Potato Market Size and Share

Potato Market Analysis by Mordor Intelligence

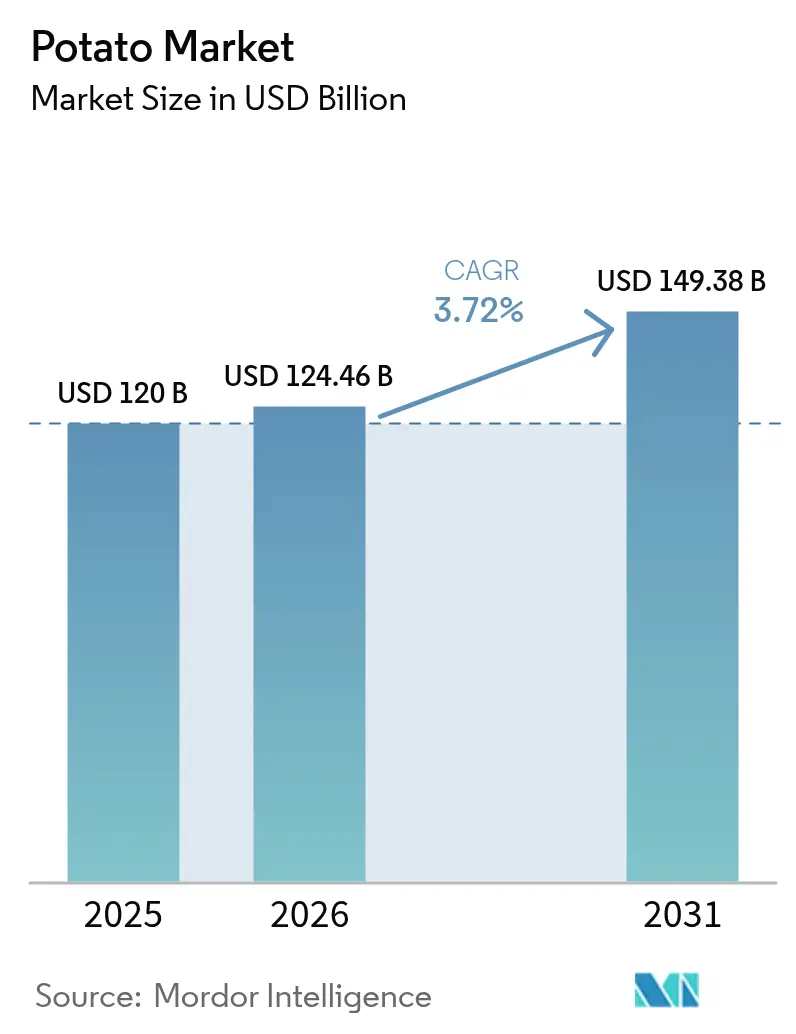

The potato market size was valued at USD 120 billion in 2025 and estimated to grow from USD 124.46 billion in 2026 to reach USD 149.38 billion by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). Rising demand from frozen processors, aggressive quick-service restaurant expansion, and adoption of climate-smart agronomy keep volumes growing even as weather shocks and regulatory costs create pricing volatility. Processors are locating new plants closer to croplands to trim freight costs, while growers invest in controlled-environment seed systems that lift yields and reduce disease losses. Government-backed breeding programs for drought and heat tolerance are gaining momentum in Africa, South Asia, and parts of Europe. Together, these forces are reshaping trade flows, prompting exporters to pivot toward higher-value cuts and organic offerings as consumer preferences shift toward premium and sustainably grown products.

Key Report Takeaways

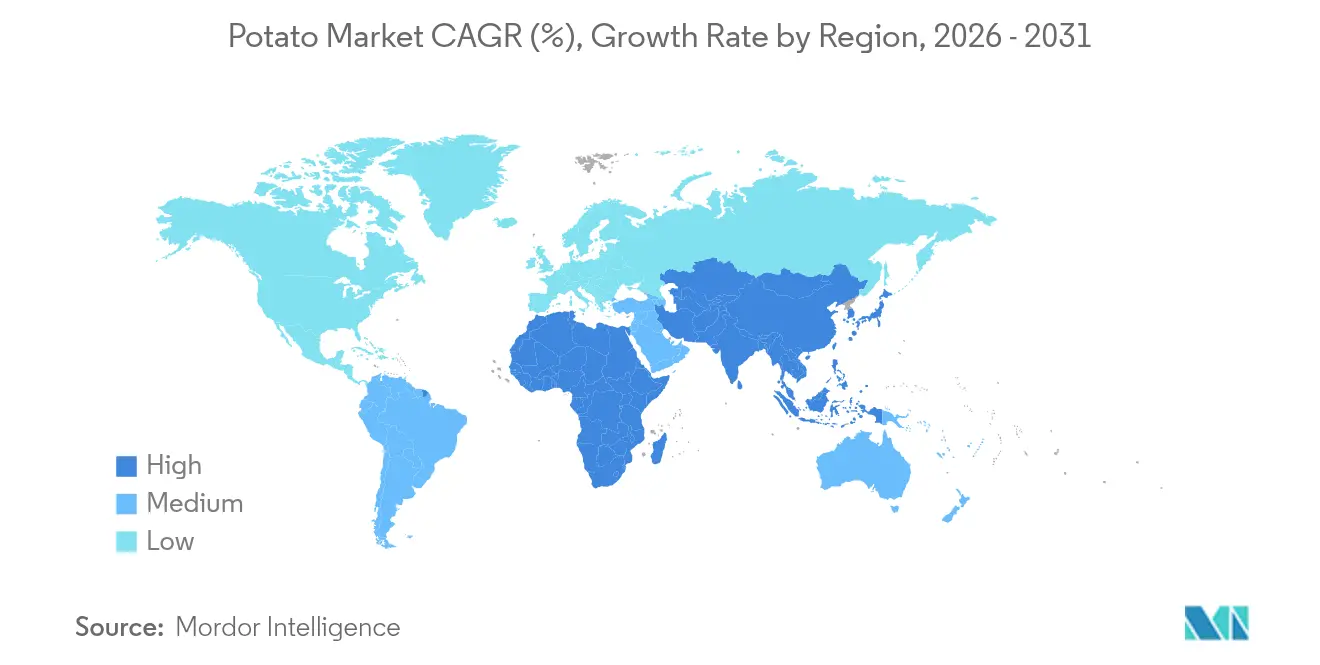

- By consumption volume, Asia-Pacific commanded 50.18% of global potato demand in 2025; Africa is anticipated to register the highest 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Potato Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from frozen potato product processors | +1.2% | Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in quick-service restaurant chains | +0.9% | Global focus on Asia-Pacific, Africa | Short term (≤ 2 years) |

| Government support for climate-smart potato breeding | +0.6% | Europe, Africa, South Asia | Long term (≥ 4 years) |

| Expansion of controlled-environment agriculture for seed potatoes | +0.4% | Europe and North America | Medium term (2-4 years) |

| Increasing adoption of regenerative farming practices | +0.2% | Global, priority in Africa and South America | Long term (≥ 4 years) |

| Emerging carbon-credit revenue streams for growers | +0.1% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Frozen Potato Product Processors

Industrial buyers now account for 60% of commercial output in developed economies as retail and institutional frozen segments join traditional QSR channels. McCain Foods invested EUR 350 million (USD 385 million) in regenerative supply programs covering 71% of its growers to ensure a steady raw-material flow and sustainability credentials. Premium cuts and organic variants command price uplifts that offset higher input costs for growers. Co-location of plants near croplands is reducing cold-chain spending and shrinkage. The push for plant-based alternatives is actually boosting potato volumes because processors rely on its familiar texture and starch profile.

Growth in Quick-Service Restaurant Chains

McDonald’s plans 1,000 new Chinese outlets in 2025, aiming for 10,000 units by 2028, a 67% network jump that will intensify local procurement of fries-grade tubers. Chains are locking in multi-year contracts that reward growers meeting tight solids, sugar, and size specs, pushing specialty varieties into wider cultivation. Digital delivery platforms extend reach beyond shopping malls into suburban districts, raising throughput for central kitchens. Regional QSR operators across Africa and South America are replicating this model, creating cluster demand for frozen inputs and supporting new cold-storage projects.

Government Support for Climate-Smart Potato Breeding

Heat and drought cut Russia’s 2024 harvest by 14.5% to 7.3 million metric tons, highlighting the urgency of tolerant cultivars. CGIAR pipelines target 15-20% yield stability lifts under stress. Kenya’s adoption of biofortified lines raised farm output 30% while improving vitamin A intake. Regulatory fast-track channels in the EU now trim variety approval cycles to six years, accelerating commercialization. Integration of digital advisory tools speeds on-farm uptake and fertilizer optimization.

Expansion of Controlled-Environment Agriculture for Seed Potatoes

Aeroponic units yield 900 mini-tubers per m², versus 8 in soil, slashing land needs by 80%. Indonesia’s agriculture ministry reports break-even at 3,507 tubers with an R/C ratio of 1.4, making the tech viable for commercial adoption. Dutch firms lead rollouts, cutting generation time from 18 to 12 months and boosting disease-free certification rates. Precision nutrient delivery trims fertilizer use by 60% yet lifts output to 75%.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of farm-gate prices due to weather shocks | -0.8% | Global, with highest impact in Europe and North America | Short term (≤ 2 years) |

| Stringent pesticide residue regulations | -0.5% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Supply-chain disruptions from geopolitical conflicts | -0.6% | Europe and Asia-Pacific, with spillover effects globally | Short term (≤ 2 years) |

| Rising competition from alternative carbohydrates (e.g., cassava) | -0.4% | Asia-Pacific and Africa, with growing impact in South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of Farm-Gate Prices Due to Weather Shocks

European prices jumped 23% in 2024 after drought curbed yields, forcing buyers to seek imports at premiums[1]Source: European Commission, “Agricultural Price Report 2024,” ec.europa.eu. Russia’s shortfall redirected flows from China, whose exports leaped fivefold to 46.7 thousand t, demonstrating how regional shocks echo through global trade. Insurance and forward contracts partly buffer risk, but coverage gaps persist in emerging markets where exposure is greatest.

Stringent Pesticide Residue Regulations

EU limits on glyphosate and neonicotinoids lifted rejection rates for non-compliant shipments and pushed exporters to spend USD 500 per consignment on residue testing[2]Source: European Food Safety Authority, “Pesticide Residue Monitoring 2024,” efsa.europa.eu . Smallholders face cash-flow strain during the two-to-three-year transition to organic or integrated pest programs, which may initially dent yields by 10-15%. Divergent maximum residue levels across markets complicate compliance for global traders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific retains 50.18% of worldwide potato consumption in 2025. China’s 95.6 million-ton crop and India’s surge in new processing lines approved by the Ministry of Food Processing Industries underpin the region’s dominance and accelerate demand for on-farm cold storage and logistics upgrades. The Ministry of Commerce confirmed that McDonald’s China subsidiary secured foreign-investment clearance for a network expansion to 10,000 outlets by 2028, a move anticipated to lock in long-term contracts for fries-grade potatoes Regional growth over the next five years will rely on the rollout of aeroponic seed units and sensor platforms to smaller producers, initiatives already funded through the Asian Development Bank’s AgriTech corridor program.

Africa delivers the fastest regional gains, with 5.08% CAGR through 2031. Nigeria’s National Bureau of Statistics attributes rising output to government-financed irrigation corridors in Kaduna and Plateau States that lifted yields 18% over two seasons. Kenya’s Ministry of Agriculture reports that distribution of foundation seed from aeroponic hubs increased certified-seed use among smallholders from 5% to 18% in 2024, translating into a 22% yield jump. South Africa’s Department of Trade, Industry and Competition cleared two greenfield processing plants that will double national frozen-fries capacity by 2026, while Egypt’s General Authority for Investment approved incentives that encourage multinational processors to locate cold-chain warehouses near Red Sea ports. Sustained growth hinges on timely road and cold-storage upgrades under the African Development Bank’s Special Agro-Industrial Processing Zone program.

Russia’s Federal State Statistics Service reported that adverse weather cut the 2024 harvest 14.5% to 7.3 million metric tons, underscoring climate risk across the wider region. Maintaining competitiveness through 2030 will require deeper uptake of regenerative farming methods supported by the EU Common Agricultural Policy and rapid deployment of heat-tolerant cultivars certified by the Community Plant Variety Office.

Recent Industry Developments

- December 2024: McCain Foods completed its EUR 350 million (USD 385 million) regenerative agriculture market rollout covering 71% of growers.

- October 2024: EarthFresh acquired Mountain King Potatoes, widening U.S. retail distribution

Global Potato Market Report Scope

Potato (Solanum tuberosum) is a tuber crop that originates from tropical areas of high altitudes.

The Potato Market is segmented by Geography into North America, Europe, Asia-Pacific, South America, and Africa. The report includes the Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis of potatoes globally. The report offers market estimation and forecast in value (USD thousand) and volume (metric ton).

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Europe | Russia |

| France | |

| United Kingdom | |

| Italy | |

| Germany | |

| Spain | |

| Belgium | |

| Netherlands | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Middle East | Turkey |

| Iran | |

| Africa | South Africa |

| Egypt |

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Russia | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Germany | ||

| Spain | ||

| Belgium | ||

| Netherlands | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Middle East | Turkey | |

| Iran | ||

| Africa | South Africa | |

| Egypt | ||

Key Questions Answered in the Report

How large is the potato market in 2026?

The potato market size reached USD 124.46 billion in 2026 and is forecast to grow at a 3.72% CAGR to reach USD 149.38 billion by 2031.

Which region leads global consumption?

Asia-Pacific holds the largest consumption share at 50.18%, powered by large-scale production in China and India.

Why do processors favor contract farming?

Contracts secure uniform tuber quality, lower procurement risk, and allow processors to align agronomic practices with sustainability pledges.

What new industrial uses are emerging?

Potato starch is being blended into bio-plastic resins for compostable cutlery and packaging, offering processors a route to diversify beyond food.

Page last updated on: