Patient Derived Xenograft Models Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

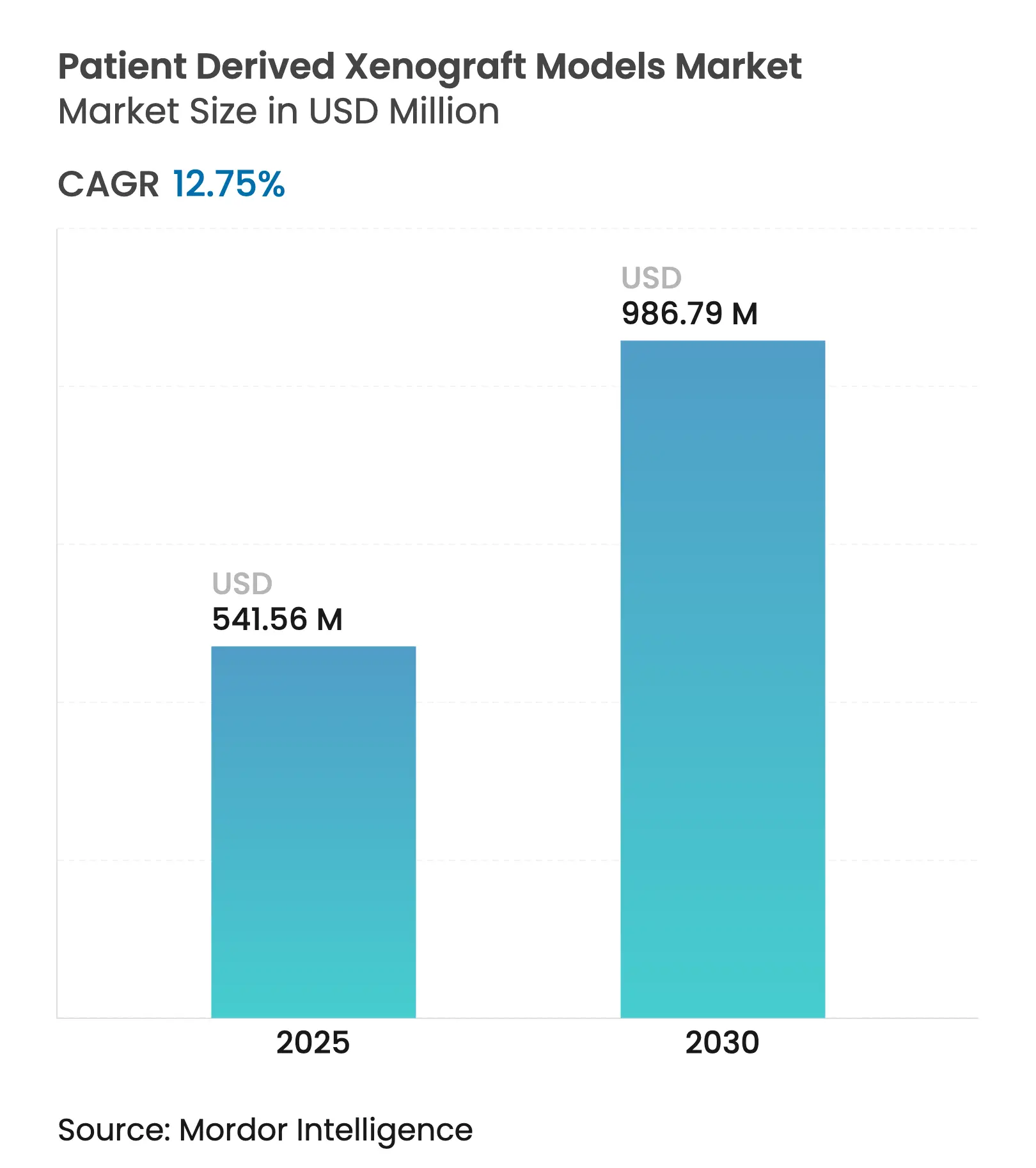

| Market Size (2025) | USD 541.56 Million |

| Market Size (2030) | USD 986.79 Million |

| Growth Rate (2025 - 2030) | 12.75 % CAGR |

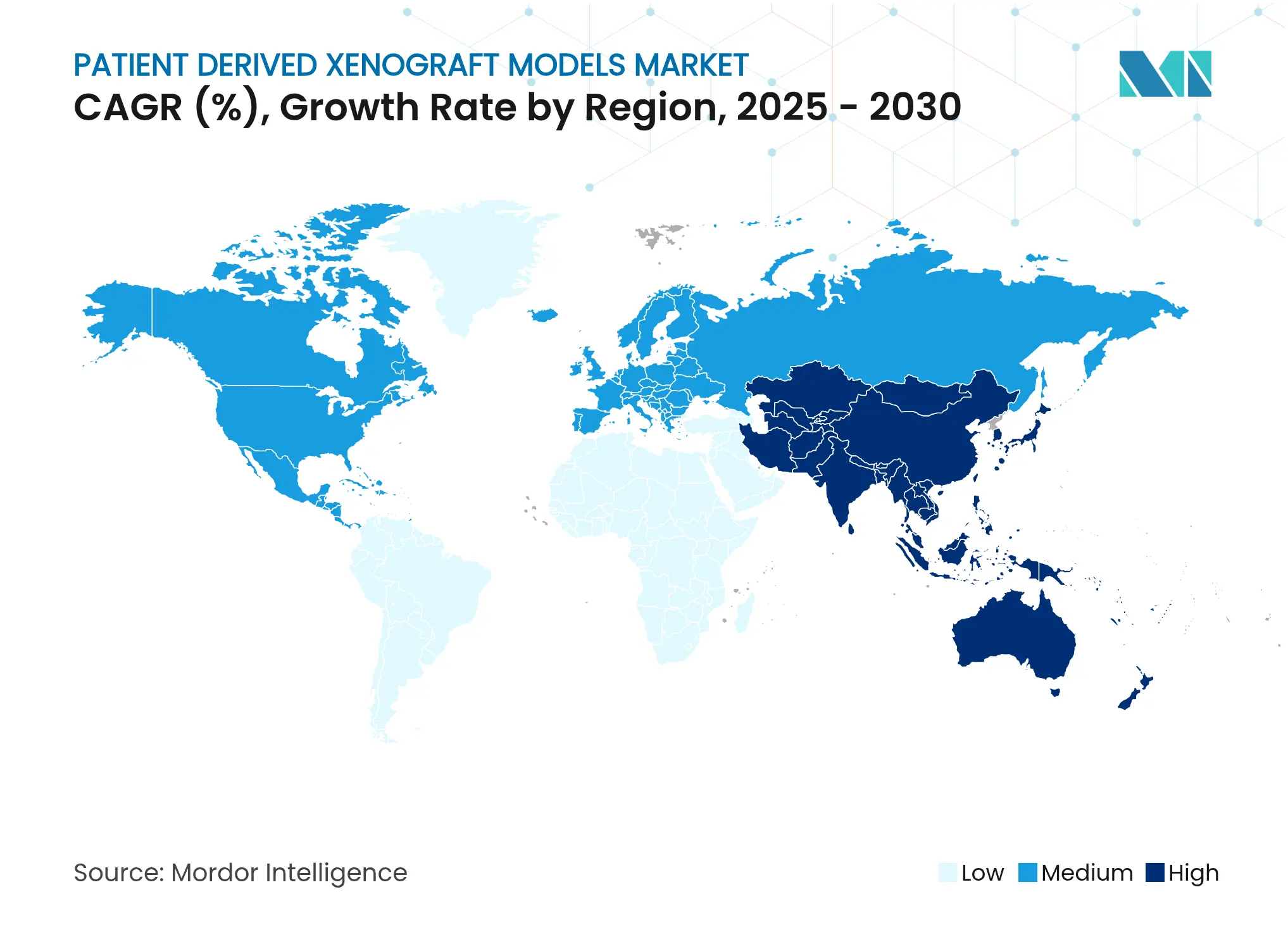

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Patient Derived Xenograft Models Market Analysis by Mordor Intelligence

The patient-derived xenograft models market is valued at USD 541.56 million in 2025 and is projected to reach USD 986.79 million by 2030, expanding at a 12.75% CAGR. Growth stems from the rising global cancer burden, modernized regulations that recognize PDX data in investigational filings, and steady improvements in humanized mouse, zebrafish, and AI-integrated imaging platforms. Federal oncology funding, notably the USD 650 million Peer Reviewed Cancer Research Program, preserves a pipeline of translational studies that rely on patient-derived xenografts for target validation and efficacy profiling. Consolidation among suppliers, paired with strategic acquisitions targeting rare-tumor assets, is reshaping competitive dynamics as larger players look to embed CRISPR-engineered, immune-humanized platforms within integrated discovery workflows.

Key Report Takeaways

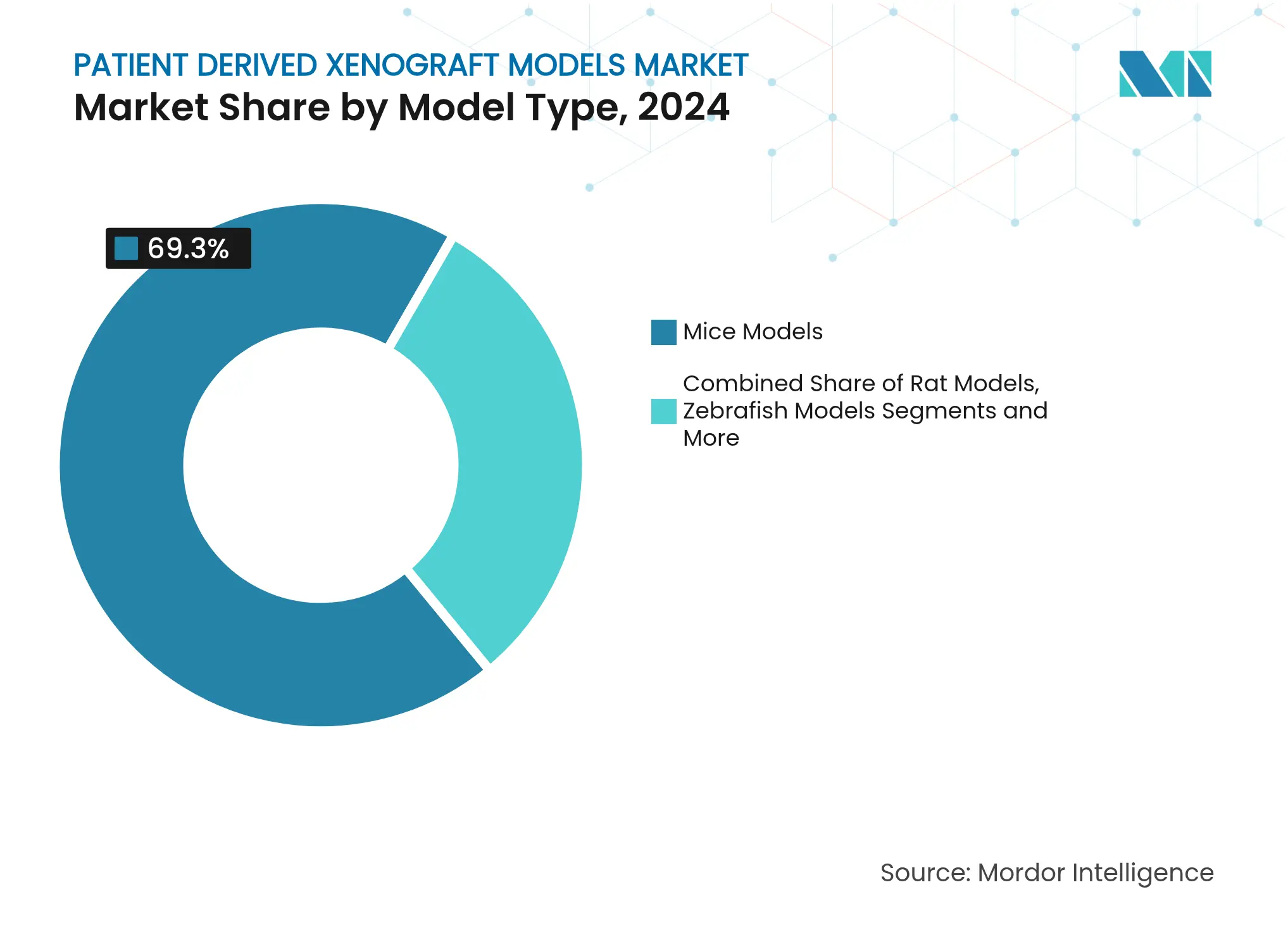

- By model type, mice platforms led with 69.35% revenue share in 2024, while zebrafish models are forecast to record a 14.25% CAGR through 2030.

- By tumor type, gastro-intestinal xenografts held 28.53% of the patient-derived xenograft models market share in 2024; hematological models are advancing at a 13.85% CAGR to 2030.

- By engraftment technique, orthotopic implantation accounted for 45.82% of the patient-derived xenograft models market size in 2024, whereas subcutaneous methods expand at 13.31% CAGR.

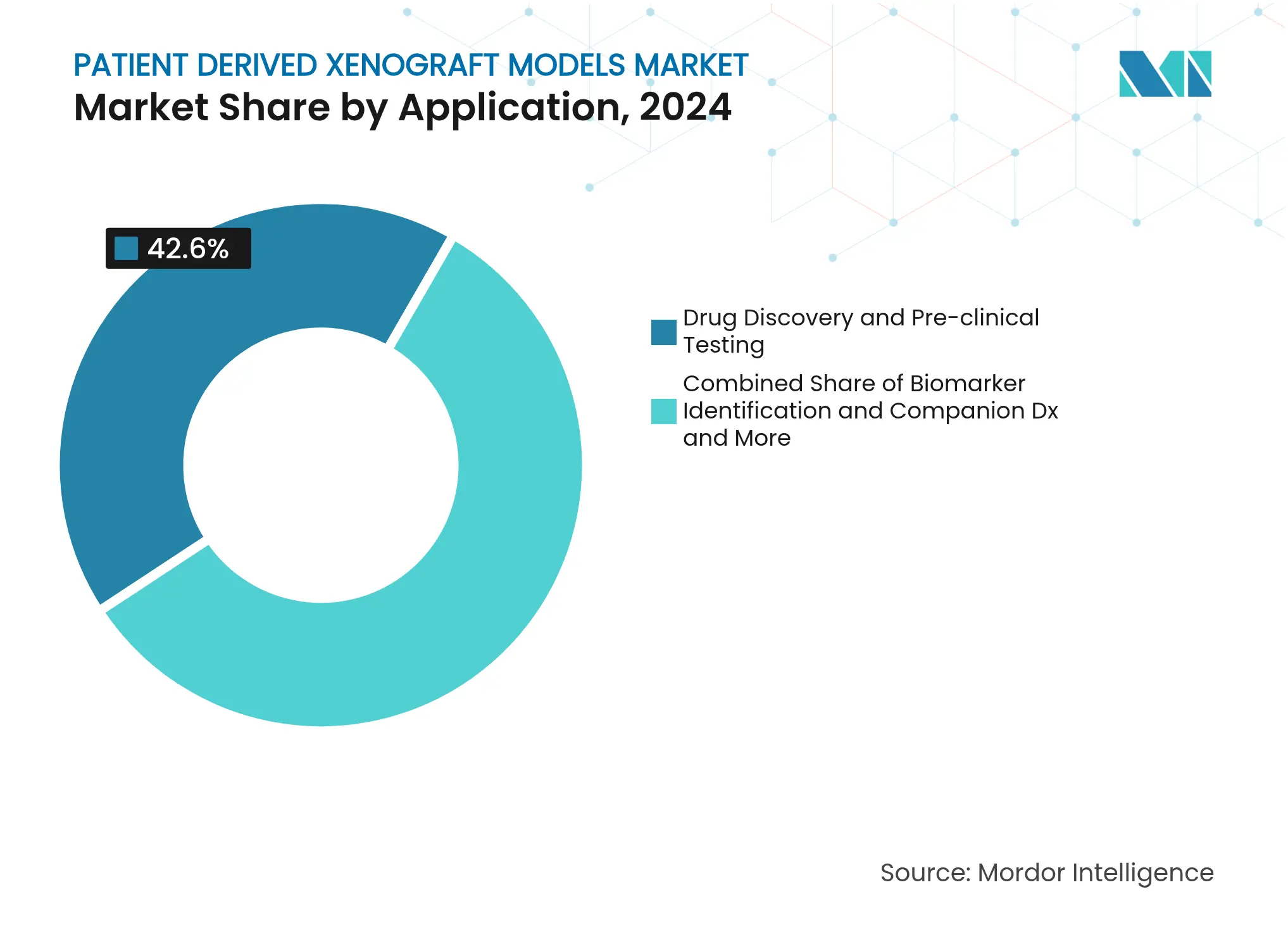

- By application, drug-discovery studies maintained 42.63% revenue share in 2024; personalized oncology avatar trials climb at a 15.25% CAGR through 2030.

- By end user, pharmaceutical and biotechnology companies captured 60.36% of 2024 spending, while CRO revenue is projected to increase at 14.57% CAGR to 2030.

- By geography, North America dominated with 44.63% share in 2024; Asia-Pacific is poised for a 13.27% CAGR through 2030.

Global Patient Derived Xenograft Models Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Incidence & Earlier Detection Of Cancer

Rising Incidence & Earlier Detection Of Cancer

| +2.5% | Global, with early gains in North America, EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.5% | Geographic Relevance:

Global, with early gains in North America, EU

| Impact Timeline:

Medium term (2-4 years)

|

Surge In Pharma/Biotech R&D Outsourcing To CROs

Surge In Pharma/Biotech R&D Outsourcing To CROs

| +1.8% | APAC core, spill-over to MEA | Short term (≤ 2 years) | |||

Favorable Regulatory Acceptance Of PDX Data In IND Filings

Favorable Regulatory Acceptance Of PDX Data In IND Filings

| +1.5% | North America & EU | Medium term (2-4 years) | |||

Growing Public–Private Oncology Funding Pools

Growing Public–Private Oncology Funding Pools

| +2.2% | Global | Long term (≥ 4 years) | |||

Emergence Of CRISPR-Engineered, Humanized PDX Models

Emergence Of CRISPR-Engineered, Humanized PDX Models

| +1.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

Integration Of AI-Enabled Imaging & Digital Biomarker

Analytics

Integration Of AI-Enabled Imaging & Digital Biomarker

Analytics

| +1.7% | Global, with early gains in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising cancer incidence & earlier detection

Global oncology incidence reached 20 million new cases in 2022, and forecasts point to 35 million by 2050, a trend that multiplies demand for clinically relevant pre-clinical systems. In the United States, 2,041,910 new cases were logged during 2025, with faster growth observed in women under 50, thereby requiring tumor models that capture age-specific biology. Earlier diagnosis programs enlarge the population eligible for precision therapies, and PDX platforms replicate patient heterogeneity better than immortalized cell lines. Public investments such as ARPA-H’s USD 25 million at-home multi-cancer screening initiative create downstream demand for xenografts that evaluate subtype-specific regimens[1]Advanced Research Projects Agency for Health, “ARPA-H launches program to develop at-home multi-cancer screening test,” arpa-h.gov. Collectively, these forces sustain double-digit expansion across the patient-derived xenograft models market.

Surge in pharma/biotech R&D outsourcing to CROs

Pharmaceutical pipelines added hundreds of early-stage programs during 2024–2025, stretching in-house capacity and steering sponsors toward external partners with turnkey xenograft capabilities. Leading Asian CROs report record revenues, underpinned by cost advantages and expanded vivarium space that accommodates large PDX colonies. Integrated CRDMO offerings unite model generation, pharmacology, bioanalytics, and clinical supply, shrinking timelines and lowering coordination risk. As outsourcing becomes the default option for complex studies, contract providers specialising in PDX services achieve above-market growth and reinforce regional leadership in China, Singapore, and India. The broader outsourcing wave, therefore, propels incremental demand across the patient-derived xenograft models market.

Regulatory acceptance of PDX data in IND filings

The FDA’s April 2025 plan to eliminate mandatory animal testing for monoclonal antibodies legitimises human-relevant pre-clinical evidence, positioning PDX datasets as primary proof in novel drug applications. NIH’s pledge to align with the agency cements a US-wide policy shift favouring models that recapitulate patient biology. Europe’s Directive 2010/63/EU reinforces similar expectations by promoting the Three Rs principle, creating a trans-Atlantic consensus that accelerates PDX adoption. Sponsors now treat xenografts as credible primary evidence for efficacy and safety, unlocking fresh commercial opportunities throughout the patient-derived xenograft models market.

Emergence of CRISPR-engineered, humanized PDX models

Genome-editing advances enable insertion of patient-matched HLA and cytokine-support genes into immunodeficient mice, producing sophisticated platforms such as MISTRG that resolve earlier engraftment gaps in hematologic disease modelling. These models sustain functional human immune compartments, critical for immuno-oncology studies and antibody screening. Vendors that combine CRISPR toolkits with proprietary xenograft libraries secure competitive differentiation, particularly when layered with AI-guided biomarker analytics. The technology therefore injects long-term growth momentum into the patient-derived xenograft models market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost & Lengthy Timelines Versus 3-D Organoid

Alternatives

High Cost & Lengthy Timelines Versus 3-D Organoid

Alternatives

| -1.2% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.2%

| Geographic Relevance:

Global

| Impact Timeline:

Short term (≤ 2 years)

|

Stringent Animal-Welfare Regulations & Ethical

Scrutiny

Stringent Animal-Welfare Regulations & Ethical

Scrutiny

| -0.8% | North America & EU | Medium term (2-4 years) | |||

Limited Engraftment Success For Hematologic &

Immune-Rich Tumors

Limited Engraftment Success For Hematologic &

Immune-Rich Tumors

| -0.9% | Global | Medium term (2-4 years) | |||

Competitive Uptake Of In-Silico & Organ-On-Chip Models

Competitive Uptake Of In-Silico & Organ-On-Chip Models

| -1.1% | Global, with early gains in North America, EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High cost & lengthy timelines versus 3-D organoid alternatives

Patient-derived organoids form within weeks and run on lower budgets than several-month PDX engraftments, narrowing the economic appeal of animal studies. Organoid-on-chip systems integrate perfusion bioreactors, enabling dynamic drug exposure assays that enhance throughput and reduce reagent use. Regulators are increasingly receptive to such in-vitro platforms, adding near-term pressure on sponsors to justify animal work. These cost-time considerations shave up to 1.2 percentage points from the forecast CAGR but do not negate the long-term relevance of PDX for whole-organism pharmacology studies.

Stringent animal-welfare regulations & ethical scrutiny

The commitment by US and EU agencies to curtail animal studies heightens protocol review stringency and imposes refinements that elevate per-study costs[2]Nature Protocols, “The OBSERVE guidelines provide refinement criteria for rodent oncology models,” nature.com. Institutional Animal Care and Use Committees now demand proof that no in-vitro alternative can achieve the same scientific objective. Public campaigns questioning animal research methods add reputational concerns that can influence investor decisions. Although these pressures subtract 0.8 percentage points from forecast growth, suppliers that demonstrate welfare-minded practices—such as virtual control groups or reduced animal cohorts—are mitigating impact across the patient-derived xenograft models market.

Segment Analysis

By Model Type: Mice Platforms Maintain Scale Edge

Mice xenografts represent USD 375 million of 2025 revenue and held 69.35% share in 2024, a position supported by well-defined immunocompromised strains and extensive historical datasets. The patient-derived xenograft models market size for mice-based platforms is projected to reach USD 670 million by 2030, equal to a 12.1% CAGR, as CRISPR engineering embeds fully human cytokine circuits to improve immune-oncology modelling. Although scale advantages persist, growth tapers relative to alternative organisms.

Zebrafish models deliver the fastest rise at 14.25% CAGR on the strength of transparent embryos and automated screening lines that enable rapid compound efficacy assessment. Low maintenance cost and high fecundity make zebrafish attractive for early phenotypic screens, prompting sponsors to deploy dual-organism strategies that marry zebrafish speed with murine translational depth. This complementary usage sustains expansion across the patient-derived xenograft models market while preventing direct cannibalisation of mice revenue.

Note: Segment shares of all individual segments available upon report purchase

By Tumor Type: GI Segment Holds the Revenue Lead

Gastro-intestinal xenografts generated 28.53% of 2024 billings, equating to USD 154 million, and are projected to reach USD 278 million by 2030 at an 11.9% CAGR, anchored in colorectal and pancreatic indications. Orthotopic colon models replicate metastatic cascades to liver and lung, a capability mandatory for anti-metastatic drug screening. Consequently, researchers continue prioritising GI tissues within their patient-derived xenograft models market budgets.

Hematological malignancy xenografts expand 13.85% per annum, driven by MISTRG and similar cytokine-humanised mouse innovations that overcome prior engraftment failures in acute myeloid leukaemia and myelodysplastic syndrome. As these platforms mature, sponsors gain access to clinically faithful blood-cancer avatars that guide combination therapy design. The resulting volume uptick further diversifies demand across the patient-derived xenograft models market.

By Engraftment Technique: Orthotopic Relevance Versus Subcutaneous Speed

Orthotopic implantation captured 45.82% of 2024 outlays and is forecast to deliver USD 420 million by 2030, reflecting its unmatched capacity to preserve host-organ microenvironments and metastatic tropism. The patient-derived xenograft models market size attached to orthotopic work is expected to expand at 11.5% CAGR, partly constrained by surgical complexity and extended setup times.

Subcutaneous implantation, while less physiologically faithful, benefits from simplified surgery and easy caliper measurement, fuelling 13.31% CAGR to 2030. Sponsors increasingly combine first-pass subcutaneous screening with later orthotopic confirmation, equalising quality and cost. Automated stereotactic devices under development should further boost reproducibility and reduce operator variability, enhancing value creation for the patient-derived xenograft models market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: Drug Discovery Dominance Gives Way to Avatar Acceleration

Drug discovery and toxicology protocols accounted for 42.63% revenue in 2024, representing USD 231 million, and will likely climb to USD 415 million by 2030 at a steady 10.7% CAGR. These programmes rely on extensive dose-response and biomarker correlation studies that remain difficult to replicate in vitro.

Personalised avatar trials are, however, expanding at 15.25% CAGR, lifting their slice of the patient-derived xenograft models market above USD 200 million by 2030. Time-matched engraftment and high-throughput drug screens permit clinicians to tailor therapies within actionable windows, especially when supported by AI-driven multi-omic analytics. This evolution signals an era where individualised decision support adds fresh value beyond traditional discovery contracts.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharma Leads, CROs Accelerate

Pharmaceutical and biotechnology sponsors commanded 60.36% spending in 2024, equating to USD 327 million, and will reach USD 560 million by 2030 at 11.2% CAGR as internal discovery operations remain reliant on proprietary xenograft panels. The patient-derived xenograft models market share scales back marginally as outsourcing intensifies.

CRO revenue is climbing at 14.57% CAGR, lifting its slice from 26% in 2024 to nearly one-third by 2030, driven by end-to-end PDX services, AI-enabled analytics, and virtual control cohorts that cut animal usage. Academic centres remain critical innovators but allocate lower budget shares, relying on grant support.

Geography Analysis

North America generated 44.63% of 2024 revenue on the back of USD 4 billion-plus federal cancer funding, extensive biopharma pipelines, and proactive regulatory stances that recognise PDX evidence in IND submissions[3]National Cancer Institute, “Cancer Grand Challenges announces new teams,” cancer.gov. The region’s forecast CAGR of 11.4% reflects a mature but still expanding customer base that prioritises CRISPR-humanised mice and AI-enabled imaging. Strategic consortia such as PDXNet ensure protocol standardisation, lowering technical barriers for new entrants.

Asia-Pacific is the growth pacesetter at 13.27% CAGR, supported by rising oncology incidence, cost-efficient CRO capacity, and government initiatives that incentivise digital biomarker R&D. China and Singapore are establishing expansive vivariums, while Japan leverages strong regulatory clarity to attract multinational trials. Combined, these factors increase the region’s importance within global procurement strategies for the patient-derived xenograft models market.

Europe maintains a balanced 10.2% CAGR, anchored in rigorous academic research and progressive welfare rules that reward refined xenograft practices. Harmonised quality frameworks and public-private projects such as Cancer Grand Challenges keep utilisation high, although cost pressures encourage selective outsourcing to lower-cost geographies. The continent thus remains an essential but efficiency-focused contributor to patient-derived xenograft models market volumes.

Competitive Landscape

Market Concentration

Moderate concentration characterises the field as top providers integrate vertical capabilities while smaller specialists capture niche tumour types. Charles River, the most diversified supplier, strengthened its portfolio through alliances covering virtual control groups, lentiviral manufacturing, and AI-guided discovery services. Merck KGaA’s pending USD 3.9 billion SpringWorks purchase exemplifies big-pharma appetite for assets that leverage PDX-validated oncology pipelines.

Technology leadership hinges on fusing CRISPR gene editing with multi-modal imaging and machine learning to produce immune-competent, data-rich xenografts. Firms offering such integrated platforms achieve premium pricing and longer contract tenures. Meanwhile, disruptive zebrafish avatar providers entice early-stage biotech budgets, demonstrating rapid turnaround times that mitigate patient-care lag. The competitive field is repositioning around these differentiated capabilities, creating acquisition targets among data-analytics start-ups and specialty vivarium operators.

Regulatory modernisation works as both catalyst and challenge: players ready with non-rodent models and validated digital readouts can seize early-mover advantage, whereas firms tied to older mouse colonies risk margin compression. Viewed collectively, strategic depth rather than sheer colony size is becoming the primary determinant of success across the patient-derived xenograft models market.

Patient Derived Xenograft Models Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NIH aligns with FDA to curtail animal testing across funded studies, accelerating demand for human-relevant PDX alternatives.

- April 2025: FDA outlines a 3-to-5-year timetable to phase out animal testing requirements for monoclonal antibodies, elevating PDX data as pivotal evidence in IND filings.

Table of Contents for Patient Derived Xenograft Models Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence & Earlier Detection Of Cancer

- 4.2.2Surge In Pharma/Biotech R&D Outsourcing To Cros

- 4.2.3Favorable Regulatory Acceptance Of PDX Data In IND Filings

- 4.2.4Growing Public-Private Oncology Funding Pools

- 4.2.5Emergence Of CRISPR-Engineered, Humanized PDX Models

- 4.2.6Integration Of AI-Enabled Imaging & Digital Biomarker Analytics

- 4.3Market Restraints

- 4.3.1High Cost & Lengthy Timelines Versus 3-D Organoid Alternatives

- 4.3.2Stringent Animal-Welfare Regulations & Ethical Scrutiny

- 4.3.3Limited Engraftment Success For Hematologic & Immune-Rich Tumors

- 4.3.4Competitive Uptake Of In-Silico & Organ-On-Chip Models

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Model Type

- 5.1.1Mice Models

- 5.1.1.1Nude (Athymic)

- 5.1.1.2NOD/SCID

- 5.1.1.3NSG

- 5.1.1.4Humanized Mice

- 5.1.2Rat Models

- 5.1.3Zebrafish Models

- 5.1.4Avian CAM Models

- 5.2By Tumor Type

- 5.2.1Gastro-intestinal Tumors

- 5.2.2Gynecological Tumors

- 5.2.3Respiratory (Thoracic) Tumors

- 5.2.4Central Nervous System Tumors

- 5.2.5Hematological Malignancies

- 5.2.6Dermatological (Melanoma) Tumors

- 5.2.7Other Solid Tumors

- 5.3By Engraftment Technique

- 5.3.1Heterotopic (Subcutaneous) Implantation

- 5.3.2Orthotopic Implantation

- 5.4By Application

- 5.4.1Drug Discovery & Pre-clinical Testing

- 5.4.2Biomarker Identification & Companion Dx

- 5.4.3Personalized Oncology (Avatar Trials)

- 5.4.4Translational & Co-clinical Trials

- 5.5By End User

- 5.5.1Pharmaceutical & Biotechnology Companies

- 5.5.2Contract Research Organizations (CROs)

- 5.5.3Academic & Research Institutions

- 5.5.4Others

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Champions Oncology

- 6.3.2Charles River Laboratories

- 6.3.3Crown Bioscience

- 6.3.4WuXi AppTec

- 6.3.5Oncodesign

- 6.3.6Hera BioLabs

- 6.3.7EPO Berlin-Buch GmbH

- 6.3.8Pharmatest Services Ltd

- 6.3.9Urolead

- 6.3.10Xentech

- 6.3.11The Jackson Laboratory

- 6.3.12Explora BioLabs

- 6.3.13Inotiv Inc.

- 6.3.14Models Genetix

- 6.3.15GEMPharmatech

- 6.3.16Envigo

- 6.3.17Novotech

- 6.3.18SOPHiA GENETICS

- 6.3.19Shanghai LIDE Biotech

- 6.3.20Reaction Biology Corp.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Patient Derived Xenograft Models Market Report Scope

As per the scope of the report, patient-derived xenografts (PDX) are models in which cancerous tissue from a patient's tumor is implanted directly into humanized mice or rats. The xenograft model offers fast testing of novel compounds on cancer cell lines. The Patient Derived Xenograft Models Market is Segmented By Type (Mice Model, Rats Model), Tumor Type (Gastrointestinal Tumor Model, Gynecological Tumor Model, Respiratory Tumor Model, and Other Tumor Model), End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutions, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and Rest of the World). The report offers the value (in USD million) for the above segments.