Protein A Resin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

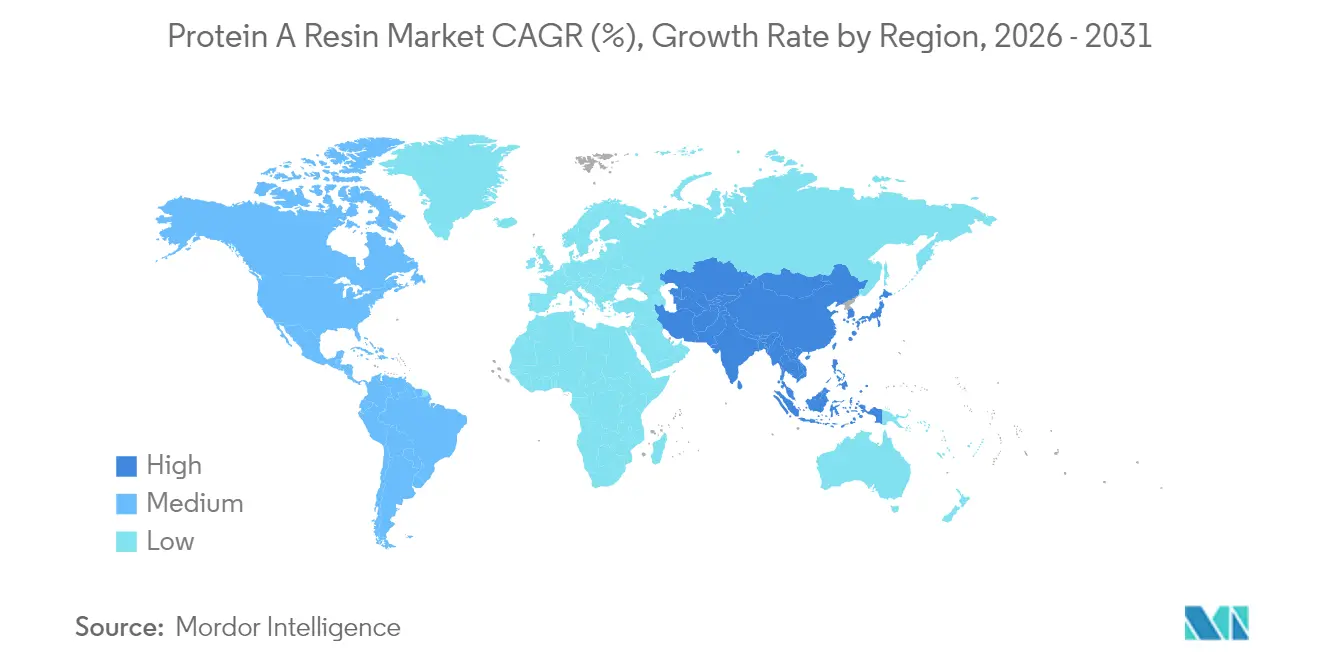

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

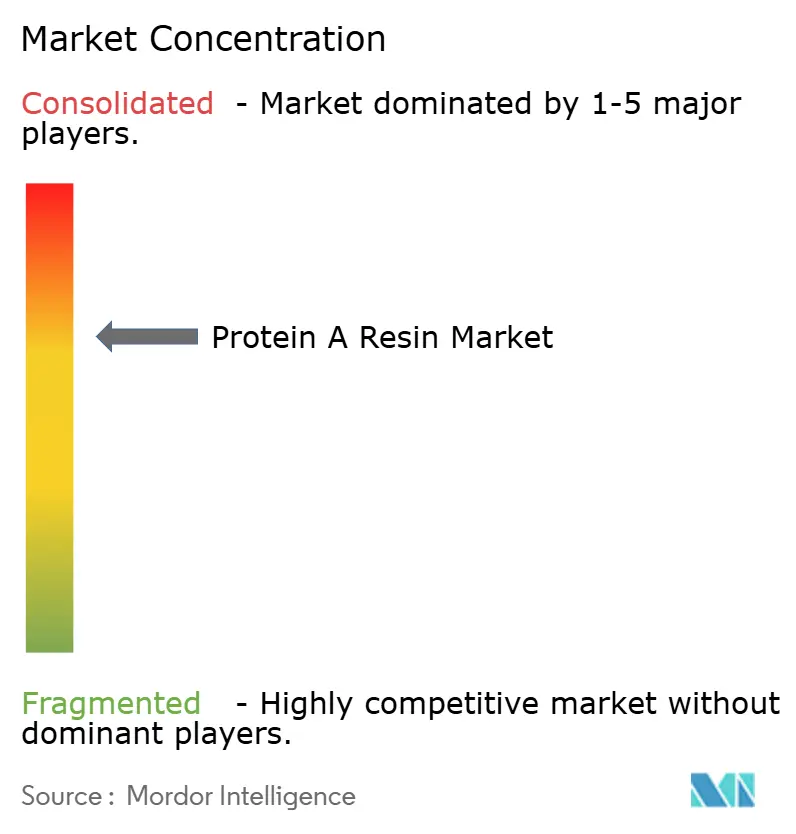

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protein A Resin Market Analysis by Mordor Intelligence

The Protein A Resin Market size was valued at USD 1.27 billion in 2025 and estimated to grow from USD 1.38 billion in 2026 to reach USD 2.08 billion by 2031, at a CAGR of 8.58% during the forecast period (2026-2031). Strong uptake of monoclonal antibody (mAb) therapeutics, rapid biosimilar commercialization, and wider deployment of single-use bioprocessing equipment collectively underpin this expansion. Large-volume antibody manufacturers are scaling capture chromatography capacity in parallel with upstream titer gains, prompting sustained procurement of high-capacity agarose and next-generation fiber matrices. Suppliers are also benefiting from dual-sourcing strategies that biopharma firms have adopted to reduce supply-chain risk, a move that opens incremental opportunities for regional resin producers. Meanwhile, emerging fiber-based adsorbents offering minute-level cycles appeal to process-development groups chasing aggressive productivity targets. Competitive dynamics remain moderate: leading vendors defend share through recombinant-ligand innovations and global regulatory-support programs, yet polymer and fiber challengers are narrowing performance gaps.

Key Report Takeaways

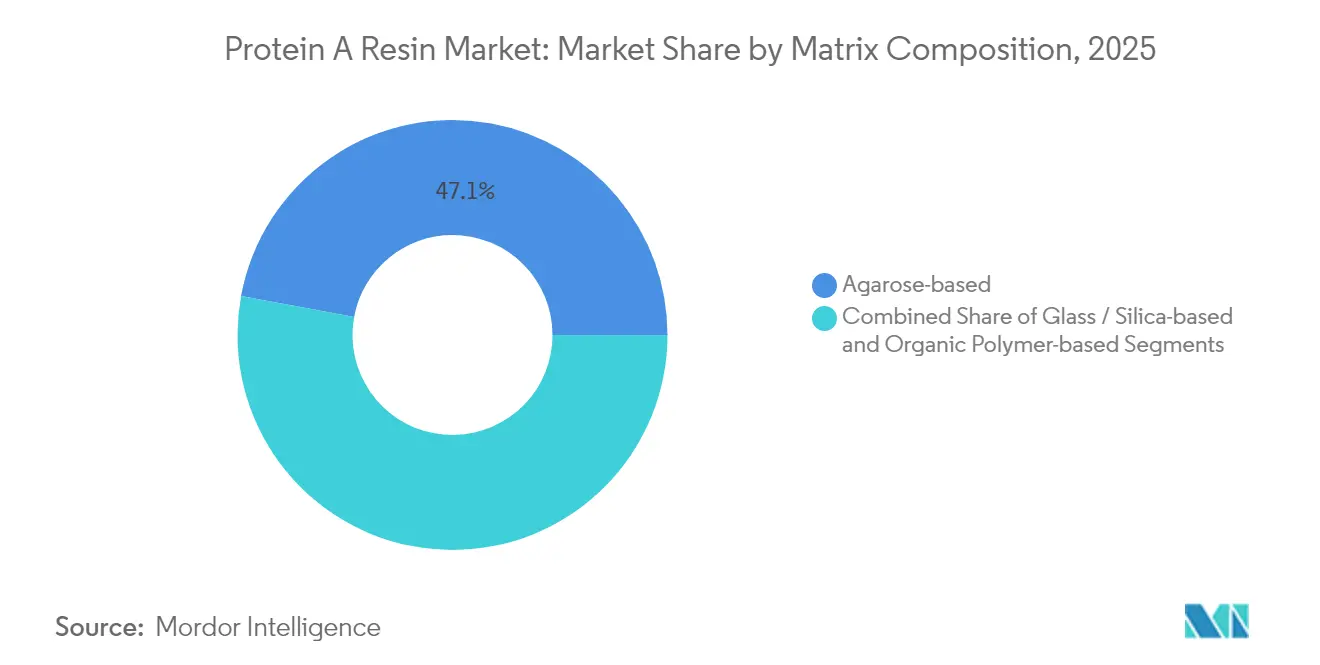

- By matrix composition, agarose commanded 47.10% share of the Protein A resin market size in 2025 and organic polymer-based media are projected to grow at 9.31% CAGR during 2026-2031.

- By ligand source, recombinant Protein A captured 59.10% share of the Protein A resin market size in 2025; natural Protein A is advancing at a 9.55% CAGR to 2031.

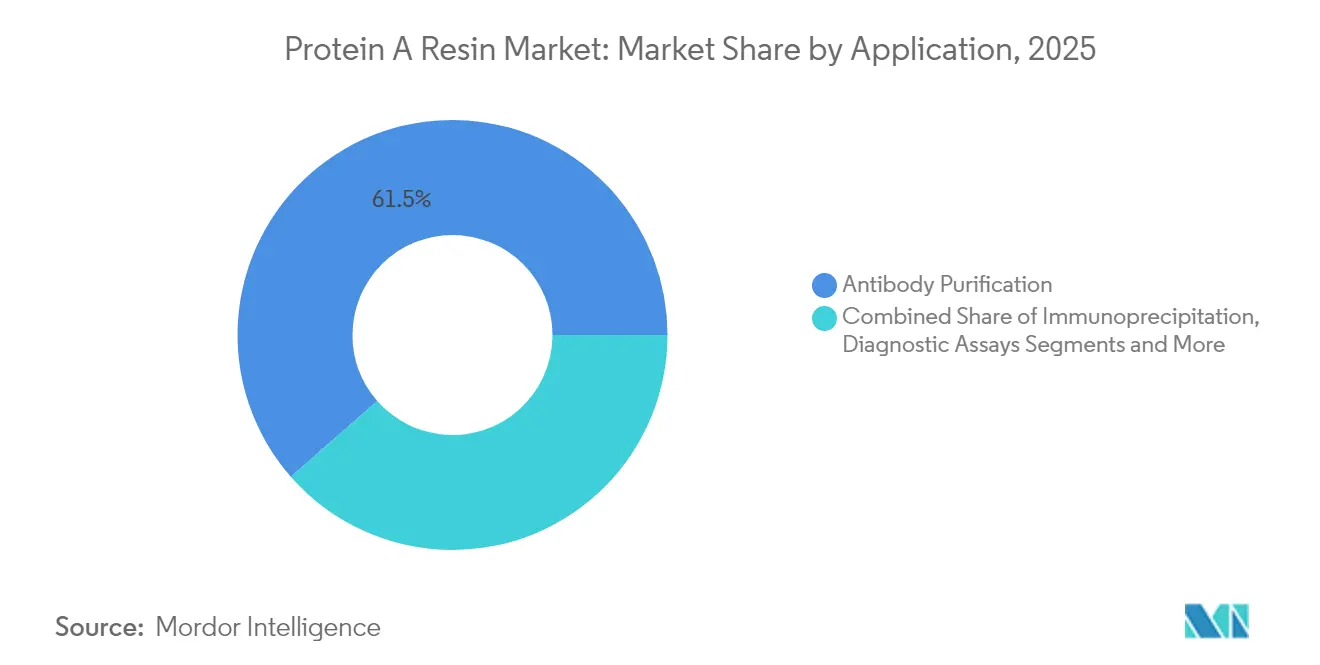

- By application, antibody purification led with 61.45% of Protein A resin market share in 2025, while immunoprecipitation is forecast to expand at a 9.05% CAGR through 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 59.80% of Protein A resin market share in 2025, whereas academic and research institutes are rising fastest at 9.42% CAGR through 2031.

- By geography, North America accounted for 40.50% of Protein A resin market share in 2025 and Asia-Pacific is on track for a 9.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein A Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Monoclonal Antibodies | +2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expansion of Biosimilar Manufacturing Capacity | +1.8% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Growing Adoption of Single-Use Bioprocessing Systems | +1.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Increasing R&D Spending by CDMOs & Big Pharma | +1.3% | Global, with emphasis on North America & APAC | Long term (≥ 4 years) |

| Emergence of Fiber-Based Protein A Media for Rapid Cycles | +0.9% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Dual-Sourcing Strategies to Mitigate Resin Supply-Chain Risk | +0.7% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Monoclonal Antibodies

Global mAb revenue growth continues near 8% per year, triggering new antibody-capture installations and repeat purchases of Protein A adsorbents.[1]Source: BioProcess International, “30 Years of Upstream Productivity Improvements,” bioprocessintl.com Contract manufacturers have responded with large-scale expansions, including a 15,000 L line in Hangzhou that trimmed per-gram costs by nearly 70%. Average upstream titers moved from 0.5 g/L in the 1980s to 2.56 g/L in 2024, raising downstream workload and rewarding high-capacity resins. Emerging bispecifics and antibody-drug conjugates further widen purification demand because each format still relies on Fc-binding capture. Suppliers offering NaOH-tolerant recombinant ligands and high-flow matrices are ideally positioned for these productivity-driven buyers.

Expansion of Biosimilar Manufacturing Capacity

Asia-Pacific manufacturers secure cost advantages and streamlined approval pathways, spurring volume orders for Protein A columns that mirror reference biologic purification standards. Survey data show CMOs and hybrid firms moving from 43% of global biologics capacity in 2024 toward 54% by 2028, concentrating resin demand among a smaller buyer set. Chinese facilities rank top among outsourcing destinations, reinforcing regional pull for resin supply. Harmonized regulations allow standardized purification templates across multiple markets, encouraging suppliers to build logistic hubs near major biosimilar clusters.

Growing Adoption of Single-Use Bioprocessing Systems

Single-use facilities require roughly 40% lower capital outlays than stainless-steel plants and reduce carbon footprints by a similar margin. Integrating disposable Protein A columns eliminates cleaning validation, a key benefit for personalized therapy developers with small campaign volumes. Pre-packed columns and membrane adsorbers arrive sterile and ready, shortening facility turnarounds while ensuring segregation of multi-product suites. The trend supports modular plant concepts and increases demand for cartridge-format resins that fit gamma-irradiated flow paths.

Increasing R&D Spending by CDMOs & Big Pharma

Public-sector grants continue to prime private R&D investment; economic modeling shows a 25% cut to public funding could slice U.S. GDP by 3.8%, underscoring government influence on pipeline health. University–industry alliances multiply, boosting procurement of research-grade Protein A media for candidate screening. CDMOs invest in process-development labs, adopting rapid-cycle adsorbents that support parallel experimentation. Collectively, higher R&D outlays translate to steady baseline consumption of smaller-volume, higher-value resins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Agarose-Based Resins | -1.4% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Ligand Leaching & Regulatory Validation Burdens | -1.1% | Global, with stricter enforcement in North America & Europe | Long term (≥ 4 years) |

| Competitive Threat from Alternative Affinity Ligands | -0.8% | Global, led by innovation hubs in North America & Europe | Medium term (2-4 years) |

| Sustainability Pressures on Mineral-Oil Jetting Processes | -0.5% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Agarose-Based Resins

Premium agarose adsorbents can represent more than 50% of consumable costs in a mAb campaign, straining budgets for small biotech and biosimilar firms.[2]Source: Frontiers in Bioengineering and Biotechnology, “Chromatography consumables cost,” frontiersin.org Cost-sensitive buyers evaluate polymer or membrane alternatives, or attempt resin recycling—adding complexity to validation. Contract manufacturers absorb part of this burden but pass charges through to clients. Suppliers respond with higher-capacity beads to reduce grams of resin per gram of product, yet price hurdles persist in markets with limited capital access.

Ligand Leaching & Regulatory Validation Burdens

FDA guidance on extractables and leachables and EMA process-validation updates intensify analytical scrutiny of Protein A residuals. Demonstrating ligand clearance demands orthogonal assays, lengthening development timelines and adding expense for smaller sponsors. Recombinant ligands with enhanced NaOH resistance mitigate leaching but still require equivalence dossiers. Established vendors leverage regulatory-support files to ease adoption, whereas new entrants face steeper qualification obstacles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Matrix Composition: Agarose Dominance Faces Polymer Innovation

Agarose media captured 47.10% of Protein A resin market share in 2025, buoyed by decades of regulatory acceptance and robust binding capacity. Within this group, recombinant-ligand variants supporting 0.5 M NaOH cleaning secure longer lifecycles, reducing per-gram costs and reinforcing loyalty. The Protein A resin market size tied to agarose formats is projected to grow steadily as blockbuster mAb volumes rise, yet polymer beads are encroaching due to superior pressure tolerance.

Organic polymer matrices, expanding at 9.31% CAGR, allow higher linear flow rates, trimming column footprints in space-constrained suites. Manufacturers tout hydrophilic coatings that curb non-specific binding while maintaining >50 g/L capacity. Fiber and silica chemistries remain niche but illustrate the sector’s appetite for productivity leaps. As users retrofit facilities, many adopt hybrid strategies: agarose for legacy products and polymer or fiber platforms for new assets, spreading spend across technology classes.

By Ligand Source: Recombinant Protein A Strengthens Market Position

Recombinant ligands held 59.10% share in 2025 as drug makers prioritized batch consistency, reduced adventitious-agent risk, and higher caustic stability. The Protein A resin market size attributable to recombinant platforms will rise further because emerging high-titer processes impose harsher cleaning protocols that native ligands cannot withstand.

Natural Protein A, though growing 9.55% CAGR, serves specialized R&D or diagnostic applications where authentic binding kinetics matter more than caustic durability. Suppliers engineer plant-derived production routes to sidestep animal-origin concerns, yet still face lot-variability challenges. In commercial manufacturing, stringent validation steers users to recombinant versions bundled with exhaustive leachables data, an advantage hard to replicate for newcomers.

By Application: Antibody Purification Drives Market Expansion

Antibody capture accounted for 61.45% of Protein A resin's market share in 2025, the most significant slice of the market. New drug approvals and indication expansions sustain this volume, while next-generation modalities (bispecifics, ADCs) largely retain Fc regions, ensuring continued reliance on Protein A.

Immunoprecipitation, set for a 9.05% CAGR, benefits from academic funding and high-throughput proteomics that consume small pre-packed columns. Diagnostic assay developers demand ever-tighter ligand leaching specs, fostering micro-scale resin variants with stringent QC certificates. Collectively, application diversification insulates the Protein A resin market from lifecycle dips in any single therapeutic class.

By End User: Pharma Leadership with Academic Acceleration

Commercial manufacturers controlled a 59.80% share in 2025, underpinning the bulk of recurring bulk resin orders that define the Protein A resin market. Their priorities revolve around column lifetime, supply security, and regulatory support. The Protein A resin industry also observes CDMOs increasing share as outsourcing momentum accelerates.

Academic and research institutes, expanding at a 9.42% CAGR, elevate demand for smaller cartridge formats and rapid-cycle fibers suited to parallel screening. Grant-funded labs value up-front cost and ready-to-use convenience over ultrahigh binding, prompting vendors to offer flexible pack sizes. Diagnostic labs, though niche, are exploring continuous capture to improve reagent throughput, an adjacent growth pocket for sophisticated resin chemistries.

Geography Analysis

North America commanded 40.50% of Protein A resin market share in 2025, aided by USD 1 billion-plus capacity builds from Amgen and a USD 1.2 billion CDMO expansion by Fujifilm in North Carolina. The region’s stringent FDA oversight elevates recombinant-ligand adoption and rewards suppliers offering comprehensive DMF support. Federal initiatives that link public R&D to domestic manufacturing further fortify local demand for high-performance resins.

Asia-Pacific is the fastest-growing arena, charting a 9.82% CAGR to 2031 as China consolidates its role as an outsourcing powerhouse and governments push self-sufficiency. WuXi Biologics’ 15,000 L PPQ milestone in Hangzhou signals large-scale technical maturity, stimulating broader uptake of advanced adsorbents. Regional suppliers are investing in local bead production to sidestep import duties and shorten lead times, yet multinational vendors still dominate complex ligand chemistries.

Europe retains a sizeable installed base but faces evolving GMP Annex 1 directives that tighten contamination control expectations. Sustainability mandates are reshaping procurement, causing buyers to scrutinize mineral-oil usage and resin recyclability. Vendors with verified low-carbon jetting processes gain a competitive edge. Secondary markets in South America, the Middle East, and Africa show emerging activity through technology-transfer pacts and government-backed biopark initiatives, but presently generate limited volume.

Competitive Landscape

Global competition is moderately concentrated, with Cytiva and Thermo Fisher Scientific collectively controlling a meaningful portion of the Protein A resin market share through broad portfolios and global service networks. Product innovation remains the primary differentiator: Cytiva’s PrismA fibers offer ten-fold productivity jumps, whereas Thermo Fisher leverages recombinant Poros ligands to extend caustic tolerance. Repligen pursues acquisitive growth, including its 2024 purchase of chromatography innovator Tantti to deepen modal diversification.

Strategic partnerships surface as an avenue to blend ligand expertise with bead fabrication know-how. Ecolab’s USD 3.7 billion acquisition of Purolite delivered immediate scale and proprietary jetted-bead technology, showcased in the 50-micron AP+50 launch that promises record binding per liter. Similarly, the Ecolab-Repligen DurA Cycle affinity resin collaboration enables longer operational lifetimes for large-scale plants.

Barriers to entry hinge on regulatory files, ligand IP, and supply reliability rather than manufacturing capex alone. Polymer and fiber challengers are nibbling at share, yet must overcome entrenched customer validation data sets. The competitive set increasingly markets sustainability credentials to satisfy ESG procurement filters, adding a new battlefield alongside conventional quality and cost metrics.

Protein A Resin Industry Leaders

Bio-Rad Laboratories, Inc.

Merck KGaA

Agarose Bead Technologies

Danaher Corporation (Cytiva)

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ecolab Life Sciences introduced Purolite AP+50, a 50-micron jetted affinity resin offering the highest dynamic binding capacity in its platform and shorter lead times.

- September 2024: JSR Life Sciences unveiled Amsphere A+ next-generation Protein A resin at the BioProcess International Conference, Boston.

- February 2024: Purolite and Repligen launched Praesto CH1, a 70 µm agarose resin tailored for bispecific mAbs

- January 2024: Calluna Pharma emerged from the merger of Dutch Oxitope and Norwegian Arxx after raising USD 80.4 million to advance the monoclonal antibody CAL101.

Global Protein A Resin Market Report Scope

As per the scope of the report, protein A resin is an affinity chromatography medium designed for easy, one-step purification of classes, subclasses, and fragments of immunoglobulins from biological fluids and cell culture media.

The Protein A Resin market is segmented by product type, application, end user, and geography. By product type, the market is segmented into agarose-based protein, glass or silica-based protein, and organic polymer-based protein. By application, the market is segmented into antibody purification and immunoprecipitation. By end user, the market is segmented into pharmaceutical and biopharmaceutical companies, research laboratories, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the values (USD) for all the above segments.

| Agarose-based |

| Glass / Silica-based |

| Organic Polymer-based |

| Natural Protein A |

| Recombinant Protein A |

| Antibody Purification |

| Immunoprecipitation |

| Diagnostic Assays |

| Other Applications |

| Pharmaceutical & Biopharmaceutical Companies |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Academic & Research Institutes |

| Clinical Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Matrix Composition | Agarose-based | |

| Glass / Silica-based | ||

| Organic Polymer-based | ||

| By Ligand Source | Natural Protein A | |

| Recombinant Protein A | ||

| By Application | Antibody Purification | |

| Immunoprecipitation | ||

| Diagnostic Assays | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biopharmaceutical Companies | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Academic & Research Institutes | ||

| Clinical Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Protein A resin market in 2026?

The Protein A resin market size is USD 1.38 billion in 2026.

What is the expected CAGR for Protein A resins through 2031?

The market is forecast to post an 8.58% CAGR between 2026 and 2031.

Which region is growing fastest for Protein A resin demand?

Asia-Pacific leads with a projected 9.82% CAGR over the forecast period.

Which application segment dominates Protein A resin consumption?

Antibody purification holds the largest share at 61.45% in 2025.

What is the main technological shift influencing future resin selection?

Adoption of fiber-based Protein A media that cut cycle times to minutes is reshaping purification strategies.

Page last updated on: