Polyurethane Foam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

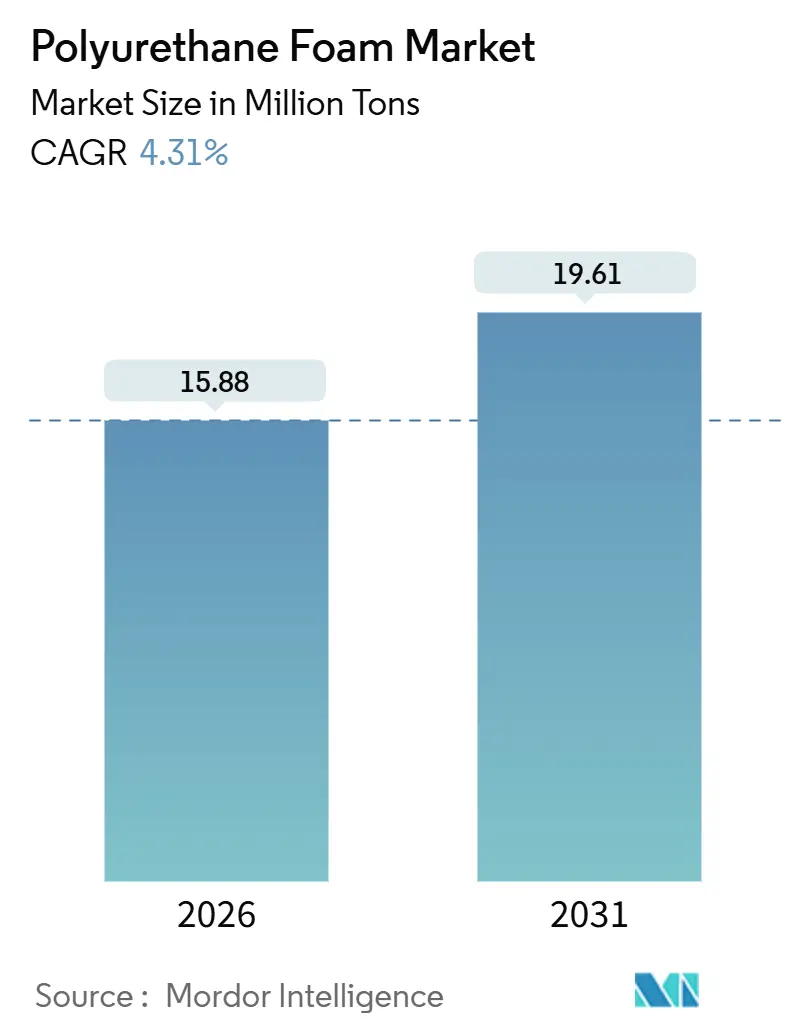

| Market Volume (2026) | 15.88 Million tons |

| Market Volume (2031) | 19.61 Million tons |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurethane Foam Market Analysis by Mordor Intelligence

The Polyurethane Foam Market size is estimated at 15.88 million tons in 2026, and is expected to reach 19.61 million tons by 2031, at a CAGR of 4.31% during the forecast period (2026-2031). Growth is migrating from green-field capacity additions toward retrofit demand generated by tougher energy-efficiency codes, rising electric-vehicle (EV) production, and the rapid build-out of global cold-chain logistics. Momentum in specialty formats such as spray, integral-skin, and viscoelastic foams is accelerating as builders look for materials that deliver high R-values in tight spaces, while automotive original-equipment manufacturers (OEMs) specify bespoke battery-pack enclosures that combine thermal management with lightweighting. Regulatory initiatives—Europe’s Energy Performance of Buildings Directive, China’s GB 50189-2024 standard, and the United States’ 2024 International Energy Conservation Code—are lifting baseline consumption, whereas price volatility in methylene diphenyl diisocyanate (MDI) and toluene diisocyanate (TDI) feeds continues to pressure converters’ margins. Integrated suppliers with captive isocyanate capacity and early-stage bio-based polyol platforms are widening the competitive gap as customers seek verified decarbonization pathways and secure raw-material availability.

Key Report Takeaways

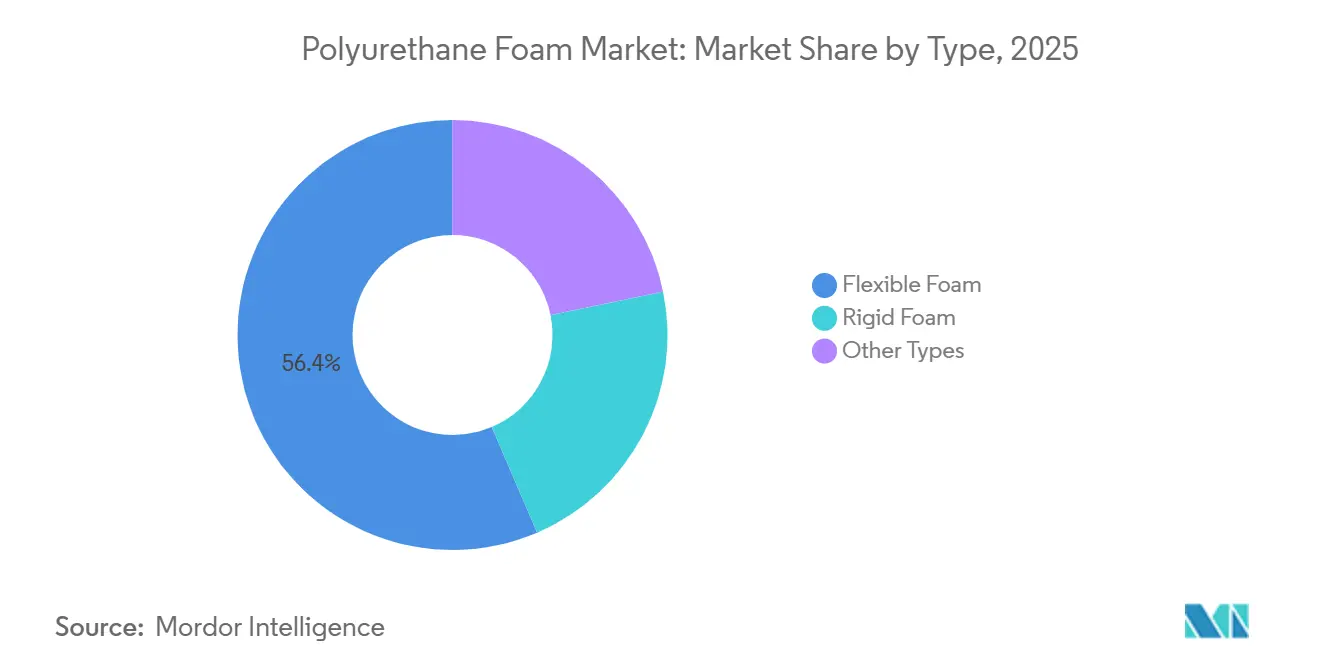

- By type, flexible foam led with 56.44% of polyurethane foam market share in 2025, while other formats are forecast to post the fastest 6.49% CAGR through 2031.

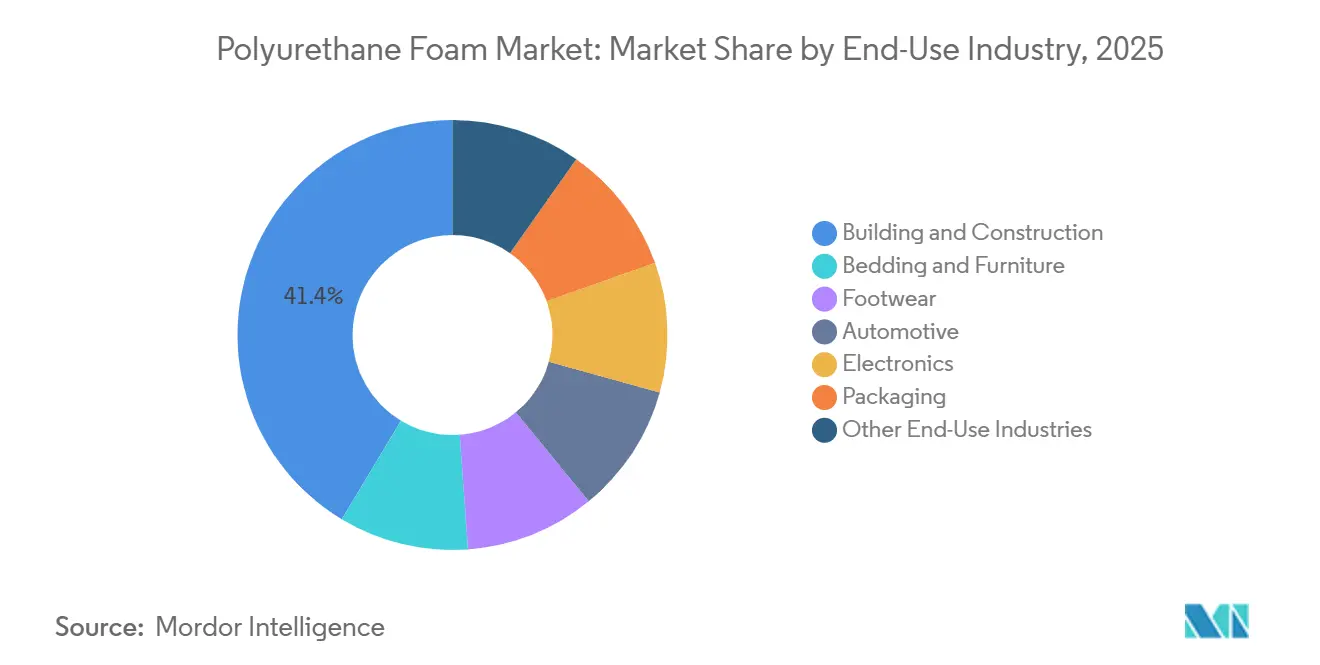

- By end-use, building and construction absorbed 41.39% of volume in 2025, but packaging is advancing at a market-leading 7.26% CAGR through 2031.

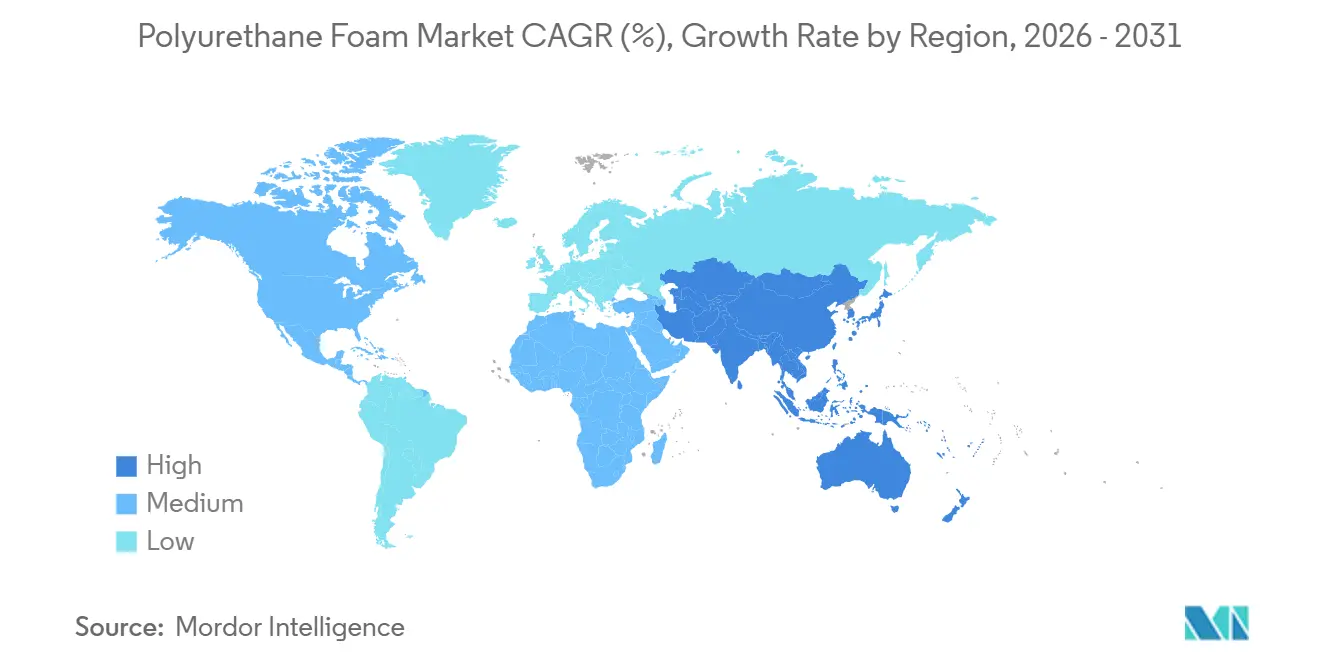

- By geography, Asia-Pacific accounted for 49.58% of global polyurethane foam market consumption in 2025; the region is projected to expand at a 6.36% CAGR to 2031, the strongest regional trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyurethane Foam Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient building insulation demand | +1.2% | Global, strongest in Asia-Pacific and Europe | Medium term (2-4 years) |

| Automotive lightweighting and comfort applications | +0.9% | Asia-Pacific core plus North America | Medium term (2-4 years) |

| Furniture and mattress production upsurge | +0.7% | Asia-Pacific, spillover Latin America | Short term (≤ 2 years) |

| Cold-chain and refrigeration capacity expansion | +0.8% | Global, fastest in Asia-Pacific and MEA | Long term (≥ 4 years) |

| EV battery thermal-management foams | +0.5% | Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Building Insulation Demand

Governments are tightening thermal-performance requirements, adding 1.2 percentage points to the baseline CAGR in the polyurethane foam market. In 2024, the European Union revised its Energy Performance of Buildings Directive, mandating member states to annually renovate public buildings. This move is guiding specifiers to favor spray polyurethane foam, which offers insulation and achieves air-sealing in a single application. In the United States, eighteen states adopted the 2024 International Energy Conservation Code, raising prescriptive wall insulation from R-13 to R-20 in colder climate zones, a change that places continuous rigid foam sheathing at the forefront of compliance. China's GB 50189-2024 has raised heating-energy limits. This move has pushed developers in northern provinces to shift from expanded polystyrene to closed-cell polyurethane panels[1]Ministry of Housing and Urban-Rural Development of China, “GB 50189-2024,” mohurd.gov.cn. Additionally, spray foam is capturing a larger share in retrofit projects. Its advantage lies in the ability to apply it without removing exterior cladding, reducing installation time. These combined policies ensure a clear demand trajectory over the coming years, especially for existing buildings where energy savings offer appealing payback periods.

Automotive Lightweighting and Comfort Applications

Automotive regulators are mandating higher fuel economy and extended EV range, contributing 0.9 percentage points to to the polyurethane foam market growth. In response to the U.S. Corporate Average Fuel Economy standard aiming for a fleet average of 58 miles per gallon equivalent by 2027, automakers are shifting from traditional padding to low-density flexible polyurethane. This change reduces seat weight without compromising ergonomics. An SAE study found that optimized foam formulations in door panels and headliners can reduce cabin noise at highway speeds, boosting passenger comfort in the quiet cabins of electric vehicles. In China, where new-energy-vehicle sales have grown significantly, local suppliers are collaborating on rigid foams for battery-module gap-filling. These foams are more effective than aerogels at inhibiting thermal-runaway propagation. With benefits in both mass reduction and safety, polyurethane's role in vehicle bills of materials is expanding, leading to increased content per vehicle in both premium and mass-market segments.

Furniture and Mattress Production Upsurge

Higher disposable incomes in Asia-Pacific deliver a 0.7 percentage-point uplift to the polyurethane foam market, most visible in India and Southeast Asia. In 2025, India's organized furniture market saw significant growth. Memory-foam mattresses gained a notable share of the bedding segment, as consumers shifted preferences from coir and cotton. In late 2025, Sheela Foam launched a flexible-foam line in Uttarakhand. The move targets tier-2 cities, where brand penetration is on the rise. Meanwhile, in China, a shift towards online furniture sales is streamlining delivery times. Manufacturers are now using vacuum-compressed foam packaging, reducing shipping volume significantly. This innovation not only supports direct-to-consumer models but also lowers the total landed cost. As a result, there's a broader market for premium foam products, especially in price-sensitive demographics.

Cold-Chain and Refrigeration Capacity Expansion

The rise of temperature-controlled logistics adds 0.8 percentage points to growth, in the polyurethane foam market driven by vaccines, fresh food, and e-commerce grocery. Saudi Arabia's Public Investment Fund allocated resources for a large-scale cold-storage space, targeting completion by 2028. The fund emphasized the use of rigid polyurethane panels with enhanced thermal conductivity to bolster moisture resistance. In 2025, India provided subsidies through its Pradhan Mantri Kisan Sampada Yojana, aiming to expedite the construction of refrigerated warehouses. India showed a preference for prefabricated polyurethane sandwich panels, which can be installed significantly faster compared to traditional site-poured concrete. The pharmaceutical sector is also driving this momentum; Pfizer's 2024 expansion of its mRNA vaccine network necessitated ultra-low-temperature freezer insulation. This specific requirement was exclusively fulfilled using rigid polyurethane in conjunction with vacuum-insulated panels. Given the persistent demand for robust cold chains, the appetite for high-performance foam systems is set to remain strong.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter isocyanate health and environmental rules | -0.6% | Global, with Europe and North America most stringent | Short term (≤ 2 years) |

| Volatility in MDI/TDI feedstock prices | -0.4% | Global, with Europe and North America most exposed | Short term (≤ 2 years) |

| Mycelium/algae bio-foams replacing PU in premium packaging | -0.2% | North America and Europe niche segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Isocyanate Health and Environmental Rules

Widening regulatory scrutiny on diisocyanate exposure is trimming 0.6 percentage points from polyurethane foam market growth. Under the 2024 Significant New Use Rule by the U.S. Environmental Protection Agency, spray-foam teams must don supplied-air respirators and utilize real-time monitoring. This mandate escalates annual compliance expenses for each team, hindering adoption in budget-conscious retrofits. Meanwhile, Europe's REACH update has tightened the occupational exposure limit for TDI. This change mandates converters to invest in closed-loop mixing systems. In 2025, California's Proposition 65 was updated to include MDI. This addition requires retailers to label products with warnings if they contain more than 0.1% MDI[2]Office of Environmental Health Hazard Assessment, “Proposition 65 Update,” oehha.ca.gov. As a result, furniture manufacturers are increasingly leaning towards water-blown formulations, albeit at a cost premium. While there's progress in non-isocyanate polyurethane chemistries, their widespread commercial adoption is still projected to be at least five years away, primarily due to existing cost and performance disparities.

Volatility in MDI/TDI Feedstock Prices

Sharp swings in diisocyanate pricing have compressed converter margins and curtailed long-term contracts. In Europe, MDI spot prices surged due to outages at BASF’s Ludwigshafen and Covestro’s Dormagen complexes. However, prices later retreated, buoyed by a surge in Chinese exports. Meanwhile, U.S. Gulf-Coast TDI quotations oscillated, influenced by force majeure events and anti-dumping duties. In response to these market fluctuations, converters have extended their feedstock holdings as a defensive strategy. This approach locks up working capital and trims their return on invested capital. Integrated suppliers, boasting captive MDI/TDI capacity, are seizing market share by offering fixed-price agreements and expedited order cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Formats Outpace Commodity Flexible

Flexible foam retained 56.44% of the polyurethane foam market share in 2025, anchored by furniture, bedding, and automotive seating applications. However, commodity blocks face margin squeeze from low-cost imports, persuading North American and European converters to shift toward high-resilience and viscoelastic lines that command 30% price premiums. Other formats—spray, integral-skin, and memory foams—are projected to grow at 6.49% CAGR, nearly double the broader market. Spray foam benefits from its ability to air-seal irregular cavities, driving residential retrofit adoption under utility rebate programs in the United States. Integral-skin foams in steering wheels and armrests are gaining favor as EV interiors prioritize tactile quality, while memory foams are migrating from premium mattresses to athletic footwear and medical cushions.

High-growth niches are gaining market share within the polyurethane foam industry by offering performance attributes that alternative materials struggle to match. The U.S. spray-foam segment expanded, spurred by the Inflation Reduction Act's rebate for air-sealing enhancements. Automotive OEMs harnessed integral-skin technology to minimize vibration transmission in EV cabins, now devoid of engine noise. This shift was bolstered by an SAE study highlighting noise reduction. Memory foams, previously limited to sleep products, gained a foothold in running shoes, thanks to Nike's introduction of a dual-density midsole that adapts to the gait cycle. These successes across diverse industries indicate that specialty polyurethane foams are poised to secure a significant portion of future innovation investments and profit margins.

By End-Use Industry: Packaging Surges on Cold-Chain Logistics

Building and construction absorbed 41.39% of volume in 2025, underpinned by mandatory insulation upgrades across Asia-Pacific, Europe, and North America. Yet packaging is the fastest-rising end-use at a 7.26% CAGR, propelled by e-commerce grocery and temperature-sensitive pharmaceuticals. By 2027, Amazon aims to ship half of its fresh groceries using reusable polyurethane-lined totes. This decision comes after recognizing that closed-cell foam can maintain temperatures between 2 °C and 8 °C for up to 48 hours, eliminating the need for gel packs. Pfizer transitioned from polystyrene to polyurethane shippers, achieving a reduction in packaging weight and a boost in pallet density. This shift underscores the potential for significant savings in air-freight costs.

The automotive sector, spurred by the rise of electric vehicles (EVs) and an increased foam content per vehicle, stands as the second-fastest-growing segment in the PU foam market. New-energy vehicles benefit from polyurethane used for seating, acoustic dampening, and battery insulation, contrasting with traditional internal-combustion models. a, the bedding and furniture sectors in the Asia-Pacific region are on a steady growth trajectory, fueled by rising incomes and a trend towards premiumization. Footwear, electronics, and other niche applications collectively represent a significant portion of the demand. Notably, the footwear segment is witnessing a surge in innovation, with brands pursuing enhanced energy returns and reduced carbon footprints through the integration of bio-attributed polyols.

Geography Analysis

Asia-Pacific dominated global consumption with a 49.58% share in 2025 and is on course to grow 6.36% annually to 2031, the highest regional pace. In 2024, China upgraded its GB 50189 standard, boosting wall insulation R-values in heating zones. This change prompted a shift from expanded polystyrene to rigid polyurethane in both commercial and residential projects. India's organized furniture market experienced significant growth in 2025. This uptick coincided with Sheela Foam's capacity expansion, aimed at meeting the rising demand for memory-foam mattresses in tier-2 cities. Japan and South Korea, despite their market maturity, are capitalizing on innovations in electronics and EV batteries. A notable instance is LG Energy Solution's qualification of phase-change-enhanced polyurethane for the E-GMP platform, underscoring the region's technological advancements. In Southeast Asia, investments in cold-chain warehousing, especially in Vietnam and Indonesia, are bolstered by government incentives targeting a reduction in post-harvest food loss.

North America accounted for a significant market share in 2025 and registered steady growth in the US polyurethane foam market. Spray-foam retrofits and EV battery enclosures largely drove the momentum. A significant contributor to this growth was the U.S. Inflation Reduction Act’s Home Energy Rebates, which spurred an increase in spray-foam installations in 2025. Homeowners capitalized on these rebates to mitigate installation expenses. Meanwhile, Canada’s National Building Code 2025 is steering builders towards rigid foam sheathing by mandating continuous insulation across all climate zones. In 2025, Mexico, with a strong vehicle production base, is witnessing a trend where U.S. OEMs are integrating higher polyurethane content. This move aligns with their strategy to near-shore EV assembly, ensuring compliance with regional-content requirements.

Europe is navigating a steady growth trajectory in the polyurethane foam industry. The region grapples with stringent isocyanate regulations while aggressively pursuing retrofit targets. The Energy Performance of Buildings Directive mandates an annual renovation rate for public buildings. This directive leans towards high-efficiency spray foam, even with the challenge of elevated labor compliance costs. South America and the Middle East and Africa (MEA), collectively representing a notable portion of global demand, are experiencing robust growth. In Brazil, municipalities are incentivizing LEED-certified buildings with property-tax rebates, leading to a heightened adoption of polyurethane insulation. In Saudi Arabia, a substantial investment in cold storage is driving demand for rigid panels. Concurrently, in South Africa, the addition of new solar capacity in 2025 is spurring the use of polyurethane-insulated transport for exporting perishables.

Competitive Landscape

The PU foam market is moderately fragmented. Covestro’s Cardyon platform, commercialized in 2024, embeds up to 20% captured CO₂ into polyols and has earned purchase orders from European automotive OEMs looking to trim Scope 3 emissions without compromising crashworthiness. BASF followed in 2025 with Lupranat Bio, a tall-oil fatty-acid-based MDI targeting furniture and mattress customers pressured by retailer carbon-footprint pledges. Startups are exploiting white-space in EV battery and cold-chain packaging where incumbents have limited domain expertise. As sustainability metrics and real-time quality control gain importance, players with integrated feedstock positions, verified low-carbon technologies, and advanced manufacturing analytics are poised to consolidate share.

Polyurethane Foam Industry Leaders

Covestro AG

BASF SE

Dow

Huntsman International LLC

Wanhua Chemical Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: UFP Technologies has enhanced its presence in medical-grade polyurethane foam applications through the acquisition of AQF Medical, reinforcing its expertise in specialized foam solutions. This strategic move is expected to drive innovation and competition in the polyurethane foam market.

- July 2024: BASF has launched Haptex 4.0, a fully recyclable polyurethane solution for synthetic leather. This innovation removes the necessity for layer separation in the recycling process, establishing a new standard for sustainable materials in footwear, automotive interiors, and furniture.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the polyurethane foam market as all freshly manufactured flexible, rigid, and spray polyurethane foams that leave the producer or converter and enter trade channels, expressed in metric tons. We follow volumes flowing into construction, bedding and furniture, automotive, packaging, electronics, and other smaller industrial uses, country by country.

Scope exclusion: rebonded scrap foams, polyurea elastomers, and in-plant cavity-filled systems remain outside this review.

Segmentation Overview

- By Type

- Flexible Foam

- Rigid Foam

- Other Types (Spray Foam, Integral Skin Foam, Memory Foam)

- By End-Use Industry

- Building and Construction

- Bedding and Furniture

- Footwear

- Automotive

- Electronics

- Packaging

- Other End-Use Industries (Medical Devices, Textiles and Apparel, Aerospace)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed foam formulators, panel manufacturers, mattress assemblers, and regional distributors across Asia-Pacific, North America, Europe, and the Gulf. Conversations clarified average sheet densities, scrap rates, seasonality swings, and post-pandemic capacity utilization, allowing us to validate desk assumptions and fine-tune apparent consumption balances.

Desk Research

We began with public fundamentals such as UN Comtrade trade codes, Eurostat production statistics, US Geological Survey plastics data, and construction spending series from bodies like FIEC and the US Census. Patent trends from Questel, building energy code updates posted by the International Energy Agency, and insulation demand notes from the World Bank's housing dashboards helped us gauge end-use pull. Company 10-Ks, investor decks, and press releases provided pricing guidance, which we paired with trade association briefs from sources such as PU Europe and the Center for the Polyurethanes Industry. When needed, we referred to D&B Hoovers and Dow Jones Factiva for standardized revenue splits. These sources are illustrative; many additional publications were consulted for cross-checks and context.

Market-Sizing & Forecasting

A top-down apparent consumption build starts from national production and net trade, followed by adjustments for known captive use. Select bottom-up tests, such as sampled panel board ASP × board feet and seating cushion unit counts, act as reasonableness filters. Key drivers in the model include new home completions, refrigerator output, light vehicle builds, e-commerce parcel growth, MDI/TDI price spreads, and insulation R-value regulations. A multivariate regression on these indicators underpins the 2025-2030 forecast; scenario analysis shades high and low cases where policy or feedstock shocks are plausible.

Data Validation & Update Cycle

We run variance scans against historical trajectories, flag outliers, and reroute queries to experts before sign-off. Reports refresh each year, with interim flashes if material plant outages, policy shifts, or sharp feedstock moves alter our baseline.

Why Mordor's Polyurethane Foam Baseline Stands Firm

Published estimates often differ because firms mix value and volume, fold in downstream CASE products, or apply varying refresh cadences.

Key gap drivers here include Mordor's volume first lens, its exclusion of composites and adhesives, and our annual update rhythm, whereas others publish revenue snapshots based on broader chemistry groupings or older price decks. Currency conversions and divergent ASP inflation assumptions further widen the spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 15.23 million tons (2025) | Mordor Intelligence | - |

| USD 55.70 billion (2024) | Global Consultancy A | Combines foams with coatings and counts distributor mark-ups |

| USD 46.94 billion (2024) | Trade Journal B | Excludes spray foam and uses pre-2023 pricing for rigid grades |

The comparison shows that when scope, metric, and price year are aligned, Mordor's disciplined, annually refreshed volume baseline offers decision-makers a traceable and repeatable starting point they can trust.

Key Questions Answered in the Report

How large is the polyurethane foam market in 2026?

The polyurethane foam market size is 15.88 million tons in 2026, with a forecast to reach 19.61 million tons by 2031, registering a CAGR of 4.31%.

Which region is growing fastest for polyurethane foam demand?

Asia-Pacific is the fastest-growing region, expected to register a 6.36% CAGR through 2031 on the back of stricter building-energy codes and an expanding cold-chain network.

Which end-use is expected to add the most new volume?

Packaging, especially for cold-chain and e-commerce grocery, is projected to grow at a 7.26% CAGR, the highest among all end-uses.

What is the main regulatory headwind facing polyurethane foam producers?

Tightening isocyanate exposure limits in Europe and North America are increasing compliance costs and slowing spray-foam adoption.

How are leading companies improving their sustainability credentials?

Integrated suppliers such as Covestro and BASF have commercialized bio-based polyols and MDI grades that embed captured CO₂ or tall-oil derivatives, reducing product carbon footprints without sacrificing performance.

Page last updated on: