Construction Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 11.52 Billion |

| Growth Rate (2026 - 2031) | 12.58% CAGR |

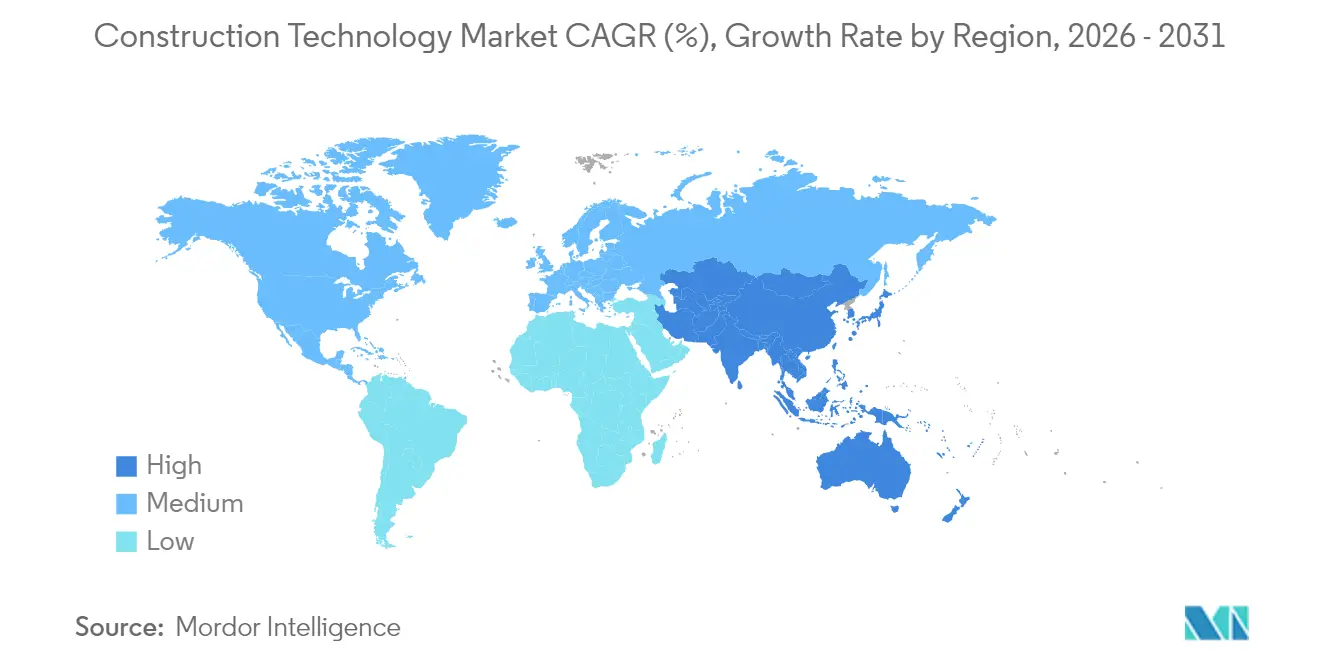

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

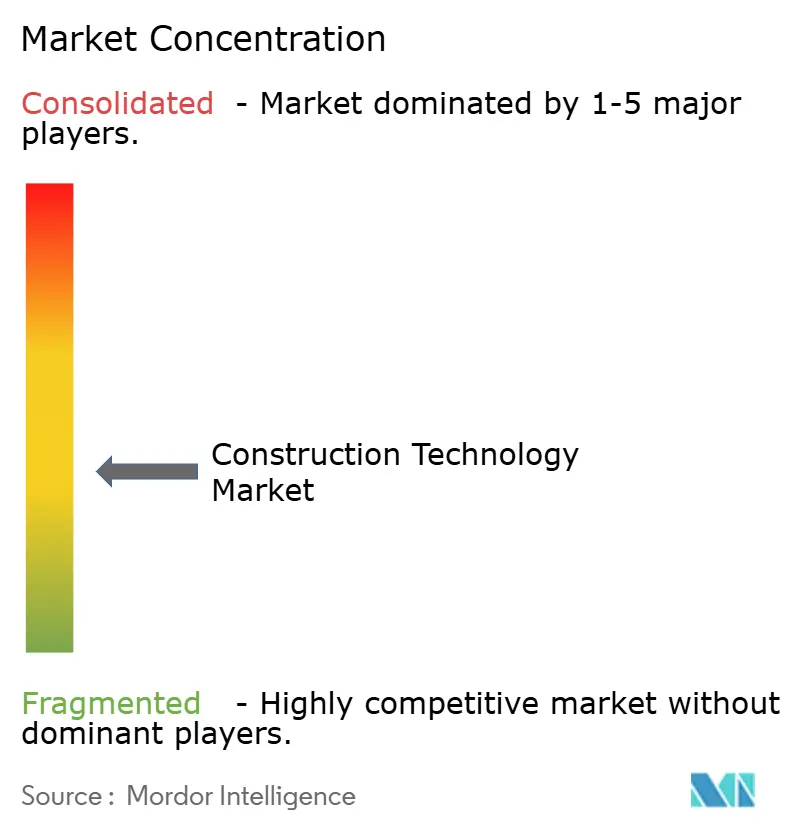

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Technology Market Analysis by Mordor Intelligence

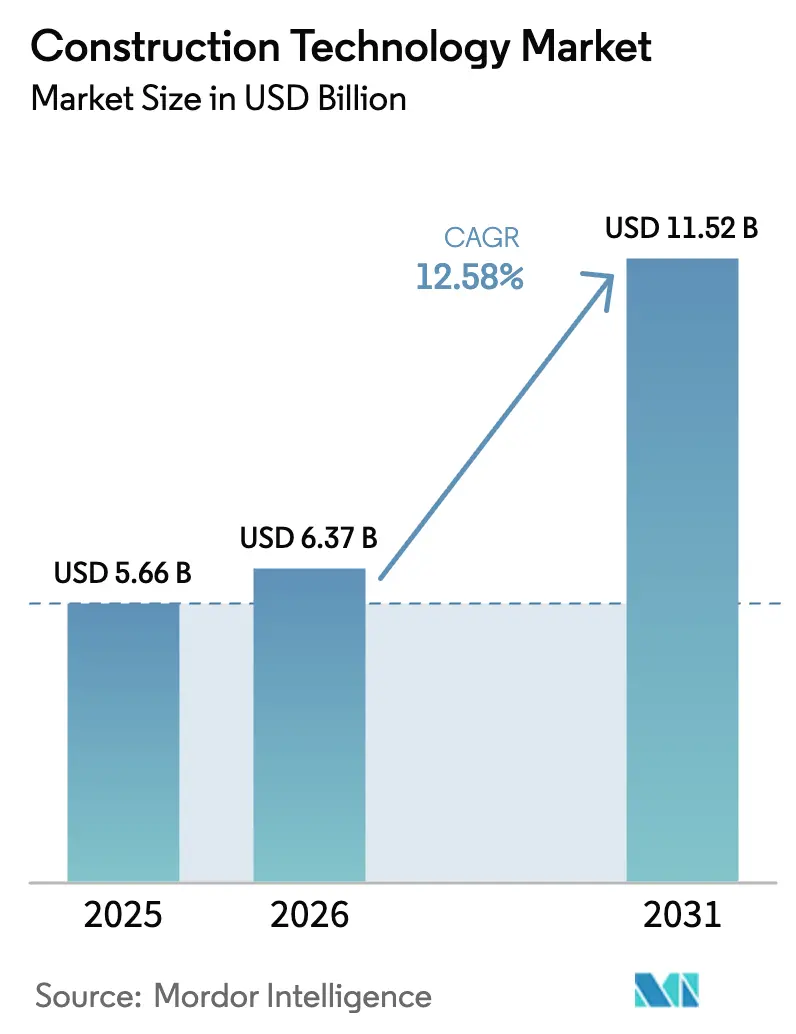

The Construction Technology market size was valued at USD 5.66 billion in 2025 and estimated to grow from USD 6.37 billion in 2026 to reach USD 11.52 billion by 2031, at a CAGR of 12.58% during the forecast period (2026-2031). Accelerating the adoption of Building Information Modeling (BIM), job-site automation, and real-time safety analytics is expanding digital footprints across construction value chains. Government mandates that require BIM for public projects, including Poland’s MacroBIM program and Hong Kong’s HKD 30 million (USD 3.82 million) threshold, are shifting procurement criteria toward interoperable digital ecosystems[1]Source: Ewelina Mitera-Kiełbasa and Krzysztof Zima, “BIM Policy in Eastern Europe,” bibliotekanauki.pl. Acute skilled-labor shortages affecting more than 80% of North American contractors are reinforcing demand for autonomous equipment and robotics as workforce multipliers. ESG-linked financing now favors projects that document carbon footprints digitally, underpinning sustained investments in embodied-carbon analytics. Consolidation is gaining momentum as software leaders acquire niche innovators to expand vertically integrated platforms, evidenced by Autodesk’s purchase of Payapps and Hexagon’s acquisition of Voyansi.

Key Report Takeaways

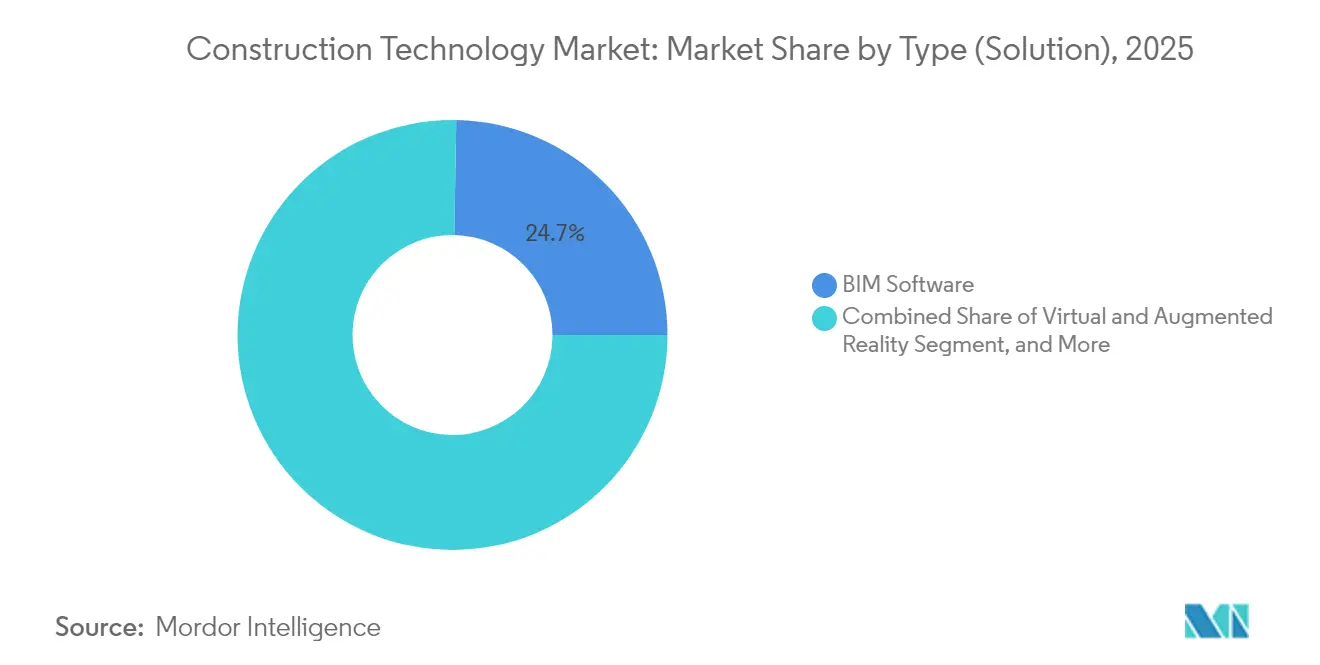

- By solution type, BIM Software captured 24.72% of the Construction Technology market share in 2025, while 3D Printing and Additive Construction is forecast to expand at a 14.12% CAGR through 2031.

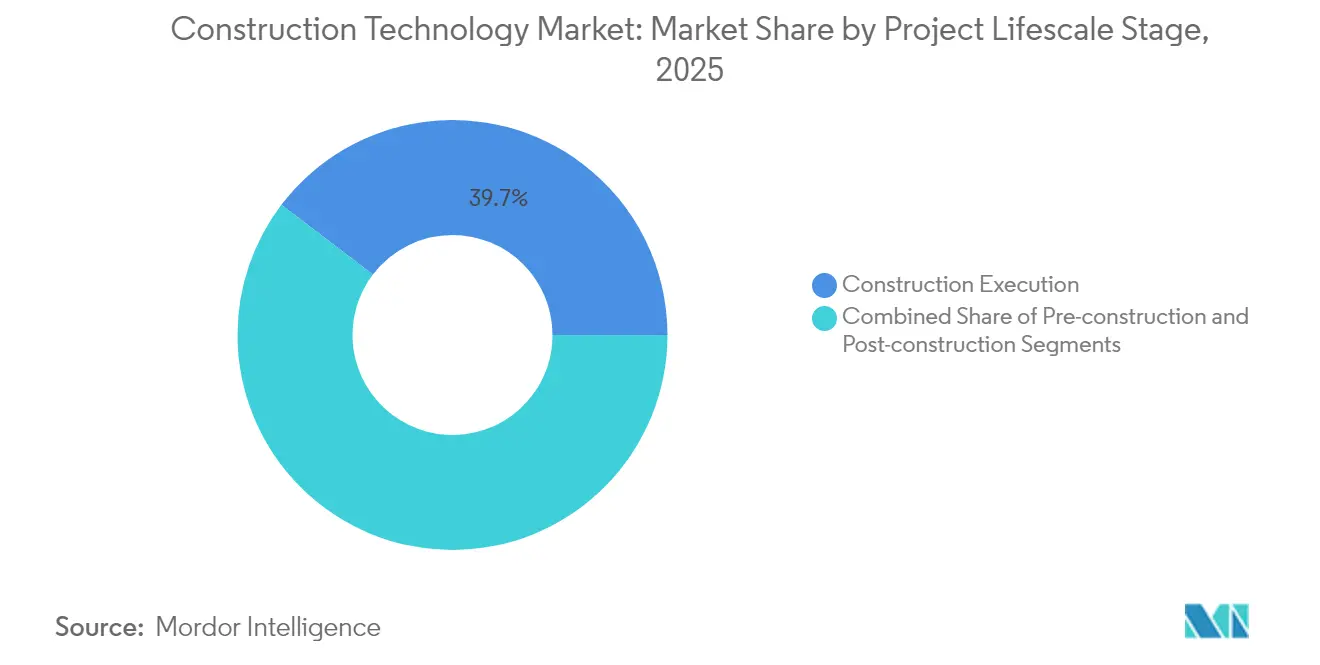

- By project lifecycle stage, Construction Execution accounted for a 39.65% share of the Construction Technology market size in 2025, and Pre-construction is advancing at a 14.38% CAGR to 2031.

- By end-user, Infrastructure and Heavy-Civil contractors led with 29.08% revenue share in 2025; the same segment records the highest projected CAGR at 14.64% through 2031.

- By geography, Asia-Pacific led with 33.25% revenue share in 2025; the same segment records the highest projected CAGR at 14.31% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Construction Technology Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Government BIM Mandates Accelerating Digital Adoption | +2.8% | Global, early leadership in the United Kingdom, the Europe, and Singapore | Medium term (2-4 years) |

| Acute Skilled-Labor Shortage Pushing Job-site Automation | +3.2% | North America and Europe core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Heightened Safety and Compliance Standards Requiring Real-time Monitoring | +1.9% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| ESG-Linked Financing Favouring Digitally Traceable Projects | +2.1% | Asia-Pacific core, North America and Europe | Long term (≥ 4 years) |

| Insurtech-Driven Risk-Based Premium Discounts for Tech-Enabled Sites | +1.4% | North America and Europe | Medium term (2-4 years) |

| Embodied-Carbon Disclosure Rules Boosting Digital Material Tracking | +1.7% | Europe leadership, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government BIM Mandates Accelerating Digital Adoption

Mandatory BIM requirements are resetting qualification criteria for public infrastructure bids across multiple regions. Singapore’s revised Code of Practice and Poland’s EUR 10 million (USD 11.70 million) MacroBIM threshold embed digital workflows from tender to commissioning, while Dubai and Hong Kong enforce BIM documentation for permit approval.[2]Source: Pennsylvania Department of Transportation, “Digital Delivery Directive 2025,” penndot.pa.gov These policies elevate interoperability to a prerequisite for cross-border projects and compress decision cycles as 3D models replace paper-based reviews. Early adopters report measurable gains in cost predictability and schedule adherence that offset initial investments, positioning BIM fluency as a competitive differentiator for international contractors.

Acute Skilled-Labor Shortage Pushing Job-site Automation

North American and European contractors face persistent trade vacancies that exceed 80% of surveyed firms, leading to premium wages and delayed project starts. Autonomous earthmoving units and robotic pile drivers are bridging capacity gaps, with system integrators offering lease models to mitigate capital hurdles. Wearable exoskeletons credited with 83% injury reductions at Toyota and Ford extend productive careers for aging workers, while AI-enabled scheduling reallocates scarce crews to high-value tasks. These labor dynamics convert automation from optional efficiency upgrades into strategic necessities.

Heightened Safety and Compliance Standards Requiring Real-time Monitoring

OSHA’s 2025 update on properly fitting PPE and forthcoming heat-stress rules compel continuous monitoring at project sites. In response, contractors deploy IoT sensors that track environmental thresholds and worker biometrics, generating auditable datasets that satisfy regulators and insurers. Computer-vision platforms flag unsafe behaviors in real time, and ISO 19650-6:2025 sets a global framework for sharing safety information digitally. Early evidence shows reduced incident rates and faster close-out of safety observations, reinforcing technology ROI narratives.

ESG-Linked Financing Favoring Digitally Traceable Projects

Financial institutions now embed carbon-tracking clauses in construction loan covenants as the built environment accounts for 37% of global emissions. Digital twin models that quantify embodied carbon during design phases unlock preferential interest rates, shifting technology adoption from operational choice to capital-access requirement. Bentley’s Carbon Analysis tool exemplifies this trend by guiding material selection toward low-carbon alternatives without cost overruns. ESG scoring transparency thus steers bid evaluations and narrows financing spreads.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Up-front Hardware and Software Costs | -2.1% | Global, higher barriers in emerging markets | Short term (≤ 2 years) |

| Lack of Industry-wide Data Standards and Interoperability | -1.8% | Global fragmentation across regional standards | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities Across Connected Jobsites | -1.6% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Scarcity of Digital-Skilled Workforce in Mid-tier Contractors | -1.4% | Global, with acute shortages in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-front Hardware and Software Costs

Comprehensive BIM suites, drones, and IoT networks require capital outlays that strain cash-flow-dependent contractors, especially in emerging markets where technology leasing is limited. Although subscription models reduce entry barriers, recurring expenses trigger hesitancy among firms operating on thin bid margins. In India, low-cost labor further dampens cost-benefit perceptions, delaying widespread 3D-printing adoption. Demonstrated return on investment remains vital for unlocking latent demand.

Lack of Industry-wide Data Standards and Interoperability

Construction firms juggle a median of 11 disconnected data environments, inflating software expenses and undermining collaboration benefits. ISO 19650 offers a unifying framework, yet divergent regional implementations generate compatibility gaps in multinational projects. Custom integrations absorb IT budgets and introduce version-control risks that erode productivity gains, prompting calls for open-standard acceleration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type (Solution) – BIM Software Anchors Digital Workflows

The BIM Software sub-segment held 24.72% of the Construction Technology market share in 2025, confirming its status as the backbone of collaborative design environments. Continuous enhancements in clash detection and 4D scheduling integrate stakeholders early, establishing BIM data sets that feed downstream applications throughout project lifecycles. The Construction Technology market size attributed to 3D Printing and Additive Construction is projected to grow at a 14.12% CAGR as material science breakthroughs, such as graphene-reinforced concrete with 31% lower emissions, expand structural use cases. Virtual and Augmented Reality applications are proliferating for safety training, with OSHA-funded VR modules improving fall-hazard knowledge retention, a critical metric for insurers.

Project management platforms capitalize on distributed teams that require cloud accessibility, while robotics evolves from pilot deployments to scaled operations in solar, tunnel, and heavy-civil settings. Artificial intelligence gains momentum beyond task automation into generative design tools that evaluate thousands of layout permutations within minutes, a capability recently commercialized in Bentley’s civil site design suite. Digital twins transition from novelty to operating standard, aligning maintenance programs with real-time sensor feeds for predictive asset management.

By Project Lifecycle Stage – Pre-construction Emerges as Growth Engine

Construction Execution accounted for the largest share at 39.65% in 2025 as contractors digitalized field workflows with drones and wearable sensors. Even so, Pre-construction activities record the highest 14.38% CAGR because early-stage optimization yields cascading savings during the build and operate phases. Mandatory BIM submissions for permit issuance force digital modeling before ground-breaking, concentrating technology investment at design freeze. Generative design capabilities embedded in OpenSite+ accelerate scenario testing, compressing scheduling windows and stabilizing budgets.

Post-construction Operations and Maintenance, currently smaller, gains traction as owners exploit digital twins for lifecycle performance monitoring. South Korea’s tunnel monitoring example illustrates how integrating IoT sensors with BIM delivers proactive maintenance triggers that reduce downtime. As performance-based contracts spread, digital twins create recurring revenue for software vendors beyond project close-out.

By End-user – Infrastructure Contractors Lead Adoption

Infrastructure and Heavy-Civil contractors commanded 29.08% of the Construction Technology market size in 2025 due to government stimulus and megaproject complexity. Semi-autonomous machinery adopted by Brazil’s Construtora Barbosa Mello underscores safety gains in high-risk zones. The segment’s 14.64% forecast CAGR reflects rising global infrastructure pipelines tied to climate resilience and mobility upgrades. Commercial and Institutional builders integrate cloud collaboration to manage multiple subcontractors, while Residential developers deploy prefabrication and modular approaches to shorten cycle times under housing-supply pressure.

Public-sector owners institutionalize BIM and digital twin standards within procurement documents, pushing technology through supply chains. Real-estate developers leverage ESG-aligned construction credentials to command valuation premiums. Specialty trade contractors, though resource-constrained, adopt equipment-as-a-service models that democratize access to advanced tools.

Geography Analysis

Asia-Pacific commanded a 33.25% share of the Construction Technology market in 2025 and is on track for a 14.31% CAGR through 2031. China’s prefabricated building segment anchors regional dominance and aligns with national carbon neutrality objectives. India’s infrastructure ambitions, 20 million new homes and high-speed corridors, create a sizable runway despite early-stage BIM adoption. Japan’s risk-averse contractors contemplate digital tools to meet labor-shortage pressures and government incentives for productivity improvement.

North America benefits from systemic digital-delivery mandates such as Pennsylvania’s 3D-first infrastructure directive, which sets statewide precedent for model-based project documentation. Mature venture capital ecosystems accelerate startup innovation in AI and robotic integration, while well-defined safety regulations stimulate demand for monitoring technologies.

Europe drives standardization through ISO and embodied-carbon disclosure legislation, positioning the region as a hub for low-carbon material tracking solutions. Poland’s MacroBIM initiative complements the UK’s early BIM agency leadership, creating templates exported globally. The Middle East and Africa present emerging opportunities, anchored by Dubai’s BIM permit requirement and Saudi Arabia’s Vision 2030 megaprojects that embed digital performance criteria. These markets leapfrog legacy systems as greenfield developments adopt integrated platforms from inception.

Competitive Landscape

The Construction Technology market exhibits moderate fragmentation, where top software ecosystems coexist with specialized niche players. Autodesk leverages its design heritage to integrate cost and payment modules after acquiring Payapps, while Trimble expands field robotics via partnerships and data-rich equipment fleets. Hexagon’s EUR 14 million (USD 16.38 million) purchase of Voyansi enhances BIM services, signaling a strategy to blend consulting with software.[5]Source: Hexagon, “Hexagon acquires Voyansi,” hexagon.com

Bentley Systems differentiates through AI integration, reporting USD 349.8 million revenues in Q4 2024 and projecting 2025 growth on infrastructure digital-twin demand. Procore crosses USD 1 billion in annual recurring revenue with 94% gross retention, underscoring the pull of cloud collaboration for mid-market contractors. WakeCap and Buildots target IoT and computer-vision niches, respectively, offering modular solutions that integrate into broader ecosystems.

Strategic partnerships intensify as hardware vendors integrate sensors directly into machinery, enabling out-of-the-box data flows into project dashboards. White-space opportunities remain in blockchain-enabled smart contracts and AI-augmented exoskeletons that merge worker safety with productivity. Competitive differentiation thus pivots on interoperability and data-driven insights rather than standalone feature sets.

Construction Technology Industry Leaders

Autodesk, Inc.

Trimble Inc.

Procore Technologies, Inc.

Bentley Systems, Incorporated

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bentley Systems posted USD 349.8 million Q4 2024 revenue, up 12.6%, and projected 2025 revenue up to USD 1.49 billion on digital-twin momentum.

- January 2025: Quikrete Holdings agreed to acquire Summit Materials for USD 11.5 billion, including debt, consolidating aggregates, cement, and ready-mix portfolios.

- October 2024: Bentley launched OpenSite+ generative AI and Carbon Analysis capabilities for automated site design and real-time embodied-carbon evaluation.

- July 2024: WakeCap acquired Crews by Core and opened a Silicon Valley research and development hub to enhance AI-powered job-site analytics.

Global Construction Technology Market Report Scope

Construction technology encompasses the cutting-edge tools, equipment, and methodologies employed in the construction sector to boost efficiency, safety, and sustainability. This domain spans diverse solutions, including 3D printing, drones, augmented reality, and automated machinery, all aimed at bolstering pre-construction activities and elevating the quality of building materials produced. The study tracks the revenue generated by selling several market vendors' solutions and services. The study also tracks the underlying growth trends and macroeconomic impacts on the market.

The construction technology market is segmented by type (solutions [virtual and augmented reality, artificial intelligence, 3D printing, building information modeling (BIM) software, automated data collection and predictive analytics, drones, robotics, project management software, wearables, other Types (digital twin, sustainable technology, blockchain technology, 4D simulation, etc.)] and services) and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Virtual and Augmented Reality |

| Building Information Modeling (BIM) Software | |

| Project Management and Collaboration Platforms | |

| Drones and Unmanned Aerial Vehicles | |

| Robotics and Autonomous Equipment | |

| 3D Printing and Additive Construction | |

| Artificial Intelligence and Machine Learning | |

| Automated Data Collection and Predictive Analytics | |

| Wearables and Exoskeletons | |

| Digital Twin and 4D/5D Simulation | |

| Sustainable and Green Construction Tech | |

| Blockchain for Supply-chain and Payments | |

| Services | Consulting and Integration |

| Managed Services | |

| Training and Support |

| Pre-construction (Design and Engineering) |

| Construction Execution |

| Post-construction (Operations and Maintenance) |

| Residential Construction Companies |

| Commercial and Institutional Builders |

| Infrastructure and Heavy-Civil Contractors |

| Specialty Trade Contractors |

| Government and Public-Sector Owners |

| Real-Estate Developers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Solutions | Virtual and Augmented Reality | |

| Building Information Modeling (BIM) Software | |||

| Project Management and Collaboration Platforms | |||

| Drones and Unmanned Aerial Vehicles | |||

| Robotics and Autonomous Equipment | |||

| 3D Printing and Additive Construction | |||

| Artificial Intelligence and Machine Learning | |||

| Automated Data Collection and Predictive Analytics | |||

| Wearables and Exoskeletons | |||

| Digital Twin and 4D/5D Simulation | |||

| Sustainable and Green Construction Tech | |||

| Blockchain for Supply-chain and Payments | |||

| Services | Consulting and Integration | ||

| Managed Services | |||

| Training and Support | |||

| By Project Lifecycle Stage | Pre-construction (Design and Engineering) | ||

| Construction Execution | |||

| Post-construction (Operations and Maintenance) | |||

| By End-user | Residential Construction Companies | ||

| Commercial and Institutional Builders | |||

| Infrastructure and Heavy-Civil Contractors | |||

| Specialty Trade Contractors | |||

| Government and Public-Sector Owners | |||

| Real-Estate Developers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Construction Technology market in 2026?

The Construction Technology market size reached USD 6.37 billion in 2026.

What is the projected CAGR for Construction Technology through 2031?

The market is forecast to grow at a 12.58% CAGR from 2026 to 2031.

Which solution type holds the highest Construction Technology market share?

BIM Software leads with a 24.72% share in 2025.

Which end-user segment is expanding the fastest?

Infrastructure and Heavy-Civil contractors show the highest growth at 14.64% CAGR.

Page last updated on: