Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

New Zealand Data Center Power Market is Segmented by Component (Electrical Solutions, Services), by Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), by Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), by Tier Type (Tier I and II, Tier III, Tier IV). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

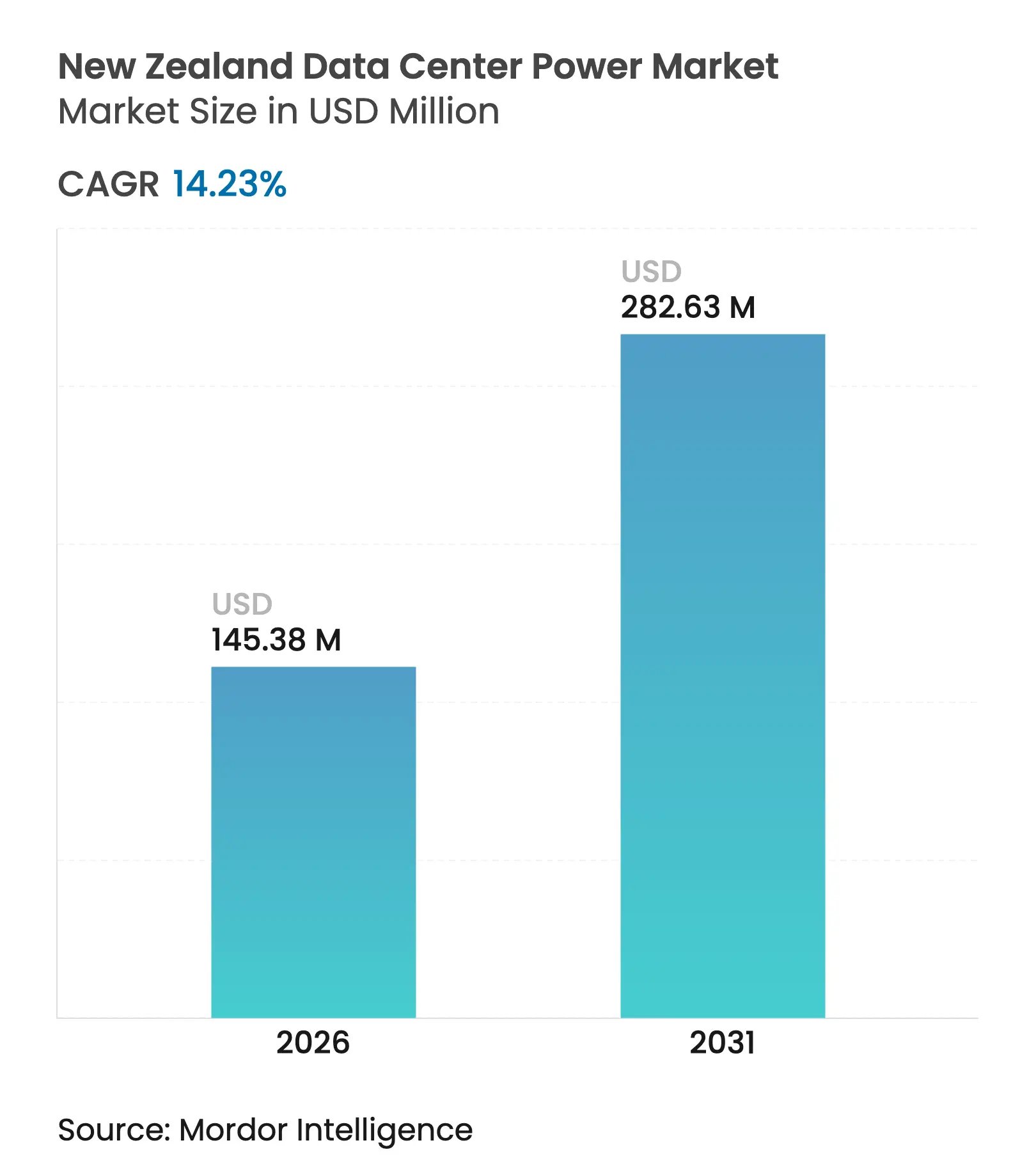

| Market Size (2026) | USD 145.38 Million |

| Market Size (2031) | USD 282.63 Million |

| Growth Rate (2026 - 2031) | 14.23 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The New Zealand data center power market size is expected to grow from USD 127.28 million in 2025 to USD 145.38 million in 2026 and is forecast to reach USD 282.63 million by 2031 at 14.23% CAGR over 2026-2031. Operators are prioritizing high-efficiency UPS architectures, intelligent PDUs, and on-site storage to trim operating costs and satisfy stringent sustainability targets. Hydrogen fuel-cell pilots and grid-interactive battery systems are also moving from proof-of-concept to early deployment as providers seek resilience in a nation prone to seismic risk. Geographic diversification beyond Auckland has begun, with South Island sites leveraging cooler air for free cooling and abundant hydro capacity to cut power usage effectiveness ratios. Competitive differentiation is shifting toward carbon metrics rather than only PUE, pushing vendors to integrate real-time carbon monitoring and renewable matching into power platforms.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Hyperscale and cloud adoption

Hyperscale and cloud adoption

| +4.2% | National; focused in Auckland | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+4.2%

|

Geographic Relevance

:

National; focused in Auckland

|

Impact Timeline

:

Medium term (2-4 years)

|

High-efficiency power architectures

High-efficiency power architectures

| +3.1% | National | Short term (≤ 2 years) | |||

Renewable-energy and carbon-neutral mandates

Renewable-energy and carbon-neutral mandates

| +2.8% | National | Long term (≥ 4 years) | |||

Submarine-cable expansion for edge services

Submarine-cable expansion for edge services

| +1.9% | Auckland and Wellington coastlines | Medium term (2-4 years) | |||

Off-peak renewable surplus incentives

Off-peak renewable surplus incentives

| +1.3% | South Island emphasis | Medium term (2-4 years) | |||

Cool marine climate for free-air cooling

Cool marine climate for free-air cooling

| +0.7% | South Island coasts | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising adoption of hyperscale and cloud data centers

AWS will bring a USD 4.24 billion region online in Auckland in 2025, and Microsoft’s first Azure region became operational in 2024, each requiring 20–40 MW per campus, twice the typical enterprise load. Auckland’s installed data-center power is therefore projected to double to almost 100 MW by 2027, forcing Transpower to accelerate grid reinforcement programs.[1]Transpower New Zealand Limited, “Transmission Planning Report 2023,” static.transpower.co.nz Hyperscale operators are piloting high-voltage direct-current distribution that offers 10-15% efficiency gains over AC, reflecting a broader pivot toward deep energy savings.

Growing need to cut OPEX via high-efficiency power architectures

Next-generation UPS platforms now exceed 99% efficiency, shaving several megawatt-hours of losses annually compared with legacy 94–96% units. ABB’s PCS100 medium-voltage UPS combines that efficiency with modularity up to 6 MVA, enabling operators to scale capacity as rack density.[2]ABB Ltd., “Complete Power Protection at Medium Voltage,” library.e.abb.com AI-driven power analytics embedded in Vertiv’s SmartAisle 3 allow predictive maintenance that can lower unscheduled downtime and reduce energy outlays.

Government renewable-energy and carbon-neutral mandates

Electricity generation is already 87% renewable and the policy pathway targets 96-98% by 2050. Data-center operators respond by contracting certified zero-carbon electricity, such as Microsoft’s supply agreement with Ecotricity for its three facilities. State-backed initiatives like the NZ Battery Project aim to buffer intermittent wind and hydro, reinforcing power quality for mission-critical loads.

Expansion of submarine cable connectivity enabling edge services

Seven cables in service and three more planned by 2027 are shortening latency to the United States, Australia, and the Pacific Islands. The forthcoming Hawaiki Nui route is prompting edge-node build-outs near landing stations, each demanding compact but highly reliable power blocks. Prefabricated, containerised UPS-battery assemblies are gaining ground because they can be installed in weeks rather than months.[3]

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex and maintenance costs

High capex and maintenance costs

| -2.1% | National | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

National

|

Impact Timeline

:

Short term (≤ 2 years)

|

Grid capacity limits and price volatility

Grid capacity limits and price volatility

| -1.8% | Auckland urban cluster | Medium term (2-4 years) | |||

Seismic design premiums

Seismic design premiums

| -1.2% | National; highest in Wellington | Long term (≥ 4 years) | |||

Limited local manufacturing lead-times

Limited local manufacturing lead-times

| -0.9% | National | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High installation and maintenance costs of advanced power systems

Tier IV electrical fit-outs are 25–30% more expensive than Tier III, challenging return-on-investment for smaller operators. The domestic talent pool for servicing MV UPS and STATCOMs is tight, so providers must import expertise or sign premium service contracts, adding to lifetime cost. Power-as-a-service models that shift capex to opex are under trial, yet commercial uptake remains nascent.

Grid capacity constraints and volatile electricity prices

Transpower models a significant climb in national consumption by 2050, with data centers singled out as a top growth driver. Growth concentration in Auckland forces new builds to co-fund substation upgrades, while reliance on coal-fired peakers during winter peaks adds both cost and emissions uncertainty.transpower.co.nz. Hybrid on-site generation coupled with battery storage is gaining traction, though economic viability hinges on facility scale and location.

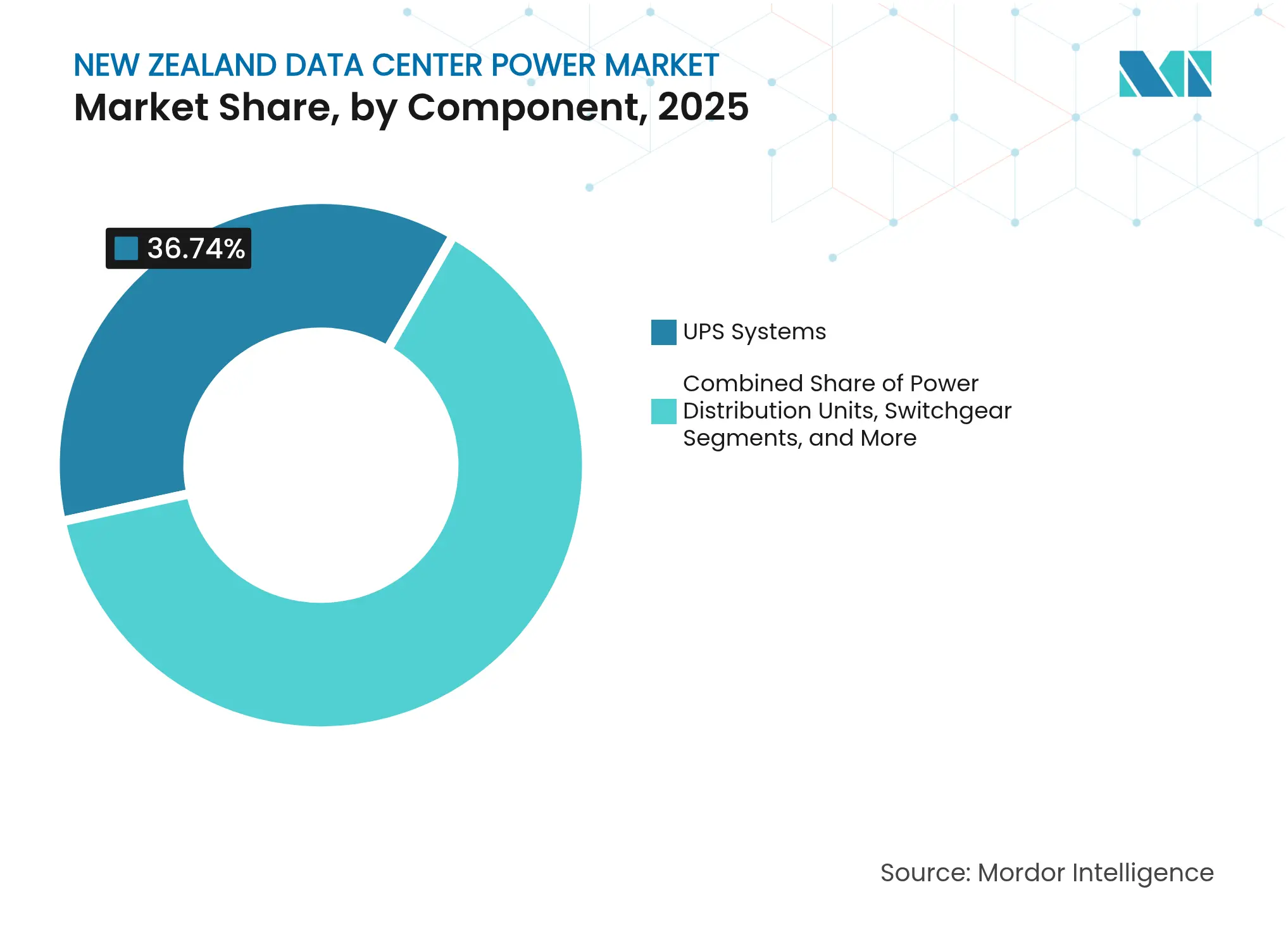

By Component: UPS leadership underpins critical power resilience

The New Zealand data center power market recorded UPS systems capturing 36.74% share in 2025, reflecting their central role in ride-through capability during grid disturbances. Modular designs enable N+1 or 2N topologies without over-provisioning, a priority in seismically active zones where runtime continuity is paramount. ABB’s 99%-efficient PCS100 is popular among mega-site operators because it slots into existing MV switchboards without derating, preserving floor space and reducing cooling loads. Operators pair these UPS blocks with lithium-ion strings that provide higher energy density and faster recharge than legacy VRLA, further enhancing availability.

PDUs are the fastest-growing component, rising at a 15.05% CAGR as intelligent models deliver granular per-outlet monitoring, automated branch-circuit alerts, and remote firmware updates. Such visibility helps operators tune loads in real time, driving lower PUE and meeting carbon reporting requirements. Switchgear, transfer switches, and remote power panels also see steady demand, while fuel-cell generators begin supplanting diesel in pilot deployments for carbon-free backup. Together, these dynamics keep the New Zealand data center power market on a technology-refresh cycle that favours efficiency and resilience upgrades every five to seven years.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Colocation capacity expands fastest

Colocation providers held 41.35% revenue share of the New Zealand data center power market in 2025 and are expanding at 15.9% CAGR, buoyed by enterprise outsourcing and by software-as-a-service firms seeking certified green power. CDC Data Centres’ plan to add 200 MW epitomises the scale of future builds and underscores how operators leverage renewable credentials to win multi-tenant contracts.

Hyperscalers follow close behind, driven by AWS and Microsoft expansions that prioritise fault-tolerant electrical designs and carbon-free backup. Enterprise and edge facilities remain smaller in aggregate capacity but are vital for compliance-sensitive workloads requiring data sovereignty and low latency. Edge deployments rely on prefabricated power pods that can be shipped to cable landing sites, offering <100 kW blocks with integrated lithium-ion storage. The diverse mix of facility types ensures that the New Zealand data center power market remains attractive across the value chain, from multi-megawatt switchgear suppliers to niche PDU innovators.

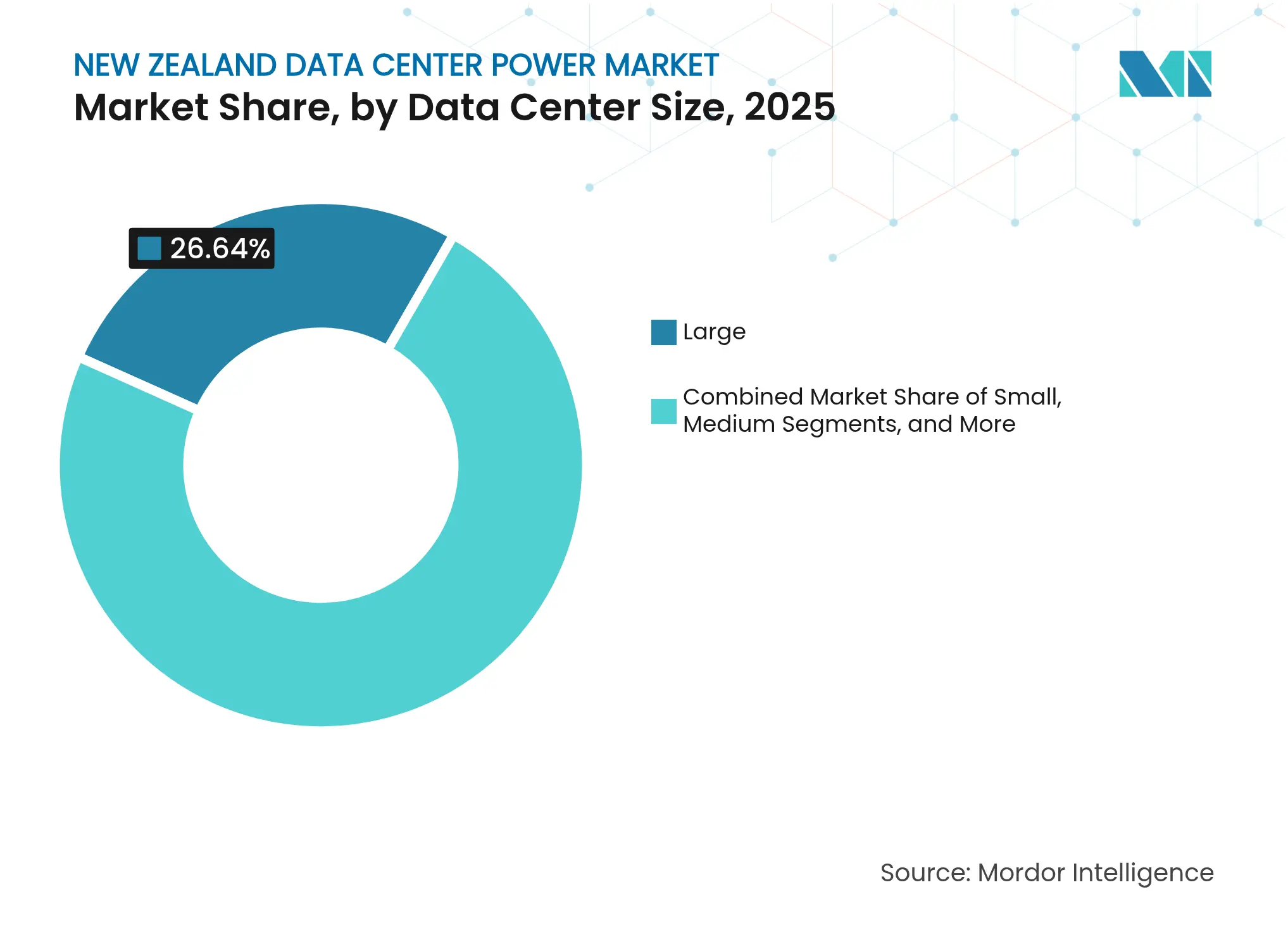

By Data Center Size: Large sites dominate, massive sites accelerate

Large data centers (5-10 MW) commanded a 26.64% share of the New Zealand data center power market size in 2025, striking a balance between scale economies and urban grid constraints. Many serve colocation tenants who demand expandable suites without incurring the risk of oversupply. Design templates typically feature ring-bus MV distribution and modular UPS strings to align capex with utilisation.

Massive sites (>20 MW) are the fastest-growing cohort at a 14.55% CAGR to 2031, driven by hyperscale cloud roadmaps. Their step-change in load density requires early engagement with Transpower to reinforce grid nodes and may include STATCOMs for voltage regulation, as implemented at the Ōtāhuhu substation in 2025. Medium and small facilities continue to serve niche requirements such as government, private cloud, and retail edge caching, ensuring a multi-tier demand structure that keeps the New Zealand data center power market diversified.

Note: Segment shares of all individual segments available upon report purchase

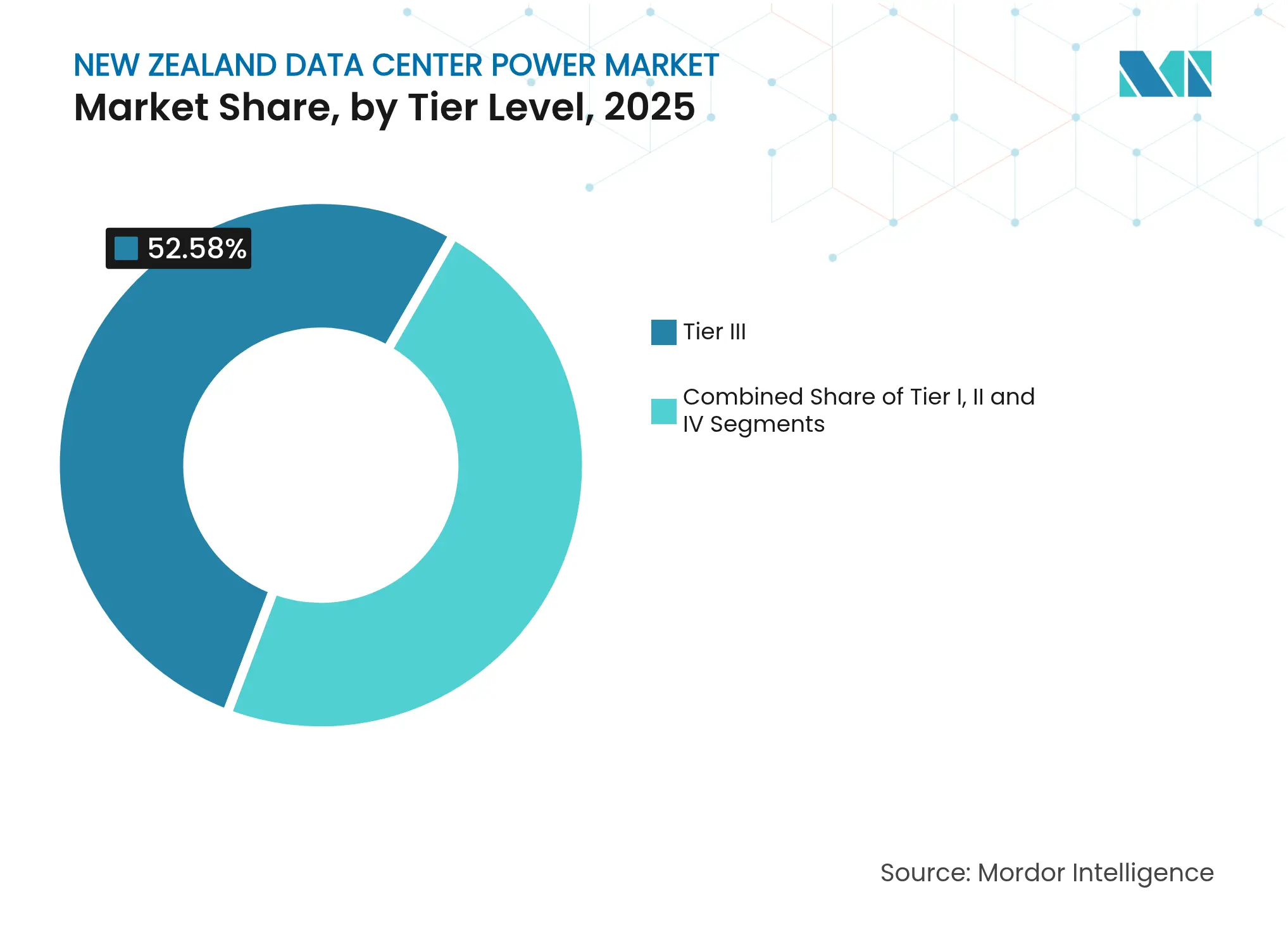

By Tier Level: Tier III remains mainstream while Tier IV gains ground

Tier III facilities held 52.58% of the New Zealand data center power market size in 2025, offering concurrent maintainability without the premium of full fault tolerance. Typical electrical topologies deploy N+1 UPS and multiple utility feeds, a configuration seen as sufficient for most financial services and SaaS clients.

Tier IV growth is strongest at 16.1% CAGR because hyperscalers and critical public-sector workloads require zero downtime. These designs layer 2N+1 UPS redundancy, segregated electrical rooms, and dual MV utility connections. Seismic bracing adds 15-20% to electrical installation costs, but operators accept the premium to guarantee uptime in quake-prone Wellington. Tier I and Tier II footprints continue shrinking as legacy enterprise rooms migrate into colocation footprints aligned with higher resilience expectations.

Note: Segment shares of all individual segments available upon report purchase

Auckland houses seven facilities totaling 49 MW, anchoring the New Zealand data center power market as the nation’s digital gateway. Vector’s ongoing underground-cable projects aim to reduce outage incidence, yet data-center load growth still outpaces distribution upgrades, prompting joint investment models where operators co-finance substations. Cooling relies increasingly on indirect evaporative systems that exploit the city’s temperate marine climate to limit compressor runtime.

Wellington represents an emerging cluster shaped by seismic realities. The Wellington Lifelines study quantifies NZD 3.9 billion in resilience capex that could avert NZD 6 billion in post-quake losses, underscoring the economic case for flexible cable trays, isolated switchgear skids, and quick-couple battery racks. Transpower lists the region as a priority for grid-hardening, with STATCOM installations planned to stabilise voltage amid rising electric-transport and data-center peaks.

South Island sites in Christchurch and Invercargill harness cooler ambient temperatures and proximity to hydro dams, enabling free-air cooling for 11-12 months per year. DLA Piper notes these factors could unlock a wave of sustainable builds once additional subsea cables land in 2026, effectively widening the New Zealand data center power market beyond its North Island stronghold. Transmission limitations remain a bottleneck, however, prompting discussions on dedicated high-voltage spurs to future hyperscale parks.

Market Concentration

Global OEMs dominate the New Zealand data center power market, yet tailor portfolios to local conditions. Schneider Electric combines lithium-ion UPS modules and EcoStruxure DCIM into integrated energy platforms that now embed machine-learning-based failure prediction, delivering 15-20% additional efficiency in pilot rollouts. Vertiv’s Liebert APM2 UPS offers hot-swappable power cores and 97.5% online efficiency, while SmartAisle 3 orchestrates dynamic load balancing for AI workloads. ABB leverages its PCS100 MV UPS for mega-sites where operators seek retrofit-friendly, high-efficiency modules.

Local systems integrators bridge international hardware with New Zealand’s seismic codes, providing flexible cable containment, shock-isolated switchboards, and commissioning services. Emerging niches include hydrogen fuel-cell generator projects led by Microsoft and Renewable Innovations, aiming for zero-carbon backup by 2030. Battery energy-storage vendors are positioning systems that couple UPS strings with peak-shaving algorithms to capture arbitrage from off-peak hydro surplus, aligning cost savings with carbon targets.

Competition is increasingly measured by carbon transparency rather than headline efficiency. Vendors now publish real-time CUE dashboards and interoperate with utility renewable-matching APIs. As green procurement policies tighten, supply-chain provenance and embodied-carbon disclosures have become bid differentiators, ensuring the New Zealand data center power market evolves toward holistic sustainability metrics.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the New Zealand data-center power market as all revenues that arise from the sale, installation, and support of electrical solutions, including uninterruptible power supplies, diesel and alternative-fuel generators, power-distribution units, switchgear, transfer switches, remote-power panels, energy-storage systems, and the professional services wrapped around them inside purpose-built, colocation, enterprise, edge, and hyperscale facilities. Mordor analysts measure value at factory gate and service-provider billing levels, expressed in USD and mapped to calendar years.

Cooling equipment, building shell costs, and IT hardware are excluded, so figures isolate the power stack only.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

To balance desk findings, we interviewed facility engineers at hyperscale builds in Auckland, procurement heads of colocation chains expanding in Wellington, and electrical-equipment distributors that serve edge pods across the South Island. Their insights on real-world load factors, PPA clauses, and UPS replacement cycles sharpened usage assumptions and pricing curves.

Desk Research

We began by mining open datasets that quantify grid supply and large-user demand, including Electricity Authority monthly generation statistics, Energy Efficiency and Conservation Authority load-management briefs, and Ministry of Business, Innovation and Employment energy balance tables, because they anchor national power availability and tariff trends. Trade associations such as the New Zealand Data Centre Association and UPS/Generator import data from New Zealand Customs supplied shipment volumes, while peer-reviewed work in IEEE Xplore helped trace PUE improvements relevant to power sizing.

We then pulled company-level revenue splits and installed-base counts from D&B Hoovers, cross-checked them with 10-K filings, investor decks, and news feeds on Dow Jones Factiva. Press releases, consultant white papers, and regional tender portals filled residual gaps. This list is illustrative; many additional sources were reviewed during validation.

Market-Sizing and Forecasting

A top-down model converts national data-center electricity draw into potential spend using prevailing tariff bands and typical power-system cost shares. Then, it is corroborated with selective bottom-up cross-checks, including supplier shipment roll-ups and sampled ASP multiplied by MW installs, to refine totals. Key variables include installed IT-load capacity additions, average PUE, weighted ASP of three-phase UPS cabinets, diesel versus biofuel generator mix, and renewable-energy PPA penetration; each is forecast through multivariate regression that blends historical series with policy and capex outlooks confirmed during interviews. Where vendor shipment data were incomplete, gap filling used moving-average imputation aligned to grid-connection approvals.

Data Validation and Update Cycle

Outputs pass variance screens against historic import values and MBIE energy-demand scenarios. Then, a senior analyst reviews anomalies before sign-off. Reports refresh each year, with mid-cycle updates triggered by material events such as utility-scale tariff shifts or greater than 10 MW facility announcements; a final pre-publication pass ensures clients receive the most current view.

Why Mordor's New Zealand Data Center Power Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because researchers pick different power-equipment lists, convert currencies on varied dates, or project capacity using unverified ramp rates.

Key gap drivers here are that some studies roll cooling and building capex into 'power,' a few apply global ASPs without adjusting for New Zealand's freight premiums, and others promote an aggressive hyperscale pipeline that our primary contacts deem unlikely before grid upgrades complete.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 127.8 M (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 250 M (2024) | Global Consultancy A | Includes mechanical infrastructure and uses global ASP benchmarks | ||

USD 814 M (2024) | Industry Publisher B | Values entire data-center investment, not just power stack |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.