Predictive Maintenance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

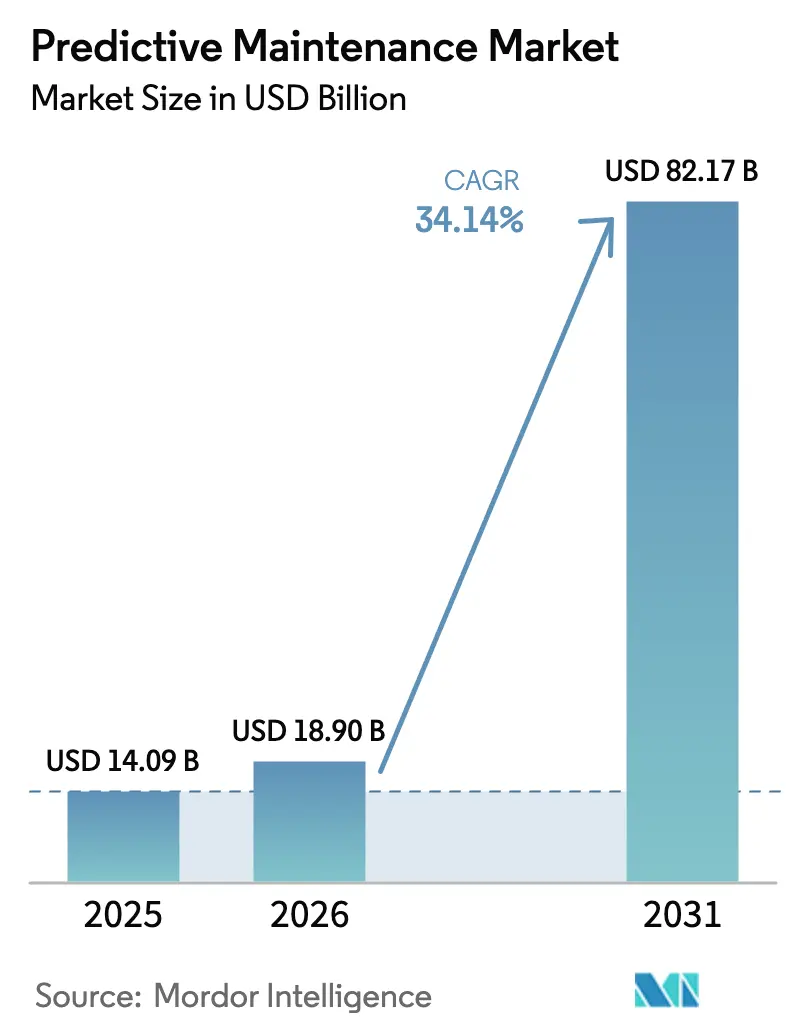

| Market Size (2026) | USD 18.90 Billion |

| Market Size (2031) | USD 82.17 Billion |

| Growth Rate (2026 - 2031) | 34.14% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Predictive Maintenance Market Analysis by Mordor Intelligence

The predictive maintenance market size was valued at USD 14.09 billion in 2025 and estimated to grow from USD 18.9 billion in 2026 to reach USD 82.17 billion by 2031, at a CAGR of 34.14% during the forecast period (2026-2031). Sensor price declines, edge–cloud convergence, and wider industrial digitization collectively accelerate deployment across asset-intensive sectors. Enterprises now view advanced maintenance as a competitive necessity because AI models can flag failures weeks or months in advance, enabling precise scheduling of repairs and resource allocation. Cloud scalability removes traditional infrastructure barriers, while edge analytics lowers latency and bandwidth needs, making solutions viable for remote or connectivity-constrained sites. Supply-chain volatility and semiconductor cost inflation have lifted hardware prices, yet these pressures also spur innovation in lighter, on-device processing architectures that cut data-transfer costs.

Key Report Takeaways

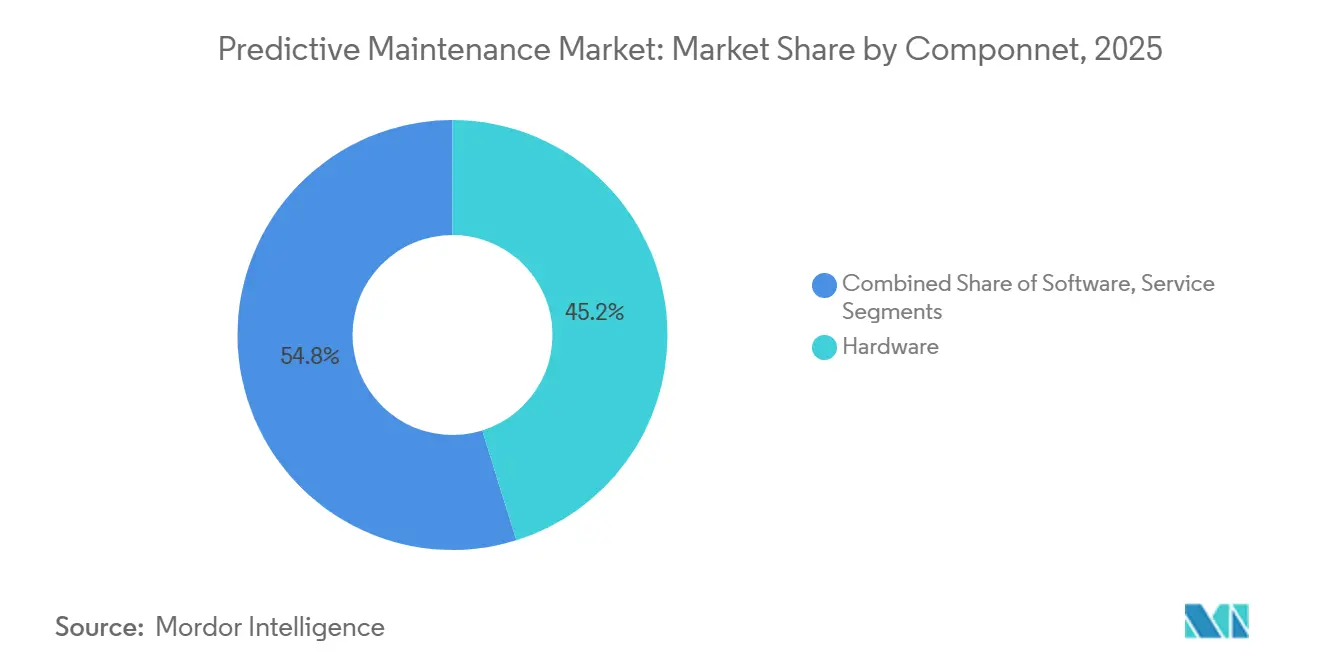

- By component, hardware claimed 45.18% of predictive maintenance market share in 2025, whereas software is set to expand at a 35.82% CAGR to 2031.

- By enterprise size, large enterprises held 63.65% revenue share in 2025; small and medium enterprises record the highest projected CAGR at 36.2% through 2031.

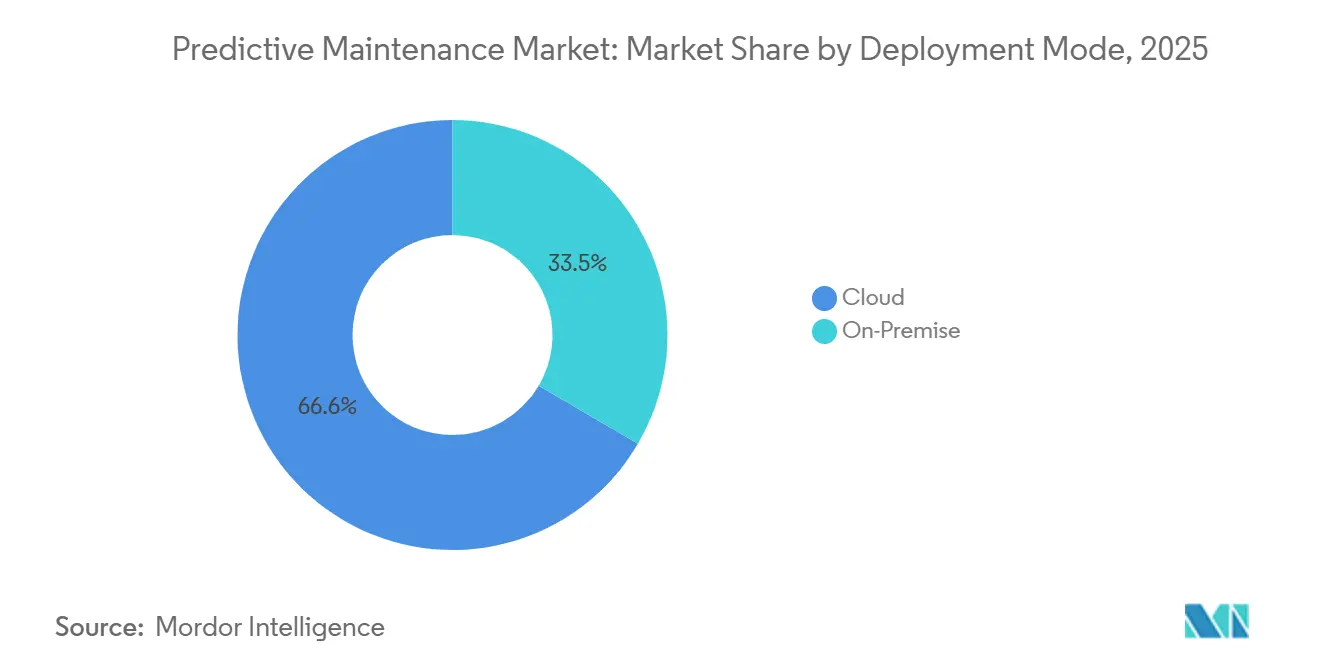

- By deployment mode, cloud platforms represented 66.55% of the predictive maintenance market size in 2025 and are growing at 36.95% CAGR.

- By end-user industry, industrial manufacturing led with 22.95% revenue share in 2025, while the energy and utilities segment is forecast to grow 34.6% annually to 2031.

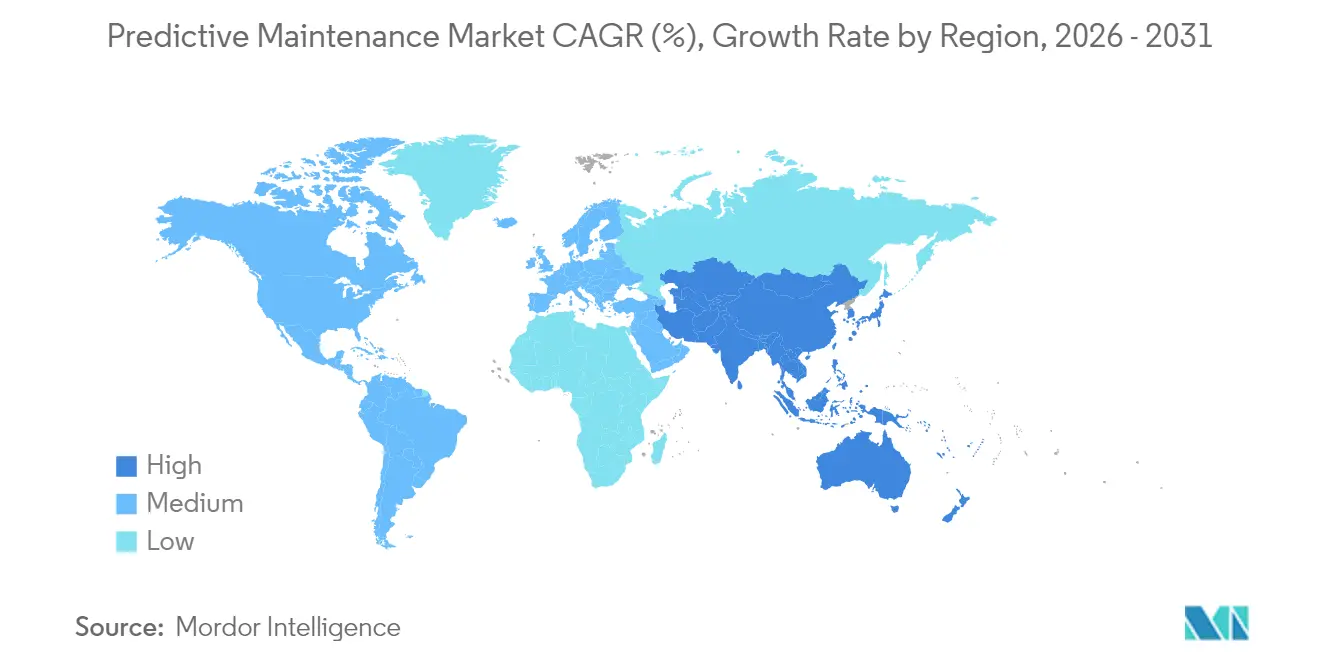

- By geography, North America commanded 28.85% revenue in 2025; Asia-Pacific is projected to progress at a 35.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Predictive Maintenance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT-enabled asset connectivity boom | +6.2% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| AI/ML accuracy breakthroughs | +4.8% | North America & Europe early, Asia-Pacific scaling | Short term (≤ 2 years) |

| Downtime-reduction cost pressures | +5.1% | Global, manufacturing-heavy regions | Short term (≤ 2 years) |

| Cloud-native deployment scalability | +4.3% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Digital-twin-driven prescriptive workflows | +3.9% | Europe and North America advanced manufacturing | Long term (≥ 4 years) |

| ESG-linked maintenance KPIs | +2.7% | Europe regulatory-driven, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IoT-Enabled Asset Connectivity Boom

Mass adoption of industrial IoT sensors now extends beyond vibration and temperature probes to include acoustic, thermal, and power-signature monitoring on a single board. Edge gateways process thousands of data points per second locally, ensuring immediacy of alerts while limiting traffic back to the cloud.[1]Wevolve ,"The 2025 Edge AI Technology Report,"wevolver.comWireless mesh networks cut installation costs up to 60% relative to wired layouts, bringing remote mines, offshore rigs, and mobile equipment into predictive regimes. Standardized protocols such as MQTT and OPC-UA raise interoperability, reducing integration complexity for multi-vendor plants. Hardware inflation since 2024 has slowed procurement cycles, yet the resulting focus on edge efficiency means many plants are replacing complex servers with compact inference units.

AI/ML Accuracy Breakthroughs

Ensemble machine-learning pipelines and domain-adapted deep-learning models now achieve 85–95% precision in predicting bearing, pump, and motor failures 30–60 days in advance. Synthetic data and transfer-learning techniques let teams train models in weeks rather than years, even when historical failure events are scarce. Edge inference chips deliver real-time insights without persistent connectivity, maintaining operations in bandwidth-limited areas. Generative AI copilots embedded in maintenance suites provide technicians with contextual repair steps, parts lists, and safety checks using natural-language queries. Higher accuracy directly improves user trust, driving wider rollout across smaller production sites.

Downtime-Reduction Cost Pressures

Unexpected line stoppages cost high-volume manufacturers USD 50,000–200,000 per hour, prompting finance teams to prioritize failure-prevention budgets. In power generation, daily revenue losses during forced outages can exceed USD 2 million, reinforcing the business case for turbine, transformer, and switchgear monitoring. Hospitals quantify equipment idle time by its impact on patient throughput, with diagnostic imaging backlog costs of USD 10,000–15,000 per day pushing facility managers toward connected-asset strategies. Longer global lead times for replacement parts—often 6–18 months—further elevate the value of condition-based interventions over reactive maintenance.[2]Crothall ,"Bidding Farewell to OEM Dependence: Infirmary Health’s Path to USD 2 million in Savings," crothall.com

Cloud-Native Deployment Scalability

Subscription-based predictive maintenance suites reduce total cost of ownership 30–50% compared with traditional on-premise builds, enabling multi-site rollouts without proportional hardware growth. Multi-tenant architectures lower entry thresholds so that SMEs pay on a per-asset basis, aligning fees with realized savings. Schneider Electric reported 140% growth in SaaS revenues during H1 2024, driven by EcoStruxure platform adoption that provides predictive analytics as a subscription service rather than capital expenditure. [3]Schneider Electric SE, “EcoStruxure Annual Performance 2024,” se.comHybrid edge–cloud frameworks keep latency-sensitive inference on-site while pushing heavy analytics and cross-plant benchmarking to secure data centers. Enterprises benefit from continuous algorithm updates, automated patching, and compliance certifications that match or exceed internal IT standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy gaps | -2.8% | Global, EU GDPR compliance critical | Short term (≤ 2 years) |

| Skilled-talent shortage | -1.9% | North America and Europe acute, Asia-Pacific emerging | Medium term (2-4 years) |

| Legacy-protocol interoperability issues | -1.5% | Global, manufacturing-heavy regions | Medium term (2-4 years) |

| AI model drift and liability risk | -1.2% | Regulated industries globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Privacy Gaps

Expanded sensor networks enlarge attack surfaces, exposing operational technology to cyberthreats. Legacy protocols lack native encryption, forcing retrofit of secure tunneling and authentication layers to meet regulations such as GDPR and NERC CIP. Balancing real-time data flows with strict security policies remains a challenge, especially in healthcare and critical-energy sites where both patient safety and grid stability are paramount. Enterprises therefore prioritize platforms featuring device-level encryption, zero-trust architectures, and audit-ready data-handling practices.

Skilled-Talent Shortage

Successful predictive programs require hybrid expertise in mechanical engineering, data science, and network security; however, the labor market supplies few professionals with this triple skill set. Traditional technicians need upskilling to interpret model outputs, while statisticians often lack domain context to recognize genuine degradation signatures. Universities are only starting to integrate curricula covering operational technology analytics, creating a pipeline lag that may last years. Managed-service providers and AI-enabled copilots partly bridge the gap but do not fully offset institutional knowledge shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Foundation Enables Software Growth

Hardware captured a 45.18% share of the predictive maintenance market in 2025. High-performance sensors and edge gateways create the data backbone that software analytics depend on. The segment remains pivotal because new installations expand the addressable base each year. Software revenues are climbing quickest, advancing at a 35.82% CAGR to 2031 as AI libraries mature and cloud subscriptions proliferate. Services, though smaller, deliver critical deployment, calibration, and model-tuning expertise across complex industrial estates.

Continued miniaturization and cost reductions in wireless sensors allow multi-parameter monitoring from a single device, reducing total installed cost. Edge units now execute machine-learning inference locally, trimming bandwidth usage and ensuring deterministic latency for safety-critical assets. Software providers focus on modular designs, allowing plants to license analytics packs specific to pumps, drives, or HVAC systems. Generative-AI front ends further lower training overhead by letting technicians converse with maintenance systems in plain language. Services firms combat talent shortages by offering turnkey packages that include remote monitoring, periodic model refreshes, and cybersecurity safeguards.

By Enterprise Size: SME Uptake Surges via Cloud Accessibility

Large corporations controlled 63.65% of predictive maintenance market revenue in 2025 owing to expansive asset portfolios and deep IT budgets. However, SMEs represent the most dynamic constituency, advancing at a 36.2% CAGR to 2031 as barriers to adoption fall. Pay-as-you-go pricing lets smaller plants launch pilots for USD 50–100 per asset per month, achieving positive ROI within 12–18 months.

Enterprise incumbents leverage private clouds and internal data-science teams to tailor algorithms for proprietary equipment. They also integrate predictive dashboards into existing MES and ERP environments, streamlining workflow orchestration. SMEs, conversely, rely on vendor-managed cloud tools where updates, security patches, and model retraining occur automatically. Managed-service partners further ease uptake by bundling sensors, gateways, and analytics in a single subscription. Edge AI mitigates bandwidth constraints in rural factories, reducing dependence on high-capacity connections.

By Deployment Mode: Cloud Dominance Reflects Scalability Needs

Cloud platforms secured 66.55% share of the predictive maintenance market size in 2025 and are projected to rise at 36.95% CAGR. Organizations favor managed environments that simplify expansion from dozens to thousands of assets. Hybrid architectures keep latency-sensitive tasks on site while forwarding aggregated data to secure clouds for deep analytics. On-premise systems persist in highly regulated or connectivity-limited domains but increasingly interface with cloud APIs for model updates and benchmarking.

Enterprises appreciate that cloud providers assume responsibility for uptime, disaster recovery, and compliance certifications. Continuous deployment pipelines deliver model improvements without production downtime, ensuring algorithms remain current with evolving asset behavior. Security features, including hardware-rooted identity and end-to-end encryption, now rival or surpass internal data centers. Cost models based on asset counts or data volumes align spending with productivity gains, appealing to finance teams seeking predictable OPEX structures.

By End-User Industry: Manufacturing Leads, Energy Surges

Industrial manufacturing represented 22.95% of revenue in 2025, reflecting the direct correlation between line uptime and shipment commitments. Predictive analytics target motors, conveyors, and robotic cells, with plants reporting maintenance cost reductions of 10–40% and unplanned-downtime cuts of 70–90%. The energy and utilities sector is poised for the fastest growth at 34.6% CAGR through 2031. Grid modernization, renewable-power integration, and strict reliability mandates compel utilities to monitor turbines, transformers, and cables continuously.

In manufacturing, the combination of aging equipment and just-in-time inventories amplifies the financial impact of unscheduled stoppages. Energy firms face hefty penalties for service interruptions, making predictive insights essential for asset management. Healthcare, telecom, and aerospace also expand their adoption footprints, applying predictive logic to imaging equipment, 5G radios, and aircraft systems. Each vertical demands domain-specific models, reinforcing the need for specialist software modules and pre-trained algorithm libraries.

Geography Analysis

North America held 28.85% revenue share in 2025 thanks to early digital-factory investment, abundant venture funding, and a supportive regulatory climate. Widespread adoption of industrial IoT platforms, coupled with high labor costs, drives continued spending on predictive solutions. Strategic collaborations between automation giants and hyperscale-cloud providers accelerate product innovation and market penetration. Nonetheless, acute shortages of cross-disciplinary talent and heightened cyber-risk awareness challenge smaller enterprises.

Asia-Pacific is the fastest-expanding region, advancing at a 35.25% CAGR through 2031. National Industry 4.0 programs, sizeable manufacturing output, and growing technical expertise underpin demand. Local governments subsidize sensor retrofits and digital-skills training to offset aging workforces and sustain export competitiveness. Regional firms benefit from lower hardware costs and in-region electronics supply chains, although legacy-system connectivity and data-governance concerns require targeted solutions.

Europe combines mature industrial automation with stringent data-protection laws, yielding steady adoption growth. German automotive and machinery sectors pilot advanced digital-twin projects that embed predictive routines, while the United Kingdom modernizes aging energy grids with condition-monitoring frameworks. Vendor ecosystems anchored by Siemens, ABB, and Schneider Electric provide integrated offerings certified for CE-marked environments. Middle East and Africa markets remain nascent but show promise in oil, gas, and renewables where asset reliability is paramount and remote-site logistics are costly.

Competitive Landscape

The predictive maintenance market features moderate concentration as diversified automation leaders, cloud hyperscalers, and AI-first specialists vie for share. Siemens, ABB, and Schneider Electric leverage installed-base knowledge and vertically integrated portfolios to deliver turnkey packages spanning sensors to analytics. Microsoft and IBM supply scalable cloud stacks, providing platform-as-a-service layers that software vendors build upon. Pure-play AI firms such as C3.ai and Uptake differentiate through transfer-learning libraries and rapid-deployment templates targeting specific machine classes.

Partnerships shape go-to-market strategies. Siemens integrates its Edge portfolio with Azure IoT services, while ABB invests in startups focused on energy optimization and predictive analytics to fortify its grid offerings. Vendors pursue intellectual-property protection around time-series algorithms and on-device inferencing. Edge-focused newcomers emphasize hardware-agnostic software that simplifies retrofits, posing a credible threat to hardware-tied incumbents. Vertical specialization healthcare imaging, telecom networks, aircraft systems offers niches where domain know-how outweighs generic analytic capability.

Predictive Maintenance Industry Leaders

-

IBM Corporation

-

Microsoft Corporation

-

SAP SE

-

Siemens AG

-

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABB announced USD 120 million expansion of U.S. electrification factories to meet rising predictive-maintenance demand.

- January 2025: Infirmary Health cited USD 2 million annual savings after full predictive-maintenance rollout.

- January 2025: ABB launched Ability Genix Copilot, a generative-AI assistant for field technicians.

- October 2024: Schneider Electric acquired Motivair Corporation, enhancing data-center cooling monitoring capabilities.

Global Predictive Maintenance Market Report Scope

Predictive Maintenance employs data analysis and predictive analytics to assess equipment conditions and forecast optimal maintenance timings. Various technologies, such as sensors, IoT devices, machine learning, and data analytics, are employed to monitor equipment health in real time.

The predictive maintenance market is segmented by component (hardware, software (cloud, on-premise), and services), enterprise size (small and medium enterprises, and large enterprises), end-user industry (healthcare, automotive and transportation, industrial, telecommunications, energy and utilities, aerospace and defense, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Hardware |

| Software |

| Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-Premise |

| Cloud |

| Industrial Manufacturing |

| Automotive and Transportation |

| Energy and Utilities |

| Healthcare |

| Telecommunications |

| Aerospace and Defense |

| Others (Oil and Gas, Mining, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Deploymet Mode | On-Premise | ||

| Cloud | |||

| By End-user Industry | Industrial Manufacturing | ||

| Automotive and Transportation | |||

| Energy and Utilities | |||

| Healthcare | |||

| Telecommunications | |||

| Aerospace and Defense | |||

| Others (Oil and Gas, Mining, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the predictive maintenance market?

The predictive maintenance market stands at USD 18.9 billion in 2026

How fast is the predictive maintenance market expected to grow?

It is projected to expand at a 34.14% CAGR during the forecast period (2026-2031), reaching USD 82.17 billion by 2031.

Which component segment is growing quickest?

Software solutions show the highest pace, advancing at a 35.82% CAGR through 2031.

Why are SMEs adopting predictive maintenance rapidly?

Cloud subscriptions, pay-per-asset pricing, and managed services let SMEs deploy advanced analytics without large capital outlays, driving a 36.2% CAGR.

Page last updated on: