Alkaline Fuel Cells Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

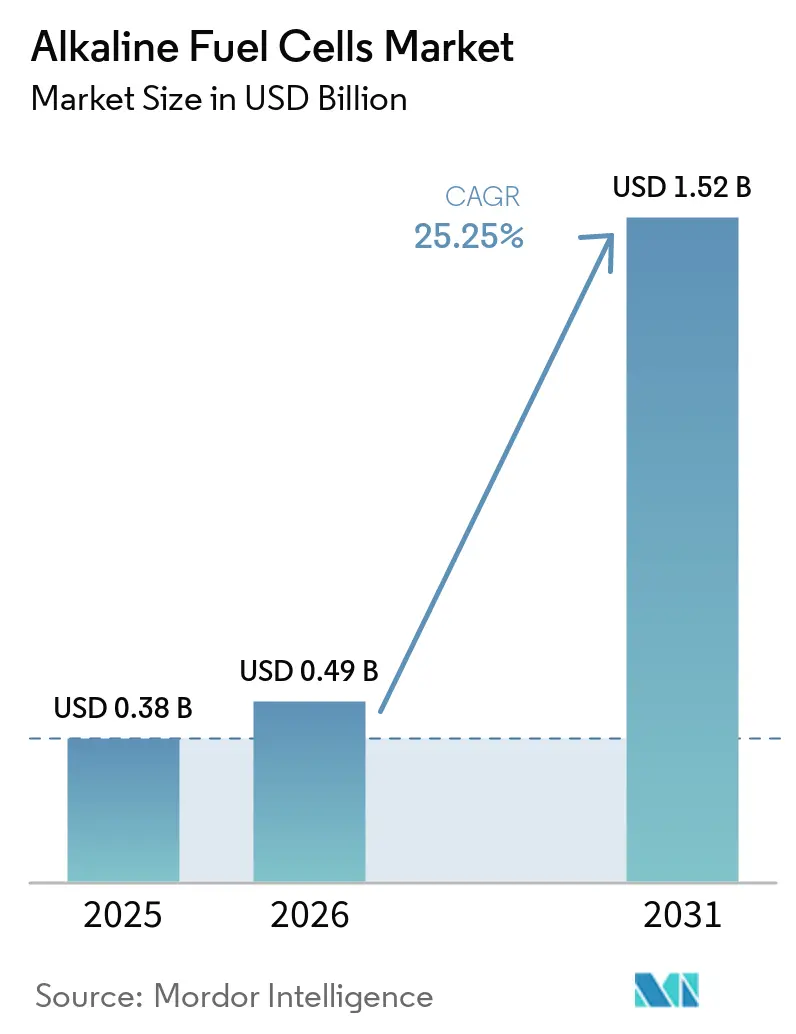

| Market Size (2026) | USD 0.49 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 25.25% CAGR |

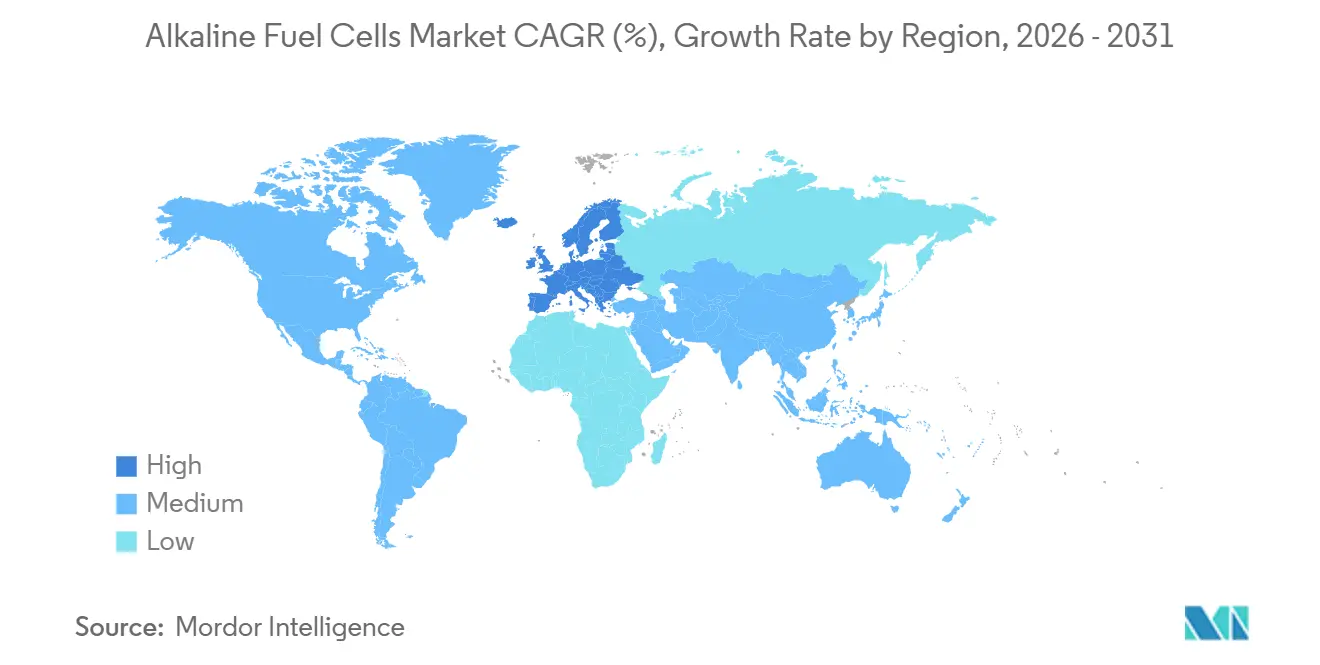

| Fastest Growing Market | Europe |

| Largest Market | North America |

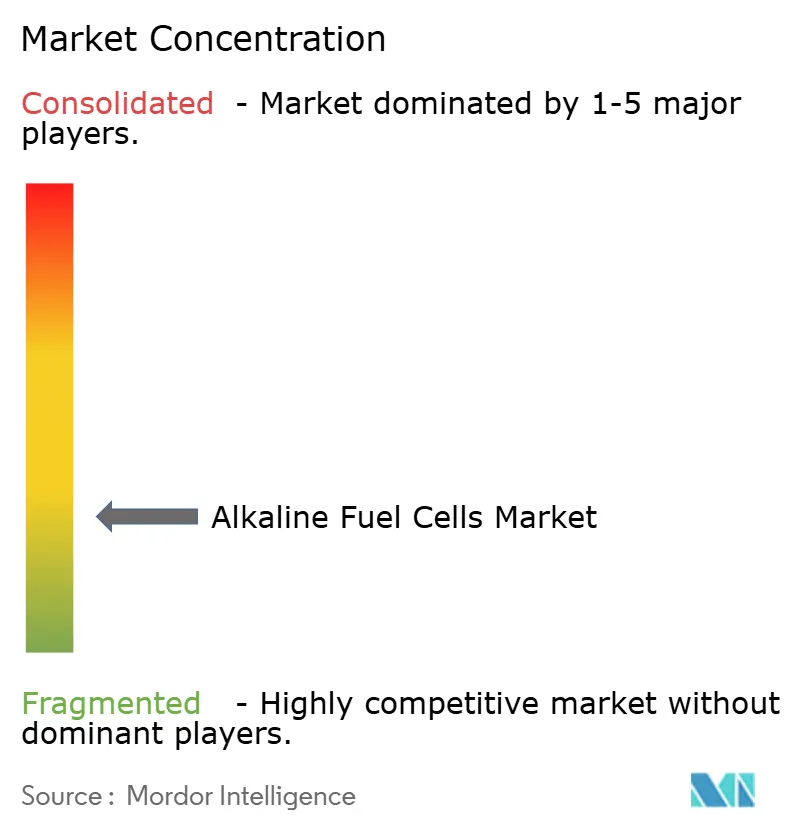

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alkaline Fuel Cells Market Analysis by Mordor Intelligence

The Alkaline Fuel Cells Market size was valued at USD 0.38 billion in 2025 and is estimated to grow from USD 0.49 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 25.25% during the forecast period (2026-2031). A confluence of defense procurement, falling electrolyzer prices, and maritime demand for green-ammonia bunkering is accelerating adoption. Statutory hydrogen-hub incentives in the United States and the European Hydrogen Bank’s offtake auctions are lowering project risk. At the same time, telecom operators and mining majors validate multi-megawatt installations that displace diesel. Venture investment in anion-exchange platforms is rising because lower platinum-group-metal loadings reduce stack costs, and this dynamic is attracting PEMFC incumbents seeking portfolio diversification. Headline risks such as CO₂-induced electrolyte poisoning and shorter stack life relative to PEMFC temper near-term penetration in automotive, but have a limited effect on stationary opportunities where cost per kilowatt dominates.

Key Report Takeaways

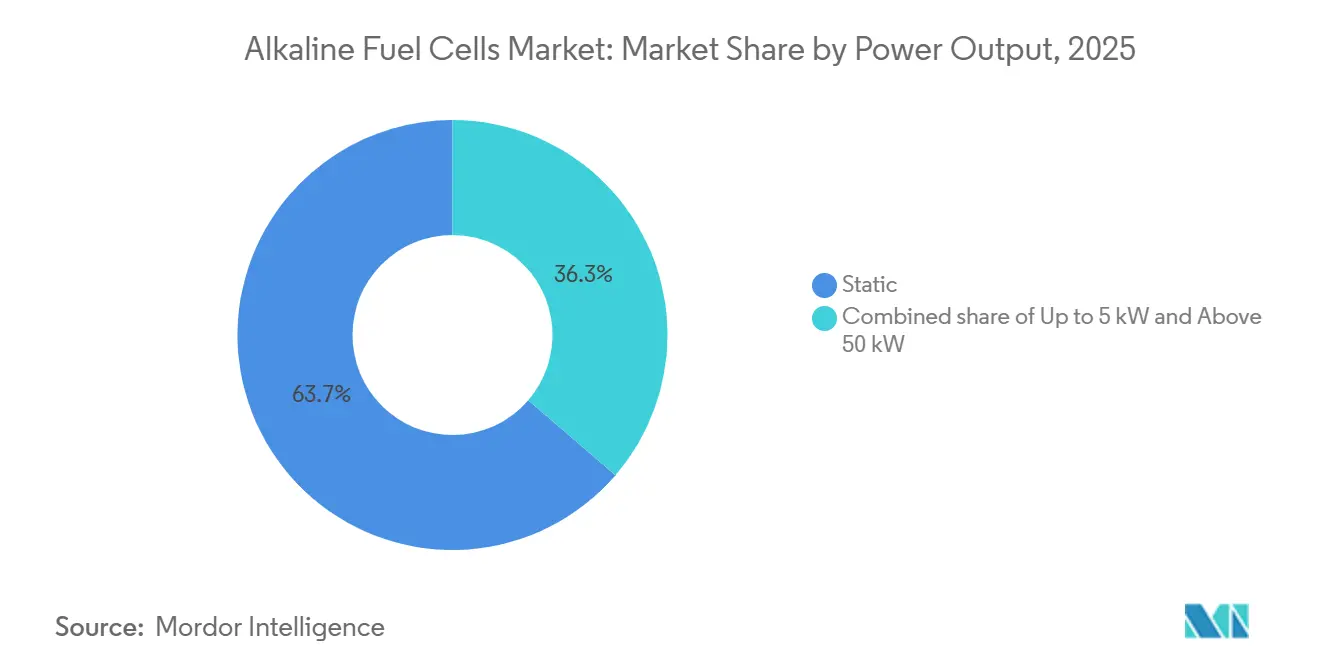

- By type, static systems led with 63.7% of the alkaline fuel cells market share in 2025; mobile and portable variants are set to expand at a 27.3% CAGR to 2031.

- By power output, the 5–50 kW range accounted for 44.5% of the alkaline fuel cells market size in 2025, while the sub-5 kW class is advancing at 28.9% CAGR through 2031.

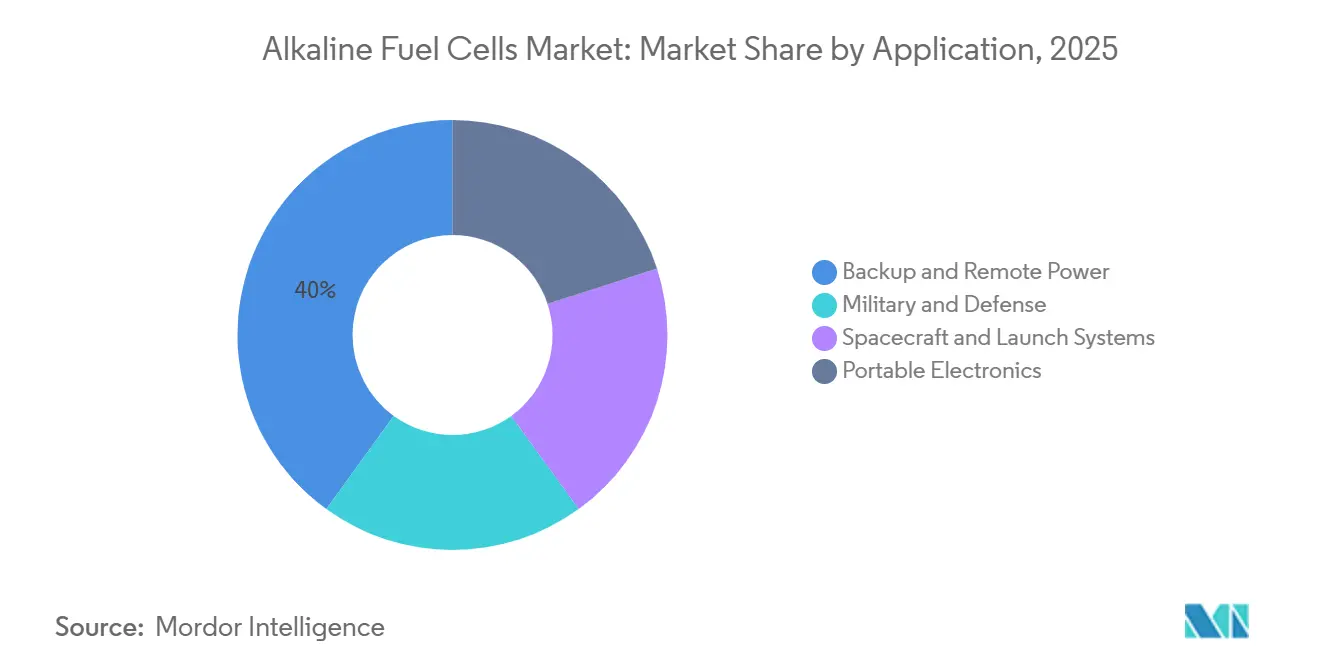

- By application, backup and remote power represented 40% revenue share in 2025, and military and defense usage is growing at 28.2% CAGR over the forecast window.

- By geography, North America held 37.4% share in 2025, whereas Europe is forecast to deliver a 26.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alkaline Fuel Cells Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining electrolyzer costs | +6.80% | Global, with early gains in Europe, China, and Middle East | Medium term (2-4 years) |

| Growing military demand for silent power | +7.20% | North America & Europe, spillover to APAC allies (Japan, South Korea, Australia) | Short term (≤ 2 years) |

| Rise of green ammonia bunkering needs | +5.50% | Europe & Asia-Pacific maritime hubs, emerging in Middle East | Long term (≥ 4 years) |

| Stranded-renewable integration at remote mines | +4.90% | Global, concentrated in Canada, Australia, Chile, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Electrolyzer Costs Drive Commercial Viability

Widespread scale-up brings alkaline electrolyzer capex to USD 389.5 per kW for sub-20 MW plants and USD 82.8 per kW for larger units, narrowing hydrogen’s cost gap with fossil fuels(1) U.S. Department of Energy, “U.S. DOE Hydrogen Program 2023 Annual Merit Review,” energy.gov. Nickel-based electrodes avoid platinum group metals, trimming bill-of-materials risk and pushing stack life beyond 80,000 h. Targeted R&D support, such as the U.S. Department of Energy’s USD 5 million grant to Avium, continues to improve catalyst efficiency and longevity(2) Sophia Espinosa, “Engineer Research and Development Center Celebrates US Army's First Hydrogen-Powered Nanogrid,” army.mil. Similar EU initiatives funnel funding toward next-generation alkaline technology, hastening the rollout of 40 GW of renewable hydrogen electrolyzers by 2030. These developments amplify near-term bankability and underpin the alkaline fuel cells market’s aggressive growth path.

Growing Military Demand for Silent Power Systems

Defense establishments are accelerating procurement to replace noisy diesel generators with silent, high-energy-density hydrogen solutions. The U.S. Army’s first hydrogen nanogrid at White Sands Missile Range validates 24/7 off-grid surveillance power and establishes a blueprint for broader base deployment(3)FuelCellsWorks, “Department of Energy Awards USD 5 Million to Avium,” fuelcellsworks.com. Soldier-portable targets call for over 1,000 Wh/kg energy densities at 0.1-3 kW, readily achievable with nickel-based alkaline stacks dispensing with precious metals. European forces mirror this trend, evidenced by Bundeswehr orders for off-grid units. Resultant near-term demand adds meaningful volume to the alkaline fuel cells market and de-risks manufacturers’ scale-up plans.

Rise of Green Ammonia Bunkering Needs

International Maritime Organization carbon limits encourage operators to retrofit or build vessels fueled by ammonia. Direct-ammonia alkaline stacks sidestep the need for energy-intensive hydrogen cracking and tolerate trace impurities, overcoming a key hurdle PEM units face. DNV approvals of 1 MW demonstrators and Wärtsilä’s engine platforms underscore readiness. Growth of green-ammonia bunkering corridors in the EU and APAC expands the serviceable obtainable market over the long term.

Stranded-Renewable Integration at Remote Mines

Wind-rich but grid-poor mining sites increasingly deploy hybrid systems combining turbines, batteries, and alkaline fuel cells. Case studies such as Canada’s Raglan Mine highlight 50% CO₂ cuts and sub-12-year paybacks. Hydrogen storage cushions multi-day intermittency, making alkaline stacks a linchpin for continuous operations. As commodity producers pledge decarbonization, remote energy demand feeds directly into the alkaline fuel cells market pipeline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CO₂-induced electrolyte poisoning | -3.20% | Global, acute in urban and industrial environments with high ambient CO₂ | Short term (≤ 2 years) |

| Short stack life vs PEMFC | -2.80% | Global, particularly impactful in high-utilization commercial applications | Medium term (2-4 years) |

| Nickel price volatility impact on electrode costs | -1.70% | Global, with supply concentrated in Indonesia, Philippines, Russia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

CO₂-Induced Electrolyte Poisoning Limits Deployment Flexibility

Potassium hydroxide electrolytes react with atmospheric CO₂ to form carbonate salts, lowering ionic conductivity and cutting efficiency over time. High-purity hydrogen and scrubbing hardware add cost and complexity, discouraging deployment in CO₂-rich industrial settings. Mitigation through membrane innovations is promising yet remains nascent, constraining near-term addressable volume.

Short Stack Life Compared with PEM Technology

AFC stacks average 10,000-15,000 h against PEMFC’s 20,000-30,000 h, doubling the levelized cost in high-duty sites. NREL’s 2025 field data showed telecom AFC stacks needed replacement every 18 months while PEM equivalents ran 36 months. AFC Energy is trialing nickel-alloy electrodes aimed at 20,000 h, and academic consortia are testing membrane-based alkaline designs, but until commercialization, the durability gap caps penetration in 24-7 industrial loads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Static Systems Dominate, Portables Accelerate

Static units captured 63.7% of 2025 revenue as telecom, microgrid, and industrial users valued low cost per kilowatt and multi-day autonomy. Verizon’s national cell-tower program illustrates how diesel displacement creates recurring demand for hydrogen cartridges and service spares. Portable and mobile systems, although smaller, are advancing at 27.3% CAGR as militaries procure silent power below 5 kW. A 2025 U.S. Special Operations Command order for 500 units highlights rising tactical adoption.

Lighter composite vessels halve hydrogen weight, and integrated pumps shrink balance-of-plant footprints, enabling 1-3 kW packs under 20 kg that deliver 48-72 h runtime. Commercial users, film crews, and emergency responders value low noise and rapid refueling. Static installations will still command the bulk of the alkaline fuel cells market through 2031 because large-scale backup outspends portable volumes, yet mobile growth signals diversification beyond infrastructure.

By Power Output: Mid-Range Leads, Micro Systems Surge

Systems rated 5–50 kW held 44.5% share in 2025 because they align with diesel genset retrofits in telecom, retail microgrids, and hydrogen dispensers. AFC Energy’s S-Series can be paralleled for hundreds of kilowatts, offering modular resilience. Sub-5 kW platforms are growing fastest at 28.9% CAGR, and their alkaline fuel cells market size is forecast to triple by 2031 as ruggedized electronics, sensors, and off-grid cabins seek multi-day power without battery mass.

Above-50 kW deployments serve mining microgrids and maritime auxiliary loads where reversible operation adds value; Nedstack’s 100-250 kW stacks showed >50% round-trip efficiency in Dutch pilots.

By Application: Backup Power Leadership Faces Military Challenge

Backup and remote power comprised 40% of 2025 demand because utilities, telecoms, and data centers replaced diesel to cut carbon and theft. AFC systems running on locally cracked ammonia provide unattended operation for up to 5,000 h, fitting stringent uptime targets. Military and defense spending is scaling at 28.2% CAGR as fuel-cell nanogrids, unmanned aerial vehicles, and soldier-portable kits mature.

Spacecraft, though niche, burnish technology credentials; ESA chose regenerative AFC for its lunar base-camp because water by-product supports life support, a factor that raises profile for extreme environments. Portable electronics remain limited by cartridge distribution but find adoption in professional cinematography and scientific fieldwork. Seasonal backup for agriculture and rural clinics represents latent upside as hydrogen supply chains deepen.

Geography Analysis

North America generated 37.4% of 2025 revenue, buoyed by USD 3 kg-¹ hydrogen production credits and Department of Defense contracts. Gulf Coast hubs leverage repurposed gas pipelines, while Canada’s remote mines substitute diesel at USD 2 L-¹ parity. Mexico lags but may piggyback on cross-border hydrogen trade as U.S. production scales.

Europe is the fastest-growing region at 26.6% CAGR to 2031, powered by REPowerEU, the EUR 9 billion German hydrogen budget, and port-side ammonia cracking for logistics hubs. The Renewable Energy Directive III sets binding RFNBO quotas that secure long-term offtake, stabilizing the alkaline fuel cells market. Nordic hydropower offers low-carbon hydrogen at competitive cost, driving early adoption in datacenters and ferry fleets.

Asia-Pacific growth is uneven. Japan and South Korea subsidize residential fuel cells, yet alkaline chemistries stay focused on backup duty. Australia and Chile replicate Canadian mine microgrids, while Middle East ports explore AFC auxiliary units tied to solar-linked ammonia exports. South America’s Chilean roadmap targets 25 GW of electrolyzers by 2030, implying downstream fuel-cell balancing demand.(4)Federal Ministry for Economic Affairs and Climate Action, “German National Hydrogen Strategy Update 2025,” bmwk.de

Competitive Landscape

The alkaline fuel cells market is fragmented. AFC Energy and GenCell dominate the stationary and telecom niches on the back of multi-year reference projects, whereas EvolOH and Next Hydrogen pursue anion-exchange designs that remove liquid electrolyte and cut noble-metal use. EvolOH’s USD 30 million Series A aims to commission a 100 MW factory by 2026, pairing with Mitsubishi Heavy Industries to field reversible systems for storage projects.

Strategic alliances multiply as firms secure distribution. AFC Energy’s pact with H-Power targets 50 MW in South Korea, combining local manufacturing and refueling integration. GenCell partners with BOXPower to embed AFCs in solar-storage microgrids for public-safety PSPS zones, a step that widens U.S. rural utility exposure.

White-space plays include agricultural backup, refrigerated transport APUs, and humanitarian relief kits. Patent activity in anion-exchange membranes rose 40% in 2024-2025, led by Japanese and Chinese institutes, hinting at next-gen designs that may finally close the durability gap with PEMFC and unlock automotive volumes. Compliance with IEC 62282 safety norms has become a procurement prerequisite, favoring companies with mature test infrastructure and generating a niche for certification specialists.(5)World Intellectual Property Organization, “Anion-Exchange Membrane Patent Filings 2025,” wipo.int

Alkaline Fuel Cells Industry Leaders

AFC Energy plc

GenCell Ltd.

FuelCell Energy Inc.

Plug Power Inc.

Ballard Power Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AFC Energy announced a strategic pivot toward commercializing hydrogen generators that hit diesel cost parity by 2026 and launched the Hy-5 portable ammonia cracker for maritime use.

- August 2024: Stargate Hydrogen partnered with BGR Tech to supply alkaline electrolyzers for India’s National Green Hydrogen Mission rollout.

- July 2024: AFC Energy signed a supplier deal with Zollner Elektronik to scale S Series module manufacturing in Germany.

- July 2024: GenCell deployed its first EVOX system at the California Mobility Center, integrating hydrogen fuel cells, batteries, and AI software for fast EV charging.

Global Alkaline Fuel Cells Market Report Scope

Alkaline Fuel Cells (AFCs) are high-efficiency, low-temperature electrochemical devices that convert hydrogen and oxygen into electricity, water, and heat. Utilizing an alkaline electrolyte, commonly potassium hydroxide, they allow for cheaper, non-noble metal catalysts (e.g., nickel or silver) at the electrodes, providing a cost-effective alternative to acidic fuel cells.

The Global Alkaline Fuel Cells Market is segmented into type, power output, application, and geography. By type, the market is segmented into static and mobile/portable systems. By power output, the market is segmented into up to 5 kW, 5 to 50 kW, and above 50 kW. By application, the market is segmented into military and defense, spacecraft and launch systems, backup and remote power, and portable electronics. The report also covers the market size and forecasts for the alkaline fuel cells market in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Static Alkaline Fuel Cells |

| Mobile/Portable Alkaline Fuel Cells |

| Up to 5 kW |

| 5 to 50 kW |

| Above 50 kW |

| Military and Defense |

| Spacecraft and Launch Systems |

| Backup and Remote Power |

| Portable Electronics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Static Alkaline Fuel Cells | |

| Mobile/Portable Alkaline Fuel Cells | ||

| By Power Output | Up to 5 kW | |

| 5 to 50 kW | ||

| Above 50 kW | ||

| By Application | Military and Defense | |

| Spacecraft and Launch Systems | ||

| Backup and Remote Power | ||

| Portable Electronics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the alkaline fuel cells market by 2031?

It is expected to reach USD 1.52 billion by 2031 at a 25.25% CAGR.

Which region will grow fastest through 2031?

Europe is forecast to register the quickest expansion at 26.6% CAGR, driven by REPowerEU targets and Hydrogen Bank auctions.

Why are military agencies adopting AFC technology?

Silent operation, low thermal signature, and reduced fuel-convoy logistics make AFCs attractive for forward bases and unmanned systems.

What technical barrier most restricts broad deployment?

CO₂-induced electrolyte poisoning shortens stack life in ambient-air applications, raising maintenance costs.

How do alkaline fuel cells compare to PEM fuel cells in durability?

Current AFC stacks last 10,000-15,000 h versus 20,000-30,000 h for PEM, though next-generation anion-exchange designs aim to close the gap.

Page last updated on: