Diamond Coating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

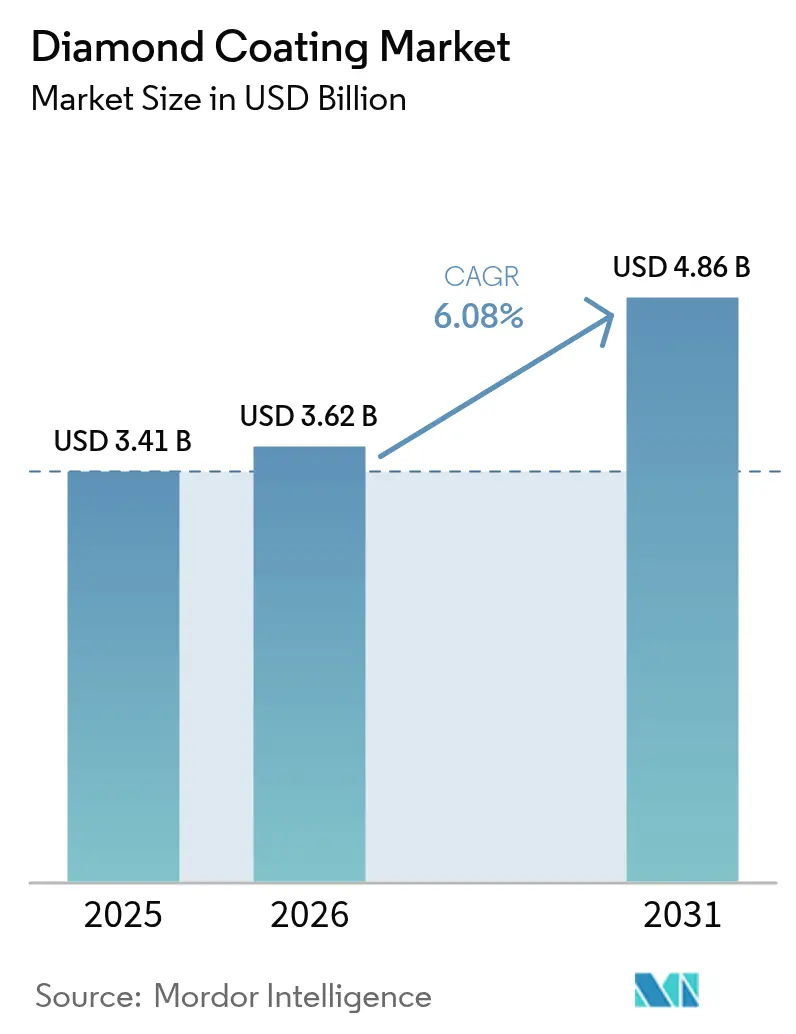

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

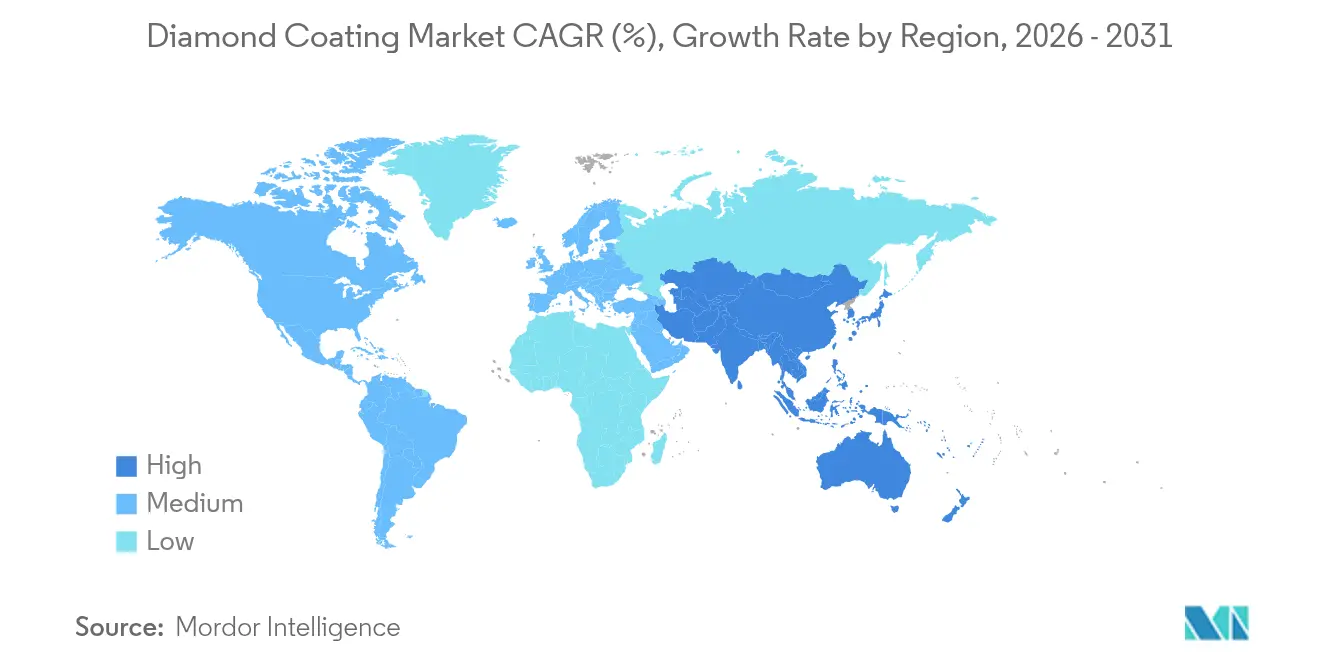

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

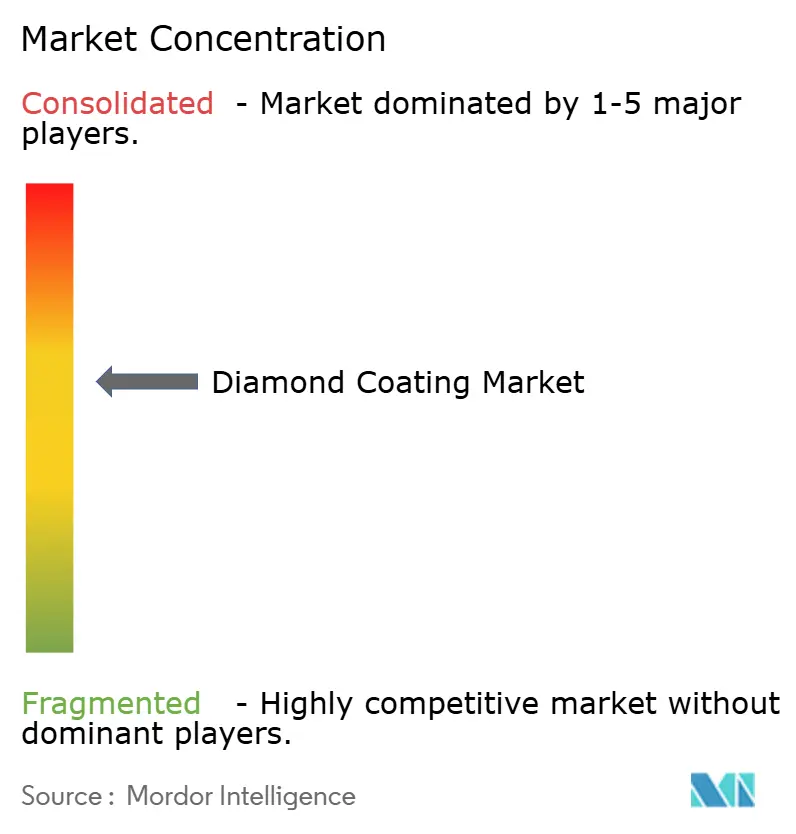

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diamond Coating Market Analysis by Mordor Intelligence

The Diamond Coating Market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 4.86 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). Sustained investment in cutting-tool upgrades, thermal-management materials for AI hardware, and biocompatible medical instruments anchors this expansion even as overall capital spending in manufacturing remains selective. Semiconductor makers are turning to metallised diamond heat spreaders that move heat four to five times faster than copper, keeping next-generation GPUs within safe operating windows. In parallel, surgeons and dentists increasingly specify diamond-like carbon (DLC) coatings because they tolerate repeated autoclave cycles without flaking, a property that reduces re-sterilisation costs for hospitals. Policy pressure to eliminate lead in consumer electronics soldering also strengthens demand for diamond-coated soldering tips that resist the higher process temperatures of lead-free alloys. Taken together, these shifts keep the diamond coating market on a clear growth trajectory despite high equipment outlays and lingering adhesion challenges on temperature-sensitive substrates.

Key Report Takeaways

- By technology, Chemical Vapour Deposition (CVD) retained a 66.70% revenue share in 2025, while Physical Vapour Deposition (PVD) posted the leading CAGR at 7.18% through 2031.

- By coating type, Diamond-Like Carbon captured 78.92% of the 2025 diamond coating market share, whereas composite/doped films are projected to expand at a 6.9% CAGR to 2031.

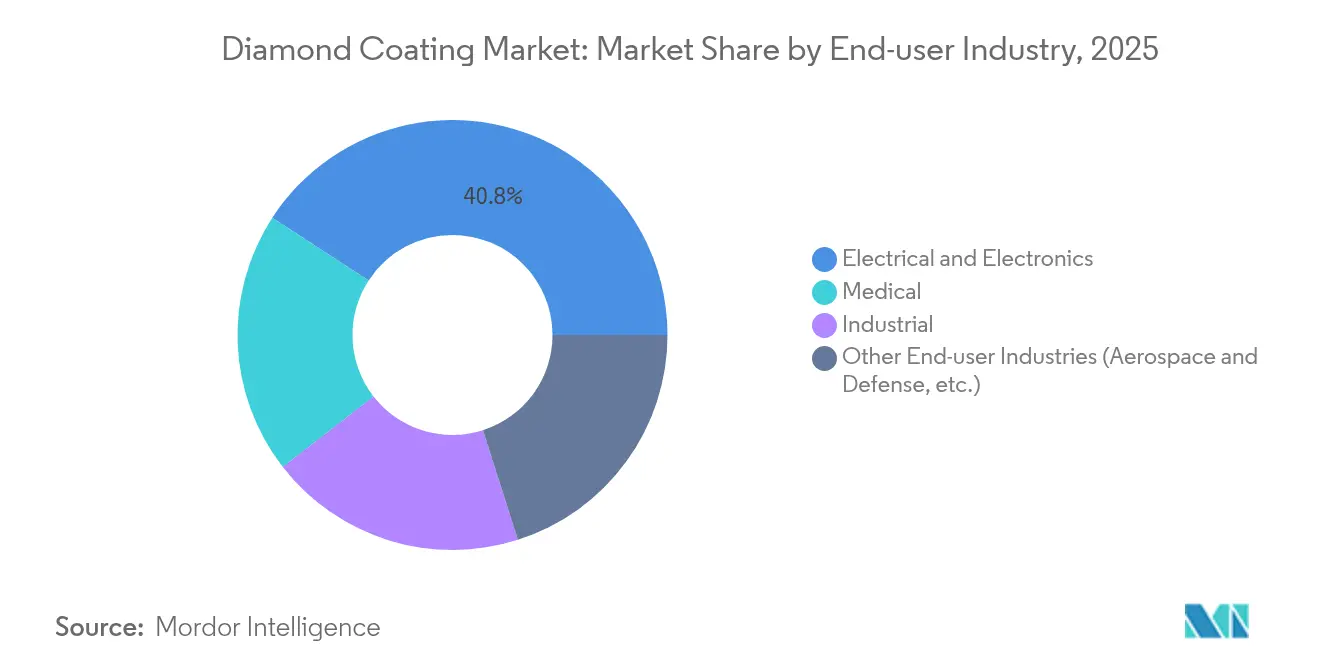

- By end-user industry, electrical and electronics accounted for 40.82% of 2025 revenues, while medical is advancing at a 7.22% CAGR through 2031.

- By geography, Asia-Pacific commanded 56.10% of 2025 sales and is set to post the fastest 6.79% regional CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diamond Coating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption in Cutting Tools for Light-Weight Composites | +1.2% | Global, with concentration in North America and EU aerospace | Medium term (2-4 years) |

| Growing Demand for Thermal-Management Solutions in Consumer Electronics | +1.8% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Accelerating Use of Diamond-Coated Surgical and Dental Tools | +1.0% | Global, with early gains in North America, EU, Japan | Medium term (2-4 years) |

| Regulatory Push for Lead-Free Precision Soldering Equipment | +0.7% | EU, North America, with adoption in APAC | Long term (≥ 4 years) |

| Increased Wear-Life Needs of EV Battery Welding Electrodes | +0.8% | China, South Korea, with expansion to global EV hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption in Cutting Tools for Light-Weight Composites

Machining carbon-fiber reinforced plastics generates abrasive dust that blunts conventional carbide inserts after limited passes. CVD diamond-coated cutters last 15-30 times longer, shaving tool-change downtime and scrap on aerospace composite structures[1]Crystallume, “Diamond-Coated Tools for CFRP Machining,” crystallume.com. Dual-layer micro-crystalline/nano-crystalline stacks further suppress crack propagation, lowering delamination risk on wing panels and automotive body panels As Boeing and Airbus lift composite content, suppliers specify diamond coatings to achieve clean edges at high spindle speeds. The result is rising unit demand for diamond-ready drills, routers, and end mills across North America and Europe. Medium-term growth remains secure because the installed fleet of composite airframes is still young and spare-parts machining volumes are only beginning to scale.

Growing Demand for Thermal-Management Solutions in Consumer Electronics

Data-center GPUs now dissipate beyond 700 W per module, forcing operators to rethink baseplate materials. Copper-diamond composites delivering 800 W/mK thermal conductivity cut core temperatures by up to 20 °C in pilot AI servers deployed by Akash Systems under a USD 27 million supply contract. Laboratory single-crystal diamond spreaders reach 1,500-2,200 W/mK, far eclipsing copper at 400 W/mK, creating a clear performance gap that favors adoption. Fraunhofer USA’s flexible diamond nanomembranes promise five-fold faster EV battery charging by extracting heat from power electronics more efficiently. The collision of miniaturisation and higher power density therefore keeps thermal-grade diamond coatings firmly on the procurement road-maps of smartphone, laptop, and datacenter OEMs. Short-term pull is strongest in Asia-Pacific where volume device assembly occurs.

Accelerating Use of Diamond-Coated Surgical and Dental Tools

Diamond-like carbon scalpels retain sharpness after repeated autoclave cycles, reducing replacement frequency for hospitals already facing staffing cost pressure. DLC exhibits an adhesion strength of 24 N versus traditional black chrome at roughly 9 N, a jump that eliminates edge flake failures during neurosurgery. University of Alabama Birmingham studies show orthopedic implants coated with nanodiamond last two to three times longer than cobalt-chrome devices, potentially outliving a 30-year postoperative horizon. FDA clearance of nano-scaled diamond finishes reassures OEMs about cytotoxicity, widening the application range to cardiovascular stinting and dental burrs. As aging populations in the United States, Germany, and Japan raise hip and knee replacement counts, demand for long-wear coatings climbs correspondingly.

Regulatory Push for Lead-Free Precision Soldering Equipment

RoHS and REACH restrictions push electronics brands to completely remove lead from tin-based solder. The switch lifts reflow temperatures by 30-40 °C, accelerating wear on conventional iron plating. Diamond-coated tips withstand this thermal shock, retaining wetting performance across extended duty cycles. Japanese industry standards now codify DLC thickness and hardness requirements, giving OEMs a blueprint for global sourcing. The EU’s pending Ecodesign updates further reinforce adoption by penalising early failure of assembly equipment. Long-term impact is therefore positive, especially for contract manufacturers servicing automotive and medical device boards where zero-defect solder joints are mandatory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Long Payback Periods | -1.5% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Adhesion Challenges on Temperature-Sensitive Substrates | -0.8% | Global, particularly affecting medical and electronics applications | Medium term (2-4 years) |

| Competing Lower-Cost Coating Alternatives | -0.6% | Price-sensitive markets in APAC and emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Long Payback Periods

A single three-chamber CC800 Diamond unit from CemeCon costs multiple millions of USD and demands customised exhaust, gas handling, and clean-room retrofits[2]CemeCon, “CC800 Diamond Coating System,” cemecon.com. SMEs therefore struggle to justify outlays when cutting-tool clients resist premium pricing. Even for large foundries, depreciation stretches beyond five years, lengthening return horizons. Financing has become more selective, with lenders scrutinising utilisation rates before approving leases. In emerging markets the hurdle is steeper because local electricity and skilled-labour costs narrow operating margin cushions. These realities shave near-term adoption, particularly outside tier-one suppliers.

Adhesion Challenges on Temperature-Sensitive Substrates

DLC deposition typically exceeds 280 °C, a threshold that induces residual stress on aluminum and some surgical-grade steels. Delamination risk rises when thermal expansion mismatch creates shear forces at the interface. Researchers now explore chromium-nitride or vanadium-carbide interlayers to buffer these stresses, yet each additional layer adds cost and process steps. Low-temperature plasma-enhanced CVD variants show promise but scale-up remains limited. Medical and consumer electronics OEMs therefore wait for broader proof before committing high-volume orders, dampening mid-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: CVD Reinforces Market Leadership

CVD processes commanded 66.70% of 2025 revenue, and this slice of the diamond coating market is forecast to climb at a 6.74% CAGR to 2031. The technique’s ability to tailor grain size, build dense films, and hit thickness uniformity below ±3 µm keeps it at the core of high-performance cutting-tool and heat-spreader production. Element Six’s 800 W/mK copper-diamond composite illustrates how CVD can embed diamond grains in metal matrices without voids, unlocking rapid heat flow for AI processors. Graphene-oxide assisted growth now accelerates deposition by 35%, trimming cycle time and lowering per-wafer costs. PVD holds niche positions where 150-200 °C limits protect sensitive electronics boards or polymer substrates. Even so, incremental improvements in plasma-enhanced variants are expected to narrow the performance gap, allowing PVD to court medical OEMs that cannot tolerate the higher temperatures of conventional CVD. Together, both methods secure the technological backbone of the diamond coating market.

By Coating Type: DLC Dominance with Emerging Composites

DLC films held a commanding 78.92% share of 2025 revenues due to their low coefficient of friction and cost-effective batch production. Friction coefficients as low as 0.029 have been reported for molybdenum-doped DLC, illustrating the capacity to further tune performance through elemental additions. Composite and doped structures, the fastest grower at 6.9% CAGR, marry hardness with customized electrical or thermal conductivity for niche roles in quantum devices and high-frequency RF amplifiers. Polycrystalline diamond remains essential for mechanical seals in aggressive chemical pumps, where its isotropic toughness outperforms brittle ceramics. Nano- and micro-crystalline variants serve optics and precision metrology that demand sub-micron surface roughness. This diverse portfolio lets suppliers match film chemistry to each application, underpinning the broad appeal of the diamond coating market.

By End-user Industry: Electronics Anchors Demand, Medical Gains Speed

Electrical and electronics buyers generated 40.82% of 2025 turnover, reflecting relentless thermal-management challenges in semiconductors, power modules, and consumer devices. With the diamond coating market size for electronics components projected to expand at 6.47% annually, coating vendors see steady pull from foundries and datacenter builders. Medical equipment, however, is increasing 7.22% per year, outpacing all other sectors as aging societies drive joint-replacement and minimally invasive surgery volumes. Industrial tooling and wear parts still contribute steady baseline demand, while aerospace and defense customers tap super-abrasive films to mill lightweight composites at production rates impossible a decade ago. The cross-pollination of techniques between electronics and medical segments further accelerates innovation, illustrating the interconnected nature of the diamond coating industry.

Geography Analysis

Asia-Pacific controlled 56.10% of global revenue in 2025 and is pacing the field with a 6.79% CAGR through 2031. China leverages long-running “863” funding lines to integrate lab-grown diamond supply with CVD reactor manufacturing, giving local players cost advantages along the diamond coating value chain. Japan’s Orbray has scaled 2-inch single-crystal diamond wafers and targets 4-inch substrates by 2027, laying groundwork for wide-bandgap semiconductors and quantum photonics. South Korea’s EV battery boom creates a parallel surge in diamond-clad welding electrodes for tab joining.

North America follows as a mature adopter, with Sandia National Laboratories unveiling stress-free amorphous diamond films thick enough for large-area coverage without cracking. CHIPS Act grants worth more than USD 80 million have already flowed to Coherent and Akash Systems to accelerate on-shore diamond material technologies. Canada’s aerospace machining cluster and Mexico’s automotive assembly lines also specify diamond tooling to maintain tolerances on composite parts.

Europe’s market reflects an interplay of strict environmental regulations and precision engineering heritage. Germany’s OEMs rely on diamond routers to machine carbon-fiber body panels, while France’s Safran and Oerlikon together invested over USD 8 million in a joint surface-treatment lab focused on turbine efficiency. The United Kingdom has dedicated USD 5.2 million via UKRI to an Element Six–University of Warwick program developing synthetic diamond heat spreaders for space electronics. Compliance with REACH continues to steer European firms toward durable, recyclable tooling options.

South America and the Middle-East and Africa are smaller today but show rising inquiry volumes from mining, oil-field, and precision agricultural equipment producers seeking longer component life in abrasive conditions. As regional industrialisation gains pace, the diamond coating market will likely see distributor networks and toll-coating capacity expand into Brazil, Saudi Arabia, and the United Arab Emirates.

Regulatory Landscape

Regulation for diamond and diamond-like carbon (DLC) coatings is tightening around chemicals management, nanomaterial documentation, and application-specific safety. In the European Union, REACH requirements for nanoforms are a key anchor for suppliers of nanodiamond particles and nano-abrasive formulations, with ECHA-linked updates cited for 2026 that emphasize nano-specific registration and expanded safety documentation (including Nano-SDS and labeling) for EU-bound shipments. These obligations increase compliance and traceability requirements for non-EU producers exporting to Europe, and they also shape how coating formulators define particle size distributions and labeling during procurement.

Application-driven standards and approvals also influence market access. For instance, food-contact use is governed through US FDA pathways such as Food Contact Notifications (FCNs), where DLC coatings can be cleared for defined uses by individual notifiers, including an FCN held by Balzers Aktiengesellschaft. In Asia, formalized performance specifications for DLC coatings are emerging through national standards such as KS D 8353-2026 in South Korea and technical specifications such as T/CSAE 103-2019 in China, which pushes buyers toward more standardized testing for hardness, friction, and wear. Environmental permitting affects upstream synthetic diamond and coating operations as well, including UK Environment Agency permitting expectations for facilities running microwave plasma CVD processes with methane and hydrogen gas handling.

Value Chain Analysis

The diamond coating value chain starts with feedstocks and deposition equipment, including high-purity process gases such as hydrogen and methane for CVD and, where used, dopant precursors such as silicon-containing chemistries. Reactor platforms and critical components, including vacuum systems, plasma or hot-filament assemblies, gas handling, and abatement, support coating service capacity. Substrates span cemented carbides, steels, ceramics, and electronics-related materials, which often require tightly controlled pretreatment and seeding before deposition.

In the midstream, specialist coaters and integrated tooling players run pretreatment, nucleation, deposition (CVD and PVD variants), and post-process inspection to manage film stress and adhesion, which remains a central bottleneck, especially on carbide substrates where cobalt diffusion and thermal mismatch can weaken bonding. Companies such as Element Six and sp3 Diamond Technologies supply diamond materials and coating services, while industry groups such as the Industrial Diamond Association of Japan support downstream adoption. Downstream channels include direct OEM and tier-supplier qualification in cutting tools, electronics thermal management components, and medical instruments, where qualification cycles and performance verification drive repeat orders and reward suppliers with stable process control and documentation for regulated end uses.

Competitive Landscape

The diamond coating market is moderately concentrated. Element Six retains an edge through vertical control of synthetic diamond production and its Cu-Diamond composite that hit 800 W/mK thermal conductivity in 2025. CemeCon differentiates with its multi-chamber CC800® platform, allowing simultaneous deposition of nanocrystalline and multilayer films on over 80 substrate types. Oerlikon, via Balzers, broadened its Baldia Varia line to attack difficult-to-cut nickel alloys, helping turbine makers lift tool life by 20%.

Disruptors such as Akash Systems channel funding toward diamond-cooled AI servers that promise lower power bills for hyperscale operators. Diamond Quanta, fresh from stealth in 2024, pushes a unified diamond framework to yield high-purity wafers for quantum photonics, a market still in its infancy. Partnerships are multiplying: Element Six teamed with Lummus to attack PFAS water contamination using boron-doped diamond electrodes, while Orbray supplies high-quality crystals for next-generation optical interconnects. Pricing pressure is muted because switching costs are high and buyers value performance over lowest unit cost, a dynamic that sustains healthy margins for technology leaders.

Diamond Coating Industry Leaders

NeoCoat SA

Crystallume

OC Oerlikon Balzers

JCS Technologies Pte Ltd

SP3 Diamond Technologies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Thermal management for advanced electronics is creating a more visible opportunity set for diamond coatings and diamond-based films as design-in materials. In 2026, Fraunhofer IST reported a reflection mapping method intended to improve large-area diamond coating uniformity and measurement on 300 mm silicon wafers, tackling a practical barrier to scaling diamond-coated semiconductor substrates. Alongside this, semiconductor packaging R&D continues to explore diamond-based films for die-stack heat spreading and electrical connectivity, including Intel patent filings in 2026 that describe diamond-related film concepts for thermal dissipation in stacked architectures.

Process and materials opportunities also center on lowering deposition temperatures and expanding compatible substrates, particularly for temperature-sensitive electronics assemblies and medical components where adhesion and thermal stress constraints can narrow conventional DLC/CVD windows. Evidence in the current landscape points to work on lower-temperature deposition approaches, including hot-filament or remote plasma techniques referenced in patent disclosures, and to interlayer engineering such as carbide-forming layers like TiC, VC, or CrC to improve wetting and adhesion in diamond/metal composite systems. These pathways align with existing demand anchors in the broader market landscape, including metallized diamond heat spreaders for AI hardware and durability-driven DLC use in sterilizable medical instruments, while also supporting more repeatable manufacturing through improved metrology and scrap reduction.

Recent Industry Developments

- April 2026: Fraunhofer IST introduced a reflection mapping approach aimed at precision measurement of large-area diamond coating uniformity on 300 mm silicon wafers. The work targets tighter process control and faster identification of non-uniform regions, which supports scale-up for semiconductor-grade diamond-coated components. Improved metrology lowers qualification friction for electronics customers that demand wafer-level repeatability.

- June 2025: Diamond Technologies Inc. (DTI) acquired the assets of Akhan Semiconductor to broaden its electronics-grade diamond materials capabilities. The move strengthens access to diamond material know-how aligned with demanding thermal and durability requirements in electronics and semiconductor applications. Consolidation at the materials layer can shorten development loops between material supply and downstream coating commercialization.

- June 2025: Oerlikon Balzers launched BALDIA VARIA, a CVD diamond coating for cutting tools used in machining CFRPs, composites, graphite, and advanced ceramics. The product positions progressive wear behavior and consistent coating performance across a wide range of tool geometries to improve tool-life planning in high-value machining. This launch supports higher utilization of diamond-coated tooling in aerospace and other sectors where abrasive, lightweight materials drive rapid wear in conventional tool coatings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from diamond-based coatings applied to a substrate to improve hardness, wear resistance, thermal behavior, and surface performance, across industrial, electronics, and medical uses. We size the market in value terms, and the output is reported in USD.

Scope exclusions: We exclude bulk diamond materials sold as standalone components and any downstream finished products where the coating value cannot be separated from the end product price.

Segmentation Overview

- By Technology

- Chemical Vapour Deposition (CVD)

- Physical Vapour Deposition (PVD)

- By Coating Type

- Polycrystalline Diamond (PCD)

- Nano-/Micro-crystalline Diamond (NCD/MCD)

- Diamond-Like Carbon (DLC)

- Composite / Doped Diamond Coatings

- By End-user Industry

- Electrical and Electronics

- Medical

- Industrial

- Other End-user Industries (Aerospace and Defense, etc.)

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear view of where diamond coatings are used and what drives adoption, before numbers are modeled. We relied on public sources such as USGS minerals information, UN Comtrade trade statistics, USPTO and WIPO patent databases, NIST publications, and peer reviewed journals that track thin film deposition and tribology. Along with this, we reviewed company filings and presentations, association updates, and reputed press coverage to understand capacity additions, application pull, and pricing direction.

To convert that context into usable inputs, we also used paid subscriptions focused on company financials and intelligence, news and financials, patent analytics, and shipment-level import export data where it helped confirm cross-border flows of coating equipment or related materials. These sources were mainly used to set realistic ranges and to avoid missing major demand pockets in key countries. The sources listed here are illustrative only, and many other public documents and datasets were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what we had built from public information, especially around adoption by end users, typical coating value per part, and how pricing shifts with coating type and deposition method. Interviews and survey follow-ups were conducted with coating service providers, equipment and process specialists, and procurement or engineering users across APAC, EMEA, and the Americas. Where repeated feedback pointed to a consistent mismatch, we adjusted the model assumptions rather than keeping them fixed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 40% | EMEA: 37% |

| Smaller Players: 17% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing uses a top-down approach where end use demand pools are reconstructed by linking coated part volumes to coating penetration rates, and then translating those volumes into revenue using typical coating value ranges. To keep it grounded, the totals are cross-checked with selective bottom-up approximations such as sampled ASP times volume for a set of common coated components, and then compared against supplier and channel feedback before final numbers are locked.

Inputs that matter in diamond coating include deposition mix between CVD and PVD, coating type mix (such as polycrystalline and nanocrystalline or microcrystalline forms), the share of coated cutting and wear parts in industrial activity, electronics manufacturing indicators that influence coated component demand, and medical device output trends where coated tools and components are used. Where a variable moved quickly in recent years, it was smoothed using expert ranges instead of a single point estimate, and this is where we kept the model from overfitting the year-to-year noise.

For forecasting, scenario analysis is used, supported by a simple regression-style check on a few demand indicators so the trajectory stays consistent with what the market can practically absorb. In cases where bottom-up checks cannot cover smaller countries or niche uses, we apply proxy ratios from similar markets and then revalidate the resulting per-capita and per-industry intensity with interview feedback.

Data Validation & Update Cycle

Validation is done through multiple checks so the final value does not rely on one dataset or one assumption. Model outputs are compared with independent signals like regional manufacturing activity, reported tooling and electronics production trends, and visible changes in deposition capacity or equipment shipments, and then outliers are reviewed until the drivers make sense.

Before sign-off, a second analyst reviews inputs, units, and conversions, followed by a final consistency pass across regions and segments so totals add up cleanly. The report is refreshed annually, and interim updates are triggered when a material event shows up, such as a sudden capacity change, a major regulatory shift in a key end use, or sustained pricing movement. Right before delivery, the latest data is checked again so clients receive an updated view rather than an older snapshot.

Mordor Intelligence's Diamond Coating Market Size Measured Against Other Published Estimates

Published market values for diamond coatings can look different across sources, even when the topic name is the same, because the counted items and the year basis are not aligned. Differences also come from how each model treats deposition methods, coating types, and whether service revenue is blended into the same total.

Bulk diamond materials sold as standalone components sit outside Mordor Intelligence's scope, which is one reason its 2025 value can differ from sources that bundle adjacent diamond materials with coating revenue. Other gaps typically come from using a 2024 base year and then projecting forward with aggressive adoption assumptions, or from applying a single average price that does not reflect the mix shift across CVD and PVD and across higher value coating types. Currency conversion timing and refresh cadence also matter because coating prices and industrial demand can move within a year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.41 B (2025) | |

| Global Consultancy A | USD 2.88 B (2024) | Uses a 2024 base year and applies a broad global average across end uses, which can understate the 2025 value when industrial and electronics demand are rebased and when coating type mix is updated. |

| Industry Publisher B | USD 2.61 B (2024) | Leans on a narrower application set and a conservative adoption ramp, and it often treats deposition mix and price progression as steady, which can reduce the counted revenue when higher value coatings gain share. |

The spread across the table is mainly explained by what is counted, which year is used as the starting point, and how price and mix are carried forward. By keeping the inputs tied to deposition method, coating type mix, and end use demand signals, we can explain each step and also repeat the sizing when new public indicators or interview checks become available.

Key Questions Answered in the Report

What is the current value of the diamond coating market?

The diamond coating market size is USD 3.62 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 6.08% CAGR, reaching USD 4.86 billion by 2031.

Which region leads demand?

Asia-Pacific controls 56.10% of global revenue and posts the fastest 6.79% CAGR.

Why do electronics makers prefer diamond coatings?

Copper-diamond composites move heat up to five times faster than copper alone, keeping next-gen GPUs cooler and more energy-efficient.

What is the biggest restraint to wider adoption?

High capital investment for CVD equipment and long payback periods slow uptake, especially among small and medium manufacturers.

Page last updated on: