Business Jet MRO Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 31.09 Billion |

| Market Size (2031) | USD 36.39 Billion |

| Growth Rate (2026 - 2031) | 3.20% CAGR |

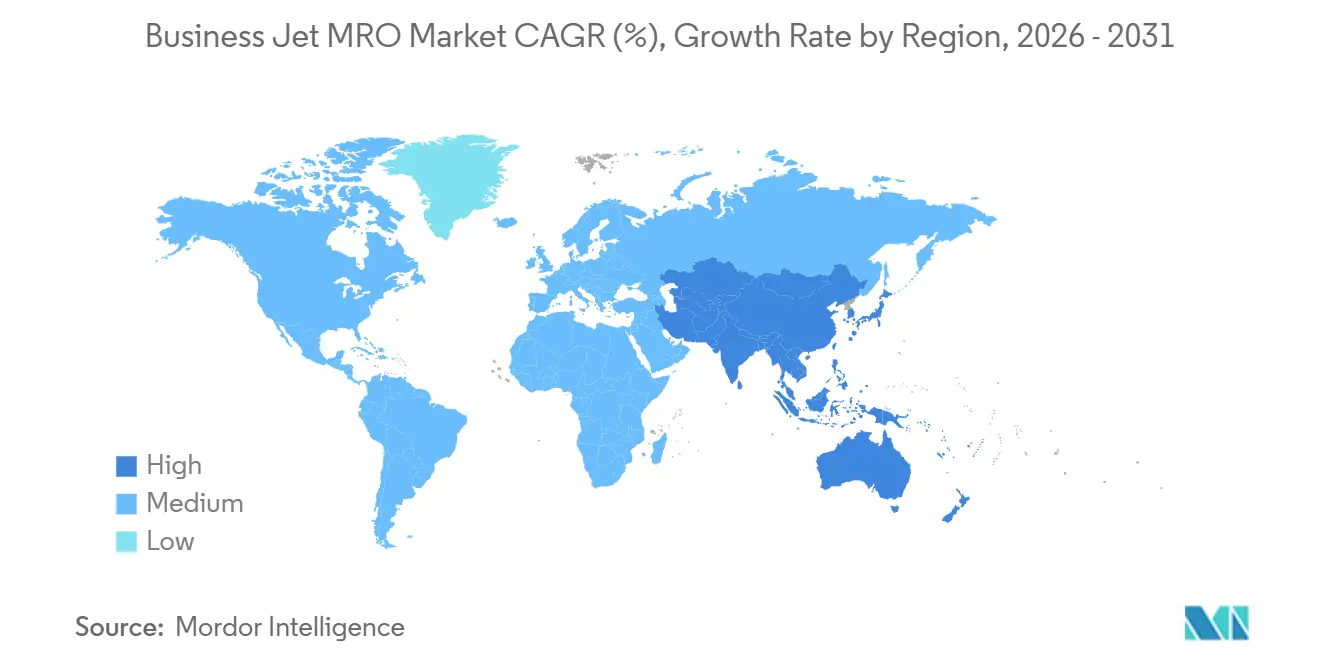

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business Jet MRO Market Analysis by Mordor Intelligence

The business jet MRO market size is expected to grow from USD 30.12 billion in 2025 to USD 31.09 billion in 2026 and is forecasted to reach USD 36.39 billion by 2031 at a 3.20% CAGR over 2026-2031. Growth is driven by operators extending aircraft life cycles, an 18- to 24-month OEM backlog, and a fleet of more than 8,000 jets that are older than 15 years and are entering heavy-maintenance windows. Flight activity in 2025 increased by 3%, led by fractional providers such as NetJets, whose utilization exceeds pre-pandemic thresholds by more than 10%, sustaining demand for on-condition inspections and rotable-pool exchanges. Avionics obsolescence and connectivity retrofits are pushing component-level work, while predictive-maintenance platforms trim unscheduled downtime and shift spending toward shops that can integrate digital diagnostics. Competitive intensity is fragmenting along service-model lines as OEM-affiliated networks bundle power-by-the-hour programs and independents counter with multi-type flexibility, e-commerce parts portals, and rapid-turn operations.

Key Report Takeaways

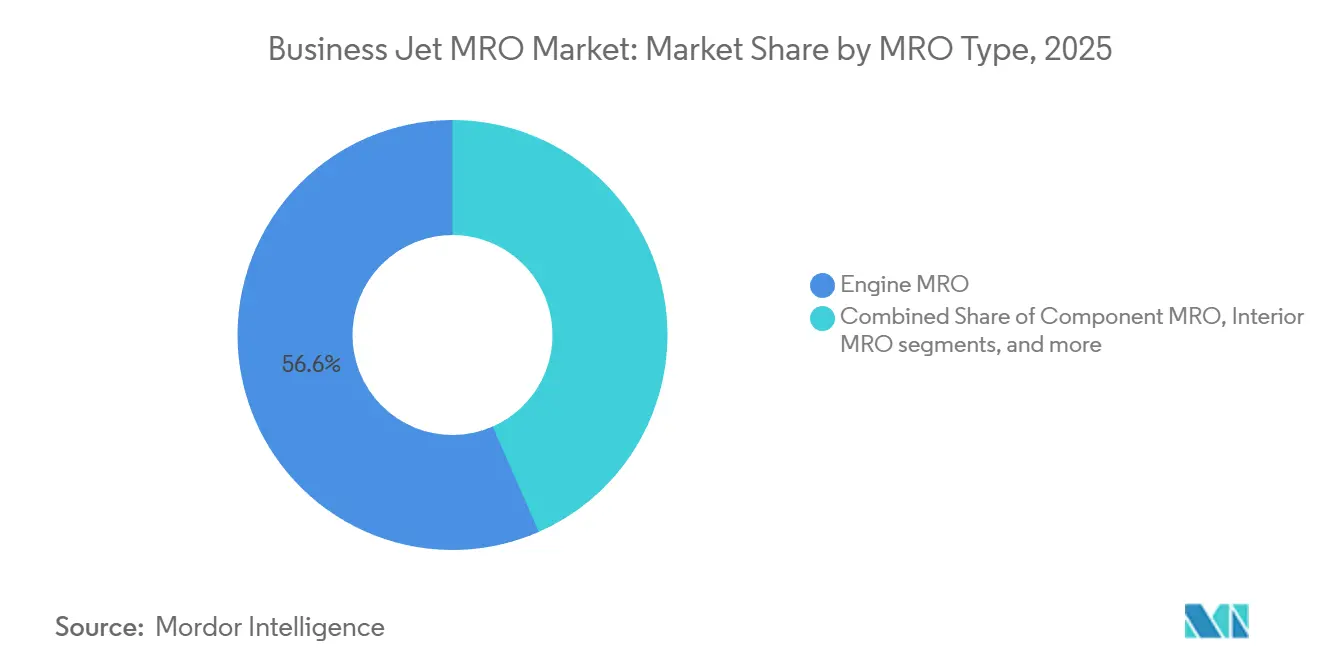

- By MRO type, engine MRO commanded 56.58% of the business jet MRO market share in 2025; component MRO is forecast to expand at a 4.84% CAGR through 2031.

- By body type, large jets led with 42.65% of revenue in 2025, while light and very light jets are projected to grow at a 4.51% CAGR through 2031.

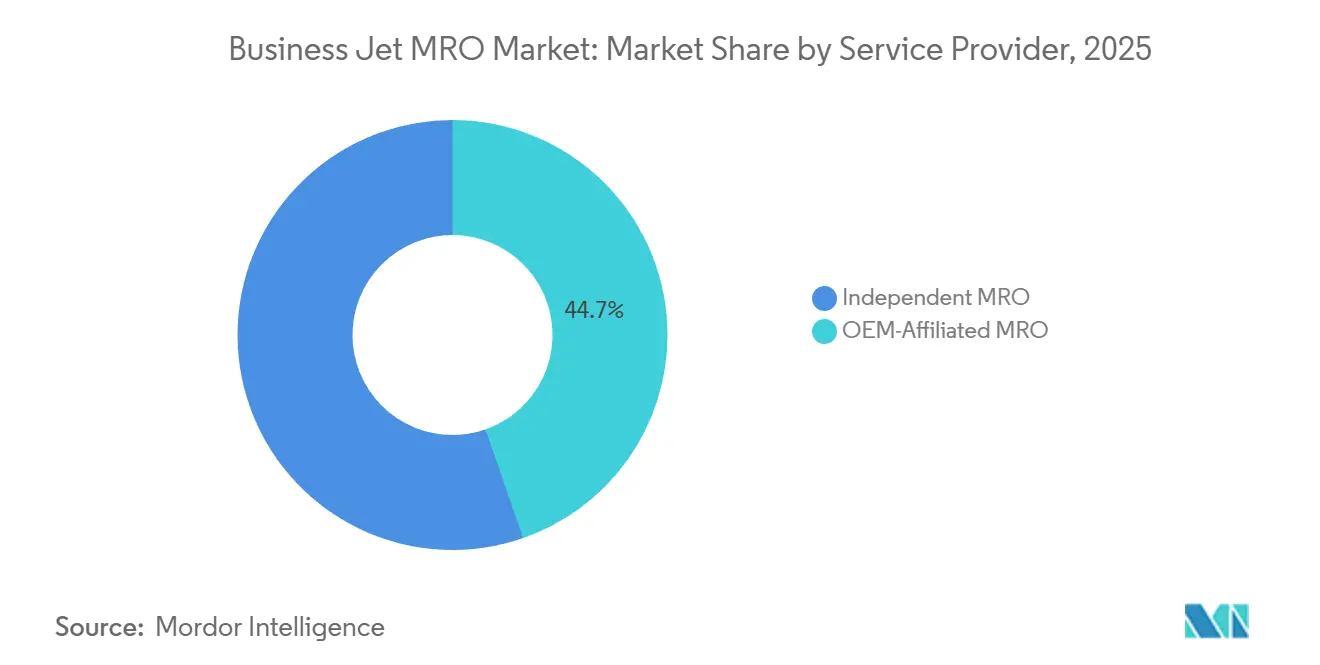

- By service provider, OEM-affiliated shops captured 44.67% of spending in 2025, while independent MROs are projected to grow at a 5.01% CAGR through 2031.

- By geography, North America accounted for 58.76% of the business jet MRO market size in 2025; the Asia-Pacific is forecast to grow at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Business Jet MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging global business jet fleet is increasing demand for heavy maintenance | +0.9% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Rising flight hours and growth in fractional operations are sustaining aircraft utilization | +0.7% | North America, Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Increasing complexity of engines and avionics is driving higher MRO expenditure | +0.6% | Global, with premium segments in North America and Middle East | Long term (≥ 4 years) |

| OEM delivery backlogs are extending the operational life of in-service aircraft | +0.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Growing demand for cabin connectivity retrofits is generating incremental MRO revenues | +0.3% | North America, Europe, Middle East | Medium term (2–4 years) |

| Special mission conversion of older business jets is creating niche maintenance demand | +0.2% | Middle East, Asia-Pacific, select North America operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Global Business Jet Fleet Increasing Demand for Heavy Maintenance

More than 8,000 in-service business jets have surpassed 15 years of operation, and the average age of aircraft listed for resale reached 22 years in 2024. Reaching the 12- to 15-year mark necessitates significant airframe inspections, gear overhauls, and corrosion control measures, shifting capital allocation toward maintenance instead of replacement. OEM order backlogs stretching up to two years, coupled with elevated pre-owned inventory dominated by older airframes, are reinforcing this life-extension strategy. Regulatory oversight under FAA Part 91 K and EASA Part-M prevents operators from deferring mandatory intervals, locking in stable heavy-check demand. Shops equipped for legacy platforms such as the Gulfstream G-IV and Bombardier Challenger 600 series are therefore entering a multi-year upcycle.

Rising Flight Hours and Growth in Fractional Operations Sustaining Aircraft Utilization

Business aviation flight activity increased by 3% in 2025, with fractional fleets accounting for a disproportionate share. NetJets alone logged roughly 190,000 flight hours from March to May 2025, keeping utilization more than 10% above pre-2020 baselines. Fractional missions average 1.5- to 2.5-hour legs, which doubles cycle counts compared to owner-flown aircraft and accelerates component wear. Each 100-hour uptick translates into more than thousands of USD in additional spending on engine borescope inspections, brake replacements, and avionics health checks. Charter and fractional operators prioritize dispatch reliability, driving demand for 24-hour AOG support and rotable pools that independent shops monetize via inventory-backed service agreements. The trend is most pronounced in the light jet category, where lower acquisition costs align with the economics of shared ownership.

Increasing Complexity of Engines and Avionics Driving Higher MRO Expenditure

Next-generation turbofans, such as the Pratt & Whitney Canada PW800 and Rolls-Royce Pearl 15, employ advanced alloys and FADEC architectures that increase time-on-wing, yet require 150% more labor during overhauls.[1]Pratt & Whitney Canada, “PW800 Engine Family Technical Overview,” pwc.ca Specialized tooling investments often surpass USD 1 million per repair station, concentrating work in shops that can amortize capital outlays. Parallel avionics upgrades integrating synthetic vision, ADS-B Out, and datalink must meet FAA AC 120-76D and EASA CS-25 Amendment 27 cybersecurity rules.[2]Federal Aviation Administration, “AC 120-76D,” faa.gov Compliance timelines are driving operators to replace legacy flight management systems even when hulls remain structurally sound, channeling spend toward component-level expertise.

OEM Delivery Backlogs Extending Operational Life of In-Service Aircraft

Gulfstream delivered 136 jets in 2024, yet it maintained a backlog exceeding USD 55 billion by mid-2025, equating to 18- to 24-month lead times for its large cabin models. Similar queues at Bombardier, Embraer Executive Jets, and Textron Aviation are prompting operators to consider upgrade packages that extend the economic life by 10 to 15 years. Pre-owned Gulfstream G450 and Bombardier Global 5000 aircraft equipped with Starlink or Gogo 5G connectivity command price premiums, underscoring how aftermarket investments substitute for new deliveries and funnel revenue to the business jet MRO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled maintenance technicians is increasing costs and turnaround times | -0.6% | North America, Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Persistent spare parts supply disruptions are extending maintenance lead times | -0.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Rising avionics certification and cybersecurity compliance costs are elevating MRO expenses | -0.3% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Expansion of OEM power-by-the-hour programs is limiting addressable opportunities for independent MROs | -0.5% | Global, most pronounced in North America and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Maintenance Technicians Increasing Costs and Turnaround Times

An aging technician workforce and insufficient training-pipeline throughput are elevating wage costs and stretching shop schedules. Entry-level AMT salaries approach more than thousands of USD, while turbine-rated specialists can command six-figure packages, yet demand still outpaces supply across North America and Europe. Turnaround times for complex engine visits have lengthened and occasionally breach 300 days, forcing operators to lease spares or accept extended downtime. Independent shops launched apprenticeship programs and partnerships with community colleges; however, producing a fully licensed technician can take up to two years, which delays relief.

Persistent Spare-Parts Supply Disruptions Extending Maintenance Lead Times

Semiconductor shortages and supplier consolidation have stretched avionics lead times, and specific flight-control components can require more than a year from order to delivery. OEMs prioritize new-production allocations, leaving aftermarket orders vulnerable to delays that can ground aircraft once strategic inventory buffers are depleted. FAA and EASA approval cycles for PMA substitutes add further lag, while export control paperwork on encrypted avionics modules can add weeks to cross-border shipments. Larger MROs are vertically integrating component repair to reduce exposure, but capital requirements limit widespread adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Component Repairs Outpace Engine Dominance

Engine MRO accounted for 56.58% of the business jet MRO market share in 2025, as turbofan overhauls are high-cost and recur every 3,500 to 5,000 flight hours. Component work is forecast to accelerate at a 4.84% CAGR, reflecting avionics obsolescence and the popularity of rotable pools that slash replacement costs by up to 70%.[3]Duncan Aviation, “Rotable Component Exchange Program,” duncanaviation.aero Landing-gear, hydraulic, and flight-control overhauls are converging as aging airframes enter their second maintenance cycle, while cabin refurbishments add incremental revenue as operators delay fleet renewal.

The business jet MRO market benefits from predictive-maintenance platforms, which focus spending on components with measurable deterioration, thereby concentrating revenue in shops that can integrate data analytics. Although engine programs remain the most significant contributor to the business jet MRO market size, power-by-the-hour contracts cap transactional growth, shifting incremental opportunity toward avionics upgrades required by evolving cybersecurity mandates.

By Body Type: Light Jets Accelerate as Fractional Models Expand

Large jets generated 42.65% of 2025 revenue, with ultra-long-range platforms posting USD 2 million - USD 4 million in annual per-aircraft MRO costs. Light and very light jets, however, are slated for a 4.51% CAGR through 2031, driven by fractional models whose aircraft log 800-1,200 hours per year, nearly double the utilization of owner-flown counterparts.

The business jet MRO market tied to light jet fleets will therefore expand faster than cabin-class peers, particularly as Part 135 rules impose more frequent inspections. Large jet growth remains constrained by acquisition economics, yet each aircraft sustains deeper maintenance spend, ensuring a stable revenue base. Mid-size jets exhibit steady but less dynamic expansion because corporate buyers balance range requirements against budget constraints, choosing proven models such as the Challenger 350 or Citation Latitude.

By Service Provider: Independents Gain Ground Through Digital Tools

OEM-affiliated networks held 44.67% of 2025 spending by bundling power-by-the-hour coverage with new-delivery warranties. Independent MROs are poised for 5.01% CAGR through 2031, leveraging multi-type capabilities and e-commerce parts portals to reduce aircraft-on-ground time by up to 40%.[4]StandardAero, “Augusta Campus Expansion Announcement,” standardaero.com

Within the business jet MRO market, independents expand market share by investing in diagnostic analytics, enlarging hangar footprints, and offering flexible scheduling that appeals to operators juggling tight mission windows. OEM shops still dominate warranty and proprietary data work scopes. Still, cost-focused customers increasingly shift out-of-warranty airframes to independent shops once the premium pricing outweighs the convenience of service.

Geography Analysis

North America captured 58.76% of the business jet MRO market size in 2025, supported by a fleet comprising 66% of the world's 24,000 business jets and an extensive network of FAA Part 145 stations. Gulfstream's Savannah expansion, which opened in 2024, adds capacity for 26 additional aircraft, underscoring the OEM's commitment to co-locating production and service. US shops face escalating labor costs driven by technician shortages, pressures that encourage investment in automation and digital work-order management, yet threaten smaller facilities lacking scale.

The Asia-Pacific is forecasted to lead the business jet MRO market at a 5.24% CAGR through 2031, as China's fleet is expected to increase by 41% to approximately 350 aircraft, and India is projected to add incremental units each year. ST Engineering's third Philippine hangar and Lufthansa Technik's planned Clark facility reflect aggressive infrastructure build-out, while bilateral airworthiness accords with Australia and Singapore streamline cross-border certifications. Skill-short training pipelines persist as a near-term bottleneck. Yet, demand for heavy checks, connectivity retrofits, and special-mission conversions continues to migrate toward the region as operators seek proximity and shorter ferry times.

Europe maintains steady demand anchored by the UK, Germany, and France, where Jet Aviation, SR Technics, and Lufthansa Technik service both regional and intercontinental fleets. EASA's unified regulatory framework underpins operator confidence, though Brexit-driven dual approvals add paperwork for UK-based shops. South America's activity is concentrated in Brazil around Embraer's service hubs, but macroeconomic volatility constrains capital announcements. The Middle East, benefiting from VIP completions and government ISR programs, offers high-margin projects for providers with security-cleared facilities. At the same time, Africa's contribution remains centered on South Africa's established cluster.

Competitive Landscape

The business jet MRO market exhibits moderate fragmentation, with no single provider controlling the majority of the worldwide revenue, and service-model differentiation outweighs pure scale. OEMs extend their reach downstream through programs such as Rolls-Royce CorporateCare, Pratt & Whitney Canada ESP, and GE OnPoint, collectively covering nearly 40% of the installed engine base. At the same time, independents counter with multi-type flexibility and data-driven predictive maintenance. Digital procurement has become a key differentiator. Private-equity activity remains robust, with a focus on stable aftermarket cash flows and platform roll-ups. StandardAero’s Augusta expansion in August 2025 enlarged large-cabin capacity by 60%, illustrating confidence that turnaround speed and technical depth can offset OEM bundling.

Blockchain pilots for parts-provenance tracking aim to mitigate counterfeit risks, but widespread adoption awaits the establishment of consensus data standards. Regulatory mandates requiring cybersecurity assessments for avionics under FAA AC 120-76D are raising barriers to entry; shops lacking certification expertise risk losing market share to providers with dedicated regulatory affairs teams.

White-space opportunity clusters in Asia-Pacific, where infrastructure is scaling faster than technician supply, and within special-mission conversions that command USD 2 million - USD 5 million per airframe. OEM-affiliated networks will likely retain dominance in warranty services; however, independent shops leveraging digital diagnostics, rapid parts fulfillment, and multi-type proficiency are well-positioned to gain share in out-of-warranty heavy checks and component work, thereby preserving a dynamic competitive equilibrium across the business jet MRO market.

Business Jet MRO Industry Leaders

Bombardier Inc.

General Dynamics Corporation

RTX Corporation

Lufthansa Technik AG

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: ITP Aero extended its MRO services contract with Pratt & Whitney Canada, an RTX business. The agreement covers the mid turbine frame (MTF) and low-pressure compressor (LPC) modules of the PW800 engine and is effective until 2028.

- May 2024: Jets MRO entered into a collaboration for complementary maintenance and avionics support services. Spirit Aeronautics boasts multiple Part 145 repair stations, focusing on avionics systems, upgrades, rotable parts, and engineering support.

Global Business Jet MRO Market Report Scope

Maintenance, repair, and overhaul (MRO) encompasses all activities involving the upkeep, inspection, repair, and enhancement of aircraft and their components. This study focuses explicitly on MRO services within the business jet industry.

The business jet MRO market is analyzed based on MRO type, body type, service provider, and geography. By MRO type, the market is segmented into engine MRO, component MRO, interior MRO, airframe MRO, and field maintenance. By body type, the market is segmented into large jets, mid-size jet, and light/very light jet. By service provider, the market is segmented into OEM-affiliated MRO and independent MRO. Furthermore, the report provides market sizes and forecasts for the business jet MRO market in key countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Engine MRO |

| Component MRO |

| Interior MRO |

| Airframe MRO |

| Field Maintenance |

| Large Jets |

| Mid-Size Jet |

| Light/Very Light Jet |

| OEM-Affiliated MRO |

| Independent MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By MRO Type | Engine MRO | ||

| Component MRO | |||

| Interior MRO | |||

| Airframe MRO | |||

| Field Maintenance | |||

| By Body Type | Large Jets | ||

| Mid-Size Jet | |||

| Light/Very Light Jet | |||

| By Service Provider | OEM-Affiliated MRO | ||

| Independent MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the business jet MRO market in 2031?

The business jet MRO market size is expected to grow from USD 30.12 billion in 2025 to USD 31.09 billion in 2026 and is forecasted to reach USD 36.39 billion by 2031 at a 3.20% CAGR through 2031.

Which service category is growing fastest within Business Jet MRO?

Component MRO is projected to record the highest growth, advancing at a 4.84% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region for business-jet maintenance?

Rising fleets in China and India, combined with new regional hangar capacity and bilateral certification agreements, propel Asia-Pacific to a 5.24% CAGR through 2031.

How are connectivity retrofits influencing maintenance demand?

Roughly 40% of jets still lack high-speed internet, and installations costing USD 150,000 – USD 300,000 per aircraft are generating a USD 1.2 billion retrofit opportunity over five years.

What competitive strategies are independents using to win market share?

Independents leverage multi-type capability, e-commerce parts platforms, and predictive diagnostics to cut aircraft-on-ground time and undercut OEM pricing on out-of-warranty work.

Page last updated on: