Artificial Disc Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

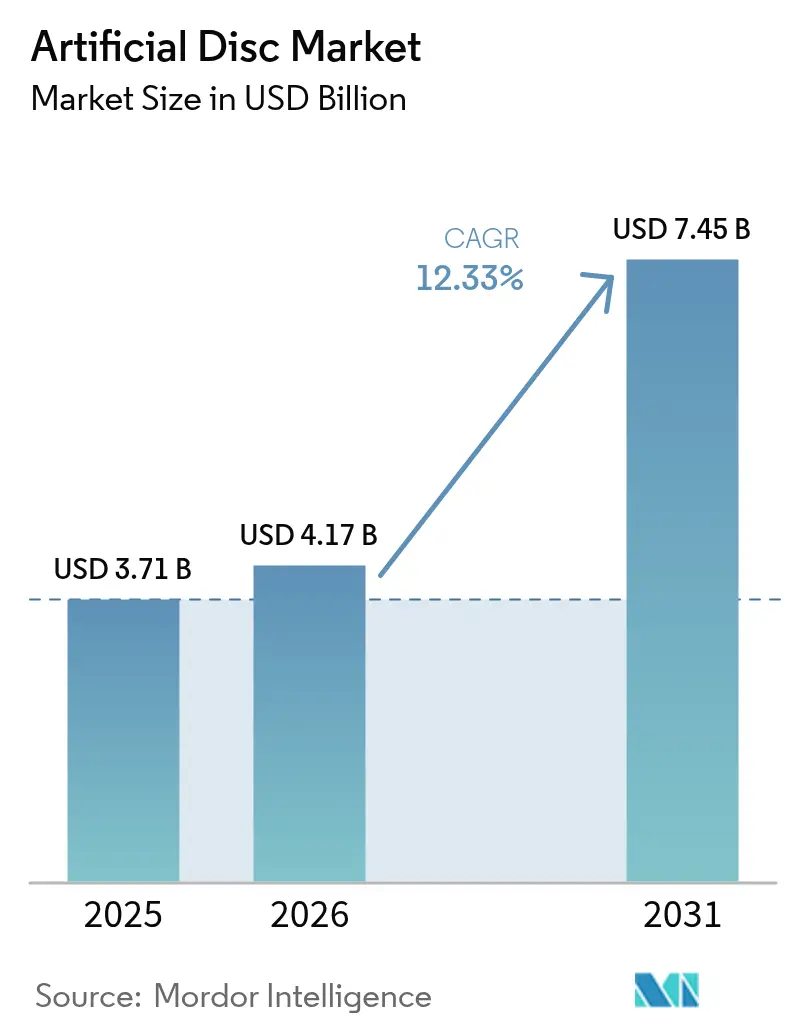

| Market Size (2026) | USD 4.17 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Disc Market Analysis by Mordor Intelligence

The artificial disc market size was valued at USD 3.71 billion in 2025 and estimated to grow from USD 4.17 billion in 2026 to reach USD 7.45 billion by 2031, at a CAGR of 12.33% during the forecast period (2026-2031). A sustained surge in degenerative disc disease, the validation of motion-preservation outcomes, and swift advances in biomimetic implant design collectively underpin this double-digit trajectory. North America retains an early-mover advantage due to broad private-payer coverage, while the Asia-Pacific region accelerates on the back of hospital build-outs and aging demographics. Metal-on-polymer systems remain the workhorse, yet ceramic-on-polymer platforms are outpacing the field, benefiting from lower wear profiles and enhanced imaging compatibility. Outpatient migration is another pivotal trend; artificial disc arthroplasty conducted in ambulatory surgical centers (ASCs) now routinely delivers 60% cost savings relative to inpatient care. Competitive intensity is sharpening as incumbents consolidate portfolios and smaller specialists commercialize viscoelastic and AI-guided offerings.

Key Report Takeaways

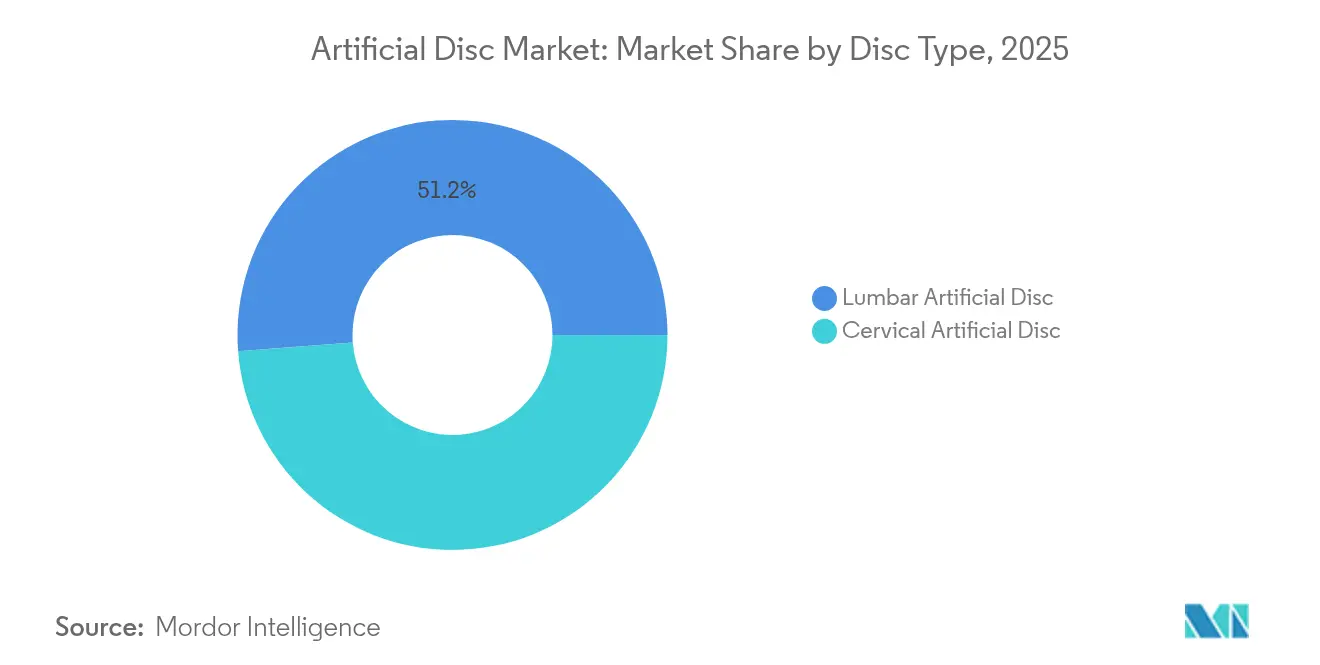

- By disc type, the lumbar segment held a 51.20% market share of artificial discs in 2025; the cervical segment is projected to grow at a 15.16% CAGR through 2031.

- By material, metal-on-polymer accounted for 59.10% of the artificial disc market size in 2025, while ceramic-on-polymer is advancing at a 15.82% CAGR between 2026 and 2031.

- By design, semi-constrained discs captured 45.40% revenue share in 2025; the non-constrained category is forecast to expand at a 14.91% CAGR to 2031.

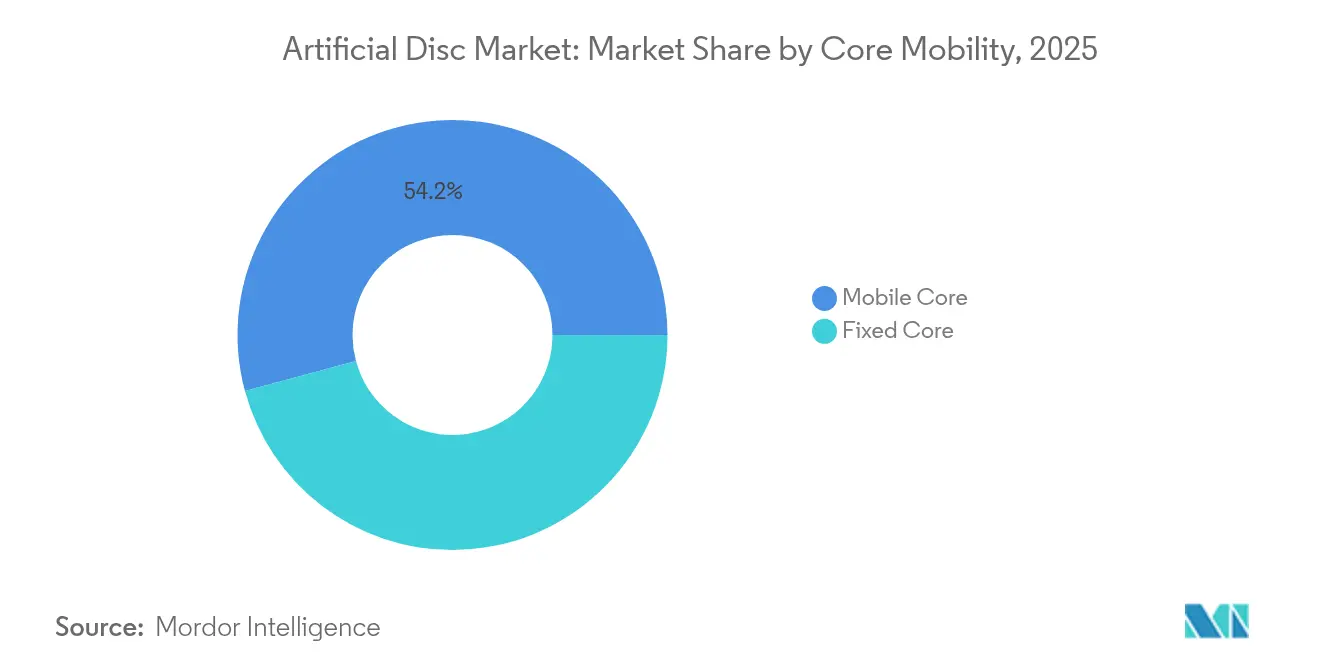

- By core mobility, mobile-core solutions led with a 54.20% share of the artificial disc market in 2025; fixed-core systems are projected to grow at a 14.36% annual rate through 2031.

- By end-user, hospitals contributed 69.10% of the artificial disc market size in 2025, whereas ASCs are expected to register a 13.22% CAGR during 2026-2031.

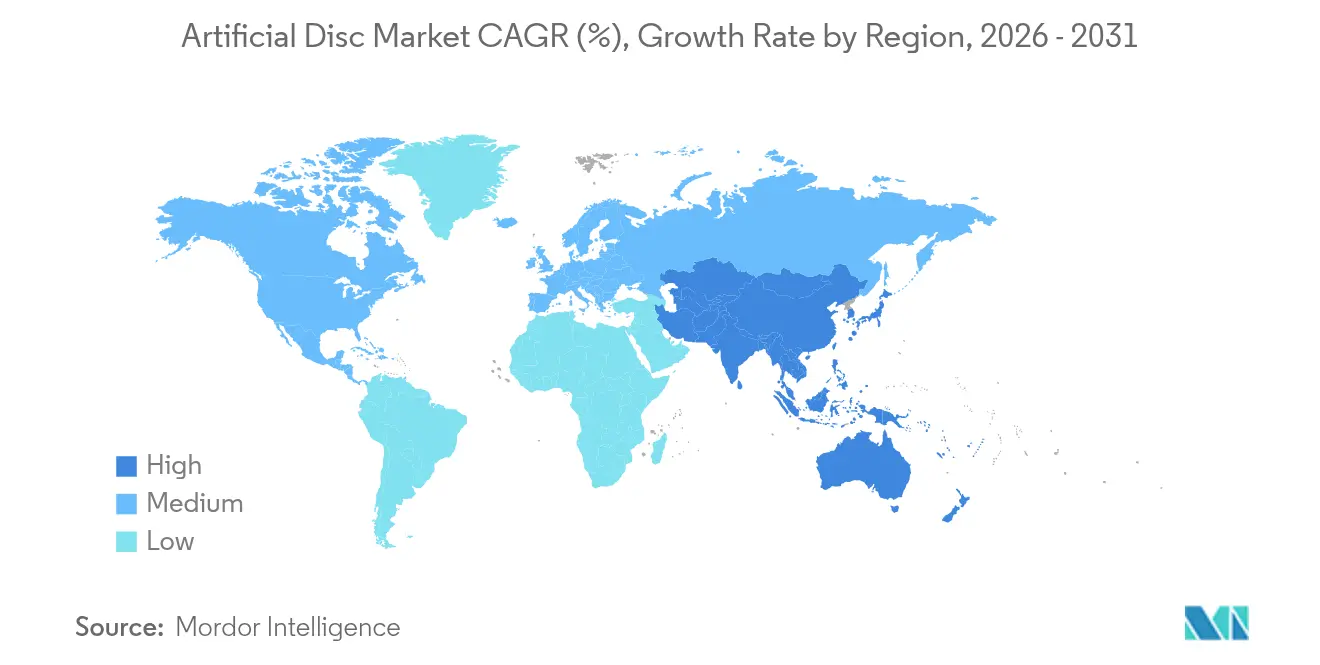

- By geography, North America contributed 37.60% of the 2025 revenue, whereas the Asia-Pacific region is advancing at a 14.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Disc Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Prevalence of Degenerative Disc Disease and Chronic Low-Back Pain | +3.5% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Rapid Technological Advances in Motion-Preservation Implants (Mobile-Core & Biomimetic Materials) | +1.2% | North America, Europe, advanced APAC markets | Medium term (2-4 years) |

| Growing Surgeon & Patient Preference for Minimally Invasive Disc Arthroplasty over Spinal Fusion | +2.3% | Global, with early adoption in North America | Medium term (2-4 years) |

| Expanding Long-Term Clinical Evidence Supporting Safety and Superior Functional Outcomes | +1.8% | Global | Long term (≥ 4 years) |

| Increasing Healthcare Expenditure and Access to Advanced Spinal Care in Emerging Economies | +1.4% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Degenerative Disc Disease

Global low-back and neck pain cases exceed 600 million and are projected to rise markedly by 2050 as populations age. Higher life expectancy and sedentary work patterns exacerbate disc degeneration, compelling payers to seek durable, motion-preserving solutions. The economic burden encompasses lost productivity and disability payments, making artificial discs an attractive option for stakeholders who look beyond short-term surgical costs. Traditional fusion often fails to restore biomechanics, positioning disc arthroplasty as a credible alternative that maintains mobility and quality of life. Public health agencies are increasingly framing musculoskeletal wellness as a productivity imperative, thereby reinforcing the demand for next-generation implants.

Rapid Technological Advances in Motion-Preservation Implants

Viscoelastic cervical discs, 3D-printed patient-specific endplates, and ceramic-on-polymer bearings illustrate a design paradigm shift toward more biomimetic constructs. These innovations reduce wear debris, permit physiologic motion in six degrees of freedom, and simplify imaging follow-up by minimizing artifacts. The incorporation of additive manufacturing enables the creation of optimized lattice structures that distribute loads evenly, potentially prolonging implant survivorship. Such advancements widen indications, including multi-level disease, and feed surgeon confidence in newer systems. AI-enhanced planning software further fine-tunes sizing and positioning, trimming OR time and revision risk.

Growing Surgeon & Patient Preference for Minimally Invasive Disc Arthroplasty

Comparative studies report 82.3% five-year composite success for cervical disc replacements versus 67.0% for fusion. Outcomes such as faster return-to-sport and preserved segmental motion are resonating with active patient cohorts. Minimally invasive techniques reduce muscle disruption, blood loss, and hospitalization, dovetailing with ASC economics. Social media amplifies positive patient experiences, accelerating consumer pull. Surgeon sentiment is also shifting as robotic guidance and real-time navigation flatten the learning curve, reinforcing arthroplasty over fusion in suitable candidates.

Expanding Long-Term Clinical Evidence Supporting Safety and Superior Outcomes

Seven- to 21-year lumbar data reveal a 0.67% index-level revision rate for established disc systems. Adjacent-segment surgery incidence remains below 2%, addressing a key criticism leveled at early-generation devices. Such longitudinal datasets persuade conservative surgeons and payers that arthroplasty durability matches or exceeds fusion constructs. Regulators have responded by clearing two-level and multi-level applications, enlarging the treatable population. Health-economic models now capture lifetime cost avoidance from reduced re-operations, reinforcing favorable reimbursement trajectories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implant & Procedure Costs Versus Fusion Alternatives in Cost-Constrained Health Systems | -1.8% | Global, with higher impact in emerging markets and public healthcare systems | Medium term (2-4 years) |

| Stringent Regulatory Approval Pathways and Lengthy Clinical Trial Requirements | -1.2% | Global, with highest impact in FDA and EMA jurisdictions | Long term (≥ 4 years) |

| Limited Surgeon Training & Learning Curve for Complex Disc Arthroplasty Techniques | -1.6% | Global, with higher impact in regions with fewer specialized centers | Short term (≤ 2 years) |

| Uncertainty Over Long-Term Implant Survivability and Revision Surgery Complexity | -1.1% | Global, with higher impact in conservative healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implant & Procedure Costs Versus Fusion Alternatives

Artificial disc systems command premium pricing versus fusion cages, challenging adoption where budgets are tight. Although lifetime economic models favor motion preservation, upfront costs remain a hurdle for public payers; Medicare still restricts lumbar coverage to patients under 60 years[1]Centers for Medicare & Medicaid Services, “Lumbar Artificial Disc Replacement Decision Memo,” cms.gov. Emerging economies grapple with capital constraints and variable private insurance penetration, slowing penetration despite rising disease burden. Volume‐based procurement and local manufacturing incentives are gradually narrowing the gap, yet cost containment will continue to temper near-term growth.

Limited Surgeon Training & Learning Curve for Complex Disc Arthroplasty

Proficiency in lumbar arthroplasty generally requires 30+ index cases; limited fellowship exposure restricts global surgeon pools. Incorrect sizing or positioning can precipitate facet overload or implant migration, heightening the perceived risk. Device makers now fund cadaveric labs, VR simulators, and AI-driven pre-op templating to expedite competency. Medtronic’s cloud-based live-stream modules exemplify industry initiatives to democratize training. These tools are mitigating but not eliminating the skill-gap bottleneck, especially in regions lacking spine subspecialty infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disc Type: Cervical Momentum Overtakes Lumbar Leadership

The lumbar segment supplied 51.20% of the artificial disc market size in 2025, reflecting the prevalence of low-back disorders. Still, cervical volumes are scaling faster, projected at a 15.16% CAGR, thanks to demonstrated 82.3% clinical success and more straightforward anatomy. Multi-level regulatory clearances and viscoelastic designs, such as the M6-C, strengthen the cervical value proposition. Lumbar devices retain traction through long-term durability data, with the Prodisc L exhibiting just 0.67% revision rate across two decades . Together, these patterns illustrate how the artificial disc market is diversifying across spinal levels rather than concentrating solely on lumbar pathology.

Enhanced cervical uptake also reshapes surgical workflow, resulting in shorter operative times, reduced blood loss, and faster ambulatory qualification, which encourages ASC migration. Reimbursement parity between cervical fusion and arthroplasty in many U.S. plans neutralizes cost objections, allowing surgeons to emphasize the functional benefits. Disc height maintenance and segmental lordosis restoration further differentiate cervical arthroplasty, influencing guidelines and referral flows.

By Material: Ceramic-on-Polymer Disrupts Metal Dominance

Metal-on-polymer constructs delivered 59.10% of the artificial disc market share in 2025, yet ceramic-based systems now post a 15.82% CAGR—the segment’s fastest rate. Zirconia-toughened alumina reduces wear debris and eliminates the risks of metal ion hypersensitivity, which affects 10-15% of patients. Improved sintering methods have mitigated earlier concerns about brittleness, while radiolucency aids postoperative imaging. As MRI follow-up becomes routine, the advantage becomes even more pronounced. Price differentials are narrowing as ceramic supply chains scale, enabling broader payer acceptance. Manufacturers continue to combine titanium endplates with ceramic-polymer cores to strike a balance between osseointegration and articulation performance.

The move toward ceramics also aligns with patient marketing, as allergy-free, low-noise implants resonate with health-conscious demographics. Europe, with stringent metal-ion monitoring, leads in adoption and provides a template for other regions. Concurrently, R&D into gradient materials and hybrid constructs signals an innovation pipeline geared to erode metal’s historical lead further.

By Design: Non-Constrained Elastics Gain Momentum

Semi-constrained platforms accounted for 45.40% of the artificial disc market size in 2025, serving surgeons transitioning from rigid fusion paradigms. Demand is now tilting toward non-constrained elastic-core designs, which are growing at a 14.91% CAGR, propelled by their ability to replicate the viscoelastic moment-rotation curve of native discs. Elastic nuclei paired with fiber annuli disperse loads more evenly, potentially mitigating adjacent segment degeneration. Early five-year data show sustained range of motion and disc height preservation, boosting surgeon confidence. Constrained discs maintain a niche for instability-prone cases but are losing share as biomimetic alternatives validate long-term safety.

Device engineers employ finite-element optimization to tailor stiffness profiles and incorporate shock-absorbing layers. The result is precise motion restoration without sacrificing stability. Such performance gains underscore why the artificial disc market is moving from ‘replacement’ toward ‘replication’ of physiologic mechanics.

By Core Mobility: Fixed Core Regains Strategic Relevance

Mobile-core constructs generated 54.20% of the revenue in 2025, yet fixed-core models are growing at a 14.36% CAGR. Enhanced bearing geometry, made possible by advanced modeling, now enables fixed cores to mimic physiologic translation and rotation, while simplifying instrumentation. Surgeons value the lower risk of core escape and more predictable kinematics, especially in complex revisions. Material convergence—ceramic surfaces articulating with highly cross-linked polyethylene—reduces wear, bridging historical longevity gaps. Fixed-core systems also trim operative steps, favoring ASC adoption. These dynamics illustrate a maturing artificial disc market where multiple design philosophies coexist to match varied clinical indications.

By End-User: Ambulatory Centers Reshape Care Delivery

Hospitals generated 69.10% of the artificial disc market size in 2025, while ASCs chart the fastest growth at a 13.22% CAGR. Cost savings up to 60%, lower infection rates, and patient preference for same-day discharge underpin the shift. Surgeons benefit from block time flexibility and specialized teams, improving throughput. Payers are increasingly linking reimbursement to site-of-service efficiency, incentivizing ASC utilization. Orthopedic specialty clinics, although smaller, often pioneer new arthroplasty techniques before hospitals adopt them. This redistribution of case volume fortifies the artificial disc market’s resilience by diversifying service venues.

Geography Analysis

North America held a 37.60% market share in the artificial disc market in 2025, driven by favorable reimbursement, extensive spine-center networks, and the rapid adoption of AI-guided planning tools. Two-level cervical approvals expanded the eligible cohort, intensifying procedure counts. The region confronts reimbursement headwinds—Medicare’s age limit on lumbar disc arthroplasty persists—but private insurers are increasingly authorizing motion preservation based on cost-effectiveness evidence.

Europe ranks second, buoyed by public systems that acknowledge long-term economic gains from reduced adjacent segment disease. Germany and France are early adopters of ceramic-dominated platforms, leveraging their local expertise in biomaterials. Harmonized CE-Mark updates in 2025 clarified post-market surveillance requirements, smoothing market entry for next-generation discs. Aging demographics and wellness-oriented cultural norms are driving the growth of procedures across the continent.

The Asia-Pacific region is the fastest-growing, projected to grow at a 14.62% CAGR through 2031. Japan’s super-aged society and government-backed robotics programs channel investment into spine technologies. [3] China, via its volume-based procurement reforms, supports domestic manufacturing and accelerates time-to-market for locally developed discs. India’s Production Linked Incentive (PLI) scheme nurtures indigenous MedTech capacity, narrowing import dependency and lowering costs. Varied regulatory pathways create complexity, yet the overarching trajectory remains upward as healthcare access widens.

Competitive Landscape

Market concentration is moderate. Medtronic, Johnson & Johnson (DePuy Synthes), and Zimmer Biomet wield scale in R&D and distribution, yet niche innovators capture share through differentiated technology. Globus Medical extends its Advanced Materials Science line with porous titanium-PPEK hybrids, underscoring the shift toward material science leadership.

Strategic themes include portfolio consolidation, AI enablement, and ASC-centric implant kits. Johnson & Johnson MedTech spotlighted a digital orthopedics suite at AAOS 2025, integrating pre-op planning, navigation, and patient engagement under a unified cloud platform. M&A remains vibrant; acquisitions of robotics startups and biomaterials specialists fill capability gaps and quicken time-to-market. White-space opportunities emerge in adjacent segment disease prophylaxis and geriatric-friendly cervical systems, areas where newcomers may outrun incumbents tethered to legacy designs.

Artificial Disc Industry Leaders

Globus Medical

Centinel Spine, LLC

Medtronic Plc

Zimmer Biomet

B. Braun Melsungen AG (Aesculap)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Newly released Mayo Clinic-led research confirmed that multi-level cervical disc arthroplasty can be performed safely in outpatient settings.

- July 2025: Dymicron secured FDA IDE approval for its Triadyme-C cervical artificial disc, initiating a pivotal trial.

Global Artificial Disc Market Report Scope

According to the report's scope, an artificial disc, also known as a disc prosthesis, disc replacement, or spine arthroplasty device, is a medical device implanted in the spine to mimic the functions of a standard disc, which carries load and allows motion. The Artificial Disc Market is Segmented by Disc Type (Cervical Artificial Disc, and Lumbar Artificial Disc), Material Type (Metal on Metal, and Metal on Polymer), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Cervical Artificial Disc |

| Lumbar Artificial Disc |

| Metal-on-Metal |

| Metal-on-Polymer |

| Ceramic-on-Polymer |

| Constrained (Fixed-Core) |

| Semi-Constrained (Mobile-Core) |

| Non-Constrained (Elastic-Core) |

| Fixed Core |

| Mobile Core |

| Hospitals |

| Orthopedic & Spine Specialty Clinics |

| Ambulatory Surgical Centers (ASCs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disc Type | Cervical Artificial Disc | |

| Lumbar Artificial Disc | ||

| By Material | Metal-on-Metal | |

| Metal-on-Polymer | ||

| Ceramic-on-Polymer | ||

| By Design | Constrained (Fixed-Core) | |

| Semi-Constrained (Mobile-Core) | ||

| Non-Constrained (Elastic-Core) | ||

| By Core Mobility | Fixed Core | |

| Mobile Core | ||

| By End-User | Hospitals | |

| Orthopedic & Spine Specialty Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Artificial Disc market in 2026?

The market is valued at USD 4.17 billion in 2026 and is projected to reach USD 7.45 billion by 2031.

Which disc type is growing fastest?

Cervical disc replacements are advancing at a 15.16% CAGR, outpacing lumbar devices thanks to favorable anatomy and strong clinical data.

Why are ceramic-on-polymer implants gaining traction?

Ceramic bearings lower wear debris, eliminate metal ion concerns, and improve imaging clarity, driving a 15.82% CAGR in this material segment.

What drives ASC adoption for disc arthroplasty?

Outpatient settings reduce procedure costs by up to 60% and offer shorter recovery, fueling a 13.22% CAGR in ASC case volume.

Which region is the quickest to grow?

Asia-Pacific will expand at 14.62% CAGR as aging populations and healthcare investments raise procedure demand.

Page last updated on: