Gene-Therapy Manufacturing Capacity Investments | +1.8% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Growing Demand for High-Throughput, Single-Use Purification Systems | +1.5% | Global | Short term (≤ 2 years) |

| Government Funding for Structural Proteomics Consortia | +1.2% | North America & EU primarily | Medium term (2-4 years) |

| Adoption of Continuous/Chromatographic Intensification Platforms | +0.9% | Developed markets initially, spillover to emerging | Long term (≥ 4 years) |

| AI-Guided Resin and Buffer Selection Software Integration | +0.7% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Monoclonal Antibody and Recombinant Biologics Pipeline

Monoclonal antibody volumes continue to rise at roughly 8% annually, driving demand for Protein A affinity chromatography skids that dominate IgG capture workflows.[1]Source: BioProcess International, “The Secret Life of Protein A,” bioprocessintl.com Fujifilm’s USD 1.2 billion facility in North Carolina adds 160,000 L of bioreactor capacity devoted to antibody production, a scale-up that necessitates proportional downstream investments. The pipeline now spans antibody–drug conjugates and bispecific formats, each introducing unique selectivity challenges that boost demand for high-capacity resins. Standardization of modular skids across sites helps global manufacturers accelerate validation and cut procurement cost. Consequently, suppliers with deep process-development expertise and global support teams capture larger slices of the protein purification and isolation market.

Surge in Cell- & Gene-Therapy Manufacturing Capacity Investments

Biopharma’s pivot toward genetic medicines is reshaping purification needs because viral vectors and plasmid DNA have larger molecular footprints and stricter contamination limits than conventional proteins. Asahi Kasei’s Bionova Scientific opened a Texas site to supply plasmid DNA solutions tailored for these modalities. Manufacturers often lock in three- to five-year capex plans that include chromatography columns designed for large-pore resins and membrane-based harvest technologies. Regulators impose heightened scrutiny on adventitious-agent control, accelerating uptake of sterile, single-use flow paths. As a result, the protein purification and isolation market gains durable revenue streams from both first-of-kind therapies and follow-on capacity expansions.

Growing Demand for High-Throughput, Single-Use Purification Systems

Thermo Fisher’s DynaDrive 5 L single-use bioreactor, launched in April 2025, delivers 27% productivity gains and scales seamlessly to 5,000 L, underscoring how disposables now serve both process-development labs and commercial suites. CDMOs that routinely juggle multi-client portfolios prefer these systems, boosting repeat purchase volumes for bags, filters, and ready-to-use columns. Disposable designs also facilitate regulatory compliance because dedicated flow paths slash the risk of product carryover.

Government Funding for Structural Proteomics Consortia

The National Science Foundation allocated USD 40 million in 2024 toward protein-design research, catalyzing academic demand for high-resolution chromatography and electrophoresis hardware. Grant recipients often purchase standardized purification kits that simplify collaboration across multicenter consortia. Domestic procurement clauses embedded in many public awards boost local suppliers and reduce lead-time uncertainty. Such public–private initiatives feed a steady pipeline of early-stage projects that ultimately transition into commercial therapeutics, thereby reinforcing long-term demand for sophisticated separation platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Downstream Hardware and Facility Retro-Fits | -1.3% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Scarcity of Advanced Purification Talent in Emerging Clusters | -0.8% | APAC emerging markets, Latin America | Medium term (2-4 years) |

| Batch-To-Batch Variability of Affinity Resins Limiting Re-Use | -0.6% | Global | Medium term (2-4 years) |

| Environmental Burden of Single-Use Plastics in Bioprocessing | -0.4% | EU & North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Downstream Hardware and Facility Retro-Fits

Modern chromatography skids often cost USD 0.5–2 million each, and converting a stainless-steel suite into a single-use environment adds incremental infrastructure bills. Small biotechnology firms and manufacturers in cost-sensitive regions frequently delay upgrades, risking capacity bottlenecks. Currency volatility elevates landed cost of imported equipment, while limited access to long-term financing prolongs payback horizons. Consequently, some companies outsource production to well-capitalized CDMOs, shifting equipment demand from buyers to service providers inside the protein purification and isolation market.

Scarcity of Advanced Purification Talent in Emerging Clusters

Rapid greenfield construction in Asia-Pacific and Latin America outpaces workforce development. Continuous chromatography and AI-enabled platforms require interdisciplinary skills that combine classical biochemistry with programming literacy. Experienced practitioners command premiums and gravitate toward mature hubs, leaving greenfield sites dependent on expatriate staff or lengthy training. Talent scarcity slows technology adoption and raises operating costs, indirectly tempering near-term segment growth in the protein purification and isolation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Dominance Driven by Single-Use Adoption

Consumables captured 62.88% of the protein purification and isolation market in 2025 as disposable filters, membranes, ready-to-use columns, and buffer kits became standard for cGMP suites. Kits and reagents sit at the heart of this lead because standardized formulations simplify validation across multi-site networks. Demand is reinforced by global harmonization of microbial-residue limits that favor sterile, pre-gamma-irradiated flow paths. The recurring nature of consumable purchases translates into stable revenue that underwrites supplier R&D.

The instruments segment, though smaller, is set to log an 11.37% CAGR as manufacturers modernize with AI-enabled chromatography systems and inline formulation skids. Capital investment cycles mirror facility build-outs such as Samsung Biologics’ multi-plant expansion in South Korea, which lifts baseline equipment shipments. Vendors linking hardware with digital twins and predictive-maintenance dashboards stand to enlarge their slice of the protein purification and isolation market size for instrumentation.

By Technology: Chromatography Leadership Challenged by Membrane Innovation

Chromatography maintained 32.10% market control in 2025, underpinned by Protein A columns that remain the benchmark for antibody capture. Ion-exchange and mixed-mode formats expand applicability across fusion proteins, enzymes, and plasma-derived products. However, ultrafiltration and diafiltration are speeding ahead at an 10.90% CAGR through novel polymer chemistries that cut buffer consumption and cycle time. Early adopters report cost reductions per gram of protein that swing financial models in favor of membrane-centric trains.

Hybrid platforms that pair flow-through chromatography with high-flux ultrafiltration create flexible trains optimized for titer variability, a growing concern as upstream titers climb. Electrophoresis retains a niche for analytical confirmation, while emerging high-resolution precipitation kits support rapid screening. This diversification helps technology providers broaden revenue opportunities across the protein purification and isolation market.

By End-User: Academic Dominance Yields to Commercial Manufacturing

Academic and research institutes accounted for 42.55% of 2025 revenue, leveraging grant funds such as the NSF award to upgrade core facilities. Universities serve as training grounds, generating operator pipelines that feed pharmaceutical employers. They also pilot early-stage modalities like nanoparticle vaccines, which demand agile purification setups.

CROs and CMOs are poised for the fastest climb at a 10.75% CAGR, mirroring pharma’s trend of outsourcing late-stage development and commercial supply. These organizations aggregate multi-client demand, making them bulk purchasers of columns, sensors, and resins. Their stringent contract turnarounds intensify demand for single-use suites and high-throughput automation, reinforcing the commercial pull within the protein purification and isolation market.

Geography Analysis

North America held 41.95% of global revenue in 2025, supported by seasoned regulators, deep capital markets, and marquee CDMOs. NSF’s USD 40 million protein-design program amplifies academic orders for high-specification chromatographs, reinforcing regional dominance. Novo Nordisk’s USD 4.1 billion expansion in North Carolina confirms the region’s ability to attract mega-projects despite cost-of-labor premiums. Manufacturers operating under FDA oversight often set global purification benchmarks, giving North American suppliers export leverage.

Asia-Pacific is projected to clock an 11.66% CAGR, making it the quickest climber within the protein purification and isolation market. Samsung Biologics’ 360,000 L of capacity across three plants, with a fourth underway, showcases regional scaling power. MilliporeSigma and Cytiva have mirrored customer moves by establishing local resin-packing and equipment-service footprints to curb supply-chain risk. Policy frameworks in China and India further catalyze domestic build-outs, although geopolitical tensions such as the prospective US BioSecure Act could reshape future supply routes.

Europe maintains mature clusters in Germany, Switzerland, and the United Kingdom, underpinned by harmonized regulatory statutes that simplify cross-border equipment validation. Environmental stewardship regulations motivate adoption of continuous processing and low-buffer technologies, opening opportunities for green-chemistry-oriented suppliers. Elsewhere, the Middle East, Africa, and South America register rising interest, particularly where governments fund vaccine sovereignty projects, but inadequate cold-chain and water infrastructure still impede wide-scale uptake.

Competitive Landscape

The protein purification and isolation market is moderately fragmented, with global conglomerates and specialist firms competing on integrated platforms rather than isolated hardware. Thermo Fisher Scientific, and Merck KGaA leverage end-to-end portfolios that span columns, resins, single-use assemblies, and digital analytics. Platform breadth plus global service centers enables quick client onboarding and aftermarket revenue.

Mergers and acquisitions concentrate capabilities. Ecolab’s USD 3.7 billion purchase of Purolite gave it a high-margin resin franchise.[3]Source: BioProcess International, “For Resins, Supply Chain Resilience Is Key,” bioprocessintl.com Thermo Fisher’s USD 4.1 billion filtration acquisition pushed it deeper into buffer management. These moves signal a race toward solution bundles that reduce customers’ supplier counts and simplify regulatory audits.

Niche innovators exploit white spaces in cell- and gene-therapy purification, offering high-throughput viral-vector kits or AI-enabled process software. Although small in revenue, they often command premium pricing thanks to specialized know-how. Larger vendors eye partnerships or bolt-on buys to fill capability gaps, a dynamic that is likely to persist as the protein purification and isolation market adopts increasingly complex therapeutic formats.

Protein Purification And Isolation Industry Leaders

Thermo Fischer Scientific Inc.

Merck KGaA

QIAGEN

Bio-Rad Laboratories, Inc.

Promega Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: FUJIFILM Wako Pure Chemical Corporation has unveiled its latest offerings: the MassivEV EV Purification Column PS and the MassivEV Purification Buffer Set. These products are meticulously crafted to facilitate the meticulous purification of extracellular vesicles (EVs), catering specifically to the burgeoning exosome research field.

- May 2024: CD Bioparticles launched its new Functional Agarose Particles designed for a variety of applications in the field of bioconjugation, isolation, and purification of biomacromolecules. These particles are ideal for researchers working in areas such as protein purification, antibody production, and nucleic acid isolation.

Global Protein Purification And Isolation Market Report Scope

As per the report's scope, protein purification can be defined as a series of steps performed to obtain and study the desired protein from a complex mixture. Protein purification is vital for characterizing the required protein's function, structure, and interactions. The protein isolation aims to safely and efficiently separate the required protein from a mixture. Protein is isolated from samples of mammals, insects, plants, yeasts, or bacteria. The protein purification and isolation market is segmented by Product (Instruments and Consumables), by Technology (Precipitation, Ultrafiltration, Chromatography, Electrophoresis, and Western Blotting), by End User (Academic and Research Institutes, Pharmaceutical and Biotechnological Companies, Contract Research Organizations (CROs), and Hospitals) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Instruments | |

| Consumables | Kits |

| Reagents and Buffers | |

| Columns and Cartridges | |

| Other Products |

| Precipitation | |

| Ultrafiltration and Diafiltration | |

| Chromatography | Ion-Exchange |

| Size-Exclusion | |

| Reverse-Phase | |

| Others | |

| Electrophoresis | Gel Electrophoresis |

| Capillary Electrophoresis | |

| Isoelectric Focusing | |

| Western Blotting and Immunoprecipitation | |

| Other Technologies |

| Academic and Research Institutes |

| Pharmaceutical and Biopharmaceutical Companies |

| Contract Research and Manufacturing Organizations (CROs/CMOs) |

| Hospitals and Diagnostic Labs |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Instruments | |

| Consumables | Kits | |

| Reagents and Buffers | ||

| Columns and Cartridges | ||

| Other Products | ||

| By Technology | Precipitation | |

| Ultrafiltration and Diafiltration | ||

| Chromatography | Ion-Exchange | |

| Size-Exclusion | ||

| Reverse-Phase | ||

| Others | ||

| Electrophoresis | Gel Electrophoresis | |

| Capillary Electrophoresis | ||

| Isoelectric Focusing | ||

| Western Blotting and Immunoprecipitation | ||

| Other Technologies | ||

| By End-User | Academic and Research Institutes | |

| Pharmaceutical and Biopharmaceutical Companies | ||

| Contract Research and Manufacturing Organizations (CROs/CMOs) | ||

| Hospitals and Diagnostic Labs | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the protein purification and isolation market?

The market is valued at USD 11.83 billion in 2026 and is forecast to reach USD 18.97 billion by 2031.

Which product category dominates revenue?

Consumables lead with 62.88% of 2025 revenue thanks to widespread single-use adoption.

Which technology segment is growing the fastest?

Ultrafiltration and diafiltration are projected to register an 10.90% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Large-scale CDMO expansions, cost-efficient labor, and supportive government incentives push the region to an 11.66% CAGR.

What challenges hinder technology adoption in emerging clusters?

High capital costs for advanced hardware and shortages of skilled purification talent slow deployment.

Page last updated on: