Polyurethane (PU) Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.18 Million |

| Market Size (2031) | USD 31.54 Million |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

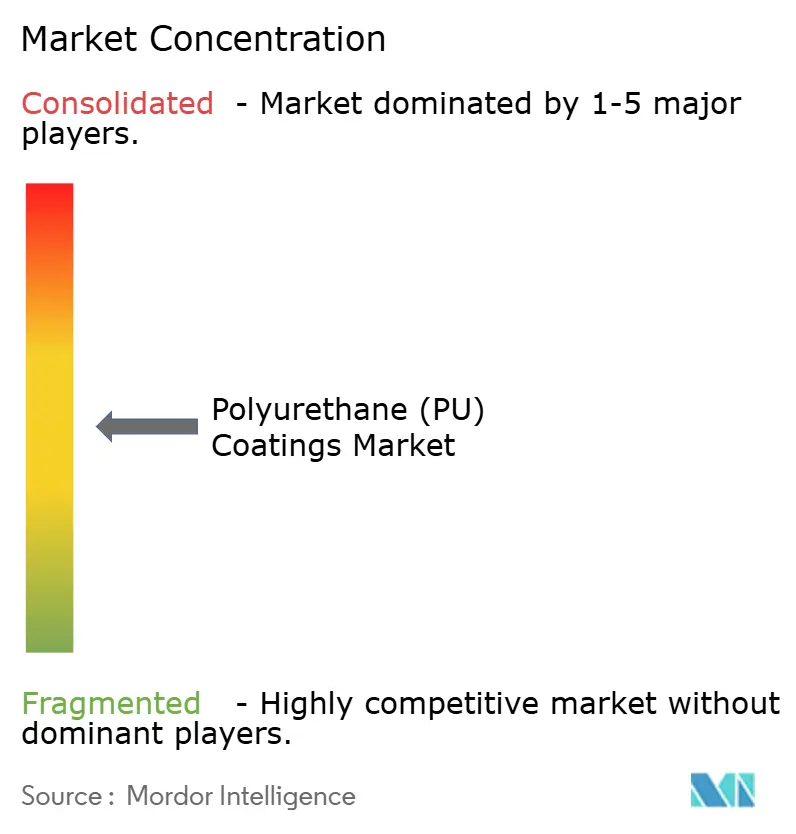

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurethane (PU) Coatings Market Analysis by Mordor Intelligence

Polyurethane Coatings market size in 2026 is estimated at USD 25.18 million, growing from 2025 value of USD 24.08 million with 2031 projections showing USD 31.54 million, growing at 4.58% CAGR over 2026-2031. Rapid innovation in waterborne dispersions, nano-enabled self-healing chemistries, and circular economy raw materials is reshaping competitive priorities. Demand accelerates where high durability, flexible adhesion, and low-VOC compliance intersect, particularly in the automotive, construction, and industrial flooring sectors. Large OEMs are enforcing sustainability protocols that favor bio-based feedstocks and isocyanate-free curing, while governments tighten emissions limits on solvent systems. Midsize formulators unable to finance broad reformulation pipelines are becoming attractive acquisition targets for global suppliers that can integrate R&D, raw materials, and regional distribution.

Key Report Takeaways

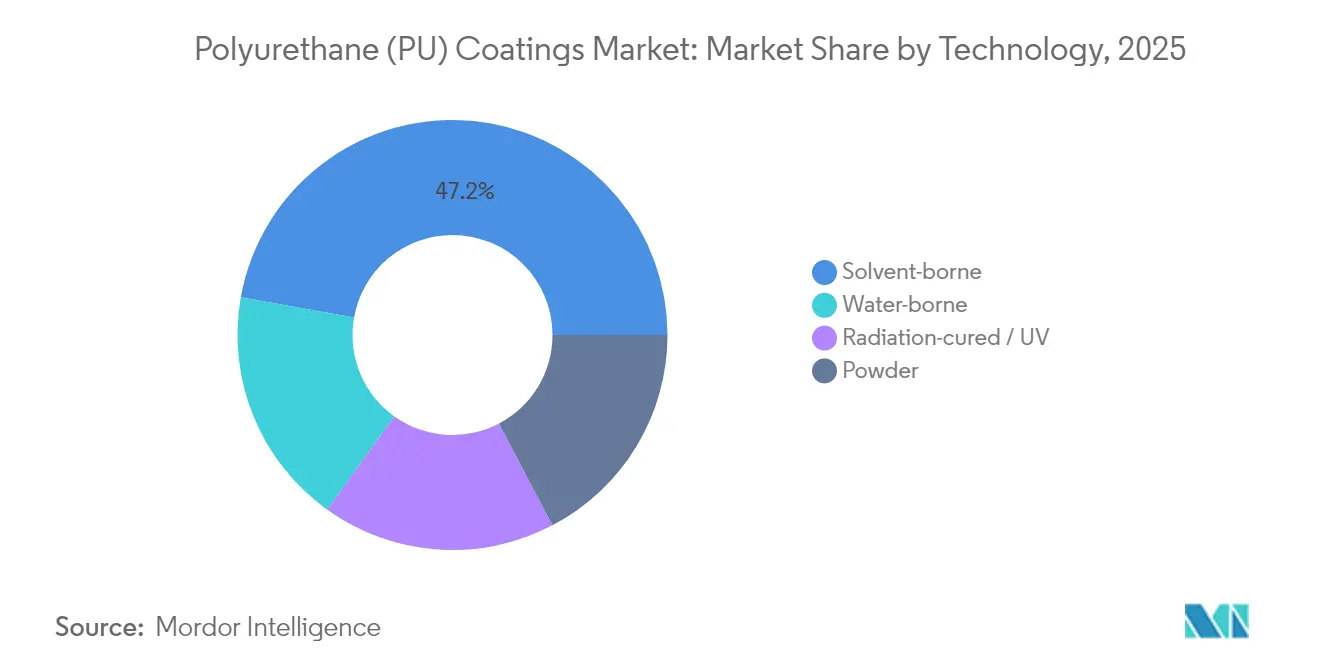

- By technology, solvent-borne coatings led the polyurethane coatings market with 47.20% of the market share in 2025. Water-borne technology is projected to grow at a 6.67% CAGR through 2031, the fastest among all technologies.

- By end-user, automotive applications accounted for 33.60% of the polyurethane coatings market size in 2025 and are expected to expand at a 4.75% CAGR during the forecast period (2026-2031).

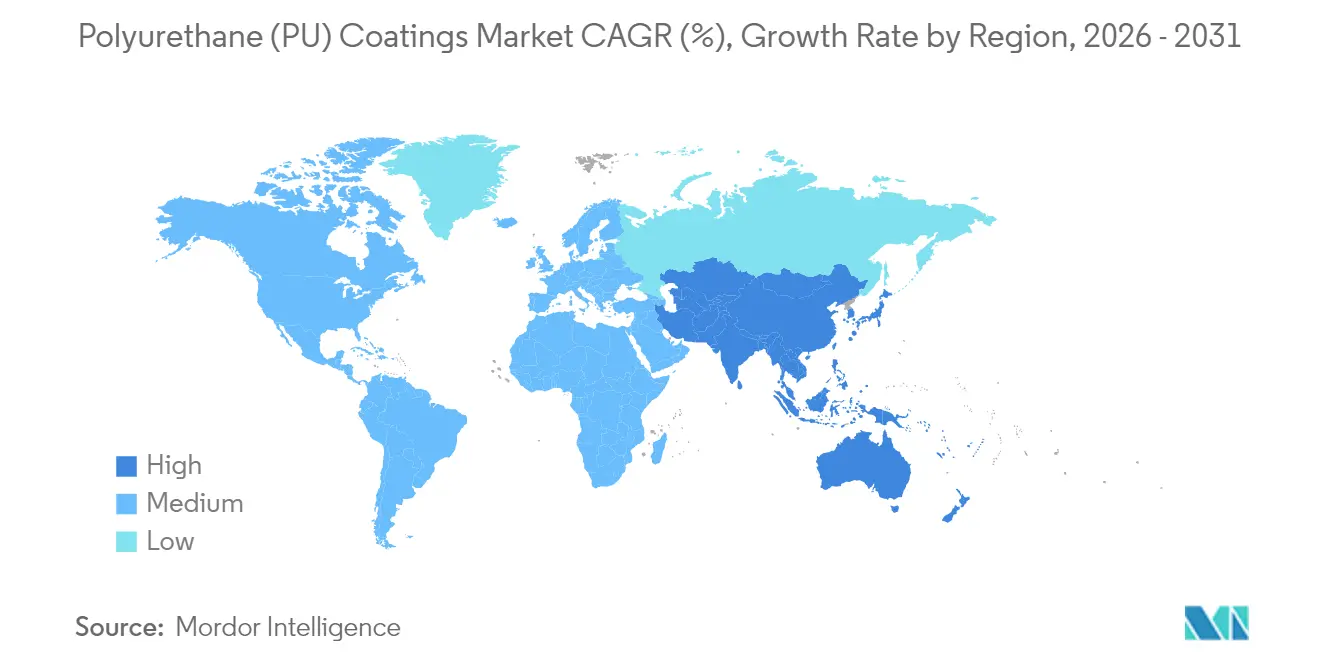

- By region, the Asia-Pacific commanded 42.75% of the polyurethane coatings market size in 2025 and is projected to advance at a 5.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Polyurethane (PU) Coatings Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction reboot in post-pandemic infrastructure stimulus | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Automotive OEM shift to lightweight composites needing high-flex PU top-coats | +0.9% | Global, led by Asia-Pacific automotive hubs | Short term (≤ 2 years) |

| Regulatory pivot to low-VOC water-borne and high-solids systems | +0.8% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| E-commerce logistics boom raising demand for industrial floor PU coatings | +0.6% | Global, with early gains in North America, China, Germany | Short term (≤ 2 years) |

| Emergence of nano-enabled self-healing PU coatings extending repaint cycles | +0.4% | North America & EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Reboot in Post-Pandemic Infrastructure Stimulus

Global infrastructure packages are unlocking steady orders for protective polyurethane finishes that endure harsh weather and chemical exposure. The United States Infrastructure Investment and Jobs Act, combined with large provincial projects in China, keeps architectural and civil engineering demand elevated. The sector also pivots toward green-building certifications, pushing architects to specify low-emission polyurethane dispersion products. Asia-Pacific contributes the highest volume, while North America and Europe emphasize premium resilience and rapid-cure performance. Modular construction growth favors factory-applied systems that reduce onsite labor. Longer project pipelines create predictable demand for suppliers, which can guarantee an uninterrupted supply.

Automotive OEM Shift to Lightweight Composites Needing High-Flex Top-Coats

Electrification targets and fuel-efficiency rules force OEMs to replace metal with carbon-fiber and glass-fiber composites that flex under dynamic loads. Conventional coatings crack or delaminate on these substrates, so manufacturers turn to elastomeric polyurethane chemistries with high elongation and chip resistance. Japanese and South Korean automakers have already updated internal paint standards, and US and European brands are aligning specification sheets. Sensor-laden body panels for autonomous vehicles introduce electromagnetic shielding requirements that high-solids polyurethane formulas can effectively address. Suppliers with in-house application-equipment labs gain an edge by co-developing spray parameters for new body architectures.

Regulatory Pivot to Low-VOC Water-Borne and High-Solids Systems

The US EPA, Environment and Climate Change Canada, and EU member states each introduced stricter VOC ceilings in industrial and architectural categories, rendering many solvent-borne grades obsolete. Simultaneously, REACH is tightening limits on certain di-isocyanates. Producers are investing in polyurethane dispersions and novel cross-linkers to replicate the solvent-borne gloss, hardness, and outdoor durability of traditional coatings. Early movers benefit from easier approval at OEM plants, faster green-building certification, and improved worker safety profiles. Compliance costs accelerate consolidation because smaller firms often lack both capital and expertise for wholesale reformulation.

E-Commerce Logistics Boom Raising Demand for Industrial Floor Coatings

The global warehouse footprint expanded sharply as Amazon, Alibaba, JD.com, and others automated fulfillment centers that operate around the clock. Forklifts, robots, and automated guided vehicles impose unique abrasion and chemical spills that conventional epoxy floors fail to resist. High-solids polyurethane coatings, applied in multilayer systems, combine elasticity with superior chemical tolerance, cutting downtime and repair budgets[1]“Warehouse Floor Resilience Study,” Paint & Coatings Industry Magazine, pcimag.com. Operators also require faster return-to-service cures to minimize lost throughput, so formulators develop rapid-cure aliphatic systems. Low-odor water-borne products further support indoor-air-quality objectives mandated by corporate ESG policies.

Restraints Impact Analysis of Polyurethane (PU) Coatings Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate and polyol feedstock prices | -1.10% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Tightening worker-safety rules on di-isocyanates | -0.70% | North America & EU, expanding globally | Medium term (2-4 years) |

| Carbon-border tariffs raising import costs of precursors | -0.50% | EU core, potential expansion to North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate and Polyol Feedstock Prices

Rigid and flexible MDI/TDI chains remain tied to crude-oil swings and planned or unplanned outages at a handful of global reactors. LyondellBasell’s annual report flagged thin spreads in 2024, and its refinery exit highlights the risk profile associated with oil-derived inputs. New capacity in Yeosu from Kumho Mitsui provides relief but cannot fully insulate buyers from force-majeure events. Larger formulators hedge their risks via multi-year contracts or backward integration, whereas many niche producers lack these options, forcing them to pass through prices or experience margin erosion. Specialty grades, which contain higher proportions of performance additives, are the most affected by the most profound cost spikes.

Tightening Worker-Safety Rules on Di-Isocyanates

OSHA and EU regulators are lowering workplace exposure limits and mandating additional medical surveillance. Lines must invest in ventilation upgrades, training, and personal protective gear that raise operating expenses. Smaller applicators struggle with compliance documentation, prompting some to exit the segment. Research on isocyanate-free polyurethane is accelerating, although present formulations trade off hardness or weatherability compared to conventional chemistry. Global suppliers with robust EHS departments offer audit services and application guidance, transforming compliance challenges into a customer-retention advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Polyurethane (PU) Coatings Market Segment Analysis

By Technology:

Water-Borne Systems Drive InnovationSolvent-borne formulations retained 47.20% of the polyurethane coatings market share in 2025 owing to legacy installations, extensive product catalogs, and familiarity with OEM lines. Water-borne alternatives, advancing at a 6.67% CAGR, receive investment from automotive, electronics, and wood-furniture plants seeking to reduce VOC emissions without compromising gloss. Powder coatings are ideal for areas where electrostatic lines are already installed, leveraging near-zero waste and low-energy curing. UV-curing segments carve out niches in electronics and automotive clear-outs where throughput speed offsets equipment costs.

Water-borne dispersions are increasingly comparable to solvent systems in terms of corrosion resistance after the adoption of self-cross-linking polyurethane backbones. Covestro commissioned a dispersion line in Shanghai that doubles its Asian capacity, lowering freight charges and shortening lead times. Research teams are also blending polycarbonate diols to enhance hydrolysis resistance, opening doors to marine applications previously dominated by solvent systems. Hybrid chemistries that integrate silicone or fluoropolymer segments offer stain resistance for premium kitchen cabinets and smartphone casings. The segment benefits from ISO 14001 incentives at customer factories, which weigh entire plant emissions rather than single product metrics.

By End-User Industry:

Automotive Leadership Drives InnovationThe automotive segment retained a 33.60% share of the polyurethane coatings market size in 2025. Electric-vehicle platforms require flexible protection for plastic and composite underbodies, reinforcing the segment’s lead at 4.75% CAGR. Aerospace and marine markets rely on aliphatic polyurethane topcoats for UV permanence, though volume remains lower. Construction consumes higher tonnage but at a lower value per unit, especially in roof and wall panels. The electronics sector grows quickly from a smaller base because camera modules, wearable devices, and 5G boards need thin dielectric coatings.

Automotive R&D teams collaborate with coating vendors on inline quality monitoring and smart factory requirements. High-speed automatic spray robots demand rheology profiles that minimize overspray while preserving edge retention. Polyurethane dispersions meet this need by allowing for lower viscosity without the need for extra solvent. Battery makers request fire-retardant intumescent polyurethane layers that Huntsman recently commercialized under the POLYRESYST EV5005 brand. The auto industry’s tight validation cycle fosters sticky vendor relationships, granting first movers multi-year supply contracts.

Geography Analysis

APAC Polyurethane (PU) Coatings Market

The Asia-Pacific region controlled 42.75% of the polyurethane coatings market in 2025, driven by automotive assembly, consumer electronics exports, and accelerated infrastructure programs. Regional demand will climb at a 5.36% CAGR through 2031, outpacing every other territory. China’s CO2-based polyol project by Changhua Chemical reduces carbon intensity and secures local feedstock. Vietnam’s Pearl Group has added a fifth system house that supplies flexible batch sizes to Southeast Asian plants, improving delivery times and mitigating currency risks. Japanese OEMs maintain R&D leadership in water-borne chemistry, and South Korea’s MDI expansion offers domestic paint makers stable supply at competitive cost.

North America Polyurethane (PU) Coatings Market

North America represents a mature yet lucrative market, where industrial floor projects and specialty aerospace coatings help offset slower volume growth. Major federal-state infrastructure packages sustain bridge and highway repaint cycles. Low-VOC mandates shepherd investment into dispersion and 2K high-solids chemistries, providing higher average selling prices per liter.

Central and Eastern Europe Polyurethane (PU) Coatings Market

Europe anchors regulatory frameworks that shape global formulation norms. REACH phase-outs of certain di-isocyanates force proactive reformulation. The MOL-thyssenkrupp polyol unit in Hungary improves regional input security and shortens supply lines for Central European OEMs. Eastern European automotive clusters rely on this plant to hedge against maritime freight volatility.

LATAM and MEA Polyurethane (PU) Coatings Market

Latin America, the Middle East, and Africa together represent a long-run upswing where infrastructure, mining, and oil & gas facilities demand durable, chemical-resistant coatings. Local producers often lack advanced R&D, so international suppliers partner through licensing or joint ventures. Smaller volumes and fluctuating currencies make modular batch plants advantageous, and large global players weigh selective capital deployment.

Regulatory Landscape

Polyurethane (PU) coatings compliance is being shaped by parallel tightening of VOC and chemical-safety frameworks, pushing formulation and label requirements across solvent-borne to water-borne and high-solids systems. In the United States, the EPA finalized amendments to the National Volatile Organic Compound Emission Standards for Aerosol Coatings (40 CFR Part 59 Subpart E) on January 17, 2025, reinforcing the need for formulation and label compliance in aerosolized PU coating products, while federal VOC standards for architectural coatings under 40 CFR Part 59 Subpart D remained in force as of March 2026.

In Europe, REACH continues to be a central driver for raw-material selection and workplace controls. Annex XVII Entry 74 requires mandatory training for industrial and professional users of products containing more than 0.1% monomeric diisocyanates (in effect since August 2023), which increases the compliance burden for diisocyanate-containing PU systems and affects substitution toward lower-free-monomer, prepolymer-based, or alternative curing approaches. ECHA updates to the SVHC Candidate List (253 entries by April 2026) add ongoing screening pressure on additives and intermediates used across PU coating formulations.

Value Chain Analysis

The polyurethane (PU) coatings value chain starts with petrochemical and bio-based feedstocks routed into isocyanates (MDI/TDI), polyols (polyether and polyester), chain extenders/crosslinkers, solvents (where used), and performance additives, then moves into resin synthesis (PU dispersions, 2K binders, prepolymers), formulation, application, and end-market installation across automotive, construction, industrial flooring, electronics, wood, and other segments. Vertical integration at large producers (notably across isocyanates, polyols, and formulated systems) is a key lever for cost and supply control, while mid-tier formulators rely more on merchant raw materials and distributors for reach and technical service.

Recent supply-side actions and policy shifts point to where constraints and advantages sit in the chain. BASF Coatings expanded polyester and polyurethane resin capacity at its Caojing, Shanghai site to 18,800 metric tons per year (March 2025), which supports closer-to-customer supply for Asia-Pacific manufacturing hubs. Upstream, China canceled the 13% VAT export rebate on polyether polyols in April 2026, changing export economics for a key PU input and prompting buyers to reassess sourcing and inventory strategies. Concentrated isocyanate production on the US Gulf Coast also creates seasonal continuity risk during hurricane season (starting June 1), reinforcing the value of dual sourcing, regional warehousing, and formulation flexibility for PU coating producers and applicators.

Competitive Landscape

The Polyurethane (PU) Coatings market is moderately fragmented. Global chemical majors, including BASF, Sherwin-Williams, PPG, AkzoNobel, and Covestro, dominate commodity volumes and leverage backward integration in MDI, TDI, and polyols. Mid-tier players focus on niche applications such as medical devices, optical films, or water pipeline linings. M&A momentum is likely, as solvent-centric formulators seek water-borne technology and broader sales reach. Private equity funds target regional distributors that offer last-mile tinting, repackaging, and technical service. Lines blur between raw-material company and finished-coating supplier as vertical integration appeals to large clients seeking single-invoice solutions.

Polyurethane (PU) Coatings Industry Leaders

Akzo Nobel N.V.

The Sherwin-Williams Company

PPG Industries, Inc.

Axalta Coating Systems

BASF

- *Disclaimer: Major Players sorted in no particular order

Polyurethane (PU) Coatings Market Companies Covered in this Report

- Akzo Nobel N.V.

- Asian Paints

- Axalta Coating Systems

- BASF

- Evonik Industries AG

- Hempel A/S

- IVM Chemicals SRL

- Jotun

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings

- Polycoat Products

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

Market Opportunities and Future Outlook

Opportunity is expanding where sustainability requirements and OEM qualification processes favor reformulated PU systems that cut VOC emissions and reduce product carbon footprint without sacrificing durability. BASF introduced certified biomass-balanced additives for architectural coatings (Dispex AA 4145 MB, Rheovis PU 1333 MB, Rheovis HS 1169 MB) in July 2026, giving formulators a tangible path to address customer-facing footprint documentation while maintaining performance in water-borne and hybrid systems. At the same time, tighter worker-safety rules around diisocyanates and REACH training requirements create room for low-free-monomer systems, alternative crosslinkers, and non-isocyanate polyurethane (NIPU) research directions, especially in indoor applications where odor and emissions constraints are most visible.

Supply reconfiguration and capacity additions in isocyanates and derivatives are also supporting new sourcing and localization strategies for coating producers serving automotive and industrial markets. Covestro expanded its HDI-derivatives footprint by acquiring former Vencorex production sites in Rayong, Thailand and Freeport, Texas (July 2026), strengthening regional access to aliphatic building blocks used in high-weatherability PU coatings. It also announced plans for a new MDI facility in Shanghai, China with 660,000 metric tons per year of capacity and launched a feasibility study for a similar plant in the UAE (July 2026), reflecting a shift toward Asia and Middle East supply bases that can shorten lead times and reduce exposure to inter-regional freight volatility. On the downstream side, industrial flooring and logistics facilities continue to reward rapid-return-to-service, abrasion-resistant PU systems, while OEM-driven adoption in automotive topcoats supports ongoing co-development of application parameters and validated coating stacks for lightweight composite substrates.

Recent Industry Developments in Polyurethane (PU) Coatings Market

- July 2026: Covestro expanded its coatings and adhesives feedstock footprint by completing the acquisition of two former Vencorex production sites for hexamethylene diisocyanate (HDI) derivatives in Rayong, Thailand and Freeport, Texas. This acquisition increases access to aliphatic isocyanate derivatives used in high-durability polyurethane coatings and improves regional supply options for formulators serving industrial and OEM customers.

- August 2025: Sherwin-Williams Protective and Marine launched Acrolon 680, a single-coat, high-solids direct-to-metal polyurethane coating for industrial and marine applications. By reducing coat count and surface-prep complexity versus multi-coat systems, the product targets faster project cycles and supports compliance-driven shifts toward lower-VOC, higher-solids technologies.

- November 2024: Sherwin-Williams Industrial Wood introduced a new crosslinker positioned for industrial wood coating systems, supporting performance upgrades in factory-applied finishing lines. The development aligns with broader customer requirements for low-emission formulations and improved durability in wood and furniture applications where polyurethane chemistry is widely used.

Polyurethane (PU) Coatings Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the polyurethane coatings market covers polyurethane based coatings used to protect and decorate surfaces in industrial and architectural settings. The market value is counted as coating product revenue sold into end uses such as transportation, construction, electronics, and wood finishes.

Scope exclusions: We exclude polyurethane used mainly as foams, elastomers, or cast systems where surface coating is not the primary function. We also exclude niche restoration formulations that do not meaningfully add to total revenue.

Segments Covered in This Report

- By Technology

- Powder

- Solvent-borne

- Water-borne

- Radiation-cured / UV

- By End-user Industry

- Automotive

- Transportation

- Construction

- Electrical and Electronics

- Wood and Furniture

- Other End-user Industries

- By Geography

- Asia–Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- South Africa

- Rest of Middle-East and Africa

- Asia–Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building the demand and supply context for PU coatings, then aligning it to coatings technologies used in real applications. Public sources anchored the model, including US Census construction spending, Eurostat industrial production series, UN Comtrade trade flows for relevant coating and resin categories, and environmental agency documents that set VOC and emissions rules affecting solvent-borne and water-borne adoption. Technical papers and patents were also reviewed to see where UV cured and powder technologies are realistically applied.

To keep the market map current, we used company filings, investor presentations, and press releases that describe capacity additions, product launches, and exposure to end markets. In parallel, we referenced paid subscriptions for company financials and intelligence, patent analytics, and shipment-level import-export signals where they helped cross-check volumes and the direction of price movement. These desk sources are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys focused on talking with stakeholders across the PU coatings value chain so assumptions could be tested in plain terms. This included formulators, raw material intermediaries, distributors, and large end users that specify coatings for durability and compliance. We collected inputs across Asia, Europe, and the Americas to confirm the technology mix shift toward water-borne, solvent-borne, powder, and UV-cured systems. The same inputs were used to pressure-test application-level average selling price ranges before the final totals were signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 16% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

The market was sized using a mix of top-down and bottom-up logic, where macro coatings demand signals and technology penetration were first reconstructed by region, then checked using selective supplier and channel approximations. In practice, we built a demand pool from end use activity and coatings intensity, then applied realistic splits across solvent-borne, water-borne, powder, and UV-cured technologies.

Key inputs in the model included indicators such as construction output and renovation activity, automotive and broader transportation production trends, industrial output for machinery and general manufacturing, and trade movement for coating and resin related categories. Regulatory pressure on VOC was also treated as a driver that shifts the mix toward water-borne and powder systems. Pricing was handled through application-level ASP ranges (and their expected change) rather than a single blended price, since automotive OEM coatings, wood finishes, and industrial maintenance coatings can move differently.

For forecasting, we used scenario analysis with a base case that reflects the most common view from industry contacts on demand normalization and technology substitution. When a bottom-up check was incomplete for a specific country or niche end use, we filled gaps using proxy indicators such as import dependence, industrial output, and neighboring market adoption patterns. Totals were adjusted only after the logic held at the regional roll-up level.

Data Validation & Update Cycle

Validation was done through several passes where model outputs were compared with independent signals, then reviewed for unusual changes in volume, pricing, or technology mix. If a variance appeared too large, we revisited the underlying assumption, checked the desk evidence again, and re-contacted selected respondents to confirm what changed and why.

Before sign off, market totals and growth rates were reviewed by another analyst to ensure the calculations could be followed and repeated. The report is refreshed annually, and interim updates are triggered when there are material events such as major capacity moves, regulatory shifts, or sharp raw material price swings. Just before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Polyurethane Coatings Market Size Measured Against Other Published Estimates

Published market values for polyurethane coatings often do not match because each publisher draws the boundary differently on what counts as a coating, which pricing basis is used, and when currency and inflation adjustments are applied. Differences also show up when one estimate leans more on end use demand signals, while another leans more on supplier side revenue mapping.

The spread is also influenced by refresh timing and price logic, since quarterly raw material movements and a mid-year FX rate versus a full-year average can shift USD totals even if volumes are similar. When ASPs are updated by application and then cross-checked against trade and end market indicators during annual refresh cycles, the resulting number stays closer to the real demand pool, which is the approach applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.03 B (2026) | |

| Global Consultancy A | USD 20.53 B (2024) | Uses a much larger value base that likely includes broader polyurethane related coatings and adjacent chemistries, and it anchors sizing on a different base year with its own pricing basket and currency timing. |

| Industry Publisher B | USD 22.10 B (2025) | Applies a longer horizon forecast and may count additional polyurethane systems beyond conventional coatings, which can expand the scope and lift the blended ASP assumptions used for the base year. |

Across the three figures, the main takeaway is that scope boundaries and how pricing is refreshed explain most of the gap, not a single right or wrong demand signal. By keeping the demand pool tied to clear end uses, updating application level ASPs on a defined cadence, and running simple cross checks before finalizing totals, the estimate remains easier to reconcile and repeat over time.

Key Questions Answered in the Report

What is the current size of the global polyurethane coatings space and how fast is it expanding?

It reached USD 25.18 million in 2026 and is projected to climb to USD 31.54 million by 2031, reflecting a 4.58% CAGR.

Which technology segment is growing fastest within polyurethane coatings?

Water-borne systems are advancing at 6.67% CAGR through 2031, outpacing all other technologies due to tightening VOC limits and OEM sustainability mandates.

Why are automotive producers prioritizing polyurethane top-coats for new vehicle platforms?

Lightweight composite body panels and electric-vehicle fire-protection requirements demand flexible, chip-resistant, and intumescent polyurethane chemistries that conventional coatings cannot match.

How much share does Asia-Pacific hold in polyurethane coatings and what drives its dominance?

Asia-Pacific commanded 42.75% share in 2025 and is growing at 5.36% CAGR, supported by automotive assembly, electronics exports, and large infrastructure programs across China, India, and Southeast Asia

What are the main raw-material risks facing polyurethane coaters?

Volatile MDI, TDI, and polyol prices—linked to crude-oil swings and concentrated production hubs—can cut margins by up to 1.1 percentage points on projected CAGR.

Page last updated on: