Power Strip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

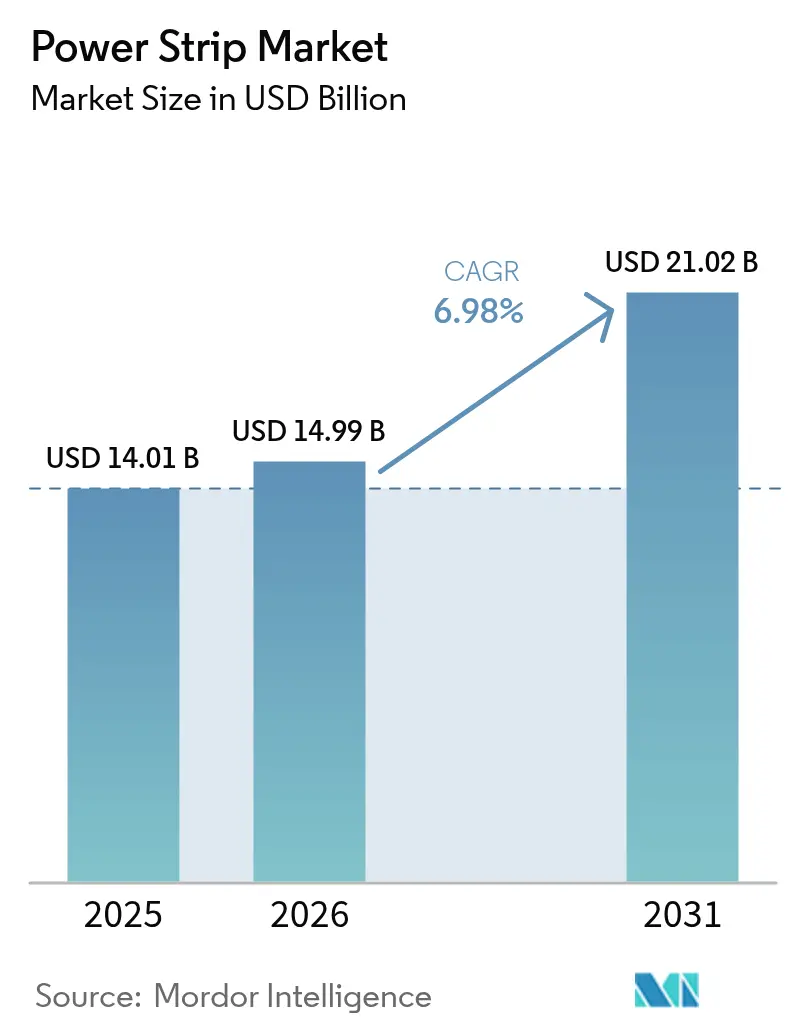

| Market Size (2026) | USD 14.99 Billion |

| Market Size (2031) | USD 21.02 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Strip Market Analysis by Mordor Intelligence

The power strip market size is expected to grow from USD 14.01 billion in 2025 to USD 14.99 billion in 2026 and is forecast to reach USD 21.02 billion by 2031 at 6.98% CAGR over 2026-2031. Growth is propelled by the convergence of data-center electrification, smart-home mandates, and industrial IoT roll-outs that collectively increase outlet density requirements and elevate functionality expectations. Operators of hyperscale data halls are demanding intelligent rack-mount power distribution units (PDUs) with outlet-level metering, while residential buyers seek WiFi-enabled models that can shed standby loads automatically. Rising automation across manufacturing lines, combined with government efficiency incentives, is widening the customer base and nudging average selling prices upward. Competition remains moderate as safety certification costs curb new-entrant expansion, yet profitability is supported by premium pricing for compliant, feature-rich SKUs.

Key Report Takeaways

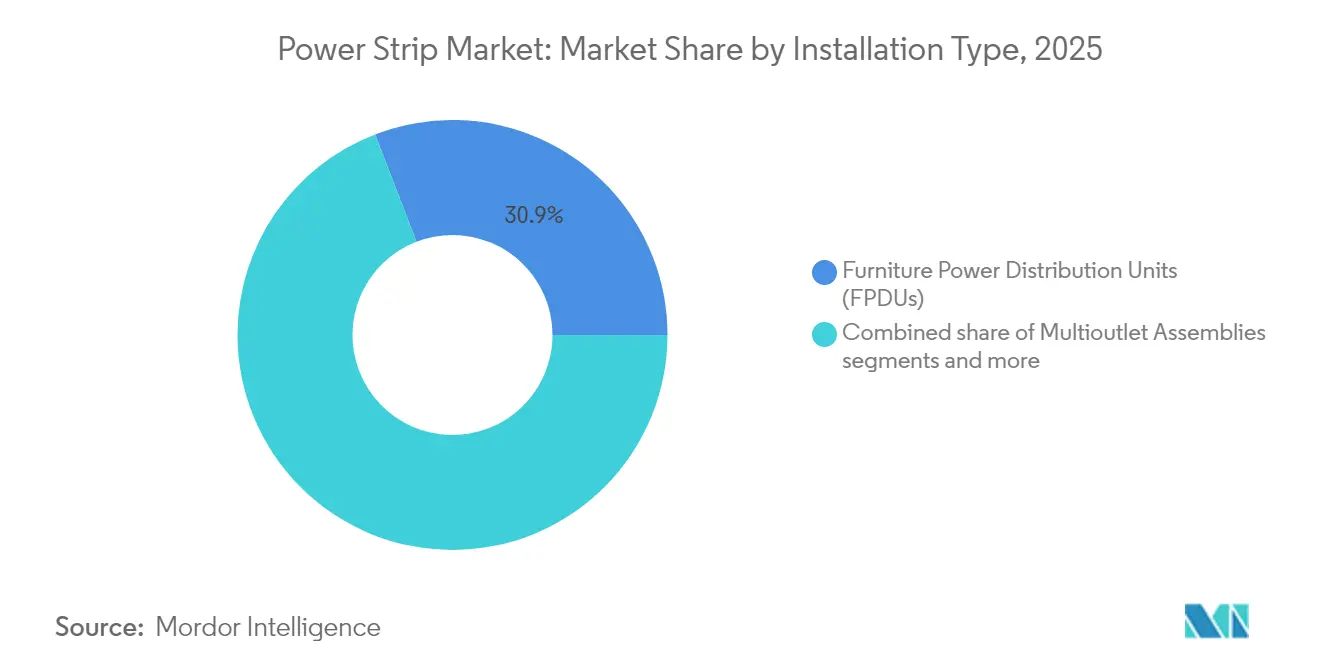

- By installation type, Furniture Power Distribution Units (FPDUs) led with 30.86% of power strip market share in 2025; Smart WiFi/Bluetooth models are projected to expand at a 7.45% CAGR through 2031.

- By protection feature, surge-protected units captured 37.05% revenue share of the power strip market in 2025, while energy-monitoring variants are advancing at an 7.78% CAGR to 2031.

- By application, general-purpose products accounted for 50.42% of the power strip market in 2025; smart applications post the fastest trajectory at 7.96% CAGR.

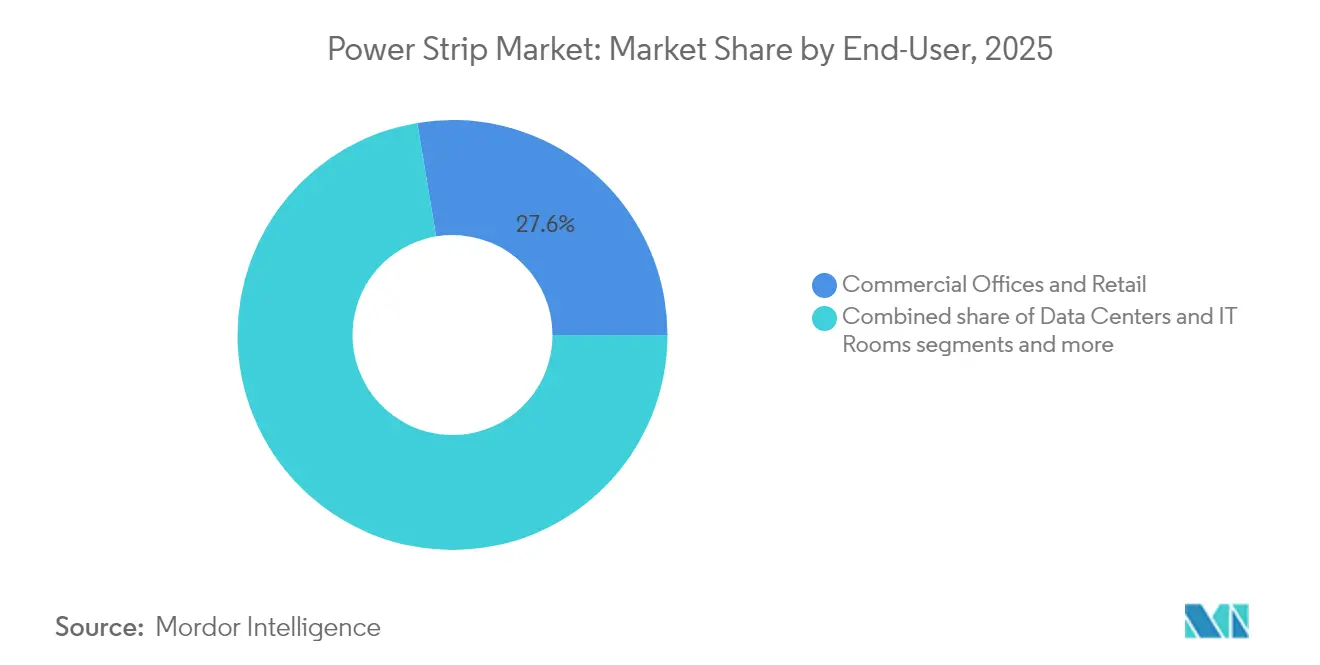

- By end user, commercial offices and retail spaces held 27.62% of the power strip market share in 2025, whereas the residential category is poised for a 7.46% CAGR to 2031.

- By distribution channel, offline outlets dominated with 66.85% revenue share in 2025; online platforms exhibit an 8.35% CAGR outlook to 2031.

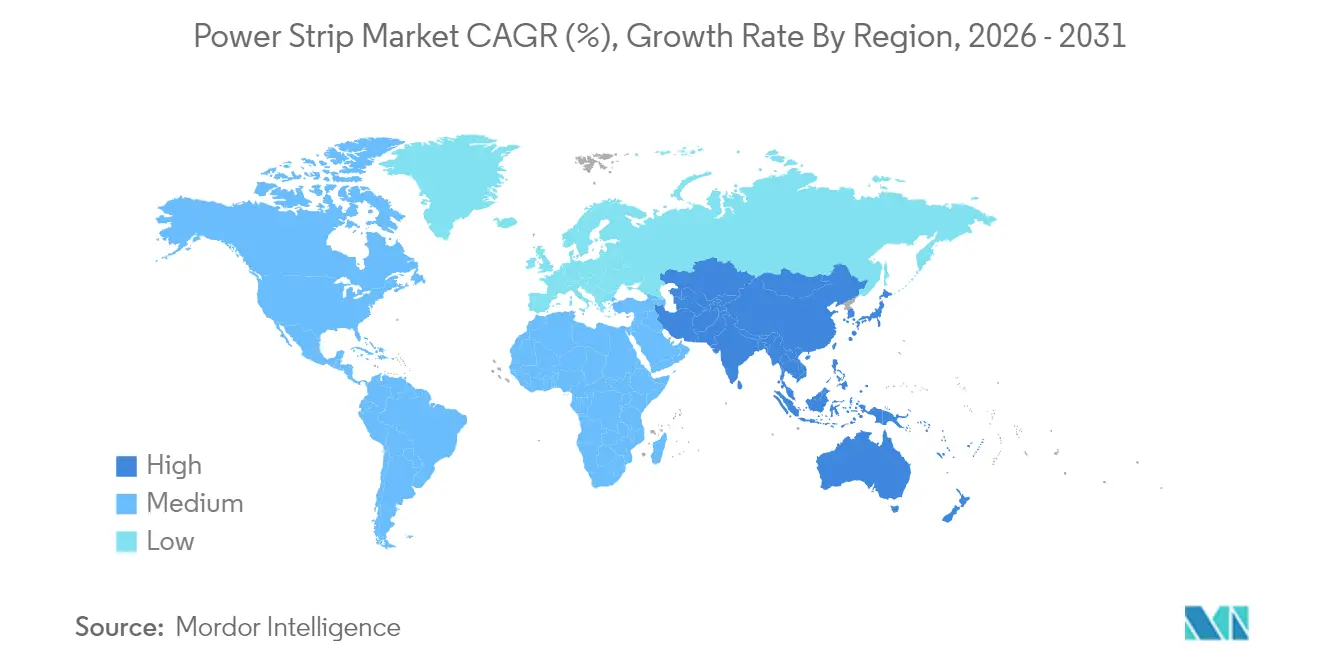

- By geography, Asia-Pacific commanded 45.05% revenue in 2025 and is on track for a 7.55% CAGR, driven by data-center buildouts and smart-city deployments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Strip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of electronic devices in households | +1.2% | Global – North America and APAC hot spots | Medium term (2-4 years) |

| Demand for energy-efficient smart-home power management | +1.0% | North America and EU lead, APAC follows | Medium term (2-4 years) |

| Data-center and IT-infrastructure expansion | +1.8% | Global – APAC and North America pivotal | Short term (≤ 2 years) |

| Surge in remote working worldwide | +0.9% | Global – higher in developed economies | Short term (≤ 2 years) |

| Utility rebates and building-code mandates for APS | +0.7% | North America and EU | Long term (≥ 4 years) |

| Industrial-IoT-driven networked PDU adoption | +0.8% | Core in APAC, expanding to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Electronic Devices in Households

Average connected-device counts per home have surpassed 25 in the United States, stretching traditional outlet configurations and intensifying demand for multi-socket solutions with integrated surge protection. New York State research shows that intelligent advanced power strips can save 106.1 kWh and USD 78.81 per household each year by curbing standby losses[1]New York State Energy Research and Development Authority, “Standby Power Reduction with Tier 2 Advanced Power Strips,” nyserda.ny.gov. WiFi-enabled strips giving residents real-time visibility into consumption patterns are therefore gaining traction, especially in markets where energy codes actively discourage phantom load draw. Manufacturers are responding with slimmer form factors and voice-assistant compatibility to align with prevailing smart-home ecosystems.

Demand for Energy-Efficient Smart-Home Power Management

Utility rebate programs and revised building codes are converting smart strips from optional upgrades into baseline fixtures. California’s Emerging Technology Program validated marketing blueprints that drove widespread adoption of auto-switching models through retailer education and incentive alignment. Europe follows a similar arc, with Commission rules capping networked equipment standby to 0.5 watts and accelerating uptake of strips capable of full circuit isolation. As firmware now incorporates machine-learning algorithms that forecast load cycles, vendors seize recurring-revenue opportunities around cloud dashboards and remote firmware updates.

Data-Center and IT-Infrastructure Expansion

Artificial-intelligence clusters are boosting rack densities above 20 kW, requiring metered PDUs that combine thermal sensing, phase balancing, and secure remote outlets. Global data-center power demand is set to rise 50% by 2027, turning power strip market growth into a strategic imperative for suppliers aligned with hyperscale clients. Schneider Electric’s USD 700 million capacity build-out in the United States earmarks significant spend on next-generation PDU labs calibrated for AI power trains. Concurrently, edge-computing proliferation is fueling orders for compact PDUs suitable for space-constrained micro-sites.

Surge in Remote Working Worldwide

Hybrid work models are redistributing daytime electricity loads to residential circuits. Households now require professional-grade distribution capable of feeding dual monitors, VoIP phones, and broadband routers while safeguarding against grid disturbances. Smart strips integrating small-format UPS modules or lithium backup packs are selling briskly, spurred by the perceived cost of downtime in freelance and consultancy roles. Employers embracing at-home stipend programs often specify devices certified to UL 1449 and cybersecurity frameworks such as IEC 62443 to mitigate liability exposures.

Utility Rebates and Building-Code Mandates for APS

North American rebate schedules reimburse up to 100% of incremental costs for Tier 2 advanced power strips, hastening market conversion. New Jersey’s Technical Reference Manual codifies standardized kWh-savings algorithms, simplifying ROI calculations for facility managers[2]New Jersey Board of Public Utilities, “2023 Triennial Technical Reference Manual,” nj.gov. In parallel, European directives incentivize smart-meter integration, leading builders to pre-install energy-monitoring strips in new-construction flats.

Industrial-IoT-Driven Networked PDU Adoption

Smart factories outfitted with sensor networks require deterministic power sequencing during maintenance cycles. Ethernet-enabled PDUs supporting SNMP and Modbus protocols are becoming the default choices in automotive and semiconductor plants. Asian manufacturers in Japan, South Korea, and China spearhead deployments, encouraged by government grants that prioritize Industry 4.0 retrofits to lift productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent safety-certification compliance costs | -0.8% | Global – higher burden in developed markets | Long term (≥ 4 years) |

| Counterfeit low-cost products pressure pricing | -0.6% | APAC epicenter, global distribution spill-over | Medium term (2-4 years) |

| PoE adoption reducing outlet demand | -0.4% | North America and EU early movers | Long term (≥ 4 years) |

| E-waste directives raising producer responsibility | -0.5% | EU leadership, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety-Certification Compliance Costs

Manufacturers must navigate UL 1363, UL 1449, and sector-specific rules such as UL 60601-1 for healthcare, each requiring exhaustive destructive testing that can exceed USD 250,000 per variant. Emerging cybersecurity add-ons further mandate penetration tests and secure-boot validations, stretching project cycles and engineering budgets. Smaller vendors consequently face longer payback horizons and often retreat to niche or price-led positions, allowing multinationals with compliance teams to widen competitive moats.

Counterfeit Low-Cost Products Pressure Pricing

Illicit channels funnel uncertified strips into online marketplaces where price-first buying behavior dominates. Counterfeits lack flame-retardant casings or thermal fuses, posing fire hazards that erode public trust and force legitimate brands to invest heavily in awareness campaigns. Semiconductor Industry Association reports frequent reclamation of salvaged sockets from e-waste streams, raising shock and short-circuit risks[3]Semiconductor Industry Association, “Counterfeit Electronics Supply Chain Risk Overview,” semiconductors.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: FPDUs Lead While Smart Strips Accelerate

FPDUs commanded 30.86% of 2025 revenue on the back of open-plan office refurbishments specifying under-desk trunking and soft-wiring. The power strip market size for FPDU deployments is projected to expand at 6.62% annually as mobility-first furniture gains momentum. Smart WiFi/Bluetooth strips, while only 14.72% of current volumes, post a 7.45% CAGR as households digitize lighting, security, and entertainment clusters. Relocatable Power Taps retain relevance in events and construction, but their share is trending down amid stricter site-safety enforcement. Rack-mount products in data halls are pivoting toward high-density form factors with hydraulic-magnetic breakers and color-coded phase identifiers to streamline installation. Manufacturers increasingly bundle in-line energy and environmental sensors, setting the stage for Software-as-a-Service add-ons focused on predictive maintenance.

Second-generation flat-head designs answer millwork constraints in hospitality and education builds, while wall-flush variants simplify compliance with aesthetics-oriented building codes. International furniture giants now embed USB-C PD outlets in workstations, embedding power management at the design phase and supplying incremental lift to the power strip market.

By Protection Feature: Surge Protection Dominates, Energy Monitoring Emerges

Surge-protected models held 37.05% revenue in 2025 because transient over-voltage mitigation remains a non-negotiable specification across geographies. The power strip market size linked to energy-monitoring SKUs will, however, outpace at 7.78% CAGR through 2031 as utilities tighten demand-response frameworks. Premium models integrate metering ICs accurate to ±1% and expose cloud APIs, enabling building-management systems to fine-tune loads. Overload protection remains table stakes, yet differentiation now revolves around algorithmic breaker reset that distinguishes inrush from genuine faults. IP-rated waterproof series secure share in agriculture, construction, and food-processing, while fire-retardant casings compliant with UL 94 V-0 escalate usage in hospitals.

By Application: General Purpose Leads, Smart Applications Accelerate

General-purpose variants serve legacy sockets in residences, malls, and light industry, capturing 50.42% share in 2025. That slice will erode as smart categories extend connectivity into all tiers. The power strip market share for smart applications is forecast to climb alongside building digitization targets and IoT adoption in hospitality and education. Special-protection units, once confined to labs, are crossing into mission-critical public-safety infrastructure owing to growing cybersecurity scrutiny. Meanwhile, heavy-duty industrial lines bank on 600 V ratings and gasketed enclosures to tackle oil-and-gas and mining electrification.

By End-User: Commercial Offices Lead, Residential Growth Accelerates

Open offices and retail chains remained the power strip market’s largest buyers with a 27.62% share in 2025, deploying desk-grommet units and floor boxes to feed laptops and display panels. The residential rush, fueled by work-from-home norms, clocks 7.46% CAGR as consumers future-proof living spaces with USB-C PD and GaN chargers. Data-center operators demand metered PDUs with secure firmware updates, pushing vendors to certify ISO/IEC 27001 processes. Manufacturers are now counting on industrial clients now engineer rugged IP54 and IP65 lines to survive wash-downs and solvents. Health-care procurement, regulated by CMS, continues to require hospital-grade receptacles with locking plugs, ensuring a recurring replacement cycle.

By Distribution Channel: Offline Dominates, Online Accelerates

Electrical wholesalers and big-box DIY stores collectively moved 66.85% of 2025 unit volume, a testament to contractor reliance on immediate availability and local inventory. The power strip market size flowing through e-commerce will expand fastest at 8.35% CAGR as product standardization reduces consultative selling needs. Manufacturers are piloting direct-to-consumer portals offering serialized authenticity checks to combat gray-market leakage. Some are layering subscription-based warranty extensions to sustain lifetime revenue.

Geography Analysis

Asia-Pacific retained 45.05% of worldwide revenue in 2025, underpinned by new server farms in Singapore, Malaysia, and India. The region’s power strip market size is pegged for a 7.55% CAGR through 2031 as state energy-efficiency mandates and smart-city budgets gain steam. In China, Tier-2 urban centers are accelerating apartment retrofits with embedded wall outlets hosting Ethernet-based power strips. India’s production-linked incentive schemes for electronics amplify domestic demand and favor certified local manufacturing under BIS guidelines. Southeast Asian governments, meanwhile, bundle surge-protected strips into school modernization grants, alleviating import duties for compliant products.

North America remains a sizeable but maturing territory. Data-center expansions across Virginia’s “Data Alley” and Arizona’s solar-powered campuses buoy demand for intelligent rack PDUs. Smart-home penetration rates surpass 60% in Canada’s major provinces, lifting residential upgrade cycles. Utility rebate programs for Tier 2 advanced power strips underpin sustained household uptake.

Europe’s prospects hinge on eco-design directives and electrification of heating loads; German and French building codes now earmark receptacle counts per square meter, indirectly driving aftermarket installations. South America and MEA represent opportunistic plays tied to infrastructure rollouts and tourism growth, though currency volatility often skews project timelines.

Competitive Landscape

The power strip market hosts a mid-tier oligopoly where the top five brands collectively account for roughly 55% of global sales, yielding healthy yet contestable margins. Multinationals such as Eaton, Schneider Electric, and Legrand leverage entrenched distributor relationships and multi-vertical product suites to defend share. Their in-house testing labs streamline UL and IEC certifications, compressing time-to-market for AI-ready PDUs. Schneider Electric’s USD 700 million U.S. footprint expansion exemplifies the capital depth required to sustain latency-sensitive supply chains while integrating cybersecurity hardening into firmware[4]Schneider Electric, “Schneider Electric Expands U.S. Manufacturing Footprint,” se.com. Eaton deploys mass-configuration tooling so colocation operators can commission hundreds of racks within days.

Emerging challengers center offerings on software-defined load orchestration and predictive analytics. Many pursue direct-to-consumer webstores to bypass wholesale mark-ups, bundling mobile apps and cloud dashboards under freemium models. Patent filings show start-ups experimenting with silicon carbide (SiC) surge modules that slash clamping response times. Meanwhile, specialist vendors of healthcare-grade strips forge alliances with nurse-call platform providers to embed preventative alerting within patient rooms.

MandA activity is expected to intensify as incumbents close feature gaps and broaden geographic reach. Private-equity-backed roll-ups target niche Asian suppliers adept at low-cost manufacturing yet lacking certification muscle to penetrate Western markets. Vendors face rising stakes in counterfeit mitigation; serialization, blockchain traceability, and tamper-evident packaging are being piloted to protect brand equity. Pricing discipline is upheld by the cost and complexity of UL listings, conferring a defensive hurdle against commoditization even as raw-material prices fluctuate.

Power Strip Industry Leaders

Belkin International, Inc.

Leviton Manufacturing Co., Inc.

Panasonic Corporation

Legrand SA

Hubbell Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Legrand reported 3.9% 2024 topline rise with data-center activities now 20% of revenue and set a 6%-10% 2025 growth goal supported by digital building innovation.

- April 2025: Sonepar divested Vallen Asia to focus on core electrical distribution, maintaining EUR 33.3 billion 2023 sales across 40 countries.

- March 2025: Schneider Electric committed USD 700 million to U.S. supply-chain and laboratory expansion to test AI-focused data-center PDUs, adding 1,000 jobs across six states.

- February 2025: Vertiv unveiled Q1 2025 net sales of USD 2.036 billion, a 24% jump propelled by hyperscale infrastructure roll-outs.

- January 2025: Eaton cited data-center spending and electrification standards as catalysts for double-digit sales growth in its electrical segment.

Global Power Strip Market Report Scope

A power strip is a block of electrical sockets that provides additional cord length and mobility to otherwise immovable wall sockets that are generally placed in obscure and hard-to-reach places. Power Strips are made and installed as Furniture Power Distribution Units (FPDUs), Multioutlet Assemblies, and Relocatable Power Taps (RPTs). Power strips are used in Residential, Commercial, and Industrial applications.

| Furniture Power Distribution Units (FPDUs) |

| Multioutlet Assemblies |

| Relocatable Power Taps (RPTs) |

| Rack-mount Power Distribution Strips |

| Flat-head / Low-profile Power Strips |

| Embedded / In-wall Power Strips |

| Smart WiFi / Bluetooth Power Strips |

| Surge Protection |

| Overload Protection |

| Waterproof / Dust-proof (IP Rated) |

| Fire-resistant Casing |

| Energy Monitoring and Metering |

| Common / General Purpose |

| Special Protection |

| Smart Power Strips |

| Heavy-duty Industrial |

| Industrial Manufacturing Facilities |

| Data Centers and IT Rooms |

| Commercial Offices and Retail |

| Healthcare Facilities |

| Hospitality and Leisure |

| Education and Public Institutions |

| Residential |

| Offline (Electrical Wholesalers and Retail) |

| Online (E-commerce Platforms) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Installation Type | Furniture Power Distribution Units (FPDUs) | ||

| Multioutlet Assemblies | |||

| Relocatable Power Taps (RPTs) | |||

| Rack-mount Power Distribution Strips | |||

| Flat-head / Low-profile Power Strips | |||

| Embedded / In-wall Power Strips | |||

| Smart WiFi / Bluetooth Power Strips | |||

| By Protection Feature | Surge Protection | ||

| Overload Protection | |||

| Waterproof / Dust-proof (IP Rated) | |||

| Fire-resistant Casing | |||

| Energy Monitoring and Metering | |||

| By Application | Common / General Purpose | ||

| Special Protection | |||

| Smart Power Strips | |||

| Heavy-duty Industrial | |||

| By End-User | Industrial Manufacturing Facilities | ||

| Data Centers and IT Rooms | |||

| Commercial Offices and Retail | |||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Education and Public Institutions | |||

| Residential | |||

| By Distribution Channel | Offline (Electrical Wholesalers and Retail) | ||

| Online (E-commerce Platforms) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the global power strip market?

The market stands at USD 14.99 billion in 2026 and is forecast to reach USD 21.02 billion by 2031.

What compound annual growth rate (CAGR) is projected for the power strip market?

The market is projected to advance at a 6.98% CAGR between 2026 and 2031.

Which region holds the largest share of the power strip market?

Asia-Pacific leads with 45.05% revenue share in 2025 and continues to post the fastest growth.

Which installation type currently dominates global demand?

Furniture Power Distribution Units (FPDUs) lead with 30.86% market share in 2025.

Which power-strip feature is expanding fastest?

Energy-monitoring and metering capabilities are expanding at an 7.78% CAGR between 2026 and 2031, reflecting rising demand for consumption visibility.

Why are smart power strips gaining rapid traction in homes?

Smart strips curb standby losses, integrate with WiFi networks, and qualify for utility rebates, making them attractive for energy-conscious households.

Page last updated on: