Power Device Analyzer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

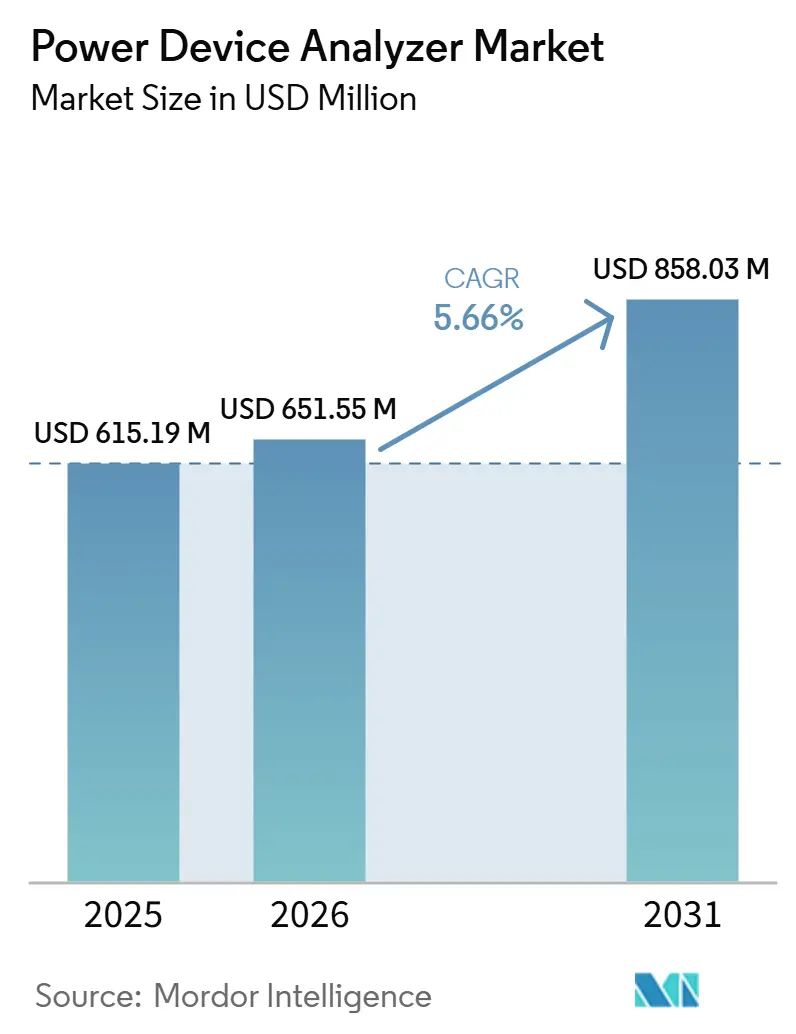

| Market Size (2026) | USD 651.55 Million |

| Market Size (2031) | USD 858.03 Million |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

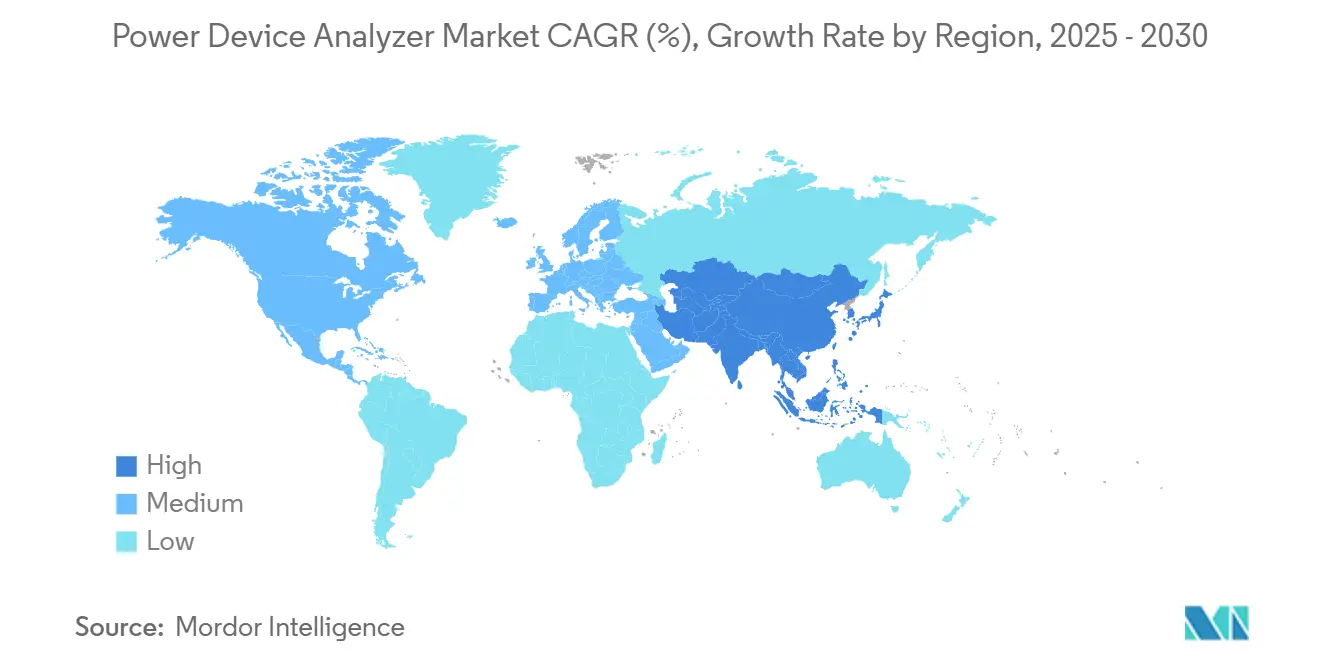

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

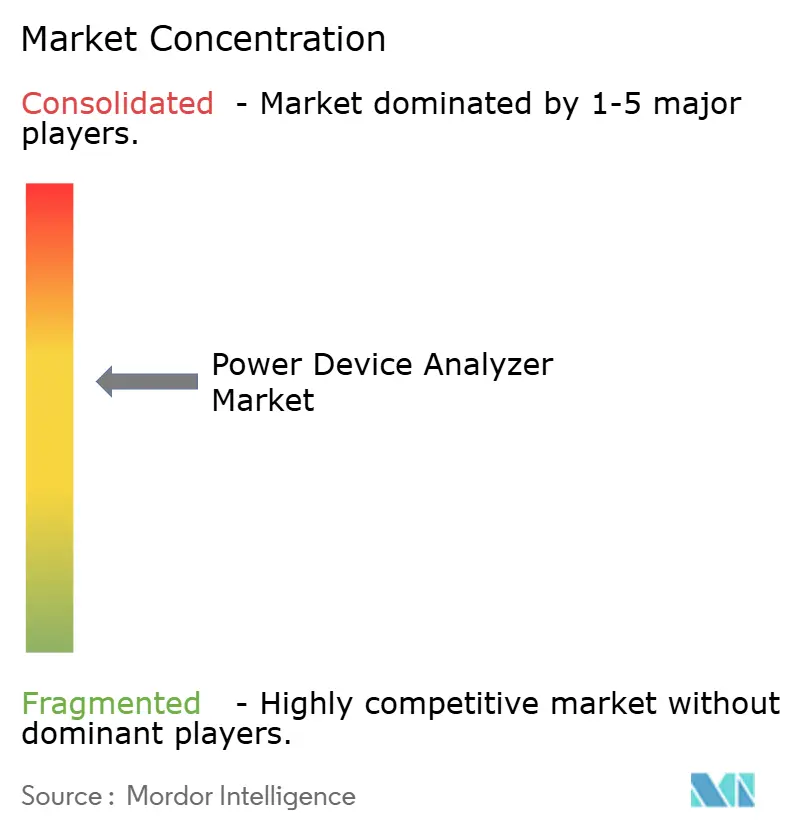

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Device Analyzer Market Analysis by Mordor Intelligence

The Power Device Analyzer Market size is projected to expand from USD 615.19 million in 2025 and USD 651.55 million in 2026 to USD 858.03 million by 2031, registering a CAGR of 5.66% between 2026 to 2031. Rising electrification mandates, rapid adoption of wide-bandgap semiconductors, and the need to validate next-generation power electronics across higher voltages and switching frequencies are the key factors driving this growth. Dual-mode AC/DC platforms are increasingly preferred as they support hybrid power architectures found in electric vehicles, grid-tied inverters, and high-density data center power supplies. Additionally, stricter standby-power limits for consumer devices and megahertz-class gallium-nitride chargers are expanding demand beyond traditional industrial users. Vendors are responding with regenerative sources that return energy to the grid, embedded thermal cameras, and automation tools that reduce test cycles while meeting sustainability targets. Although high capital costs and a shortage of skilled test engineers are limiting near-term adoption, leasing models and AI-driven workflows are beginning to lower these barriers and are expected to support medium-term growth in the power device analyzer market.

Key Report Takeaways

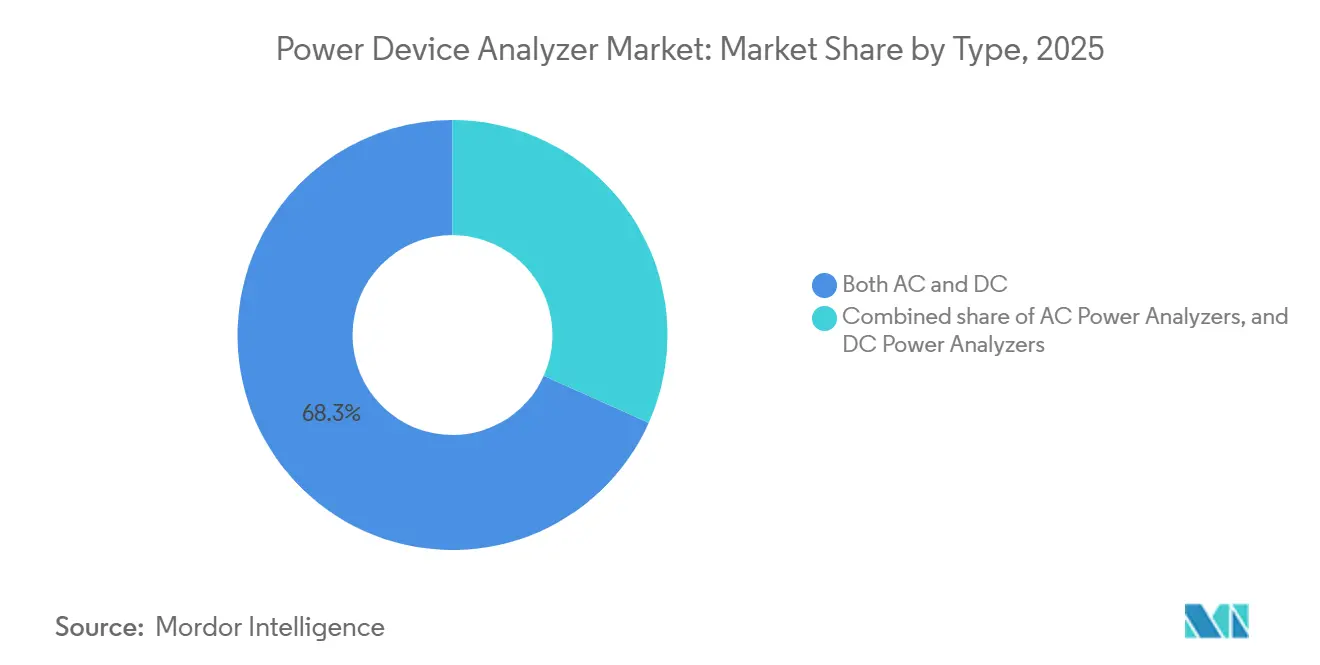

- By type, AC + DC analyzers held a 68.3% share of the power device analyzer market in 2025, and the segment is projected to grow at a 6.0% CAGR through 2031.

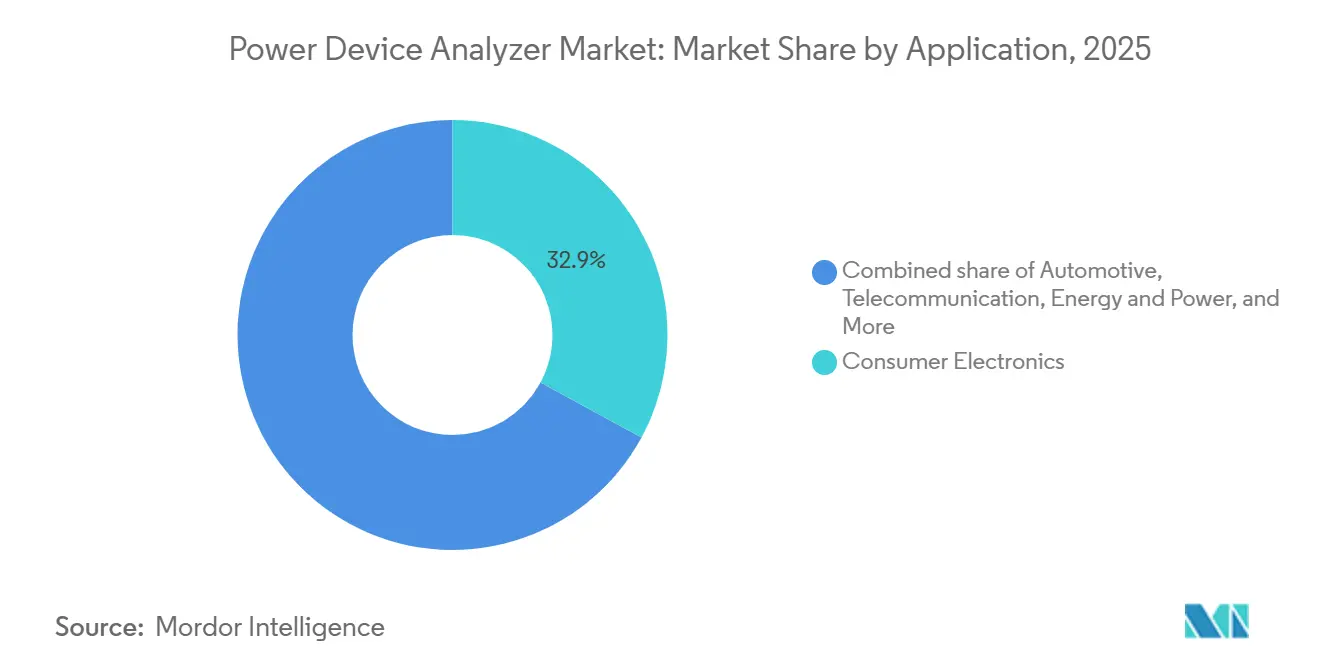

- By application, consumer electronics and appliances accounted for a 32.9% share of the power device analyzer market in 2025 and are also expected to grow at a 6.3% CAGR through 2031.

- By region, Asia-Pacific held a 35.8% revenue share in 2025 and is projected to grow at a 6.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Power Device Analyzer Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV power-electronics boom | +1.80% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Renewable-energy capacity expansion | +1.20% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Efficiency push in consumer electronics | +0.90% | Global, with EU and North America regulatory leadership | Short term (≤ 2 years) |

| Regulatory mandates on power quality | +0.70% | Europe, North America, Japan | Medium term (2-4 years) |

| Wide-bandgap (SiC / GaN) adoption | +1.50% | Global, with manufacturing hubs in Asia-Pacific and North America | Medium term (2-4 years) |

| AI-driven automated test benches | +0.60% | North America, Europe, advanced APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Power-Electronics Boom

Automotive traction inverters, onboard chargers, and DC-DC converters are transitioning to 800 V and trialing 1,200 V stacks, requiring analyzers that source and measure beyond 1,700 V and 250 A while resolving nanosecond switching edges. Silicon-carbide MOSFETs now account for a majority of future automotive design wins, operating at junction temperatures up to 200 °C, making sub-nanosecond timing resolution and synchronized thermal-transient capture baseline requirements. High-volume wafer production moving to 200 mm is doubling die counts per boule, driving demand for larger fleets of burn-in ovens and parallel test sites. Production systems such as Cohu's Neon carrier can stress 2,500 V per device and dissipate 3 kW of heat, reflecting throughput demands that directly contribute to higher analyzer shipments. As electric vehicle unit sales grow, the power device analyzer market is benefiting from backlog orders for high-voltage, high-current test cells across Asia, Europe, and the United States.

Renewable-Energy Capacity Expansion

Rapid solar and wind build-outs compel utilities to monitor bidirectional power flow, flicker, and inter-harmonics under IEEE 1547-2018 grid-interconnection mandates.[1]IEEE Standards Association, “IEEE 1547-2018 Interconnection Standard,” ieee.org Battery energy storage systems add further complexity because analyzers must maintain accuracy during charge and discharge cycles while logging data for UL 9540 certification.[2]UL Solutions, “UL 9540 Battery Energy Storage System Standard,” ul.com European grid operators, guided by the 2050 carbon-neutral target, invest in high-channel-count analyzers to supervise distributed generators, inverters, and flexible loads in real time, elevating demand for cloud-enabled, cybersecurity-hardened instruments.

Efficiency Push in Consumer Electronics

European Regulation 2023/826 reduced standby-power allowances to as low as 0.5 W in 2025, with a further reduction to 0.3 W by 2027. This requires consumer electronics manufacturers to verify sub-milliampere current draws. Gallium-nitride chargers switching above 1 MHz create demand for 100 MHz bandwidth and ±0.1% uncertainty even at low power factors. IEC 62301 Edition 2 specifies sampling rates of 500 kS/s, prompting many manufacturers to replace legacy wattmeters with higher-speed analyzers. Instruments that incorporate thermal imaging and automated ripple-noise routines help engineers reduce certification cycle times, supporting the near-term outlook for the power device analyzer market.

Wide-Bandgap (SiC / GaN) Adoption

JEDEC has issued dedicated reliability guidelines for SiC MOSFETs and GaN HEMTs, covering gate-oxide stress, high-temperature reverse bias, and cosmic-ray robustness. Measurement windows extend into the nanosecond domain, and test environments now exceed 200 °C, requiring analyzers with low thermal drift and isolated probe systems. Infineon's CoolSiC introduction highlighted the need for double-pulse testing at over 3 kA µs⁻¹ di/dt, prompting instrument vendors to improve common-mode rejection and timing accuracy. Analyzers that combine high-bandwidth acquisition with synchronized voltage, current, and temperature logging support predictive lifetime modeling for automotive and grid applications.

Restraints Impact Analysis of Power Device Analyzer Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront analyzer cost | -0.80% | Global, acute in developing markets and smaller firms | Short term (≤ 2 years) |

| Scarcity of skilled test engineers | -0.50% | Global, with shortages in North America and Europe | Medium term (2-4 years) |

| Precision-shunt supply bottlenecks | -0.30% | Global, with dependencies on specialized suppliers | Short term (≤ 2 years) |

| On-chip monitoring cannibalization | -0.40% | North America, Europe, advanced APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Analyzer Cost

High-end, eight-channel solutions from Keysight or Yokogawa exceed USD 100,000, limiting access for small and mid-sized electronics firms. Leasing models reduce capital outlay but often restrict customization or data ownership, impeding proprietary algorithm development. Some OEMs attempt to substitute oscilloscopes with math-based power modules; however, accuracy limitations at low power factors expose them to compliance risks, slowing adoption of such substitutes.

Scarcity of Skilled Test Engineers

Global test-equipment installation outpaces talent supply, especially in high-frequency measurement and wide-bandgap device characterization. IEEE Spectrum surveys indicate 53% of experienced semiconductor employees consider leaving within six months, with test engineering among the hardest positions to backfill.[3]Source: IEEE Spectrum, “The Semiconductor Workforce Challenge,” spectrum.ieee.org Companies counter with internal boot camps and joint curricula with equipment vendors, yet productivity gaps remain as new hires climb learning curves on complex, safety-critical benches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Power Device Analyzer Market Segment Analysis

By Type:

Dual-Mode Platforms DominateDual-mode AC/DC instruments held 68.3% of the power device analyzer market share in 2025. Their 6.0% CAGR through 2031 reflects user preference for a single platform that covers grid input, battery storage, and bidirectional loads. The market size for this segment is projected to grow steadily as engineers replace separate AC and DC benches with regenerative systems that also meet corporate energy-recovery goals.

This trend benefits vendors offering modular plug-ins that scale voltage up to 4 kV and current above 250 A without increasing rack space. Keysight's 12 kW RP5900 supply and Yokogawa's 720301 module both illustrate the shift toward software-defined setups that switch measurement ranges within milliseconds. DC-only analyzers remain essential in battery cyclers and photovoltaic labs, but even in these applications, engineers increasingly require AC emulation to verify anti-islanding algorithms, suggesting further share gains for dual-mode designs within the power device analyzer market.

By Application:

Consumer Electronics Lead, Automotive AcceleratesConsumer electronics and appliances accounted for 32.9% of 2025 revenue, driven by tighter standby-power regulations and megahertz gallium-nitride adapters. This segment of the power device analyzer market is tracking a 6.3% CAGR as brands upgrade to instruments capable of ±0.1% accuracy at milliampere levels.

Automotive testing is expected to witness significant growth through 2031 because 800 V drivetrains and silicon-carbide inverters require burn-in racks rated above 1,200 V and 250 A. Regenerative loads that replicate road cycles, along with thermal chambers simulating liquid-cooling loops, are now standard. Grid energy, data-center supplies, and medical equipment represent additional sources of demand, each with specialized compliance requirements, from IEEE 1547 ride-through verification to IEC 60601 leakage-current measurement, that collectively expand the addressable power device analyzer market.

Geography Analysis

APAC Power Device Analyzer Market

Asia-Pacific led the power device analyzer market in 2024 with a 35.4% share and is projected to log a robust 6.3% CAGR to 2030. Government incentives, such as China’s strategic fund for third-generation semiconductors and India’s Production Linked Incentive scheme for electronics, stimulate analyzer procurement across fab expansion, EV component validation, and appliance efficiency testing. Japan and South Korea extend spending in automotive electronics and memory fabs, leveraging local metrology ecosystems to maintain export competitiveness.

North America Power Device Analyzer Market

North America commands high average selling prices owing to advanced EV development, aerospace electrification, and CHIPS Act-funded fab projects. OEMs require analyzers that satisfy OSHA and NFPA 70E safety protocols, leading to strong adoption of isolated high-bandwidth probes. Utilities invest in Class A portable analyzers to monitor renewable integration and to validate FERC-mandated power-quality indices, anchoring replacement demand.

EMEA and South America Power Device Analyzer Market

Europe’s stringent environmental regulations and rapid renewable rollout fuel analyzer upgrades that capture energy-direction reversals under high distributed-generation penetration. Germany’s inverter manufacturers now bundle cloud-ready analyzers in demonstration labs to streamline utility certification. Scandinavian utilities pilot wide-area harmonic-logging networks, driving orders for rack-mount analyzers with GPS-synced event correlation. The Middle East and Africa witness rising solar capacity and industrial diversification; however, analyst replacement cycles remain longer due to limited local service support. South America sees localized automotive and appliance assembly, sustaining steady but moderate instrument demand amid currency volatility.

Competitive Landscape

The power device analyzer market is moderately concentrated. Key competitors include Keysight, Tektronix, Rohde & Schwarz, Yokogawa, National Instruments, and Microtest, which compete on bandwidth, accuracy, and integrated automation. Keysight's 2 U, 12 kW regenerative supply recovers energy and doubles channel density compared with legacy units, reflecting the broader industry shift toward sustainability and compact form factors.

Yokogawa's 720252 isolation plug-in cancels DC offsets above 1 GΩ and resolves microvolt fluctuations, providing battery researchers with low-noise measurement capability that legacy probes cannot match. Microtest's VIP Ultra scales from 48 low-voltage sites to 16 sites at 4 kV within the same chassis, simplifying high-mix production for Si, SiC, and GaN discretes.

Beyond the top tier, Chroma ATE, Hioki, and NH Research compete by offering specialized solutions such as battery cyclers or regenerative grid simulators, supported by local calibration services. Track-and-trace software, cybersecurity compliance, and cloud analytics are emerging as differentiators, particularly for aerospace and defense contracts. Acquisitions that incorporate power devices such as Infineon acquiring GaN Systems and Renesas absorbing Transphorm indicate growing in-house test capability among device manufacturers. However, external vendors remain essential for safety certification and multi-physics validation, supporting a stable outlook for the broader power device analyzer market.

Power Device Analyzer Industry Leaders

Keysight Technologies

Yokogawa Electric

Tektronix

Rohde & Schwarz

Chroma ATE

- *Disclaimer: Major Players sorted in no particular order

Power Device Analyzer Market Companies Covered in this Report

- Aplab Limited

- B&K Precision Corporation

- Chroma ATE Inc.

- Dewesoft d.o.o.

- Fluke Corporation

- GW Instek (Good Will Instrument Co., Ltd.)

- Hioki E.E. Corporation

- Iwatsu Electric Co., Ltd.

- Keysight Technologies, Inc.

- Magna-Power Electronics, Inc.

- National Instruments Corporation

- NH Research, Inc.

- Newtons4th Ltd.

- Omicron Lab (OMICRON Lab GmbH)

- Pintek Electronics Co., Ltd.

- Rigol Technologies Co., Ltd.

- Rohde & Schwarz GmbH & Co. KG

- Tektronix, Inc.

- Yokogawa Electric Corporation

- ZES Zimmer Electronic Systems GmbH

Recent Industry Developments in Power Device Analyzer Market

- March 2026: Yokogawa Test & Measurement introduced the 720252 isolation module and the 720301 power measurement module, designed to capture microvolt signals at a 1 GΩ input impedance and perform cycle-by-cycle power calculations with a resolution of 0.1 ms. These modules are intended for applications such as EV battery research and development and data-center UPS validation.

- May 2025: Chroma ATE announced upgrades to the 3650-S2 platform and a forthcoming HTMU board integrating AI-guided test flows for power chips.

- March 2025: Keysight Technologies introduced DCA-M sampling oscilloscopes engineered for 1.6 T optical transceiver verification, featuring 240 Gb/s per lane analysis and integrated clock recovery.

- November 2024: Tektronix launched TICP IsoVu probes and EA-PSB 20000 triple bidirectional power supplies to address automotive and renewable high-power tests.

- June 2024: Yokogawa introduced CT1000S split-core sensors and DLM5000HD oscilloscopes for high-current, high-definition power analysis.

Global Power Device Analyzer Market Report Scope

A power analyzer is a precision instrument used to measure, analyze, and record electrical power parameters, including voltage, current, harmonics, and power factor, in AC/DC systems. It functions as a "power multimeter," offering detailed, real-time insights into energy efficiency and consumption, and is commonly used to ensure compliance with quality standards.

The Global Power Device Analyzer Market is segmented into type, application, and geography. By type, the market is segmented into AC power analyzers, DC power analyzers, and both AC and DC power analyzers. By application, the market is segmented into automotive, energy and power, consumer electronics, telecommunications, healthcare devices, industrial automation, and others. The report also covers the market size and forecasts for the power device analyzer market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

Segmentation Overview

| AC Power Analyzers |

| DC Power Analyzers |

| Both AC and DC |

| Automotive |

| Energy and Power |

| Consumer Electronics |

| Telecommunications |

| Healthcare Devices |

| Industrial Automation |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | AC Power Analyzers | |

| DC Power Analyzers | ||

| Both AC and DC | ||

| By Application | Automotive | |

| Energy and Power | ||

| Consumer Electronics | ||

| Telecommunications | ||

| Healthcare Devices | ||

| Industrial Automation | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Power device analyzer market be by 2031?

The sector is expected to reach USD 858.03 million by 2031, reflecting a 5.66% CAGR from 2026 to 2031.

Which segment is growing fastest inside the field?

Automotive testing shows the strongest momentum, advancing at roughly a 10% CAGR as 800 V drivetrains and SiC inverters proliferate.

Why are dual-mode AC/DC platforms overtaking single-mode instruments?

Engineers prefer one chassis that measures both grid and battery paths, and regenerative designs now return energy to the grid, lowering operating costs.

What is the main barrier to wider adoption?

High upfront capital outlay can exceed USD 500,000 per test cell, limiting purchases by smaller firms until leasing and service models mature.

Which region leads in demand?

Asia-Pacific holds the largest revenue slice at 35.8% thanks to expanding semiconductor fabs and aggressive electrification goals.

How are vendors differentiating their offerings?

Leading suppliers embed automation, regenerative energy recovery, wide-bandwidth probes for SiC/GaN, and cloud analytics that shorten validation cycles.

Page last updated on: