Europe Powder Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.75 Billion |

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

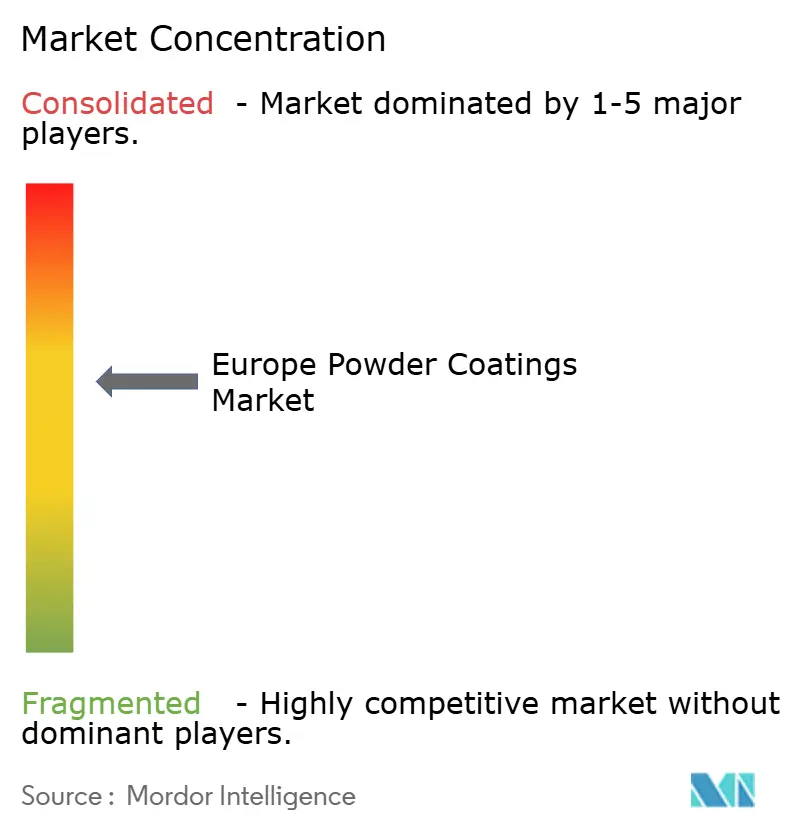

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Powder Coatings Market Analysis by Mordor Intelligence

The Europe Powder Coatings Market size was valued at USD 3.75 billion in 2025 and estimated to grow from USD 3.86 billion in 2026 to reach USD 4.49 billion by 2031, at a CAGR of 3.05% during the forecast period (2026-2031). Consistent regulatory tightening on volatile organic compound (VOC) emissions, rapid advances in low-temperature curing chemistries, and the modernization of European industrial assets underpin this growth trajectory. Demand expansion remains broad-based: architecture and infrastructure projects adopt durable polyester powders, automotive producers specify new polyurethane grades for battery housings, and machinery builders shift toward energy-efficient finishing lines. Competitive positioning hinges on sustainable formulations that exclude per- and polyfluoroalkyl substances (PFAS), automation-ready application equipment, and the ability to localize raw-material sourcing amid ongoing anti-dumping duties. The drive toward carbon-neutral manufacturing further solidifies powder technologies as the preferred choice for original equipment manufacturers (OEMs) seeking to reduce embodied emissions throughout product lifecycles. Meanwhile, supply-side challenges, ranging from titanium dioxide duty surcharges to epoxy resin price spikes, continue to prompt capacity rationalizations, regional sourcing strategies, and hedging mechanisms to protect profitability.

Key Report Takeaways

- By resin type, polyester captured 42.01% of the Europe Powder Coatings market share in 2025, while polyurethane is projected to expand at a 3.62% CAGR through 2031.

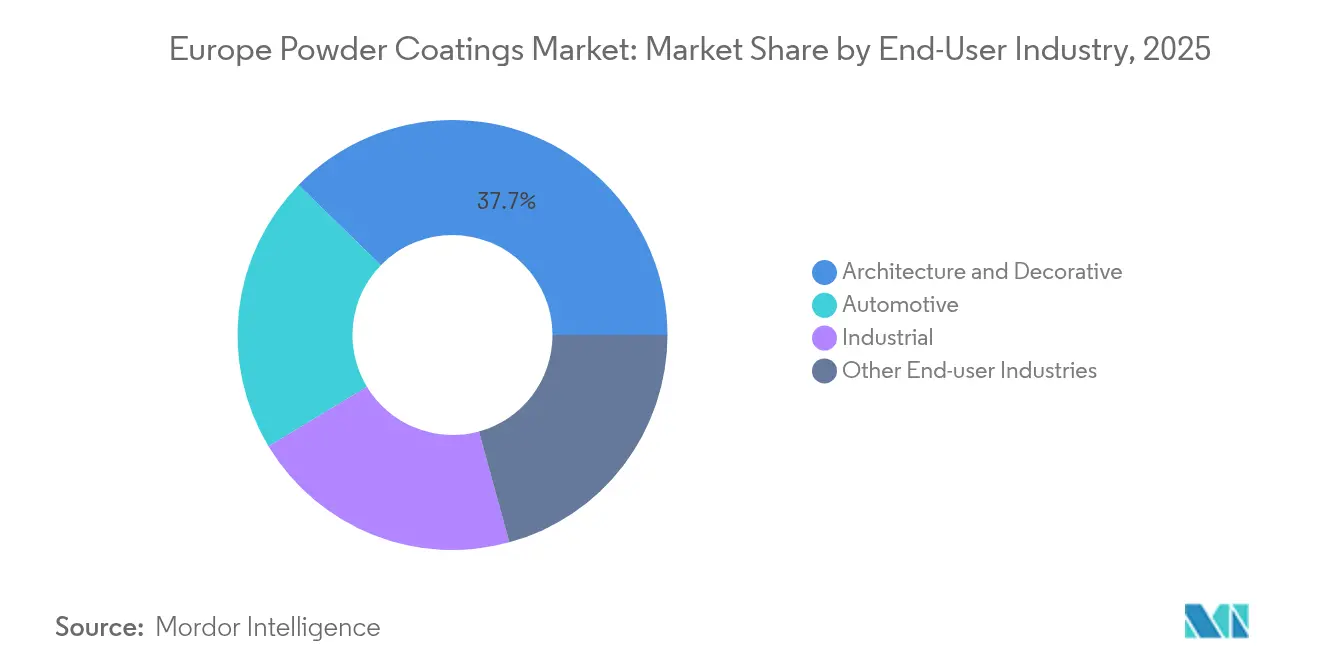

- By end-user industry, architecture and decorative held 37.70% revenue share of the Europe Powder Coatings market size in 2025, whereas automotive is advancing at a 3.4% CAGR over the forecast horizon.

- By geography, Germany led with 21.08% of the Europe Powder Coatings market share in 2025; Rest of Europe is set to post the highest 3.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global powder coatings market data by Mordor Intelligence represents that combined structure.

Europe Powder Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU VOC and carbon-neutrality regulations | +0.8% | EU-wide, strongest in Germany, France, Nordic countries | Medium term (2-4 years) |

| Rising automotive OEM and aftermarket powder usage | +0.6% | Germany, Czech Republic, Slovakia, Poland | Short term (≤ 2 years) |

| Growth of architectural aluminium extrusion demand | +0.5% | Central and Eastern Europe, Italy, Spain | Medium term (2-4 years) |

| Superior recyclability and first-pass transfer efficiency | +0.4% | Global, early adoption in Nordic countries | Long term (≥ 4 years) |

| Low-temperature cure powders enable MDF and plastics | +0.3% | Germany, Italy, Poland, furniture manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU VOC and carbon-neutrality regulations

The Industrial Emissions Directive and the EU Green Deal combine to cap VOC stack emissions at 20 mg/m³ for several surface-treatment categories, effectively prioritizing solvent-free powder processes. Facilities emitting more than 200 tonnes of solvent annually must achieve compliance within four years, accelerating capital deployment toward closed-loop powder booths and energy-efficient curing ovens[1]European Commission, “Industrial Emissions Directive: Best Available Techniques Conclusions for Surface Treatment of Metals,” eur-lex.europa.eu. New PFAS thresholds for food-contact coatings and revised REACH Annex XVII restrictions reinforce the transition by penalizing fluorinated chemistries typical in many liquid systems. Automotive refinish markets now require VOC labeling, with Denmark limiting cleaners to 200 g/L and specialty finishes to 840 g/L, a policy stance that has been quickly mirrored in other Nordic states. ISO 14001 audits are increasingly mandating the use of powder as the “best available technique,” thereby embedding conversion objectives into corporate environmental roadmaps.

Rising automotive OEM and aftermarket powder usage

Electrification reshapes finishing requirements: battery enclosures, cooling plates, and high-voltage casings demand electrically insulative yet thermally conductive coatings. Automakers are therefore adopting low-bake powders that cure at 80 °C—down from legacy 140 °C cycles—cutting paint-shop energy consumption by 11-13% and improving mixed-substrate processing flexibility. Supplier qualification hinges on meeting AAMA standards for weatherability and OEM Class A finish criteria, eroding the competitive position of incumbent liquid suppliers. Wheel refurbishers, commercial-vehicle upfitters, and agricultural equipment remanufacturers likewise migrate toward powders for their abrasion resistance and long service life.

Growth of architectural aluminum extrusion demand

EU transport and energy corridors—backed by more than EUR 7 billion in approved projects—continue to lift demand for coated extrusions in rail stations, port terminals, and photovoltaic mounting systems. AkzoNobel’s Interpon D Stone Effect line demonstrates the segment’s emphasis on lightweight, realistic stone finishes that comply with Qualicoat Class 1 regulations while meeting Leadership in Energy and Environmental Design (LEED) scoring requirements. Southeast European extrusion giant Alumil operates eight powder lines with an annual capacity of 57,500 tonnes, underscoring the region’s architectural appeal. Performance specifications such as AAMA 2605 (10,000-hour Florida exposure) drive demand for super-durable polyester formulations.

Superior recyclability and first-pass transfer efficiency

Closed-loop reclaim systems enable powder booths to achieve more than 95% transfer efficiency, significantly reducing hazardous waste volumes compared to solvent-borne facilities[2]AkzoNobel, “Interpon Powder Coatings Sustainability Whitepaper,” akzonobel.com . Sherwin-Williams’ Powdura ECO line embodies the circular economy promise by incorporating 25% post-consumer PET, equivalent to 16 recycled water bottles per pound of coating. PPG’s Enviroluxe Plus eliminates intentionally added PFAS and incorporates 18% post-industrial plastic, shrinking its cradle-to-gate carbon footprint by 30%. Reclaimable overspray and simplified end-of-life disassembly strengthen OEM take-back initiatives across appliances and mobility equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulty in achieving <30 µm smooth films | -0.4% | Germany, Italy, precision manufacturing regions | Short term (≤ 2 years) |

| High retrofit CAPEX for liquid-to-powder conversion | -0.6% | Southern Europe, SME-concentrated regions | Medium term (2-4 years) |

| EU anti-dumping duties inflating epoxy resin prices | -0.3% | EU-wide, strongest impact on price-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Difficulty in achieving less than 30 µm smooth films

Premium automotive interiors and consumer electronics housings require near-perfect surface topography at film builds of less than 30 µm. Current powder formulations rely on narrow particle-size distributions and specialty flow modifiers, yet maintaining uniformity on complex geometries remains challenging. Allnex’s ultra-low-temperature hybrids cure at 125 °C and improve leveling, but they necessitate tighter humidity control and advanced application hardware. Evonik’s spherical SPHERILEX AC 45 pigments enhance dispersion but require reformulation work across the value chain. Until turnkey solutions reach market maturity, liquid systems retain a technical edge in select high-gloss sectors.

High retrofit CAPEX for liquid-to-powder conversion

Swapping a solvent line for powder typically demands new booths, cyclone separators, infrared or convection ovens, and compressed-air upgrades, with basic installations costing upward of EUR 500,000; fully automated lines run into the multimillion-euro range. European Investment Bank data show that 25% energy-price inflation between 2023 and 2024 eroded discretionary budgets, particularly for SMEs in Southern Europe. Although EU climate grants cover approximately 36% of eligible capital expenditure, application complexity and co-financing requirements deter smaller operators. Leasing constraints and uncertain production volumes further dampen retrofit appetite despite the long-run operational savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyester Dominance Faces Polyurethane Innovation

Polyester maintained 42.01% of the Europe Powder Coatings market share in 2025, translating to the largest slice of the Europe Powder Coatings market size. Its popularity stems from favorable economics, broad color latitude, and established supply chains that serve both façade panels and general industrial machinery. Formulators have extended performance envelopes by introducing super-durable grades that meet AAMA 2604 and Qualicoat Class 2 specifications. Conversely, polyurethane grades are projected to grow at a 3.62% CAGR, as automotive manufacturers pursue lighter structures and extended corrosion warranties. Low-temperature urethane chemistries also enable coating of medium-density fiberboard (MDF) fixtures, opening incremental opportunities in European furniture hubs.

Technological advancements now center on curing efficiency. AkzoNobel’s Interpon D2525 Low-E polyester requires just 150°C, cutting booth dwell times by 20% and widening applicability to heat-sensitive alloys. Allnex’s CRYLCOAT 4488-0 offers decade-long Florida exposure resistance, while TGIC-free systems dominate new capacity due to impending toxicological re-classifications. Epoxy resins continue to underpin pipeline valves and chemical reactors; hybrids bridge decorative and functional needs; acrylics target ultra-weatherable signage; and niche thermoplastics serve household-appliance and anti-graffiti segments. Across these chemistries, powder suppliers increasingly tout Environmental Product Declarations (EPDs), aligning formulations with customer carbon audits.

By End-User Industry: Architecture Leadership Meets Automotive Acceleration

The architecture and decorative segment accounted for 37.70% of the Europe Powder Coatings market in 2025, buoyed by public-sector building retrofits that specify 15-year warranties and chromium-free pre-treatments. Aluminum curtain-wall systems, metal roofing, and street furniture drive tonnage, while color-stable matte finishes gain popularity among specifiers. Compliance with EN 13523 accelerated conversion from liquid polyesters as municipalities require near-zero VOC construction materials.

Automotive applications are forecast to post the fastest 3.4% CAGR through 2031, as electric vehicle output multiplies. Battery pack enclosures, brake calipers, and alloy wheels feature two-coat powder builds that combine epoxy primers with polyurethane topcoats. Magna notes that switching to 80 °C cure cycles reduced annual paint-shop energy by 20 GWh at its Graz facility. Elsewhere, general industry, including agricultural equipment, compressors, and machine tools, embraces powders to meet enhanced salt-spray benchmarks. Appliance OEMs exploit single-coat systems that eliminate primer stages and enhance factory throughput, while European furniture producers specify soft-touch polyurethane powders on MDF to bypass solvented lacquers.

Geography Analysis

Germany commanded 21.08% of the Europe Powder Coatings market in 2025, supported by a EUR 263 billion machinery sector employing 955,000 people and exporting 81% of output. Fully automated robotic lines, such as those at Hans Stork Oberflächentechnik, utilize dense-phase spray guns and closed-loop reclaim systems to meet Federal Emission Control mandates. The nation’s vocational training landscape supplies skilled coaters, enabling high first-run yields and reduced color change downtime. Energy-efficiency subsidies further encourage upgrades to variable-frequency drive ovens and advanced air-handling units.

Rest of Europe represents the fastest-growing sub-region, set to advance at a 3.22% CAGR through 2031. EU-backed infrastructure outlays, EUR 7 billion for rail corridors and EUR 850 million for grid interconnectors, drive aluminum extrusion and structural-steel demand. Investment rates reached 78% among Central and Eastern Europe manufacturing firms in 2024, with 33% of capital expenditures directed to machinery replacement, which often includes powder-coating lines. Automation adoption is brisk, with 45% of surveyed plants implementing IoT sensors and robotic sprayers to improve coating consistency.

Western Europe, encompassing the United Kingdom, France, Italy, and Spain, shows stable replacement demand. The UK ban on hexavalent chromium in 2024 accelerated adoption of titanium-zirconium and silane pre-treatments compatible with powders; Powdertech Corby reports full chrome-free processing across façade contracts. Italy’s Emilia-Romagna furniture cluster increasingly specifies low-cure powders for MDF to bolster export competitiveness. Nordic markets pioneer PFAS-free formulations, incentivized by stringent environmental labeling schemes and consumer preference for circular products. Benelux benefits from Antwerp-Rotterdam chem-port proximity, ensuring secure feedstock supply for formulators and toll coaters.

The powder coatings market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America.

Competitive Landscape

The Europe Powder Coatings market features moderate concentration. AkzoNobel, PPG Industries, Sherwin-Williams, Axalta, and BASF command brand loyalty through extensive distributor networks, a broad range of color libraries, and localized technical service centers. Their R&D pipelines prioritize low-bake chemistries, recycled-content binders, and PFAS-free additives. Raw-material inflation remains a shared headwind: January 2025 titanium dioxide duties of EUR 0.25–0.74/kg inflated the cost of goods sold by 4–6%, prompting formulators to consider alternative pigments, such as Venator’s TMP- and TME-free TIOXIDE TR81. Epoxy anti-dumping tariffs reaching 40.8% accelerate a pivot to polyester-dominant portfolios and regional resin suppliers. Energy price volatility incentivizes the adoption of infrared boost zones and recuperative burners to mitigate exposure to natural gas.

Europe Powder Coatings Industry Leaders

-

Akzo Nobel N.V.

-

Jotun

-

PPG Industries, Inc

-

The Sherwin-Williams Company

-

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AkzoNobel N.V. partnered with IPG Photonics to harness laser technology in curing powder coatings worldwide, including Europe. Their approach fine-tunes AkzoNobel N.V.'s Interpon powder coatings to work seamlessly with IPG's laser curing solutions.

- June 2024: Arkema unveiled a pioneering manufacturing process that incorporates up to 40% post-consumer recycled content (post-consumer PET (Polyethylene terephthalate)) from discarded packaging into its powder coating resins.

Europe Powder Coatings Market Report Scope

Powder Coatings are used to provide color/texture for various objects. Apart from aesthetic applications, coatings are also used to protect/increase the shelf life of metals and other materials. Owing to the factors above, they are increasingly used in various end-user sectors, including construction and infrastructure, automotive and transportation, oil & gas, and other industries.

Europe's powder coatings market is segmented by resin type, end-user industry, and geography. The market is segmented by resin type the market is segmented into acrylic, epoxy, polyester, polyurethane, epoxy-polyester, and other resin types (polyvinyl chloride, polyolefins, etc.).By end-user industry, the market is segmented into architecture and decorative, automotive, industrial, and other end-user industries (furniture, appliances, etc.). By geography, the market is segmented into Germany, the United Kingdom, France, Italy, and Rest of Europe. The report also covers the market size and forecasts for the Europe Powder Coatings market for 4 major countries.

For each segment, the market sizing and forecasts are provided in terms of value (USD).

| Epoxy |

| Polyester |

| Epoxy-Polyester (Hybrid) |

| Polyurethane |

| Acrylic |

| Other Resin Type (Thermoplastic (Polyvinyl Chloride, Polyolefins,etc.) |

| Architecture and Decorative |

| Automotive |

| Industrial |

| Other End-user Industries (Furniture, Appliances, etc.) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Benelux |

| NORDIC Countries |

| Rest of Europe |

| By Resin Type | Epoxy |

| Polyester | |

| Epoxy-Polyester (Hybrid) | |

| Polyurethane | |

| Acrylic | |

| Other Resin Type (Thermoplastic (Polyvinyl Chloride, Polyolefins,etc.) | |

| By End-user Industry | Architecture and Decorative |

| Automotive | |

| Industrial | |

| Other End-user Industries (Furniture, Appliances, etc.) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Benelux | |

| NORDIC Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe powder coatings market?

The market is valued at USD 3.86 billion in 2026.

How fast will demand for powder coatings in automotive applications grow?

Automotive usage is projected to post a 3.4% CAGR from 2026 to 2031 as electric-vehicle output scales.

Which resin type dominates European powder formulations?

Polyester resins lead with 42.01% share in 2025 due to cost-effectiveness and weatherability.

Why are European manufacturers converting from liquid to powder systems?

Powder technologies eliminate VOC emissions, cut energy consumption through low-temperature curing, and enable closed-loop recyclability, aligning with EU carbon-neutrality targets.

Which European region will see the fastest growth?

Rest of Europe is expected to record a 3.22% CAGR from 2026 to 2031, driven by large-scale infrastructure investments.

Page last updated on: