Predictive Maintenance In The Energy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 8.61 Billion |

| Growth Rate (2026 - 2031) | 25.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

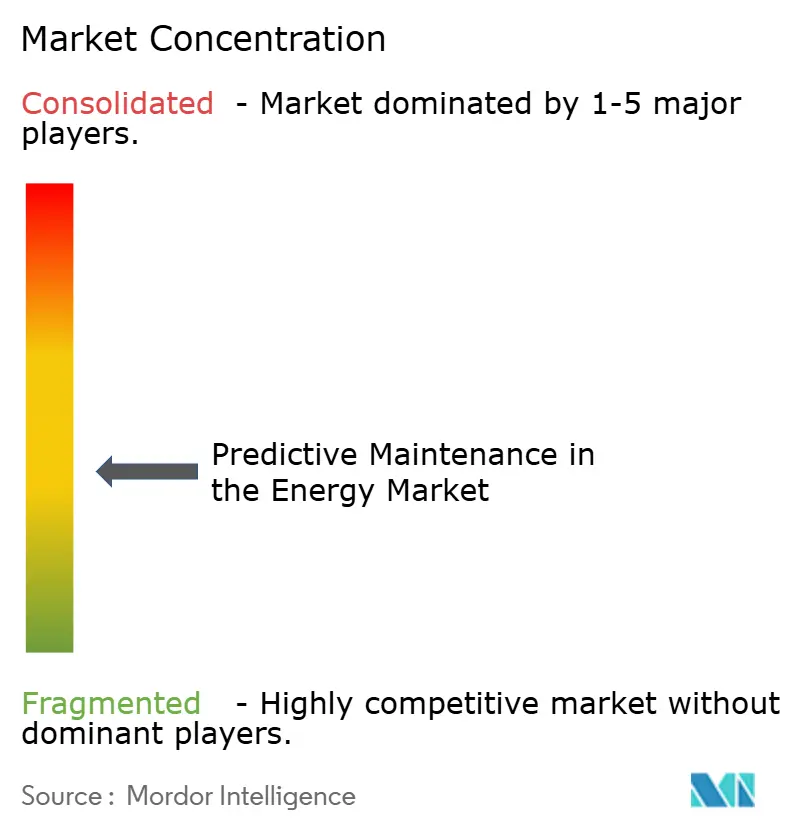

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Predictive Maintenance In The Energy Market Analysis by Mordor Intelligence

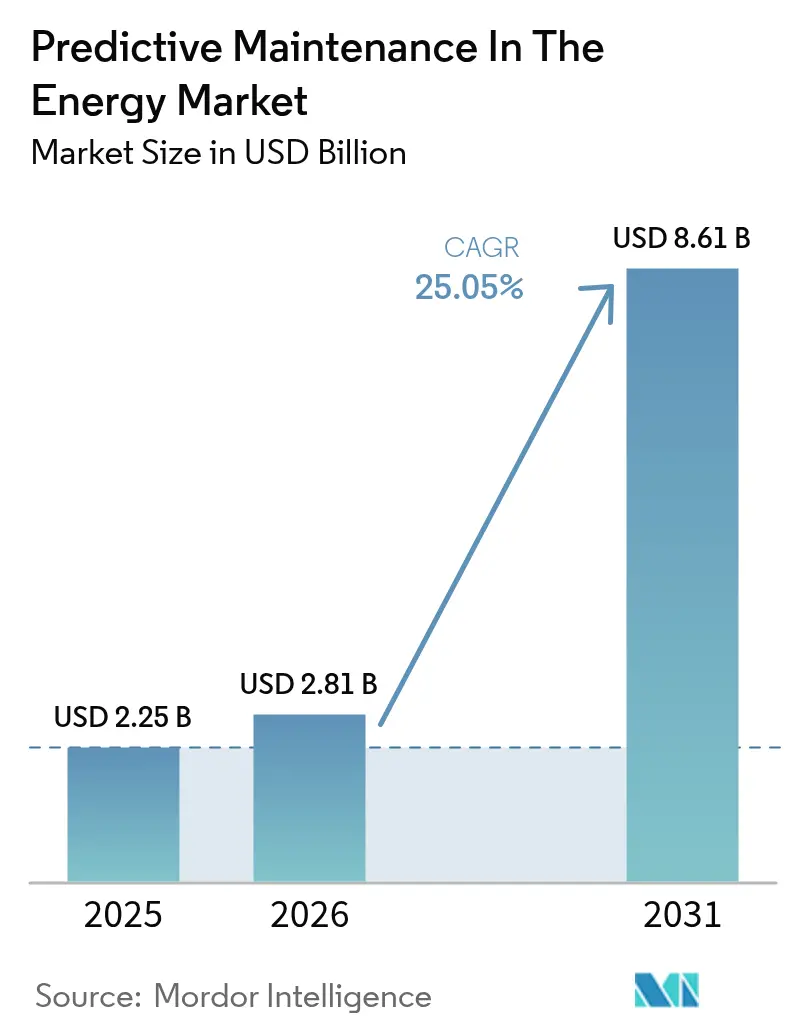

The predictive maintenance in the energy market size is expected to grow from USD 2.25 billion in 2025 to USD 2.81 billion in 2026 and is forecast to reach USD 8.61 billion by 2031 at 25.05% CAGR over 2026-2031. Unrelenting electrification, surging data-center build-outs, and mounting grid-reliability concerns are pushing asset owners to replace run-to-failure routines with data-driven models that lower the lifetime cost of ownership while stretching remaining asset life. Regulatory mandates such as the EPA’s 90% carbon-capture rule for long-term coal plants and the EU’s Corporate Sustainability Reporting Directive are catalyzing digitalization budgets because operators must now prove both uptime and emissions performance. Simultaneously, rapid IIoT sensor price declines and maturing AI algorithms are shrinking payback cycles to 18-24 months for large fleets, amplifying adoption momentum across turbine halls, substations, and midstream pipelines. Vendors that fuse edge computing with cloud analytics already report nine-figure savings driven by shorter outage windows and optimized part inventories.

Key Report Takeaways

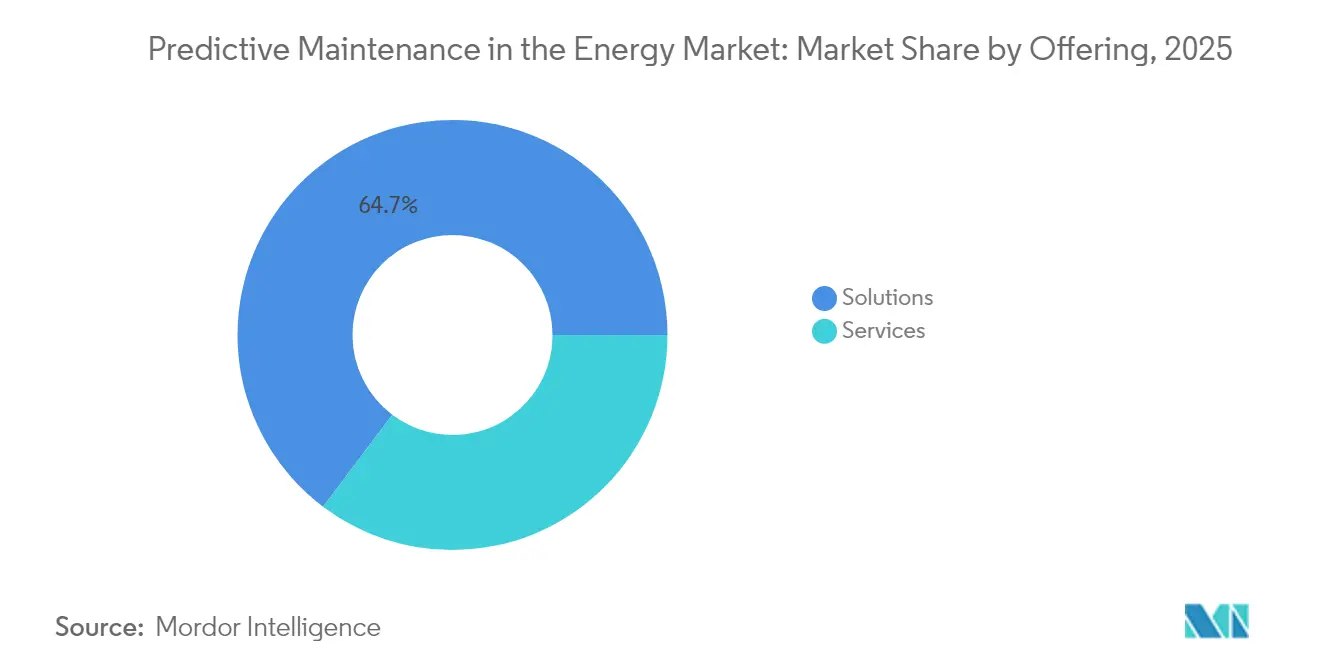

- By offering, solutions captured 64.72% of the predictive maintenance in the energy market share in 2025, whereas services are projected to grow the fastest at 25.3% CAGR to 2031.

- By deployment model, the cloud segment held 72.05% revenue share of the predictive maintenance in the energy market in 2025; it is also forecast to expand at a 26.1% CAGR through 2031.

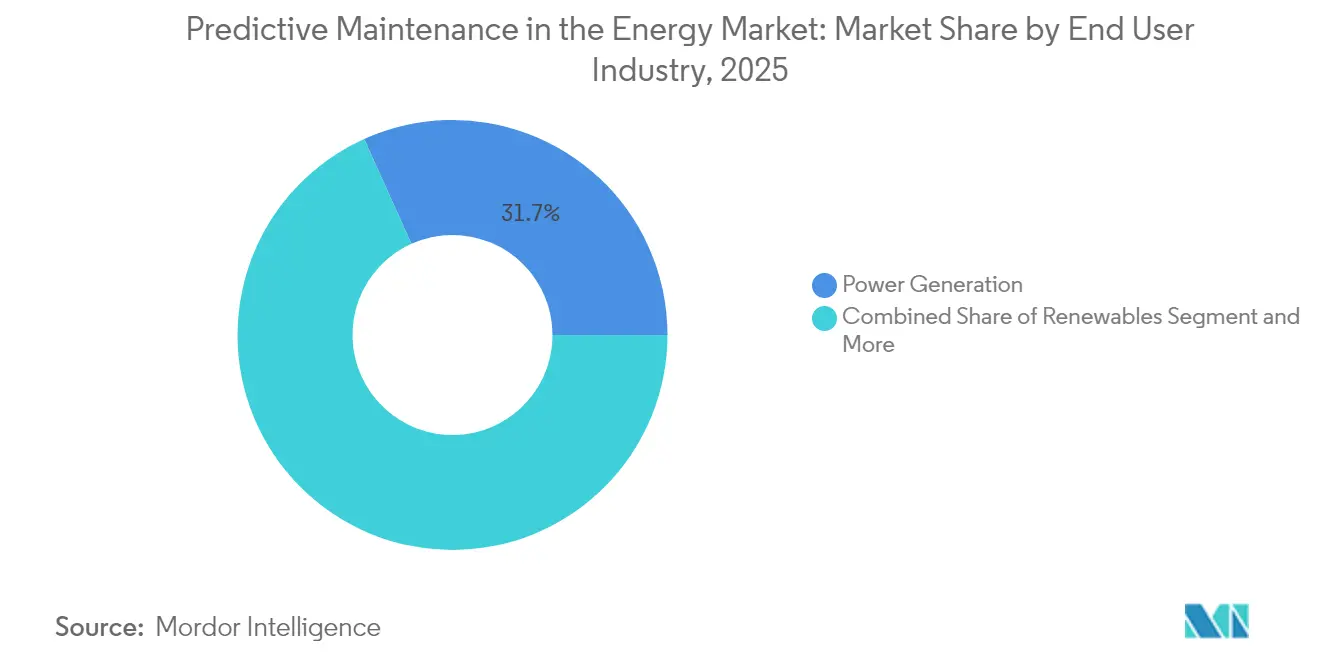

- By end-user industry, power generation led with 31.74% share in 2025, while renewables are advancing at 25.9% CAGR to 2031.

- By asset type, turbines and rotating equipment accounted for 35.02% of the predictive maintenance in the energy market size in 2025; transformers and substations will accelerate at 26.4% CAGR between 2026-2031.

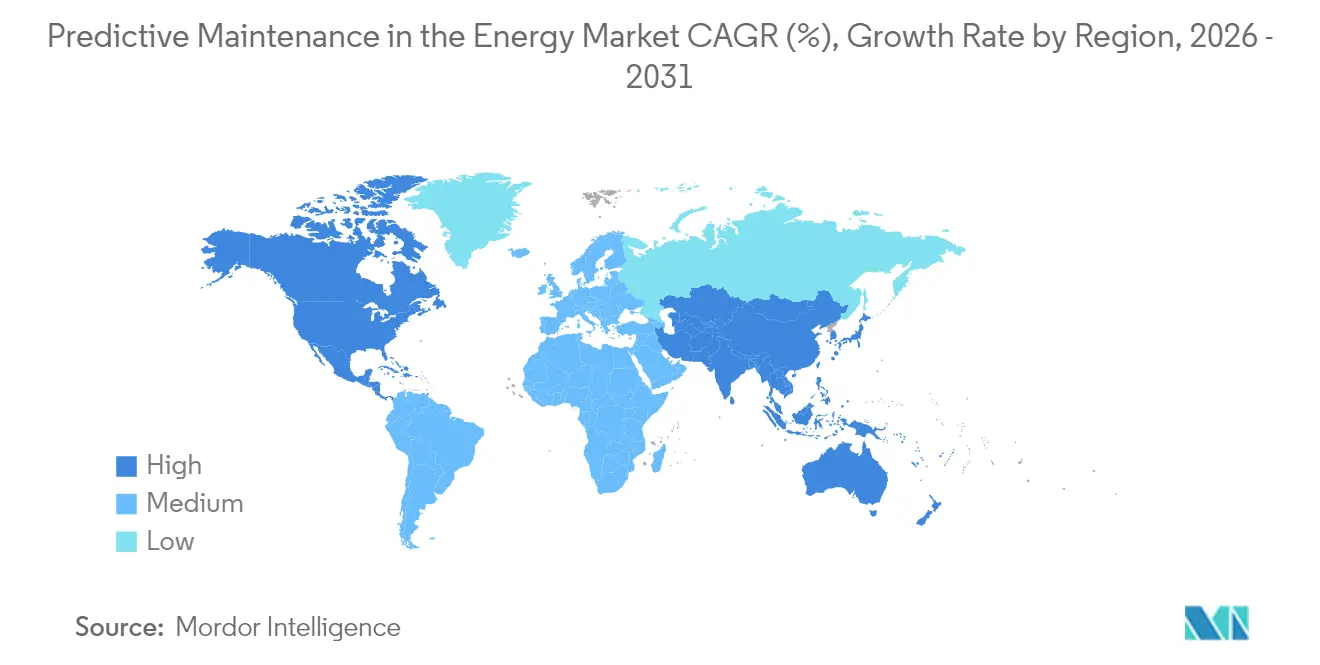

- By geography, North America commanded 27.55% of 2025 revenue, but Asia-Pacific is the fastest-growing region at 25.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Predictive Maintenance In The Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging energy infrastructure and grid reliability focus | +4.2% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Integration of IIoT, AI and big-data analytics | +6.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Cost pressure to cut unplanned downtime | +5.1% | Global | Short term (≤ 2 years) |

| Regulatory mandates on safety / emissions | +3.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Drone- and satellite-enabled remote sensing fusion | +2.8% | Global, early adoption in offshore applications | Long term (≥ 4 years) |

| Digital-twin-driven risk-based maintenance | +3.4% | North America and EU, pilot deployments in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration of IIoT, AI and Big-Data Analytics

The fusion of low-cost sensors with AI pattern-recognition algorithms is recasting maintenance from reactive to prescriptive modes across turbine decks and compressor stations.[1]Chevron Corporation, “Chevron Digital Transformation,” chevron.comSiemens’ Senseye platform now generates digital behavior models automatically, slicing maintenance spend by up to 40% while addressing acute workforce shortages. Chevron’s real-time anomaly detection for leak prevention safeguards continuous power delivery to energy-intensive data-center clusters. Edge nodes process torrents of vibration and temperature data locally before forwarding condensed insights to the cloud for fleet-wide pattern mining, creating near-autonomous ecosystems that schedule interventions without human prompts. These developments place predictive maintenance in the energy market squarely at the center of digital-transformation roadmaps for asset-heavy utilities.

Cost Pressure to Cut Unplanned Downtime

Escalating outage penalties and demand spikes from AI workloads are making downtime a board-level risk, moving predictive maintenance from a discretionary line item to an operational imperative. NextEra Energy’s gas-turbine program delivered a 23% outage reduction and USD 25 million in annual savings, validating the hard ROI underpinning the predictive maintenance in the energy market. Large oil-and-gas operators have documented 20–40% asset-life extension through optimized service intervals, compounding value over decades-long equipment cycles. Firms that lag on adoption face customer-experience erosion and higher delivered-energy costs as competitors sustain higher asset availability with leaner spares inventories.

Aging Energy Infrastructure and Grid Reliability Focus

With average transformer ages topping 38 years in the United States, utilities earmark roughly 9.8% of annual revenue for grid modernization.[2]IBM, “Grid Modernization Spending Patterns,” ibm.com U.S. infrastructure alone needs USD 600 billion by 2030 to keep pace with electrification, elevating predictive maintenance investments that pre-empt cascading failures. Hitachi Energy’s USD 155 million North American expansion embeds online monitoring in every new distribution transformer to slash unplanned downtime by up to 50% . Drone and satellite imagery now map vegetation encroachment and hotspot signatures across thousands of miles of lines, generating actionable work orders that enhance service reliability.

Regulatory Mandates on Safety / Emissions

Performance-based environmental regulation is tightening simultaneously in the United States, EU, and California, forcing power producers to demonstrate verifiable emissions reductions.[3]Morgan Lewis, “EPA 2024 GHG Standards Overview,” morganlewis.com GE Vernova’s USD 14.2 billion Saudi program showcases how advanced carbon-capture units rely on predictive maintenance to keep scrubbers within compliance thresholds. As operators roll out granular carbon-accounting frameworks to satisfy SB-253 and CSRD disclosures, the same data backbone supports condition monitoring, reinforcing uptake of the predictive maintenance in the energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront implementation and integration cost | -3.8% | Global, more acute in emerging markets | Short term (≤ 2 years) |

| Rising cyber-security vulnerabilities | -2.9% | Global, critical in North America and EU | Medium term (2-4 years) |

| Scarcity of energy-domain data-science talent | -2.1% | Global, severe in Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Data-ownership and liability disputes in multi-party assets | -1.7% | North America and EU regulatory environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Implementation and Integration Cost

Comprehensive sensor retrofits, edge gateways, and cloud orchestration commonly push project budgets into eight figures for large utilities, deterring cash-constrained operators in developing economies. GE Vernova’s nearly USD 600 million U.S. factory upgrades illustrate the scale of modernization needed to unlock predictive value at fleet level. Rising copper and rare-earth prices have inflated hardware outlays by up to 25% since 2024. Nonetheless, leading adopters recuperate capital within two years, and financial barriers are softening as vendors roll out subscription models linked to performance guarantees, reiterating the long-term competitiveness of the predictive maintenance in the energy market.

Rising Cyber-Security Vulnerabilities

The rapid proliferation of connected sensors has expanded the attack surface across generation and grid assets, with 68 OT-linked cyber incidents causing physical consequences in 2023. Research on solar-inverter exploits underscores how maintenance telemetry can become an entry point for threat actors. Utilities now embed zero-trust architectures and AI-assisted threat detection, but these layers add cost and complexity that may slow smaller utilities from entering the predictive maintenance in the energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Drive Market Foundation

Solutions controlled 64.72% of the predictive maintenance in the energy market in 2025, reflecting operators’ preference for unified platforms that amalgamate analytics, visualization, and workflow automation. Software suites capable of ingesting terabytes of turbine and transformer data per day remain central, while embedded sensors equipped with on-device inference augment edge intelligence, reducing unnecessary data egress and accelerating insights. Services, although smaller in absolute revenue, sprint ahead at 25.3% CAGR as utilities and independent power producers rely on vendors for integration, change management, and 24×7 monitoring.

Service providers benefit from widening talent gaps in data science and rotating-machinery physics. Integration and implementation are especially valued when operators migrate legacy historian databases into cloud data lakes without production interruptions. Managed services, often structured as outcome-based contracts, guarantee availability metrics that align vendor incentives with asset performance. As clients prioritize outcomes over toolkits, the predictive maintenance in the energy industry is steadily morphing into a service-oriented market where operational excellence overrides feature checklists.

By Deployment Model: Cloud Dominance Accelerates

Cloud deployments represented 72.05% share of the predictive maintenance in the energy market in 2025, a position expected to strengthen as algorithm complexity and data volumes outstrip on-premise compute capacity. A single offshore wind farm now generates tens of terabytes of SCADA and lidar data daily; instant scalability and continuous model retraining favor cloud-native architectures. Edge-cloud hybrids mitigate latency for load-shedding or blade-pitch adjustments, keeping mission-critical loops local while bulk analytics run centrally.

On-premise systems persist in remote basins and nuclear sites with stringent sovereignty or latency requirements, yet most vendors bundle cloud connectors for future migration. Honeywell’s 5G-enabled smart-meter roll-out with Verizon exemplifies the shift: secure cellular backhaul funnels sub-second telemetry into an AI engine that forecasts transformer hot-spots days in advance. Such use cases underscore why the predictive maintenance in the energy market is entwined with broader grid-digitalization initiatives premised on ubiquitous, low-latency connectivity.

By End-User Industry: Power Generation Leads, Renewables Accelerate

Power generation held 31.74% of 2025 revenue, cementing its role as the core customer base for the predictive maintenance in the energy market. Fossil and nuclear operators have the most to lose from unplanned outages that can idle GW-scale capacity and breach emissions permits. Gas turbines alone contain more than 300 monitored parameters, making them fertile ground for AI diagnostics that identify combustion anomalies weeks before failure.

Renewables, however, is the standout growth engine at 25.9% CAGR through 2031. Remote wind farms, desert-based solar arrays, and battery-storage systems require minimal on-site staff, favoring AI-guided inspections and automated work orders delivered to drone fleets. GE Vernova’s 2.7 GW SunZia supply deal signals the colossal installation base now coming under predictive purview, swelling the predictive maintenance in the energy market size.

By Asset Type: Rotating Equipment Dominates, Transformers Surge

Turbines and other rotating equipment contributed 35.02% to the predictive maintenance in the energy market size in 2025, owing to their high failure cost and mature vibration-analysis toolsets. Predictive models flag misalignment or lubrication faults long before catastrophic damage, permitting planned interventions during scheduled outages. Continuous improvements in MEMS accelerometers and acoustic sensors feed richer datasets that sharpen failure-probability curves.

Transformers and substations, meanwhile, post the strongest growth trajectory at 26.4% CAGR. Grid-edge volatility from distributed solar and EV charging stresses decades-old transformers, driving utilities to embed fiber-optic temperature probes and dissolved-gas monitors for real-time diagnostics. Hitachi Energy’s U.S. factory investments integrate these capabilities at manufacturing stage, reinforcing reliability and accelerating adoption. Pipelines, compressors, pumps, and valves constitute sizable niches where wireless sensors lower deployment friction, collectively widening addressable revenue for the predictive maintenance in the energy market.

Geography Analysis

North America retained leadership with 27.55% of 2025 revenue, supported by federal infrastructure programs, aggressive utility spending, and early adoption of AI platforms. The Energy Information Administration projects domestic electricity demand to rise 15-20% by 2030, partly due to hyperscale data centers, intensifying the focus on outage prevention. Cloud-native regulatory environments and ample venture financing further accelerate new-tech pilots, anchoring regional dominance in the predictive maintenance in the energy market.

Europe maintains steady momentum driven by the Green Deal’s decarbonization targets and strict outage-penalty regimes that elevate reliability metrics. The Corporate Sustainability Reporting Directive obliges utilities to disclose real-time emissions and energy-efficiency KPIs, for which predictive-maintenance datasets are highly synergistic. Large fleet operators are combining digital twins with satellite-based vegetation monitoring to meet both compliance and resilience goals.

Asia-Pacific is the fastest-growing territory at 25.95% CAGR, buoyed by China’s state-backed digital-grid blueprint and Southeast Asia’s rapid electrification. China Southern Power Grid’s end-to-end digital transformation shows how leapfrog technology can embed predictive workflows directly into new infrastructure, bypassing legacy bottlenecks. Concurrently, India and Indonesia invest heavily in transmission upgrades, creating greenfield demand for cloud-delivered analytics. The Middle East and Africa, though smaller, show rising interest as mega-projects under Vision 2030 and similar initiatives demand flawless uptime under harsh desert conditions, expanding the predictive maintenance in the energy market footprint.

Regulatory Landscape

Regulation is increasingly shaping predictive-maintenance deployments through cyber and reliability standards for digitalized grid operations, and through governance frameworks for AI used in critical infrastructure. In the United States, FERC Order No. 919 issued in March 2026 approved 11 modified NERC CIP Reliability Standards that recognize virtualization and newer technologies, anchoring governance around OT security and asset visibility. NIST is advancing a Trustworthy AI profile for critical infrastructure, and H.R. 9339 in the 119th Congress aligns with auditable AI governance requirements for bulk-power contexts.

In Europe, the EC published a Digitalisation and AI Strategy Roadmap in June 2026, signaling data-access and interoperability priorities for AI enabled services, while the EU AI Act timeline and related discussions influence how utilities formalize risk-management controls. In the UK, Ofgem and DSAP guidance in March 2026 reinforces data best practices and digitalization standards under RIIO-ED2 and RIIO-3 for condition monitoring and maintenance traceability.

Competitive Landscape

The predictive maintenance in the energy market is moving from fragmented point tools to vertically integrated ecosystems. Tier-one OEMs such as GE Vernova, Siemens Energy, and ABB now bundle AI analytics, sensors, and managed services, pressuring pure-play software entrants to specialize in niche algorithms or domain-specific datasets. Consolidation is also visible in cross-industry alliances: Hitachi Energy’s AWS partnership delivers satellite-driven vegetation management, while Honeywell’s Verizon deal layers 5G connectivity onto grid endpoints to feed real-time AI models.

Investment priorities center on edge-cloud synergy, autonomous maintenance orchestration, and cross-asset optimization. Patent filings related to failure-prediction neural networks and federated-learning approaches for privacy-sensitive data have surged, underscoring the sector’s innovation cadence. Traditional IT giants leverage hyperscale infrastructure to offer pay-as-you-go AI engines, enticing mid-tier utilities that lack the capital for bespoke systems but still seek entry into the predictive maintenance in the energy market

Predictive Maintenance In The Energy Industry Leaders

IBM Corporation

SAP SE

Siemens AG

Intel Corporation

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Utility programs at the distribution and transmission edge are creating whitespace beyond rotating-equipment monitoring, particularly for transformers, substations, and line-corridor reliability. In India, Maharashtra State Electricity Distribution Company Ltd (MSEDCL) launched the Vitaran Intelligence AI platform in May 2026 for distribution network management, and Karnataka Power Transmission Corporation Limited (KPTCL) reported an 85% reduction in transmission outages after deploying drone-based monitoring for HV/EHV corridors in June 2026. These deployments support an opportunity for vendors that combine inspection inputs (thermal imaging, LiDAR, drone imagery) with SCADA and asset histories, then convert detections into prioritized work orders and outage-prevention actions across large fleets.

A separate growth corridor is predictive maintenance expansion into thermal networks and multi-energy systems through digital twins and real-time optimization. Operational teams are looking for simulation-backed setpoint changes and fault localization, rather than isolated anomaly alerts. Gradyent projects in Europe reflect this direction: Utilitas selected Gradyent in March 2026 for a real-time digital twin supporting Tallinns district heating network, and Veolia Warsaw selected Gradyents digital twin platform in April 2026 to optimize Europes largest district heating system. As operators integrate operational historian workflows, such as IBM Maximo-connected processes, with AI models that forecast failures weeks ahead, differentiation is increasingly tied to data integration speed, governance for multi-party assets, and closed-loop execution that connects predictions to maintenance scheduling and spare-parts decisions.

Recent Industry Developments

- July 2026: ABB and Orsted commenced an AI-based fault prediction pilot at the Avedore Power Station in Denmark, using electrical system data to support planned maintenance. The project indicates growing use of AI diagnostics in complex power-station environments where failure detection needs to translate into actionable maintenance windows and reduced outage risk.

- June 2026: Shell expanded its AI-driven predictive maintenance collaboration with C3.ai, scaling deployment across its global operations and monitoring more than 13,000 pieces of equipment. This shows how enterprise rollouts are shifting predictive maintenance from isolated pilots to standardized, fleet-level programs with repeatable data pipelines and governance.

- April 2025: Duke Energy agreed to procure up to 11 U.S.-made gas turbines from GE Vernova, supported by GE's USD 600 million Greenville facility expansion. The deal strengthens the installed base for long-term service and digital monitoring, broadening the scope for predictive maintenance platforms tied to turbine performance and availability commitments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software, services, and supporting deployments used to predict equipment failures in energy operations, so maintenance can be planned before breakdowns happen. It includes solutions used across power generation, transmission and distribution, renewables, and oil and gas assets.

Scope exclusions: Routine reactive maintenance activities and general plant automation systems are excluded unless they are sold and used specifically for predictive maintenance outcomes.

Segmentation Overview

- By Offering

- Solutions

- Software Platforms

- Embedded Hardware and Sensors

- Services

- Integration and Implementation

- Managed Services

- Solutions

- By Deployment Model

- Cloud

- On-premise

- By End-user Industry

- Power Generation (Thermal, Nuclear, Hydro)

- Renewables (Wind, Solar, Storage)

- Oil and Gas (Upstream, Mid, Downstream)

- Utilities and TandD

- Mining and Minerals

- By Asset Type

- Turbines and Rotating Equipment

- Transformers and Sub-stations

- Pipelines and Compressors

- Pumps and Valves

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the factual backbone for the model, especially around energy asset fleets, operating spend, and digital adoption signals. We refer to public sources such as the International Energy Agency (IEA), the US Energy Information Administration (EIA), the World Bank, the US Bureau of Labor Statistics, and the International Renewable Energy Agency (IRENA) to understand asset additions, generation mix shifts, and operating patterns.

To shape realistic price and adoption assumptions, we also review company annual reports, investor presentations, regulatory filings, and industry association publications, along with credible press and technical papers on condition monitoring and analytics. When needed, paid subscriptions are used for company financials and intelligence, patent landscaping, and shipment level trade checks on relevant sensors and industrial equipment categories. These desk research sources are illustrative, and additional public and paid references are used for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work focuses on validating what predictive maintenance is actually being bought and deployed in energy settings, and how budgets are split between software, services, and ongoing support. We speak with a mix of utilities and power operators, renewable asset owners, oil and gas maintenance teams, system integrators, and domain specialists. We then reconcile differences across regions so adoption assumptions are not driven by one geography alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 19% | APAC: 41% |

| Mid tier: 45% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 20% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool from energy asset counts and operating intensity, then applies adoption and spend factors tied to predictive maintenance programs. The model is then corroborated through selective bottom-up approximations such as sampled vendor revenue disclosures, channel feedback on typical contract sizes, and sanity checks using average annual spend per monitored asset category.

Key inputs include the installed base and additions of critical assets (such as turbines, transformers, rotating equipment, and grid substations), outage and reliability pressure indicators, digitalization and IIoT penetration in energy operations, cloud versus on-premise deployment preference, and typical software plus services attach rates. Where bottom-up signals are incomplete, gaps are handled by using bounded ranges from interviews and applying conservative roll-forward assumptions until a repeatable data trail is available.

For forecasts, scenario analysis is used, with base, conservative, and faster adoption cases linked to capital cycle timing, grid expansion, renewable additions, and cybersecurity and data governance constraints. The final trajectory is only accepted after scenarios align with expert views on budget cycles and expected improvements in analytics performance over the forecast period.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals like energy OPEX trends, digital maintenance spend discussions in public filings, and observed rollout patterns across regions and asset types. When a variance looks unusual, we revisit the assumptions behind adoption rates, pricing progression, and the split between solutions and services. We then re-contact select respondents to confirm whether the change reflects real market movement or is driven by model mechanics.

Before sign-off, the dataset and calculations are reviewed in multiple steps so arithmetic, currency conversion timing, and regional roll-ups are consistent. Reports are refreshed annually, and interim updates are made when a material event changes adoption or spending patterns. Right before delivery, the latest public updates are rechecked so clients receive the most current view available at that time.

Mordor Intelligence's Energy Predictive Maintenance Market Size Compared With Other Published Estimates

Published market numbers for predictive maintenance in energy often differ because the scope boundary is not always the same, and the time window used as the starting year varies across sources. Differences also come from whether services are fully counted, how cloud subscription pricing is treated, and how quickly adoption is assumed to expand across asset-heavy parts of the energy value chain.

The benchmark table shows a spread that is mainly explained by what gets counted as energy-specific predictive maintenance and when the value is recognized. In Mordor Intelligence's model, the total includes both solutions and services across major energy end uses, rather than focusing only on AI-driven use cases or a narrower asset list.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.81 B (2026) | |

| Marketplace Publisher A | USD 2.25 B (2025) | Uses an earlier base year and a shorter horizon, and the inclusions around services and multi-year software recognition are not clearly explained in the public summary, which can shift the starting value. |

| Industry Research Outlet B | USD 1.40 B (2025) | Centers on AI-driven predictive maintenance for power generation and high-voltage transmission with a limited asset list, which typically excludes broader energy end uses and non-AI predictive maintenance spending. |

When the scope is widened from a few AI-led asset classes to the full set of energy operations, and when solution plus service spending is treated consistently, the midpoint estimate tends to move toward the broader view. That is why we anchor the model to observable energy asset footprints and repeatable spend drivers, and then validate the totals with interview-based reality checks and bottom-up reasonableness tests.

Key Questions Answered in the Report

What is the current value of the predictive maintenance in the energy market?

The predictive maintenance in the energy market size stands at USD 2.81 billion in 2026.

How fast is the predictive maintenance in the energy market expected to grow?

The market is forecast to register a 25.05% CAGR, reaching USD 8.61 billion by 2031.

Which deployment model is most popular?

Cloud solutions dominate with 72.05% share in 2025 and are expanding at 26.1% CAGR.

Which end-user segment is growing the fastest?

Renewables lead growth at 25.9% CAGR as wind and solar installations proliferate.

Page last updated on: