Spinal Implants And Surgical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

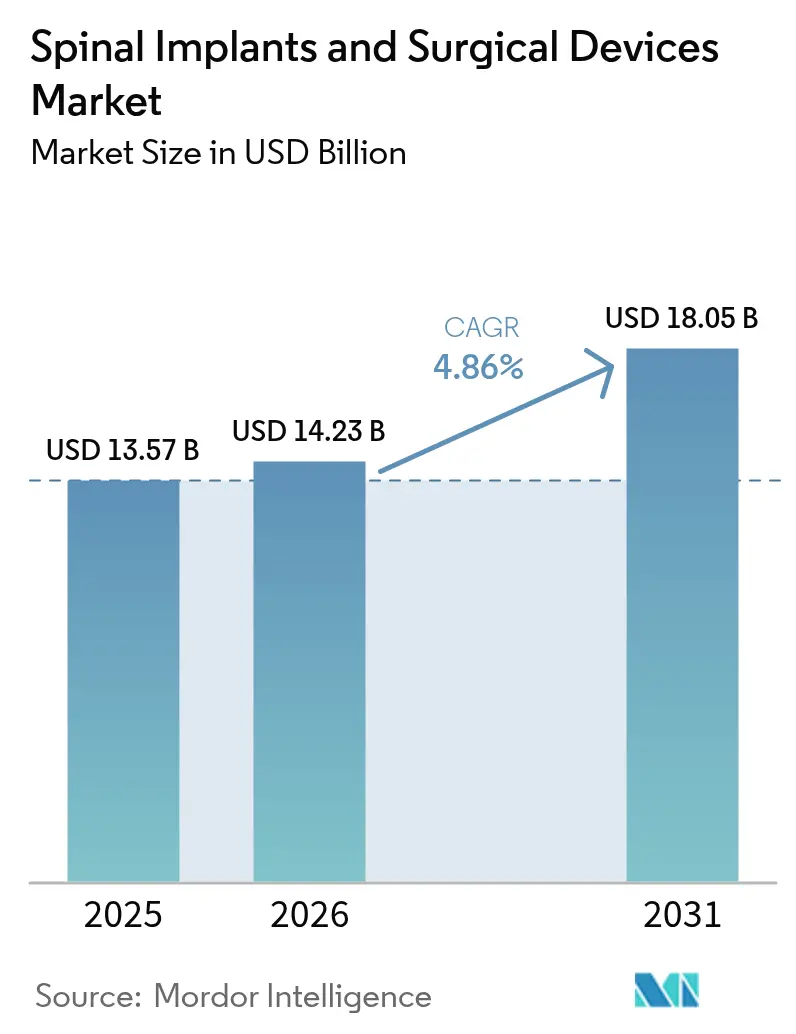

| Market Size (2026) | USD 14.23 Billion |

| Market Size (2031) | USD 18.05 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

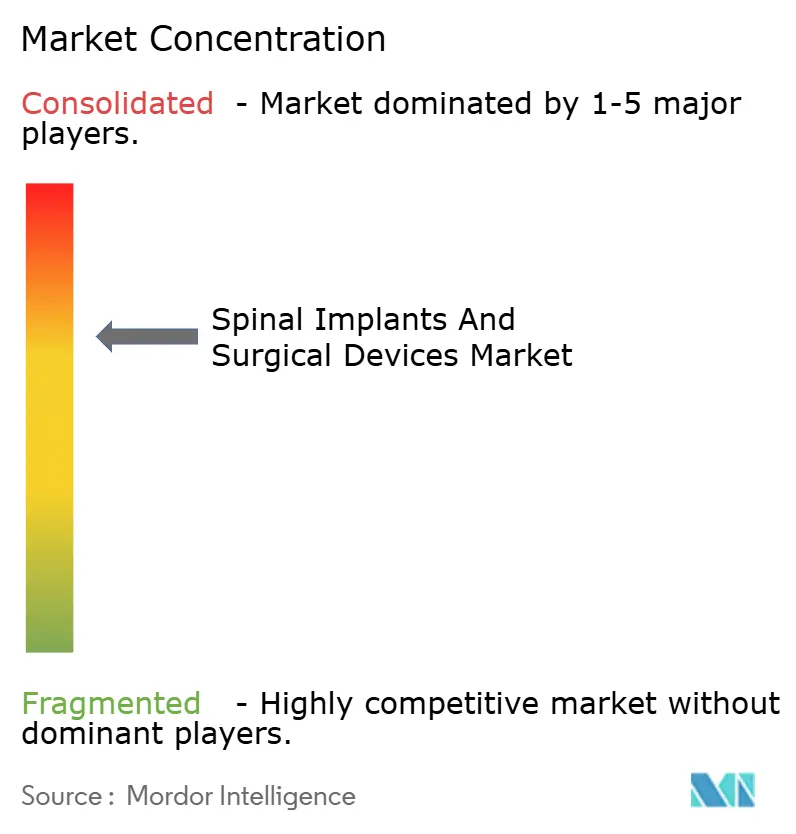

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spinal Implants And Surgical Devices Market Analysis by Mordor Intelligence

The spinal implants and surgical devices market size is expected to grow from USD 13.57 billion in 2025 to USD 14.23 billion in 2026 and is forecast to reach USD 18.05 billion by 2031 at 4.86% CAGR over 2026-2031. Demand expands as aging populations, sedentary lifestyles, and rising traumatic injuries converge with rapid technology adoption in AI-guided robotics, navigation, and 3D-printed biomaterials. Spinal fusion systems still anchor revenue, yet motion-preserving technologies and minimally invasive techniques gain momentum because they reduce adjacent-segment disease, shorten hospital stays, and support outpatient care models. Geographical momentum shifts toward Asia-Pacific as procedure volumes soar in China and Japan, while North America continues to set the pace on reimbursement reforms and breakthrough device clearances. Competitive dynamics pivot around integrated surgical ecosystems that blend implants, imaging, robotics, and digital health, even as capital costs and regulatory paths temper the speed of diffusion.

Key Report Takeaways

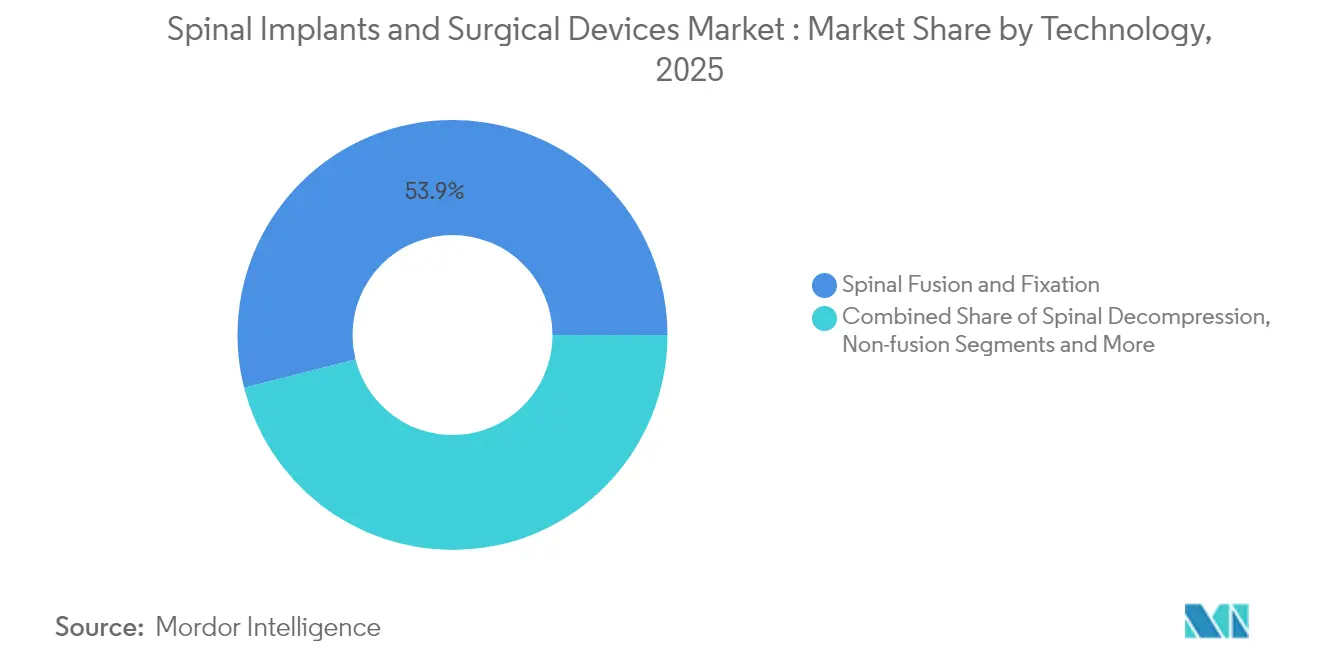

- By technology, spinal fusion and fixation claimed 53.94% of spinal implants and surgical devices market share in 2025, while motion-preservation solutions are set to accelerate at an 8.41% CAGR through 2031.

- By product, thoracic and lumbar fusion devices contributed 40.16% of the spinal implants and surgical devices market size in 2025, yet non-fusion devices are on track for an 8.23% CAGR through 2031.

- By type of surgery, open procedures held 60.45% of the spinal implants and surgical devices market size in 2025; minimally invasive techniques are forecast to advance at a 8.95% CAGR to 2031.

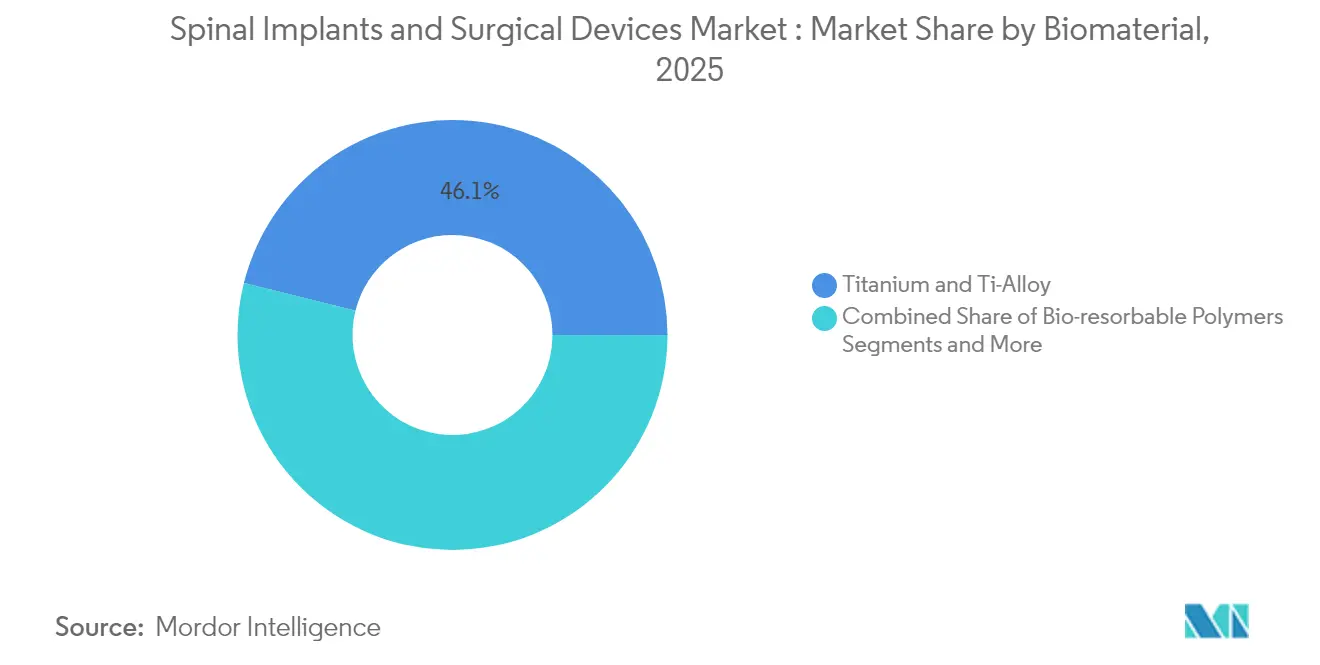

- By biomaterial, titanium and titanium alloys held 46.12% of spinal implants and surgical devices market share in 2025; porous 3D-printed metals are growing at a 8.74% CAGR.

- By end user, hospitals accounted for 48.63% of the spinal implants and surgical devices market in 2025, while ambulatory surgical centers are expanding at an 8.32% CAGR.

- By geography, North America led with 43.78% revenue share in 2025, whereas Asia-Pacific is expected to record the fastest 7.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spinal Implants And Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of spinal disorders and aging population | +1.8% | Global, led by North America, Europe, Japan | Long term (≥ 4 years) |

| Rapid uptake of minimally invasive procedures | +1.2% | North America and Europe lead, APAC follows | Medium term (2-4 years) |

| Technological advancement in implants and devices | +0.9% | Global innovation hubs in North America, Europe | Medium term (2-4 years) |

| Growing demand for outpatient and ambulatory spine surgeries | +0.7% | North America first, expanding to Europe and APAC | Short term (≤ 2 years) |

| AI-guided robotic screw placement improving outcomes | +0.5% | High-income markets, selective emerging uptake | Medium term (2-4 years) |

| Growing focus on customizable 3D implants | +0.4% | North America and Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burden of Spinal Disorders and Aging Population

Global life expectancy gains create a sustained rise in degenerative spine conditions, compression fractures, and trauma-related injuries. Epidemiological studies project an 80% increase in spine surgery volume by 2060, with vertebral compression fractures already showing 48.9% vertebral-height deterioration despite percutaneous treatments.[1]Luthfi Gatam, “Robotic Pedicle Screw Placement for Minimal Invasive Thoracolumbar Spine Surgery,” Frontiers in Surgery, frontiersin.org Annual U.S. spinal cord injury incidence stands at 17,000 cases, and first-year costs for high tetraplegia surpass USD 1 million, reinforcing the imperative for preventive and reconstructive solutions. These clinical and economic factors lift procedure counts, broaden indications, and keep reimbursement authorities focused on cost-effective innovations.

Rapid Uptake of Minimally Invasive Procedures for Spine

Endoscopic and tubular techniques combine exoscope visualization, fluoroscopy, and navigation to lower blood loss, reduce postoperative pain, and facilitate same-day discharge. A transforaminal approach for lumbar discectomy, for example, shows lower complication rates than open microdiscectomy.[2]Antonacci C.L. et al., “A Narrative Review of Endoscopic Spine Surgery: History, Indications, Uses, and Future Directions,” Journal of Spine Surgery, jss.amegroups.org Outpatient lumbar fusion delivers safety comparable to inpatient settings with fewer medical complications, enabling payer endorsement of bundled payments. These clinical outcomes accelerate the shift toward dedicated spine ambulatory centers and push vendors to refine navigation software for constrained anatomical corridors.

Technological Advancement in Spinal Implants and Surgical Devices

Selective laser melting and electron-beam melting enable lattice structures that match cancellous bone elasticity, minimizing stress shielding. One porous Ti-6Al-4V scaffold exhibits 794 MPa compressive strength and 41.35% fracture strain while supporting bone ingrowth.[3]Tairong Li et al., “Preparation and Post-Processing of Three-Dimensional Printed Porous Titanium Alloys,” Materials, mdpi.comCarbon-fiber frames reduce CT scatter, aiding radiotherapy planning, and smart implants with wireless sensors deliver real-time load monitoring that guides rehabilitation. Together, these innovations drive surgeon demand for patient-specific solutions and underpin premium pricing strategies.

Growing Demand for Outpatient and Ambulatory Spine Surgeries

Ambulatory surgical centers now handle 72% of U.S. surgeries, offering 45-60% cost savings and 20% shorter wait times with 92% patient satisfaction. Medicare expanded its outpatient spine-procedure list from 12 to 58 between 2010 and 2021, reflecting confidence in safety profiles. This payment evolution compels device firms to design lighter, workflow-compatible systems and drives anesthetic protocols that favor rapid ambulation, thereby re-shaping capital-equipment demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implant & navigation capital costs | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Stringent multi-jurisdiction regulatory approvals | -0.8% | Global, variable across FDA, CE, others | Medium term (2-4 years) |

| Shortage of skilled spine surgeons | -0.6% | Global, acute in Africa and Latin America | Long term (≥ 4 years) |

| Risk of surgical complications and implant failure | -0.4% | Global, higher in complex revisions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implant & Navigation Capital Costs

Acquiring a top-tier robotic or navigation suite surpasses USD 1 million, and 77% of surveyed surgeons cite price as the primary barrier. Procedure-level economics also bite: lumbar disc replacement ranges USD 20,000-70,000, and spinal cord stimulation can hit USD 50,000 before add-ons. Annual service contracts, staff training, and OR redesign raise total cost of ownership, delaying procurement decisions in ambulatory centers and emerging nations.

Stringent Multi-Jurisdiction Regulatory Approvals

FDA breakthrough designations shorten review clocks but still demand rigorous clinical evidence, extensive bench testing, and manufacturing audits. Firms must then replicate dossiers for CE Mark and CFDA, multiplying compliance costs. These hurdles favor cash-rich incumbents and slow market entry for start-ups, prolonging patient access to novel concepts such as antibacterial coatings and bio-resorbable hardware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fusion Dominance Faces Motion-Preservation Challenge

Spinal fusion and fixation technologies commanded 53.94% of spinal implants and surgical devices market revenue in 2025. The spinal implants and surgical devices market size for motion-preservation systems is forecast to advance at an 8.41% CAGR, reflecting surgeon interest in preserving segmental biomechanics. Evidence shows artificial cervical discs reduce adjacent-segment degeneration versus fusion, while dynamic stabilization mitigates postoperative stiffness. The field also witnesses hybrid constructs that blend disc arthroplasty at one level and fusion at another, matching patient pathology. Smaller footprints, modular plating, and porous coatings underscore design improvements in contemporary cages. Meanwhile, automation through computer-planned screw trajectories raises fusion accuracy, reinforcing its present dominance.

Patient preferences fuel the transition as long-term quality-of-life studies favor motion preservation for select indications. Mobi-C, with more than 225,000 implants, demonstrates non-inferiority for two-level disease compared with standard ACDF ZimVie Cervical. In the lumbar arena, Prodisc L shows sub-1% reoperation after 25 years, validating durability. These data prompt insurers to revisit coverage exclusions, potentially speeding adoption in the spinal implants and surgical devices market.

By Product: Interbody Devices Drive Innovation Convergence

Thoracic and lumbar fusion devices provided 40.16% of spinal implants and surgical devices market share in 2025, yet non-fusion counterparts grow at an 8.23% CAGR. Interbody cages headline revenue thanks to additive manufacturing that tailors porosity and endplate fit. The spinal implants and surgical devices market size for interbody cages is projected to rise as PEEK-titanium hybrids address radiolucency while maintaining surface roughness for bone adhesion. Bone graft substitutes combining rhBMP-2 and demineralized matrix inflate fusion probability.

Additive manufacturing unlocks biomimetic lattices; Stryker’s Tritanium TL cage uses AMagine to mirror cancellous bone architecture Stryker. Medtronic’s Adaptix system integrates Titan nanoLOCK nanotopography to achieve higher pull-out strength. Spine stimulators complement these hardware gains by boosting osteogenesis, posting fusion rates of 86.8% versus 73.7% for controls in meta-analysis.

By Type of Surgery: Minimally Invasive Gains Momentum

Open surgery still represented 60.45% of global revenue in 2025, yet minimally invasive techniques are growing at a 8.95% CAGR within the spinal implants and surgical devices market. Tubular retractors, endoscopes, and percutaneous fixation enable decompressions and fusions through incisions often under 2 cm. The spinal implants and surgical devices market share for endoscopic lumbar discectomy continues to climb as same-day discharge becomes norm. Robust data confirm lower blood loss, faster ambulation, and reduced narcotic use vs. open benchmarks Spine.

Robotics amplifies this trend by stabilizing instrument positioning while decreasing fluoroscopy exposure. Hospitals move complex deformity work into MIS corridors, integrating interbody cages, expandable screws, and navigation head-up displays. Outpatient facilities install CT-on-rails platforms to maintain accuracy without excessive radiation, further normalizing MIS across indications.

By Biomaterial: Advanced Materials Challenge Titanium Dominance

Titanium retained 46.12% of 2025 revenue, but porous 3D-printed metals are compounding at 8.74%, eroding the incumbent’s lead. The spinal implants and surgical devices market size for porous titanium substitutes climbs as lattice structures reduce modulus mismatch and foster bone ingrowth. PEEK and carbon-PEEK provide radiographic clarity that assists radiotherapy and postoperative MRI planning. Bio-resorbable PLA-PGA blends carry load temporarily before degrading, curbing stress shielding for adolescent cases.

Surface engineering shines in research: nanotube anodization on titanium promotes osteoblast adhesion, and hydroxyapatite coatings shorten fusion windows. Carbon fiber frames paired with tantalum markers achieve near-artifact-free imaging during proton therapy, addressing oncology overlap. Bio-resorbables armed with growth-factor reservoirs show promise in pediatric deformity, pointing to a diversified biomaterial roadmap.

By End User: Ambulatory Centers Reshape Delivery Models

Hospitals maintained 48.63% revenue share in 2025, yet ambulatory surgical centers (ASCs) are the fastest-growing venue at an 8.32% CAGR. The spinal implants and surgical devices market thrives in these facilities because lower overhead allows rapid adoption of cost-effective navigation platforms. Workflow redesign focuses on same-day mobility and anesthetic regimens that minimize nausea. Medicare’s broader ASC coverage list catalyzes volume migration.

ASCs invest in modular, smaller-footprint robotics optimized for limited OR space. Vendors respond with portable intraoperative CT and cloud-based navigation to align capital outlay with ASC economics. Specialty orthopedic clinics adopt similar models, bundling pain management and rehabilitation, thereby offering an end-to-end spine care continuum that still ties back to hospital networks for high-acuity cases.

Geography Analysis

North America led the spinal implants and surgical devices market with 43.78% revenue share in 2025. Robust reimbursement frameworks, early adoption of navigation, and a high concentration of fellowship-trained surgeons sustain leadership. Medicare’s incremental inclusion of outpatient spine procedures and FDA breakthrough device designations shorten the technology-to-patient timeline. Academic-industry partnerships, typified by Medtronic’s imaging pact with Siemens Healthineers, integrate platforms and set service benchmarks.

Asia-Pacific posts the highest 7.96% CAGR as demographics and incomes change procedure mix. China logged a 12.32% annual rise in surgeries, with winter and spring peaks reflecting elective scheduling habits. Japan’s nationwide JSIS-DB registry, now at 5,400 cases, enables outcome-based reimbursement and informs device design. Yet disparities persist: rural Indonesia and Philippines lack navigation infrastructure, requiring vendor outreach and training grants.

Europe remains steady, balancing fiscal prudence with evidence-based adoption. CE agencies demand long follow-up, thus elongating go-to-market timetables. Still, Germany and France accelerate outpatient volumes as payers endorse DRG realignments. Latin America and Middle East & Africa contribute single-digit revenue today but represent white-space growth: fluoroscopy is used in 96.5% of African cases, offering a springboard for low-cost navigation solutions accompanied by NGO-backed surgeon training.

Regulatory Landscape

Regulation is shaped by multi-jurisdiction pathways that combine premarket evidence requirements with post-market surveillance expectations across the United States, Europe, and China. In the United States, FDA activity in 2026 clarified requirements around patient-specific workflows, including a May 2026 final guidance on Patient-Matched Guides for Orthopedic Implants, while FDA-recognized consensus standards continue to influence test methods and submission packages (for example, ASTM F3292-25 for inspection practices for spinal implants recognized in December 2025). Together, these updates reinforce documentation rigor for implant design, validation, and manufacturing controls, particularly for systems that interact with navigation, robotics, or patient-specific instrumentation.

In Europe, conformity assessment under the EU MDR remains a central gating factor for implant commercialization, with 2026 policy action targeting process relief for mature technologies. Delegated Regulation (EU) 2026/1359 expanded the list of Class IIb implantable devices exempt from systematic technical documentation assessment by notified bodies, explicitly covering categories that include spinal fixation devices. This can reduce review bottlenecks for established product lines while keeping MDR obligations in place. In China, the NMPA increased standardization and oversight in 2026 through Announcement No. 24 of 2026, which introduced 26 medical device industry standards, including mandatory standards for metal bone plates (YY 0017-2026) and metal bone screws (YY 0018-2026). Alongside a 2026 National Inspection Plan listing spine hardware such as plates, rods, screws, and interbody fusion cages, these changes raise compliance and readiness requirements for both domestic and imported manufacturers.

Value Chain Analysis

The value chain spans raw-material supply (titanium and titanium alloys, PEEK and carbon-PEEK polymers), component and instrument manufacturing, implant finishing (surface treatments such as anodizing and passivation), sterilization, packaging and kitting, and distribution to hospitals, ambulatory surgical centers, and specialty orthopedic clinics. Production often blends CNC machining with additive manufacturing for porous, patient-matched, and lattice-structure implants, then follows validated cleaning and sterilization workflows that are tightly linked to regulatory documentation. Manufacturing and engineering clusters remain concentrated in major medtech hubs across the United States and Western Europe, while Asia-Pacific contributes both manufacturing capability and fast-growing procedure demand.

Bottlenecks and risk points cluster upstream and at critical service nodes, including extended lead times for titanium inputs, constraints in sterilization capacity, and the operational burden of multi-market regulatory compliance. These factors can slow change notifications and line extensions. OEMs frequently use specialized contract manufacturers for implant production, assembly, kitting, and sterilization to scale capacity, shorten time-to-market, and manage cost, while retaining quality-system oversight. On the distribution side, shifting site-of-care toward ASCs increases the importance of reliable, just-in-time logistics and standardized implant sets, and it aligns with policy moves that increase transparency and continuity planning. One example is the European Union requirement introduced in January 2025 for mandatory reporting of potential medical device shortages.

Competitive Landscape

The spinal implants and surgical devices industry exhibits moderate fragmentation that edges toward consolidation as vendors chase scale, R&D synergies, and digital capabilities. Full-line conglomerates hold multi-category portfolios that span biomaterials, navigation, robotics, and biologics, leveraging cross-selling to lock in purchasing agreements. Mid-tier specialists carve out niches in motion preservation, expandable cages, or sensorized hardware, while start-ups pursue bio-resorbables and AI-first navigation algorithms.

Strategic moves emphasize vertical stack ownership: implant firms buy robotics start-ups to unify hardware-software ecosystems, creating one-vendor value propositions that resonate with health-system supply chains. Globus Medical’s plan to acquire Nevro Corp for USD 250 million extends its presence into neuromodulation and pain management. Meanwhile, Stryker divested its U.S. spine implant line to VB Spine to sharpen focus on enabling technologies, signaling a pivot to high-margin digital platforms.

Technology licensing, co-development, and surgeon fellowship sponsorships underpin go-to-market execution. Firms pilot usage-based pricing on navigation units to reduce CAPEX barriers for ASCs. Cloud dashboards capture implant telemetry, feeding predictive analytics that flag non-union risk. Intellectual-property intensity and regulatory know-how thus remain pivotal differentiators within the spinal implants and surgical devices market.

Spinal Implants And Surgical Devices Industry Leaders

Medtronic

Stryker Corporation

Johnson and Johnson

Nuvasive Inc

Globus Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One near-term opportunity is faster product iteration and broader participation in adjacent spine care categories as regulatory pathways evolve, particularly where oversight has shifted toward special controls rather than the highest-risk route. In April 2026, FDA finalized the reclassification of non-invasive bone growth stimulators from Class III to Class II and established special controls. This can reduce development friction for compliant designs and widen commercialization options for bone-healing adjuncts that complement fusion hardware. The regulatory shift also aligns with the report scope that includes spine bone stimulators as a product segment, creating whitespace for companies to pair stimulation therapy with interbody cages, fixation systems, and post-operative pathways.

A second opportunity sits in integrated surgical ecosystems that package implants with enabling technologies tailored to minimally invasive and outpatient workflows. Evidence of market movement shows up in recent FDA clearances and adoption focus around combined planning, navigation, and robotics platforms (for example, Medtronic received FDA clearance for its Stealth AXiS spine system in February 2026), as well as in clinical emphasis on improving pedicle screw placement accuracy and managing radiation exposure through intraoperative 3D imaging and navigation. As ASCs expand their spine case mix, vendors that offer smaller-footprint, workflow-compatible navigation and robotics and a compatible implant portfolio can address procurement barriers tied to capital costs and training, while using outcome data collection to support payer and provider standardization decisions.

Recent Industry Developments

- May 2026: Globus Medical received FDA 510(k) clearance (K253739) covering updates across stabilization offerings, including elements associated with SCRIPT Rods and the NuVasive Reline system. The clearance supports portfolio continuity and streamlines commercialization for system-level changes that hospitals and ASCs evaluate when standardizing instrument trays and implant sets.

- May 2025: Stryker received FDA 510(k) clearance for the OptaBlate BVN Basivertebral Nerve Ablation System. The move expands minimally invasive back pain treatment participation and broadens spine-adjacent procedural options that can be routed through outpatient settings.

- July 2024: Stryker announced FDA 510(k) clearance for Spine Guidance 5 Software featuring Copilot, adding an automatic depth stop feature for pedicle screw placement. Software-led enhancements reinforce the shift toward navigation-enabled precision and help vendors differentiate within integrated implant-plus-guidance workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue from spinal implants and the linked surgical device kits that are used to stabilize, fuse, or preserve motion in the spine, across open and minimally invasive procedures.

Scope exclusions: Standalone regenerative biologics, diagnostic imaging systems, and routine single use consumables are excluded from the market totals.

Segmentation Overview

- By Technology

- Spinal Fusion & Fixation

- Vertebral Compression Fracture Treatment

- Motion Preservation / Non-fusion

- Spinal Decompression

- By Product

- Thoracic & Lumbar Fusion Devices

- Cervical Fusion Devices

- Interbody Fusion Cages

- Spine Biologics

- Non-fusion Devices

- Vertebral Compression Fracture Treatment Devices

- Spine Bone Stimulators

- By Type of Surgery

- Open Surgery

- Minimally-invasive Surgery

- By Biomaterial

- Titanium & Titanium-Alloy

- PEEK & Carbon-PEEK

- Bio-resorbable Polymers

- Porous 3-D Printed Metals

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Orthopedic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build realistic procedure-level demand signals, and anchor price ranges for common implant systems. Public sources were reviewed, including CDC and WHO statistics on musculoskeletal conditions, OECD health spending, and hospital activity indicators, plus procedure guidance and reporting standards from organizations such as the American Academy of Orthopaedic Surgeons and the North American Spine Society.

In parallel, we reviewed company annual reports, investor presentations, and reputable press coverage to understand portfolio mix, geographic exposure, and recent shifts in surgeon adoption. Patent databases were checked to track innovation intensity in areas such as motion preservation and minimally invasive instrumentation, and an import export shipment-level database was referenced selectively to sanity-check trade flows for implant components in key regions. The desk sources listed here are illustrative, and other public materials were also used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to close gaps that desk research cannot resolve cleanly, especially around procedure mix shifts, typical implant configurations, and how pricing changes when hospitals renegotiate contracts. The fieldwork included spine surgeons, hospital procurement teams, ambulatory surgery center administrators, distributors, and product managers, with balanced coverage across mature and faster-growing countries.

These discussions were used to pressure-test the assumed share of open versus minimally invasive approaches, confirm common add-on instrument usage, and validate the timing of new implant adoption in elective surgery backlogs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 42% |

| Mid tier: 52% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 19% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool using procedure volumes and care setting mix, and then converts it into device revenue using typical implant sets and average selling prices by region. Because spinal procedures vary by indication and technique, inputs were adjusted using market fingerprints such as spinal fusion versus motion preservation shares, open versus minimally invasive penetration, elective surgery deferral and catch-up patterns, aging population trends tied to degenerative spine conditions, and hospital versus ambulatory surgery center throughput.

After the top-down totals were produced, they were corroborated with selective bottom-up approximations where data was available, such as sampled ASP times estimated unit volumes for common implant constructs and distributor channel checks on regional product mix. Where a supplier roll-up could not be completed cleanly, for example due to private revenue disclosure gaps, the model used scenario ranges that were narrowed using primary feedback on market shares and replacement cycles. For forecasting, we used scenario analysis supported by a short list of drivers agreed with experts, mainly procedure growth, site-of-care shift, and price pressure versus mix upgrades, then reviewed the outputs for realism against recent historical movement.

Data Validation & Update Cycle

Validation was done through repeated checks that compare model outputs against independent signals, including reported procedure activity trends, import patterns for implant categories, and public revenue commentary on spine portfolios. When an input change created an unusual jump for a specific country or product line, we traced the variance back to the driver and either corrected the assumption or re-ranged it, then rechecked the model outputs before sign-off.

Reports are refreshed annually, with interim updates made when material events occur, such as major reimbursement changes, large regulatory actions, or sharp swings in elective surgery capacity. Before delivery, a fresh final pass is completed so clients receive the most current view that still matches the documented assumptions and calculations.

Mordor Intelligence's Spinal Implants and Surgical Devices Market Size Versus Other Published Estimates

It is normal to see different market sizes for spinal implants and surgical devices because each publisher draws the scope line differently, then applies its own mix and price assumptions across regions. Variation can also come from which year is treated as the base, how currency conversion is timed, and whether recent procedure recovery is treated as temporary or sustained.

Some external estimates expand the market by adding spine biologics, bone stimulators, and vertebral compression fracture devices into the same total. In Mordor Intelligence, the market total is limited to spinal implants and matched surgical instrument kits used in spine stabilization, fusion, or motion preservation, with standalone regenerative biologics and routine consumables kept outside the calculation so procedure-to-device revenue stays consistent.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.57 B (2025) | |

| Healthcare Publisher A | USD 14.55 B (2025) | Uses a broader device basket described as spinal implants and devices, which can pull in adjacent spinal surgery tools and categories that are not always tied to implant kit revenue in a procedure-based build. |

| Industry Publisher B | USD 11.97 B (2024) | Anchors the estimate to a different base year and includes spine biologics, bone stimulators, and vertebral compression fracture treatment devices, which changes the mix and the implied ASP progression versus an implants-and-instruments-only view. |

Taken together, the spread is largely explained by category inclusion and the year used for anchoring the model, followed by how each source treats mix upgrades versus pricing pressure. By keeping the calculation tied to procedure activity, typical implant configurations, and region-specific ASP checks that can be re-validated, the resulting number stays traceable and easier to reproduce for planning.

Key Questions Answered in the Report

What is the current size of the spinal implants and surgical devices market?

The market generated USD 14.23 billion in 2026 and is expected to climb to USD 18.05 billion by 2031, reflecting a 4.86% CAGR.

Which technology segment is growing fastest?

Motion-preservation systems, including artificial discs and dynamic stabilization devices, are expanding at an 8.41% CAGR through 2031.

How quickly are ambulatory surgical centers gaining share?

ASCs are the fastest-growing end-user group, advancing at an 8.32% CAGR as payers back outpatient fusions and decompressions.

Why are porous 3D-printed metals important in spine surgery?

They match bone elasticity, encourage vascularization, and are rising at a 8.74% CAGR, challenging traditional titanium dominance.

Page last updated on: