Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

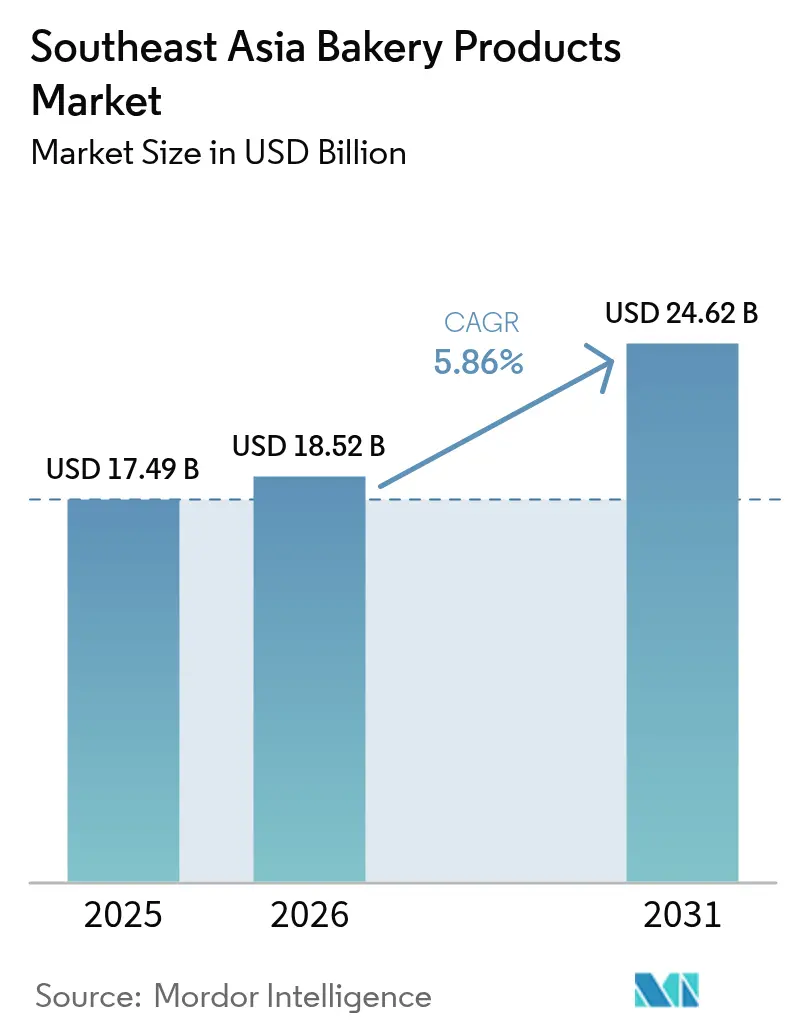

| Base Year Market Size (2025) | USD 17.49 Billion |

| Market Size (2026) | USD 18.52 Billion |

| Market Size (2031) | USD 24.62 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Bakery Products Market Analysis by Mordor Intelligence

Southeast Asia bakery products market size in 2026 is estimated at USD 18.52 billion, growing from 2025 value of USD 17.49 billion with 2031 projections showing USD 24.62 billion, growing at 5.86% CAGR over 2026-2031. Demographic momentum, higher disposable incomes, and a visible tilt toward Western-style consumption in urban centers underpin this expansion. The market’s steady uptrend also mirrors the deepening middle-class footprint across Indonesia, Vietnam, and the Philippines, where consumers increasingly balance indulgence with wellness cues in daily food choices. Domestic baked-goods manufacturers are scaling production in step with modern retail rollouts, while global brands leverage franchising to accelerate store counts. At the same time, supply-side efficiencies from regional flour-milling investments and diversified wheat sourcing temper cost volatility and sharpen margins for large and mid-sized players.

Key Report Takeaways

- By product type, cakes, pastries, and sweet pies led with 42.10% of the Southeast Asia bakery products market share in 2025, followed by crackers and savory biscuits, which are forecast to advance at a 7.26% CAGR through 2031.

- By form, fresh bakery dominated 60.55% of the Southeast Asia bakery products market size in 2025. Frozen bakery is projected to expand fastest, supported by emerging cold-chain investments that unlock wider geographic reach.

- By distribution channel, specialty stores and artisanal bakeries accounted for 40.20% of sales in 2025, while online retailers are expected to record the highest forecast CAGR of 10.92% from 2026 to 2031.

- By geography, Indonesia accounted for 27.60% of the 2025 value, while Vietnam is set to grow at a 7.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of modern grocery retail formats | +1.2% | Indonesia, Philippines, Vietnam with spillover to Thailand | Medium term (2-4 years) |

| Rapid rise of video-commerce for impulse bakery purchases | +0.8% | Vietnam, Thailand, Singapore with early adoption in urban centers | Short term (≤ 2 years) |

| Flour-milling capacity expansions lowering input costs | +0.9% | Indonesia, Philippines, Malaysia with regional supply chain benefits | Long term (≥ 4 years) |

| Micro-retail digitalisation enabling rural reach | +0.7% | Indonesia, Vietnam, Myanmar with focus on tier 2-3 cities | Medium term (2-4 years) |

| Health-oriented reformulations (high-fibre, gut-health) | +0.6% | Singapore, Malaysia, Thailand with premium segment focus | Long term (≥ 4 years) |

| Government push for wheat import diversification | +0.4% | Regional, with primary impact in Indonesia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Modern Grocery Retail Formats

Supermarket and hypermarket footprints continue to widen across large metros and tier-2 cities, giving packaged bread and pastry brands premium shelf space and stable refrigeration. The modern-trade channel’s organized layout enhances product visibility, enables date-coded inventory rotation, and supports value-added features such as resealable packaging. As retail chains refine planograms, in-store bakeries flourish by coupling fresh aromas with impulse-driven displays. Large chains also extend private-label lines, offering affordability while standardizing quality benchmarks that smaller traditional outlets struggle to match. The broader retail formalization trend, therefore, remains a structural engine for the Southeast Asia bakery products market.

Rapid Rise of Video-Commerce for Impulse Bakery Purchases

Live-stream commerce blends entertainment with instant purchasing, allowing bakers to demonstrate product freshness and craftsmanship in real time. With smartphone penetration exceeding 80% in urban pockets, consumers gravitate to short, interactive sessions that showcase limited-edition cakes, seasonal cookies, or buy-one-get-one bundles. Integrated payment gateways eliminate checkout friction, while last-mile couriers deliver within hours, sustaining product integrity and spontaneous satisfaction. Brands that invest in charismatic hosts and on-screen baking theatrics capture new audiences at lower customer-acquisition costs compared with traditional advertising. Consequently, video-commerce’s experiential pull is enlarging the consumer base for the Southeast Asia bakery products market.

Flour-Milling Expansion and Wheat-Source Diversification

Indonesia’s Bogasari and the Philippines’ Universal Robina have recently expanded daily milling throughput, unlocking scale economies that compress per-unit costs. Parallel policy pushes to broaden wheat origins beyond historic suppliers buffer raw-material price swings and strengthen bargaining positions during global supply shocks. Together, higher milling capacity and diversified sourcing feed a steadier pipeline of competitively priced flour to downstream bakers, anchoring profit stability even when ocean-freight markets gyrate. Over the long term, these supply-chain gains translate into more predictable margins and calibrated price points for consumers, reinforcing demand growth across value tiers .

Digital Micro-Retail and Health-Focused Reformulations

Digitalization platforms now plug hundreds of thousands of warungs and sari-sari stores into real-time ordering systems, enabling bakeries to dispatch mixed loads efficiently to rural and peri-urban districts. Simultaneously, reformulation efforts introduce high-fiber, gut-health, and gluten-free breads that satisfy wellness-oriented shoppers without sacrificing taste. Ingredient innovators turn to green banana flour, resistant-starch-rich barley, and plant-based proteins to widen product repertoires. The dual thrust of expanded last-mile reach and clearly signaled functional benefits elevates penetration among households newly attuned to both convenience and nutrition. This synergy continues to lift value sales for the Southeast Asia bakery products market

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat import prices amid El Niño freight spikes | -1.8% | Regional, with acute impact in Philippines, Indonesia, Vietnam | Short term (≤ 2 years) |

| Halal-certification bottlenecks for new SKUs | -0.9% | Indonesia, Malaysia, Brunei with spillover to Muslim consumer segments | Medium term (2-4 years) |

| Tight cold-chain infrastructure for frozen dough | -0.7% | Myanmar, Vietnam, rural areas across region | Long term (≥ 4 years) |

| Rising sugar-tax discussions in Thailand & Malaysia | -0.4% | Thailand, Malaysia with potential regional contagion effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Wheat Import Prices Amid El Niño Freight Spikes

Shipping-lane disruptions have inflated container rates, adding unplanned cost layers to imported wheat destined for Indonesia, the Philippines, and Vietnam. Since local grain alternatives remain limited, millers pass on at least part of the burden to bakeries, pressuring the shelf prices of staple bread. Retail promotions and pack-downs mitigate volume erosion, yet margin squeeze persists for smaller manufacturers with thin working capital. Hedging strategies and diversified supplier contracts partly offset risk, but near-term volatility continues to weigh on the Southeast Asia bakery products market.

Certification, Logistics, and Fiscal Hurdles

Indonesia’s rigorous halal framework extends approval lead times to about four months per new SKU, raising compliance costs and delaying innovation pipelines. Concurrently, patchy cold-chain infrastructure hampers frozen-dough distribution to secondary cities, limiting assortment breadth outside major metros. On the fiscal front, Thailand and Malaysia have revived sugar-tax deliberations that would elevate ingredient costs for high-sucrose recipes, spurring reformulation but also stoking price increases. Together, these factors temper growth momentum, especially for SMEs seeking rapid across-border scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premiumization Meets Functional Demand

Cakes, pastries, and sweet pies commanded 42.10% of the Southeast Asia bakery products market in 2025, lifting celebratory sales around festivals and personal milestones. Local chains replicate European patisserie aesthetics while overlaying familiar flavors such as pandan and durian, keeping relevance high. Concurrently, crackers and savoury biscuits post the fastest volume gains, propelled by 7.26% CAGR expectations amid snack-on-the-go lifestyles and portion-control preferences. Manufacturers combine multigrain bases with reduced-sugar glazing to widen appeal, and e-commerce bundles encourage pantry stocking for remote work routines. Regional exporters also target halal-certified savoury biscuits to serve Muslim diaspora channels in the Middle East, reinforcing outbound opportunities for the Southeast Asia bakery products market.

Rising health consciousness steers reformulation toward high-fiber, gut-friendly inclusions such as beta-glucan-rich barley and inulin. Brands emphasize digestive comfort and blood-sugar moderation on front-of-pack labels to secure premium shelf prices. Gluten-free ranges, once niche, now attract mainstream curiosity, especially in Singapore and Thailand, where affluent consumers trial novel grains. Co-branding with specialty ingredient suppliers boosts perceived credibility. These dynamics suggest the crackers segment will keep outpacing the broader Southeast Asia bakery products market while indulgent cakes retain a stable, albeit slower, value base.

By Form: Fresh Dominance Despite Frozen Infrastructure Gaps

Fresh lines generated 60.55% of 2025 revenue, illustrating Southeast Asians’ cultural regard for morning-baked bread and pastries. Supermarket in-store bakeries, high-street artisan outlets, and café chains synchronize bake times with commuter peaks, maximizing aroma-driven footfall. Local grain blends and tropical fruit fillings offer flavor distinctiveness without sacrificing convenience. The Southeast Asia bakery products market size for fresh bread is expected to widen further as urban density favors walk-to retail clusters.

Frozen dough and par-baked offerings occupy 7.34%, constrained by fragmented cold-chain nodes. Urban quick-service restaurants nevertheless adopt freeze-thaw inventory to uphold 24-hour availability with lower labor inputs. Investment in reefer trucks and micro-fulfillment centers is accelerating, with logistics providers extending pay-as-use pallets to SME bakers. Such infrastructure, paired with rising preference for home-baking kits, positions the frozen segment to narrow the share gap over the long term, bolstering variety access across the Southeast Asia bakery products market

By Distribution Channel: Digital and Specialty Channels Reshape Access

Specialty stores and artisanal bakeries captured 40.20% distribution share in 2025, capitalizing on handcrafted positioning and immediate freshness. Interior design cues such as open kitchens and aroma vents reinforce experiential resonance, driving higher average tickets per visit. Café culture further entrenches pastry-plus-beverage bundles, sustaining store traffic beyond breakfast. Brick-and-mortar resonance earns ongoing loyalty even as digital options proliferate, anchoring a stable pillar in the Southeast Asia bakery products market.

Online retailers, projected at 10.92% CAGR, ride the expansion of food-delivery platforms and quick-commerce hubs. Flash-sale events and time-limited vouchers stimulate off-peak orders, smoothing production loads for bakeries. Subscription models supplying weekly bread boxes gain traction among young families seeking convenience and portion predictability. Meanwhile, supermarkets grow assortments of pre-packed loaves; convenience stores double down on ready-to-eat croissants that claim shelf visibility at eye level. This blend of traditional craft and digital ease drives omni-channel complexity yet unlocks broader consumption occasions.

Geography Analysis

In 2025, Indonesia, buoyed by its 270 million population and an expanding middle class, commanded a significant 27.60% share of the market's value. Urban consumers flock to chain-owned convenience stores, while their rural counterparts utilize digital "warung" platforms, paving the way for branded snacks. Bogasari, a leading domestic milling giant, adeptly manages wheat throughput, shielding against foreign-exchange fluctuations and ensuring price stability. With stringent regulatory oversight on halal compliance, multinationals are increasingly opting for local joint ventures, expediting their label approval processes. Consequently, Indonesia's bakery products market in Southeast Asia continues to thrive, both in volume and value. Vietnam, on track for a 7.22% CAGR, is riding the wave of its USD 79.3 billion food-processing industry, a vibrant café culture, and a surge in social commerce. Western bakery chains share the stage with local brands, infusing products with native ingredients like coffee and coconut. Gen-Z's strong brand loyalty drives limited-edition releases, often sold through live streams, bolstering premium pricing. Meanwhile, the government tightens food-safety protocols, notably aflatoxin limits in flour, elevating industry standards.

Singapore and Malaysia carve out distinct roles: Singapore as an innovation hub and Malaysia as a center for halal exports. Retailers in Singapore harness real-time analytics for category management, leading to micro-assortment tweaks that boost shelf efficiency. In Malaysia, state-sponsored halal grants promote automation, balancing compliance with cost reduction. Thailand's push for a sugar-reduction strategy accelerates the adoption of whole-grain bread, while Myanmar, with its limited local capacity, relies on imported mixes. Together, these national stories create a rich and interconnected demand landscape for Southeast Asia's bakery products market.

Competitive Landscape

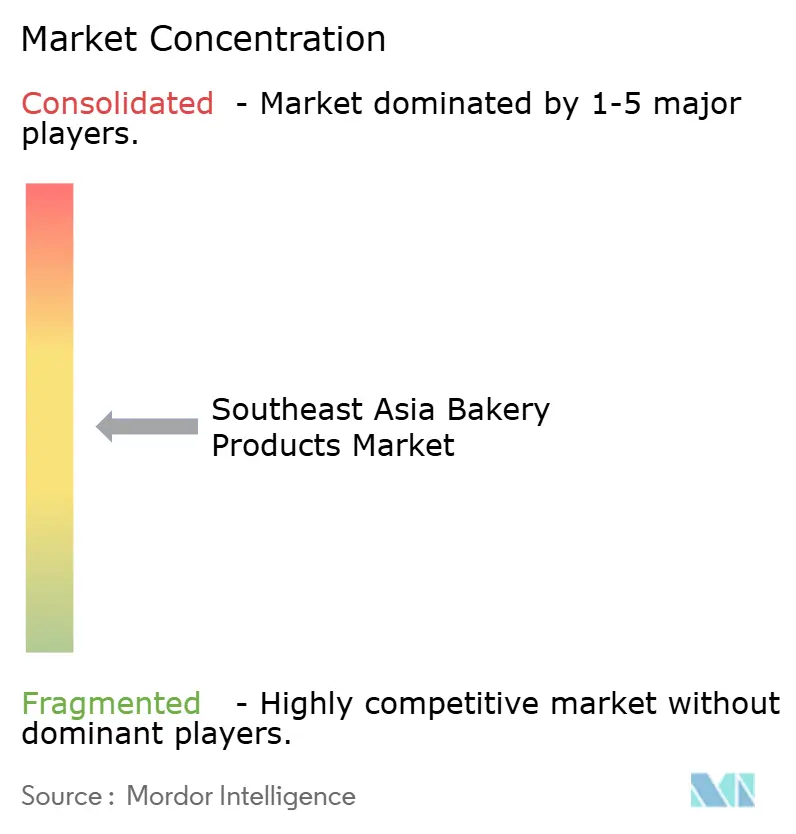

With a concentration score of 5/10, the Southeast Asia bakery products market is moderately fragmented. Domestic leaders like PT Nippon Indosari Corpindo, QAF Ltd, and Mayora Indah dominate the scene, utilizing integrated production, proprietary distribution, and aggressive brand-building campaigns. Meanwhile, international players such as Mondelez International and SPC Group are making their mark by franchising café-bakery formats, adapting global recipes to local tastes. Mid-tier challengers are shaking things up further by experimenting with cloud-kitchen models, effectively reducing rental overheads. Strategic investments in automation are evident: Monde Nissin has upgraded its Davao facility, and Universal Robina has expanded its Sariaya mill, both incorporating robotics for efficient dough handling and increased throughput. On the digital front, initiatives span from predictive ordering algorithms to QR-based traceability, catering to regulatory demands and the transparency sought by consumers. Cross-border mergers and acquisitions (M&A) are proving to be a strategic avenue for achieving regional scale, as highlighted by Lotus Bakeries’ establishment of a Thai production base for Biscoff exports. There's a noticeable uptick in intellectual-property filings, especially around plant-based texturizers and extended-shelf-life packaging, signaling a push for differentiated margins.

Brands are keenly exploring white spaces, particularly in functional snacks and rural micro-retail. They're customizing product sizes and pricing for tier-3 towns, while offering premium, low-GI cakes in affluent areas. Sustainability is emerging as a competitive edge, with pioneers in the market adopting recyclable packaging and ensuring palm-oil traceability. All these strategic moves underscore the dynamic and opportunity-laden landscape of the Southeast Asia bakery products market.

Southeast Asia Bakery Products Industry Leaders

QAF Limited

President Bakery Public Company Limited

PT Nippon Indosari Corpindo TBK

Mondelēz International, Inc

Mayora Indah Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Paris Baguette, a globally recognized bakery brand under SPC Group, has formally inaugurated its newest regional manufacturing hub in Johor, Malaysia. This facility signifies a strategic initiative in Paris Baguette's global expansion efforts, enhancing the efficiency of its supply chain to support the brand's growing presence across Southeast Asia, the Middle East, and other regions.

- August 2025: Europastry, a prominent bakery company based in Spain, has acquired a 60% stake in Thailand's Art of Baking. This acquisition represents a strategic initiative aimed at enhancing Europastry's presence in Southeast Asia. The move is expected to facilitate the company's expansion across the Asia-Pacific region while strengthening its global customer network.

Southeast Asia Bakery Products Market Report Scope

Bakery products include a range of products like bread, rolls, cookies, pies, pastries, and muffins are typically made with flour or meal that comes from grains of some kind.

The Southeast Asia bakery products market has been segmented by product type, distribution channel, and geography. By product type, the market studied is segmented into bread, sweet biscuits, crackers and savory biscuits, cakes, pastries, sweet pies, and morning goods. By distribution channel, the market has been divided into supermarkets/hypermarkets, specialty stores, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into Indonesia, Malaysia, Philippines, Vietnam, Thailand, Singapore, Myanmar, and the Rest of Southeast Asia.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Bread |

| Sweet Biscuits |

| Crackers & Savoury Biscuits |

| Cakes, Pastries & Sweet Pies |

| Morning Goods |

| Others |

By Form

| Fresh |

| Frozen |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience / Grocery Stores |

| Specialty Stores & Artisanal Bakeries |

| Online Retail Stores |

| Other Channels |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Myanmar |

| Rest of Southeast Asia |

| By Product Type | Bread |

| Sweet Biscuits | |

| Crackers & Savoury Biscuits | |

| Cakes, Pastries & Sweet Pies | |

| Morning Goods | |

| Others | |

| By Form | Fresh |

| Frozen | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience / Grocery Stores | |

| Specialty Stores & Artisanal Bakeries | |

| Online Retail Stores | |

| Other Channels | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Myanmar | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia bakery products market in 2026?

The Southeast Asia bakery products market size stands at USD 18.52 billion in 2026, with expectations of reaching USD 24.62 billion by 2031.

Which product category leads regional sales?

Cakes, pastries, and sweet pies hold the top position, capturing 42.10% of 2025 revenue.

What growth rate is forecast for crackers and savoury biscuits?

Crackers and savoury biscuits are projected to post a 7.26% CAGR over 2026-2031, the fastest among all product types.

Which distribution channel is expanding most rapidly?

Online retailers record the strongest momentum with an 10.92% CAGR outlook, driven by food-delivery and quick-commerce adoption.

Page last updated on: