Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

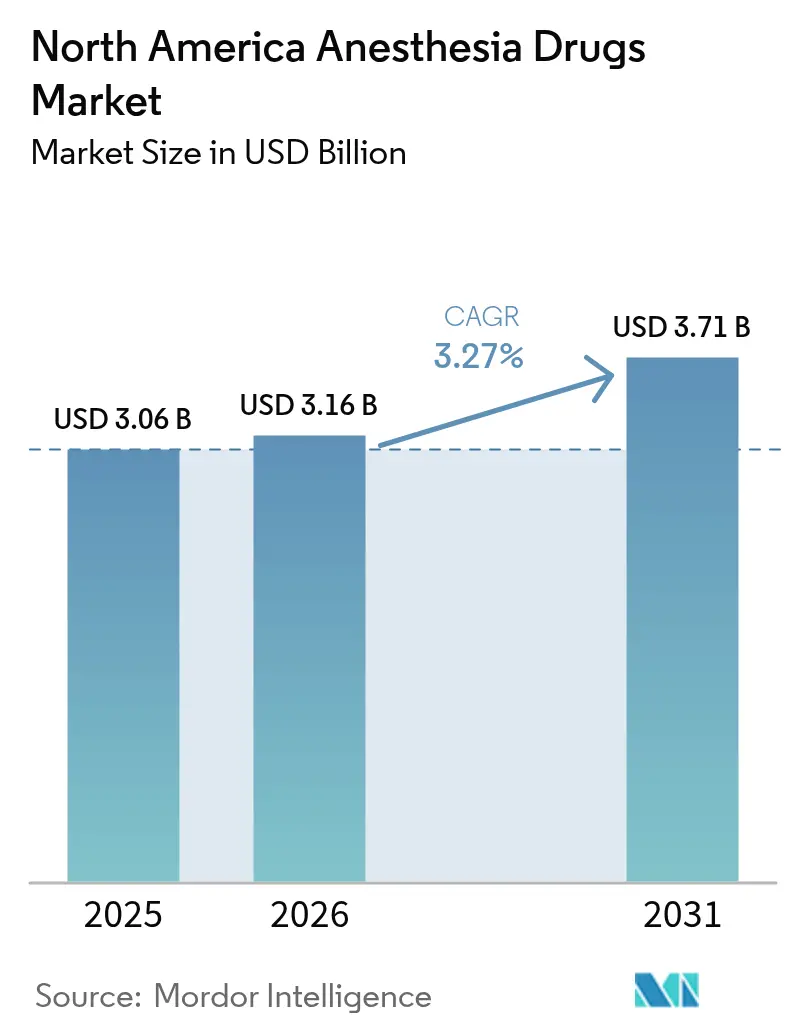

| Base Year Market Size (2025) | USD 3.06 Billion |

| Market Size (2026) | USD 3.16 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Anesthesia Drugs Market Analysis by Mordor Intelligence

North America anesthesia drugs market size in 2026 is estimated at USD 3.16 billion, growing from 2025 value of USD 3.06 billion with 2031 projections showing USD 3.71 billion, growing at 3.27% CAGR over 2026-2031. This moderate pace signals a maturing environment in which technological advances, rather than procedure volume growth, contribute most of the incremental value. Artificial intelligence (AI) now guides closed-loop delivery systems that fine-tune propofol and sevoflurane dosing, cutting drug waste while improving hemodynamic stability. Machine-learning models also outperform manual methods in predicting intraoperative complications, leading to shorter recovery times and lower readmission rates. Ambulatory surgery centers (ASCs) are pivotal: procedures shifting from inpatient suites to outpatient theaters expand demand for ultra-short-acting agents that enable same-day discharge. Meanwhile, next-generation molecules such as ciprofol and remimazolam are positioned to erode propofol’s lead by offering milder cardiovascular effects.

Key Report takeaways

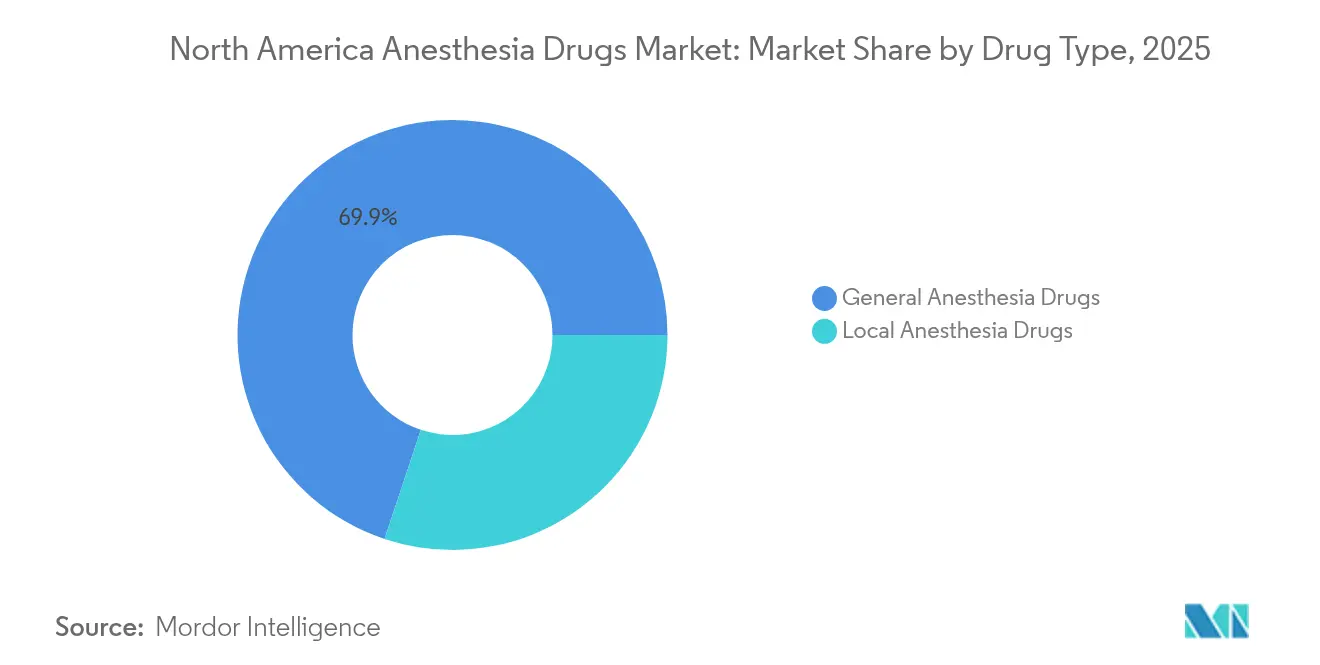

- By drug type, general anesthetics led with 69.88% of the North America anesthesia drugs market share in 2025, while local anesthetics record the fastest 3.80% CAGR through 2031.

- By route of administration, inhalation agents accounted for 62.94% of the North America anesthesia drugs market size in 2025; injectable agents are expected to grow at a 4.10% CAGR to 2031.

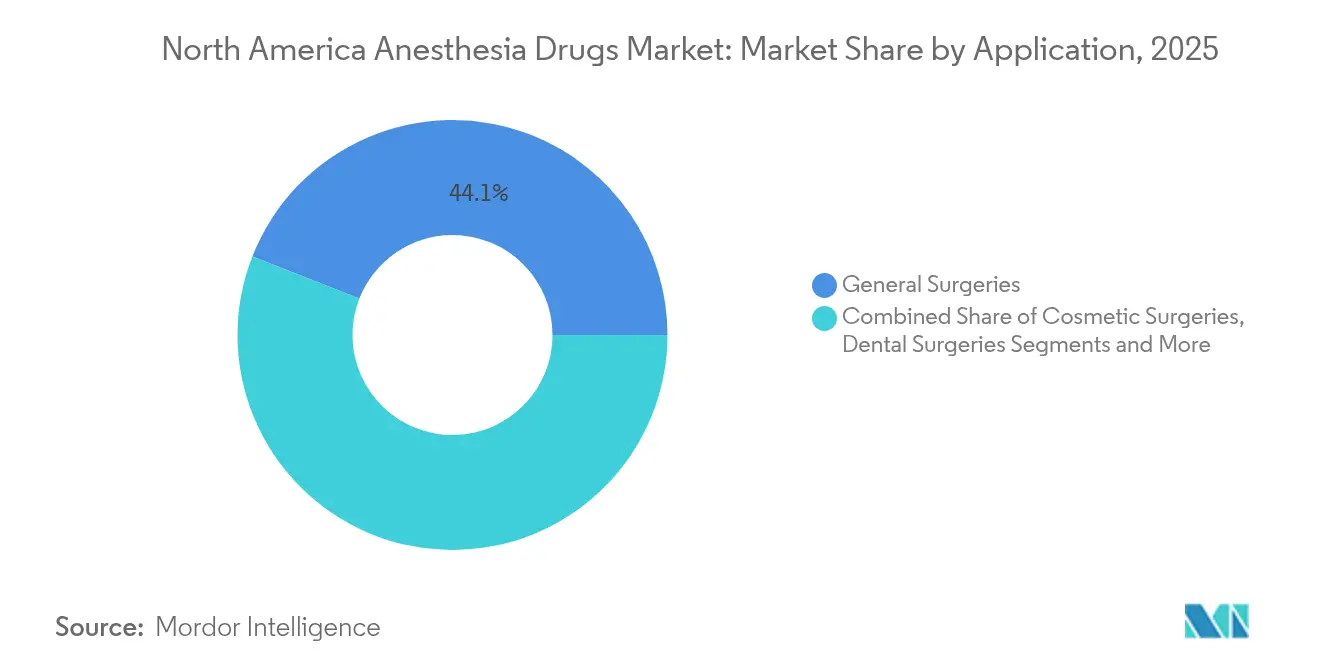

- By application, general surgery captured 44.05% revenue in 2025; cosmetic surgery is set to expand at a 4.22% CAGR to 2031.

- By end user, hospitals held 57.92% of the North America anesthesia drugs market share in 2025, whereas ASCs post the highest 4.55% CAGR to 2031.

- By geography, the United States commanded 87.96% share in 2025; Mexico is forecast to accelerate at a 4.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Anesthesia Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of surgeries | +0.9% | North America, with strongest impact in US and Canada | Medium term (2-4 years) |

| Growing R&D investment by pharmaceutical companies | +0.6% | Global, with concentration in US biotech hubs | Long term (≥ 4 years) |

| Shift toward outpatient/ambulatory surgeries driving demand for ultra-short-acting anesthetics | +0.7% | North America, led by US ASC expansion | Short term (≤ 2 years) |

| Rapid adoption of AI-enabled anesthesia monitoring improving drug utilization efficiency | +0.5% | North America, primarily in academic medical centers | Medium term (2-4 years) |

| AI-enabled anesthesia monitoring | +0.4% | North America, with spillover to advanced healthcare systems globally | Medium term (2-4 years) |

| Commercialization of next-gen agents (e.g., ciprofol/HSK3486) offering improved safety profiles | +0.6% | Global, with initial focus on North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Surgeries

Surgical episodes across the region keep rising, with Medicare reporting 5.7% annual gains in procedures per beneficiary during 2024. ASCs anticipate a 22% lift in procedure counts by 2033, reinforcing demand for fast-acting anesthesia formulations. The 65-plus cohort undergoes more complex operations, which lengthen anesthetic exposure and elevate drug consumption. Cosmetic interventions now generate USD 13 billion yearly, expanding use of tailored agents that limit postoperative nausea in aesthetic clinics [1]Li-Hua Zhou, “Machine Learning for Anesthesia Depth Prediction,” BMC Medical Informatics and Decision Making, bmcmedinformdecismak.biomedcentral.com.

Growing R&D Investment by Pharmaceutical Companies

Pharma sponsors channel record sums into anesthesia pipelines, with AbbVie overseeing roughly 90 active compounds and USD 56.3 billion in 2024 revenue that funds clinical programs. Pfizer lists 64 novel entities among 112 pipeline projects, underscoring broad discovery momentum. The FDA cleared Journavx (suzetrigine) in January 2025, a non-opioid that could reshape perioperative pain protocols and curb opioid co-administration [2]Fred E. Shapiro, “Anesthesia for Outpatient Cosmetic Surgery,” Current Opinion in Anesthesiology, journals.lww.com.

Shift Toward Outpatient/Ambulatory Surgeries Driving Demand for Ultra-Short-Acting Anesthetics

Same-day procedures favor agents such as desflurane and propofol for swift emergence. Enhanced Recovery After Surgery pathways heighten reliance on nerve blocks that reduce opioid exposure. Economic incentives further steer hospitals to adopt outpatient models that intensify competition for drugs with rapid pharmacokinetics.

Rapid Adoption of AI-Enabled Anesthesia Monitoring Improving Drug Utilization Efficiency

Closed-loop systems keep mean arterial pressure 10 mmHg higher than manual protocols, cutting hypotension episodes. The Hypotension Prediction Index posts mean squared error of 0.0062 in depth prediction tasks [3]U.S. Food and Drug Administration, “FDA Approves Journavx (Suzetrigine),” U.S. Food and Drug Administration, fda.gov. Academic hospitals are early adopters and influence community facilities through residency rotations. Drug makers integrating formulations with these platforms gain switching costs that deter generic competition.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse effects and safety concerns | -0.5% | Global, heightened scrutiny in US | Long term (≥ 4 years) |

| Stringent FDA & DEA controls | -0.4% | North America, particularly US | Medium term (2-4 years) |

| Shortages of key APIs | -0.6% | North America import-dependent supply chain | Short term (≤ 2 years) |

| Supply-chain vulnerability | -0.4% | Global, with US concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects & Safety Concerns of General Anesthetics

FDA pharmacovigilance tallied 1,126 sevoflurane adverse events between 2004 and 2022, ranging from atrial fibrillation to malignant hyperthermia. Pediatric surveillance uncovered novel signals such as encephalopathy, prompting clinician caution. Environmental moves like the NHS plan to phase out desflurane pressure hospitals to substitute agents despite familiarity advantages. These factors favor newer molecules that claim narrower cardio-respiratory profiles but may require costly education programs.

Stringent FDA & DEA Regulations on Controlled Substances

DEA quota ceilings on fentanyl analogues and Schedule II anesthetics constrain output flexibility during demand spikes. In 2024, the FDA pulled 65 abbreviated drug applications, including several injectable anesthetics, highlighting compliance hurdles for smaller generics. Delays such as PharmaTher’s ketamine dossier, now pushed to June 2025, illustrate how regulatory reviews extend shortages for critical agents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: General Agents Hold Volume, Locals Lead Growth

General anesthetics accounted for 69.88% of the North America anesthesia drugs market share in 2025. Propofol’s rapid onset underpins this lead, yet ciprofol is gaining clinician interest because it mitigates injection pain and cardiovascular swings. Sevoflurane remains the dominant inhaled choice for pediatric cases even as desflurane usage fades under green-house gas scrutiny. Dexmedetomidine enjoys expanding roles in awake procedures and intensive care where respiratory stability is vital. Remifentanil provides ultra-short opioid support for brief ambulatory cases, whereas midazolam remains a versatile anxiolytic adjunct.

Local anesthetics advance at a 3.80% CAGR, the fastest among all segments, and they benefit from regional blocks that reduce opioid reliance. Bupivacaine leads for its prolonged analgesia in orthopedic and obstetric settings. Ropivacaine’s lower cardiotoxic risk makes it the spinal agent of choice for high-risk populations. Lidocaine, still indispensable for infiltration, now sees extended uses in intravenous regional anesthesia. Ultrasound-guided techniques broaden indications for locals, raising total consumption. The North America anesthesia drugs market size for local agents is projected to swell at a volume pace that outstrips the overall sector during 2026-2031.

By Route of Administration: Injection Growth Challenges Inhalation Leadership

Inhalation drugs held 62.94% of the North America anesthesia drugs market in 2025 due to operating room infrastructure geared toward volatile agents. Sevoflurane’s predictable kinetics underpin its primacy. Supplier concentration is rising after Baxter invested in Puerto Rico fill-finish lines that secure regional stocks. Environmental policies, however, accelerate substitution into total intravenous anesthesia.

Injectables are recording a 4.10% CAGR as ASCs and ERAS pathways reward precise titration. Propofol remains the anchor but fresh FDA clearance for ciprofol and remimazolam will diversify options. The North America anesthesia drugs market size for injectable agents is expected to reach USD 1.93 billion by 2031, reflecting clinician preference for rapid turnover. Ready-to-use vials reduce medication errors and contamination, sustaining demand. Although topical and transdermal routes stay niche, innovation in liposomal lidocaine foams and dermal patches could open incremental revenue.

By Application: General Surgery Dominates, Cosmetic Leads Momentum

General surgery retained 44.05% share of the North America anesthesia drugs market in 2025 with steady inpatient case loads and complex laparoscopic procedures. Medicare’s 5.7% annual growth in surgeries indicates robust baseline volume. ERAS adoption within this segment promotes multimodal analgesia that enlarges total drug cocktails per case. Balanced anesthesia, which blends inhaled and intravenous agents, secures broad demand across drug classes.

Cosmetic surgery cases grow at a 4.22% CAGR, reflecting consumer acceptance and financing options. The 457% rise in aesthetic procedures since 1997 shows enduring upside. Short recovery windows require ultra-short anesthetics to avoid overnight admission, lifting use of desflurane, remifentanil, and regional nerve blocks. Dental and pain-management interventions also scale steadily, adding to segment diversification.

By End User: Hospitals Anchor Demand While ASCs Accelerate

Hospitals captured 57.92% of the North America anesthesia drugs market share in 2025 owing to their capacity for complex surgeries and critical care. Academic centers spearhead AI pilots that fine-tune anesthetic infusion rates, yielding cost savings and quality scores. Bulk purchasing allows hospitals to negotiate favorable pricing, though shortages push some systems toward in-house compounding.

ASCs expand at 4.55% CAGR, benefitting from payer reimbursement that favors outpatient care. Medicare spent USD 6.8 billion on ASC bills in 2023, underlining scale. ASCs prefer single-dose vials and ultra-short agents that support 23-hour observation rules. Office-based surgery centers and specialty clinics round out demand but face regulatory variation across states.

Geography Analysis

The United States commanded 87.96% of the North America anesthesia drugs market in 2025 as its surgical intensity, reimbursement levels, and early technology adoption reinforce premium drug use. Workforce shortages rose to 78% by late-2022, encouraging AI systems that reduce provider workload. Chronic shortages, some exceeding three years, led Washington to allocate USD 34 billion for domestic pharma resilience, while Amneal secured FDA approval for in-house propofol that should stabilize key supply.

Canada holds lower coverage at 29.4% of US anesthesia capacity, which constrains operating room throughput. Its physician-only anesthesia delivery model magnifies staffing gaps. Eleven provincial reimbursement systems fragment procurement, resulting in higher per-unit drug costs. The Canadian device market reached USD 6.8 billion in 2024 and grows 5.4% yearly, opening opportunities for bundled drug-device solutions.

Mexico is the fastest-growing sub-region with a 4.74% CAGR through 2031. Infrastructure upgrades and medical tourism raise demand for international-grade anesthesia standards. Mexico also positions itself as an alternate API source for propofol and sevoflurane, aligning with the North American Preparedness Initiative to diversify supply chains. Adoption of regional blocks and AI monitors is nascent but climbing in tertiary centers.

Competitive Landscape

The North America anesthesia drugs market features mid-level concentration with competition fueled by supply assurance and digital integration more than simple price rivalry. Fresenius Kabi grew revenue 11% year-on-year in Q3 2024 after vertical integration bolstered API availability. Baxter raised injectable launches to ten in 2024, focusing on ready-made formats that cut pharmacy prep times. Patent cliffs for drugs like Nucynta ER in 2029 invite generic challengers that fragment opioid segments.

Strategic thrust now centers on technology linkages. Companies partner with AI software vendors to embed dose algorithms directly into infusion pumps, locking prescribers into proprietary ecosystems. Environmental stewardship emerges as a differentiator: suppliers developing capture kits for volatile waste gases could gain tender preference in Canada and selected US states. Acquisition activity remains brisk. AbbVie’s late-2024 buys of ImmunoGen and Cerevel add neuro-modulatory assets that complement sedation portfolios.

Disruptors include manufacturers of ciprofol and remimazolam, which aim to displace propofol in high-risk cohorts. Hikma’s West-Ward subsidiary scales injectable anesthetics, filling gaps left by defunct suppliers. Sagent concentrates on syringe fills for regional blocks, while Hospira leverages Pfizer distribution muscle to reclaim hospital share. The North America anesthesia drugs industry thus pivots toward integrated solutions that pair molecules with predictive analytics and eco-friendly handling.

North America Anesthesia Drugs Industry Leaders

Baxter International

Fresenius SE & Co. KGaA

AbbVie Inc.

Eisai Co. Ltd

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vertex Pharmaceuticals received FDA clearance for Journavx (suzetrigine) 50 mg tablets, introducing a non-opioid pain option for perioperative settings.

- December 2024: Fresenius Kabi introduced the first US generic epinephrine 1 mg/1 mL vial, expanding emergency and anesthesia drug supply.

- December 2024: Baxter International launched five injectable products, pushing its 2024 anesthesia-critical care releases to ten.

- August 2024: Amneal Pharmaceuticals gained FDA approval for single-dose propofol emulsion vials targeting a USD 314 million annual market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America anesthetic drugs market as the yearly value of prescription general and local anesthetic agents, injectable, inhalation, topical, and transdermal, cleared for human surgical or procedural use across the United States, Canada, and Mexico. Drugs solely used for veterinary purposes or for conscious-sedation dentistry are outside the scope.

Scope exclusion: Adjunct analgesics, neuromuscular blockers, and anesthesia machines are not counted.

Segmentation Overview

- By Drug Type

- General Anesthesia Drugs

- Propofol

- Sevoflurane

- Desflurane

- Dexmedetomidine

- Remifentanil

- Midazolam

- Other General Anesthesia Drugs

- Local Anesthesia Drugs

- Bupivacaine

- Ropivacaine

- Lidocaine

- Chloroprocaine

- Prilocaine

- Benzocaine

- Other Local Anesthesia Drugs

- General Anesthesia Drugs

- By Route of Administration

- Inhalation

- Injection (IV/IM)

- Other Routes (Topical, Transdermal, etc.)

- By Application

- General Surgeries

- Cosmetic Surgeries

- Dental Surgeries

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital pharmacy managers, ASC administrators, anesthesiologists, and procurement heads across all three countries. Discussions clarified real-world dose mix shifts, average case counts, and the pace at which novel agents like ciprofol or remimazolam enter formularies, which let us validate desk assumptions and adjust uptake curves.

Desk Research

We built the baseline with open datasets from sources such as the US FDA Orange Book, Health Canada's Drug Product Database, and Mexico's COFEPRIS listings, which map marketed molecules and dosage forms. Volume indicators came from the American Hospital Association annual surgery statistics, OECD Health-Care Utilization tables, and UN Comtrade import codes that track bulk anesthetic APIs. Company 10-Ks and hospital group purchasing documents informed average selling prices, while D&B Hoovers and Dow Jones Factiva supplied historical revenue splits for leading suppliers. This list is illustrative, and many additional public and proprietary references informed the desk phase.

Market-Sizing & Forecasting

We apply a top-down and bottom-up blend. National surgery volumes are multiplied by drug-specific penetration and mean dose per case, then cross-checked with supplier shipments and sampled ASP × unit trackers to close gaps. Key variables include inpatient versus outpatient surgery ratios, aging population growth, novel agent launch timelines, guideline changes favoring opioid-sparing protocols, and average wholesale price inflation. Forecasts use multivariate regression that ties unit demand to procedure growth, demographic shifts, and payor reimbursement trends, with scenario analysis layering regulatory or supply shock sensitivities. Where bottom-up estimates lag import data or audited financials, variance factors are transparently disclosed before roll-up.

Data Validation & Update Cycle

Outputs pass a two-step peer review within Mordor, followed by anomaly checks against quarterly trade data and price trackers. Models refresh annually, with interim updates when recalls, major approvals, or currency swings alter the outlook, so clients always receive the latest vetted view.

Why Mordor's North America Anesthesia Drugs Baseline Commands Reliability

Published values often differ because firms choose narrower drug lists, project only the United States, or assume uniform ASPs.

Key gap drivers include competitor focus on general agents alone, exclusion of Mexico, reliance on retail pricing, and less frequent refresh cadences that miss recent outpatient migration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.06 B (2025) | Mordor Intelligence | - |

| USD 2.10 B (2024) | Regional Consultancy A | Counts general agents only and omits topical/local drugs |

| USD 1.89 B (2024) | Trade Journal B | Excludes Mexico and bases totals on sampled hospital sales |

| USD 2.40 B (2025) | Industry Association C | Covers United States only and applies retail instead of ex-factory prices |

The comparison shows that once scope, geography, and pricing bases align, Mordor's balanced mix of procedure-linked demand modeling and continual primary validation delivers the most traceable and decision-ready baseline for stakeholders.

Key Questions Answered in the Report

How big is the North America Anesthesia Drugs Market?

The North America Anesthesia Drugs Market size is expected to reach USD 3.16 billion in 2026 and grow at a CAGR of 3.27% to reach USD 3.71 billion by 2031.

What is the current North America Anesthesia Drugs Market size?

In 2026, the North America Anesthesia Drugs Market size is expected to reach USD 3.16 billion.

Who are the key players in North America Anesthesia Drugs Market?

Baxter International, Fresenius SE & Co. KGaA, AbbVie Inc., Eisai Co. Ltd and B. Braun SE are the major companies operating in the North America Anesthesia Drugs Market.

Why are ambulatory surgery centers important for future growth?

ASCs post the highest 4.55% CAGR because outpatient procedures demand ultra-short-acting agents that support same-day discharge.

Page last updated on: