Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

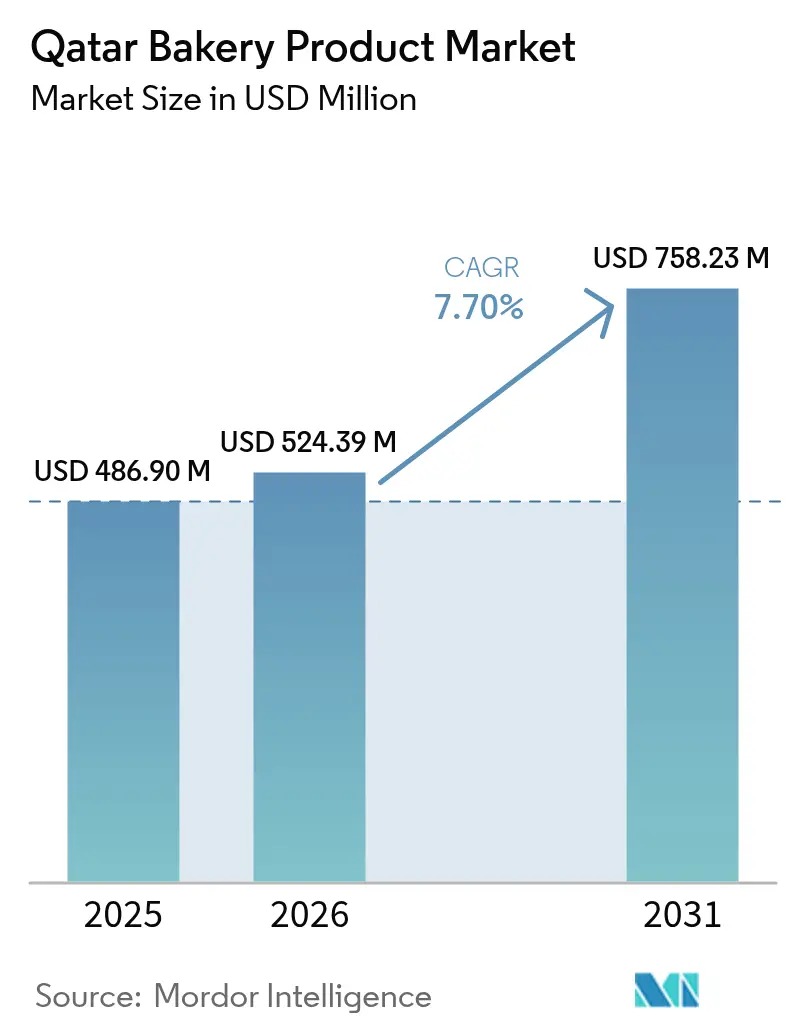

| Base Year Market Size (2025) | USD 486.90 Million |

| Market Size (2026) | USD 524.39 Million |

| Market Size (2031) | USD 758.23 Million |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Qatar Bakery Product Market Analysis by Mordor Intelligence

The Qatar bakery products market size was valued at USD 486.90 million in 2025 and estimated to grow from USD 524.39 million in 2026 to reach USD 758.23 million by 2031, at a CAGR of 7.70% during the forecast period (2026-2031). This healthy expansion mirrors Qatar’s broader economic diversification, with non-hydrocarbon activities now contributing roughly two-thirds of national output, according to the International Monetary Fund data from 2023 [1]Source: International Monetary Fund, "Qatar: 2024 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Qatar," imf.org. Four forces frame the current outlook. First, government-led stimulus under the Third National Development Strategy continues to channel private investment toward food manufacturing, lifting domestic supply capacity, according to the International Trade Association [2]Source: International Trade Administration, “Qatar Country Commercial Guide,” trade.gov. Second, a multicultural population, in which expatriates outnumber Qatari nationals, sustainsa steady demand for Western-style bakery lines alongside traditional Arabic staples. Third, rapid improvements in digital commerce let bakeries bypass geographic constraints, reach new consumers, and collect real-time feedback to fine-tune assortments. Finally, policy support through zero customs duties on wheat flour and subsidized loans for food processors protects margins and encourages scale-up.

Key Report Takeaways

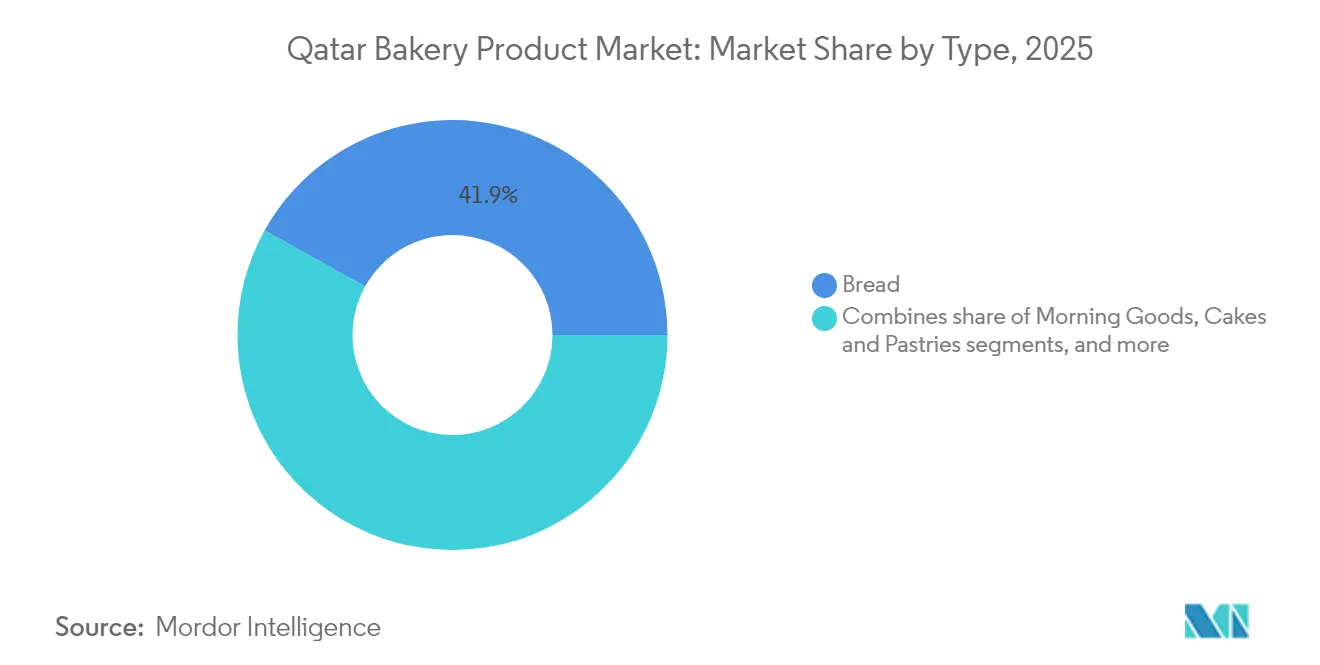

- By type, bread products account for 41.92% of the Qatar bakery products market share in 2025, with morning goods emerging as the fastest-growing segment at a projected CAGR of 7.78% during 2026-2031.

- By form, fresh products constitute 63.60% of the Qatar bakery products market share in 2025, while frozen products are expected to grow at a CAGR of 8.95% through 2031.

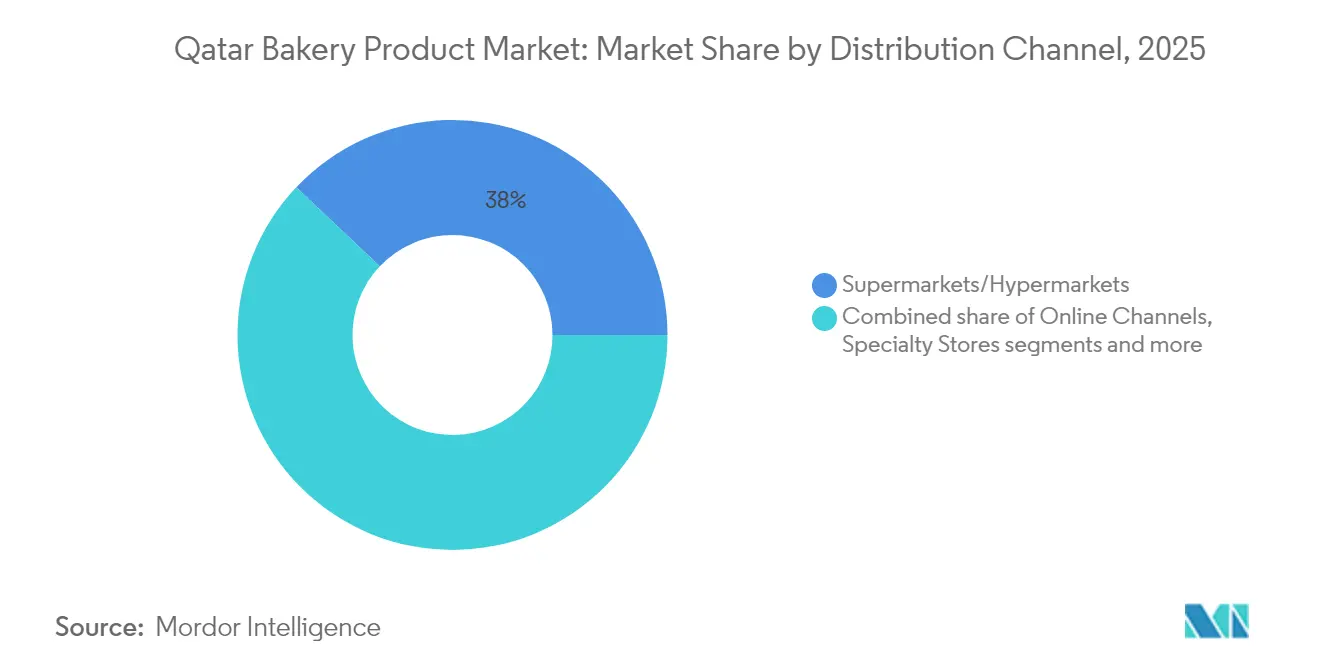

- By distribution channel, supermarkets/hypermarkets control 37.95% of the distribution channel share in 2025, with online retail projected to expand at a CAGR of 10.98% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Bakery Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expatriate population growth diversifying product preferences | +1.2% | Qatar National, with spillover to GCC | Medium term (2-4 years) |

| Influence of western culture | +0.8% | Qatar National, urban centers | Long term (≥ 4 years) |

| Surge in online retail and food delivery services | +1.5% | Qatar National, concentrated in Doha | Short term (≤ 2 years) |

| Government support for local production | +1.0% | Qatar National | Medium term (2-4 years) |

| Demand for health-oriented and functional bakery products | +0.9% | Qatar National, premium segments | Long term (≥ 4 years) |

| Growing tourism and hospitality sectors | +1.1% | Qatar National, hospitality zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expatriate population growth diversifying product preferences

Qatar's expatriate population drives sophisticated demand patterns that extend beyond traditional Arabic bakery offerings toward international varieties. The demographic composition creates distinct consumption clusters, with Western expatriates favoring artisanal breads and pastries, while South Asian communities drive demand for specialized baked goods. This segmentation enables premium positioning strategies, as evidenced by the success of international bakery chains establishing operations in Qatar's major retail centers. The expatriate influence extends to ingredient preferences, with increased demand for organic and specialty flours that command higher margins. Government data indicates expatriate spending on food and beverages has grown consistently, supporting sustained market expansion in premium bakery segments, according to the Planning and Statistics Authority Qatar data.

Influence of Western culture

Western cultural penetration reshapes traditional consumption patterns, particularly among younger demographics who demonstrate higher acceptance of non-traditional bakery products. This cultural shift manifests in increased demand for breakfast pastries, artisanal breads, and celebration cakes that align with Western lifestyle preferences. The trend accelerates through social media influence and international brand presence, creating opportunities for premium product positioning. Educational institutions and multinational corporations further reinforce Western dietary patterns among their communities. The cultural evolution supports market premiumization, with consumers willing to pay higher prices for authentic Western-style bakery products that meet quality expectations established in their home countries.

Surge in online retail and food delivery services

Digital transformation accelerates bakery product accessibility through sophisticated delivery networks that overcome traditional distribution limitations. Talabat's expansion of its 'Made in Qatar' brand promotion increased local bakery product distribution to regional markets by 30% in business collaborations. The online channel enables smaller bakeries to reach broader customer bases without substantial physical infrastructure investments. AI-driven personalization enhances customer engagement, with local startups like Dieture implementing multilingual AI assistants to provide customized nutritional guidance. According to the International Trade Administration, the digital economy's projected USD 11 billion contribution to non-hydrocarbon GDP by 2030 directly supports bakery market expansion through enhanced distribution capabilities [3]Source: International Trade Administration, “Qatar Country Commercial Guide,” trade.gov. Subscription models and bulk ordering options create predictable revenue streams while reducing customer acquisition costs.

Government support for local production

Qatar's strategic food security initiatives drive substantial investments in domestic bakery production capabilities, reducing import vulnerability while supporting local economic development. The QDB Jahiz program provides comprehensive support, including training facilities, equipment financing, and market access assistance specifically targeting food and beverage manufacturers. Manufacturing sector contributions reached QAR 80,254 million to GDP in 2022, with food processing representing a strategic priority for continued expansion. Government fee reductions of up to 90% for business registration significantly lower barriers to entry for new bakery operations, according to Qatar Law. The National Manufacturing Strategy's emphasis on advanced manufacturing technologies positions Qatar's bakery sector for productivity gains and quality improvements that enhance competitiveness against imported alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported raw materials | -0.7% | Qatar National | Short term (≤ 2 years) |

| Preference for traditional and ethnic bakery products | -0.5% | Qatar National, traditional segments | Long term (≥ 4 years) |

| Stringent food regulations | -0.4% | Qatar National | Medium term (2-4 years) |

| Seasonal consumption pattern | -0.3% | Qatar National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on imported raw materials

Qatar's limited agricultural capacity necessitates substantial raw material imports, creating vulnerability to global supply chain disruptions and price volatility. Wheat flour, despite benefiting from zero customs duties, remains subject to international market fluctuations that directly impact production costs. The blockade demonstrated the strategic risks of import dependency, prompting government initiatives to diversify supply sources and enhance strategic reserves. Transportation costs and logistics complexities add additional layers of expense that compress margins for local producers. Currency fluctuations against major commodity currencies create unpredictable cost structures that challenge long-term pricing strategies. The constraint intensifies during global commodity price spikes, as witnessed during recent geopolitical tensions affecting grain markets.

Stringent food regulations

Qatar maintains a comprehensive food safety framework aligned with GCC standards, which imposes significant compliance costs that affect smaller bakery operations. The mandatory requirements include detailed Arabic labeling specifications, extensive health certificates documentation, and rigorous Halal certification processes, increasing the complexity of product development and import procedures. New products require thorough pre-import approvals and documentation, which extend the timeline for market entry of bakery items. The regulatory structure creates substantial entry barriers that benefit established companies with robust compliance capabilities and dedicated regulatory teams. Companies must continuously invest in extensive staff training programs and comprehensive system upgrades to maintain compliance with frequently updated regulations and evolving food safety standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Morning Goods Drive Premium Segment Expansion

Morning Goods represents the fastest-growing segment with a 7.78% CAGR forecast for 2026-2031, capitalizing on evolving breakfast consumption patterns among Qatar's diverse population. The segment benefits from convenience-driven lifestyles and increased adoption of Western breakfast traditions, particularly among expatriate communities and younger demographics. Bread maintains the largest market share at 41.92% in 2025, supported by its staple status across all demographic segments and cultural preferences. The traditional Arabic bread varieties continue dominating volume sales, while artisanal and specialty breads command premium pricing in upscale retail channels.

The cakes and pastries segment shows consistent growth due to the rising trend of celebrating personal and social occasions, along with increasing demand from the hospitality sector. The biscuits and cookies segment experiences growth primarily because of their extended shelf life, which reduces wastage and storage concerns. Their convenient packaging and ready-to-eat nature make them popular choices among retail consumers seeking quick snacks.

By Form: Frozen Products Reshape Supply Chain Dynamics

The frozen products segment is projected to grow at a CAGR of 8.95% during 2026-2031, driven by supply chain optimization and demand for consistent quality from retailers and consumers. Frozen bakery products provide extended shelf life, minimize waste, and enable centralized production, improving manufacturers' cost efficiency. Additionally, frozen products help businesses manage inventory fluctuations and seasonal demand variations effectively. Fresh products remain dominant with a 63.60% market share in 2025, as consumers continue to prefer traditional bread and pastries for immediate consumption, valuing the sensory experience of freshly baked goods and their superior taste characteristics.

The frozen food segment is growing due to increasing consumer demand for convenience and standardized quality products. Advanced freezing technologies, including blast freezing and cryogenic systems, preserve nutritional value and texture while preventing ice crystal formation. Modern thawing processes utilize controlled temperature chambers and microwave technologies to maintain product integrity. These technological improvements enable products to reach distant markets while retaining their quality characteristics. This development aligns with Qatar's food security strategy by allowing effective inventory management through long-term storage capabilities and reducing reliance on daily production cycles, which helps buffer against supply chain disruptions and seasonal variations in food availability.

By Distribution Channel: Digital Transformation Accelerates Market Access

Online retail emerges as the fastest-growing distribution channel with an 10.98% CAGR forecast for 2026-2031, driven by digital platform expansion and changing consumer shopping behaviors. The channel's growth reflects Qatar's digital economy development, with e-commerce infrastructure supporting seamless bakery product delivery across the country. Supermarkets/hypermarkets maintain the largest share at 37.95% in 2025, benefiting from their established customer relationships and comprehensive product assortments. These large-format retailers provide essential visibility for new product launches and seasonal promotions.

Convenience Stores serve a growing demand for grab-and-go bakery items, particularly morning goods and snacks that align with busy lifestyles. Specialty Stores maintain niche positions serving specific cultural communities and premium product segments. The digital transformation enables smaller bakeries to compete effectively against larger players by reaching customers directly without substantial physical infrastructure investments.

Geography Analysis

Qatar's bakery products market benefits from concentrated urban demand centered in Doha and surrounding metropolitan areas, where expatriate populations and tourism activities drive consumption patterns. The country's compact geography enables efficient distribution networks that support both fresh and frozen product categories across all market segments. Government infrastructure investments, including the expanded Hamad Port and improved logistics capabilities, enhance supply chain efficiency for both domestic production and imported raw materials. The post-FIFA World Cup infrastructure legacy continues supporting sector growth, creating sustained demand for commercial bakery products.

Regional integration within the GCC creates opportunities for cross-border expansion, as evidenced by Talabat's success in promoting Qatar-made products to Kuwait and other neighboring markets. The geographic concentration enables targeted marketing strategies and efficient customer service delivery that support premium positioning. Qatar's strategic location as a regional hub enhances its potential as a distribution center for international bakery brands seeking GCC market access. The limited geographic scope allows for comprehensive market coverage through focused distribution strategies that maximize market penetration and customer reach.

Economic zones and free trade areas provide additional opportunities for bakery product manufacturing and distribution, with government incentives supporting local production capabilities. The geographic stability and political environment create favorable conditions for long-term investment in production facilities and distribution infrastructure. Climate-controlled storage and transportation capabilities ensure product quality maintenance across the distribution network, supporting both domestic consumption and potential export opportunities to regional markets.

Regulatory Landscape

Qatar regulates bakery manufacturing and imports primarily through the Ministry of Public Health (MoPH) Food Safety Department, with mandatory registration of food establishments and food products via MoPH's Wathiq platform and associated Qatar Food Regulatory System (QFRS) workflows. Bakery items and ingredients must meet applicable GCC/GSO food safety and labeling standards, including Arabic or bilingual (Arabic and English) labeling that states product name, ingredients, net weight, production and expiry dates, and country of origin.

For imported bakery products and key inputs, clearance is routed through the General Authority of Customs using the Al Nadeeb single-window procedures, followed by risk-based inspection at points of entry by the Ports Health and Food Control Section. Where products include additives of animal origin, Halal documentation is required, supported by MoPH guidance for importing Halal food and recognition of certificates from approved Islamic bodies. This makes documentation readiness and supplier qualification central to compliant market access.

Value Chain Analysis

The value chain starts with imported grains, flour, fats, sugars, dairy, yeast, and packaging, reflecting Qatars limited agricultural base for key bakery inputs. Hamad Port functions as the critical logistics gateway, supported by high-capacity grain silos at the Food Security Facility and broader government-led food security infrastructure that buffers supply through strategic stocks and diversified sourcing.

Midstream conversion is split between industrial manufacturers and in-store or artisanal bakeries, with production clusters in industrial zones such as the New Industrial Area of Doha. As of March 2026, the Ministry of Commerce and Industry reported 138 national food manufacturing factories operating in Qatar, including 15 facilities dedicated to bakery and pasta production, indicating an expanding local manufacturing base. Downstream distribution is led by modern trade (supermarkets and hypermarkets), foodservice (hotels, cafes, and restaurants), convenience formats, and rapidly scaling delivery-enabled online channels. These platforms enable direct-to-consumer reach for fresh assortments and improved rotation for frozen lines.

Competitive Landscape

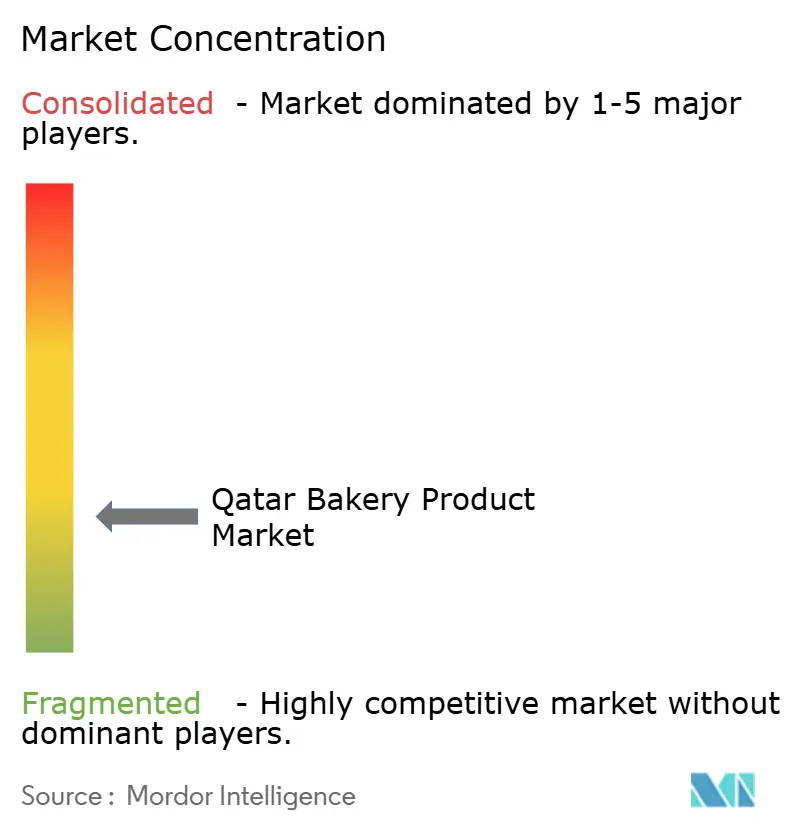

The Qatar bakery products market exhibits fragmented competition, indicating substantial opportunities for market share consolidation among established players. Local companies like Qbake (Qatar Flour Mills Co.) and Doha Modern Bakery compete alongside international brands including Mondelez International, Dunkin' (Inspire Brands), and Kellanova, creating a diverse competitive environment. The fragmentation enables niche positioning strategies, with companies focusing on specific product categories, distribution channels, or customer segments to establish competitive advantages.

Companies in the market differentiate themselves through technology adoption, implementing advanced digital platforms to streamline customer interactions and gather consumer data. These digital solutions enable businesses to monitor and enhance supply chain efficiency, from procurement to distribution. Additionally, companies utilize technology for research and development, resulting in innovative product formulations and packaging designs. The competitive environment aligns with GCC market trends, particularly in premium product offerings that target affluent consumers and health-focused innovations that address growing wellness concerns among the population.

Companies enter and expand in the market through strategic partnerships and joint ventures, which help international brands gain local market knowledge and distribution networks. The regulatory framework benefits organizations with strong compliance systems, creating entry barriers that protect established companies while rewarding operational efficiency and consistent quality standards.

Qatar Bakery Product Industry Leaders

-

Korean Bakeries WLL

-

Yasmeen Sweets

-

Mondelez International

-

Wadia group

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate around localization and resilience initiatives anchored in the National Food Security Strategy 2024-2030 and related state programs that prioritize local manufacturing, strategic reserves, and diversified trade sourcing. With 15 dedicated bakery and pasta facilities included within the 138 national food factories reported by the Ministry of Commerce and Industry as of March 2026, there is whitespace for additional scale in industrial baking, co-manufacturing, and modernization of freezing, packaging, and quality systems to support broader assortments across fresh and frozen products.

A second opportunity sits at the intersection of compliance and cross-border-ready supply chains. Stricter facility and product registration requirements via MoPH's Wathiq/QFRS and the use of customs single-window processes (Al Nadeeb) reward operators that standardize documentation, labeling (Arabic/bilingual), and Halal certification across suppliers. On the demand side, ongoing expansion of online ordering and delivery in Doha strengthens the case for centralized production and frozen or par-baked formats that travel better and reduce wastage, while enabling bakeries to extend beyond single-store catchments without heavy retail capex.

Recent Industry Developments

- June 2026: Yasmeen Sweets expanded its Levantine dessert offering in Doha through the Yasmeen destination at Maysan Doha, featuring traditional sweets such as Umm Ali alongside broader dessert menu items. The expansion strengthens premium positioning in hospitality-linked locations and supports higher-margin dessert and celebration-driven bakery demand.

- August 2025: Qatars Ministry of Commerce and Industry issued an administrative decision to close Ritos Bakery and Trading Company for one month for violating Article (13-7) of Law No. (8) of 2008 on Consumer Protection, citing the use of products of unknown origin. The action underscores enforcement intensity and raises the operational cost of weak traceability and supplier controls for bakery producers and distributors.

- December 2024: SGS highlighted its Product Conformity Assessment (PCA) services in Qatar to support Certificates of Conformity for regulated imports, aligning with market access requirements tied to MoPH-approved conformity pathways. The emphasis on structured conformity documentation reinforces the need for import-ready labeling, testing, and supplier documentation for packaged bakery products and ingredients entering Qatar.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of bakery products sold in Qatar across fresh and frozen formats, captured at the point they are purchased by consumers and food service buyers.

Scope exclusions: It excludes wheat milling as a raw material industry, home baking ingredients, and non-bakery snacks that are not produced and sold as bakery items.

Segmentation Overview

-

By Type

- Bread

- Cakes and Pastries

- Biscuits and Cookies

- Morning Goods

- Others

-

By Form

- Fresh

- Frozen

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was first used to establish the factual base for Qatar, so the model inputs are anchored to what can be checked publicly. We reviewed official statistics and trade indicators from sources such as Qatar Planning and Statistics Authority releases, UN Comtrade, FAOSTAT, and WTO tariff and trade notes, then linked them with published standards and category definitions from Codex Alimentarius and similar bodies.

In parallel, we used company annual reports and investor presentations, plus retail and food service announcements covered by reputable press, to understand capacity additions, channel shifts, and pricing behavior. Where needed, paid subscriptions for company financials and intelligence, plus an import and export shipment-level database, were used to cross-check supplier presence and trade intensity. The sources named here are illustrative rather than exhaustive, and additional public references were also used to collect data, validate figures, and clarify assumptions.

Primary Interviews and Surveys

Primary work was focused on filling gaps that desk sources do not cover fully, especially fresh bakery throughput, channel mix, and realistic price ladders across mass and premium products. We spoke with stakeholders across manufacturing, distribution, retail, and food service, and the discussions were tied to Qatar demand conditions rather than wider regional averages.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 15% | Managers: 46% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where national demand signals and category structure are reconstructed into bakery product consumption value for Qatar. This is then corroborated with selective bottom-up approximations, including sampled average selling price by channel multiplied by estimated volumes. Supplier and distributor roll-ups were also used as a reasonableness check where gaps appear.

Key inputs included population and visitor flows, the split between fresh and frozen bakery, retail versus food service consumption patterns, import reliance for specific bakery lines, and observed price bands by product group such as bread, cakes and pastries, biscuits and cookies, and morning goods. Because reporting for small bakeries and on-premise production can be uneven, gaps were handled through interview-led penetration assumptions and cross-checks against trade data and store count signals, then adjusted conservatively.

For forecasting, scenario analysis was applied around key demand and cost drivers, and assumptions were stress tested with expert feedback so the final path reflects likely outcomes rather than a single aggressive case. Where inflation and currency timing could distort results, price progressions were kept consistent with observed local retail behavior and validated through channel checks.

Data Validation & Update Cycle

After the first model run, outputs were checked against independent signals such as trade movement, announced capacity, and channel expansion, then reviewed again to explain any variance that looked unusually high or low. When a mismatch could not be explained using desk evidence, follow-up calls were triggered to confirm whether the issue came from pricing, product mix, or a one-time supply event.

Before sign-off, the analysis goes through multi-step internal reviews, and the final numbers are rechecked for unit consistency and year-on-year logic. Reports are refreshed annually, and interim updates are made when material events occur that can shift demand or supply assumptions. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Qatari Bakery Product Market Size Measured Against Other Published Estimates

Published market sizes for Qatar bakery products can look far apart because each publisher sets its own product basket, pricing basis, and update timing, and these choices can move the final value by a noticeable amount.

Some estimates use an earlier base year or broader food groupings that can blend bakery with adjacent sweet snacks, while others apply faster price growth without separating fresh and frozen demand or validating retail versus food service splits. In some cases, published figures appear to extend into dessert-like items sold alongside bakery, then Mordor Intelligence counts only defined bakery products (such as bread, cakes and pastries, biscuits and cookies, and morning goods) across listed channels. Pricing checks are kept tied to local shelf behavior and trade signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 524.39 M (2026) | |

| Industry Publisher A | USD 510.00 M (2024) | Uses an earlier current year, so recent channel mix shifts and price resets can be under-reflected when values are carried forward. |

| Industry Publisher B | USD 545.70 M (2025) | Uses a different current year and may apply a wider channel and product interpretation, which can change how artisanal production and food service value are captured. |

The comparison shows that year selection and what gets counted as a bakery product explain most of the spread. When the scope is kept tight to bakery items and checked against channel and trade signals, the resulting total is easier to reproduce and explain step by step.

Key Questions Answered in the Report

What is the current value of the Qatar bakery products market?

The market is worth USD 524.39 million in 2026 and is projected to advance to USD 758.23 million by 2031 at a 7.70% CAGR.

Which product category leads sales in 2026?

Bread remains the largest category, commanding 41.92% of 2025 revenue and continuing to expand on the back of daily-consumption habits.

How fast is online retail growing for bakery items in Qatar?

Online Retail is forecast to register an 10.98% CAGR between 2026 and 2031, outpacing all other channels.

Why are frozen bakery products gaining traction?

Frozen lines grow at 8.95% CAGR because they deliver longer shelf life, consistent quality and lower wastage for retailers and food-service operators.

Page last updated on: