Portable Fuel Cell Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

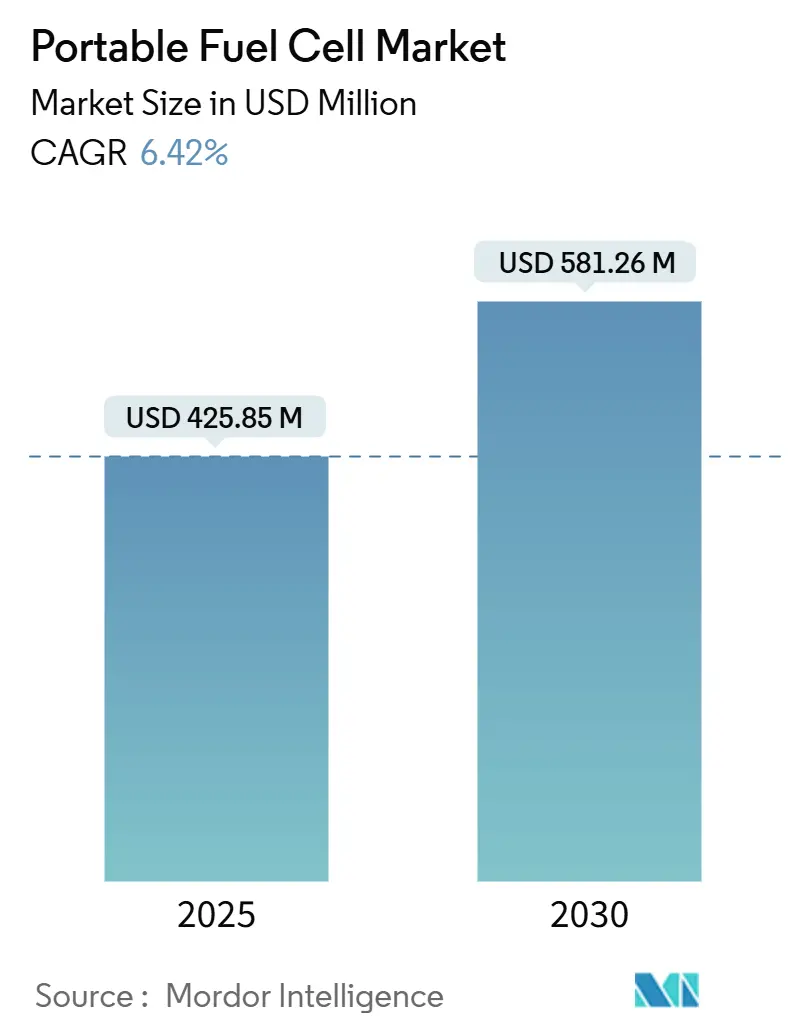

| Market Size (2025) | USD 425.85 Million |

| Market Size (2030) | USD 581.26 Million |

| Growth Rate (2025 - 2030) | 6.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Fuel Cell Market Analysis by Mordor Intelligence

The Portable Fuel Cell Market size is estimated at USD 425.85 million in 2025, and is expected to reach USD 581.26 million by 2030, at a CAGR of 6.42% during the forecast period (2025-2030).

Rising defense modernization budgets, edge-computing backup needs, and breakthrough catalysts that extend system lifespans beyond 200,000 hours are the primary forces driving the acceleration. Military nanogrid rollouts, hydrogen-powered data center pilots, and standardized hydrogen cartridges are expanding commercial opportunities in locations where grid reliability remains uncertain. Competitive intensity is intensifying as scale production lowers price points, while novel materials temper platinum loading requirements, thereby narrowing the total cost gap with lithium-ion batteries. Parallel progress in off-grid hydrogen generation and liquid-organic hydrogen carriers is further improving fuel logistics, especially for remote deployments.

Key Report Takeaways

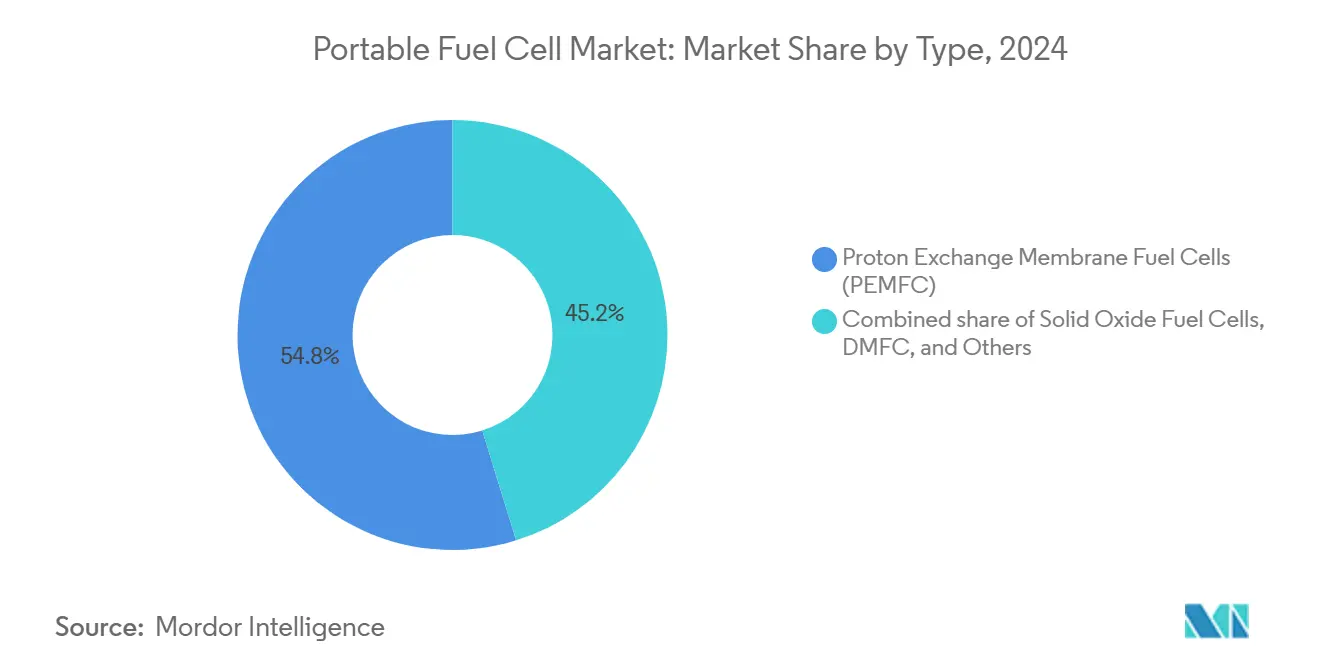

- By technology, proton exchange membrane fuel cells (PEMFC) held 54.8% of the portable fuel cell market share in 2024, while solid oxide fuel cells (SOFC) is projected to advance at a 6.8% CAGR through 2030.

- By power rating, sub-100 W systems accounted for 49.5% share of the portable fuel cell market size in 2024; the 100 W–1 kW band is forecast to grow at 7.4% between 2025 and 2030.

- By fuel type, hydrogen captured 59.1% of the portable fuel cell market share in 2024 and is projected to grow at a 7.0% CAGR through 2030.

- By application, consumer electronics held a 34.7% revenue share in 2024, whereas the military and defense sector is poised to expand at a 7.3% CAGR by 2030.

- By geography, North America commanded a 38.3% share of the portable fuel cell market size in 2024, while the Asia-Pacific region is projected to accelerate at an 8.3% CAGR through 2030.

Global Portable Fuel Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for off-grid & backup power | +1.8% | Global, concentrated in North America & APAC | Medium term (2–4 years) |

| Military & defense field deployments | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Emission-driven regulatory mandates | +0.9% | EU & North America, cascading to APAC | Long term (≥ 4 years) |

| Mini data centers & edge-computing backup | +0.7% | North America & EU urban centers | Short term (≤ 2 years) |

| Standardized hydrogen cartridge ecosystems | +0.5% | Global, early adoption in developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Demand for Off-Grid & Backup Power

AI-centric data centers are projected to double electricity demand by 2030, underscoring the importance of on-site generation solutions that can sustain over 90% capacity factors and respond quickly to fluctuating GPU loads.(1)Data Center Frontier, “ECL Debuts 1 GW Off-Grid Hydrogen-Powered ‘AI Factory’ Data Center,” datacenterfrontier.com The first 1 GW off-grid hydrogen data center near Houston shows a PUE of 1.05 and zero water draw, demonstrating technical viability for large-scale deployments. Military pilots, such as those utilizing the hydrogen nanogrid at White Sands, demonstrate the feasibility of diesel-generator substitution in isolated locations by integrating electrolyzers, storage, and water harvesting into a single microgrid.(2)U.S. Army, “Engineer Research and Development Center Celebrates U.S. Army's First Hydrogen-Powered Nanogrid,” army.mil

Military & Defence Field Deployments

NATO identifies portable fuel cells as silent, thermal-signature-low power sources for forward units requiring energy resilience. The U.S. Air Force is trialing hydrogen systems for agile logistics to curtail supply-chain risk in contested zones. Honeywell’s prototype aligns with U.S. Army electronic device specifications, underscoring readiness for tactical rollout.

Emission-Driven Regulatory Mandates

NHTSA’s FMVSS No. 307 and 308, effective July 2025, codify hydrogen vehicle safety and indirectly normalize components for portable systems. The FAA’s hydrogen aircraft certification roadmap identifies fuel cells as potential candidates for auxiliary power by 2032. ISO 6583:2024 guides methanol purity, easing the adoption of DMFCs in marine and portable applications.(3)International Organization for Standardization, “ISO 6583:2024,” iso.org

Mini-Data-Centres & Edge-Computing Backup

Projected 47 GW of new U.S. data center capacity by 2030 is catalyzing demand for emission-free backup power in cities with strict diesel limits. Bloom Energy’s Illinois project and Hitachi Energy’s HyFlex generator highlight a shift toward modular hydrogen systems compatible with AI workloads. Automotive OEMs such as Honda leverage tech-sector volumes to lower stack costs for future hydrogen vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership | -1.4% | Global, strongest in price-sensitive markets | Medium term (2–4 years) |

| Competition from advanced Li-ion power banks | -1.1% | Consumer electronics globally | Short term (≤ 2 years) |

| Hydrogen-cartridge reverse-logistics gap | -0.6% | Developed regions with strict disposal rules | Medium term (2–4 years) |

| Methanol-handling toxicity rules | -0.3% | Maritime & industrial applications worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership

The DOE targets call for USD 5/W for 5–50 W units, yet portable stacks average well above that, challenging penetration where the upfront price dominates the buying criteria.(4)U.S. Department of Energy, “DOE Technical Targets for Fuel Cell Systems for Portable Power,” energy.gov Battery packs are trending toward USD 86/kWh by 2035, widening the economic gap in low-power consumer gadgets.(5)Argonne National Laboratory, “Cost Analysis and Projections for U.S.–Manufactured Automotive Lithium-ion Batteries,” anl.gov Printed-circuit-board fuel cells promise lower tooling costs but still face catalyst price pressures and certification lead-times.

Competition from Advanced Li-ion Power Banks

High-nickel NMC cells now exceed 300 Wh/kg, narrowing the runtime advantage once exclusive to fuel cells. Convenience and ubiquitous charging networks make lithium-ion preferable for small electronics, forcing fuel-cell vendors to pivot toward applications where refueling speed or silent operation supersede cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: PEMFC Dominance Faces SOFC Challenge

Proton Exchange Membrane Fuel Cells (PEMFC) technology captured 54.8% of the portable fuel cell market share in 2024 and benefits from mass power density approaching 1,000 W/kg. UCLA’s graphene-protected platinum catalyst pushes projected lifespans beyond 200,000 hours, staving off durability concerns. Solid Oxide Fuel Cells (SOFCs) are projected to achieve a 6.8% forecast CAGR through 2030, driven by fuel flexibility and the development of new proton-conductive perovskites that enable operation at temperatures ranging from 200 to 500 °C without degradation. Direct methanol fuel cells remain a niche technology in marine and surveillance devices, sacrificing 20–30% efficiency for the convenience of liquid fuel.

Field data show PEMFC units powering soldier radios reset within seconds after cold starts, whereas SOFC modules deliver multi-fuel versatility for telecom towers where diesel replacement is mandated. Hybrid stacks that couple PEMFC startup speed with SOFC steady-state efficiency are under early testing.

By Power Rating: Sub-100 W Systems Lead Scale-Up

Sub-100 W devices held 49.5% share in 2024, dominating consumer and IoT nodes that require lightweight packs. Mesodyne’s 10-pound LightCell, which supplies 100–200 W, illustrates the miniaturization trend while meeting MIL-STD-810 ruggedness criteria. The 100 W–1 kW band, forecasted at a 7.4% CAGR, aligns with edge-server racks, forward-operating bases, and broadcast equipment that require quick refueling versus multi-hour battery swaps.

Modular designs now scale above 1 kW by paralleling 500 W cartridges, enabling disaster-response teams to run medical refrigerators for 72 hours without grid access. High-power prototypes, such as Intelligent Energy’s 175 kW ultrathin stack, prove that portability thresholds are moving upward for aviation and heavy-lift drones.

By Fuel Type: Hydrogen Ecosystem Maturation

Hydrogen retained a 59.1% share of the portable fuel cell market in 2024 and is projected to post the fastest 7.0% CAGR as LOHC technologies simplify long-distance transport. Eneos and Honeywell’s carrier collaboration points to bulk movement using existing tanker fleets, reducing compression costs and safety hurdles. Methanol continues to serve sea buoys and polar stations, where storage temperatures make the use of gaseous fuels challenging.

Direct hydrocarbon PEMFC research reveals that unsaturated additives can mitigate carbon deposition, potentially opening the door to the use of propane or butane cartridges for recreational purposes. Standardization under ISO 6583:2024 provides quality benchmarks that spur maritime adoption.

By Application: Military Growth Outpaces Consumer Electronics

Consumer electronics commanded a 34.7% share in 2024 but now face stiff competition from high-density batteries. The military segment is forecast to grow at a 7.3% CAGR through 2030, as programs such as the U.S. Army’s STAMP achieve 50% fuel savings over diesel generators in microgrids. Emergency backup kits leveraging PEMFC extend runtimes beyond 72 hours for telecom towers during hurricanes, filling a runtime niche between batteries and trailer generators.

Industrial equipment makers retrofit warehouse forklifts with hydrogen cylinders to lower charging downtime, while UAV Corp’s hydrogen airships underscore expansion into long-endurance aerial platforms.

Geography Analysis

North America’s current dominance stems from sizable defense allocations, data center construction, and university-led catalyst innovations that extend stack lifetimes past 200,000 hours. U.S. federal safety rules covering hydrogen vehicles and aircraft auxiliary systems create a harmonized component ecosystem. Canada’s hydrogen-ammonia corridor from Alberta to the Pacific supports mobile generators for mining camps, while Mexico’s maquiladoras assemble balance-of-plant components under USMCA trade protections. Regional headwinds include slow retail hydrogen dispense build-outs, which could limit uptake in consumer electronics refills.

The Asia-Pacific’s rise is anchored by China’s public funding for FCV fleets, Japan’s leadership in safety codes, and India’s expanding low-cost manufacturing capacity. Korean conglomerates funnel fuel-cell know-how from stationary CHP into transportable frames, lowering per-unit overhead. ASEAN island nations are eyeing portable stacks for telecom towers, where storms frequently disrupt diesel supply lines. The regional ecosystem benefits from integrated supply chains that taper platinum intensity and improve membrane durability.

Europe positions portable fuel cells within its Fit-for-55 agenda, substituting diesel generators at construction sites, festivals, and emergency locations. Germany’s defense sector boosts demand for ruggedized units, while the Netherlands tests methanol cartridges on coastal surveillance buoys. The United Kingdom’s hydrogen economy targets of 10 GW by 2030 are being fostered through demonstration projects, but face permitting delays that slow down retail roll-outs. Nordic countries leverage surplus wind-hydro capacity to generate green hydrogen, which is then fed into portable cartridge filling hubs.

Competitive Landscape

The portable fuel cell competition features a blend of diversified industrial companies and niche innovators. SFC Energy’s 45% EBITDA gain in 2024 stems from Asian military orders and European construction rentals. Ballard Power’s 48% increase in stack shipments owes to data-center collaborations with Vertiv. Horizon Fuel Cell drives AEM breakthroughs that reduce electrolyzer costs, thereby indirectly lowering the hydrogen price per kilogram and expanding serviceable markets.

Emerging disruptors include ECL, whose fully leased AI-focused data center demonstrates bankability at utility scale; Intelligent Energy, whose ultrathin 175 kW stack unlocks aviation opportunities; and Mesodyne, which targets covert operations with light-cell generators. Competitive differentiation is shifting from raw efficiency to package-level integration, refill logistics, and service networks.

Patent activity around nitrogen-doped alloy catalysts and PCB-integrated membranes suggests that material advances will continue to erode cost premiums over batteries. However, the sector remains moderately fragmented, with the top five vendors controlling just under 40% of 2024 revenue, implying ample room for consolidation or strategic alliances.

Portable Fuel Cell Industry Leaders

SFC Energy AG

Ballard Power Systems

Plug Power Inc.

Horizon Fuel Cell Tech.

Intelligent Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UAV Corp secured USD 105 million LOIs for DART hydrogen airships set for early-2025 launch.

- December 2024: The U.S. Army revealed its first hydrogen nanogrid at White Sands Missile Range, replacing diesel sets.

- October 2024: ECL inaugurated the 1 GW TerraSite-TX1 off-grid hydrogen data center near Houston.

- July 2024: Intelligent Energy introduced IE-FLIGHT hydrogen stacks targeting regional aircraft.

Global Portable Fuel Cell Market Report Scope

| Proton Exchange Membrane Fuel Cells (PEMFC) |

| Direct Methanol Fuel Cells (DMFC) |

| Solid Oxide Fuel Cells (SOFC) |

| Others (Alkaline, Reversible, etc.) |

| Below 100 W |

| 100 W to 1 kW |

| Above 1 kW |

| Hydrogen |

| Methanol |

| Other Fuels |

| Consumer Electronics |

| Military and Defence |

| Emergency Backup |

| Remote Monitoring and Off-grid Power |

| Industrial Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Proton Exchange Membrane Fuel Cells (PEMFC) | |

| Direct Methanol Fuel Cells (DMFC) | ||

| Solid Oxide Fuel Cells (SOFC) | ||

| Others (Alkaline, Reversible, etc.) | ||

| By Power Rating | Below 100 W | |

| 100 W to 1 kW | ||

| Above 1 kW | ||

| By Fuel Type | Hydrogen | |

| Methanol | ||

| Other Fuels | ||

| By Application | Consumer Electronics | |

| Military and Defence | ||

| Emergency Backup | ||

| Remote Monitoring and Off-grid Power | ||

| Industrial Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the portable fuel cell market in 2030?

The market is forecast to reach USD 581.26 million by 2030.

Which technology leads current adoption?

Proton Exchange Membrane Fuel Cells hold 54.8% market share as of 2024.

Why are military programs important for growth?

Defense agencies adopt portable fuel cells for silent, runtime-rich power in contested areas, supporting the fastest 7.3% CAGR application segment.

How fast is Asia-Pacific growing?

Asia-Pacific is advancing at an 8.3% CAGR through 2030, driven by China’s hydrogen infrastructure and Japanese regulations.

What restrains consumer electronics uptake?

Falling lithium-ion battery prices and convenient charging options limit fuel cell competitiveness in small devices.

Which power band is expanding quickest?

The 100 W–1 kW range is slated to rise at 7.4% CAGR, fueled by edge-computing and tactical communications needs.

Page last updated on: