Power Quality Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.3 Billion |

| Market Size (2031) | USD 28.26 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Quality Equipment Market Analysis by Mordor Intelligence

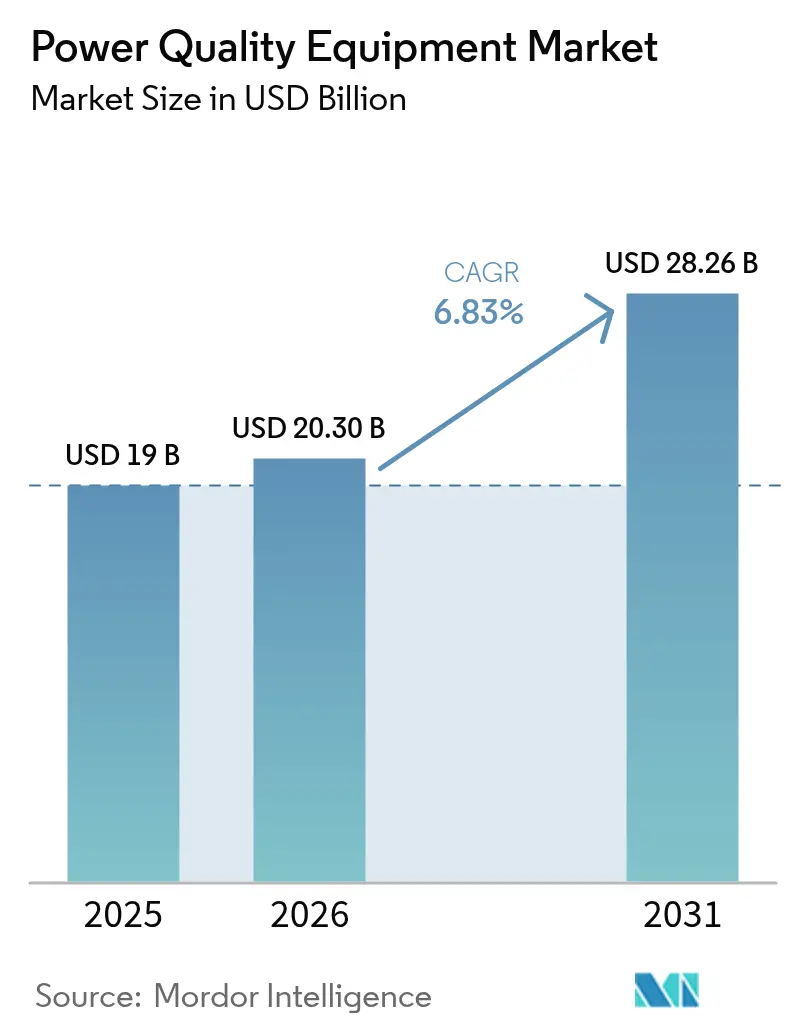

The Power Quality Equipment Market size was valued at USD 19 billion in 2025 and estimated to grow from USD 20.3 billion in 2026 to reach USD 28.26 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031).

Rising digitalization of factories, expanding renewable capacity, and rapid data-center build-outs underscore why even microsecond power disturbances now translate into costly downtime across global industries. Utilities and manufacturers are shifting from reactive protection to predictive, software-driven systems that diagnose and correct issues in real time. Growing deployment of advanced power electronics, machine-learning algorithms, and bidirectional grid controls is redefining power quality from a niche maintenance task into a strategic enabler of electrification and sustainability. Asia-Pacific commands almost one-half of global demand, underpinned by record grid investments in China and India’s renewable surge.

Key Report Takeaways

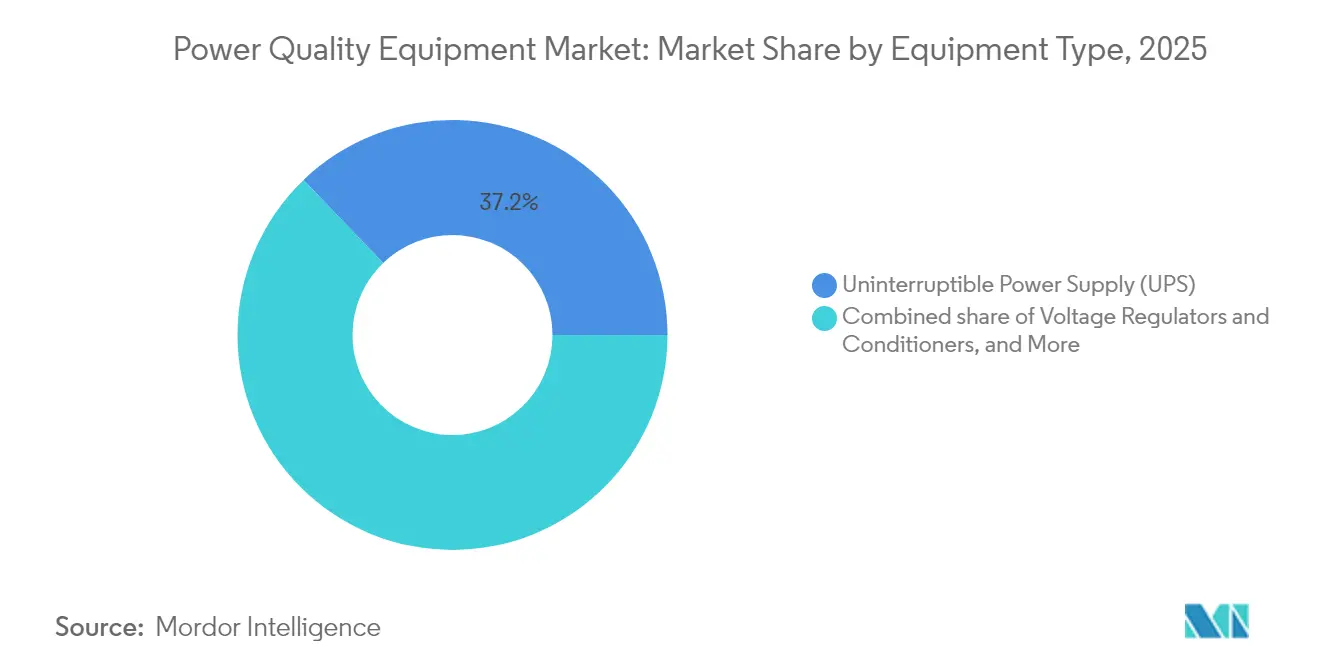

- By equipment type, Uninterruptible Power Supply systems captured 37.18% of the power quality equipment market share in 2025. Voltage regulators and conditioners are advancing at a 9.62% CAGR through 2031, the fastest pace within the power quality equipment market.

- By phase, three-phase solutions led with 60.05% share of the power quality equipment market in 2025, while single-phase products are poised for a 7.12% CAGR to 2031.

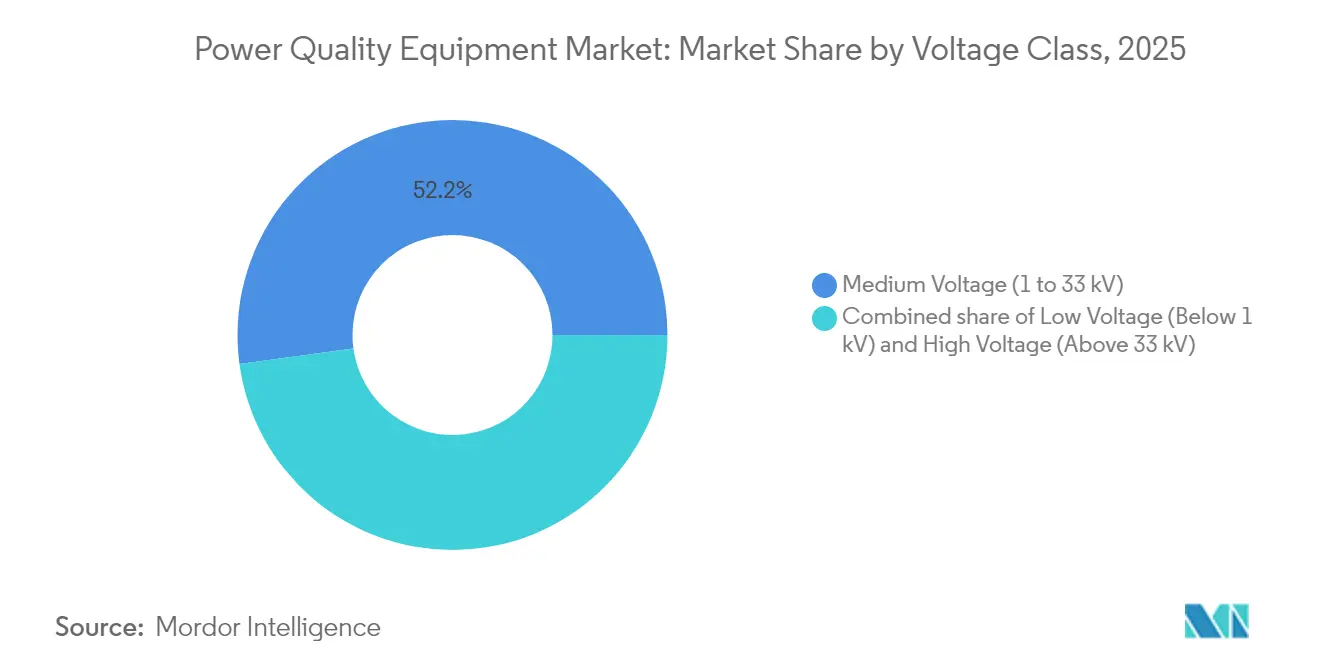

- By voltage class, medium-voltage devices accounted for 52.15% share of the power quality equipment market size in 2025; low-voltage units are forecast to post the highest 8.01% CAGR through 2031.

- By application, renewable-integration and data-center projects jointly represented 32.45% of the power quality equipment market size in 2025, whereas EV fast-charging infrastructure is projected to expand at a 9.08% CAGR between 2026 and 2031.

- By end-user, commercial and industrial facilities held 62.35% market share in 2025; utilities constitute the fastest-growing user base at a 7.18% CAGR to 2031.

- By geography, Asia-Pacific accounted for the largest share, 48.05% in 2025, and is also likely to grow the fastest, at a CAGR of 8.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Quality Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of sensitive electronics in Industry 4.0 processes | +1.8% | Global, with early gains in Germany, China, Japan | Medium term (2-4 years) |

| Expansion of data centres requiring high-availability power | +1.5% | Global, concentrated in North America, APAC core | Short term (≤ 2 years) |

| Investments in smart grids & T&D modernisation | +1.2% | Global, spill-over to developing economies | Long term (≥ 4 years) |

| Stringent global power-quality standards (IEEE 519, EN 50160) | +0.9% | Global, with regulatory enforcement in EU & North America | Medium term (2-4 years) |

| Electrification of marine vessels driving harmonic-mitigation demand | +0.6% | Global, with early gains in Norway, Netherlands, Singapore | Long term (≥ 4 years) |

| On-site green-hydrogen electrolysers needing ultra-clean power | +0.4% | EU, Australia, Middle East, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of sensitive electronics in Industry 4.0 processes

Precision manufacturing lines now rely on sub-microsecond timing and AI-driven controls that tolerate minimal voltage variation. The 2024 reapproval of SEMI F47 sag-immunity rules intensified demand for dynamic voltage restorers and active filters able to act within milliseconds [1]SEMI, “SEMI F47 Voltage Sag Immunity Standard Reapproved,” semi.org. Downtime risk in semiconductor fabs and automotive plants elevates power continuity from a maintenance cost to a competitive differentiator. As factories embed more machine-learning models, continuous clean power becomes essential for algorithmic accuracy, boosting the power quality equipment market.

Expansion of data centers requiring high-availability power

Rack densities trending toward 1 MW and liquid-cooled AI clusters impose tight ±1% voltage-regulation targets legacy UPS topologies struggle to meet. Hyperscale operators deploy modular architectures that distribute filtering and battery functions, eliminating single points of failure while cutting losses [2]Vertiv, “Data Center Trends 2025,” vertiv.com. Cooling pumps and in-row heat exchangers add harmonic distortion, heightening demand for active filters. With data centers now absorbing 3-4% of global electricity, intelligent power distribution that adapts to real-time workloads is reshaping the power quality equipment market.

Investments in smart grids and T&D modernisation

Utility distribution-system spending climbed to USD 50.9 billion in 2023, and storage outlays jumped sevenfold within a year, catalyzing the adoption of STATCOMs and advanced voltage regulators [3]U.S. Energy Information Administration, “Grid Infrastructure Investments Drive Increase in Utility Spending,” eia.gov. Dynamic line-rating and grid-forming inverters raise transfer capacity without new lines, but also demand precise harmonic control. Advanced metering infrastructure gives utilities visibility down to the customer meter, enabling targeted power-quality corrections that reinforce the long-term growth of the power quality equipment market.

Stringent global power-quality standards (IEEE 519, EN 50160)

IEEE 519’s 2022 update tightened current-distortion limits at the point of common coupling, pushing manufacturers and utilities to adopt real-time monitoring with automated corrective actions. Field studies show 37% of U.S. premises breaching harmonic thresholds, signaling latent retrofit demand. EN 50160 complements IEEE rules across Europe, ensuring equipment compatibility in cross-border grids and continuously driving procurement of instruments that verify compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced PQ solutions | -1.1% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Shortage of skilled PQ analysis professionals | -0.8% | Global, acute in APAC and MEA regions | Medium term (2-4 years) |

| Emergence of solid-state transformers reducing stand-alone PQ demand | -0.5% | North America & EU, early adoption markets | Long term (≥ 4 years) |

| OEM active-front-end drives curbing aftermarket filter sales | -0.3% | Global, concentrated in industrial automation hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of advanced PQ solutions

Utility-scale STATCOMs command USD 1-3 million per unit and often require equal amounts for engineering and commissioning, stretching payback periods to five years in some regions. Currency swings and import duties inflate prices further for developing-country buyers. Vendors are countering by modularizing systems, allowing phased upgrades that match budget cycles, while service-based financing converts capital expense into predictable opex streams, yet near-term adoption in the power quality equipment market remains constrained.

Shortage of skilled PQ analysis professionals

Modern installations blend power electronics, controls, and data analytics, but university curricula lag, producing fewer technicians to configure and maintain such systems. Southeast Asian and Gulf firms frequently import expatriate engineers, raising project costs and elongating schedules. Industry certification schemes and vendor academies are expanding, yet the supply-demand gap is projected to persist through 2028, tempering the growth of the power quality equipment industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: UPS Systems Drive Market Leadership

Uninterruptible Power Supply systems held 37.18% of the power quality equipment market in 2025, demonstrating their critical role in safeguarding servers, medical devices, and industrial controllers. Voltage regulators and conditioners lead growth at a 9.62% CAGR to 2031, reflecting the rising sensitivity of electronics to even minor voltage excursions. Smart UPS models with predictive maintenance enhance uptime and cut lifecycle costs, further anchoring segment dominance. Harmonic filters enjoy steady demand amid broader adoption of variable-frequency drives in factories.

Static VAR compensators and STATCOM platforms are gaining traction as grids integrate greater renewable energy, creating opportunities for medium-voltage deployments that stabilize voltage and frequency in real time. Socomec’s 2025 launch of a high-density UPS hitting 99% efficiency underscores how vendors blend space savings with energy gains, reinforcing overall expansion of the power quality equipment market size. Surge-protection devices also benefit from the updated IEC 61643-01:2024 standard, while static transfer switches penetrate mission-critical campuses that cannot tolerate even millisecond disruptions.

By Phase: Three-Phase Dominance in Industrial Applications

Three-phase architectures commanded 60.05% share of the power quality equipment market in 2025 as factories, refineries, and commercial towers favor their higher efficiency and inherent load balancing. Advanced controllers now measure and correct each phase independently, minimizing imbalance and reducing transformer stress. Single-phase units are projected to grow at a 7.12% CAGR, buoyed by home solar inverters and small retail sites where simplicity outweighs efficiency gains.

Residential EV chargers and rooftop PV arrays increasingly specify smart single-phase filters communicating with building-management platforms. Meanwhile, industrial users standardize on three-phase designs to exploit economies of scale in cabling and switchgear as global electrification accelerates, locking in long-term dominance within the power quality equipment market.

By Voltage Class: Medium-Voltage Leadership Reflects Infrastructure Focus

Medium-voltage (1–33 kV) systems accounted for a 52.15% share of the power quality equipment market size in 2025, serving as the interface between high-voltage transmission and low-voltage end use. Distribution feeders experience diverse harmonic sources, prompting utilities to install dynamic VAR devices at substations. Low-voltage products will grow fastest at 8.01% CAGR to 2031 as homes and small businesses add smart loads that demand local conditioning.

High-voltage solutions sustain demand in export-oriented renewables such as offshore wind, illustrated by Hitachi Energy’s STATCOM deployment at Hornsea 4, which anchors voltage on subsea cables . Modular low-voltage gear also gains ground thanks to plug-and-play designs that retrofit into existing panels without shutdowns, sustaining momentum for the broader power quality equipment market.

By Application: Renewable Integration Leads Market Transformation

Renewable-integration and data-center projects jointly captured 32.45% power quality equipment market share in 2025 as grids absorb variable solar- and wind-output while cloud providers demand near-perfect uptime. Grid-forming battery energy-storage systems now deliver energy- and power-quality services, bridging intermittent generation with sensitive digital loads.

EV fast-charging infrastructure is forecast to post the highest 9.08% CAGR through 2031, necessitating real-time harmonic suppression to protect adjacent feeders. Oil-and-gas installations maintain resilient demand for rugged power conditioners in remote sites, while marine electrification introduces niche requirements for corrosion-resistant harmonic filters, adding diversity to the power quality equipment industry.

By End-User: Commercial and Industrial Dominance

Commercial and industrial users held a 62.35% share of the power quality equipment market 2025, as downtime in factories or hospitals can cost millions per incident. Utilities, however, are poised for a 7.18% CAGR to 2031, propelled by regulatory incentives to integrate distributed energy resources while guaranteeing voltage quality.

Electric cooperatives now pilot premium-power tariffs that bundle real-time harmonic monitoring, offering differentiated service to high-tech tenants. Residential customers adopt combo inverter-conditioners bundled with rooftop PV and battery packages, widening the user base for the power quality equipment market.

Geography Analysis

Asia-Pacific retained 48.05% market share in 2025 and is set for an 8.22% CAGR through 2031, anchored by China’s USD 88.7 billion 2025 grid investment and India’s renewable expansion that together demand sophisticated conditioning. Regional innovators such as Huawei Digital Power deploy grid-forming storage that marries frequency control with energy arbitrage, accelerating adoption. Japan and South Korea add momentum via semiconductor-driven power-quality upgrades that meet stringent sag-immunity criteria.

North America ranks second, buoyed by hyperscale data-center builds and USD 1.42 billion utility modernization plans in Pennsylvania that emphasize advanced voltage regulation. Federal tax incentives for grid-hardening intensify spending on STATCOMs and harmonic filters, while Canada’s HVDC research investments cultivate indigenous expertise, thereby reinforcing regional demand in the power quality equipment market.

Europe focuses on renewable integration and industrial decarbonization, exemplified by Germany’s first 300 MVAr grid-forming STATCOM that stabilizes a wind-heavy network. EN 50160 compliance pressures commercial sites to deploy permanent monitoring. The EU’s energy-independence agenda fosters procurement of efficient power-quality devices that squeeze losses from electrified industrial clusters, sustaining steady expansion of the power quality equipment market.

Competitive Landscape

The power quality equipment market exhibits moderate consolidation as Schneider Electric, ABB, Eaton, and Siemens collectively leverage global plants and broad portfolios to secure multinational projects. Incumbents increasingly bundle cloud analytics with hardware, transforming products into subscription-based platforms that predict failures and automate service dispatch.

Strategic alliances and selective acquisitions intensify: Eaton’s 2025 tie-up with Siemens Energy accelerates turnkey data-center deployments, while ABB’s purchase of SEAM Group extends lifecycle services across North American sites. Asian challengers exploit cost advantages and state backing to penetrate emerging markets, pressuring traditional margins and pushing incumbents toward higher-value software layers.

Component shortages since 2023 prompted heavy capital injections: Hitachi Energy committed an extra USD 250 million for transformer capacity, and HD Hyundai Electric announced USD 274 million to expand U.S. and Korean plants. These moves underscore a strategic race to localize production near high-growth demand centers, further shaping competition within the power quality equipment industry.

Power Quality Equipment Industry Leaders

Siemens AG

Schneider Electric SE

Eaton Corporation plc

ABB Ltd / Hitachi Energy (combined FACTS)

Vertiv Holdings Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy is investing USD 250 million to boost global production of key components for electrical transformers. This includes ramping production capacity at its transformer factories in Virginia, Missouri, and Mississippi.

- February 2025: In a bid to tackle the persistent transformer shortage and cater to the surging demand from utilities, major commercial enterprises, industrial sites, and data centers, Eaton has unveiled plans for a USD 340 million investment. The investment will fund a state-of-the-art, three-phase transformer manufacturing facility in Jonesville, South Carolina. The facility is set to commence production in 2027.

- January 2025: GE Vernova is investing over USD 10 million to boost production of its FLEXINVERTER, a pivotal technology for utility-scale solar and energy storage, at its Pittsburgh facility.

- January 2025: Schneider Electric has unveiled Schneider Charge Pro, an innovative EV charging solution tailored for commercial fleets and multifamily residences. Emphasizing dynamic load management, this initiative seeks to boost EV adoption through a seamless, energy-efficient, intuitive charging experience.

Global Power Quality Equipment Market Report Scope

Power quality equipment are commonly electrical filters that remove or reduce the level of harmful harmonics and re-shape the sinewave for the longevity of operation of electrical systems. Power quality equipment is used in power grids to ensure a continuous flow of stable power.

The market is segmented by Equipment, Phase, End-User, and Geography. By equipment, the market is segmented by Uninterruptable Power Supply (UPS), Harmonic filters, Static VAR compensators, Power quality meters, and other equipment types; by Phase, the market is segmented into Single phase and Three phases. By end users, the market is segmented into Industrial and Manufacturing, Commercial, and others. The report also covers the market size and forecasts for power quality equipment across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Uninterruptible Power Supply (UPS) |

| Harmonic Filters |

| Static VAR Compensators (SVC/STATCOM) |

| Power Quality Meters |

| Surge Protection Devices |

| Active Power Filters |

| Static Transfer Switches |

| Voltage Regulators and Conditioners |

| Other Equipment Types |

| Single-Phase |

| Three-Phase |

| Low Voltage (Below 1 kV) |

| Medium Voltage (1 to 33 kV) |

| High Voltage (Above 33 kV) |

| Renewable Integration |

| Automation and Robotics |

| EV Fast-Charging Infrastructure |

| Oil and Gas Operations |

| Marine and Offshore Platforms |

| Others |

| Utilities |

| Commercial and Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Equipment Type | Uninterruptible Power Supply (UPS) | |

| Harmonic Filters | ||

| Static VAR Compensators (SVC/STATCOM) | ||

| Power Quality Meters | ||

| Surge Protection Devices | ||

| Active Power Filters | ||

| Static Transfer Switches | ||

| Voltage Regulators and Conditioners | ||

| Other Equipment Types | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Voltage Class | Low Voltage (Below 1 kV) | |

| Medium Voltage (1 to 33 kV) | ||

| High Voltage (Above 33 kV) | ||

| By Application | Renewable Integration | |

| Automation and Robotics | ||

| EV Fast-Charging Infrastructure | ||

| Oil and Gas Operations | ||

| Marine and Offshore Platforms | ||

| Others | ||

| By End-User | Utilities | |

| Commercial and Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current power quality equipment market size and projected growth?

The power quality equipment market size is USD 20.3 billion in 2026 and is forecast to reach USD 28.26 billion by 2031 at a 6.83% CAGR.

Which equipment category leads global revenues?

Uninterruptible Power Supply systems dominate with 37.18% market share in 2025, reflecting their central role in protecting digital infrastructure.

Which application area is expanding fastest?

EV fast-charging infrastructure is projected to grow at 9.08% CAGR between 2026 and 2031 as electric-vehicle adoption accelerates.

Why is Asia-Pacific the largest regional market?

Record grid investments in China and aggressive renewable build-outs in India push Asia-Pacific to 48.05% share and the highest 8.22% CAGR.

What major restraint could slow adoption?

High upfront costs of advanced solutions, especially STATCOMs and dynamic filters, limit near-term uptake among price-sensitive users.

How are vendors addressing the skills gap in power quality analysis?

Manufacturers have launched global training academies and certification programs to expand the pool of qualified engineers capable of deploying modern systems.

Page last updated on: