India Agriculture Industry Analysis by Mordor Intelligence

The India agriculture market size is expected to grow from USD 452 billion in 2025 to USD 471.03 billion in 2026 and is forecast to reach USD 578.89 billion by 2031 at 4.21% CAGR over 2026-2031. Strong government spending, broadened credit access, and rapidly growing digital infrastructure are combined to lift productivity and earnings across commodity segments[1]Source: Press Information Bureau, “Union Budget 2025-26 Highlights Agriculture Priorities,” pib.gov.in. Digital platforms that link 11 crore farmers to formal finance, subsidies, and advisory services are already cutting transaction costs and improving price discovery. Robust foodgrain output of 354 million tons in 2024-25 reflects favorable monsoon conditions, higher minimum support prices, and wider use of improved seed cultivars[2]Source: Assam Tribune Staff, “Foodgrain Output Hits New Record,” assamtribune.com. Trade reforms that streamline export certification and expand e-commerce hubs are widening access to premium overseas buyers, even as import substitution missions target edible oils and pulses deficits.

Key Report Takeaways

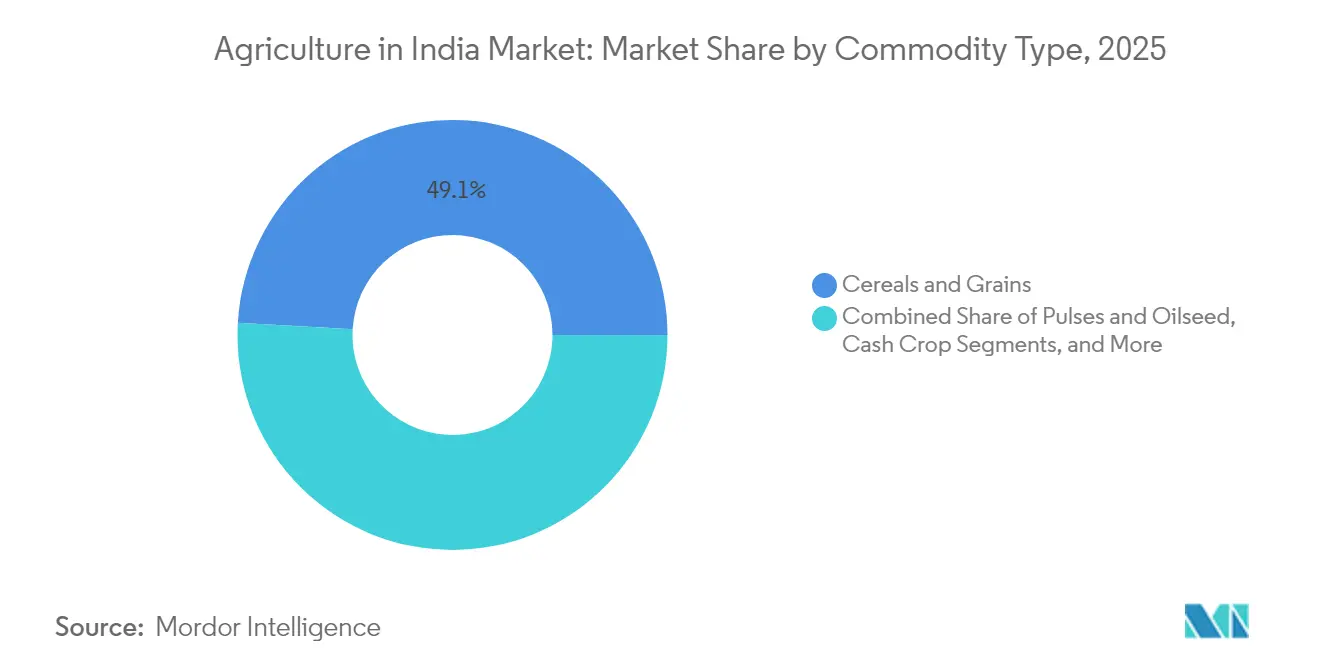

- By commodity type, cereals and grains held 49.10% of the India agriculture market share in 2025, and fruits and vegetables are projected to expand at a 7.42% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Agriculture Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government support through subsidies and policies | +1.2% | National, with higher impact in Punjab, Haryana, Uttar Pradesh | Medium term (2-4 years) |

| Rising adoption of agri-tech and mechanization | +0.8% | National, with early gains in Maharashtra, Karnataka, Gujarat | Long term (≥ 4 years) |

| Growing demand for organic and sustainable farming | +0.6% | National, with a concentration in urban markets and export zones | Long term (≥ 4 years) |

| Expanding export demand via new trade agreements | +0.5% | National, with a focus on coastal states and border regions | Medium term (2-4 years) |

| Carbon-credit monetization from regenerative farming | +0.3% | National, with pilot programs in 8 states initially | Long term (≥ 4 years) |

| Climate-resilient seed cultivars boosting yields | +0.4% | National, with priority in drought-prone and flood-affected areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Support Through Subsidies and Policies

The Union Budget 2025-26 increased the Kisan Credit Card limit to Rs 5 lakh, unlocking larger working capital lines for smallholders and easing input purchases at critical crop stages. Prime Minister Dhan-Dhaanya Krishi Yojana channels resources to 100 low-productivity districts, bundling irrigation, precision farming training, and risk-mitigation tools. Minimum support price adjustments for 2024-25 favor oilseeds such as nigerseed and sesamum, encouraging diversification into high-value crops. Input subsidies, which account for 73% of the agriculture budget, reduce fertilizer and energy costs, creating a positive cycle of investment, productivity, and rural consumption.

Rising Adoption of Agri-tech and Mechanization

A Rs 6,000 crore allocation for digital agriculture infrastructure is funding AI-based crop surveys, drone-enabled nutrient mapping, and app-based credit scoring, helping farmers access formal loans within 24 hours. National mechanization now stands at 47%; Punjab and Haryana exceed 40-45%, while northeastern states remain largely manual, revealing significant headroom for expansion. The farm machinery market is forecast to grow from USD 16.73 billion in 2024 to USD 25.15 billion by 2029, driven by labor scarcity and better cash flows. Precision tools can boost yields by 30% and cut water and fertilizer use by 15-20%, improving profitability and resource efficiency.

Growing Demand for Organic and Sustainable Farming

Urban consumers are fueling a projected 25.25% CAGR for certified organic products through 2027, rewarding farms that adopt pesticide-free practices and traceability systems. Carbon-credit programs in eight states have issued the country’s first farm-generated credits, delivering a new income stream for regenerative growers[3]Source: Indian Brand Equity Foundation, “Agricultural Export Performance,” ibef.org. Policy support for natural farming is deepening, with budget incentives for bio-inputs and AI-guided nutrient applications that protect soil microbiomes. Community seed banks preserve climate-resilient indigenous varieties, diversifying genetic resources while reinforcing farmer rights.

Expanding Export Demand via New Trade Agreements

Agricultural exports climbed 6.5% year-on-year to USD 37.5 billion for April-December 2024, defying global volatility. The Foreign Trade Policy 2024 promotes USD 2 trillion total exports by 2030, positioning agri-produce as a flagship contributor through simplified digital documentation and warehousing corridors. Spices recorded 51.01% growth, and coffee showed 40.3% growth in March 2024 shipments, aided by targeted quality and branding programs. Collaboration with Israel on water-efficient farming and tactical rice exports to food-insecure nations demonstrates the sector’s agility in balancing domestic needs with global opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented landholdings and declining soil fertility | -0.7% | National, with a severe impact in northern and eastern states | Long term (≥ 4 years) |

| Vulnerability to climate change and extreme weather | -0.5% | National, with higher impact in rain-fed areas | Medium term (2-4 years) |

| Inadequate cold-chain and storage infrastructure | -0.6% | National, with acute problems in rural and remote areas | Medium term (2-4 years) |

| Labour shortages from rural-to-urban migration | -0.4% | National, with concentration in high-growth industrial states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Landholdings and Declining Soil Fertility

Small and marginal farms now cover 85% of holdings, with average size falling below 2 hectares, making mechanization and scale efficiencies difficult without shared-service models. Fertility imbalances persist, with excess nitrogen and insufficient phosphorus-potassium inputs weakening soil structure and raising greenhouse-gas emissions. The Soil Health Card Scheme has expanded sampling, yet state-level adoption of balanced nutrient application remains uneven. Custom Hiring Centers that rent tractors and harvesters mitigate fragmentation constraints, though coverage gaps underline the need for expanded service networks.

Inadequate Cold-Chain and Storage Infrastructure

India loses 40% of fresh produce annually, about 40 million tons worth USD 13 billion because only 4% of perishables move through integrated cold chains. Operating costs for cold stores exceed Western norms due to high energy tariffs, limiting smallholder access. The Government plans to invest USD 15 billion over five years, prioritizing renewable-powered facilities and refrigerated container fleets that could cut losses by up to 35%. Roughly 20,000 refrigerated containers valued at USD 0.53 billion are required to match supply with horticulture output, signaling a sizeable opportunity for logistics providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals and Grains Accelerate, While Fruits and Vegetables Show Growth Potential

Cereals and grains controlled 49.10% of the India agriculture market in 2025. The India agriculture industry size for cereals is projected to advance steadily at the sector’s average CAGR, helped by expanded irrigation and mechanized harvesting. Pulses and oilseeds remain vulnerable to yield fluctuations, prompting a Mission for Aatmanirbharta in Pulses to foster self-sufficiency. Targeted subsidies, climate-resilient varieties, and integrated pest-management programmes are projected to stabilize these sub-segments over the forecast horizon.

Fruits and vegetables form the fastest-growing slice of the India agriculture market, projected to clock a 7.42% CAGR through 2031 as urban diets diversify and export orders climb. Horticulture output rose to 355.2 million tons in 2023-24, including 112.62 million tons of fruit and 204.96 million tons of vegetables. Targeted subsidies, climate-resilient varieties, and integrated pest-management programmes are projected to stabilize these sub-segments over the forecast horizon.

Geography Analysis

Regional disparities shape the India agriculture market, with mechanization, water availability, and market linkages varying sharply across states. Punjab and Haryana post-mechanization rates above 40%, boosting labor productivity and underpinning large grain surpluses for the national buffer stock. In contrast, northeastern states remain largely manual, which constrains the adoption of precision farming and limits the flow of agritech finance. Gujarat leads in total factor productivity thanks to robust extension services, high micro-irrigation coverage, and export-oriented horticulture clusters. Bihar lags despite policy attention, highlighting the complexity of translating subsidies into field-level gains.

Commodity specialization further differentiates state performance. Andhra Pradesh dominates mango and banana output, Maharashtra anchors premium Alphonso mango exports, Gujarat excels in Kesar mangoes, and Karnataka commands pomegranate shipments. Cotton cultivation is concentrated in Gujarat, Maharashtra, and Telangana, together accounting for roughly 65% of the national supply; weather shocks in these states wield disproportionate influence on textile input costs. The Government’s creation of a Makhana Board in Bihar and the commissioning of a new urea plant in Assam illustrate region-specific industrial policy that targets comparative advantages and addresses input shortages.

Climate variability adds another spatial layer: the Indian Meteorological Department projects an above-normal 2025 monsoon with 105% of the long-period average, which should lift kharif sowing in rain-fed belts. Yet unseasonal rainfall damaged rabi crops in Maharashtra, prompting compensation demands of Rs 50,000 per hectare and spotlighting the need for parametric insurance. Digital weather advisories, drought-resistant seed distribution, and decentralized storage hubs are emerging as essential tools to smooth regional volatility and narrow yield gaps within the India agriculture market.

Recent Industry Developments

- June 2025: India cut import duties on crude soybean, sunflower, and palm oil to 10%, lowering the effective rate from 27.5% to 16.5% to curb edible-oil inflation and enhance domestic refinery utilization.

- June 2025: Union Agriculture Minister Shri Shivraj Singh Chouhan proposed field-mounted solar panels under the PM-KUSUM scheme to transform farmers into renewable-energy suppliers.

- May 2025: The Indian Meteorological Department forecast a 59% probability of above-normal southwest monsoon, with onset on May 27 at 105% of the long-period average.

- May 2025: National foodgrain output reached 354 million tons in 2024-25, 6.6% higher than 2023-24, underpinned by MSP revisions and expanded irrigation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Indian agriculture market as the aggregate farm-gate value (constant 2024 US dollars) of all domestically grown crops and livestock, including cereals, pulses, oilseeds, horticulture produce, plantation crops, dairy, poultry, and fisheries. This value reflects quantities harvested in India multiplied by representative farm-gate prices during the base year.

Scope Exclusions: Post-farm processing, agro-input manufacturing, and rural financial services fall outside the present valuation.

Segmentation Overview

- By Commodity Type

- Cereals and Grains

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Pulses and Oilseed

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Fruits and Vegetables

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Cash Crops

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Cereals and Grains

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with agricultural economists, state extension officers, farmer-producer-organization leaders, and commodity buyers across ten producing belts. These conversations clarified average realized farm prices, irrigation uptimes, herd dynamics, and the likely impact of fresh subsidy notifications, enabling us to firm up assumptions flagged during desk work.

Desk Research

We first reviewed publicly accessible, high-credibility bodies such as the Directorate of Economics & Statistics, Ministry of Agriculture & Farmers Welfare, APEDA shipment data, FAOSTAT, Reserve Bank of India price series, and state agriculture dashboards. Company filings, leading newspapers, and court judgments on Minimum Support Price policy supplied contextual depth. Subscription databases that Mordor analysts access, including D&B Hoovers, Dow Jones Factiva, and Volza, helped cross-check corporate revenue lines and export volumes. This mixture of open and paid material anchored early estimates while alerting us to data gaps still requiring field insight. The sources named are illustrative; many additional documents supported data collection, validation, and clarifications.

Market-Sizing & Forecasting

We began with a top-down reconstruction that multiplied official production statistics by weighted farm-gate prices across forty key commodities, then reconciled results with sampled bottom-up supplier roll-ups and channel checks. Variables such as sown area, yield trend lines, livestock population, irrigated acreage share, export realization, and Minimum Support Price revisions feed our model. A multivariate regression linked these drivers to historical value, after which ARIMA smoothing projected each driver through 2030 before scenario testing by domain experts. Where district-level gaps emerged, interpolation used three-year moving averages to keep totals conservative yet representative.

Data Validation & Update Cycle

Outputs face a two-layer check. Analysts benchmark model totals against independent trade totals and national accounts, flagging variances above three percent. Senior reviewers then approve or return the file for recalibration. Our agriculture dashboards refresh yearly, with interim tweaks when policy shocks or extreme weather materially shift supply or price.

Why Mordor's India Agriculture Baseline Commands Confidence

Published estimates often diverge because firms tackle different scopes, price concepts, and refresh tempos.

By isolating pure farm-gate value and updating drivers annually, we keep noise low and comparability high.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 452 B (2025) | Mordor Intelligence | - |

| USD 612 B (2024) | Global Consultancy A | Adds midstream processing and uses nominal GDP deflator, inflating baseline |

| USD 1.20 T (2024) | Industry Association B | Counts retail-price output plus agro-inputs and rural services, overstating value |

The comparison shows that once differing inclusions and price bases are stripped away, Mordor's disciplined model offers a balanced, transparent starting point that executives can retrace and update with limited effort.

Key Questions Answered in the Report

What is the projected value of the India agriculture market by 2031?

The India agriculture market is expected to reach USD 578.89 billion by 2031, growing at a 4.21% CAGR.

Which commodity segment currently dominates the India agriculture market?

Cereals and grains dominate with a 49.10% share in 2025 due to robust public procurement and strong domestic demand.

Why are fruits and vegetables the fastest-growing segment?

Urban dietary shifts, export opportunities, and government support for horticulture are forecast to drive a 7.42% CAGR for fruits and vegetables between 2026 and 2031.

What are the main factors restraining growth in the India agriculture market?

Fragmented landholdings, declining soil fertility, inadequate cold-chain infrastructure, and climate-related weather shocks collectively weigh on long-term growth.

How is the government supporting small farmers’ access to finance?

The Kisan Credit Card limit was raised to Rs 5 lakh in the 2025-26 budget, while digital farmer IDs streamline loan disbursement and subsidy delivery.

Page last updated on: