Canada Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

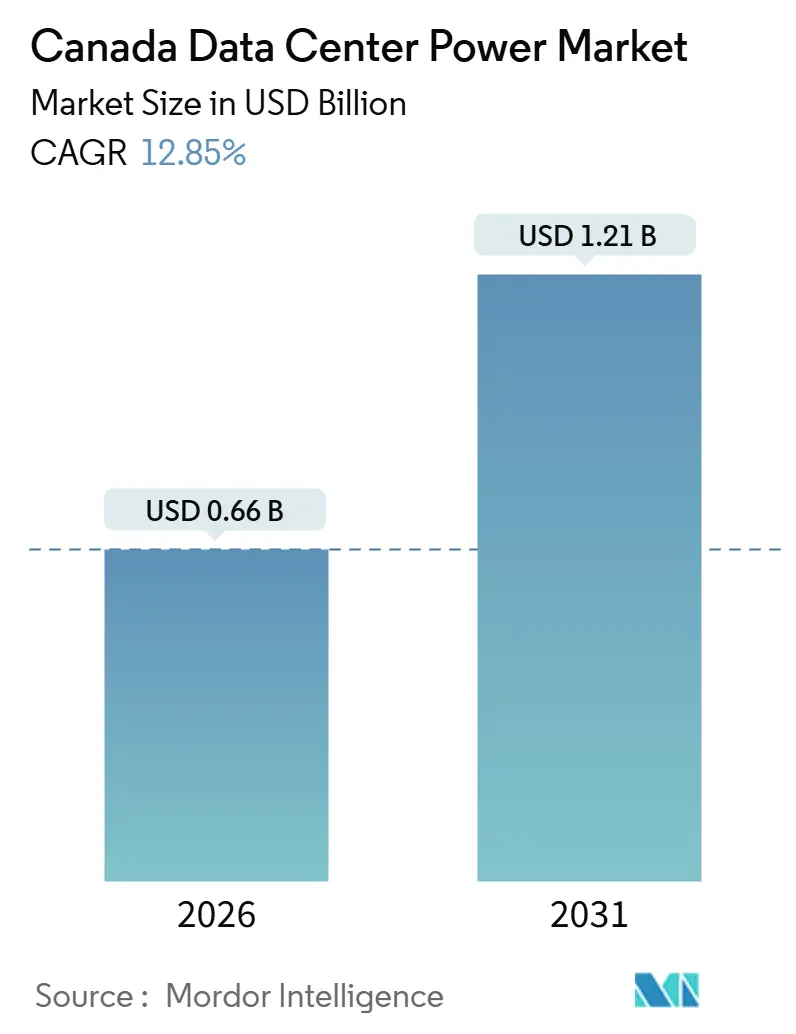

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 12.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Power Market Analysis by Mordor Intelligence

The Canada data center power market size is estimated at USD 0.66 billion in 2026, and is expected to reach USD 1.21 billion by 2031, at a CAGR of 12.85% during the forecast period (2026-2031). Surging artificial-intelligence workloads are lifting rack power densities to 150-300 kilowatts, well above legacy enterprise levels, and driving unprecedented investment in redundant electrical architectures. Federal incentives totaling CAD 4.4 billion (USD 3.17 billion) are steering new capacity toward provinces with low-carbon generation, while hyperscalers are announcing multibillion-dollar campus pipelines that accelerate demand for uninterruptible power supply systems, generators, and grid-interactive battery storage. At the same time, provincial grid congestion is constraining interconnection queues, prompting developers to adopt behind-the-meter microgrids that combine natural-gas turbines, battery energy storage, and renewable assets. Incumbent equipment vendors are responding with silicon-carbide inverter platforms that reach 98% efficiency, and hydrogen fuel-cell entrants are positioning zero-emission backup solutions to avoid tightening diesel restrictions.

Key Report Takeaways

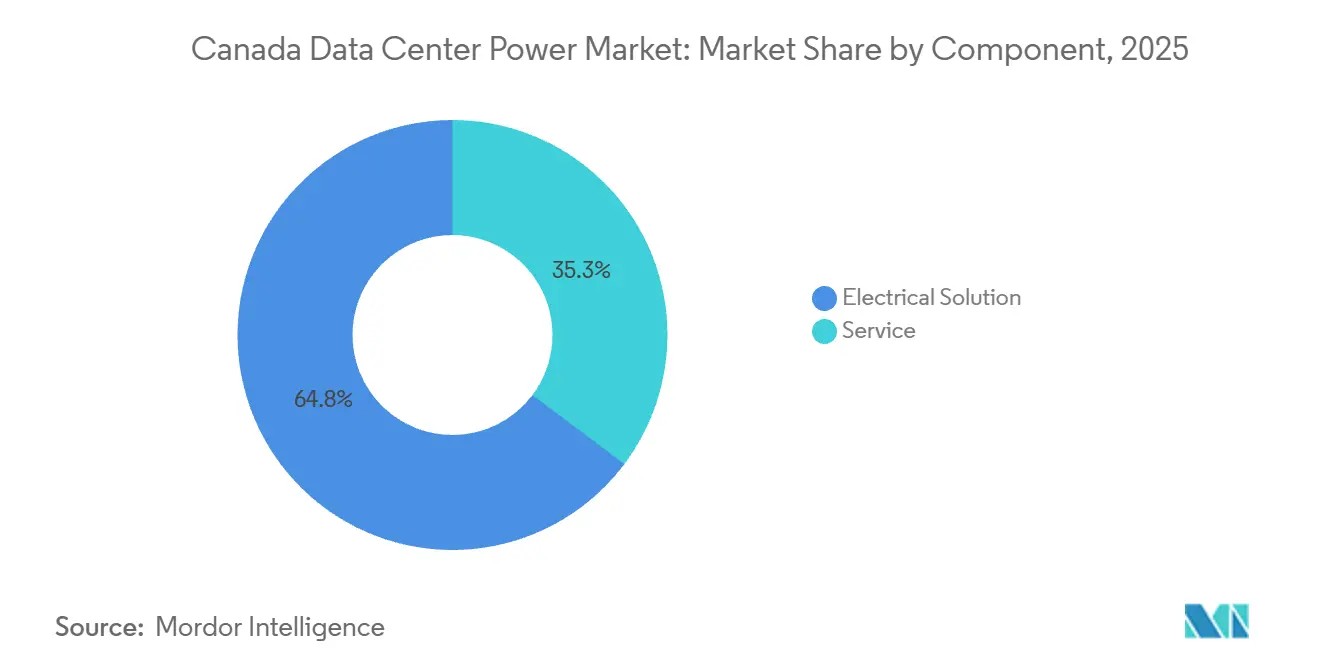

- By component, electrical solutions led with 64.75% revenue share in 2025, while service contracts are forecast to expand at a 13.43% CAGR to 2031.

- By tier, Tier 3 facilities held 63.42% share in 2025; Tier 4 deployments are advancing at a 13.65% CAGR through 2031.

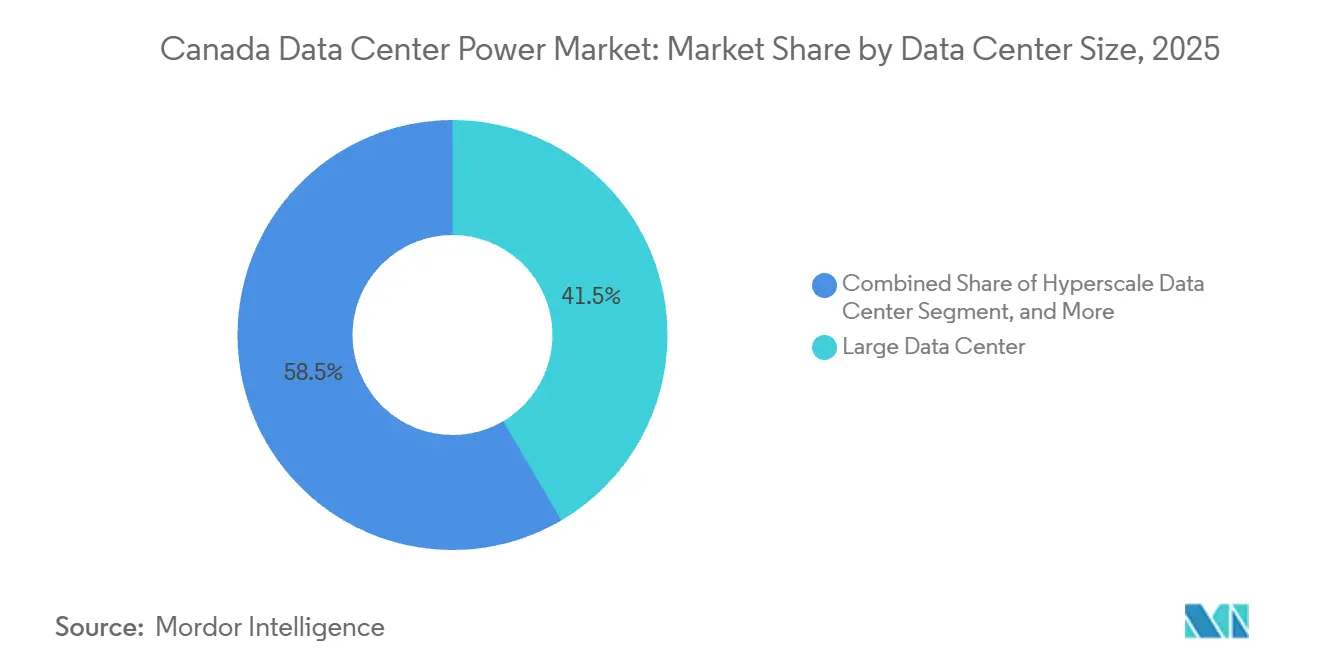

- By data center size, large data centers captured 41.54% share of the Canada data center power market size in 2025, and hyperscale campuses are projected to expand at a 13.87% CAGR between 2026-2031.

- By data center type, colocation operators held 44.65% share in 2025, whereas the hyperscaler and cloud service provider segment is set to grow at a 13.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated AI / GPU workloads demanding high-density power | +3.5% | National, concentrated in Toronto, Montreal, Vancouver, Calgary | Short term (≤ 2 years) |

| Surging deployment of hyperscale and cloud campuses | +2.8% | Ontario, Quebec, Alberta | Medium term (2-4 years) |

| Preference for low-carbon hydro-nuclear power mix | +2.0% | Quebec, Ontario, British Columbia | Long term (≥ 4 years) |

| Data-center energy-efficiency mandates by provincial utilities | +1.5% | Ontario, British Columbia, Alberta | Medium term (2-4 years) |

| Growing interest in on-site small modular reactors (SMRs) | +1.2% | Ontario, Saskatchewan, Alberta | Long term (≥ 4 years) |

| Expansion of behind-the-meter renewables plus battery solutions | +1.0% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated AI And GPU Workloads Demanding High-Density Power

Massive training clusters are pushing rack densities beyond 150 kilowatts, and operators are over-provisioning electrical capacity by up to 50% to stay ahead of successive GPU refresh cycles. eStruxture deployed AI-ready cabinets at VAN-3 in Vancouver, while federal programs earmarking CAD 2 billion for sovereign compute are channeling workloads toward domestic campuses. IREN’s 10-megawatt hydro-powered facility in British Columbia illustrates how low-carbon baseload helps operators sidestep carbon-offset costs. Ontario’s system operator forecasts data-center load rising to 13% of new provincial demand by 2035.[1]Independent Electricity System Operator, “Market and System Reporting,” ieso.ca The resulting spike in capex per megawatt is stimulating demand for high-efficiency UPS platforms and grid-interactive battery storage that can monetize reserve capacity.

Surging Deployment Of Hyperscale And Cloud Campuses

Microsoft has committed USD 7.5 billion to expand Azure Local and build a threat-intelligence hub, while Vantage is investing CAD 500 million (USD 361 million) to bring its Quebec City campus to 86 megawatts. eStruxture secured USD 1.35 billion in financing to roll out a 90-megawatt Calgary build and densify Toronto and Montreal footprints.[2]eStruxture, “Data Center Solutions,” estruxture.com Grid operators face a surge of interconnection requests, Alberta alone logged 16 gigawatts for data centers, forcing developers to consider microgrids that pair natural-gas turbines with battery storage. Hyperscale momentum is therefore magnifying equipment demand across generators, switchgear, and power distribution units within the Canada data center power market.

Preference For Low-Carbon Hydro-Nuclear Power Mix

Hydro-Québec delivers nearly 100% renewable energy at industrial Rate L tariffs of CAD 14.476 per kilowatt, allowing operators to hit carbon-neutral targets without offsets. Ontario blends hydro and nuclear, and its small modular reactor roadmap underscores long-term baseload expansion. British Columbia Hydro dedicated a 100-megawatt block exclusively to data-center customers, prioritizing energy-efficient proposals. This clean-power advantage is a decisive siting factor for hyperscalers, anchoring long-term commitments that reinforce the growth trajectory of the Canada data center power market.

Data-Center Energy-Efficiency Mandates By Provincial Utilities

Utilities now embed curtailment clauses and demand-response incentives in power contracts. Hydro-Québec pays large customers thousands of Canadian dollars per curtailed kilowatt, enabling data centers to shift batch jobs to off-peak hours. Ontario procured 2,916 megawatts of storage across 26 facilities in 2025, with costs falling 24% year on year. Programs in British Columbia reimburse up to 75% of solar-plus-storage capex, accelerating adoption of distributed resources. Equipment vendors such as Eaton are rolling out grid-interactive UPS platforms that can inject stored power during peak periods, turning backup assets into revenue generators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in Toronto-Montreal corridor | -1.8% | Ontario, Quebec | Short term (≤ 2 years) |

| Lengthy transmission-interconnection approval timelines | -1.5% | Alberta, Ontario, British Columbia | Medium term (2-4 years) |

| High up-front capex for redundant power infrastructure | -1.2% | National | Medium term (2-4 years) |

| Scarcity of skilled electrical engineers and technicians | -0.8% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion In Toronto-Montreal Corridor

The Toronto Integrated Regional Resource Plan shows Northern York Region limited to 16 megawatts of firm capacity against 750 megawatts of projected demand, with relief not expected before 2034. Hydro-Québec suspended new large-load connections in 2024, stalling all Montreal greenfield projects despite abundant hydro capacity. Developers are pivoting to behind-the-meter gas generation, Caterpillar installed 15.5 megawatts for Linamar under a 15-year power purchase agreement, to bypass constrained substations. These bottlenecks elevate project risk and temper near-term growth in the Canada data center power market.

Lengthy Transmission-Interconnection Approval Timelines

Ontario’s leave-to-construct process can stretch 12-plus months, and developers may be required to fund multi-million-dollar upgrades upfront. Alberta capped firm connections at 1,200 megawatts through 2028, obliging applicants to post CAD 14 million (USD 10.1 million) in security per 100 megawatts. Bulk stations like Kleinburg can top CAD 400 million (USD 292 million) and need four to five years from planning to energization. These delays erode return profiles and deter speculative capital, constraining expansion of the Canada data center power industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Service Contracts Capture Uptime Premiums

Electrical solutions accounted for 64.75% of 2025 revenue, underscoring their foundational role in delivering redundant architectures in the Canada data center power market. Generators, UPS systems, power distribution units, and switchgear accounted for the bulk of this spend, and vendors are integrating silicon-carbide semiconductors that boost efficiency to 98%. Generac’s 3.25-megawatt diesel line and Cummins’ Tier III-compliant Centum models underscore an active replacement cycle that favors higher-efficiency platforms.

Service contracts, growing at 13.43% annually, cover commissioning, predictive maintenance, and grid-interactive optimization as operators chase 99.995% uptime. Eaton’s EnergyAware UPS enables frequency-regulation participation, while Ballard and Vertiv’s hydrogen module eliminates diesel runtime limits. As utilities reward flexible loads, service providers that can tune assets for curtailment revenue will outpace hardware-only rivals, reinforcing the upward momentum within the Canada data center power market.

By Tier Type: Fault Tolerance Commands Premium

Tier 3 accounted for 63.42% of 2025 investment, reflecting colocation providers’ desire for concurrently maintainable designs without the cost burden of dual utility feeds. eStruxture’s Tier III TOR-5 facility exemplifies this balance with N+1 UPS strings and redundant generators.

Tier 4, expanding at a 13.65% CAGR, appeals to hyperscalers running mission-critical AI training that cannot risk single-path failures. Natural Resources Canada’s best-practice guide pegs 2N architectures as 40-60% more capital-intensive, yet hyperscalers absorb the premium to sidestep outage costs that can exceed USD 100,000 per minute. Consequently, the Canada data center power market size for Tier 4 solutions is forecast to rise sharply through 2031.

By Data Center Size: Hyperscale Drives Megawatt Appetite

Large facilities captured 41.54% of 2025 spend, but hyperscale campuses above 10 megawatts are on track for a 13.87% growth rate as Microsoft, Vantage, and eStruxture line up expansions. Vantage’s QC24 building will add 32 megawatts to an 86-megawatt campus powered by hydro, reinforcing demand for high-capacity switchgear and generators.

Alberta’s interim interconnection framework favors projects above 75 megawatts, nudging developers toward on-site gas turbines and battery storage that can scale rapidly. Modular UPS architectures, such as Eaton’s 9395XC rated at 2.25 megawatts, allow staged build-outs that match tenant ramp-up. Together, these trends maintain a strong tailwind for the hyperscale slice of the Canada data center power market.

By Data Center Type: Hyperscalers Outpace Colocation

Colocation still dominated 44.65% of 2025 revenue, anchored by dense interconnection hubs like Cologix’s Toronto portfolio linking 350 networks and 15 cloud on-ramps. Enterprise tenants value flexible power provisioning and carrier-neutral ecosystems that colocation offers.

Yet the hyperscaler and cloud segment is growing at 13.78% through 2031 as Azure Local, AWS Outposts, and Google Distributed Cloud land in sovereign zones. Build-to-suit deals, such as eStruxture’s 90-megawatt Calgary campus for anchor tenants, are blurring lines between colocation and dedicated capacity. Edge operators, meanwhile, are deploying prefabricated modules with integrated power to compress timelines, further diversifying the opportunity landscape across the Canada data center power market.

Geography Analysis

Ontario anchors the national market with more than 80 facilities and a hydro-nuclear generation mix that minimizes Scope 2 emissions. The system operator projects data centers will add 13 terawatt-hours of annual demand by 2035 and 137 megawatts by 2026. Transmission limits in Greater Toronto compel developers to adopt behind-the-meter solutions, such as the 15.5-megawatt Caterpillar installation for Linamar that shaves peak demand while ensuring backup capacity.

Quebec ranks second, hosting 54 Montreal sites and eight in Quebec City that leverage nearly 100% hydro power at industrial Rate L tariffs. Hydro-Québec’s procurement pause in 2024 stalled new builds, yet Vantage’s CAD 500 million campus expansion to 86 megawatts illustrates continued investor confidence once capacity is released. Demand-response credits worth tens of thousands of Canadian dollars per curtailed kilowatt create additional revenue streams for flexible operators.

Alberta and British Columbia form the high-growth frontier. Alberta logged 16 gigawatts of pending data-center requests against a 1.2-gigawatt interim cap, propelling interest in microgrids and gas-fired generation. British Columbia Hydro set aside a 100-megawatt block for data-center customers and supports solar-plus-storage rebates that cover up to 75% of capex.[3] BC Hydro, “Competitive Power Supply and Remote Microgrid Rebates,” bchydro.com IREN’s 10-megawatt hydro-powered AI facility showcases the province’s low-carbon edge, while eStruxture’s Vancouver campus offers 150-kilowatt racks for AI inference, reinforcing regional momentum for the Canada data center power market.

Competitive Landscape

Global incumbents, ABB, Schneider Electric, Eaton, and Vertiv, command roughly 55% of revenue through integrated portfolios that span UPS systems, switchgear, and power distribution software. Schneider’s energy-management segment grew 17.3% organically in Q1 2025, and its acquisition of Motivair adds liquid cooling for 500-kilowatt racks. Eaton’s EnergyAware platform allows UPS fleets to earn frequency-regulation revenue, while Mitsubishi Electric’s 9900D series employs silicon-carbide electronics to cut losses by 1-2 percentage points.

Generator specialists are racing to comply with tightening emissions limits: Generac introduced a 3.25-megawatt diesel line, and Cummins’ Tier III-compatible Centum series addresses jurisdictions that cap runtime hours. Hydrogen innovators are disrupting backup paradigms; Ballard and Vertiv’s 400-kilowatt module demonstrated zero-emission reliability, and Caterpillar’s 1.5-megawatt fuel-cell pilot with Microsoft simulated 48 hours of uninterrupted power.

White space lies in microgrids that co-optimize solar, storage, and gas generation. Eaton and Siemens Energy are marketing hybrid packages scalable to 500 megawatts for hyperscale campuses awaiting transmission upgrades. With provincial utilities rewarding flexible loads, vendors that deliver grid-interactive features stand to gain share within the Canada data center power industry, even as hydrogen entrants chip away at diesel incumbency.

Canada Data Center Power Industry Leaders

ABB Ltd.

Cummins Inc.

Eaton Corporation

Vertiv Group Corp.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Boralex commissioned the 80 megawatt / 320 megawatt-hour Sanjgon battery storage system in British Columbia, providing grid services and backup power for adjacent data-center loads

- December 2025: Microsoft announced a USD 7.5 billion, two-year expansion of Canadian AI data-center capacity, including a sovereign threat-intelligence hub.

- November 2025: Potentia Renewables began building Skyview 2, a 411 megawatt / 1,858 megawatt-hour storage project in Ontario costing CAD 750 million (USD 542 million).

- October 2025: Cologix acquired full ownership of TOR4 and TOR5 in Toronto, adding 14 megawatts near the 151 Front Street interconnection hub

Canada Data Center Power Market Report Scope

Data center power refers to the power infrastructure, including electrical components and electrical distribution systems, that provide the power necessary to operate and support the devices and servers within the data center. It includes various components and technologies designed to ensure a reliable, uninterruptible power supply for data center IT equipment, including uninterruptible power supplies (UPS), power distribution units (PDU), backup generators, and other power management solutions tailored to data center-specific needs. Data center operators achieve redundancy by duplicating components to maintain uninterrupted operations in the event of component failure and to maintain uptime during maintenance.

The Canada Data Center Power Market Report is Segmented by Component (Electrical Solution, and Service), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small Data Center, Medium Data Center, Large Data Center, and Hyperscale Data Center), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge). The Market Forecasts are Provided in Terms of Value (USD).

| Electrical Solution | UPS Systems | |

| Generators | Diesel Generators | |

| Gas Generators | ||

| Hydrogen Fuel-cell Generators | ||

| Power Distribution Units | ||

| Switchgear | ||

| Transfer Switches | ||

| Remote Power Panels | ||

| Energy-storage Systems | ||

| Service | Installation and Commissioning | |

| Maintenance and Support | ||

| Training and Consulting | ||

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| By Component | Electrical Solution | UPS Systems | |

| Generators | Diesel Generators | ||

| Gas Generators | |||

| Hydrogen Fuel-cell Generators | |||

| Power Distribution Units | |||

| Switchgear | |||

| Transfer Switches | |||

| Remote Power Panels | |||

| Energy-storage Systems | |||

| Service | Installation and Commissioning | ||

| Maintenance and Support | |||

| Training and Consulting | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Size | Small Data Center | ||

| Medium Data Center | |||

| Large Data Center | |||

| Hyperscale Data Center | |||

| By Data Center Type | Colocation Data Center | ||

| Hyperscalers Data Center/CSPs | |||

| Enterprise and Edge Data Center | |||

Key Questions Answered in the Report

What is the forecast value of Canada’s data-center power spending by 2031?

Spending is projected to reach USD 1.21 billion by 2031, advancing at a 12.85% CAGR.

Why are hyperscale operators prioritizing Canada for new campuses?

The country’s abundant hydro and nuclear baseload lets hyperscalers meet carbon-neutral goals while tapping federal incentives worth CAD 4.4 billion (USD 3.17 billion).

How are grid constraints in Toronto affecting new builds?

Developers are adopting behind-the-meter microgrids and gas turbines to bypass transmission bottlenecks that could delay interconnections until 2034.

Which power-infrastructure technologies are gaining most traction?

High-efficiency silicon-carbide UPS systems and grid-interactive battery storage are seeing rapid uptake as operators monetize reserve capacity.

What role will hydrogen fuel cells play in Canadian data centers?

Pilot projects with Vertiv and Microsoft show hydrogen can replace diesel for zero-emission backup, a trend likely to accelerate as carbon costs rise.

How big is the service-contract opportunity?

Service contracts tied to commissioning, predictive maintenance, and energy optimization are growing 13.43% annually through 2031, outpacing hardware sales.

Page last updated on: