Transformer Monitoring System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

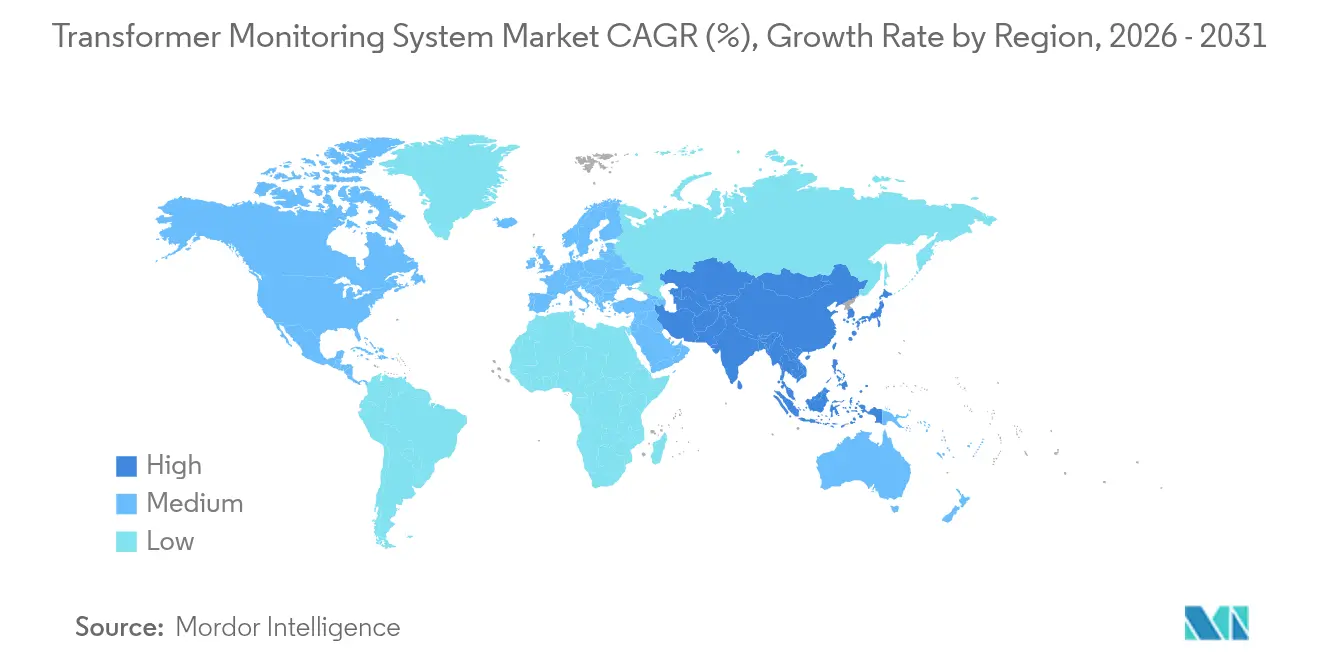

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

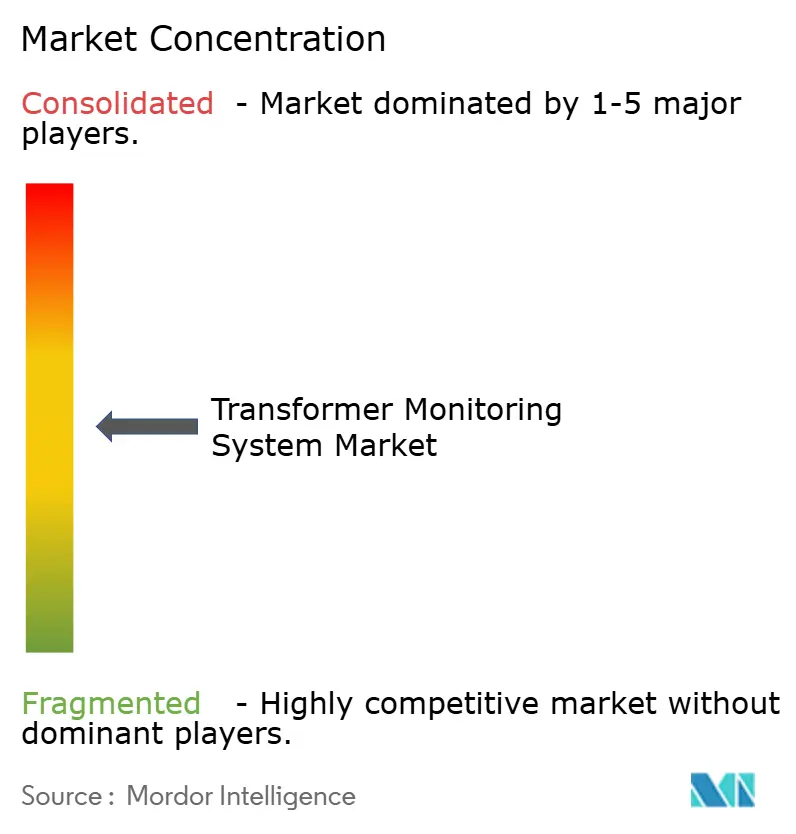

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transformer Monitoring System Market Analysis by Mordor Intelligence

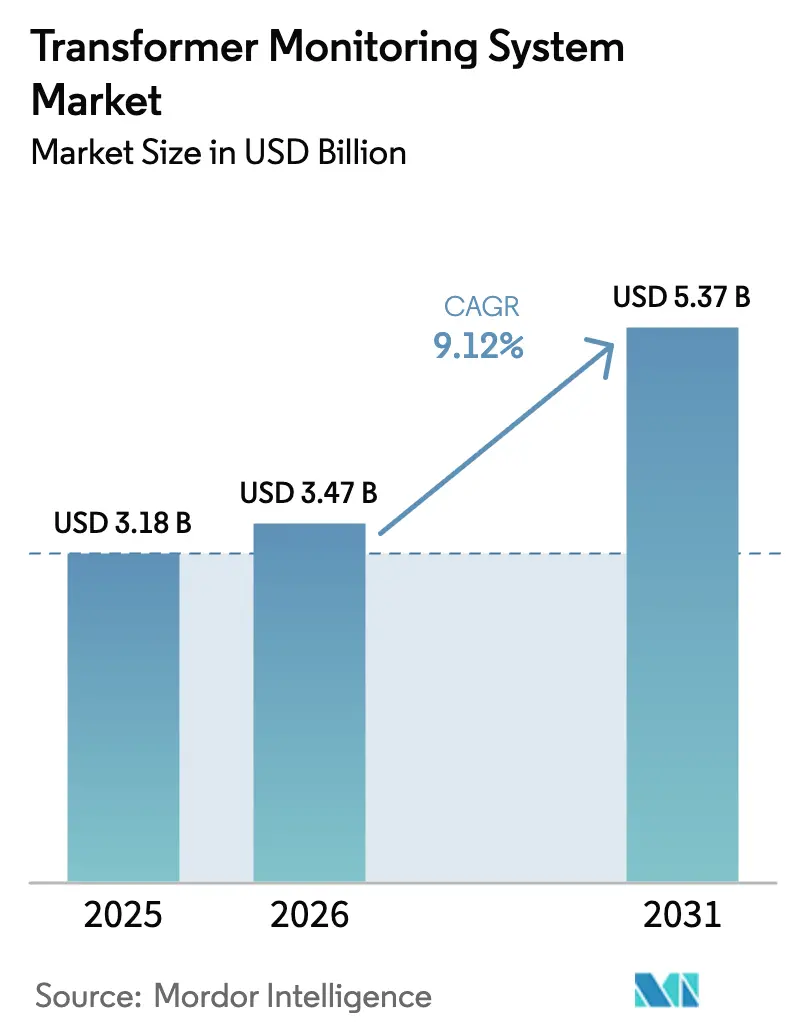

The Transformer Monitoring System market size is expected to grow from USD 3.18 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 5.37 billion by 2031 at 9.12% CAGR over 2026-2031.

Rising grid-digitalization mandates and the operational stress introduced by variable renewables are prompting utilities to favor condition-based maintenance over calendar schedules. Analytics-driven insights that avert a single forced outage on a 230 kV unit can save utilities close to USD 1 million, making monitoring investments compelling even in rate-regulated environments.[1]Transformer Monitoring Systems: Standards and Applications, IEEE Xplore Digital Library, ieee.org Continuous dissolved-gas, temperature, and partial-discharge sensing now dominate new deployments because they capture transient fault signatures that periodic oil sampling misses. Software platforms that ingest these data streams are growing faster than sensors as utilities seek fleet-wide benchmarking and AI-assisted diagnostics. Moderate supplier concentration leaves space for niche innovators that specialize in ultra-sensitive gas detection or cyber-secure edge gateways.

Key Report Takeaways

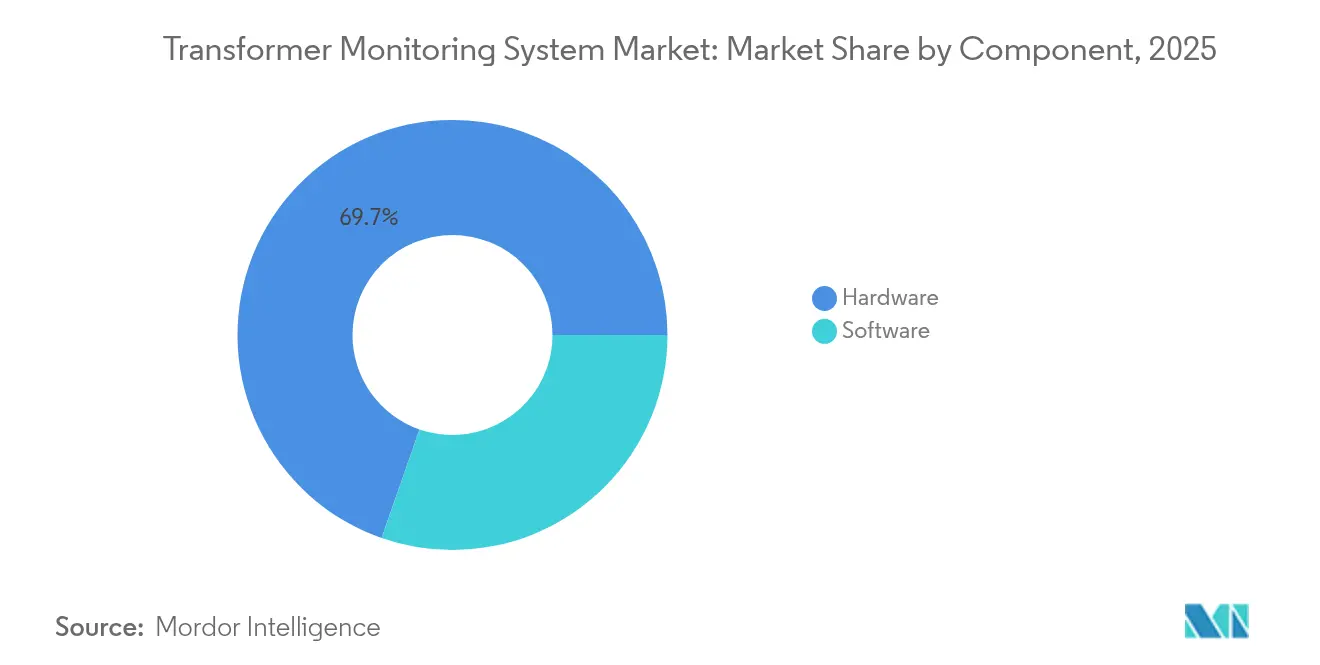

- By component, hardware led with 69.65% transformer monitoring systems market share in 2025, whereas software platforms are forecast to expand at a 11.85% CAGR through 2031.

- By monitoring type, online continuous systems captured 64.40% of the transformer monitoring systems market size in 2025 and are advancing at a 10.05% CAGR to 2031.

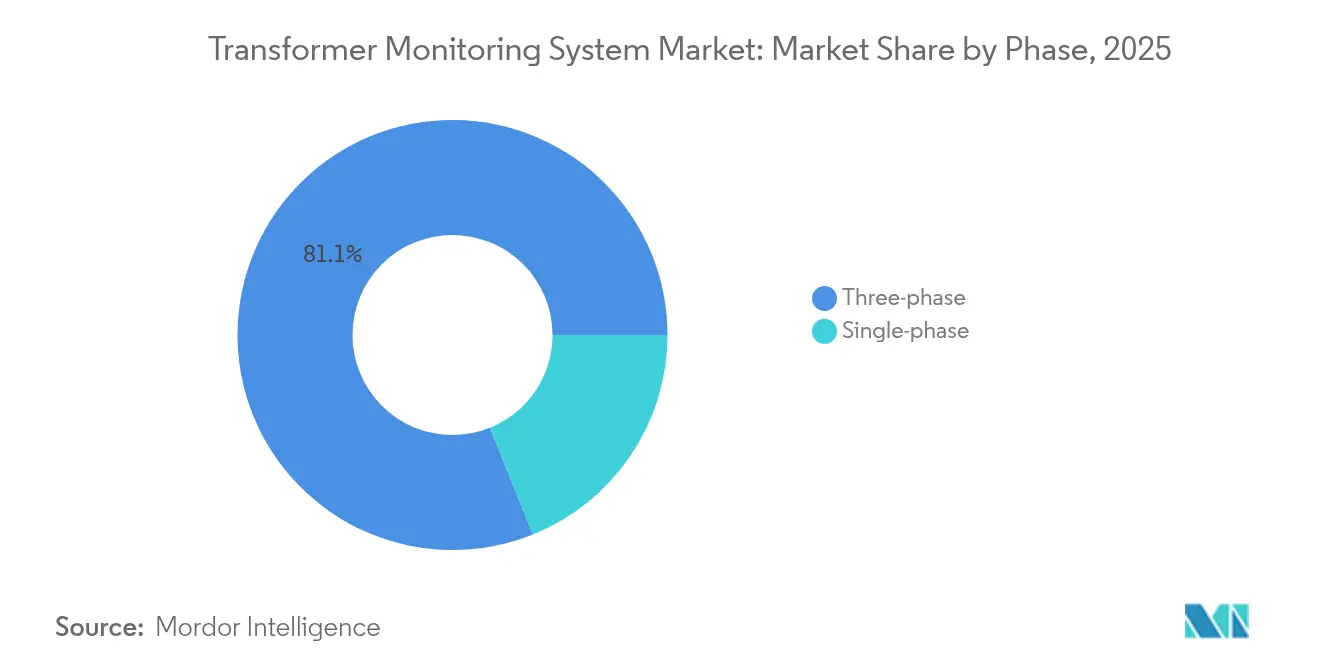

- By phase, three-phase installations dominated with an 81.10% share in 2025 and will rise at a 9.90% CAGR.

- By deployment mode, edge-based architectures accounted for 51.30% of 2025 revenue, yet cloud and hybrid modes are set to grow at a 12.65% CAGR.

- By transformer type, power units above 72.5 kV commanded 60.00% of the transformer monitoring systems market size in 2025, whereas specialty HVDC and traction transformers will surge at a 11.95% CAGR.

- By service, oil and dissolved-gas analysis held 37.70% revenue share in 2025, while partial-discharge monitoring records the highest projected CAGR at 10.55% through 2031.

- By end-user, power utilities controlled 56.80% demand in 2025, but industrial buyers are the fastest mover with a 12.05% CAGR.

- By geography, Asia-Pacific generated 38.20% of global revenue in 2025 and is projected to lead growth at a 10.20% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transformer Monitoring System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated grid digitalization mandates | +2.3% | Global, with early adoption in North America, EU, China | Medium term (2-4 years) |

| Surge in renewable-energy integration | +2.1% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Utility cap-ex to replace aging fleets | +1.8% | North America & EU, selective APAC markets | Long term (≥4 years) |

| AI-driven outage prevention for data centers | +1.5% | North America, Western Europe, Singapore | Short term (≤2 years) |

| Cyber-resilient edge analytics modules | +1.4% | Global, with priority in North America, EU, Australia | Short term (≤2 years) |

| National-security push amid transformer shortage | +1.2% | North America, EU, India, with strategic focus on domestic manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Grid Digitalization Mandates

Utilities are upgrading substations with real-time telemetry to meet new policy requirements. The U.S. Grid Modernization Initiative set aside USD 3.5 billion in 2024 for advanced metering and mandated condition-based monitoring for transformers above 100 MVA. China’s 14th Five-Year Plan requires digital twins for every 500 kV substation by 2025, driving thousands of dissolved-gas and partial-discharge sensor retrofits.[2]Smart Grid Development and Investment, State Grid Corporation of China, sgcc.com.cn Europe’s Clean Energy Package compels transmission operators to publish asset-health indices by 2026, forcing the adoption of cloud monitoring platforms that aggregate cross-border data. India links federal funding under the Revamped Distribution Sector Scheme to smart-feeder automation, indirectly making transformer monitoring a prerequisite.[3]Revamped Distribution Sector Scheme, Ministry of Power India, powermin.gov.in These policies shift monitoring from discretionary spending to compliance-driven investment, anchoring long-term demand in the transformer monitoring systems market.

Surge in Renewable-Energy Integration

Variable wind and solar resources introduce voltage flicker, harmonic distortion, and frequent tap-changer operations that accelerate insulation aging. National Renewable Energy Laboratory tests showed that transformers serving solar farms experience 40% more tap-changer cycles than conventional feeders. IEEE 2800-2022 now recommends online temperature and dissolved-gas monitoring at substations where inverter-based resources exceed 30% penetration. Australia’s grid operator enforced dynamic thermal ratings for wind-zone transformers in 2024, requiring real-time fiber-optic sensors. India targets 500 GW renewables by 2030, creating a pipeline of 15,000 new grid-scale transformers that will be monitored from commissioning. Renewable variability thus feeds a feedback loop: faster aging raises the value proposition of continuous monitoring, expanding the transformer monitoring systems market.

Utility Cap-Ex to Replace Aging Fleets

Over half of North American transmission transformers have passed their 30-year design life, yet wholesale replacement is cost-prohibitive. Utilities like Duke Energy plan to spend USD 2.1 billion through 2029 to replace select units and retrofit others with online monitoring. Germany’s grid operators earmarked EUR 18 billion (USD 19.4 billion) through 2030 for 3,500 new transformers plus retrofits on 2,000 legacy units. Monitoring extends service life by a decade at roughly 5% of replacement cost, freeing capital for new capacity additions. This dual need for greenfield and brownfield solutions ensures steady revenue growth for the transformer monitoring systems market.

AI-Driven Outage Prevention for Data Centers

Hyperscale data centers place a premium on reliability. Microsoft operates 300 facilities, each with redundant 138-230 kV transformers analyzed by edge AI that predicts failures 72 hours ahead. Google reported a 63% cut in unplanned outages after correlating partial-discharge data with weather patterns. Amazon will apply Hitachi Energy’s Lumada APM across 50 new campuses, aiming to halve transformer downtime. High willingness to pay in this segment accelerates the adoption of advanced analytics that later diffuses into utility fleets, deepening the transformer monitoring systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation & calibration cost | -1.2% | Emerging markets in South America, Africa, Southeast Asia | Short term (≤2 years) |

| Legacy-system interoperability gaps | -0.9% | North America, Europe (utilities with 1980s-era SCADA) | Medium term (2-4 years) |

| Analytics-skills talent shortage | -0.8% | Global, acute in North America, EU, Japan | Long term (≥4 years) |

| Cyber-attack surface expansion (IoT) | -0.7% | Global, with heightened concern in North America, EU, critical infrastructure sectors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Installation & Calibration Cost

Comprehensive online monitoring can cost USD 50,000-83,000 per transformer, dominated by sensor and gateway expenses. Annual calibration adds 10-15%, while service contracts run another USD 10,000-15,000. Smaller utilities in Latin America and Africa operate under cap-ex caps and often postpone investment.[4]Electricity Regulation in Emerging Markets 2024, World Bank, worldbank.org Vendors now offer tiered packages, but the up-front burden still slows penetration in cost-sensitive regions of the transformer monitoring systems market.

Legacy-System Interoperability Gaps

Utilities with 1980s SCADA face bandwidth and cybersecurity limits that hinder real-time data integration. An IEEE 2024 survey found 42% of North American operators view protocol incompatibility as the top barrier to deploying cloud-connected monitors. Upgrading to IEC 61850 devices may cost USD 30,000-50,000 per bay, nearly matching a new monitoring suite.[5]Oil-Filled Electrical Equipment – Sampling of Gases, IEC 60567, iec.ch European operators must also satisfy NIS2 encryption rules by 2025, adding firmware upgrade costs. Scarce engineers fluent in both legacy relay logic and RESTful APIs exacerbate hurdles, tempering growth for the transformer monitoring systems market in mature grids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Outpace Hardware Growth

Software revenues are set to grow at a 11.85% CAGR, the fastest among component segments, as utilities shift from sensor proliferation to analytics-focused asset optimization. Hardware dominated with 69.65% of 2025 revenue because every deployment still needs dissolved-gas, bushing, and thermal sensors. Moving workloads to the cloud trims server costs and supports fleet-level benchmarking; Southern Company cut mean time to diagnosis by 38% after migrating 4,200 transformers to a centralized dashboard. The transformer monitoring systems market size for software is forecast to climb in tandem with SaaS adoption. Sensor innovation also continues: a photoacoustic hydrogen detector released in 2024 halves detection thresholds, strengthening the hardware value proposition.

Utilities in jurisdictions such as China, where data sovereignty rules prevail, keep critical telemetry on-premises, preserving demand for local servers. Meanwhile, edge gateways now house neural-network inference engines that flag anomalies in seconds, mitigating latency risk for mission-critical assets. The evolving blend of edge inference and cloud analytics underpins balanced growth across both component categories in the transformer monitoring systems market.

By Monitoring Type: Continuous Systems Dominate Amid Renewable Volatility

Online continuous monitoring controlled 64.40% of 2025 installations and is growing at a 10.05% CAGR as variable generation magnifies the cost of missed transient events. The transformer monitoring systems market size attached to continuous systems benefits from standards such as IEEE C57.145-2020 that recommend round-the-clock sensing for high-load or renewable-linked transformers. Utilities like Duke Energy now mandate continuous dissolved-gas and partial-discharge coverage for every new transmission unit.

Offline approaches persist for low-criticality feeders or seasonal industrial loads where outages carry limited financial penalties. Hybrid offerings emerge to bridge the gap: “sentinel mode” sensors perform continuous analysis only during peak months, cutting storage needs by 30%. Continuous systems, however, will remain the reference architecture for high-value assets, anchoring long-run growth in the transformer monitoring systems market.

By Phase: Three-Phase Units Dominate Industrial and Utility Segments

Three-phase transformers accounted for 81.10% of 2025 deployments and will expand at a 9.90% CAGR, reflecting their prevalence in transmission grids, data centers, and industrial plants. Multi-phase configurations require multiple sensor sets but enable phase-differential analysis that pinpoints localized faults, enhancing diagnostic accuracy. Taiwan Semiconductor Manufacturing Company deploys real-time thermal imaging on 1,200 three-phase units to maintain near-perfect uptime. Single-phase monitoring gains ground in residential solar circuits under California Rule 21, yet its revenue contribution stays modest. The dominance of three-phase assets, therefore, anchors volume and value growth for the transformer monitoring systems market.

By Deployment Mode: Cloud Architectures Accelerate Despite Cybersecurity Concerns

Edge-centric installations held a 51.30% share in 2025, yet cloud and hybrid modes will climb at a 12.65% CAGR, the fastest among deployment schemes. Centralized analytics unlock fleet-wide learning: Hitachi Energy’s Lumada APM uses federated learning to refine models across multiple operators without sharing raw data, easing privacy risk. Exelon will invest USD 450 million to weave real-time transformer data into its upgraded SCADA, exemplifying large-scale cloud adoption.

Cyber rules such as NERC CIP-013 add cost and complexity, but vendors now embed zero-trust encryption and secure boot features in gateways, bolstering confidence. Hybrid designs that marry local inference with cloud trend analysis balance latency and security, solidifying momentum for the transformer monitoring systems market.

By Transformer Type: Specialty Units Lead Growth Amid HVDC Expansion

Power transformers above 72.5 kV generated 60.00% of unit demand in 2025 because they sit at critical grid nodes. Yet specialty HVDC, traction, and phase-shifting transformers will outpace at 11.95% CAGR as cross-border interconnectors and metro rail systems proliferate. The North Sea Wind Power Hub alone will need hundreds of converter transformers monitored around the clock to avoid valve-hall outages that can curtail gigawatt-scale flows. Hitachi Energy observed gas levels rise three times faster in HVDC units, validating the need for high-frequency dissolved-gas sampling. Growth in specialty segments thus elevates average system value in the transformer monitoring systems market.

Distribution-level monitoring remains fragmented, but India’s RDSS mandate for 33 kV and 11 kV feeders signals future upside. Together, these trends diversify revenue across transformer classes within the transformer monitoring systems market.

By Service: Partial-Discharge Monitoring Gains as Insulation Ages

Oil and dissolved-gas analysis still leads with 37.70% share, reflecting decades of field validation. Yet partial-discharge services are growing fastest at 10.55% CAGR because corona and arcing signals precede catastrophic failures. Saudi Electricity Company trimmed winding failures by 52% after installing fiber-optic temperature probes that trigger load shedding ahead of thermal limits. High-frequency ultrasonic and transient earth voltage sensors now detect discharges on heavily loaded lines, enabling planned replacements during off-peak windows and reinforcing the transformer monitoring systems market.

Bushing diagnostics and hot-spot measurements also find traction as utilities chase comprehensive health indices. Standards such as IEEE C57.104 keep dissolved-gas analysis central, but multi-modal sensor fusion is becoming the industry norm, increasing average revenue per transformer in the transformer monitoring systems market.

By End-User: Industrial Segment Accelerates on Data-Center Demand

Power utilities retained 56.80% of 2025 demand, but the industrial segment is moving fastest at 12.05% CAGR because data centers, semiconductor fabs, and mining sites cannot tolerate outages. Microsoft will spend USD 250 million to retrofit 1,500 data-center transformers by 2026. BHP plans to monitor 300 units at Chilean copper mines, preventing production stoppages that can cost USD 1 million daily. Hospitals, airports, and financial hubs also adopt targeted monitoring, enlarging the customer base and boosting the transformer monitoring systems market.

Geography Analysis

Asia-Pacific generated 38.20% of global revenue in 2025 and is set to grow at a 10.20% CAGR, the fastest rate worldwide. State Grid Corporation invests USD 58 billion yearly in grid upgrades, including 12,000 retrofits completed in 2024. India allocates INR 3.03 lakh crore (USD 36.4 billion) to modernize feeders and substations, tying funds to online sensor deployment. Japan earmarked JPY 120 billion (USD 800 million) for seismic-triggered monitoring after the 2024 Noto earthquake. South Korea targets 100% coverage of transformers above 154 kV by 2027. ASEAN’s cross-border grid requires harmonized standards, further enlarging the transformer monitoring systems market in the region.

North America held about a 28.10% share in 2025, buoyed by DOE’s USD 3.5 billion modernization grants and data-center expansion. NREL reports that 55% of U.S. transformers exceed 33 years, creating a dual market for replacements and retrofits. Canada’s 30% clean-electricity tax credit spurs utility investment, and Mexico’s CFE will monitor 1,200 transformers on cross-border lines to meet NERC reliability rules. Edge AI deployments in hyperscale campuses add incremental demand, supporting steady growth in the transformer monitoring systems market.

Europe accounted for roughly 21.70% in 2025. ENTSO-E’s asset-health disclosure rules, Germany’s EUR 18 billion grid plan, and the massive North Sea Wind Power Hub underpin strong spending. France’s RTE will retrofit 1,800 units with fiber-optic sensors by 2028, focusing on substations near nuclear plants. Cyber mandates under NIS2 and IEC 62351 favor established vendors, shaping procurement in the transformer monitoring systems market.

South America, the Middle East, and Africa collectively represented around 12.00% of 2025 revenue. Rapid solar growth in Brazil, Saudi Arabia’s NEOM project, and Eskom’s stabilization program are bright spots, yet high capital costs and interoperability challenges cap broader uptake. Tiered sensor packages and vendor-financed models may unlock latent demand, extending the transformer monitoring systems market footprint.

Mordor Intelligence provides coverage of the transformer monitoring system market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The transformer monitoring systems market features moderate concentration. The top five suppliers, Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, and Eaton, together hold about a 45% share. Platform-oriented vendors bundle sensors, gateways, and cloud analytics, aiming for 60% software margins, while specialists excel in single modalities such as ultra-sensitive gas detection or cyber-secure relays. Hitachi Energy’s Lumada APM leverages federated learning to refine models without exposing raw data, winning a 50-site AWS contract in 2024. Siemens Energy’s Sensformer Gen3 embeds a neural-network engine that flags anomalies within five seconds, removing cloud latency. Schneider acquired Aurtra to bolster AI-driven diagnostics and reported 34% software revenue growth in 2024.

Disruptors like Gasera introduced a mid-infrared laser DGA sensor detecting acetylene at 0.1 ppm and priced 30% below incumbents, securing Nordic pilots. Rugged Monitoring filed a U.S. patent for an edge AI accelerator embedded in DGA sensors that reduces transmission costs by 80%. Regulatory cybersecurity requirements such as IEC 62443 and NERC CIP-013 favor vendors with mature OT-security stacks, raising entry barriers for newcomers from low-cost regions. Overall, innovation in sensor fusion and secure cloud analytics will define competitive edges in the transformer monitoring systems market.

Transformer Monitoring System Industry Leaders

Hitachi Energy (ABB)

Siemens Energy AG

General Electric Vernova

Schneider Electric SE

Qualitrol (Fortive)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hitachi Energy invested USD 22.5 million to enlarge dry-type transformer capacity in Virginia, adding 120 jobs.

- March 2025: Hitachi Energy committed USD 250 million through 2027 to expand transformer component output, alleviating supply shortages.

- March 2025: Schneider Electric launched the AI-driven One Digital Grid Platform, claiming outage cuts of up to 40%.

- March 2025: Schneider Electric unveiled a USD 700 million US expansion plan to bolster digitalization and automation.

Global Transformer Monitoring System Market Report Scope

A transformer monitoring system is a specialized electrical utility device equipped with sensors that collect, process, and measure information relative to the current flowing through a distribution or power transformer. The transformer monitoring system market report includes:

| Software | On-premise Suites |

| Cloud-based SaaS | |

| Hardware | Sensors and IEDs |

| Communications and Gateways |

| Online Continuous |

| Offline/Periodic |

| Single-phase |

| Three-phase |

| Edge (On-site) |

| Centralised Utility SCADA |

| Cloud/Hybrid |

| Power Transformers (Above 72.5 kV) |

| Distribution Transformers (Up to 72.5 kV) |

| Specialty (HVDC, Traction) |

| Oil/Dissolved-Gas Analysis |

| Winding Hot-Spot |

| Bushing Condition |

| Partial-Discharge |

| Thermal and Load |

| Power Utilities |

| Industrial |

| Commercial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Software | On-premise Suites |

| Cloud-based SaaS | ||

| Hardware | Sensors and IEDs | |

| Communications and Gateways | ||

| By Monitoring Type | Online Continuous | |

| Offline/Periodic | ||

| By Phase | Single-phase | |

| Three-phase | ||

| By Deployment Mode | Edge (On-site) | |

| Centralised Utility SCADA | ||

| Cloud/Hybrid | ||

| By Transformer Type | Power Transformers (Above 72.5 kV) | |

| Distribution Transformers (Up to 72.5 kV) | ||

| Specialty (HVDC, Traction) | ||

| By Service | Oil/Dissolved-Gas Analysis | |

| Winding Hot-Spot | ||

| Bushing Condition | ||

| Partial-Discharge | ||

| Thermal and Load | ||

| By End-User | Power Utilities | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global transformer monitoring systems market by 2031?

The market is expected to reach USD 5.37 billion by 2031.

Which component category is growing fastest in transformer monitoring?

Software platforms are forecast to grow at a 11.85% CAGR between 2026 and 2031.

Why are continuous monitoring systems gaining preference over periodic sampling?

Variable renewable generation causes transient stresses that only online sensors can capture, leading utilities to favor continuous systems.

Which region will lead market growth through 2031?

Asia-Pacific will post the highest regional CAGR at 10.20%, supported by large-scale grid investments.

How are data centers influencing demand for transformer monitoring?

Hyperscale facilities require 99.999% uptime and invest heavily in AI-driven monitoring to avert outages that can cost millions per hour.

What are the main cybersecurity standards affecting transformer monitoring deployments?

IEC 62443 and NERC CIP-013 mandate secure design and supply-chain risk management for connected monitoring devices.

Page last updated on: