Polypropylene Absorbent Hygiene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

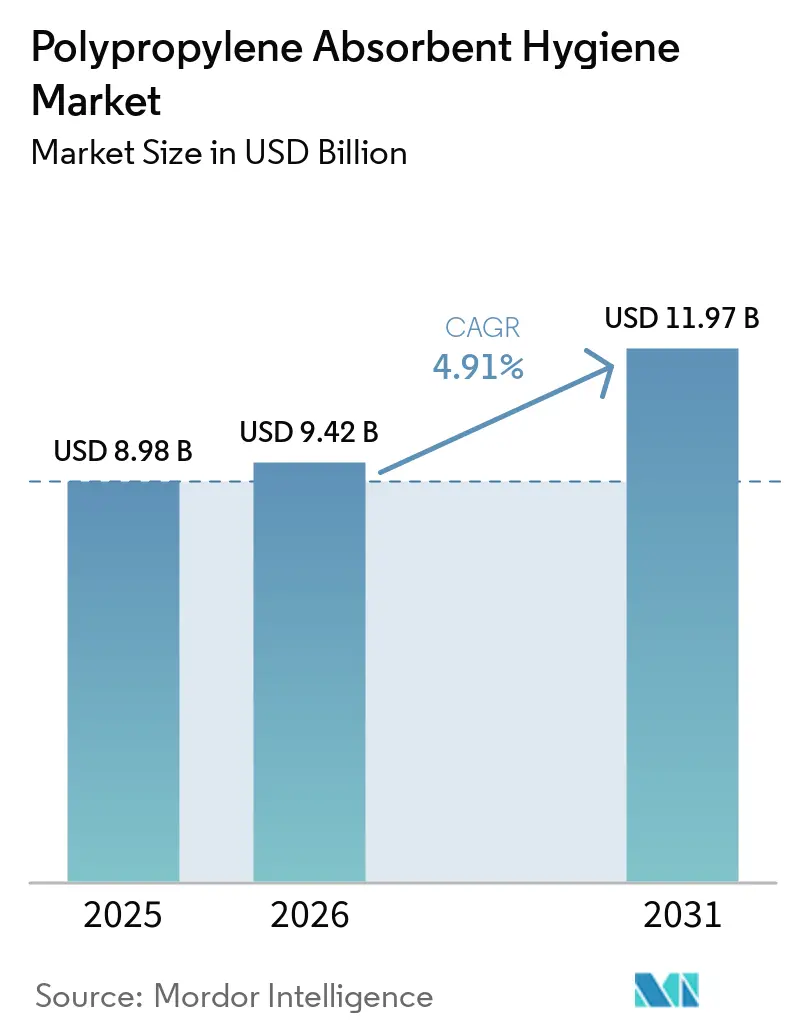

| Market Size (2026) | USD 9.42 Billion |

| Market Size (2031) | USD 11.97 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polypropylene Absorbent Hygiene Market Analysis by Mordor Intelligence

The Polypropylene Absorbent Hygiene Market size is expected to grow from USD 8.98 billion in 2025 to USD 9.42 billion in 2026 and is forecast to reach USD 11.97 billion by 2031 at 4.91% CAGR over 2026-2031. Brand owners are driving consistent headline growth by developing thinner cores with higher super-absorbent polymer (SAP) loadings, while premium spun-bond topsheets with sub-3-denier fibers are increasing per-unit resin demand. In 2026, Asian and African birth cohorts accounted for 85% of global births, providing a stable volume base for the polypropylene absorbent hygiene market, despite low diaper penetration in India and several African countries. Meanwhile, North American and European parents are opting for hypoallergenic, ultra-soft products, supporting demand for resin grades like ExxonMobil’s Exceed Flow PP3655E1, which enable finer and stronger fibers. The rise of e-commerce sales, retailer-brand expansions, and certified circular polypropylene launches are altering procurement strategies, while fluctuations in propylene prices are prompting manufacturers to mitigate feedstock risks through mass-balance or bio-based alternatives. These dynamics are creating a segmented market, where cost-efficient designs gain traction in emerging regions, while value-added features drive margins in developed economies.

Key Report Takeaways

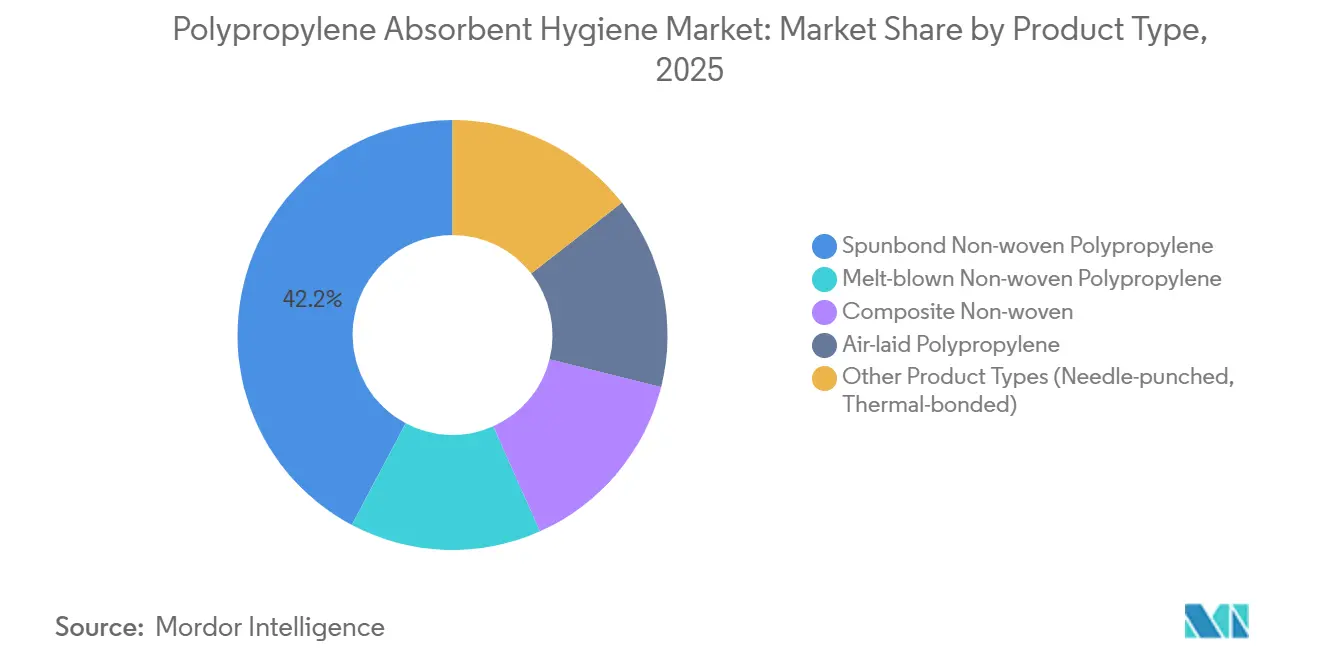

- By product category, spunbond non-woven polypropylene led with 42.24% revenue share in 2025; composite non-wovens are projected to advance at a 5.71% CAGR through 2031.

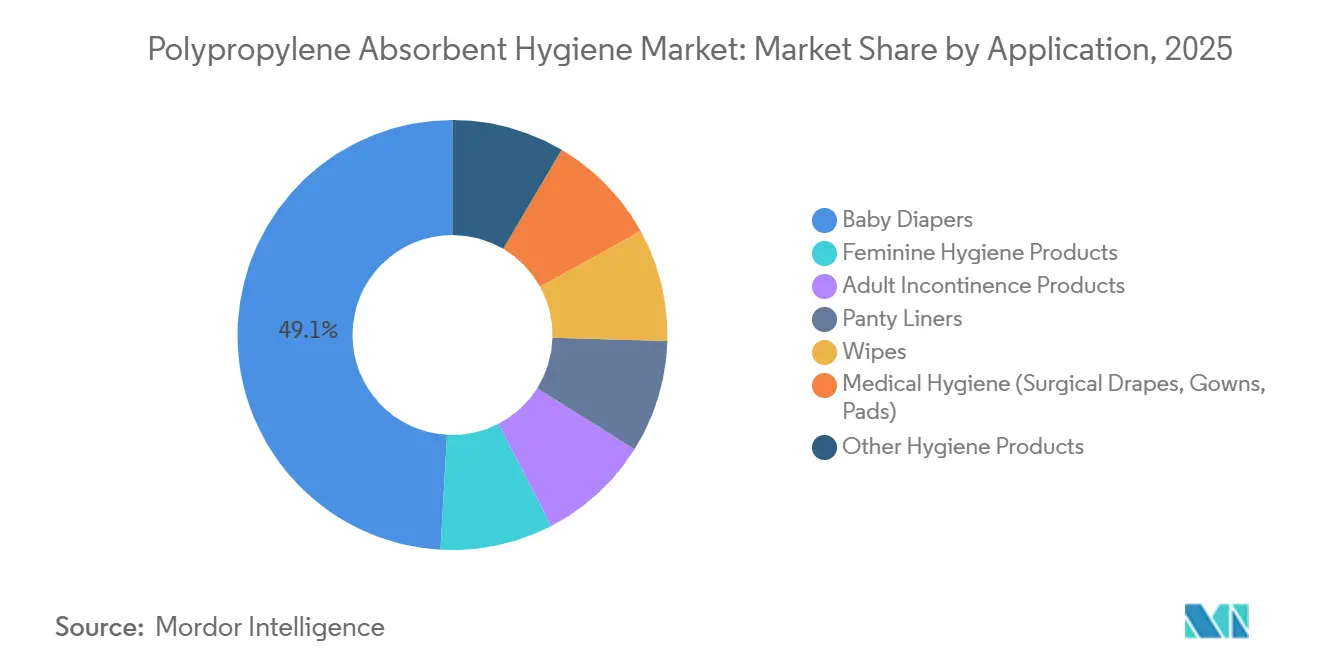

- By application, baby diapers accounted for 49.11% of the polypropylene absorbent hygiene market size in 2025 and are projected to advance at a 5.89% CAGR to 2031.

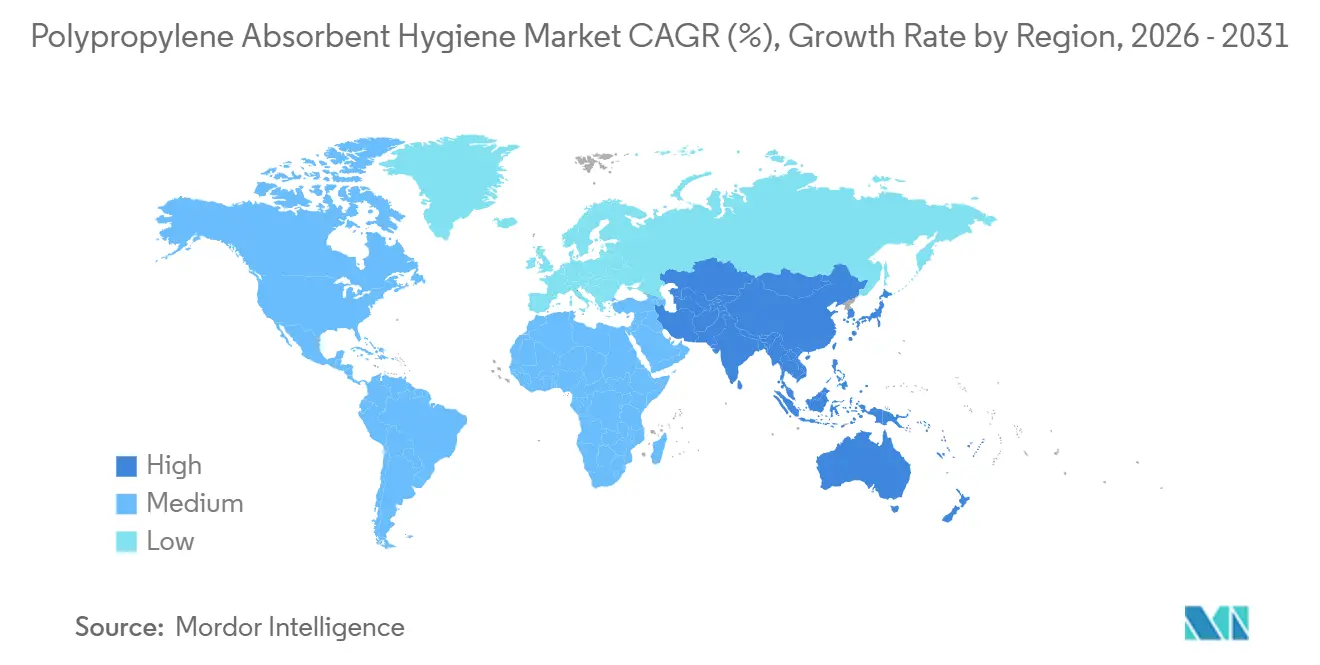

- By geography, Asia-Pacific held 40.15% of the polypropylene absorbent hygiene market size in 2025 and is set to expand at a 5.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polypropylene Absorbent Hygiene Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising birth rates in emerging Asia and Africa fuelling diaper uptake | +1.2% | Asia-Pacific (India, Southeast Asia), Sub-Saharan Africa | Long term (≥ 4 years) |

| Premiumization trend toward ultra-soft/hypoallergenic topsheets | +0.9% | North America, Europe, and premium segments in China | Medium term (2-4 years) |

| E-commerce-led private-label diaper scale-up | +0.7% | Global, with the strongest penetration in India, China, and North America | Medium term (2-4 years) |

| High-loft spun-bond PP replacing cotton and viscose webs | +0.6% | Global manufacturing hubs (China, India, North America) | Short term (≤ 2 years) |

| Closed-loop recycling credits for mono-material PP diaper designs | +0.5% | Europe (EU Single-Use Plastics Directive), North America (EPR schemes) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Birth Rates in Emerging Asia and Africa Fuelling Diaper Uptake

Demographic growth in Asia and Africa continues to sustain high demand for baby-care products, even in regions where diaper penetration remains below 10%, such as rural India and parts of West Africa[1]Ankita Balar Arya, “Asia and Africa to Account for 85% of Global Births in 2026,” MedIndia, medindia.net. Multinational companies are increasing production capacity to address these markets. For instance, Unicharm resumed operations at its third Indian plant in February 2025 to reduce lead times and logistics costs in price-sensitive areas. Local manufacturing also enables companies to offer pack sizes aligned with household cash-flow cycles, which is essential for expanding penetration beyond urban centers. Consequently, the polypropylene absorbent hygiene market benefits from volume growth rather than premiumization in these regions. Suppliers with regionally diversified propylene sourcing and advanced low-basis-weight spun-bond capabilities are positioned to gain market share.

Premiumization Trend Toward Ultra-Soft/Hypoallergenic Topsheets

In markets such as the United States, Western Europe, and affluent urban areas in China, parents are increasingly opting for fine-denier topsheets that are dermatologically tested and fragrance-free. Freudenberg’s fine-filament spun-bond line, launched in 2025, produces 2.5-3-denier polypropylene fibers that combine softness with high tear strength[2]Freudenberg Performance Materials, “Innovative Spunbond Nonwovens,” freudenberg-pm.com. These properties enable reductions in core thickness without compromising comfort, maintaining stable polymer usage per unit. E-commerce platforms prominently highlight hypoallergenic claims, encouraging higher spending among digitally active parents. As a result, the polypropylene absorbent hygiene market captures value not only through increased volumes but also by utilizing resin grades capable of producing finer, stronger fibers. Converters that provide documented skin-contact safety and secure third-party certifications gain a competitive edge both online and offline.

E-Commerce-Led Private-Label Diaper Scale-Up

Online marketplaces are increasingly offering subscription-based diaper bundles, reducing stock-outs and promoting bulk purchases, which accelerates private-label contract manufacturing. In India, e-commerce already accounts for approximately 25% of diaper sales, a figure expected to grow as quick-commerce platforms expand into smaller cities. In North America, retailers have broadened their private-label offerings, enabling suppliers like Ontex to achieve double-digit growth in baby-care volumes in 2025. This channel supports long production runs of cost-efficient stock-keeping units (SKUs), sustaining polypropylene demand even in regions with declining birth rates. However, pricing power is shifting toward e-retail algorithms and subscription-based incentives, prompting converters to secure multi-year resin supply agreements with indexed pricing to safeguard margins.

High-Loft Spun-Bond PP Replacing Cotton and Viscose Webs

Advancements in spun-melt technology have enabled the production of lofty, low-basis-weight webs that replicate the texture of carded natural fibers while being more cost-effective and efficient to produce. Avgol’s USD 100 million Reicofil line in North Carolina exemplifies this shift, offering multi-beam flexibility to laminate barrier and cushioning layers in a single process. Polypropylene is increasingly replacing cotton and viscose in acquisition layers, reducing exposure to fluctuations in agricultural commodity prices while increasing reliance on propylene supply. This substitution aligns with life-cycle assessments that show polypropylene’s lower water footprint compared to cellulosic fibers, particularly when recycling or energy recovery is considered. In the polypropylene absorbent hygiene market, expanded high-loft spun-bond capacity supports both premium diaper cores and cost-effective products requiring bulk without additional expense.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Propylene (C3) and ethylene (C2) feedstock price volatility | -0.8% | Global, with acute sensitivity in North America (PDH units) and Asia (naphtha crackers) | Short term (≤ 2 years) |

| Brand-owner pivot toward bio-based PLA/PHA non-wovens | -0.5% | Europe (sustainability mandates), North America (premium segments) | Medium term (2-4 years) |

| Cellulose-foam cores eliminating PP acquisition layers | -0.4% | Europe, North America, Japan (R&D-intensive markets with sustainability focus) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Propylene (C3) and Ethylene (C2) Feedstock Price Volatility

Polymer-grade propylene prices ranged between USD 0.30 and 0.60 per pound since mid-2023, influenced by supply constraints caused by winter storms and refinery turnarounds. These disruptions required converters operating under narrow retailer contracts to manage sudden increases in resin costs. U.S. refinery closures, such as LyondellBasell’s Houston facility, have removed nearly 200 kilotons (kt) of refinery-grade propylene from the market, contributing to price increases during periods of high heating demand. Ethylene prices have also shown significant volatility, driven by fluctuations in naphtha and crude oil prices, which have raised costs for bicomponent fibers used in diaper backsheets. This price variability affects gross margins and extends the payback period for new spun-bond production lines. While forward hedging and diversification into certified circular grades indexed to renewable feedstocks can help manage volatility, smaller converters often lack the scale to utilize these tools effectively.

Brand-Owner Pivot Toward Bio-Based PLA/PHA Non-Wovens

Regulatory requirements in the European Union and California are increasing the demand for compostable or recyclable diaper components, encouraging brands to explore PLA and PHA spun-bond materials as alternatives to polypropylene. CJ Biomaterials’ PHACT MA1350Q masterbatch, certified for home composting, is designed for diaper topsheets that decompose without requiring high-temperature facilities. Life-cycle analyses indicate that PLA pads reduce greenhouse gas impacts by 17 times compared to polyethylene alternatives, although concerns about land use and production costs remain. Additionally, processing PLA and PHA requires adjustments to equipment due to differences in processing windows compared to polypropylene. While polypropylene remains cost-competitive in the absorbent hygiene industry, the risk of long-term market share loss increases as retailers continue to test bio-based private label products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Composite Formulations Capture Performance Premiums

Spunbond polypropylene accounted for 42.24% of the projected 2025 revenue, primarily due to its application in topsheets and backsheets. Composite non-wovens are expected to achieve a 5.71% compound annual growth rate (CAGR). The polypropylene absorbent hygiene market size for composite webs is anticipated to grow steadily as converters laminate melt-blown webs and spunbond layers to optimize fluid handling and reduce basis weight. Advances in co-form technology enable the embedding of super-absorbent particles directly into melt-blown fibers, reducing adhesive usage and allowing for thinner cores. Composite designs increase polypropylene usage per square meter in premium diapers while lowering overall grammage, benefiting suppliers with precise basis-weight control capabilities.

In comparison, melt-blown polypropylene remains a niche material for filtration-focused hygiene films, while air-laid and needle-punched fabrics are used in specialty liners where loft is prioritized over tensile strength. Innovations in fine-filament technology, such as Freudenberg's spunbond webs with weights as low as 17 grams per square meter (gsm), meet mechanical performance requirements. Over the forecast period, composite structures are expected to enhance the polypropylene absorbent hygiene market share by enabling mono-material diaper designs that comply with circular-economy regulations in Europe.

By Application: Baby Diapers Extend Leadership Through Penetration and Premiumization

Baby diapers represented 49.11% of the projected 2025 market value and are expected to achieve a 5.89% CAGR, solidifying their dominant position. In India, pants-style diapers account for 90% of sales, driving the polypropylene absorbent hygiene market size for diapers beyond that of feminine hygiene products, despite demographic slowdowns in China. Procter & Gamble's ultra-thin core patents, featuring greater than or equal to 87% super-absorbent polymer (SAP) wrapped in polypropylene spun-melt, aim to reduce thickness to 0.5-3 millimeters (mm) while maintaining absorption capacity.

Adult incontinence and feminine hygiene collectively account for the majority of the remaining demand. The adult care segment benefits from aging populations and increased awareness of care needs, with Ontex deriving 46% of its group sales from this category, highlighting its growing importance. While wipes, panty liners, and medical drapes represent smaller individual segments, they collectively sustain baseline polypropylene demand due to their reliance on barrier properties that cotton or viscose cannot provide. Product differentiation in these segments increasingly depends on antimicrobial finishes and electret charging, encouraging converters to incorporate melt-blown inserts that enhance functionality without requiring significant retooling of production lines.

Geography Analysis

Asia-Pacific accounted for 40.15% of the 2025 revenue and is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.84% through 2031. India, Vietnam, and Indonesia are expected to drive volume growth due to increasing diaper penetration and the establishment of domestic manufacturing plants, which help avoid import duties. In contrast, China experienced a decline in diaper volumes in 2025 due to brand-trust issues and consumer trading-down. However, management teams at Unicharm and Kimberly-Clark anticipate a mid-single-digit recovery in local currency by 2026. Japanese demand remains stable, with a preference for premium products, supporting margins through the use of fine-denier topsheets.

North America holds a smaller market share but benefits from healthier margins. Retailer-brand partnerships enabled Ontex to achieve double-digit growth in baby-care volumes. Additionally, Avgol's new production line in North Carolina positions the company to supply high-quality composites within a single-day truck radius of major diaper plants. Certified circular polypropylene is gaining traction, driven by retailer mandates linked to voluntary recycled-content goals.

Europe experienced a decline in baby-care volumes due to record-low birth rates. However, this was partially offset by growth in premium adult incontinence pads and sustainability-focused tenders. The introduction of extended producer responsibility fees, set to begin in 2027, is already encouraging the development of mono-material diaper pilots. These initiatives could increase polypropylene demand while reducing reliance on polyethylene terephthalate (PET) films.

Latin America and the Middle East & Africa remain under-penetrated but present significant growth opportunities. Essity derives a substantial portion of its personal-care sales from Latin America, highlighting the region's importance despite currency risks. In Africa, governments are prioritizing local manufacturing to reduce import bills, leading to investments in regional spun-bond capacity, which supports domestic polypropylene consumption.

Competitive Landscape

The polypropylene absorbent hygiene market is moderately fragmented. Following the spin-off, Glatfelter acquired Berry Global’s Health, Hygiene, and Specialties unit, significantly increasing its production capacity in North America and Europe. Other key players in the integrated non-woven segment, such as Avgol, Fibertex, PFNonwovens, and Fitesa, compete for brand-owner contracts by focusing on basis-weight precision and access to circular-grade materials.

Major brand owners, including P&G, Kimberly-Clark, Unicharm, and Essity, utilize their bargaining power through multi-year volume commitments while relying on converters for material innovation. Patents related to ultra-thin cores, hypoallergenic finishes, and mono-material laminates highlight the ongoing competition for product differentiation. Meanwhile, smaller companies like Woosh and TU Wien’s gasification pilot address waste-management challenges by converting used diapers into chemical feedstocks. If these initiatives achieve economic scalability, they could reduce demand for virgin resin.

Strategic advantage in the polypropylene absorbent hygiene market now depends on obtaining International Sustainability and Carbon Certification (ISCC) PLUS mass-balance certifications and demonstrating cradle-to-cradle solutions to retailers. Companies without certified circular production lines risk being confined to commoditized tenders, whereas those investing in feedstock-recycling partnerships can command premium pricing. The industry rewards companies with balanced portfolios that cater to both cost-sensitive emerging markets and specification-driven mature markets.

Polypropylene Absorbent Hygiene Industry Leaders

Avgol Industries 1953 Ltd

Berry Global

KCWW

Fitesa S.A.

Freudenberg Performance Materials

Avgol Industries 1953 Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: BASF, Essity, and TU Wien (Technical University of Vienna) have launched a pilot project to convert used diapers into synthesis gas. This gas can be utilized in chemical production, including polypropylene for absorbent hygiene products, addressing tons of hygiene waste and advancing sustainable waste management practices.

- February 2025: Avgol has completed a USD 100 million Reicofil line in North Carolina, increasing high-loft, multi-beam spun-melt production capacity. This development supports the growing demand for polypropylene-based absorbent hygiene products, including diapers and adult care items, by enabling the production of advanced nonwoven materials.

Global Polypropylene Absorbent Hygiene Market Report Scope

Polypropylene absorbent hygiene refers to the use of thermoplastic, nonwoven polymer fibers to create soft, breathable, and liquid-wicking layers in disposable products such as baby diapers, sanitary pads, and adult incontinence products. It functions as a hydrophobic layer that keeps moisture away from the skin.

The polypropylene absorbent hygiene market is segmented by product type, application, and geography. By product type, the market is segmented into spunbond non-woven polypropylene, melt-blown non-woven polypropylene, composite non-woven, air-laid polypropylene, and other product types (needle-punched, thermal-bonded). By application, the market is segmented into baby diapers, feminine hygiene products, adult incontinence products, panty liners, wipes, medical hygiene (surgical drapes, gowns, pads), and other hygiene products. The report also covers the market size and forecasts for polypropylene absorbent hygiene in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Spunbond Non-woven Polypropylene |

| Melt-blown Non-woven Polypropylene |

| Composite Non-woven |

| Air-laid Polypropylene |

| Other Product Types (Needle-punched, Thermal-bonded) |

| Baby Diapers |

| Feminine Hygiene Products |

| Adult Incontinence Products |

| Panty Liners |

| Wipes |

| Medical Hygiene (Surgical Drapes, Gowns, Pads) |

| Other Hygiene Products |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Spunbond Non-woven Polypropylene | |

| Melt-blown Non-woven Polypropylene | ||

| Composite Non-woven | ||

| Air-laid Polypropylene | ||

| Other Product Types (Needle-punched, Thermal-bonded) | ||

| By Application | Baby Diapers | |

| Feminine Hygiene Products | ||

| Adult Incontinence Products | ||

| Panty Liners | ||

| Wipes | ||

| Medical Hygiene (Surgical Drapes, Gowns, Pads) | ||

| Other Hygiene Products | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Polypropylene Absorbent Hygiene Market?

The Polypropylene Absorbent Hygiene Market size is expected to grow from USD 8.98 billion in 2025 to USD 9.42 billion in 2026 and is forecast to reach USD 11.97 billion by 2031 at 4.91% CAGR over 2026-2031.

What is driving diaper demand in Asia and Africa?

High birth volumes and still-low penetration rates combine to lift long-term diaper uptake.

Which product type is growing fastest?

Composite non-wovens, thanks to melt-blown + spun-bond laminates that optimize fluid handling at lower basis weights.

Are bio-based fibers a near-term threat to polypropylene?

Trials are underway, but higher costs and limited composting infrastructure mean displacement remains modest through 2031.

Page last updated on: