Prosthetic Disc Nucleus Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

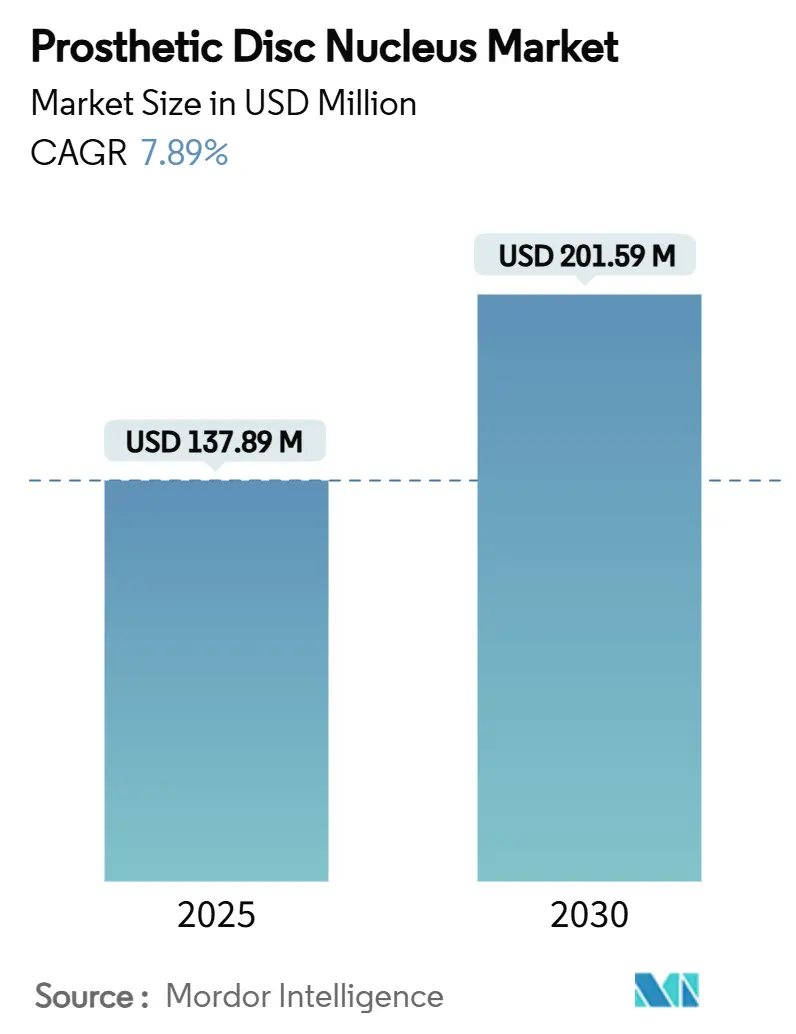

| Market Size (2025) | USD 137.89 Million |

| Market Size (2030) | USD 201.59 Million |

| Growth Rate (2025 - 2030) | 7.89% CAGR |

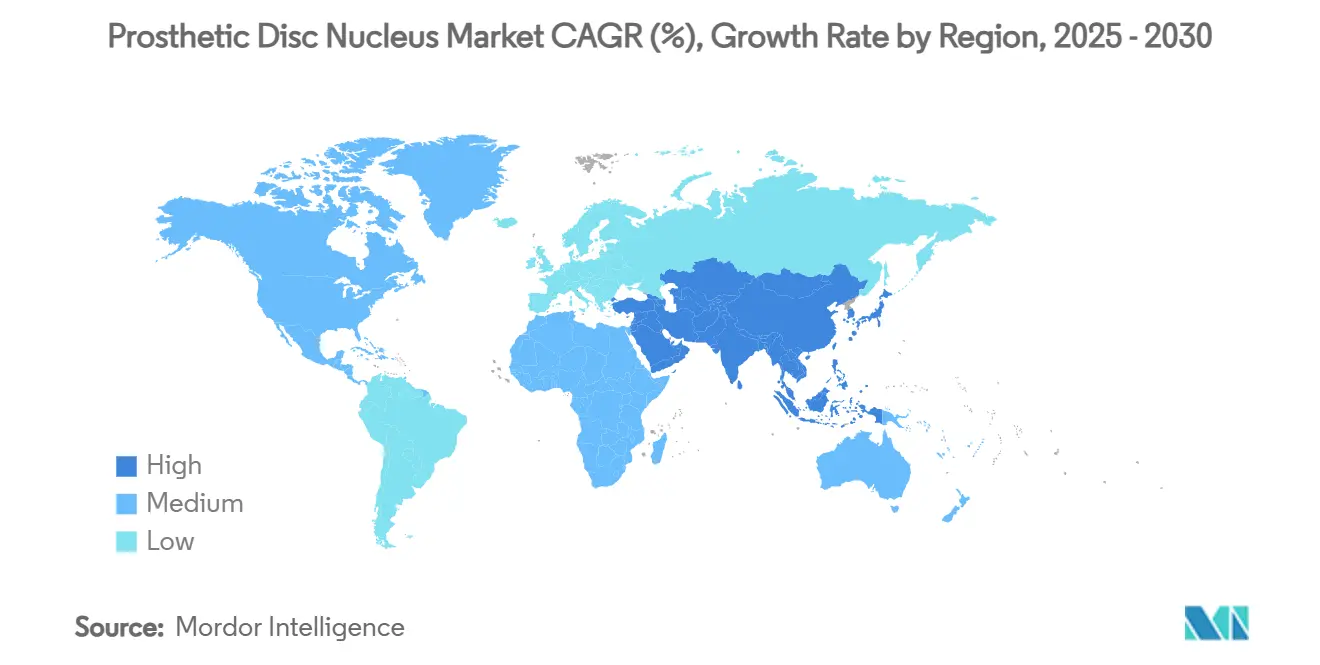

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

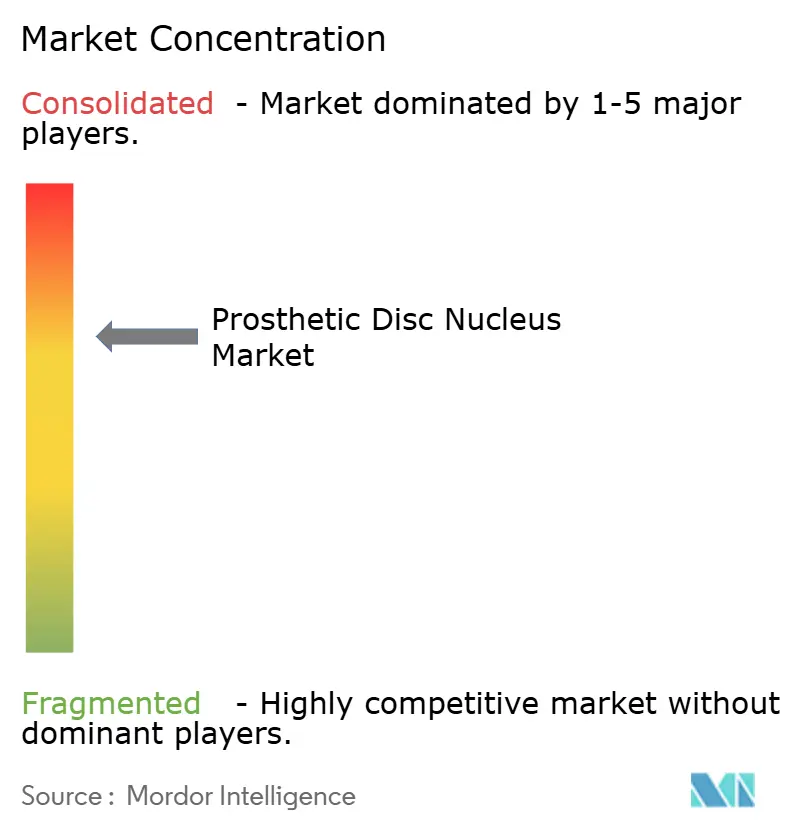

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prosthetic Disc Nucleus Market Analysis by Mordor Intelligence

The global prosthetic disc nucleus market size stands at USD 137.89 million in 2025 and is forecast to reach USD 201.59 million by 2030, expanding at a 7.89% CAGR during the period. Momentum stems from the transition of nucleus replacement from experimental practice to mainstream motion-preservation surgery. Hydrogel innovations now reproduce native biomechanical properties with fewer subsidence events, while FDA breakthrough designations shorten time-to-market for next-generation implants. Growing surgeon familiarity with percutaneous approaches is helping outpatient centers deliver same-day discharges, and favorable coverage determinations in the United States and Europe are lowering patient out-of-pocket costs. Meanwhile, Asia-Pacific hospitals are installing navigation platforms that extend minimally invasive techniques to large, underserved populations.

Key Report Takeaways

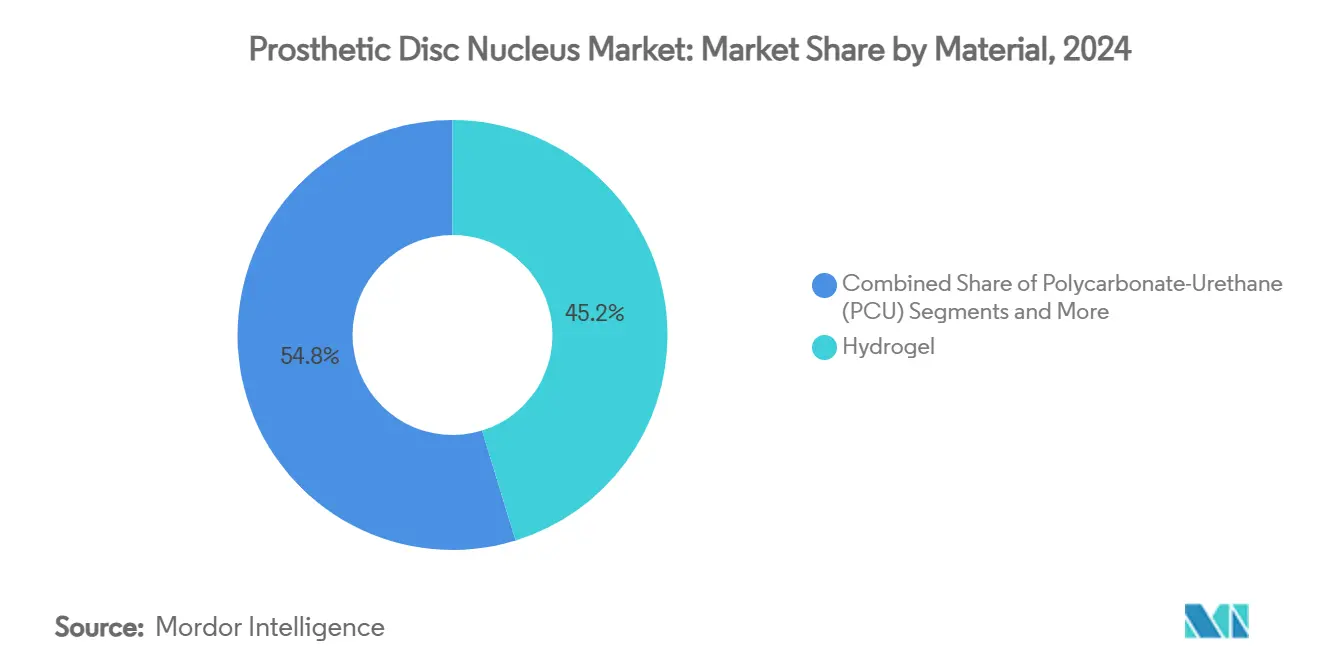

- By material, hydrogel devices captured 45.24% of the prosthetic disc nucleus market share in 2024 and are forecast to expand at an 11.77% CAGR through 2030.

- By surgery approach, minimally invasive percutaneous nucleus replacement commanded 59.66% of the prosthetic disc nucleus market share in 2024 and is projected to post an 11.94% CAGR to 2030.

- By delivery modality, pre-formed solid implants accounted for 53.48% of the prosthetic disc nucleus market size in 2024, while injectable hydrogel devices represent the fastest-growing modality at a 10.37% CAGR through 2030.

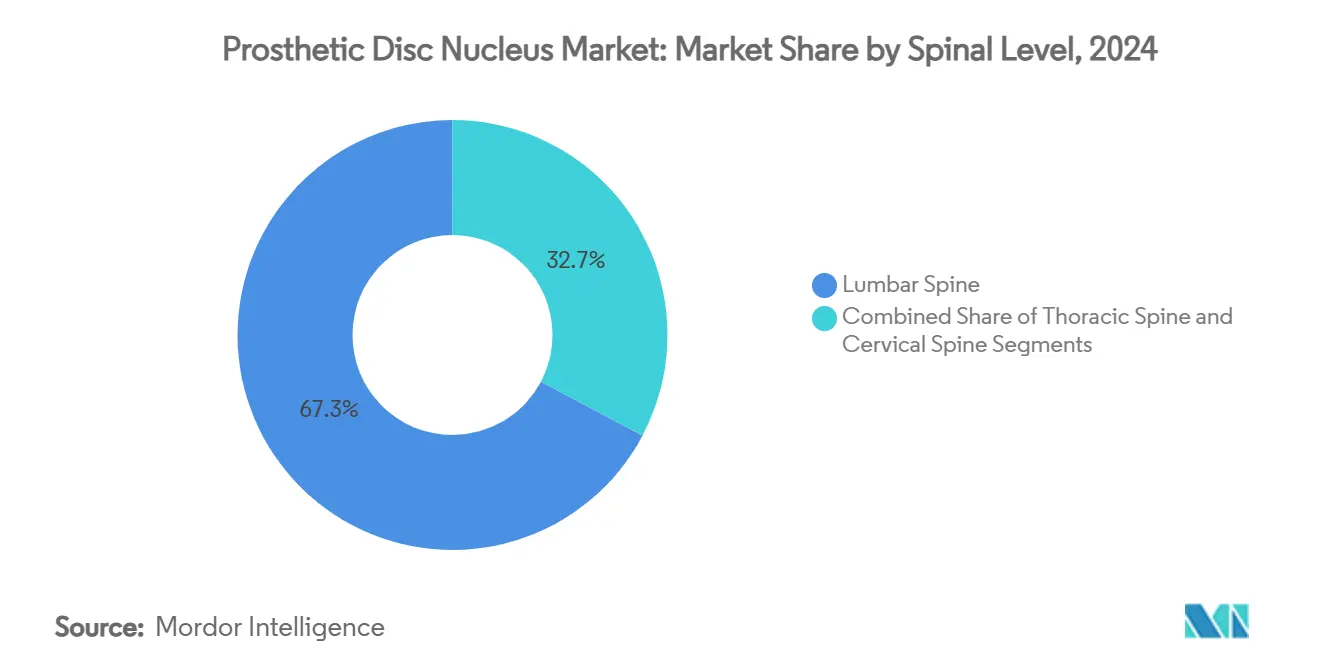

- By spinal level, lumbar applications dominated with 67.26% prosthetic disc nucleus market share in 2024; cervical indications are poised to grow at a 9.29% CAGR up to 2030.

- By end user, hospitals held 49.27% revenue share of the prosthetic disc nucleus market size in 2024, whereas ambulatory surgical centers exhibit the highest momentum with a 10.04% CAGR through 2030.

- By geography, North America led with 37.56% prosthetic disc nucleus market share in 2024, while Asia-Pacific is expected to advance at a 10.48% CAGR during the forecast window.

Global Prosthetic Disc Nucleus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of degenerative disc disease | +2.1% | Global—highest in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of minimally invasive spine surgery techniques | +1.8% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Favorable reimbursement expansions for motion-preservation devices | +1.4% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Surge in outpatient spine procedures at ambulatory surgical centers | +1.2% | North America core, spill-over to developed APAC | Short term (≤ 2 years) |

| Hydrogel-based 3D-printable nucleus prototypes entering trials | +0.9% | Global—early adoption in North America & EU | Long term (≥ 4 years) |

| FDA breakthrough device designations accelerating reviews | +0.5% | US primarily, ripple effects worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Degenerative Disc Disease

Degenerative disc disease (DDD) continues to affect millions of adults, with high-quality epidemiological work showing a persistent rise among aging populations. In the United States the annual economic burden associated with DDD-related low back pain reaches USD 118.8 billion, creating sustained demand for motion-preserving alternatives to fusion.[1]Centers for Medicare & Medicaid Services, “LCD – Intervertebral Disc Repair,” cms.gov Younger patients diagnosed earlier through advanced imaging increasingly prefer nucleus replacement because it retains segmental mobility and may delay adjacent-level disease progression.[2]Eric M. Teichner, “The Advancement and Utility of Multimodal Imaging in the Diagnosis of Degenerative Disc Disease,” Frontiers in Radiology, frontiersin.org Together these factors underpin long-term volume growth for prosthetic disc nucleus market procedures.

Growing Adoption Of Minimally Invasive Spine Surgery Techniques

Medicare claims indicate a steady shift of lumbar and cervical cases to ambulatory settings between 2010 and 2024, underscoring the appeal of less invasive methods.[3]Alex K. Miller et al., “Growing Utilization of Ambulatory Spine Surgery in Medicare Patients,” NASS Open Access Journal, nassopenaccess.org Unilateral biportal endoscopy and similar techniques achieve adequate decompression with smaller incisions, lower blood loss, and quicker return to work, aligning well with nucleus implants that require limited annular windows.[4]Malcolm Pestonji et al., “Cervical Myeloradiculopathy Treated by Unilateral Biportal Endoscopic Decompression,” Journal of Minimally Invasive Spine Surgery, jmisst.org Robotic guidance—currently available to 18% of surgeons—improves cannula placement accuracy, although high capital cost remains an adoption barrier. Immersive virtual-reality simulators are shortening learning curves for fellows, widening the pool of credentialed physicians who can offer nucleus replacement in routine practice.

Favorable Reimbursement Expansions For Motion–Preservation Devices

Local Coverage Determinations now list CPT codes that treat cervical and lumbar arthroplasty as medically necessary when specific criteria are met. United Healthcare mirrored this policy by updating its Medicare Advantage summaries in early 2024, markedly shortening authorization cycles. Five-year cost-utility analysis further shows cervical disc replacement delivering superior quality-adjusted life-year gains at lower cumulative cost than fusion, bolstering the economic rationale for payers. These shifts collectively enhance commercial traction for prosthetic disc nucleus market devices.

Surge In Outpatient Spine Procedures At Ambulatory Surgical Centers

Spine procedures newly added to the ASC-approved list—including anterior cervical discectomy—have experienced double-digit volume growth, signalling payer acceptance of outpatient complex cases. Protocols combining regional anesthesia and multimodal non-opioid pain control allow many nucleus replacement patients to ambulate within hours and leave the facility the same day. Navigation platforms designed for office-based sacroiliac fusion illustrate how high-acuity spinal interventions are migrating from hospitals to physician-owned suites. Because percutaneous nucleus delivery uses small trocar diameters, it is particularly well-suited to this setting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & procedure cost relative to lumbar fusion | -1.8% | Global—most pronounced in price-sensitive markets | Medium term (2-4 years) |

| Stringent long-term safety evidence requirements | -1.2% | Global—led by FDA & EMA | Long term (≥ 4 years) |

| Limited surgeon training outside tier-1 centers | -0.9% | Global—strongest in emerging markets | Medium term (2-4 years) |

| Implant expulsion & subsidence risk in osteoporotic bone | -0.6% | Developed economies with aging populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Cost Relative To Lumbar Fusion

Hospitals report that implant pricing can exceed USD 5,000 per level—roughly 30% of total encounter expenses—and payers scrutinize these charges despite lower revision rates over time. Where reimbursement policy is immature, patients are asked to shoulder significant co-payments, discouraging uptake in middle-income countries. Comparative cost-effectiveness studies of posterior lumbar interbody fusion show thresholds around USD 29,511 per QALY, creating a tough economic benchmark for new nucleus devices to match. Group purchasing organizations in North America are therefore negotiating price caps that compress distributor margins.

Stringent Long-Term Safety Evidence Requirements By Regulators

The FDA commonly asks for 5-to-10-year follow up on wear, migration and reoperation rates, dramatically extending development budgets compared with pedicle-based fixation devices. Historical concerns—such as the 34% revision incidence reported for one cervical prosthesis—keep regulators cautious and may trigger post-market surveillance mandates. European Notified Bodies apply parallel rigor under MDR, requiring exhaustive mechanical durability data even for minor material changes. These hurdles slow portfolio refresh cycles and favor incumbents with ample clinical resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Hydrogel Dominance Drives Innovation

Hydrogel implants captured 45.24% of prosthetic disc nucleus market share in 2024, benefiting from swelling pressure that restores disc height without excessive stiffness. The hydrogel segment is forecast to post an 11.77% CAGR to 2030, outpacing polycarbonate-urethane and silicone alternatives. Preclinical work on radiopaque granular hydrogels shows preserved disc height at 12 months in ovine models. The emergence of 3D-printable composites allows surgeons to tailor modulus gradients, and composite sealants bond firmly to annulus tissue, limiting extrusion risk.

A steady installed base of polycarbonate-urethane implants provides durability data beyond 15 years, keeping this material attractive for multi-level reconstructions. Silicone variants occupy niche trauma and tumor resection settings where chemical inertness is critical. Over the forecast, hydrogel exemplars such as ReGelTec’s HYDRAFIL and injectable alginate scaffolds are expected to shift perceptions from static cushioning to biologically interactive regeneration, bolstering prosthetic disc nucleus market size adoption rates.

By Surgery Approach: Minimally Invasive Techniques Lead Market Evolution

Minimally invasive percutaneous access maintained 59.66% share of the prosthetic disc nucleus market size in 2024 as surgeons pursued faster mobilization and lower infection exposure. The technique’s 11.94% CAGR reflects rising use of tubular retractors and fluoroscopy-guided cannula systems in outpatient suites. Studies confirm that unilateral endoscopic corridors reduce paraspinal muscle trauma and opioid prescriptions post-operatively. Robotic alignment tools, while limited in penetration, enhance trajectory planning and reduce radiation exposure.

Conventional open or mini-open discectomy remains indispensable for revisions or severe foraminal stenosis where broader visualization is critical. Nevertheless, single-level cases trend toward ambulatory execution, aligning with payer objectives for site-of-care optimization. Training curricula are evolving quickly: virtual reality modules improved novice screw placement accuracy by 26% over six sessions, implying rapid scale-up potential for percutaneous nucleus procedures.

By Delivery Modality: Injectable Systems Gain Clinical Momentum

Pre-formed solid plugs held 53.48% share of the prosthetic disc nucleus market in 2024 due to long familiarity and predictable handling. Yet injectable hydrogels are slated to register a 10.37% CAGR, buoyed by smaller incision requirements and patient-specific conformity. Early feasibility data on ultra-purified alginate gel implants revealed significant visual analogue score reductions at 6 months versus discectomy controls. Expandable articulating devices remain a niche for complex deformity corrections where height restoration must exceed 6 mm.

Manufacturers aim to combine injectable delivery with in situ polymerization to seal annular tears; mechanically tough self-healing hydrogels already demonstrate sustained compressive modulus after 10 million cycles. Regulatory guidance now classifies many injectable matrices as Class III, necessitating IDE pathways but rewarding innovators with differentiated IP positions in the prosthetic disc nucleus market.

By Spinal Level: Lumbar Applications Drive Volume Growth

The lumbar spine contributed 67.26% of prosthetic disc nucleus market share in 2024, reflecting high DDD incidence in weight-bearing segments. Injectable allograft supplementation has achieved 43% mean back-pain improvement and 50% Oswestry Disability Index reduction at 2 years, sustaining clinical enthusiasm. Demand remains strong because many patients seek to avoid fusion that could accelerate adjacent-level degeneration.

Cervical indications, while representing a smaller installed base, are predicted to grow at 9.29% CAGR through 2030 as device footprints and kinematic profiles refine. Caution persists after reports of osteolysis-related revisions with earlier cervical discs, but new coatings aim to reduce particulate wear. Thoracic nucleus replacement remains limited to trauma sequelae and oncologic resections given the segment’s lower degenerative burden.

By End User: Ambulatory Centers Drive Market Transformation

Hospitals retained 49.27% share in 2024, supported by ICU resources for complex multilevel pathology. Yet ambulatory surgical centers are growing at 10.04% CAGR as payers incentivize site-neutral payments. Office-based navigation platforms make nucleus replacement feasible in boutique settings, broadening patient access. Specialist spine clinics remain pivotal for high-volume degenerative disease, often contracting dedicated implant inventories that streamline case turnover.

Enhanced recovery after surgery protocols—incorporating regional blocks and early mobilization—have cut average length of stay to under 8 hours for single-level lumbar nucleus cases. Such efficiencies align with value-based reimbursement, positioning ASCs as growth engines for the prosthetic disc nucleus market.

Geography Analysis

North America generated 37.56% of prosthetic disc nucleus market revenue in 2024, fueled by sophisticated imaging, high procedure reimbursement, and a robust clinical-trial ecosystem. CMS coverage expansions and multiple FDA breakthrough designations have shortened commercialization timelines for startups, while mature players leverage distributor networks to penetrate ASC channels. Venture investment remains active, highlighted by Nevro’s USD 250 million acquisition by Globus Medical aimed at integrating neuromodulation with mechanical implants.

Asia-Pacific is projected to post a 10.48% CAGR, underpinned by regulatory harmonization and hospital capacity upgrades. China’s updated medical device law tightens quality standards, encouraging global manufacturers to forge joint ventures that localize production. Korea’s launch of the CUVIS-spine robot exemplifies regional commitment to technology adoption in teaching hospitals. India’s regulation now mirrors European risk-classification, smoothing import pathways for hydrogel systems. Broader insurance coverage and urban middle-class growth build a fertile addressable base for prosthetic disc nucleus market procedures.

Europe maintains steady adoption thanks to universal health coverage and a culture of cost-effectiveness evaluation. Clinical teams in Germany and the UK contribute heavily to trials on expandable facet implants and multimodal imaging, reinforcing surgeon confidence. The EU Medical Device Regulation, although stringent, provides structured guidance that companies can navigate predictably, and early reimbursement decisions in France and the Netherlands for motion-preservation devices encourage peer markets to follow.

Competitive Landscape

Competition is moderately fragmented, with legacy orthopedics firms defending share against venture-backed innovators. Medtronic, ZimVie and Orthofix anchor hospital contracts through extensive instrument trays and training support, but smaller entrants like AxioMed Spine and ReGelTec differentiate on hydrogel chemistry and injectability. Strategic consolidation accelerated in 2025: Stryker divested its U.S. spine implant line to create VB Spine yet retained exclusive rights to its Mako navigation platform, signaling a pivot toward enabling technologies.

Breakthrough device holders enjoy faster payer dialogue; DiscGenics’ allogeneic cell therapy earned Phase III approval, positioning it as a biologics adjunct rather than a mechanical device. Companies able to supply 3D-printed, modulus-tuned implants at scale could capture outpatient-focused ASCs searching for stock-keeping simplicity.

Technology roadmaps prioritize integration with AI-driven planning software to automate endplate sizing and trajectory mapping. Firms offering combined implant-navigation bundles aim to replicate the success seen in knee arthroplasty robotics, potentially increasing switching costs and solidifying prosthetic disc nucleus market positioning.

Prosthetic Disc Nucleus Industry Leaders

ZimVie Inc

Medtronic plc

Orthofix Medical Inc.

Globus Medical Inc.

Spine Wave Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Stryker completed the sale of its U.S. spinal implants business to Viscogliosi Brothers LLC, forming VB Spine while retaining rights to Mako Spine and Copilot technologies.

- February 2025: Globus Medical agreed to acquire Nevro Corp for USD 250 million to pair neuromodulation with spinal implants.

- February 2025: Medtronic launched a deformity-focused spinal system featuring advanced pre-operative planning and instrumentation.

Global Prosthetic Disc Nucleus Market Report Scope

| Hydrogel (PHEMA, PVA, etc.) |

| Polycarbonate-Urethane (PCU) |

| Silicone & Others |

| Minimally Invasive Percutaneous Nucleus Replacement |

| Open / Mini-open Discectomy with Nucleus Implant |

| Injectable Hydrogel Devices |

| Pre-formed Solid Implants |

| Expandable / Articulating Devices |

| Cervical Spine |

| Thoracic Spine |

| Lumbar Spine |

| Hospitals |

| Specialty Orthopaedic & Spine Clinics |

| Ambulatory Surgical Centers (ASCs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Hydrogel (PHEMA, PVA, etc.) | |

| Polycarbonate-Urethane (PCU) | ||

| Silicone & Others | ||

| By Surgery Approach | Minimally Invasive Percutaneous Nucleus Replacement | |

| Open / Mini-open Discectomy with Nucleus Implant | ||

| By Delivery Modality | Injectable Hydrogel Devices | |

| Pre-formed Solid Implants | ||

| Expandable / Articulating Devices | ||

| By Spinal Level | Cervical Spine | |

| Thoracic Spine | ||

| Lumbar Spine | ||

| By End User | Hospitals | |

| Specialty Orthopaedic & Spine Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the prosthetic disc nucleus market in 2025?

The prosthetic disc nucleus market size is valued at USD 137.89 million in 2025.

What is the forecast CAGR for prosthetic disc nucleus devices to 2030?

The market is projected to grow at a 7.89% CAGR through 2030.

Which material category is expanding fastest?

Hydrogel implants are forecast to advance at an 11.77% CAGR, the fastest among materials.

Why are ambulatory surgical centers important for future growth?

ASCs combine lower facility costs with minimally invasive techniques, driving a 10.04% CAGR in procedure volume.

Which region shows the highest growth potential?

Asia-Pacific is expected to record a 10.48% CAGR, the highest worldwide, due to regulatory harmonization and infrastructure expansion.

What are the chief economic barriers to adoption?

High device costs relative to fusion and extended safety data requirements are the primary constraints on wider uptake.

Page last updated on: