Market Overview

| Study Period | 2021 - 2031 |

|---|---|

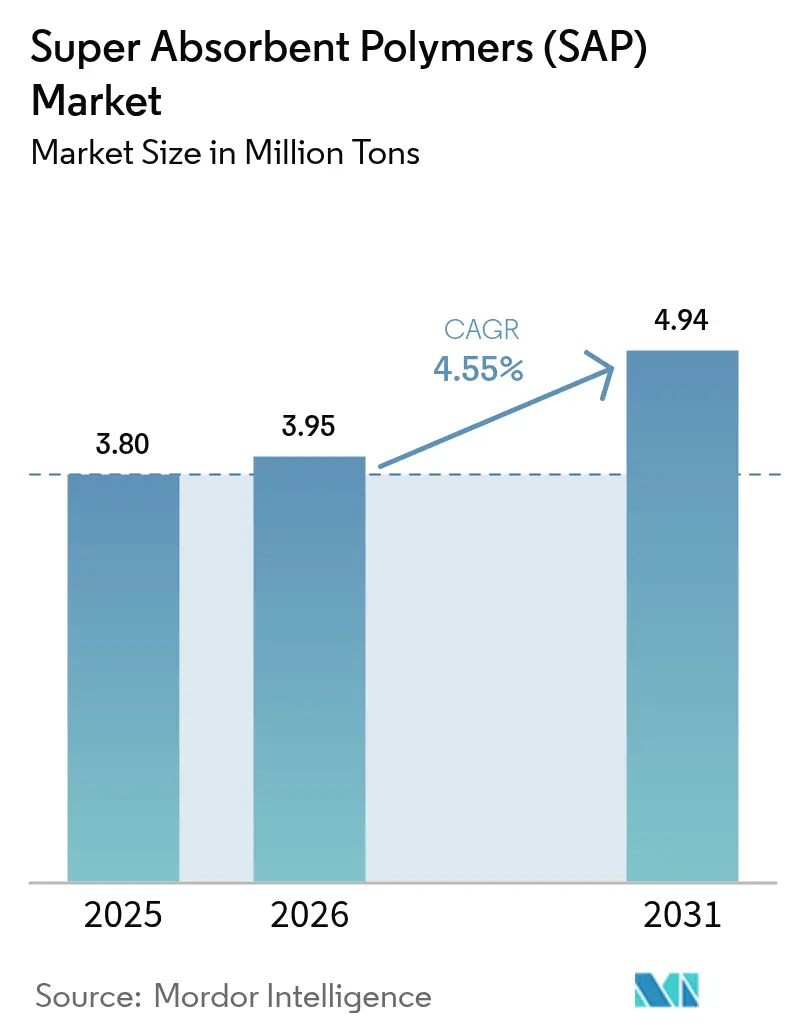

| Market Volume (2026) | 3.95 Million tons |

| Market Volume (2031) | 4.94 Million tons |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

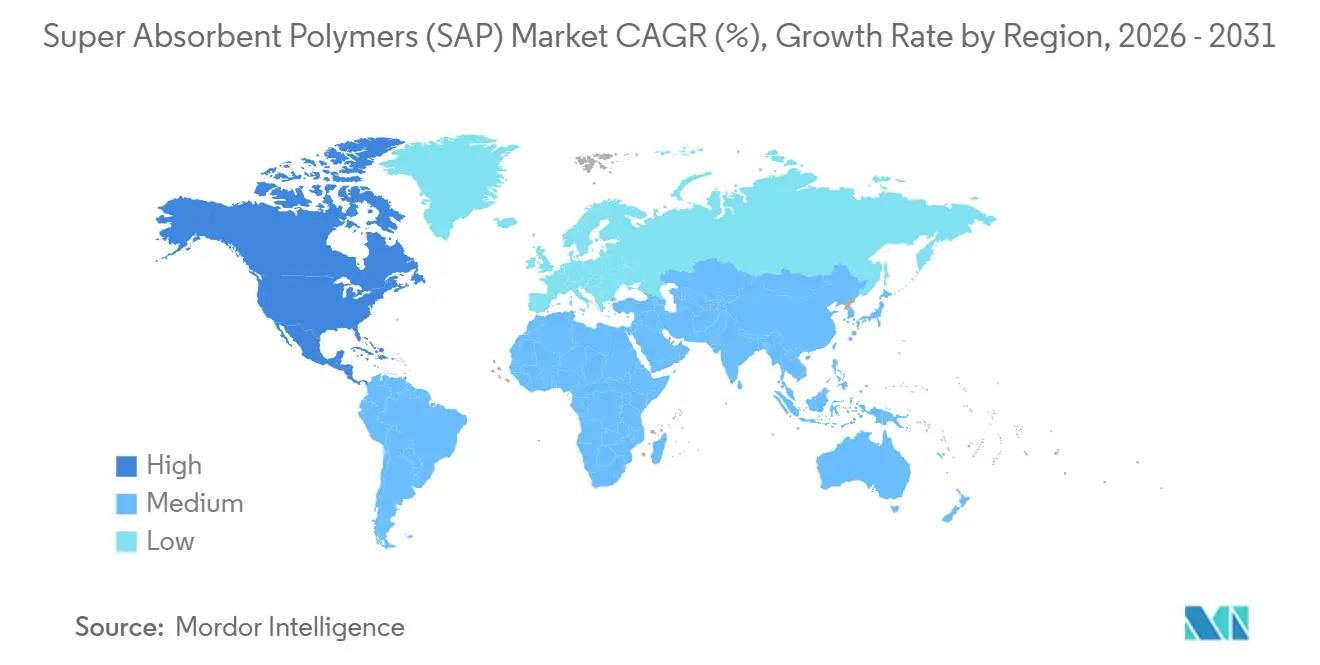

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

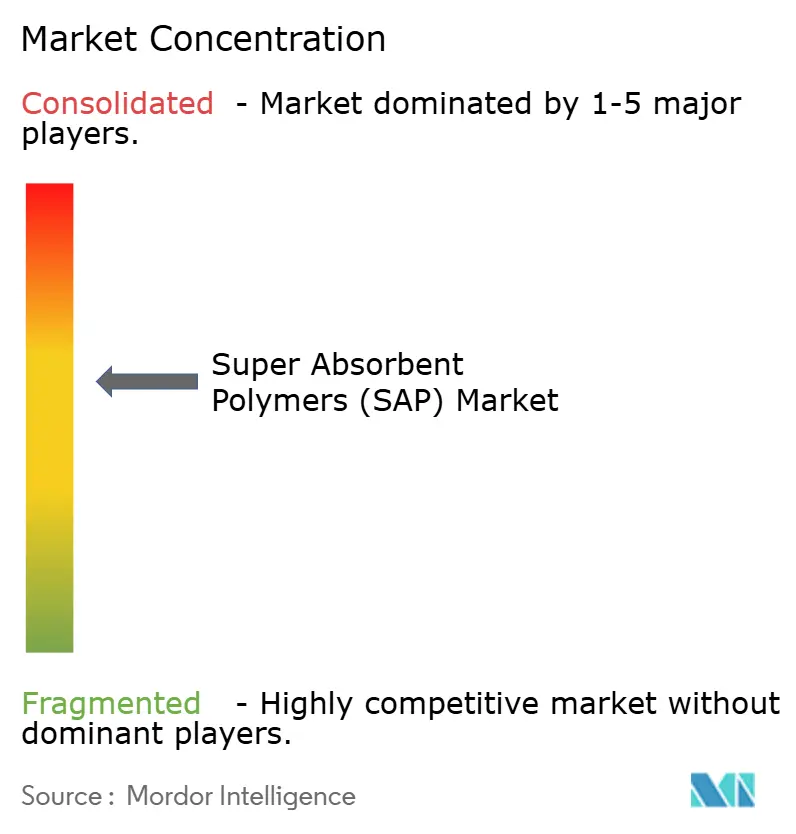

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Super Absorbent Polymers (SAP) Market Analysis by Mordor Intelligence

The Super Absorbent Polymers Market size is projected to grow from 3.80 million tons in 2025 to 3.95 million tons in 2026, and reach 4.94 million tons by 2031, growing at a CAGR of 4.55% from 2026 to 2031. Strong diaper demand in Asia, rapid take-up of high-SAP adult incontinence pads across Japan, South Korea, and Western Europe, and growing use of absorbent pads in e-commerce cold chains are reshaping global shipment flows. Producers are co-locating polymerization units next to diaper-converting lines to cut freight cost, while telecom cable makers are specifying SAP-based water-blocking yarns that swell on contact with moisture to protect expensive 5G fiber. Acrylic-acid feedstock volatility is compressing margins for non-integrated players, and landfill pressure in the European Union is accelerating pilot investment in bio-based grades that can satisfy future Extended Producer Responsibility mandates. As a result, the Super absorbent polymers market is moving toward backward-integrated and specialty-grade strategies that hedge feedstock swings and target premium applications.

Key Report Takeaways

- By product type, acrylic-acid SAP accounted for 72.54% of the super absorbent polymers market size in 2025; polyacrylamide variants are forecast to expand at a 6.67% CAGR between 2026-2031.

- By polymerization route, gel polymerization dominated with 60.64% revenue share in 2025; solution polymerization is projected to grow at 5.18% CAGR through 2031.

- By application, baby diapers held 60.12% of the super absorbent polymers market share in 2025, while adult incontinence pads are advancing at a 5.45% CAGR through 2031.

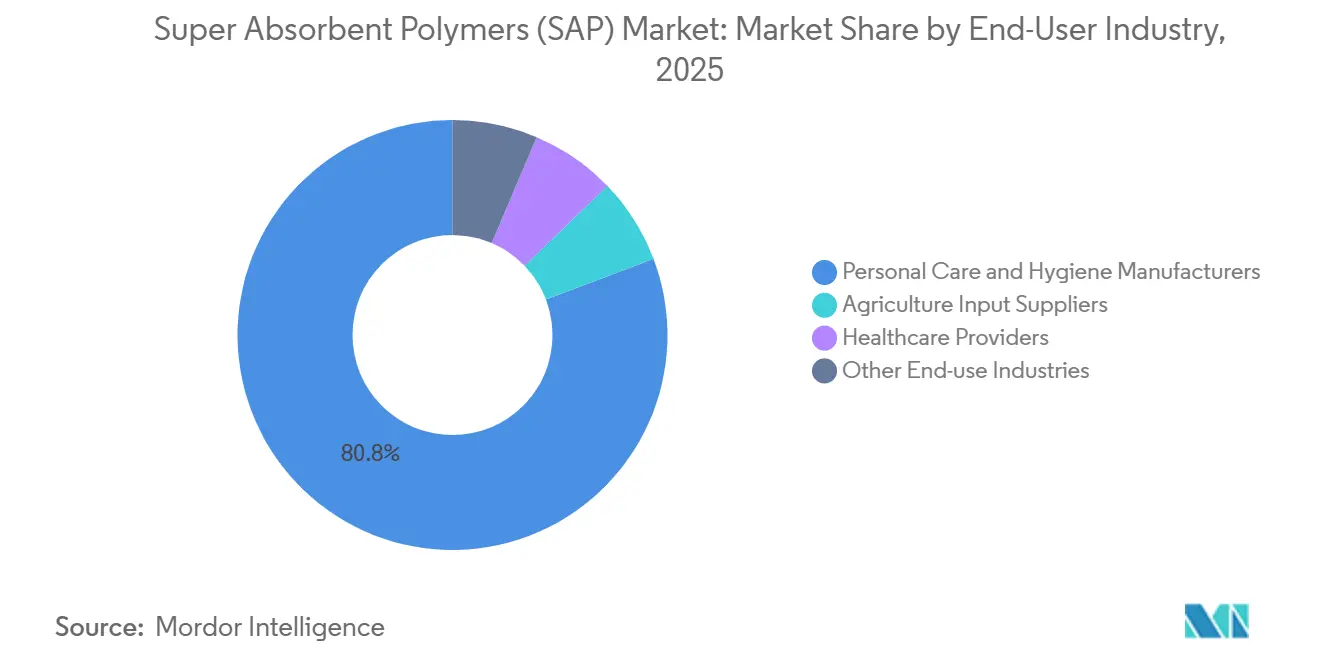

- By end-user industry, personal-care manufacturers absorbed 80.76% of 2025 volumes; agriculture input suppliers are pacing ahead at a 6.09% CAGR over 2026-2031.

- By geography, Asia-Pacific captured 42.59% shipment share in 2025, whereas North America is set to deliver the fastest 5.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Super Absorbent Polymers (SAP) Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising per-capita diaper spend in China and India | +1.2% | Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of high-SAP adult incontinence pads | +1.5% | Japan, South Korea, Germany, Italy | Long term (≥ 4 years) |

| E-commerce demand for absorbent cold-chain pads | +0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| 5G cable roll-outs pulling SAP water-blocking yarn | +0.4% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Vertical-farming substrates using SAP hydrogels | +0.3% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Per-Capita Diaper Spend in China and India

India’s disposable diaper outlays reached USD 1.74 billion in 2025 after the Goods and Services Tax on baby-care items was cut to 18% in 2024, making branded diapers more affordable for tier-two and tier-three cities. China’s infant-diaper penetration rose to 70% in 2025 as leading e-commerce platforms bundled subscription deliveries with loyalty discounts that raised average SAP loading per diaper from 8 grams to 12 grams, a jump driven by the shift to ultra-thin cores. Domestic suppliers such as Satellite Chemical have been scaling specialty polyacrylamide lines to serve this premium segment, while multinationals co-locate new SAP reactors next to diaper plants in Guangdong and Jiangsu to shorten lead times and cut inventory. The combined effect keeps the Super absorbent polymers market on a secular expansion path as Asian consumers trade up to higher SAP weights per article.

Rapid Adoption of High-SAP Adult Incontinence Pads in Asia and Europe

Japan’s population aged 65 plus crossed 29.1% in 2024, and South Korea widened National Health Insurance reimbursement for incontinence supplies, trimming consumer out-of-pocket expense by roughly 40%[1]Statistics Bureau of Japan, “Population Estimates,” stat.go.jp. European nations face a parallel aging trend, with Germany and Italy crossing the 20% threshold of seniors. Manufacturers are rolling out “active-lifestyle” pads containing 15-20 grams of SAP and using surface-cross-linking to hold more than 800 milliliters without leakage, a design that supports overnight use and fewer changes. Lower residual monomer targets—below 300 ppm—add process complexity yet allow brands to command 10-15% price premiums. This demographic tide is therefore steering the super absorbent polymers market toward higher-value adult-care grades.

E-Commerce-Led Demand Spike for Absorbent Cold-Chain Pads

Global pharmaceutical cold-chain revenue moved beyond USD 20 billion in 2024 as biologics and mRNA vaccines scaled up distribution[2]U.S. Food & Drug Administration, “Food Safety Modernization Act Guidance,” fda.gov. SAP-based pads are displacing gel packs because they weigh less, cut freight costs, and trap condensation if the outer pouch is damaged. Grocery deliverers in North America and Europe insert 30-50 gram SAP pads into cartons of seafood, dairy, and produce, extending shelf life by up to two days, a benefit aligned with the Food Safety Modernization Act’s temperature-control provisions. As urban fulfillment hubs multiply, the super absorbent polymers market receives an incremental lift from every incremental chilled parcel shipped.

5G Cable Roll-Outs Driving SAP Water-Blocking Yarn Demand

Telecom carriers installed more than 3.5 million 5G base stations in China by the end of 2024 and launched national deployments in India the same year. The fiber cables feeding these sites require water-blocking yarns that swell rapidly to stop moisture ingress, a function that SAP particles perform better than petroleum jelly. North American cable specifiers reference Telcordia GR-20-CORE, while European engineers align with IEC 60794; in both cases, SAP yarns meet the swell-time benchmarks with lower overall cable weight. Though niche, the segment commands 30-50% price premiums, supporting profit pools for specialty suppliers within the Super absorbent polymers market.

Restraint Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile acrylic-acid feedstock prices | –1.0% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Residual-monomer safety concerns in infant diapers | –0.5% | North America, Europe | Medium term (2-4 years) |

| Limited biodegradability raising landfill pressure | –0.4% | Europe, emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Acrylic-Acid Feedstock Prices

Northeast Asian acrylic-acid spot quotes swung between USD 1,200 and USD 1,600 per ton in 2024 after unplanned cracker outages, and European contracts climbed 8% quarter-on-quarter in early 2025 as refiners throttled propylene co-product output. Non-integrated SAP converters lack bargaining power for multi-year monomer deals, so margin compression reaches 150-200 basis points in a single quarter. The resulting shake-out saw Evonik sell its SAP unit to ICIG and Sanyo Chemical exit the field in 2024, evidence that scale and backward integration are prerequisites for survival in the super absorbent polymers market.

Residual-Monomer Safety Concerns in Infant Diapers

Voluntary industry limits cap residual acrylic acid at 300 ppm for baby-diaper grades, below many jurisdictions’ regulatory ceilings. California’s Proposition 65 listing of acrylic acid raises the specter of warning labels, nudging U.S. brands to tighten internal specs. Achieving sub-200 ppm typically requires extra washing or surface neutralization, adding 5-10% to unit cost and penalizing smaller firms that cannot amortize new equipment. Heightened scrutiny, therefore, drives a bifurcation toward premium low-monomer grades and accelerates capacity rationalization within the super absorbent polymers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Acrylic-Acid Variants Dominate, Polyacrylamide Advances in Agriculture

Acrylic-acid SAP captured 72.54% shipment share in 2025, owing to swelling capacity above 300 g/g and seamless fit with high-speed diaper lines. Polyacrylamide grades are pacing ahead at 6.67% CAGR to 2031 as agriculture suppliers seek cross-linked networks that hold water through extended droughts. Starch-graft and cellulose hydrogels remain niche because lower gel strength limits diaper use, and enzyme pretreatment inflates cost. Government subsidies in India and Australia encourage polyacrylamide soil conditioners, reinforcing a diversified demand base for the super absorbent polymers market.

Blended chemistries are emerging at the premium end: Japanese diaper brands specify surface-cross-linked acrylic SAP interspersed with natural polysaccharides to speed fluid uptake and lower residual monomer. With each functional tweak, suppliers secure higher margins and deepen customer lock-in, cushioning the Super absorbent polymers market from pure commodity pricing cycles.

By Polymerization Process: Gel Routes Lead, Solution Methods Pursue Finer Particles

Gel polymerization held 60.64% of 2025 capacity because it produces high-swelling particles in a single pass and avoids costly grinding. Yet solution polymerization is on a 5.18% CAGR trajectory as feminine-pad and thin-diaper makers request sub-150 micron particles that deliver uniform cores without dusting. Solution reactors also hit residual monomer below 200 ppm in-process, saving an extra washing step and aligning with tighter safety targets for infant products.

Capital profiles diverge: horizontal belt gel plants require more than USD 50 million for a 30 kt/yr line, whereas solution retrofits can leverage existing batch reactors but consume more energy due to solvent recovery. This trade-off sets the competitive tempo as firms choose between scale economies and flexibility within the superabsorbent polymers market.

By Application: Baby Diapers Anchor Demand, Adult Incontinence Accelerates

Baby diapers absorbed 60.12% of the 2025 volume, securing the highest super absorbent polymer market share among applications. Brands have lifted SAP loading per unit from 8 g in 2020 to 12 g in 2025 to create slimmer, more comfortable products, a shift that is adding around 3% a year to polymer intensity even as birth rates soften in developed economies. Ultra-thin menstrual pads occupy a mid-single-digit share and lean on surface-cross-linked grades that deliver sub-2 mm cores while holding more than 50 mL of fluid. Agriculture soil-conditioner and seed-coating uses are expanding, supported by precision-irrigation programs in the U.S. Corn Belt and Australia’s Murray–Darling Basin, where 2024 trials cut water use 35%.

Adult incontinence products are the fastest-growing outlet, forecast to rise at a 5.45% CAGR through 2031 as the 65-plus cohort passes 20% of the total population in Japan, Germany, and Italy. Premium “active-lifestyle” briefs now incorporate 15–20 g of polymer to ensure overnight protection, commanding 20–30% shelf-price premiums. Niche uses such as water-blocking yarn for 5G cables and absorbent pads for cold-chain logistics still contribute less than 5% of 2025 volume but are advancing at double-digit rates as fiber networks and grocery e-commerce expand. Together, these shifts reinforce the upward trajectory of the super absorbent polymer market size despite uneven demographic trends.

By End-User Industry: Personal-Care Manufacturers Dominate, Agriculture Suppliers Gain

Personal-care converters drew 80.76% of 2025 shipments, reinforcing their central position in the super absorbent polymer market size through diapers, adult briefs, and feminine-hygiene goods. Leading brand owners such as Procter & Gamble and Kimberly-Clark have penned multi-year supply and co-development pacts with BASF and Nippon Shokubai, speeding tailored grade launches and locking in favorable pricing. Healthcare providers, chiefly hospitals and nursing homes, evaluate incontinence pads on total cost of ownership, favoring high-SAP designs that reduce change frequency, laundry loads and skin-breakdown risk.

Agriculture input suppliers are set to expand at a 6.09% CAGR to 2031 by marketing SAP soil amendments that deliver 25–35% irrigation savings in dryland wheat and canola, findings backed by Australia’s Grains Research and Development Corporation field trials. Growth is also catalyzed by subsidy programs in water-stressed Indian states that reimburse up to 50% of SAP costs for smallholders. Unlike the consolidated personal-care channel, farm-supply chains remain fragmented, so vendors deploy digital agronomy tools, moisture sensors, and satellite imagery to prove return on investment at the plot level. Other users, from telecom-cable makers to vaccine cold-chain operators, represent a modest but rising slice of the super absorbent polymer market share as 5G rollouts and biologic drug distribution accelerate.

Geography Analysis

Asia-Pacific dominated with 42.59% of 2025 volume, led by China’s diaper uptick and Japan’s elderly-care boom. India’s disposable diaper retail climbed toward USD 1.74 billion as urban nuclear families adopted convenient baby-care products. Regional CAGR moderated versus the last decade, yet remains solid because SAP intensity per diaper rises even as birth rates flatten.

Europe held a mid-twenties share in 2025. Regulatory momentum—from the Waste Framework Directive to national EPR fees—pushes converters toward compostable cores and recycled packaging, adding research and development cost but positioning the super absorbent polymers market for a gradual pivot to bio-based grades. Nordic countries, with near-universal senior-care coverage, are testing premium adult pads that blend SAP with breathable back-sheets for skin health, reinforcing value over volume.

North America, forecast at 5.59% CAGR through 2031, benefits from precision-ag training in the U.S. Corn Belt where SAP soil conditioners cut irrigation 30-50% in maize field trials. Biologics cold-chain expansion adds another tailwind as absorbent pads become standard in last-mile pharmaceutical parcels. South America and the Middle East and Africa represent single-digit shares yet are notable for pockets of high growth: Brazil’s rising middle class lifts diaper uptake, Saudi Arabia’s fiber-optic expansion needs water-blocking yarns, and South Africa trials SAPs to buffer drought-prone maize zones.

Competitive Landscape

The super absorbent polymers market is moderately consolidated. Chinese competitors are aggressively expanding in the super absorbent polymers market, leveraging captive acrylic acid, economies of scale, and domestic logistical advantages. Differentiation is increasingly focused on specialty chemistries, sustainability credentials, and application-specific technical services. In response, Western producers are pursuing open-innovation initiatives with start-ups offering enzymatic or catalytic advancements for bio-monomer production to safeguard their margins in this dynamic market.

Super Absorbent Polymers (SAP) Industry Leaders

NIPPON SHOKUBAI CO., LTD.

BASF

SUMITOMO SEIKA CHEMICALS CO.,LTD.

LG Chem

SNF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: BASF invested USD 19.2 million to install advanced surface-cross-linking reactors at its Freeport, Texas SAP line, cutting residual monomer below 200 ppm.

- May 2024: Nippon Shokubai committed USD 80 million to add 50 kt/yr SAP capacity in Indonesia with integrated acrylic-acid units, targeting Southeast Asian diaper and agriculture demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the super-absorbent polymer (SAP) market as the global shipment and sale of cross-linked, water-swellable polymers, principally sodium polyacrylate and polyacrylamide derivatives, supplied in powder, granule, or fiber form for hygiene, medical, agriculture, and selected industrial uses.

Products blended only as minor additives in composites or used as in-situ gelling agents are outside scope.

Excluded: Loose fluff pulp, silica gels, and starch or cellulose hydro-gels that are not cross-linked to deliver >=100 g g^-1 absorbency.

Segmentation Overview

- By Product Type

- Polyacrylamide

- Acrylic Acid Based

- Others

- By Polymerization Process

- Solution Polymerization

- Suspension/Inverse-Suspension Polymerization

- Gel Polymerization

- By Application

- Baby Diapers

- Adult Incontinence Products

- Feminine Hygiene

- Agriculture Support

- Other Application

- By End-User Industry

- Personal Care and Hygiene Manufacturers

- Agriculture Input Suppliers

- Healthcare Providers

- Other End-use Industries (Telecom and Power Cable Makers and Food and Pharmaceutical Cold-Chain Logistics)

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Egypt

- Nigeria

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed polymer chemists at three leading producers, hygiene-product sourcing heads across Asia-Pacific, Europe, and North America, plus distributors serving agriculture additives. These conversations validated per-diaper SAP loading, clarified regional ASP dispersion, and stress-tested our unit growth expectations through 2030.

Desk Research

We gathered foundational data from open sources such as UN Comtrade export codes 390690, Eurostat PRODCOM 20139090, EDANA nonwovens statistics, China Customs, and the U.S. International Trade Commission; these outline trade flows and apparent consumption. Company 10-Ks and investor decks clarify installed capacities, while regulatory filings from the European Chemicals Agency and the U.S. EPA reveal technology shifts toward bio-based grades. Subscription resources in Mordor's paid stack, D&B Hoovers for producer revenues and Volza shipment logs for contract volumes, tighten volume-to-value conversion. The sources cited here illustrate the range consulted; many additional publications informed smaller datapoints.

Market-Sizing & Forecasting

We start with a top-down demand pool: live-birth counts, adult incontinence prevalence, hectare adoption of water-retention agents, and average SAP usage per unit build a consumption skeleton, which is then reconciled with producer capacity roll-ups and selected channel checks. Key model variables include global birth rate trends, 65+ population growth, acrylic-acid reference prices, diaper penetration ratios in emerging economies, and announced plant debottleneck projects. A multivariate regression links these drivers to historical tonnage, and scenario analysis adjusts for raw-material cost shocks before translating tons to revenue with region-specific ASPs. Bottom-up discrepancies larger than five percent trigger further supplier callbacks.

Data Validation & Update Cycle

Outputs pass three layers: algorithmic outlier scans, peer review by senior polymer analysts, and final sign-off from the chemicals domain lead. Reports refresh annually; interim updates occur when capacity additions, feedstock spikes, or regulatory shifts move the baseline materially.

Credibility Corner: Why Mordor's Super Absorbent Polymer Baseline Commands Reliability

Published figures often diverge because firms mix bio-gels, niche medical grades, or even fluff pulp into scope, apply rigid cost-plus ASP ladders, or freeze assumptions for several years.

Key Gap Drivers

Scope breadth, some studies fold specialty SAP for flood sacks; we retain only hygiene, medical, agri, and defined industrial grades.

Unit-price logic, our ASP series tracks quarterly acrylic-acid index and contract discounts; other publishers use list prices or global averages.

Refresh cadence, Mordor revisits capacity, utilization, and trade every twelve months, while others reference pre-pandemic data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.78 million tons (2025) | Mordor Intelligence | - |

| USD 10.39 billion (2024) | Global Consultancy A | Includes un-cross-linked hydrogels and applies uniform ASP across regions |

| USD 9.88 billion (2025) | Industry Data Provider B | Converts producer capacity to revenue without trade adjustment and uses 2022 currency rates |

In sum, our disciplined scope, driver-linked pricing, and frequent updates give decision-makers a balanced, transparent baseline they can retrace and reuse with confidence.

Key Questions Answered in the Report

What is the projected demand volume for super absorbent polymers by 2031?

Global shipments are forecast to reach 4.94 million tons by 2031 on a 4.55% CAGR.

Which application segment is growing fastest?

Adult incontinence pads post the highest 5.45% CAGR through 2031 as aging populations expand in Japan, South Korea, and Europe.

Why are acrylic-acid SAP prices volatile?

Prices track propylene feedstock swings, refinery outages, and regional supply tightness, leading to quarterly acrylic-acid moves of several hundred USD per ton.

What role do SAPs play in 5G infrastructure?

SAP-infused yarns swell on water contact, blocking moisture in fiber-optic cables to protect signal integrity during 5G network roll-outs.

Are bio-based SAPs commercially significant yet?

Pilot lines exist, but bio-based grades account for less than 0.05% of output because current costs run 40-60% above petroleum-derived equivalents.

Page last updated on: