Modified Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.15 Billion |

| Market Size (2031) | USD 19.90 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

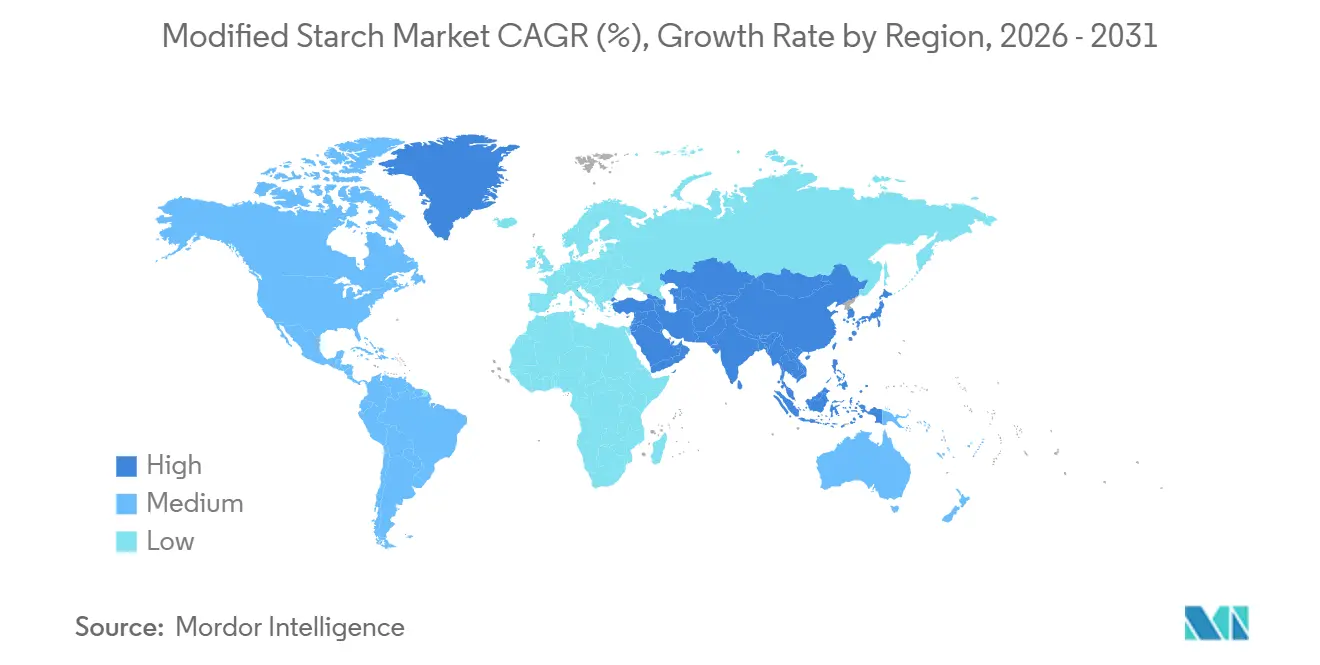

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Modified Starch Market Analysis by Mordor Intelligence

The Modified Starch Market size was valued at USD 16.65 billion in 2025 and is estimated to grow from USD 17.15 billion in 2026 to reach USD 19.90 billion by 2031, at a CAGR of 3.02% during the forecast period (2026-2031). Factors like urbanization, population growth, and changing eating habits, especially in developing countries, are driving this growth. Companies in the market are expanding their reach through partnerships and entering new regions. The rising demand for processed and ready-to-eat foods is creating opportunities for starch producers, while advancements in production technology are improving efficiency. The market is also growing due to its increasing use in industries such as food and beverage, paper, textiles, and pharmaceuticals. Consumers are showing more interest in clean-label products and natural ingredients, pushing manufacturers to create innovative modified starch solutions. The Asia-Pacific region is a major growth area, with strong demand from countries like China and India. Additionally, environmental rules and the focus on sustainability are influencing how products are developed and manufactured in the modified starch industry.

Key Report Takeaways

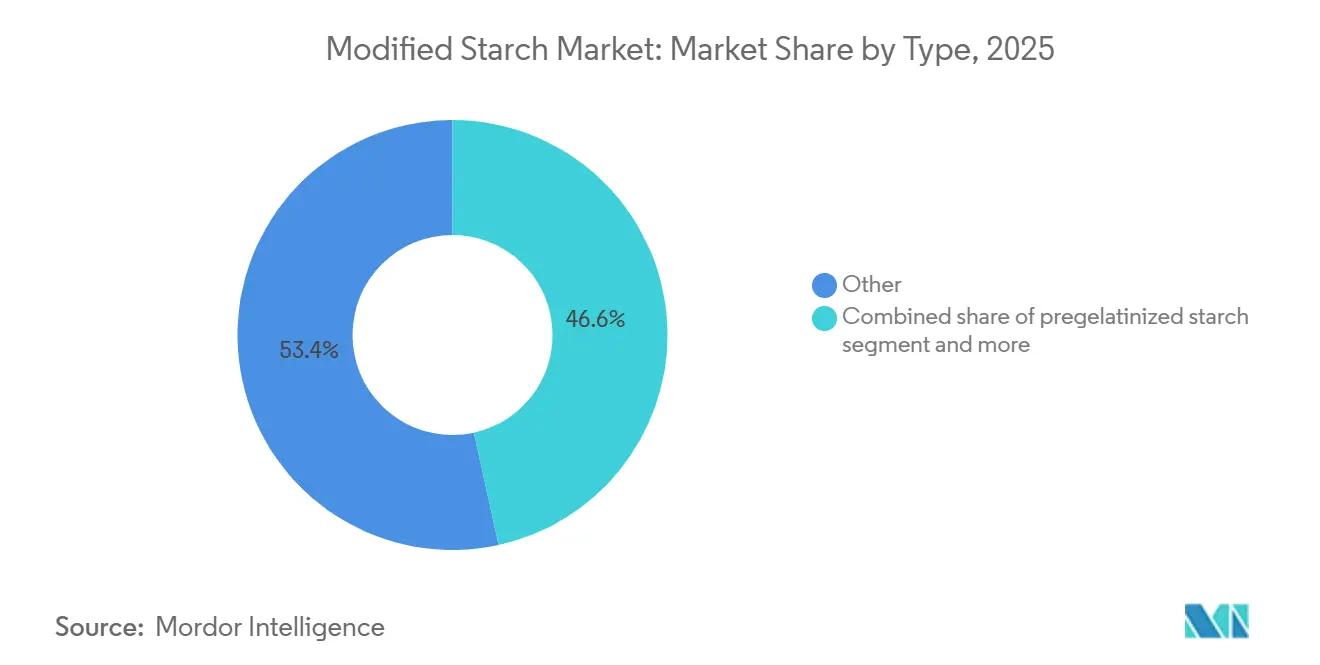

- By type, the other category held 53.44% of the modified starch market share in 2025, whereas oxidized starch is projected to grow at a 5.54% CAGR to 2031.

- By source, maize led with a 70.84% share in 2025, while potato starch is expected to grow at a 3.00% CAGR from 2026 to 2031.

- By form, powder dominated with 80.83% share in 2025; liquid forms are expected to grow at a 2.69% CAGR between 2026 and 2031.

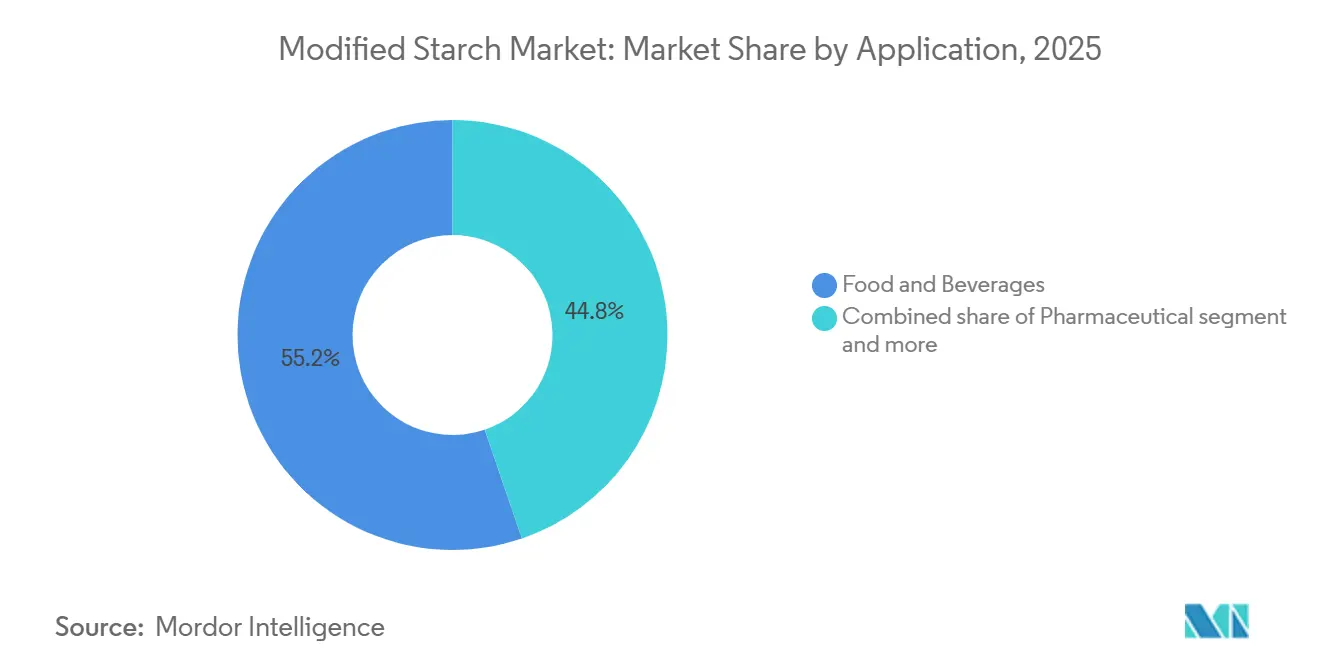

- By application, food and beverage accounted for 55.24% of the modified starch market share in 2025; pharmaceuticals are set to expand at a 3.70% CAGR to 2031.

- By geography, North America contributed a 33.98% share in 2025, whereas Asia-Pacific is expected to register a CAGR of 3.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Modified Starch Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Clean Label Ingredients Boost Modified Starch Consumption | +0.8% | Global, with stronger impact in North America & Europe | Medium term (2-4 years) |

| Expanding Use of Modified Starch in Vegan and Plant-Based Food | +0.6% | North America, Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Modified Starch as a Key Stabilizer in Dairy Products | +0.4% | Global, with significant impact in Asia-Pacific | Short term (≤ 2 years) |

| Increasing Industrial Applications in Paper and Textiles Enhancing Market Reach | +0.3% | Asia-Pacific, North America | Medium term (2-4 years) |

| Functionality of Modified Starch as a Fat Replacer in Low-Calorie Products | +0.2% | North America, Europe | Short term (≤ 2 years) |

| Modified Starch as a Natural Emulsifier in Organic Food Formulation | +0.2% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean Label Ingredients Boost Modified Starch Consumption

The clean label movement has transitioned from a niche trend to a dominant force in the market. Modified starches, which are physically altered rather than chemically treated, have surged in popularity. These starches not only uphold their clean label status but also boast functional enhancements. Food producers are turning to advanced techniques like cold plasma treatment and pulsed electric field technologies. These methods boost starch functionality sans chemical additives, allowing products to uphold clean label claims while enhancing texture and stability. Such technologies empower manufacturers to tweak starch attributes, like gelatinization temperature, viscosity, and freeze-thaw stability—all while preserving the natural ingredient label. This trend isn't confined to food; it's making waves in industrial sectors too. For instance, paper manufacturers are replacing synthetic additives with these modified starches, striking a balance between sustainability and performance. This shift in paper production has bolstered paper strength, improved surface qualities, and enhanced printability, all while lessening environmental repercussions.

Expanding Use of Modified Starch in Vegan and Plant-Based Food

The plant-based food sector's explosive growth has created unprecedented demand for functional ingredients that can replicate the sensory properties of animal-derived products. According to the United States Department of Agriculture data from 2023[1]United States Department of Agriculture, " Plant-Based Food Consumption in Germany", usda.gov., 1.58 million people in Germany followed plant-based diets. Modified starches with improved gelling and water-binding properties play a key role in creating meat analogs with realistic texture and mouthfeel. Advances in starch modification have led to variants designed specifically for plant-based products, which can replicate the fibrous structure of muscle tissue when combined with plant proteins. These specialized starches are not only important for their technical benefits but also for strengthening supply chains. Manufacturers are focusing on ingredients that can be sourced from various agricultural inputs to reduce risks from climate-related disruptions. This focus on application-specific development is driving growth in the modified starch market and benefiting companies that provide customized solutions for the challenges of plant-based formulations.

Modified Starch as key Stabilizer in Dairy Product

Dairy manufacturers are facing growing cost pressures and increasing demand for clean label products. To address these challenges, they are turning to modified starches, which serve multiple purposes by improving texture, stability, and cost efficiency. The latest modified starches provide excellent freeze-thaw stability, which is essential for dairy products. This feature helps extend shelf life and maintain quality even after repeated temperature changes, a key benefit for products distributed through complex cold chains. Additionally, these starches allow manufacturers to lower fat content without affecting the creamy texture, meeting health trends and managing fluctuating input costs. The process of customizing starches for specific dairy applications has given ingredient suppliers with technical expertise a strong competitive edge. This shift has moved the focus from basic production to creating tailored solutions and offering technical support, reshaping the competitive dynamics across the modified starch value chain.

Increase Industrial Application in Paper and Textile Enhancing Market Reach

Modified starches are now being used for more than just traditional sizing and coating, as they address sustainability challenges in the paper and textile industries. Cationic starches are becoming popular as eco-friendly alternatives to synthetic polymers in paper production, where they help retain fibers and reduce wastewater pollution. The EU Starch Industry Decarbonization Roadmap recognizes modified starches as important for cutting greenhouse gas emissions in paper manufacturing, encouraging their adoption. In the textile industry, modified starches are replacing petroleum-based sizing agents, helping manufacturers meet strict environmental rules while improving efficiency. This growing use in industrial applications is creating more stable demand compared to consumer markets, attracting investments from producers looking to reduce reliance on the unpredictable food ingredients market.

Restraints Impact Analysis of Modified Starch Market*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices Impacting Profit Margins | -0.5% | Global, with severe impact in regions with limited agricultural diversity | Short term (≤ 2 years) |

| Regulatory Pressure on Chemically Modified Starches in Food Products | -0.4% | Europe, North America, with gradual spread to Asia-Pacific | Medium term (2-4 years) |

| Health Concerns Around Crosslinked or Oxidized Starch Derivatives | -0.3% | Global, with heightened concern in health-conscious markets | Medium term (2-4 years) |

| Potential Allergenic Concern from Wheat-Based Modified Starch | -0.2% | Global, with particular impact in gluten-sensitive populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices Impacting Profit Margins

The modified starch market faced significant volatility in 2024, as corn prices fluctuated due to extreme weather events and geopolitical disruptions. Recent data from the U.S. Department of Agriculture[2]United States Department of Agriculture, " Grain: World Markets and Trade", usda.gov indicates that corn prices experienced substantial volatility in 2024, affecting manufacturers' ability to maintain consistent pricing. Severe droughts in key corn-producing areas, coupled with ongoing trade restrictions, have driven price fluctuations in the global grain market. As a result, modified starch producers faced squeezed profit margins, finding it challenging to pass on rising costs to customers in a competitive landscape. In a bid to shield themselves from disruptions tied to specific crops, these producers broadened their raw material palette, turning to potato and tapioca alongside corn. However, this pivot demanded hefty investments in both processing equipment and R&D. While diversifying sources mitigated supply risks, it introduced technical hurdles. Each botanical source necessitates distinct modification processes for consistent functionality. These nuances, ranging from temperature control and chemical treatments to processing durations, hampered swift supplier transitions.

Regulatory Pressure on Chemically Modified Starches in Food Products

Global regulatory bodies are increasing scrutiny on chemically modified food additives, requiring strict safety checks. This has driven the industry to adopt physical modification methods and enzyme-assisted processes, which offer similar benefits without being classified as chemical treatments. The shift is fueled by consumer demand for clean-label products and concerns over the long-term effects of chemical modifications. However, companies face challenges in replicating the performance of chemically modified starches, especially for applications needing specific viscosity or stability under extreme conditions. To address this, R&D teams are exploring techniques like heat-moisture treatment, annealing, and high-pressure processing. Advances in enzyme technology are also enabling targeted modifications without chemicals. The changing regulatory environment is reshaping competition, favoring companies with advanced modification capabilities and regulatory expertise. Market leaders are investing in new technologies and research to develop compliant alternatives. This shift is also creating opportunities for specialized ingredient manufacturers offering naturally modified solutions that meet both regulatory and functional needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Modified Starch Market Segment Analysis

By Type:

Oxidised Starch Leads Pharmaceutical InnovationFrom 2026 to 2031, the oxidized starch segment is expected to grow at a CAGR of 5.54%, surpassing the overall growth of the modified starch market. This growth is mainly due to its increasing use in the paper, textile, and food processing industries. Oxidized starch is preferred because it dissolves easily, forms strong films, and provides better viscosity control. In food applications, it improves texture and stability, while in industrial uses, it helps with surface sizing, coating, and binding, making it useful across various industries.

In 2025, the "Other" modified starch segment, which includes specialty starches like resistant starches and dual-modified types, held 53.44% of the global modified starch market, making it the largest category. This growth shows a clear move toward customized starch solutions designed for specific needs, such as clean-label products, better nutrition, and improved processing efficiency. As demand shifts away from traditional single-function starches, manufacturers are focusing on creating tailored, high-performance products to stand out and stay competitive in both food and industrial markets.

By Source:

Corn Dominance Challenged by Supply RisksIn 2025, maize (corn) dominated the modified starch market with a 70.84% share. This is mainly because maize is widely available, cost-effective, and supported by a strong processing system that enables large-scale production. Moreover, maize starch is highly versatile and can be easily modified to meet the needs of industries like food, paper, textiles, and adhesives.

In comparison, potato starch is projected to grow the fastest, with a CAGR of 3.00% between 2026 and 2031. This growth is due to its excellent properties, such as high viscosity, neutral flavor, and strong binding and thickening abilities, which are highly valued in food processing and specialized industrial uses. Additionally, the increasing demand for clean-label and premium products is driving the use of potato-based modified starches, even though they are more expensive to produce than maize starch.

By Application:

Pharmaceuticals Outpace Traditional SectorsIn 2025, the food and beverage sector was the largest user of modified starch, accounting for 55.24% of the total demand. This is because modified starch is widely used as a thickener, stabilizer, binder, and texturizer in products like bakery goods, dairy items, sauces, soups, confectionery, and ready-to-eat meals. It enhances texture, improves shelf life, and withstands tough processing conditions such as heat, shear, and freeze-thaw cycles, making it a key ingredient in modern food production.

In comparison, the pharmaceutical sector is expected to grow the fastest, with a projected CAGR of 3.70% between 2026 and 2031. This growth is driven by the increasing use of modified starch as an excipient in tablet binding, disintegration, and controlled-release drug delivery systems. The pharmaceutical industry is focusing on creating efficient formulations, ensuring consistent drug release, and improving patient compliance, while also meeting the need for cost-effective and biocompatible excipient solutions.

By Form:

Powder Dominates While Liquid Gains MomentumIn 2025, the powder form of modified starch held a dominant 80.83% market share. This is due to its stability, ease of use, and ability to work well in various applications. It is especially popular in food applications, where accurate measurement and even mixing are essential for maintaining product quality. On the other hand, liquid modified starches are gaining popularity, with a projected CAGR of 2.69% from 2026 to 2031. Their growth is driven by benefits like quick solubility and reduced dust issues, which make them suitable for specific processing needs.

Recent improvements in liquid-modified starch formulations have made them more stable and extended their shelf life, solving earlier issues that limited their use. These advancements are particularly useful in continuous processing systems, where skipping the need for powder handling can improve efficiency and lower contamination risks. This shift in product forms shows that even well-established markets can grow through innovations that focus on improving processes, not just product features. This trend is also encouraging collaboration between ingredient suppliers and equipment manufacturers to develop better solutions.

Geography Analysis

North America Modified Starch Market

In 2025, North America held a 33.98% share of the modified starch market, driven by its advanced food processing industry and strong pharmaceutical manufacturing capabilities. The region's large-scale corn production provides a cost advantage for local manufacturers. The USDA's 2024 report on cornstarch handling highlights the rising demand for non-GMO and organic products, creating premium opportunities in the market. Manufacturers in North America are increasingly focusing on sustainability and clean-label products by adopting physical modification techniques. These methods help maintain the natural quality of ingredients while improving their functionality. Regulatory changes are encouraging these innovations, making technical expertise in non-chemical modifications a key competitive factor over large-scale production.

APAC Modified Starch Market

Asia-Pacific is projected to be the fastest-growing region, with a CAGR of 3.32% expected from 2026 to 2031. This growth is fueled by rapid industrialization, the expansion of food processing industries, and increasing pharmaceutical production. China's significant investments in starch processing technologies are enhancing the region's production capabilities, while India's growing pharmaceutical sector is creating demand for specialized excipient-grade modified starches, according to the Indian Council of Agriculture Research data from 2023[3]Indian Council of Agriculture Research, "Modified Cassava Starch in India", ctcri.org. The region's diverse agricultural base, including cassava in Southeast Asia and potato in China, provides opportunities for source diversification beyond corn dependency.

Europe Modified Starch Market

Europe's modified starch market is shaped by strict regulations and strong sustainability initiatives. The EU's Starch Industry Decarbonization Roadmap has set ambitious goals to reduce the environmental impact of starch production. This has led to significant investments in energy-efficient technologies and circular economy practices, making sustainability a key focus in the region.

Regulatory Landscape

Modified starches used in foods are regulated as additives with defined identities and specifications, which shapes both formulation choices and labeling. In the European Union, Regulation (EC) No 1333/2008 maintains the harmonized additive framework for modified starches (E 1400 to E 1452). Commission Regulation (EU) 2026/196 updated specifications for starch sodium octenyl succinate (E 1450) and set transition arrangements, while Commission Regulation (EU) 2025/2058 updated Annexes related to use in foods for particular nutritional uses, including infants and young children. These updates raise the bar for suppliers serving sensitive application segments, especially around documentation for purity, functionality, and intended-use compliance.

In the United States, FDA regulations under 21 CFR 172.892 define permitted treatments and conditions of use for food starch-modified for direct food use, creating a clear compliance route for both chemically and enzymatically processed variants. Globally, Codex Alimentarius (GSFA) provides a reference point for GMP-based use across food categories, but exporters still need to align with destination-market specifications and labeling conventions, which places regulatory affairs capability at a premium for multinational modified starch portfolios.

Value Chain Analysis

The modified starch value chain starts with cultivation and procurement of starch-bearing crops (primarily maize, and also wheat, potato, and tapioca/cassava), followed by wet milling or extraction to produce native starch. Producers then apply physical, enzymatic, and chemical modification steps (including oxidation, crosslinking, substitution, and pregelatinization) to deliver targeted functionality for food and beverage, pharmaceutical excipients, and industrial applications such as paper and textiles. Quality systems, analytical testing, and regulatory compliance (for example, alignment with the EU E14xx framework and US FDA 21 CFR 172.892) run alongside manufacturing as core enabling activities, especially for products supplied into infant nutrition, dairy, and pharmaceutical end uses.

Downstream, modified starches move through ingredient distributors and direct supply contracts to large manufacturers, with application labs and technical service teams supporting specification-setting and reformulation. Key bottlenecks include raw material price volatility linked to weather and trade disruptions, notably for corn, and the geographic concentration of certain feedstocks, such as tapioca supply in parts of Southeast Asia. Capital and permitting intensity for modification plants also matter, particularly where environmental compliance requirements are strict. These constraints support strategies such as source diversification (potato and tapioca alongside corn), tighter supplier qualification and traceability, and closer collaboration with end users on performance-in-use targets to reduce reformulation risk.

Competitive Landscape

The modified starch market exhibits moderate concentration with a score of 6 out of 10, characterized by the presence of established global players alongside regional specialists targeting niche applications. The modified starch market is led by prominent players, including Archer Daniels Midland, Cargill Incorporated, Tate & Lyle, Ingredion, and Agrana Beteiligungs AG. These companies are increasingly focusing on product innovation as their primary strategy, with significant investments in developing clean-label and specialty modified starches to meet evolving consumer preferences.

Strategic patterns reveal a shift from cost leadership to value-added specialization, with leading companies investing in application development capabilities and sustainable sourcing initiatives rather than merely expanding commodity production capacity. White-space opportunities exist in emerging applications such as biodegradable packaging materials and pharmaceutical excipients, where technical barriers to entry create defensible positions for first movers with specialized modification expertise.

Competition intensity varies significantly across application segments, with food ingredients remaining highly competitive while pharmaceutical and industrial applications offer more differentiation potential. The competitive landscape is further shaped by vertical integration strategies, with agricultural processors expanding into higher-value modified starch production to capture margin opportunities beyond commodity processing. This strategic evolution reflects the market's maturation from volume-driven growth to value-based competition, rewarding players who can navigate the technical complexities of specialized applications while meeting increasingly stringent regulatory and sustainability requirements.

Modified Starch Industry Leaders

-

Roquette Freres

-

Ingredion Incorporated

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Tate & Lyle Plc

- *Disclaimer: Major Players sorted in no particular order

Modified Starch Market Companies Covered in this Report

- Cargill Inc.

- Archer Daniels Midland Company

- Ingredion Inc.

- Tate & Lyle PLC

- Roquette Frères

- Südzucker AG (Beneo)

- Emsland-Stärke GmbH

- AGRANA Beteiligungs-AG

- Avebe U.A.

- Tereos Group

- Grain Processing Corp.

- Universal Starch-Chem Allied Ltd.

- Sunar Misir

- China Starch Holdings Ltd.

- Global Bio-Chem Technology Group

- Spac Starch Products (India) Ltd.

- Thai Flour Industry Co.

- Visco Starch

- PT Sorini Agro Asia Corporindo Tbk

- Qingdao CBH Co.

Market Opportunities and Future Outlook

Product development whitespace centers on clean-label and regulatory-aligned solutions that preserve functionality while reducing reliance on chemical modification routes. EU updates, including Commission Regulation (EU) 2026/196 on starch sodium octenyl succinate (E 1450) and the 2025/2058 amendment covering foods for particular nutritional uses, increase the premium for excipient-grade and high-purity food additive grades supported by strong specifications, analytical validation, and customer-facing documentation. This supports opportunities for suppliers with physical and enzyme-assisted modification capabilities (heat-moisture treatment, annealing, high-pressure processing) to back reformulation in applications where labeling and additive acceptability influence purchasing decisions.

Capacity additions and localization initiatives also expand room for new supply relationships, particularly in Asia-Pacific where demand spans food processing and pharmaceuticals. India provides an example of domestic capacity being built closer to end-use growth centers, with Cargill commissioning a corn milling plant in Madhya Pradesh (via Saatvik Agro Processors) in March 2025 and Regaal Resources commissioning an expanded maize processing facility in Kishanganj, Bihar in May 2026, alongside stated plans to introduce additional modified starch products in FY27. For buyers, these investments add regional sourcing options, while for suppliers they heighten the need to differentiate through application-specific performance (dairy stability, plant-based texture, paper sizing efficiency) and sustainability-led process improvements aligned with regional decarbonization roadmaps.

Recent Industry Developments in Modified Starch Market

- June 2026: Ingredion announced a recommended all-cash offer to acquire Tate & Lyle PLC, aiming to broaden its specialty ingredients footprint across texturants and adjacent functional solutions. The deal signals consolidation among scaled ingredient platforms and increases competitive pressure on mid-sized suppliers to differentiate through application development and specialty modified starch portfolios.

- May 2026: Ingredion announced a joint venture and a 9% equity investment in Sanstar Limited in India to expand manufacturing capabilities for corn-based specialty products, including modified starches. The investment strengthens localized supply and technical collaboration in a high-growth consumption geography where regional production helps manage lead times and raw material volatility.

- August 2024: Roquette expanded its texturizing solutions portfolio with four tapioca-based cook-up starches under the CLEARAM TR range for food applications. The update adds formulation options for sauces, dairy desserts, yogurt, and bakery fillings, reinforcing the shift toward application-specific starch systems rather than commodity-style offerings.

Modified Starch Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market is defined as the value of modified starch sold for use as a functional ingredient in food, feed, paper, textiles, pharmaceuticals, and similar end uses, regardless of whether modification is physical, enzymatic, or chemical.

Scope exclusions: We exclude native starch, high-fructose sweeteners, maltodextrin derivatives, and bioplastic resin blends from the market totals.

Segments Covered in This Report

-

By Type

- Pregelatinized Starch

- Acid Modified

- Oxidised Starch

- Cationic Starch

- Acetylated Starch

- Others

-

By Source

- Maize

- Wheat

- Potato

- Tapioca

- Others

-

By Form

- Powder

- Liquid

-

By Application

- Food and Beverage

- Pharmaceutial

- Personal Care & Cosmetics

- Animal Feed

- Textile

- Paper and Corrugating

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base on starch supply, demand, and trade, so the later model inputs were not guessed. Public sources were used to anchor the macro picture, such as FAOSTAT for crop and starch feedstock availability, UN Comtrade for trade flows, and USDA publications for price and utilization signals where available.

We then added evidence on end use pull and product rules by reading sources such as the US FDA and EFSA for food ingredient and labeling context, plus association and standards bodies publications that explain usage in paper, packaging, and industrial applications. Company filings, investor presentations, and trusted press were also reviewed to understand capacity additions, product mix shifts, and pricing commentary. In a few spots, paid subscriptions for company financials and patent databases were used to cross-check revenue ranges and innovation activity, but only as supporting inputs. These examples are not exhaustive, and many other public sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on pricing, conversion factors, and application mix, since those items drive most of the value swings in modified starch. We spoke with a mix of producers, distributors, and large buyers across food processing and industrial uses, and the questions were kept consistent so inputs could be compared across regions (APAC, EMEA, and the Americas). When answers diverged, follow-ups were done with a different respondent type so the final assumption set reflects how the market is actually purchased and specified.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 21% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, with the top-down view doing most of the heavy lifting. In simple terms, we reconstructed demand pools by linking starch derivative consumption to downstream output indicators, and then applied modified-starch penetration rates by application where substitution with native starch is common.

A few practical inputs were tracked because they move the totals in a visible way, such as processed food output trends, paper and packaging production indexes, industrial adhesive demand signals, feed usage trends, and regional price spreads between native starch and modified grades. Pricing was handled through application-weighted average selling prices, which were adjusted for product mix changes and then checked against procurement feedback from interviews. After the top-down totals were produced, selective bottom-up approximations were used as a check, like sampling supplier sales ranges by region and validating volume-to-value consistency through typical price bands.

Forecasts were developed using scenario analysis supported by short time-series smoothing on the core demand indicators, and then refined with expert views on capacity additions and expected pricing progression. Where bottom-up information was missing for smaller countries or niche industrial uses, gaps were filled using proxy indicators like industrial output and food manufacturing scale, and then normalized so regional totals stayed consistent with the broader model logic.

Data Validation & Update Cycle

Model outputs were validated through multiple steps, starting with internal consistency checks across volume, price, and implied consumption by end use. We then compared the results against independent signals like trade direction, crop-linked cost movements, and major capacity announcements, and any unusual jumps were reviewed again before sign-off.

If an assumption materially shifts the market level, respondents are re-contacted and the desk evidence is revisited so the change is explainable and repeatable. Reports are refreshed on an annual cycle, and interim updates are triggered when large events occur, such as a major capacity change or a sharp feedstock price swing. Before delivery, the latest data is rechecked so clients receive an up-to-date view.

Mordor Intelligence's Modified Starch Market Sizing Compared With Other Published Estimates

Published market sizes for modified starch often do not match because the scope lines are drawn differently and the pricing logic is not handled the same way across end uses. Gaps usually come from what is counted as modified starch versus adjacent starch derivatives, the year used for pricing conversion, and how industrial applications are scaled when public data is thin.

Some estimates broaden the pool by blending in nearby carbohydrate derivatives or by using a single blended price across food and industrial grades, which can move the total even if volumes are similar. The split mainly comes from scope and price construction: Mordor Intelligence keeps the count limited to modified starch sold into defined applications and keeps native starch, sweeteners, and maltodextrin derivatives out, and then applies application-weighted ASPs that are checked through buyer interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.15 B (2026) | |

| Industry Report A | USD 14.48 B (2024) | Uses a different base year and shorter forecast window, and the published snapshot does not clarify exclusions, so adjacent starch derivatives and blended pricing across grades may compress the reported value versus an application-weighted build. |

| Industry Report B | USD 13.20 B (2024) | Anchors the market on a 2024 base and a long-range 2034 forecast, and it appears to rely on broad segment buckets, which can understate value if industrial grade pricing and regional mix shifts are not updated with recent capacity and procurement signals. |

Looking across the figures, the spread is explained less by growth expectations and more by what each publisher counts and how pricing is carried into the base year. By tying the total to clear end use demand indicators and then validating the ASP and mix assumptions through interviews, the estimate stays traceable to inputs that can be checked and updated in a repeatable way.

Key Questions Answered in the Report

What is the current value of the modified starch market?

The modified starch market size is USD 17.15 billion in 2026 and is forecast to reach USD 19.90 billion by 2031 on a 3.02% CAGR.

Which type is the fastest growing?

Oxidized starch is projected to grow at a 5.54% CAGR.

Why is Asia-Pacific the quickest-growing region?

Rising cassava and potato processing, coupled with expanding drug manufacturing in China and India, drives a 3.32% CAGR for the region.

How are clean-label demands affecting the market?

Brands seek physically or enzymatically modified starches that avoid chemical processing, allowing “natural” claims and commanding premium prices.

Page last updated on: