Clean Label Starch Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

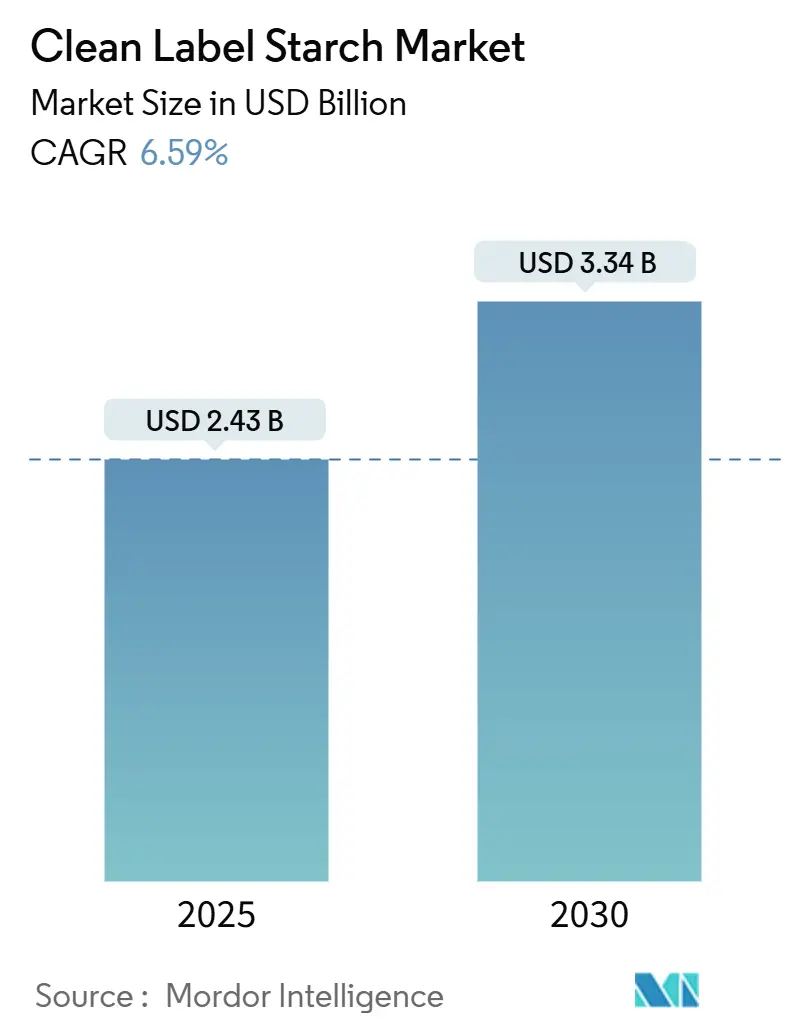

| Market Size (2025) | USD 2.43 Billion |

| Market Size (2030) | USD 3.34 Billion |

| Growth Rate (2025 - 2030) | 6.59% CAGR |

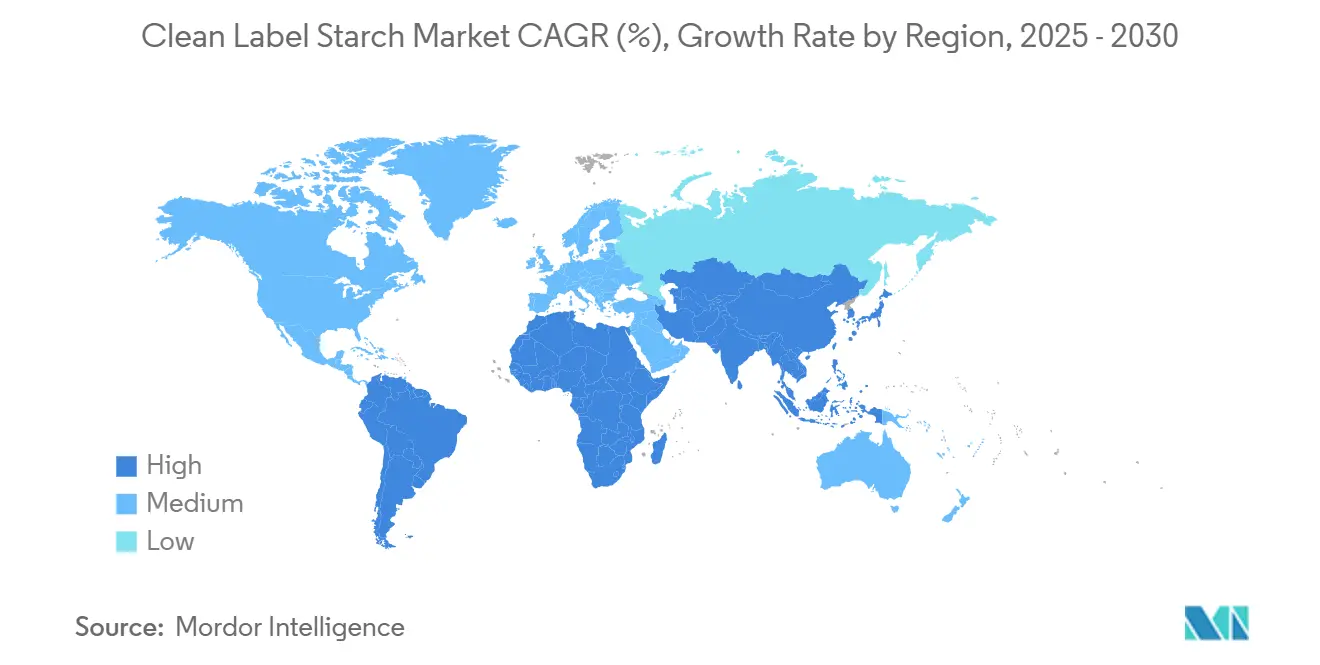

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Clean Label Starch Market Analysis by Mordor Intelligence

The global clean label starch market achieved a significant milestone, reaching USD 2.43 billion in 2025, and is poised to expand further to USD 3.34 billion by 2030, demonstrating a steady compound annual growth rate (CAGR) of 6.59%. This upward trajectory in market size stems from the evolving regulatory landscape and heightened consumer awareness regarding ingredient transparency. Notable regulatory developments include the FDA's comprehensive revision of the "healthy" definition, which came into effect in February 2025, and China's implementation of stringent food labeling standards (GB 7718-2025), set to commence in March 2027 [1]Source: U.S. Food & Drug, “Use of the "Healthy" Claim on Food Labeling,” fda.gov. The market's advancement is primarily facilitated by innovative physical modification technologies, enabling manufacturers to deliver optimal functional performance without resorting to chemical alterations. This technological progress effectively addresses the industry's challenge of maintaining processing efficiency while adhering to clean label requirements.

Key Report Takeaways

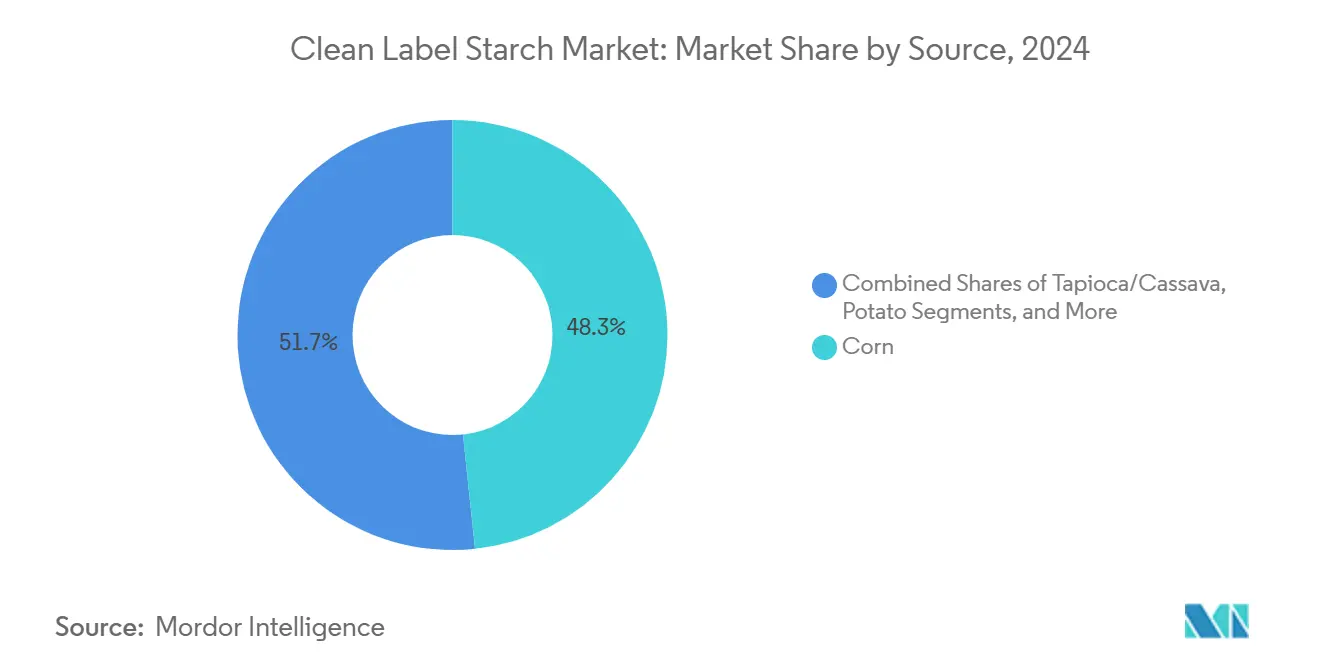

- By source, corn held 48.33% of the 2024 clean label starch market share and tapioca/cassava is forecast to grow at a 7.48% CAGR between 2025-2030.

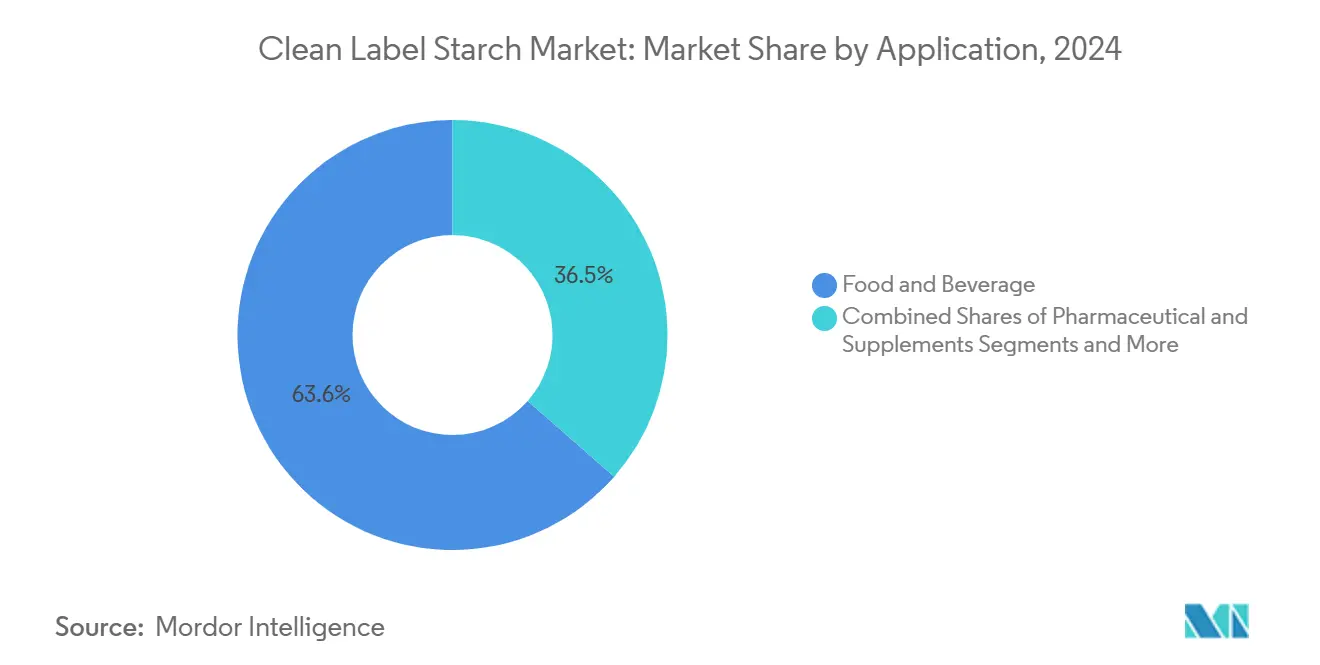

- By application, food and beverage commanded 63.55% of the clean label starch market size in 2024 while pharmaceutical and supplements is advancing at a 7.64% CAGR through 2030.

- By geography, North America led with 37.94% revenue share in 2024 whereas Asia-Pacific is projected to register a 7.83% CAGR from 2025-2030.

Global Clean Label Starch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and minimally processed ingredients | +1.8% | Global with premium positioning in North America & EU | Medium term (2-4 years) |

| Increased consumer focus on food transparency and ingredient labeling | +1.5% | North America & EU core, expanding to APAC | Short term (≤2 years) |

| Preference for plant-based and allergen-friendly foods | +1.2% | Global, accelerated adoption in urban centers | Medium term (2-4 years) |

| Technical advancements in physical starch modification | +0.9% | Manufacturing hubs in North America, EU, Thailand | Long term (≥4 years) |

| Health and wellness trends prioritizing additive-free products | +0.8% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Ability of clean label starch to withstand varied processing conditions | +0.6% | Global manufacturing centers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural and Minimally Processed Ingredients

Consumer demand has evolved significantly, with customers now seeking not only health-focused products but also complete transparency in how ingredients move from source to shelf. The FDA's comprehensive revision of the "healthy" definition represents a crucial shift, requiring manufacturers to include specific food groups that directly match what consumers expect from their products. This regulatory update effectively eliminates confusion between marketing claims and actual nutritional value. In response to market needs, manufacturers have adopted innovative physical modification techniques, such as ultrasound and hydrothermal treatments, which enhance starch performance without relying on chemical processes. This technological advancement directly addresses industry challenges in maintaining product quality while meeting consumer preferences for simpler ingredient lists. The business case for this approach is compelling, as companies implementing these methods have successfully captured price premiums ranging from 15-20% above traditional modified starch products, demonstrating strong market acceptance of clean label initiatives.

Increased Consumer Focus on Food Transparency and Ingredient Labeling

Global regulatory alignment is transforming transparency requirements across major markets, fundamentally changing how companies operate. China's implementation of GB 7718-2025 now demands comprehensive ingredient disclosure, while the EU's General Product Safety Regulation enforces more rigorous traceability standards throughout the supply chain. This move toward standardization provides significant operational advantages for large manufacturers but simultaneously places a substantial financial burden on smaller companies trying to maintain compliance. The FDA's proposed front-of-package nutrition labeling guidelines represent a significant shift toward consumer-friendly nutritional information, which may substantially influence how manufacturers position and market clean label starches in comparison to their synthetic alternatives [2]Source: Federal Register, “Food Labeling: Front-of-Package Nutrition Information,” federalregister.gov. At the state level, Texas and Louisiana have introduced regulations requiring QR code transparency for specific additives, mirroring broader federal trends and creating a complex compliance landscape that naturally favors organizations with deep regulatory expertise. In response to these dual pressures of regulatory requirements and evolving consumer expectations, companies are making substantial investments in sophisticated supply chain documentation systems that can effectively validate clean label claims through comprehensive, traceable data.

Preference for Plant-Based and Allergen-Friendly Foods

Plant-based products now address environmental and ethical concerns beyond dietary preferences, with clean label starches functioning as essential components in alternative protein formulations. In the Asia-Pacific region, consumers prioritize clean label standards in alternative proteins and remain cautious about highly processed products, despite increasing acceptance of plant-based options. The focus on allergen-free products creates premium market opportunities as manufacturers work to remove common allergens while preserving texture and stability. As of 2024, pea starch has emerged as a clean label alternative to traditional corn and potato sources, with market research indicating strong consumer preference for clean labels and willingness to pay premium prices for such products. The combination of plant-based trends and allergen-free requirements provides differentiation opportunities for manufacturers who can deliver functional performance through alternative starch sources.

Technical Advancements in Physical Starch Modification

As of 2024, physical modification technologies are becoming commercially viable, with techniques such as pulsed electric fields and microfluidization enhancing functionality without chemical additives. Green Plains' Clean Sugar Technology facility demonstrates this advancement through its commercial-scale implementation, producing substantial volumes of low-carbon dextrose with significantly lower greenhouse gas emissions than traditional methods. Thermal technologies, including drum drying, extrusion, and the DIC process, prove cost-effective while maintaining safety standards that align with clean label requirements. However, scaling these technologies while remaining economically competitive with chemically modified alternatives requires substantial capital investment, giving an advantage to established manufacturers with research capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent supply chain demands for high-quality, non-GMO raw materials | -1.2% | Global, with acute pressure in North America & EU | Short term (≤ 2 years) |

| Higher research and development investment required to innovate without chemical modification | -0.8% | Manufacturing centers with R&D capabilities | Long term (≥ 4 years) |

| Potential for allergen cross-contamination | -0.5% | Global manufacturing facilities | Medium term (2-4 years) |

| Limited shelf-life improvement compared to synthetic counterparts | -0.4% | Global, particularly affecting export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Supply Chain Demands for High-Quality, Non-GMO Raw Materials

The complexity of non-GMO ingredient sourcing continues to present significant challenges in the market as consumer demand consistently surpasses the available certified supply. In response to this market dynamic, major agricultural companies like Cargill have established specialized producer programs to ensure a stable supply of raw materials. The substantial price premiums associated with non-GMO crops introduce financial pressures that impact manufacturers' ability to maintain competitive pricing, particularly in market segments where price sensitivity is high. The rigorous supply chain verification process necessitates comprehensive documentation and regular testing protocols, which not only increases operational complexity but also requires substantial working capital investments. Despite Japan's Ministry of Agriculture data demonstrating minimal cross-contamination risks between GM and non-GM crops, strong consumer preferences continue to necessitate strict segregation protocols, adding layers of complexity to logistics operations. The geographic concentration of non-GMO crop production in specific regions exposes manufacturers to potential supply disruptions, compelling them to develop robust risk mitigation strategies through diversified sourcing approaches and establishing long-term contractual partnerships with producers.

Higher Research and Development Investment Required to Innovate Without Chemical Modification

Physical modification research demands significant upfront capital investment, often running into millions of dollars, while offering uncertain commercial returns. This financial burden particularly affects smaller manufacturers who aim to position their products with clean labels in the market. The intricate process of achieving comparable functionality through physical methods necessitates not only advanced equipment but also a team of skilled technicians and researchers - resources typically available to established companies with well-developed research and development facilities. The complex web of patents surrounding physical modification techniques creates significant intellectual property challenges, making it difficult for new companies to access and implement these technologies. In the realm of natural alternatives, while cross-linked starch development using compounds like citric acid shows encouraging results, manufacturers must invest considerable time and resources in validation studies to ensure these products perform as effectively as their chemically modified counterparts. The absence of clear regulatory guidelines for new physical modification processes across various regions introduces additional market uncertainties, compelling companies to carefully weigh their investment decisions and market entry strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Corn Dominance Faces Diversification Pressure

The global starch market landscape demonstrates corn's continued dominance, holding a substantial 48.33% market share in 2024. This strong market position stems from corn's extensive supply chain networks and sophisticated processing infrastructure developed over decades. In response to market dynamics and risk management strategies, manufacturers are increasingly turning to tapioca/cassava as an alternative raw material source, which is projected to achieve a notable growth rate of 7.48% CAGR through 2030.

Thailand has established itself as a pivotal player in the global starch industry, leading worldwide cassava production with an impressive processing capacity exceeding 30 million tons annually, of which 80% is converted into starch [3]Source: Thai Tapioca Starch Association, “Tapioca Background,” thaitapiocastarch.org. This significant production volume has created a stable pricing environment that effectively challenges corn's historical cost advantages in the market. Within the premium market segment, potato starch maintains its essential role in specific applications, particularly where product clarity and taste neutrality are crucial quality parameters. While wheat starch offers distinct functional benefits in certain manufacturing processes, its market expansion faces increasing resistance from the growing consumer shift toward gluten-free alternatives.

By Application: Pharmaceutical Growth Outpaces Food Innovation

The pharmaceutical and supplements segment is projected to achieve a compound annual growth rate of 7.64% through 2030. This growth is primarily driven by manufacturers expanding clean label ingredients beyond traditional food applications. In response to market demands, excipient manufacturers are actively developing natural alternatives to replace synthetic binders and disintegrants in their formulations. A notable example is Roquette's LYCATAB pregelatinized starch, which has demonstrated strong commercial viability in oral dosage forms. Its compliance with both European and United States Pharmacopeia standards has enabled broad market access across global regions.

The food and beverage segment currently maintains a dominant position with a 63.55% market share in 2024. However, this segment is experiencing significant market maturation challenges. This shift occurs as clean label ingredients transition from being a distinctive competitive advantage to becoming an essential industry requirement. Manufacturers in this space must now navigate a market where clean label formulations are considered a baseline expectation rather than a differentiating factor.

Geography Analysis

North America maintains its dominant position in the clean label market, commanding a substantial 37.94% market share in 2024. This leadership stems from the region's well-established regulatory infrastructure and sophisticated consumer base that prioritizes premium, transparent food products. The market benefits from significant regulatory developments, including the FDA's comprehensive revision of the "healthy" definition and proposed front-of-package labeling regulations. State-level initiatives continue to shape the landscape, with Texas implementing stringent ingredient disclosure requirements. The region's manufacturing capabilities are expanding, as evidenced by Jungbunzlauer's strategic USD 200 million investment in a state-of-the-art xanthan gum facility in Port Colborne, Ontario, which capitalizes on local corn resources while implementing advanced environmental protection measures.

The Asia-Pacific region emerges as the fastest-growing market, projecting a robust 7.83% CAGR through 2030. This remarkable growth trajectory is driven by rapid industrialization, strengthening food safety standards, and evolving regulatory frameworks. China's implementation of GB 7718-2025 food labeling standards demonstrates the region's commitment to transparency and alignment with global clean label trends, including specific provisions to prevent misleading claims such as "no food additives." The region's expanding manufacturing capabilities and efficient supply chain networks further support this growth momentum.

Europe maintains its significant market presence through sophisticated regulatory mechanisms, including comprehensive labeling requirements under Regulation 1169/2011 and new sustainability mandates through Directive 2024/825. The implementation of the EU's General Product Safety Regulation in December 2024 introduces enhanced traceability requirements, creating advantages for established manufacturers with robust documentation systems. These regulations particularly focus on preventing misleading environmental claims and ensuring product transparency, reinforcing Europe's position in the global clean label market.

Competitive Landscape

The clean label starch market demonstrates moderate concentration, where companies actively reshape competitive dynamics through strategic consolidation efforts. This transformation is evident in the increasing focus on vertical integration and technology acquisitions across the industry. A notable example is Tate & Lyle's significant investment of USD 1.8 billion in acquiring CP Kelco, which underscores the substantial value placed on nature-based ingredients. This strategic move reflects the industry trend where pectin and specialty gums command higher profit margins compared to conventional starches, while enabling companies to position their products with clean label credentials across diverse applications.

The competitive landscape is increasingly influenced by technological capabilities, particularly in physical modification processes, which create substantial barriers to entry for smaller market participants lacking robust research and development infrastructure. Green Plains has positioned itself as an industry pioneer with its Clean Sugar Technology, achieving a remarkable 40% reduction in greenhouse gas emissions while maintaining the functional performance that justifies premium pricing in the market. Similarly, Ingredion's substantial investment of USD 100 million in its Indianapolis facility expansion demonstrates the company's commitment to developing texture and healthful solutions. This strategic investment proved successful, generating an impressive 34% growth in operating income during 2025, validating the economic viability of clean label positioning in the market.

While emerging companies are actively exploring alternative sources and innovative processing technologies, they encounter significant challenges in scaling their operations to commercial levels. This situation naturally favors established manufacturers who possess well-developed distribution networks and extensive regulatory expertise. The increasing number of patent applications focusing on physical modification techniques, including advanced processes like microfluidization and pulsed electric field applications, creates strong intellectual property protection. These patent portfolios effectively limit technology accessibility to competitors and help maintain competitive advantages for companies leading in innovation, shaping the future direction of the clean label starch market.

Clean Label Starch Industry Leaders

-

Cargill, Incorporated

-

Tate & Lyle PLC

-

Archer Daniels Midland

-

Ingredion Incorporated

-

Roquette Frères

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ingredion announced a USD 100 million expansion to its Indianapolis westside plant to enhance production capabilities and support future growth in texture solutions, reflecting commitment to clean label product demand

- November 2024: Roquette Frères issued EUR 600 million in senior notes to finance acquisition of Target Business from International Flavors and Fragrances, strengthening capabilities in clean label starch market and food nutrition sectors

- November 2024: Tate & Lyle completed acquisition of CP Kelco for USD 1.8 billion, creating leading global specialty food and beverage solutions business with enhanced capabilities in sweetening, mouthfeel, and fortification

Global Clean Label Starch Market Report Scope

| Corn |

| Tapioca/Cassava |

| Potato |

| Wheat |

| Others |

| Food and Beverage | Bakery and Confectionery |

| Snacks | |

| Soups, Sauces and Dressings | |

| Dairy Products | |

| Meat and Meat Products | |

| Others | |

| Pharmacuetical and Supplements | |

| Personal care and Cosmetics | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Corn | |

| Tapioca/Cassava | ||

| Potato | ||

| Wheat | ||

| Others | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Snacks | ||

| Soups, Sauces and Dressings | ||

| Dairy Products | ||

| Meat and Meat Products | ||

| Others | ||

| Pharmacuetical and Supplements | ||

| Personal care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the clean label starch market by 2030?

The market is projected to reach USD 3.34 billion by 2030, expanding at a 6.59% CAGR.

Which source segment is expected to register the fastest growth to 2030?

Tapioca/cassava is forecast to record a 7.48% CAGR as manufacturers diversify away from corn.

Why is the pharmaceutical sector gaining momentum in clean label starch adoption?

Regulatory pressure to replace synthetic excipients and rising consumer trust in natural ingredients push pharmaceutical adoption, which is growing at a 7.64% CAGR.

How are recent regulatory changes influencing regional market dynamics?

Updated FDA definitions, EU sustainability directives, and China’s GB 7718-2025 collectively elevate transparency standards, driving global demand for clean label starch.

How concentrated is the global supplier base?

The top ingredient companies hold enough share signifying moderate consolidation with room for niche innovators.

Page last updated on: