Powder Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

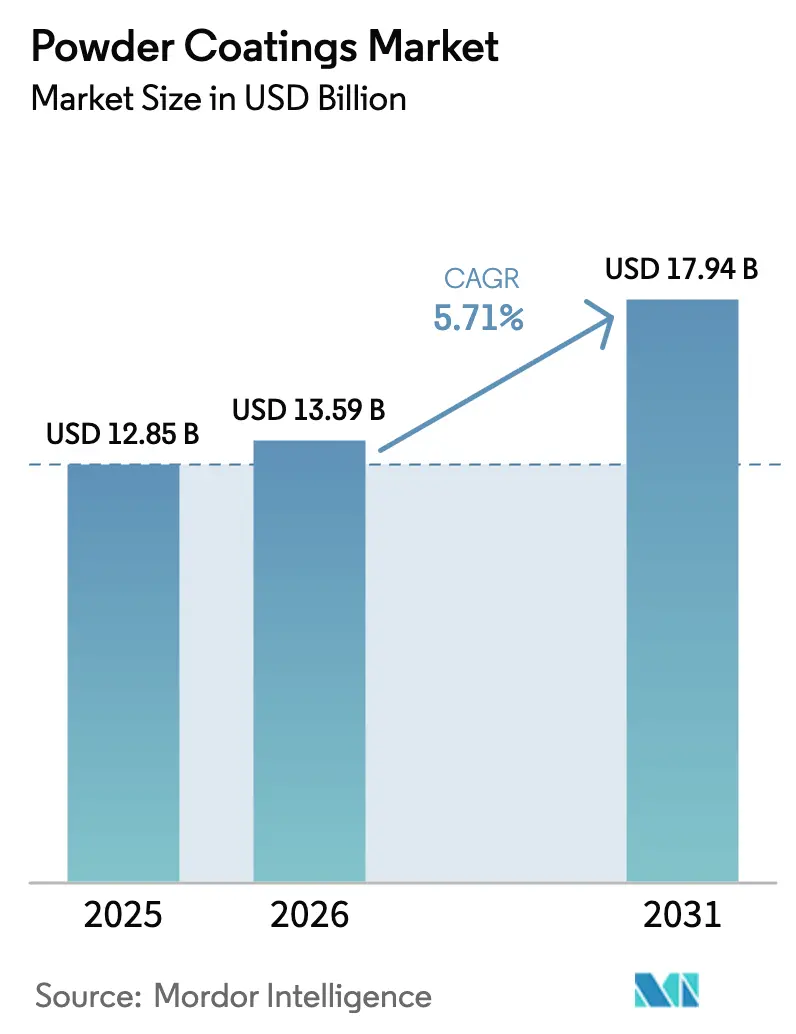

| Market Size (2026) | USD 13.59 Billion |

| Market Size (2031) | USD 17.94 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Powder Coatings Market Analysis by Mordor Intelligence

The Powder Coatings Market size is projected to expand from USD 12.85 billion in 2025 and USD 13.59 billion in 2026 to USD 17.94 billion by 2031, registering a CAGR of 5.71% between 2026 to 2031. Momentum stems from regulatory tailwinds that narrow the cost gap with liquid finishes, robust appliance output in Southeast Asia, and expanded use of medium-density fiberboard (MDF) enabled by low-temperature chemistries. Polyester formulations remain the workhorse for exterior durability, while thermoplastic grades are carving niches where recyclability is paramount. Capacity additions in Vietnam, China, and the United States illustrate an industry pivot toward regional hubs that shorten lead times and reduce embedded emissions. Feedstock inflation and thin-film application hurdles temper growth but have not derailed capital spending on new automated spray lines.

Key Report Takeaways

- By resin type, polyester led with 39.18% of powder coatings market share in 2025 and is forecast to expand at a 6.29% CAGR to 2031.

- By coating type, thermoset chemistries captured 91.05% revenue in 2025, while thermoplastic grades are advancing at a 6.17% CAGR through 2031.

- By end-use industry, the industrial segment held 44.46% of demand in 2025 and is progressing at the fastest 6.42% CAGR to 2031.

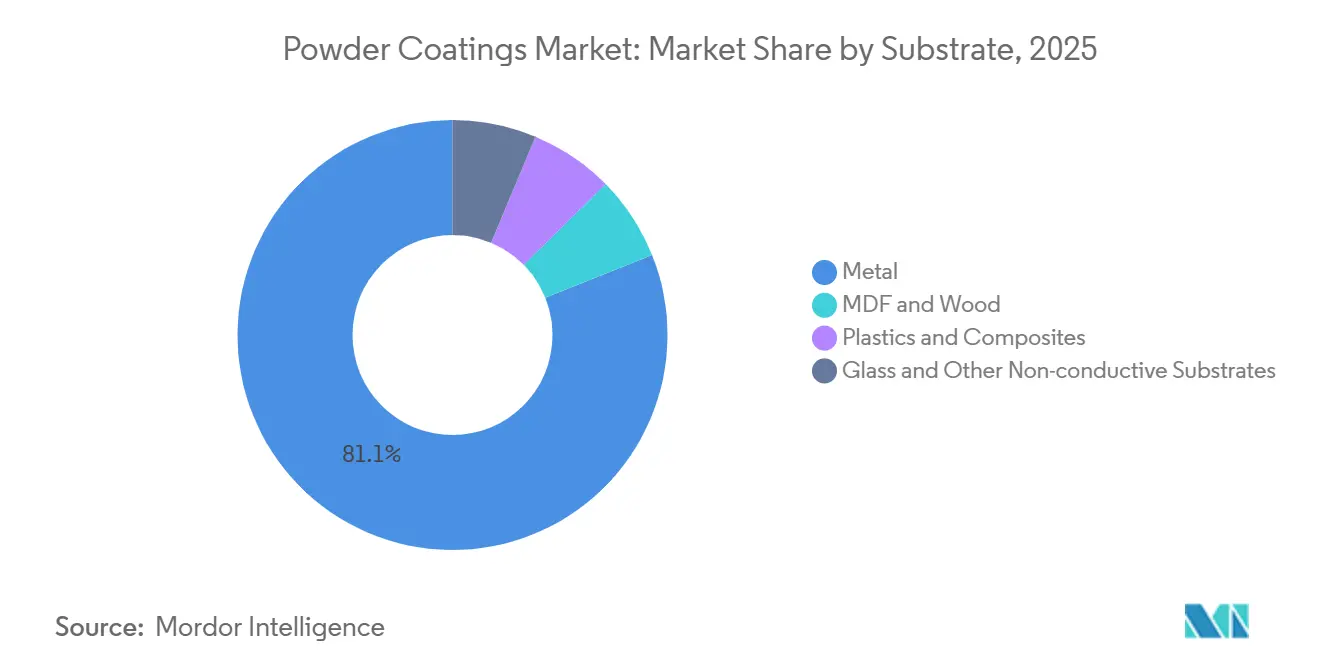

- By substrate, metal accounted for 81.08% volume in 2025, whereas MDF and wood are pacing ahead at a 6.16% CAGR to 2031.

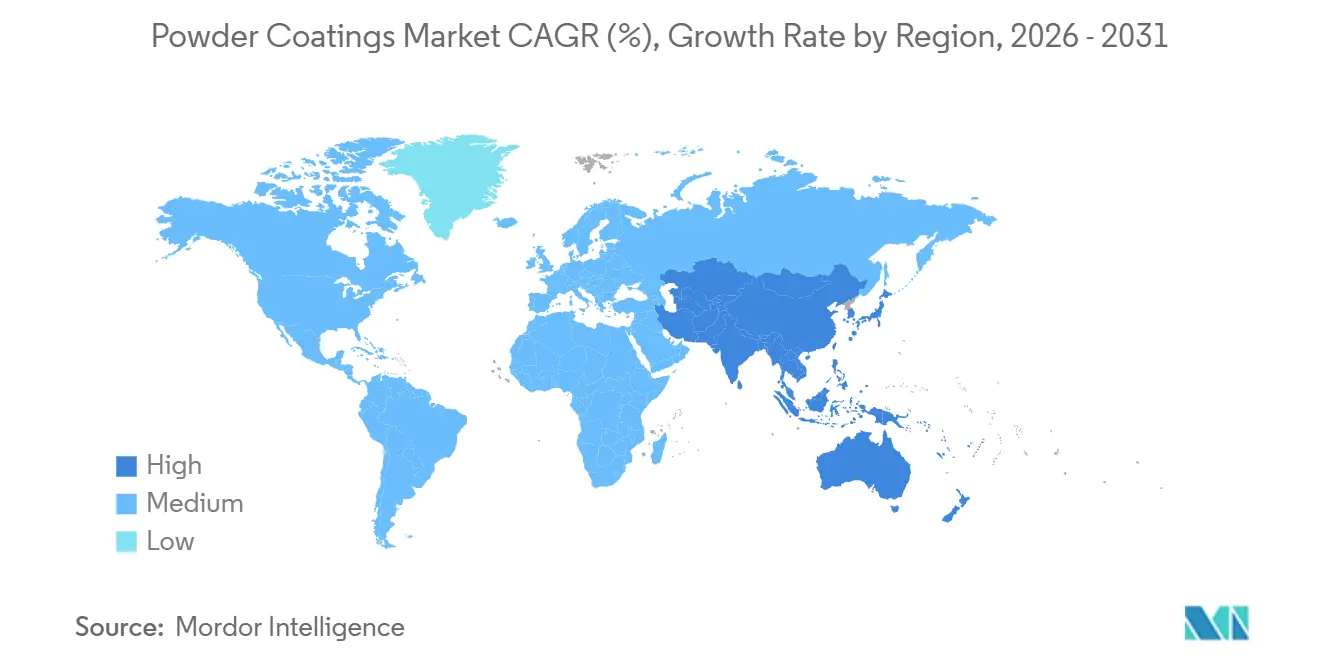

- By geography, Asia-Pacific dominated with a 55.65% share in 2025 and is tracking a 5.91% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Powder Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and carbon-pricing rules accelerating solvent-free finishes | +1.4% | Europe, North America, China | Medium term (2-4 years) |

| Low-temperature chemistries unlocking MDF and heat-sensitive substrates | +0.9% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| ASEAN appliance build-out fuelled by FDI | +1.2% | ASEAN core (Vietnam, Thailand, Indonesia), spill-over to India | Short term (≤ 2 years) |

| Re-shoring of auto OEM lines | +0.8% | North America, Europe | Medium term (2-4 years) |

| GCC giga-projects spurring architectural aluminium demand | +0.6% | Middle East (Saudi Arabia, UAE), spill-over to North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent VOC And Carbon-Pricing Rules Accelerating Solvent-Free Finishes

Regulations are increasingly favoring powder lines over liquid booths, leading to a reduced total cost of ownership. In December 2024, the U.S. EPA set a VOC content cap at 350 g/L. This move has forced converters to evaluate the cost of abatement hardware against the option of installing powder booths. Meanwhile, in Europe, the Carbon Border Adjustment Mechanism, set to take effect in January 2026, will apply the EU-ETS carbon price to imported metal goods. This has led exporters in Turkey and India to pivot towards powder solutions to sidestep tariffs. In China, provincial subsidies in Jiangsu and Guangdong are covering a portion of powder equipment costs. This initiative aligns with China's 10% VOC-reduction goal under its 14th Five-Year Plan. Thanks to these concerted efforts, the payback period for mid-scale powder installations has been significantly reduced. Additionally, OEMs are adopting solvent-free finishes, bolstering their corporate net-zero commitments and driving the uptake of powder coatings in the furniture, appliance, and transportation industries.

Low-Temperature Chemistries Unlocking MDF And Heat-Sensitive Substrates

Breakthrough formulations now cure at temperatures between 110 °C and 130 °C, enabling their application on engineered wood and select plastics without causing substrate distortion. BASF’s Ultradur High Speed polyester achieves full cross-linking at 130 °C, adhering to ISO 2409 standards on MDF without the need for primers[1]BASF, “Ultradur High Speed Powder Coating Launch,” basf.com. Similarly, Axalta’s AquaEC system performs on polypropylene bumpers at 110 °C, successfully passing ASTM D3359 tape tests[2]Axalta Coating Systems, “AquaEC Low-Bake Technology,” axalta.com. Furniture manufacturers are quick to adapt: IKEA utilized the low-bake powder on its cabinet frames, highlighting energy savings and resolving grain-raising challenges typical of water-borne liquids. While resin costs are higher than standard polyesters, the significant energy and labor savings make a strong case for the technology's long-term growth in decorative panels, office furniture, and automotive interiors.

ASEAN Appliance Build-Out Fueled By FDI

In 2024-2025, Vietnam and Thailand attracted significant investment in the appliance and electronics sector. This surge has birthed a dedicated market for powder coatings, specifically tailored for refrigerator and washing-machine cabinets. Notably, expansions by industry giants Samsung, LG, and Haier have driven this growth. These companies stand to gain a finishing-cost advantage from powder coatings, especially when factoring in waste handling and solvent recovery. In Indonesia, the push for energy efficiency is underscored by the mandatory SNI 8000 labeling. This regulation has heightened the appeal of powder coatings, as their uniform thin films significantly boost thermal insulation in refrigerator liners. While regional capacity is striving to keep pace, challenges remain. PPG's new plant in Binh Duong, inaugurated in April 2025, is grappling with lead times during peak seasons.

Re-Shoring Of Auto OEM Lines

North American and European automakers are increasingly localizing their electric vehicle (EV) platforms, with powder technology playing a pivotal role in their revamped paint shops. General Motors, as part of a significant investment announced in August 2024, is retooling three U.S. plants to incorporate powder-coated battery enclosures and subframes. Ford's Oakville site, which commenced EV production in late 2025, adopted a two-coat powder sequence. This innovation replaces the traditional water-intensive e-coat dip, contributing to water conservation efforts. Across the Atlantic, Volkswagen has transitioned a substantial portion of its Emden underbody processing to powder. This move not only aligns with the tightened VOC limits set by the Industrial Emissions Directive but also underscores the industry's commitment to sustainability. The adoption of shorter cure cycles and reduced bake temperatures further emphasizes powder's integral role in modernizing automotive paint lines, aligning with broader lean manufacturing objectives.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thin-film (less than 25 µm) application limits | -0.7% | Global, most acute in automotive Class-A surfaces | Medium term (2-4 years) |

| UV-cure powders still geometry-restricted | -0.5% | Global, particularly complex automotive and industrial parts | Long term (≥ 4 years) |

| Polyester/epoxy feedstock price volatility | -1.1% | Global, with highest impact in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thin-Film Application Limits Below 25 Microns

Particle size constraints hinder the production of uniform films, preventing the use of powder in premium exterior auto panels and shells of consumer electronics. Powders face challenges with fluidization and electrostatic charge, leading to higher reject rates in automotive audits compared to their liquid counterparts. Sherwin-Williams' resin upgrade in 2025 pushed the viable build down but still falls short of the targets set by automakers. Until advancements are made in thin-film deposition, liquid topcoats will continue to dominate Class-A surfaces, limiting powder's application in categories where appearance is paramount.

UV-Cure Powders Still Geometry-Restricted

While rapid-cure UV powders boost throughput, they struggle with shadowed recesses where light fails to uniformly activate photoinitiators. IGP's technology is primarily adopted for flat or gently curved components, like interior trims and shelving. However, complex automotive frames, heat sinks, and lattice structures are still incompatible, capping volume potential for the next decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyester Dominance Anchored By Outdoor Durability

Polyester powders generated 39.18% of the powder coatings market size for resins in 2025 and are enjoying a 6.29% CAGR through 2031, well ahead of epoxies and acrylics. Notably, polyester-TGIC systems consistently achieve AAMA 2605 weatherability standards, enduring a decade of Florida's sun without significant chalking.

Architectural aluminum extrusions, agricultural equipment, and outdoor furniture, all demanding high UV stability at competitive prices, drive the strongest demand. While epoxies are valued for their corrosion protection, their use is largely limited to appliance interiors and underbody auto parts due to their tendency to discolor in sunlight. Hybrid epoxy-polyesters serve as a middle ground for indoor metal furniture and HVAC cabinets, where a balanced performance is adequate. Niche polyurethanes, catering to oil-and-gas pipelines, offer abrasion resistance that commands a price premium. Acrylic powders, while maintaining gloss for decorative wheels, face cost constraints. With the rise of offshore wind and solar farms, dual-layer epoxy primers topped with polyester systems, compliant with ISO 12944 C5-M, are increasingly favored in challenging marine environments.

By Coating Type: Thermoset Platforms Lock In Share Through Cross-Link Density

Thermoset grades dominated revenue at 91.05% in 2025, and although their growth trails thermoplastics, the absolute volume advantage will persist. Superior solvent and abrasion resistance from irreversible covalent bonding suits chassis, battery trays, and white-goods casings that must survive detergent and salt exposure. The powder coatings market size for thermoplastic grades is smaller but rising at a 6.17% CAGR as electronics and automotive interiors pursue recyclability targets outlined in the EU Circular Economy Action Plan.

BASF's Relest trials demonstrate that polyolefin thermoplastics can be reground and reapplied. However, these thermoplastics lag in hardness and chemical durability, limiting their applications to low-stress scenarios. The move by BASF and Covestro to expand their portfolios into bio-based polyesters hints at a future where performance meets sustainability. This shift could lead to a significant market share change, especially once cost parity is realized.

By End-Use Industry: Industrial Segment Captures Fastest Growth Through Diversification

Industrial machinery absorbed 44.46% of demand in 2025, and its 6.42% CAGR through 2031 outstrips other verticals as powder migrates into construction equipment, material-handling systems, and agricultural implements. Caterpillar and John Deere conversions to single-coat epoxy systems illustrate durability gains that cut warranty claims and field failures.

Architecture follows closely, led by high-rise façades in the Middle East and refurbishment projects in Europe seeking AAMA-compliant finishes. Automotive adoption is accelerating in EV underbodies and battery housings, but exterior panels still mainly use liquids. Appliance and furniture producers continue to push powder to meet zero-VOC mandates and reduce curing energy. Diversification across these sectors insulates suppliers from cyclical swings in any one market.

By Substrate: Metal Dominance Continues As MDF Gains Momentum

Metal remained the workhorse with 81.08% volume in 2025, underpinned by the conductive nature of steel and aluminum that eases electrostatic deposition. The powder coatings market share for MDF and wood is, however, rising quickly on a 6.16% CAGR path enabled by chemistries that cure at or below 120 °C. Tiger Coatings’ low-bake polyester now provides Class 1 furniture surfaces per EN 12720 without primer, removing steps and emissions compared with solvent stains.

Plastics and composites remain experimental, constrained by the need for conductive primers or flame treatment, yet OEM initiatives in circular design may accelerate trials. Glass and other non-conductive substrates are negligible, limited to decorative partitions and specialty lighting where powder offers unique textures.

Geography Analysis

Asia-Pacific commanded 55.65% of the powder coatings market revenue in 2025 and is tracking a 5.91% CAGR to 2031. Vietnamese appliance exports necessitated a significant annual draw of powder for white-goods casings. Thailand's automotive production relied on powder for underbodies, enabling OEMs to comply with Phase 4 emissions standards. In a bid to achieve higher market penetration in furniture and appliances by 2025, China is backing its target with subsidies for powder equipment in Jiangsu and Guangdong. Meanwhile, India's ambition to increase vehicle production is driving an expansion of domestic powder capacity, particularly near Pune and Chennai.

North America is reaping the rewards of re-shored EV lines and the stipulations of USMCA origin rules. GM, Ford, and Stellantis invested heavily in their U.S. and Canadian facilities, with a focus on using powder for battery enclosures and frames. Mexico's adoption of powder coatings increased significantly, while Canadian extruders utilized powder for curtain walls, ensuring compliance with AAMA 2605 standards.

The Industrial Emissions Directive heavily influences Europe's powder coatings market and mandates promoting a circular economy. To align with CAFE targets, German automakers turned to powder coatings for battery trays. French builders, adhering to the RE2020 low-carbon regulations, used powder on a majority of their aluminum frames. The UK's Environmental Act 2021 is pushing appliance manufacturers towards zero-VOC coatings. In Italy, furniture producers in Lombardy achieved a significant milestone, reducing solvent use through a shift towards powder coatings.

Though smaller in scale, South America and the Middle East-Africa regions are witnessing rapid growth in the powder coatings market. Brazil boosted powder usage in commercial vehicles, spurred by tax incentives promoting low-emission manufacturing. Thanks to Saudi Arabia's ambitious giga-projects, imports surged significantly. In the UAE, green-building codes mandated the use of powder coatings on a majority of curtain walls. South Africa's auto plants, primarily focused on exports, are transitioning to powder coatings to meet Euro 6-equivalent standards.

Mordor Intelligence provides coverage of the powder coatings market across other key regional markets, including North America and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The powder coatings market is moderately fragmented. Akzo Nobel's acquisition of Huarun's powder division has expanded its reach into China's appliance and furniture sector. PPG's plant in Vietnam, strategically located alongside OEM clusters, has successfully reduced custom-color lead times. In a bid to stand out, specialty players are turning to innovative technologies: IGP's UV-cure powders now boast a rapid cure time for flat parts. Meanwhile, Sherwin-Williams has clinched a patent for conductive primers, allowing powder application on polypropylene bumpers. This breakthrough could pave the way for significant new applications.

Powder Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Axalta Coating Systems, LLC

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kansai Helios Coatings announced a new USD investment to construct its largest United States powder plant in Johnstown, Ohio. This expansion aims to quadruple the company's production capacity and enhance infrastructure, reflecting a strong commitment to sustainability, innovation, and excellence in coatings capabilities.

- September 2024: Akzo Nobel India has commenced commercial production of powder coating products at its Gwalior plant in Madhya Pradesh. This development is expected to strengthen the company's position in the powder coatings market by enhancing its production capacity and meeting the growing demand in the region.

- October 2024: AkzoNobel introduced Interpon A5000 for commercial vehicles, targeting superior chip resistance and reduced bake cycles. This new line offers superior corrosion protection, UV resistance, and durability against chemicals like petrol, diesel, and oil.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the powder coatings market as all dry, electrostatically applied thermoset and thermoplastic polymer films that melt and cure under heat to form a protective finish on metal or engineered substrates used in appliances, automotive, architectural, furniture, and general-industrial lines. According to Mordor Intelligence, sales are captured at the formulators' gate, net of captive in-house reuse and without double counting reclaimed overspray.

Scope exclusion: Liquid paints, toll-coating services, raw resin sales, and application equipment remain outside this scope.

Segmentation Overview

- By Resin Type

- Epoxy

- Polyester

- Epoxy-Polyester

- Polyurethane

- Acrylic

- Other Resin Types (Polyvinyl Chloride, Polyolefins)

- By Coating Type

- Thermoset Powder Coatings

- Thermoplastic Powder Coatings

- By End-use Industry

- Architecture and Decorative

- Automotive

- Industrial

- Others (Furniture, Appliances, etc.)

- By Substrate

- Metal

- MDF and Wood

- Plastics and Composites

- Glass and Other Non-conductive Substrates

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed formulators, line integrators, appliance OEM buyers, and distributors across Asia-Pacific, North America, and Europe; structured surveys clarified average selling prices, reclaim ratios, and adoption timelines, tightening assumption ranges before final triangulation.

Desk Research

First, we mapped historic demand using open statistics from the United States Census Bureau ASM, Eurostat PRODCOM, China's NBS industrial output, and OICA vehicle assemblies, which signal substrate volumes that dictate coating consumption. Industry briefs from the Powder Coating Institute, American Coatings Association, and CEPE enriched insight on line utilization and thin-film shift. Company 10-Ks, investor decks, and customs shipment tables helped align regional revenue splits and cross-border flows. Paid repositories such as D&B Hoovers for financials, Dow Jones Factiva for deal news, and Questel patent feeds for resin chemistry trends filled residual gaps. The sources listed illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

We applied a top-down production and trade reconstruction, then cross-checked with selective bottom-up supplier roll-ups to size 2025 demand. Key variables include metal furniture output, light-vehicle builds, household appliance shipments, polyester resin index, and regional VOC policy scores. Forecasts to 2030 use multivariate regression with ARIMA error correction, while expert consensus guides scenario bounds. Any bottom-up gaps are reconciled to verified ASP ranges.

Data Validation & Update Cycle

Draft models pass peer review; variance flags trigger source re-checks and follow-up calls. Models refresh annually, with interim updates for material events. Before release, an analyst reruns the workbook so clients receive the latest view.

Why Mordor's Powder Coatings Baseline Commands Reliability

Published market values often differ because firms adjust scope lines, currency anchors, or refresh cadence. We acknowledge those realities and clarify how our disciplined selections improve comparability.

Key gaps arise when others bundle coating equipment, exclude Asia's fragmented supply, or project single-factor CAGR growth without resin price reconciliation; Mordor's annual source roll-ups minimize such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.86 bn (2025) | Mordor Intelligence | - |

| USD 15.4 bn (2024) | Global Consultancy A | Includes equipment and liquid powder hybrids; limited primary checks |

| USD 10.93 bn (2024) | Trade Journal B | Counts only resin revenue, normalizes to 2023 dollars |

| USD 15.20 bn (2024) | Industry Consultancy C | Uses single-factor CAGR without substrate verification |

These contrasts show that Mordor's stepwise, variable anchored model delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the projected value of the powder coatings market by 2031?

The market is forecast to reach USD 17.94 billion by 2031, expanding at a 5.71% CAGR from USD 13.59 billion in 2026.

Which resin holds the largest share in powder formulations?

Polyester commanded a 39.18% share in 2025 thanks to its outdoor durability and cost efficiency.

Why are low-temperature powders important for MDF furniture?

Chemistries that cure at 110 °C–130 °C allow powder to coat MDF without charring, cutting energy use, and eliminating solvent emissions.

How are automotive OEMs using powder coatings in electric vehicles?

Re-shored EV lines apply powder on battery enclosures, subframes, and underbodies to meet zero-VOC targets and streamline paint-shop water use.

What is limiting powder adoption on premium car exterior panels?

Achieving uniform films below 25 µm remains challenging, leading to surface defects that keep liquids dominant on Class-A panels.

Which region represents the fastest-growing opportunity through 2031?

Asia-Pacific maintains the lead, driven by appliance manufacturing in Vietnam and Thailand and sustained automotive production growth in China and India.

Page last updated on: