Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

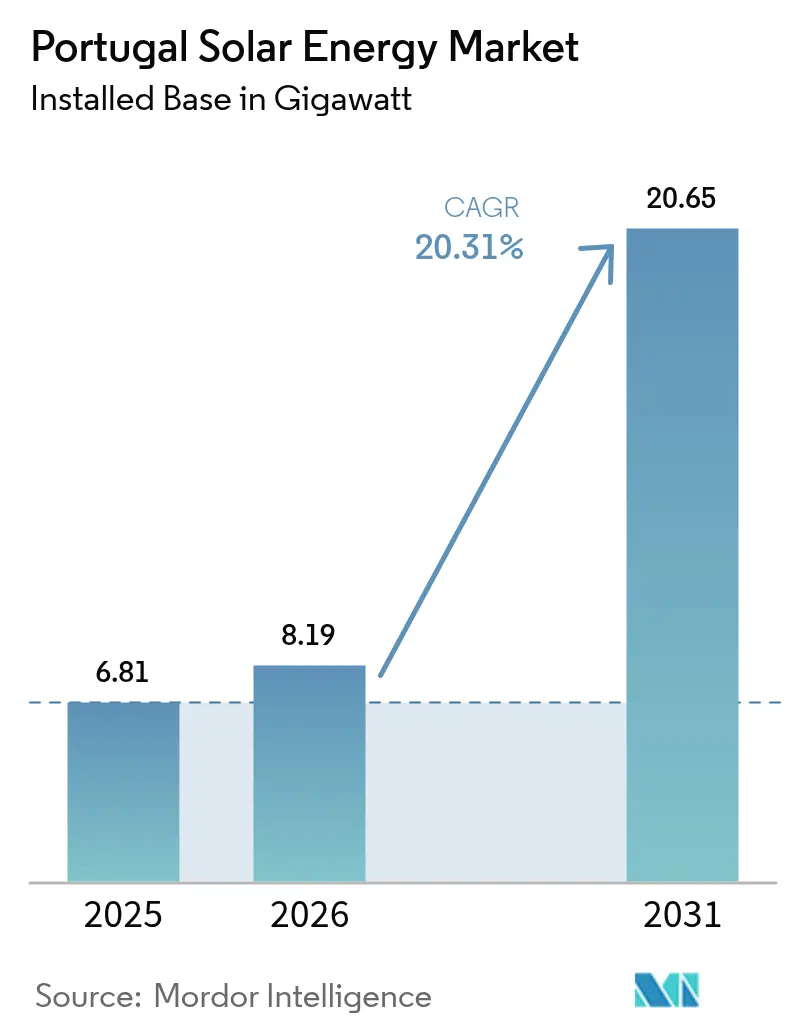

| Base Year Market Size (2025) | 6.81 gigawatt |

| Market Volume (2026) | 8.19 gigawatt |

| Market Volume (2031) | 20.65 gigawatt |

| Growth Rate (2026 - 2031) | 20.31% CAGR |

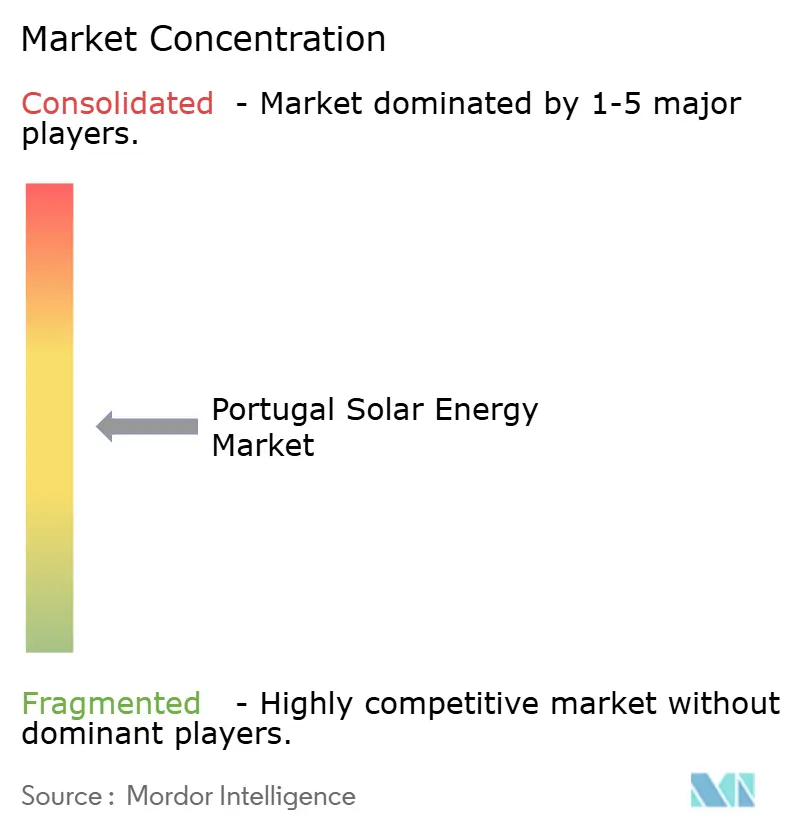

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Solar Energy Market Analysis by Mordor Intelligence

The Portugal Solar Energy Market size was valued at 6.81 gigawatt in 2025 and estimated to grow from 8.19 gigawatt in 2026 to reach 20.65 gigawatt by 2031, at a CAGR of 20.31% during the forecast period (2026-2031).

Recent gains stem from the 1.77 GW added in 2024, the auction-linked pipeline that aligns with the 2030 National Energy and Climate Plan, and the release of 1.2 GW of grid headroom following the retirement of the Sines coal plant. Module prices under USD 0.12 per W, streamlined licensing under Decree-Law 99/2024, and a surge in self-consumption systems have drawn both infrastructure funds and corporate offtakers into the Portugal solar energy market. Competitive activity sharpened after Brookfield and EQT completed acquisitions worth a combined USD 3.91 billion, concentrating utility-scale pipelines among the top five developers. Meanwhile, policy signals, such as the July 2025 VAT reversion for rooftops, introduce near-term uncertainty, yet upside persists in floating solar, agrivoltaics, and storage-hybrid projects that ease curtailment risk in the congested Alentejo grid.

Key Report Takeaways

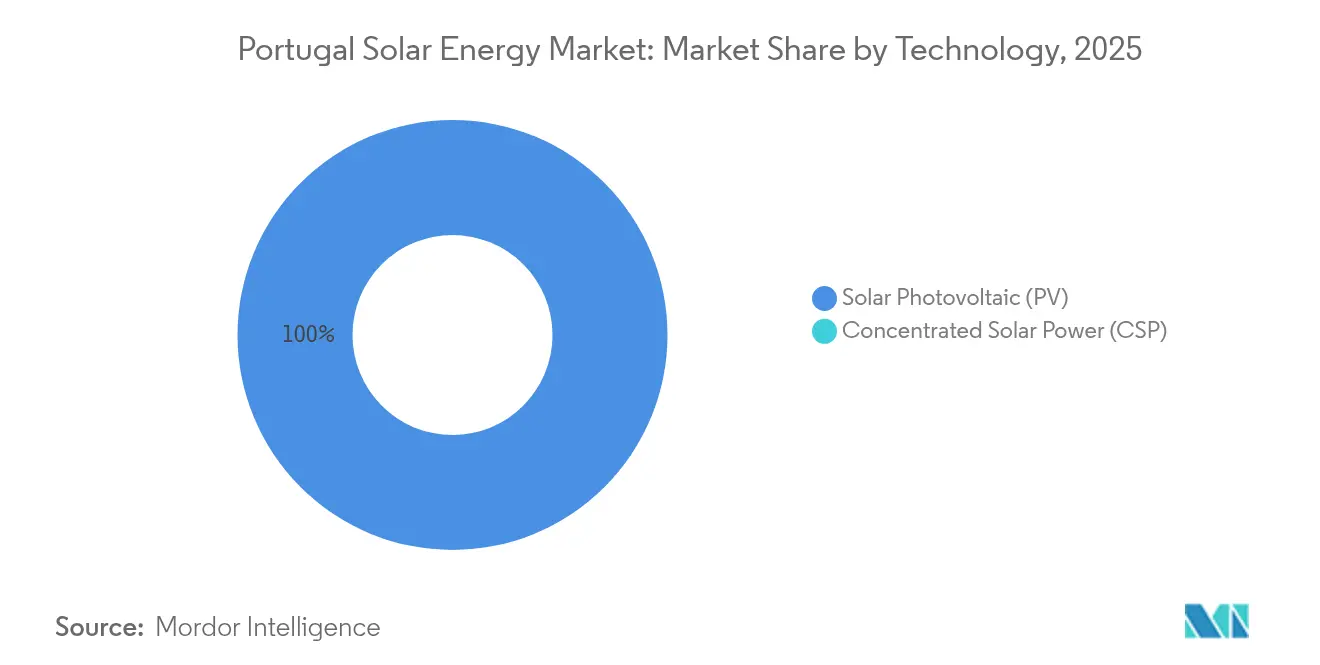

- By technology, solar PV secured 100.00% of the Portugal solar energy market share in 2025, while concentrated solar power remained absent.

- By grid type, on-grid installations accounted for 95.90% of the Portuguese solar energy market size in 2025; the off-grid niche is projected to expand at a 23.20% CAGR through 2031.

- By end-user, utility-scale assets controlled an 84.50% share of the Portugal solar energy market in 2025, whereas residential capacity is advancing at a 24.30% CAGR to 2031 thanks to the UPAC framework.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Portugal Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government auctions & 2030 NECP solar target | +6.2% | National (Alentejo, Ribatejo) | Long term (≥ 4 years) |

| Falling module prices & lower LCOE | +4.8% | National; Azores, Madeira | Medium term (2-4 years) |

| Corporate PPA momentum | +3.5% | Lisbon, Porto, nationwide | Medium term (2-4 years) |

| Freed Sines grid capacity post-coal exit | +2.9% | Alentejo, Setúbal | Short term (≤ 2 years) |

| UPAC self-consumption boom | +2.7% | Urban and industrial hubs | Medium term (2-4 years) |

| Floating-solar & agrivoltaics rollout | +1.1% | Alqueva, Cabril, pilot sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Auctions & 2030 NECP Solar Target

The 20.8 GW 2030 target requires average annual additions of 2.5 GW, which is well above 2024’s record. Auctions between 2020 and 2023 cleared 2.2 GW at some of Europe’s lowest bids, reinforcing long-term cost leadership. Yet the 2024 auction deferral revealed grid-connection bottlenecks, prompting developers to pivot toward bilateral PPAs that trade auction certainty for counterparty risk. Substation upgrades in the Alentejo lag commissioning by up to 18 months, underlining the mismatch between policy ambition and infrastructure readiness. The Portugal solar energy market, therefore, hinges on timely grid reinforcement to keep its growth curve intact.

Falling Module Prices & Lower LCOE

Polysilicon oversupply pushed module prices to USD 0.10–0.12 per W in 2024, compressing LCOEs to EUR 20–30 per MWh in high-irradiance zones and rendering solar cheaper than onshore wind for the first time in Portugal.(1)International Energy Agency, “World Energy Outlook 2024,” iea.org Developers now specify bifacial modules and single-axis trackers that lift yields by up to 20%, yet ultra-thin manufacturer margins could reverse price declines if trade actions or capacity closures emerge. Projects locked through 2025 are insulated, but 2026 deliveries may face renewed cost pressure, underscoring procurement-timing risk for the Portugal solar energy market.

Corporate PPA Momentum

More than 800 MW of offtake closed through ten deals in 2024, with contract prices between EUR 40–50 per MWh, roughly half the 2024 wholesale average. Offtakers range from ceramics to public-sector aggregations, diversifying credit exposure. The landmark 166 MW public-sector PPA with eSPap offers proof of concept for pooled demand structures, although replicating them in the private sphere remains complex. This PPA wave anchors revenue for merchant projects and buffers the Portugal solar energy market against auction delays.

UPAC Self-Consumption Boom

Net-metering privileges drove UPAC installations to 192,000 by the end of 2024, given retail tariffs of EUR 0.18 per kWh and the exemption from grid-access queues. The July 2025 VAT shift from 6% to 23% will increase the cost of a 5 kW rooftop system by EUR 600 and extend its payback period beyond seven years, likely reducing residential demand. Commercial rooftops sidestep the VAT hit but face structural constraints, as only 35% of industrial roofs in Lisbon and Porto meet PV suitability criteria. Nonetheless, self-consumption remains a crucial safety valve that keeps the Portugal solar energy market diversified.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & slow permitting | -3.4% | Alentejo, Algarve, Beiras | Medium term (2-4 years) |

| High interest-rate financing environment | -2.1% | Nationwide, merchant projects | Short term (≤ 2 years) |

| VAT on residential PV returning to 23% | -1.6% | Urban residential zones | Short term (≤ 2 years) |

| Local land-use & heritage opposition | -0.9% | Lisbon periphery, Algarve, rural sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Slow Permitting

Connection queues in the Alentejo region have stretched beyond 18 months, and REN’s EUR 1.5–1.7 billion investment plan will not fully alleviate backlogs until 2027. Administrative reforms reduce paperwork, yet physical bottlenecks persist, forcing developers to accept curtailment risk or invest in substation upgrades. Environmental reviews can add six to nine months near protected areas, and the Portugal solar energy market could face a mid-decade plateau if reinforcement is delayed.

High Interest-Rate Financing Environment

ECB rate cuts have begun, but debt costs for Portuguese solar remain at 4–6%, double the 2021 levels, trimming merchant IRRs by 200–300 bps.(2)European Central Bank, “Monetary Policy Decisions 2024,” ecb.europa.eu Banks now require 1.4x DSCR, squeezing smaller sponsors that lack balance-sheet strength. Unless rates ease further, financing headwinds will continue to shadow the Portuguese solar energy market through mid-2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Leaves CSP Unviable

Solar PV captured 100.00% of the installed capacity in 2025 and is set to retain that position, growing at a 20.31% CAGR within the Portuguese solar energy market. Converging module and polysilicon costs have widened PV’s edge over CSP, whose direct-normal irradiance requirements exceed Portugal’s diffuse profile. Bifacial modules already account for 60% of shipments and, when paired with single-axis trackers, deliver 15–20% yield boosts that offset the mild curtailment risk in the saturated Alentejo grid. TOPCon and heterojunction cells are pushing conversion efficiencies past 24%, and when paired with central inverters that offer ancillary-service functions, they underpin the next efficiency wave. Storage hybrids, such as EDP’s 17 MW battery at Alqueva, illustrate emerging value-stacking paths that mitigate grid-constraint risk and anchor long-term competitiveness for the Portugal solar energy industry.

PV’s absolute grip shapes procurement dynamics: developers aim to keep all-in capital costs below EUR 500,000 per MW and lock module supply at negative-margin pricing before potential trade actions reset costs. CSP remains sidelined, and no pilot projects are slated through 2030, indicating that the Portuguese solar energy market will likely remain PV-exclusive absent a significant step-change in CSP economics.

By Grid Type: Off-Grid Niche Expands

On-grid systems held 95.90% of the Portuguese solar energy market in 2025, leveraging generous net metering and grid banking. Off-grid capacity, though small, is tracking a 23.20% CAGR as island territories and remote farms adopt solar-plus-battery microgrids when grid extension costs exceed USD 50,000 per km. Decree-Law 15/2022 simplified licensing for sub-100 kW systems, catalyzing uptake among vineyards and olive groves that use solar to power irrigation pumps. Hybrid diesel-PV solutions in the Azores displace up to 70% of imported fuel, validating the off-grid economics, where avoided diesel costs amount to USD 0.22 per kWh.

Grid-tied self-consumers bank surplus generation for 12 months, effectively using the grid as free storage, but ERSE’s 2025 tariff review may introduce capacity charges that shave 10–15% off savings. Off-grid adopters face higher battery CAPEX yet avoid policy risk. As a result, the Portuguese solar energy market is likely to see incremental off-grid diversification that cushions policy swings in net metering.

By End-User: Residential Surge Reshapes Demand

Utility-scale assets controlled 84.50% of the installed capacity in 2025; however, the residential segment is expanding at a 24.30% CAGR and is set to add a disproportionate share of incremental megawatts to the Portuguese solar energy market by 2031. Homeowners monetize retail tariffs nearly twice as much as wholesale prices, and the ability to sidestep grid queues sharpens the value proposition. Rooftop suitability studies show that Lisbon and Porto are leading the adoption, aided by municipal subsidies that cover roughly 30% of the upfront cost. The looming VAT hike will stretch payback timelines past seven years, tempering some demand but leaving commercial roofs and C&I ground-mounts largely unscathed.

Corporate and industrial systems benefit from daytime load alignment and PPA structures that mitigate project revenue risk. By 2024, C&I installs rose 26.6% with typical self-consumption ratios of 70–90%, and Vidrala’s and Sakthi’s PPAs illustrate how industrial offtake underwrites growth. Utility-scale builds remain the capacity anchor, with 1.2 GW commissioned in 2024; yet, distributed generation is capturing a growing share of investment, solidifying a dual-engine model that underpins the Portuguese solar energy market.

Geography Analysis

The Alentejo region hosts 54.20% of utility-scale additions due to its high irradiance, near 1,800 kWh/m², and low land costs, ranging from EUR 5,000 to EUR 10,000 per hectare. However, the Ferreira do Alentejo substation reached 95% utilization in 2024, compelling developers to fund upgrades costing up to EUR 10 million each. The Algarve added 280 MW but faces land-use conflicts with tourism and protected zones that cover 40% of its area. Lisbon and Porto dominate self-consumption, together hosting 120,000 UPAC systems. Municipal rebates seeded momentum in 2024 and are expected to continue into 2025.

Beiras is emerging as a growth frontier, driven by floating solar, notably Voltalia’s 47.77 MW Cabril project, which sidesteps agricultural displacement. In the Azores and Madeira, hybrid diesel-solar arrays reduce annual fuel imports worth EUR 150 million, justifying higher storage costs. Northern regions with lower irradiance attract agrivoltaic pilots that merge grazing and generation, creating dual revenue streams for farmers while contributing incremental megawatts to the Portuguese solar energy market.

Competitive Landscape

The top five developers, EDP Renováveis, Iberdrola, Voltalia, Greenvolt, and Acciona, control 62% of utility-scale pipelines, placing the Portugal solar energy market in a moderately concentrated tier. Residential and C&I installs remain fractured across more than 300 regionally focused EPCs. Large players pursue vertical integration: EDP earmarked EUR 2.5 billion for distributed projects, while mid-tier firms, such as R.Power, differentiate themselves via PPA structuring. The 2024 buyouts of Greenvolt and Sonnedix demonstrate the appetite of infrastructure funds for contracted assets, driving EBITDA multiples to 12–14x and nudging smaller developers toward build-and-flip strategies.

Technology serves as a battlefield. Developers specify bifacial modules paired with trackers to shave EUR 2–3 per MWh off LCOE. Inverter vendors fight for grid-support features that unlock ancillary-service revenues of up to EUR 10,000 per MW annually. Module oversupply pressures margins, but suppliers offering 25–30-year warranties and 90% output guarantees win residential share. ERSE’s ISO 9001 installer rules raise market-entry thresholds, sparking consolidation among rooftop installers and professionalizing after-sales support within the Portugal solar energy market.(4)Financial Times, “Brookfield Buys Greenvolt for EUR 2.1 Billion,” ft.com

Portugal Solar Energy Industry Leaders

SGS SA

Voltalia SA

Acciona SA

Gesto Energia SA

Iberdrola SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EDP Renováveis committed EUR 400 million to build 600 MW of capacity across Alentejo and Ribatejo, including 17 MW of storage.

- February 2025: Sonnedix has acquired two renewable energy projects in Portugal, increasing its total capacity in the country to nearly 500 MW. Upon completion, the two ready-to-build solar and battery energy storage projects are expected to generate approximately 120,000 MWh of clean electricity annually. This output is sufficient to power nearly 40,000 households and reduce over 42,000 metric tonnes of CO2 emissions per year.

- November 2024: Iberdrola inked a 10-year 25 GWh PPA with a Portuguese ceramics maker from its 37 MW Montechoro array.

- October 2024: ACCIONA Energía signed a EUR 800 million 166 MW PPA with public-sector agency eSPap, Portugal’s largest public renewable contract.

Portugal Solar Energy Market Report Scope

Solar energy is the heat and radiant light from the Sun that can be harnessed through technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications like water heating).

The Portugal Solar Energy Market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar Photovoltaic, concentrated solar power. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial, Industrial, and residential. The report also covers the market size and forecasts for Portugal.

For each segment, market sizing and forecasts have been conducted based on installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the Portugal solar energy market in 2026?

Installed capacity stood at 8.19 GW in 2026 and is on track to reach 20.65 GW by 2031.

What is the forecast CAGR for Portuguese solar between 2026 and 2031?

Capacity is projected to expand at a 20.31% CAGR during the 2026–2031 period.

Which technology dominates new Portuguese solar projects?

Photovoltaic systems hold 100.00% share, with bifacial modules and single-axis trackers becoming standard in utility-scale builds.

Why are corporate PPAs important in Portugal?

They provide revenue certainty for developers and lock in electricity costs below wholesale rates for offtakers, supporting more than 800 MW of deals in 2024.

What risks could slow down future solar growth?

Grid congestion, elevated financing costs, and the July 2025 VAT increase on residential systems are the primary headwinds.

Where are the best opportunities outside ground-mounted projects?

Floating solar on reservoirs and agrivoltaic installations that combine farming and generation are emerging high-growth niches.

Page last updated on: