Power Over Ethernet (PoE) Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.31 Billion |

| Market Size (2031) | USD 10.73 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

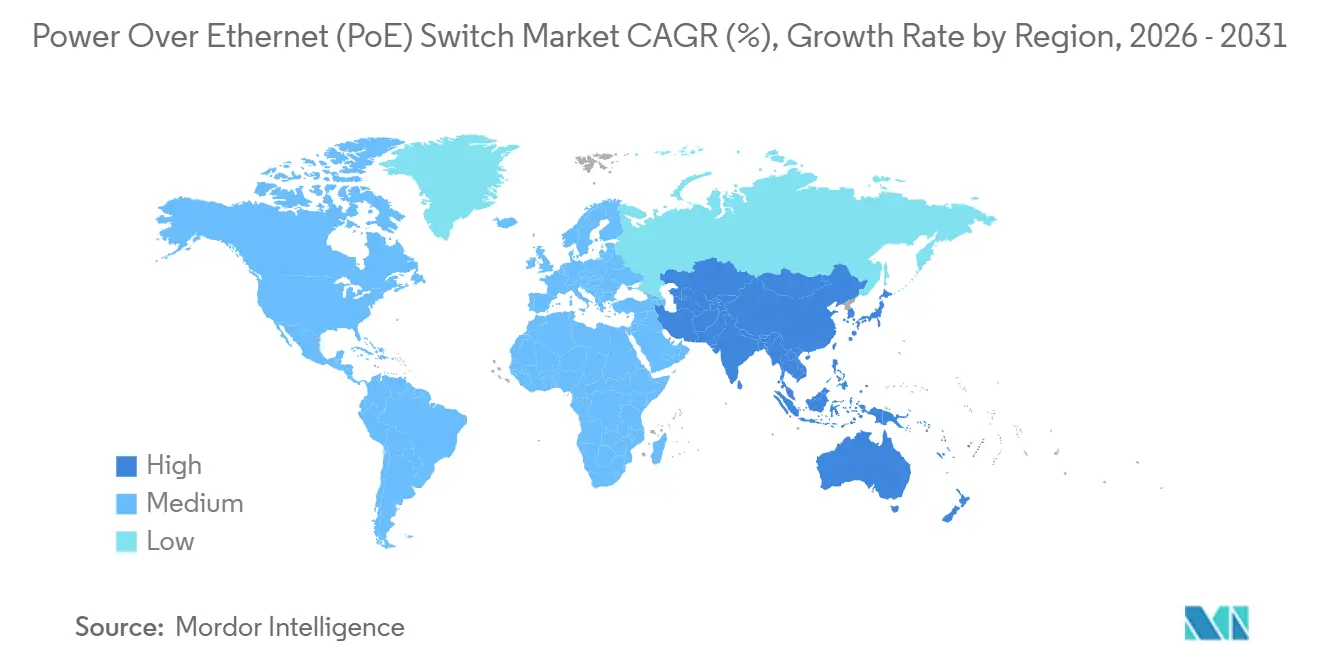

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

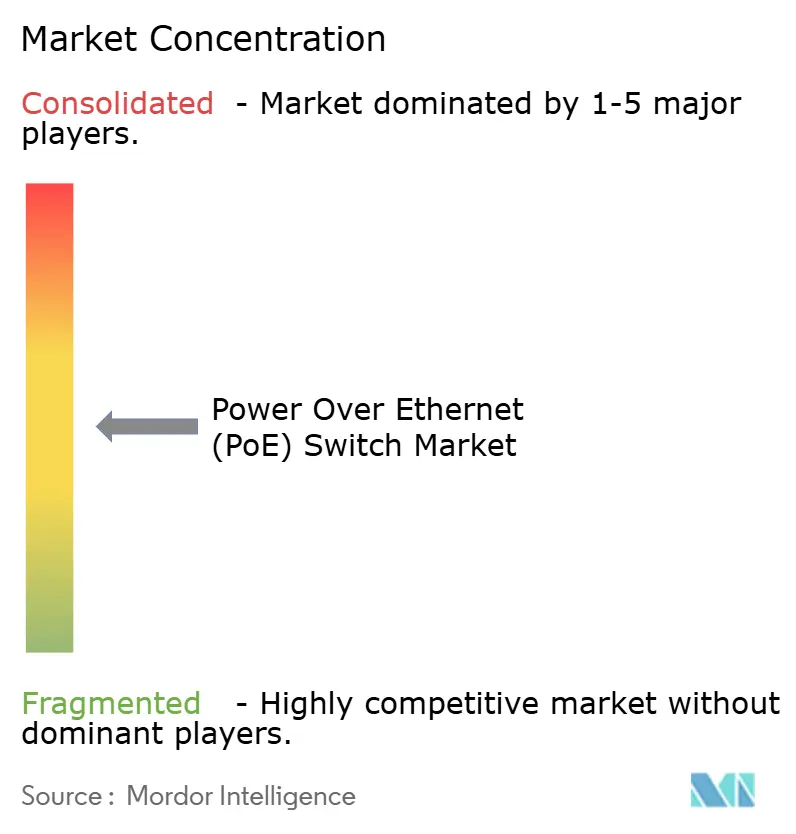

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Over Ethernet (PoE) Switch Market Analysis by Mordor Intelligence

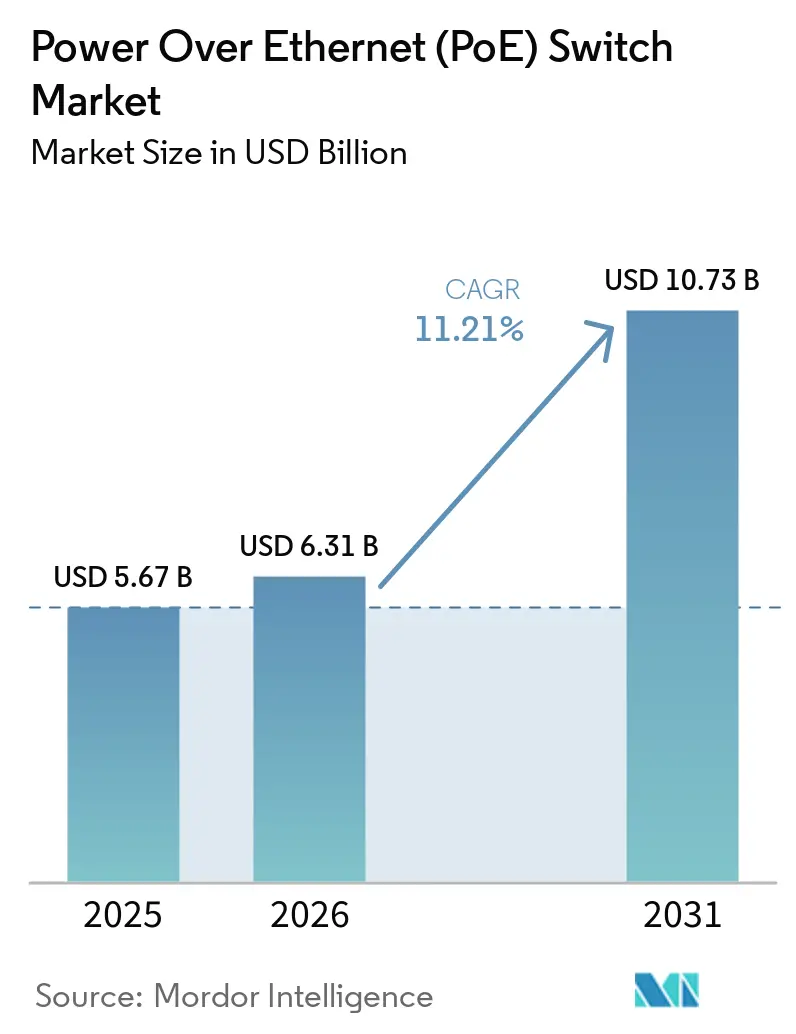

The Power over Ethernet (PoE) switch market size is projected to expand from USD 5.67 billion in 2025 and USD 6.31 billion in 2026 to USD 10.73 billion by 2031, registering a CAGR of 11.21% between 2026 to 2031. Network managers are accelerating refresh cycles to accommodate Wi-Fi 6E and Wi-Fi 7 access points that demand up to 90 watts per port, while smart-building programs continue shifting lighting, security, and HVAC controls onto a single low-voltage backbone. Industrial automation is another structural tailwind as factories replace proprietary fieldbus links with Ethernet and power hundreds of sensors from hardened Power over Ethernet (PoE) switches. Meanwhile, stricter cyber-resilience mandates in the United States and European Union are compressing replacement timelines, favoring vendors that bundle zero-trust security into the operating system. Moderate but rising consolidation, illustrated by Hewlett Packard Enterprise’s 2025 purchase of Juniper Networks, indicates that silicon scale and integrated software will separate leaders from followers over the next five years.

Key Report Takeaways

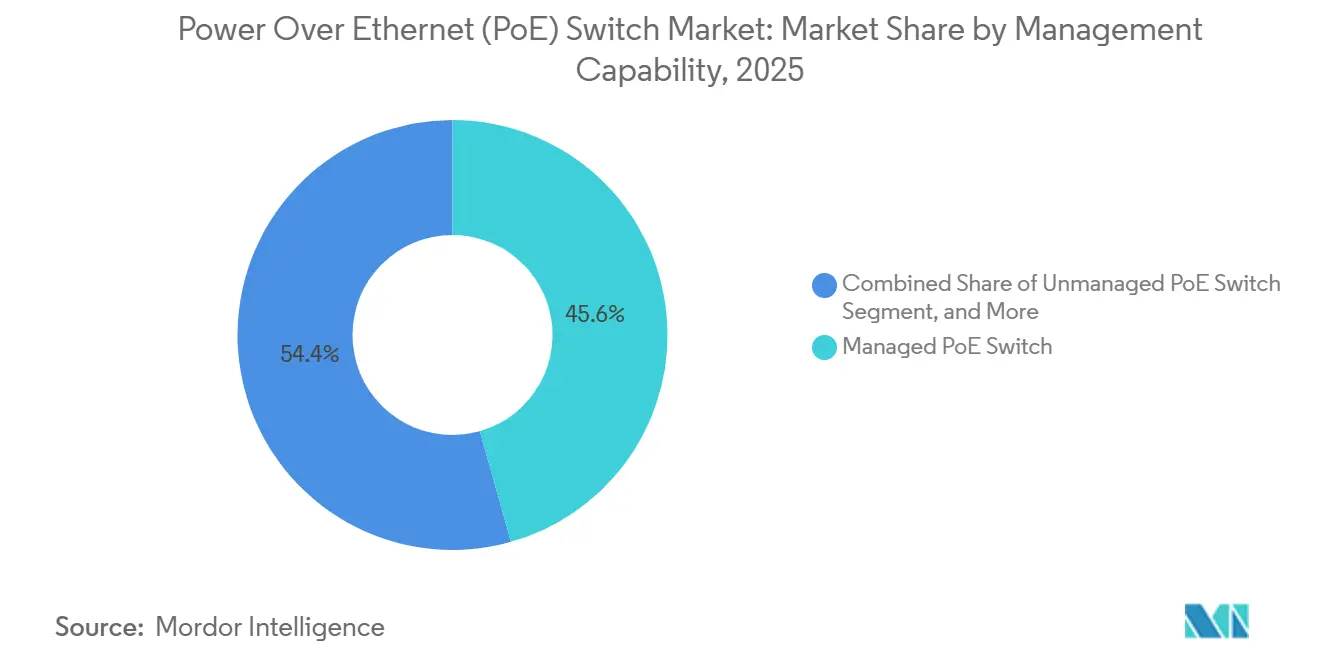

- By management capability, managed platforms led with a 45.61% revenue share in 2025, while industrial-grade variants are advancing at a 13.23% CAGR through 2031.

- By power class, up-to-30-watt models accounted for 49.94% of 2025 shipments, whereas 90-watt switches are expanding at a 15.81% CAGR over the forecast window.

- By port count, the 24-port format held 36.31% revenue share in 2025, and the 48-port chassis represents the fastest trajectory at 12.46% CAGR.

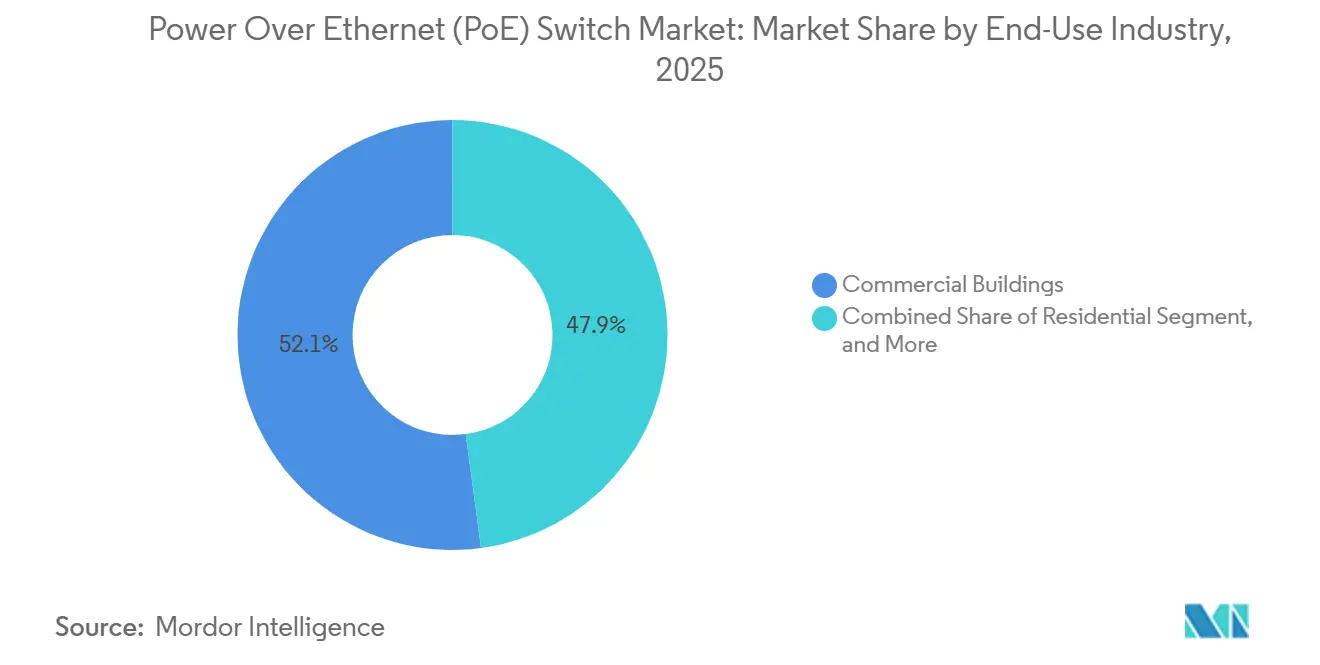

- By end-use industry, commercial buildings captured 52.11% of 2025 deployments, yet industrial and manufacturing sites show the highest growth at 14.62% CAGR.

- By application, IP surveillance dominated with 37.62% of 2025 revenue, while edge-AI computing boxes are set to grow at 16.33% CAGR.

- By geography, North America commanded 38.12% of the 2025 value, and the Asia Pacific is the quickest-growing region with a 13.87% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Power Over Ethernet (PoE) Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| IoT-Driven Smart-Building Deployments | +2.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| IP-Video Surveillance Expansion | +2.4% | Global, accelerating in Asia Pacific and Middle East | Short term (≤ 2 years) |

| Wi-Fi 6 / 6E / 7 Access-Point Power Needs | +2.1% | North America and Europe, early APAC hubs | Short term (≤ 2 years) |

| PoE-Based Smart Lighting Roll-Outs | +1.6% | North America and Europe commercial real estate | Medium term (2–4 years) |

| Edge-AI Device PoE Powering | +1.9% | APAC manufacturing core, spill-over to North America | Long term (≥ 4 years) |

| Cyber-Secure Network Mandates | +1.4% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IoT-Driven Smart-Building Deployments

Commercial property owners are migrating from proprietary building-automation controllers to Ethernet-based sensors that monitor occupancy, temperature, and indoor air quality. That change multiplies the number of Power over Ethernet (PoE) ports required per floor by three to five, pushing facility managers toward 802.3bt switches with chassis power budgets exceeding 740 watts. The integration of operational technology devices into corporate IP networks also exposes them to cyber threats, so purchasing teams increasingly specify switches with embedded firewalls and zero-trust segmentation. Siemens reported in its 2025 results call that smart-building bids in Germany and the United Kingdom now require on-board security engines that meet forthcoming EU Cyber Resilience Act obligations.[1]Siemens AG, “Building Technologies Earnings Call 2025,” siemens.com Vendors that marry high Power over Ethernet (PoE) budgets with native security are therefore winning tenders ahead of rivals that treat protection as an optional license.

IP-Video Surveillance Expansion

Municipalities and large campuses are replacing analog CCTV with 4K and 8K IP cameras that draw 25-90 watts, far above the 15-watt budgets of earlier devices. New York City’s 2024 traffic-camera contract consumed roughly 20,000 Power over Ethernet (PoE) ports, exemplifying how a single smart-city project can lift regional demand.[3]New York City Department of Transportation, “Traffic Camera Modernization Plan,” nyc.gov Camera makers such as Hikvision and Dahua shipped Type 4-powered models with on-board AI analytics in 2025, driving integrators to pick 90-watt switches or risk voltage sag. Insurance carriers have begun offering premium discounts when encrypted, tamper-proof IP surveillance is installed, adding a financial nudge that shortens replacement cycles even in budget-constrained sectors.

Wi-Fi 6 / 6E / 7 Access-Point Power Needs

Sixteen-stream Wi-Fi 7 radios consume up to 65 watts, well beyond IEEE 802.3at limits. Juniper disclosed in February 2025 that its Mist APs require 60 watts for full throughput, while Arista shipped a 90-watt-per-port campus switch the same year.[2]Arista Networks, “Campus PoE 90-Watt Design Guide,” arista.com Higher education has emerged as an early adopter because lecture halls host dense user populations, and administrators want to avoid stranded cabling when Wi-Fi 7 peaks in 2027-2028. Universities now specify 48-port distribution switches with 2,880-watt power supplies, doubling prior-generation capacity and setting a de facto baseline for future procurements.

Power over Ethernet (PoE)-Based Smart Lighting Roll-Outs

Hospitality and healthcare operators are shifting from fluorescent and AC-LED fixtures to Power over Ethernet (PoE)-powered luminaires with integrated sensors. Clarke County Hospital in Iowa finished a retrofit in 2024 that cut electricity costs by USD 500,000 and shortened installation times because Ethernet cabling does not require licensed electricians. Modern Power over Ethernet (PoE) lighting also supports emergency-battery packs through 90-watt ports, satisfying U.S. life-safety codes without separate electrical circuits. The ability to reconfigure office layouts by simply moving patch cords appeals to flexible workspace providers and is driving double-digit shipment growth for vendors such as Philips Lighting.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Upfront Hardware Costs | -1.8% | Global, acute among SMEs and schools | Short term (≤ 2 years) |

| Heat-Dissipation Limits at 90 W | -1.2% | Global, especially industrial and outdoor | Medium term (2–4 years) |

| Semiconductor Supply Imbalance | -0.9% | Global | Short term (≤ 2 years) |

| EMI Concerns in Medical Labs | -0.3% | North America and Europe hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware Costs

Enterprises can face costs of USD 800-1,200 per port when factoring in a fully loaded 48-port 802.3bt switch (priced at USD 15,000), redundant power, UPS systems, and support contracts. These high upfront costs pose a significant barrier, particularly for smaller organizations and budget-constrained sectors. Price-sensitive small firms often resort to mid-span injectors, which lack centralized management capabilities, thereby limiting operational efficiency. Public schools, bound by U.S. E-Rate guidelines, must adhere to lowest-bid rules, further restricting their ability to invest in advanced Power over Ethernet (PoE) switch solutions. To address these challenges, vendors have introduced leasing and subscription programs, effectively converting capital expenditures (capex) into operational expenditures (opex). These programs aim to make Power over Ethernet (PoE) switches more accessible by spreading costs over time. Notably, Cisco’s 2025 PoE-as-a-service offering is said to reduce initial cash outlays by as much as 70%, providing a viable alternative for organizations seeking to manage their budgets while adopting advanced Power over Ethernet (PoE) technologies.

Heat-Dissipation Limits at 90 W

When delivering 90 watts across all ports in a 24-port chassis, the system generates over 2,000 watts of waste heat. This poses a significant challenge for fanless designs, especially in environments prone to dust or vibrations. In the Power over Ethernet (PoE) Switch Market, this issue is particularly critical as Power over Ethernet (PoE) switches are increasingly required to support higher power outputs for devices such as IP cameras, wireless access points, and VoIP phones. To address this, manufacturers have turned to oversized aluminum extrusions and conformal-coated boards, which can withstand temperatures up to 75 °C. However, these enhancements come at a cost, increasing bill-of-materials expenses by 30-50%. Additionally, data-center operators often derate these 90-watt switches by 10-20% to safeguard upstream cooling budgets. This cautious approach has slowed adoption in the market, especially in scenarios where rack power density is already under pressure, further complicating the deployment of high-power Power over Ethernet (PoE) solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Management Capability: Centralized Visibility Sustains Managed Leadership

Managed switches commanded 45.61% of 2025 revenue, underscoring how network teams depend on SNMP monitoring, VLAN segmentation, and quality-of-service to prioritize real-time traffic. The Power over Ethernet switch market size for managed products is projected to outpace unmanaged units as enterprises integrate access control lists and zero-trust policies directly into distribution layers. A parallel rise in industrial-grade models shows that ruggedized housings, extended-temperature operation, and IEC 61850 compliance now matter as much as port counts, particularly on factory floors that house motion-control robots and high-speed cameras.[4]International Electrotechnical Commission, “IEC 61850 and Industrial Ethernet,” iec.ch Smart switches address a mid-tier audience by bundling browser-based configuration with limited analytics, which resonates with small businesses that lack certified engineers yet still want visibility beyond plug-and-play behavior. The Power over Ethernet switch market has also embraced cloud onboarding; Extreme Networks’ zero-touch provisioning, launched in 2025, allows branches to install equipment without specialized staff, cutting deployment windows from hours to minutes.

Industrial Power over Ethernet (PoE) variants are advancing at a 13.23% CAGR, the fastest clip inside this segmentation. Growth is propelled by predictive-maintenance projects that add hundreds of vibration and temperature sensors to each assembly line, each pulling 15-25 watts. Vendors such as Moxa and Advantech have responded with DIN-rail switches that tolerate −40 °C to 75 °C and survive 5 g shocks, attributes that shield electronics from forklift traffic and oil-mist exposure. Unmanaged devices still sell into home and micro-office sites where cost trumps features, but their share of the Power over Ethernet switch market is slowly eroding as cloud dashboards become cheap or free companions to managed gear. On the horizon, embedded AI engines, as previewed by Lantronix in 2026, blur the line between network hardware and edge-computing node, suggesting that tomorrow’s managed switch could double as an inference accelerator for surveillance feeds or production metrics.

By Power Class: 90-Watt Adoption Rewrites Power Budgets

Up-to-30-watt models retained 49.94% of 2025 shipments because legacy 802.3at cameras and Wi-Fi 6 access points still dominate installed bases. However, devices needing more than 60 watts, including Wi-Fi 7 radios and AI-enabled PTZ cameras, are stoking 15.81% annual growth for Type 4 switches through 2031. The Power over Ethernet switch market share of the 15.4-watt 802.3af class is shrinking as vendors retire 100-Mb/s uplinks in favor of gigabit interfaces. A transitional 60-watt band serves digital signage and interactive kiosks yet could fade if ultra-high-power proprietary specs, such as Cisco’s 100-watt Universal Power over Ethernet (PoE), gain wider traction.

Looking ahead, campus and healthcare customers are budgeting for 90-watt headroom even when today’s devices draw only 25-45 watts, reflecting lessons learned during the jump from 15 watts to 30 watts a decade ago. Industry codes such as U.S. NEC Article 840 allow low-voltage installers to handle cables below 100 watts without master-electrician licenses, which accelerates rollout in office renovations. Conversely, the European Low-Voltage Directive still obliges certified labor, adding a cost premium that tempers 90-watt uptake. Silicon vendors are shrinking DC-DC conversion losses, and switch makers project that 100-watt-capable silicon could ship by 2028, positioning the Power over Ethernet switch market for another generational leap in delivered wattage.

By Port Count: Density Shifts from 24 to 48 Ports

Twenty-four-port chassis earned 36.31% of 2025 revenue because they neatly fit branch offices that run thirty to forty Power over Ethernet (PoE) endpoints. Yet the Power over Ethernet switch market size attached to 48-port units is rising at 12.46% CAGR as multibuilding campuses prefer fewer racks and lower per-port costs. High-density switches also simplify cable management by halving the number of uplinks to aggregate layers, a benefit that resonates in data centers and university dormitories alike. Vendors now ship 48-port models with modular power supplies that top 2,880 watts, enabling full 90-watt delivery without brownouts.

Growth is not confined to large boxes. DIN-rail 24-port products give industrial engineers rack-mount-class density inside 19-inch control cabinets, while 8-port fanless units remain popular in retail outlets and remote surveillance poles. Economics favor larger models: a 48-port managed unit prices at USD 167-250 per port, versus USD 208-333 for a 24-port equivalent, creating an implicit 15-25% tax on buyers that stick with lower density. Over 48-ports, modular core switches serve carrier central offices where stacking latency would otherwise degrade 5G backhaul timing. Taken together, the move toward denser gear is reshaping distributor inventory and prompting makers to rethink cooling and backplane design.

By End-Use Industry: Factory Digitization Spurs Industrial Outperformance

Commercial real estate retained a 52.11% share in 2025 because offices, hotels, and shopping centers converge IP surveillance, access points, and VoIP onto existing structured cabling. Yet industrial plants offer the steepest upside: the segment is scaling at 14.62% CAGR as edge-AI vision systems perform split-second quality checks and demand 60-90 watts from local switches. The Power over Ethernet switch market size tied to factory automation expands every time a production engineer swaps a fieldbus gateway for an Ethernet sensor.

Government smart-city programs add steady volume through traffic cameras and smart streetlights, though budget cycles stretch lead times to 18-24 months. Healthcare facilities modernize nurse-call panels and patient monitors with Power over Ethernet (PoE) to simplify infection-control cleaning, while K-12 districts in the United States tap enhanced E-Rate funding of USD 201.57 per student to replace aging Fast Ethernet gear. Telecom operators leverage Type 4 switches inside 5G small-cell aggregation huts, eliminating separate AC feeds in rooftop or pole-top locations. Although residential demand remains niche, sub-USD 100 five-port unmanaged devices are expanding the consumer market and may seed future prosumer upgrades.

By Application: Edge Intelligence Climbs the Value Stack

IP surveillance captured 37.62% of 2025 revenue as 4K streams became a standard corporate insurance requirement. Edge-AI boxes, however, represent the fastest trajectory at 16.33% CAGR because semiconductor makers now integrate neural-processing units alongside modest GPUs, enabling real-time inference on vibration data, video feeds, or predictive maintenance metrics directly inside a Power over Ethernet (PoE)-powered enclosure. Wireless access points remain a mature demand pillar, but Wi-Fi 7 upgrades are condensing refresh intervals from seven years to roughly five.

VoIP handsets are declining as softphones cannibalize desk sets, yet ruggedized call buttons survive in hospitals and industrial sites. Building-automation gateways and Power over Ethernet (PoE) lighting are emerging segments that receive incremental momentum from energy-performance regulations in Europe and the United States. Industrial sensors are migrating to Single Pair Ethernet with Power over Ethernet (PoE), extending reach to 1,000 m for oil rigs and mines. Finally, 5G small cells lean on 90-watt ports to power integrated radios in street furniture, reinforcing the Power over Ethernet switch market as a backbone of urban densification.

Geography Analysis

North America held 38.12% of 2025 revenue as enterprises swapped out decade-old Catalyst 3750 units and migrated to Wi-Fi 6E-ready distribution layers. Federal E-Rate funding boosts K-12 refreshes, and the Cybersecurity Maturity Model Certification in defense supply chains pushes prime contractors toward switches with hardware roots of trust. Canada mirrors U.S. trends, with an added lift from smart-campus programs at major universities.

Asia Pacific is the fast-growth engine with a 13.87% CAGR through 2031. China and India are embedding Power over Ethernet (PoE) within Industry 4.0 retrofits that unify operational and information technology, expanding port density by three to five times on each line. Southeast Asian nations follow similar paths as electronics-assembly hubs proliferate, while Australian hospitals and colleges adopt Wi-Fi 6E access points and 90-watt lighting drivers under digital-inclusion grants.

Europe posts mid-single-digit growth, buoyed by NIS2 and DORA mandates that force critical-infrastructure operators and banks to segment Power over Ethernet (PoE) endpoints. The Energy Performance of Buildings Directive also incentivizes PoE lighting retrofits across the commercial stock. Latin America remains smaller, concentrated in Brazilian finance and Argentine agricultural exports where grain elevators adopt IP surveillance against theft. The Middle East and Africa are project-driven; Saudi Arabia’s NEOM and Dubai Smart City specify PoE street infrastructure, but rollouts depend on public-sector tender cycles.

Competitive Landscape

The PoE switch market is moderately concentrated, with Cisco Systems, Hewlett Packard Enterprise (HPE), and Huawei Technologies collectively holding a significant share of global revenues. A key milestone occurred in July 2025 when HPE acquired Juniper Networks for USD 14 billion. This acquisition elevated the combined entity to approximately 25% market share and enhanced Aruba’s switching portfolio by incorporating Juniper’s Mist AI wireless technology, creating substantial cross-selling opportunities in enterprise networking. Cisco continues to maintain its leadership in the high-end market segment by leveraging proprietary innovations such as 100-watt Universal PoE and advanced in-silicon analytics, powered by AMD Ryzen V3000 embedded processors introduced in April 2026. These developments emphasize the importance of scale, proprietary standards, and integrated intelligence in shaping competitive dynamics.

While global leaders dominate the premium enterprise segment, regional specialists are securing strong positions in localized markets. Companies like Ruijie in China, Allied Telesis in Japan, and PLANET Technology in Taiwan excel in price-sensitive or ruggedized deployments, areas where global vendors often hesitate to localize firmware or address niche requirements. Simultaneously, disruptors such as Lantronix are redefining the competitive landscape by integrating high-performance AI engines capable of 8 TOPS directly into switch fabrics. This innovation enables on-premise video analytics without relying on cloud infrastructure, reducing latency and appealing to industries that require real-time processing. These advancements demonstrate how smaller players can compete effectively by focusing on specialized use cases and advanced edge capabilities.

In addition to competitive positioning, external factors are influencing market dynamics. Persistent semiconductor shortages remain a critical challenge, with lead times for power-management integrated circuits exceeding 40 weeks. This supply chain disruption often shifts purchasing decisions toward vendors with larger inventory reserves, reinforcing the advantages of established players. Furthermore, regulatory compliance is becoming a significant barrier to entry. The EU Cyber Resilience Act, effective September 2026, mandates secure boot and hardware root-of-trust features for all suppliers. While these requirements increase costs for established vendors, they also create substantial obstacles for white-box entrants, narrowing the competitive field. Together, supply chain volatility and regulatory mandates are driving market consolidation, favoring well-capitalized players capable of absorbing compliance costs and managing inventory risks.

Power Over Ethernet (PoE) Switch Industry Leaders

Cisco Systems, Inc.

Hewlett Packard Enterprise (Aruba)

Huawei Technologies Co., Ltd.

Netgear, Inc.

TP-Link Corporation Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AMD announced that Ryzen V3000 embedded processors power Cisco Catalyst 9300 and 8000 series switches, inserting AI telemetry and real-time threat detection at the hardware layer.

- March 2026: Lantronix launched SmartSwitch.ai with an 8-TOPS edge-AI engine to deliver on-switch video analytics for retail and traffic monitoring.

- January 2026: NETGEAR released the M4350 AV-over-IP switch series featuring 48 ports and a 1,130-watt Power over Ethernet (PoE) budget aimed at broadcast studios and conference centers.

- September 2025: Extreme Networks added zero-touch provisioning that downloads configurations on first boot, slashing branch-deployment times.

Global Power Over Ethernet (PoE) Switch Market Report Scope

The Power over Ethernet (PoE) switch market is an industry focused on network switches that provide both data transmission and electrical power over a single Ethernet cable. Power over Ethernet (PoE) switches enable the operation of devices such as IP cameras, wireless access points, VoIP phones, IoT sensors, and smart building systems without requiring separate power sources. These switches simplify deployment, reduce infrastructure costs, and address the growing demand for connected devices across various sectors.

The Power over Ethernet (PoE) Switch Market Report is Segmented by Management Capability (Managed, Unmanaged, and Smart), Power Class (Up to 15.4W, Up to 30W, Up to 60W, Up to 90W, and Above 90W), Port Count (4-8, 9-16, 17-24, 25-48, and Above 48), End-Use Industry (Residential, Commercial, Industrial, Government, IT and Telecom, Healthcare, Education, and Other End-Use Industries), Application (IP Surveillance, Wireless APs, VoIP, Building Automation, Industrial Sensors, Edge AI, and 5G Small Cells), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Managed PoE Switch |

| Unmanaged PoE Switch |

| Smart PoE Switch |

| Up to 15.4 W (802.3af) |

| Up to 30 W (802.3at) |

| Up to 60 W (Type 3) |

| Up to 90 W (Type 4) |

| Above 90 W (Ultra PoE) |

| 4-8 Ports |

| 9-16 Ports |

| 17-24 Ports |

| 25-48 Ports |

| Above 48 Ports |

| Residential |

| Commercial Buildings |

| Industrial and Manufacturing |

| Government and Public Infrastructure |

| IT and Telecom |

| Healthcare |

| Education |

| Other End-Use Industries (Retail, Transportation and Logistics) |

| IP Surveillance Cameras |

| Wireless Access Points |

| VoIP Phones and UC Endpoints |

| Building Automation and PoE Lighting |

| Industrial Sensors and Controllers |

| Edge Computing Nodes and AI Boxes |

| 5G Small Cells and DAS |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Oceania | ||

| Rest of the Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Management Capability | Managed PoE Switch | ||

| Unmanaged PoE Switch | |||

| Smart PoE Switch | |||

| By Power Class | Up to 15.4 W (802.3af) | ||

| Up to 30 W (802.3at) | |||

| Up to 60 W (Type 3) | |||

| Up to 90 W (Type 4) | |||

| Above 90 W (Ultra PoE) | |||

| By Port Count | 4-8 Ports | ||

| 9-16 Ports | |||

| 17-24 Ports | |||

| 25-48 Ports | |||

| Above 48 Ports | |||

| By End-Use Industry | Residential | ||

| Commercial Buildings | |||

| Industrial and Manufacturing | |||

| Government and Public Infrastructure | |||

| IT and Telecom | |||

| Healthcare | |||

| Education | |||

| Other End-Use Industries (Retail, Transportation and Logistics) | |||

| By Application | IP Surveillance Cameras | ||

| Wireless Access Points | |||

| VoIP Phones and UC Endpoints | |||

| Building Automation and PoE Lighting | |||

| Industrial Sensors and Controllers | |||

| Edge Computing Nodes and AI Boxes | |||

| 5G Small Cells and DAS | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Oceania | |||

| Rest of the Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the Power over Ethernet switch market be by 2031?

The Power over Ethernet switch market size is projected to hit USD 10.73 billion by 2031, expanding at an 11.21% CAGR from 2026 to 2031 (Mordor Intelligence).

Which segment grows fastest within Power over Ethernet (PoE) switching?

Power over Ethernet (PoE) switches that deliver up to 90 watts per port are expected to post the highest CAGR of 15.81% through 2031, driven by Wi-Fi 7 access points and AI-enabled PTZ cameras (Mordor Intelligence).

What application currently dominates Power over Ethernet (PoE) demand?

IP surveillance leads with a 37.62% revenue share, reflecting corporate and municipal moves toward 4K and 8K camera deployments (Mordor Intelligence).

Which region shows the highest growth momentum?

Asia Pacific is forecast to grow at a 13.87% CAGR as Chinese and Indian manufacturers adopt smart-factory architectures (Mordor Intelligence).

How concentrated is vendor competition?

Cisco, Hewlett Packard Enterprise, and Huawei collectively hold about 55-60% share.

What is the biggest barrier to adoption for small organizations?

Upfront capital outlays that can exceed USD 800-1,200 per port are the primary restraint, though subscription programs are emerging to lower initial costs.

Page last updated on: