Expanded Polypropylene (EPP) Foam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

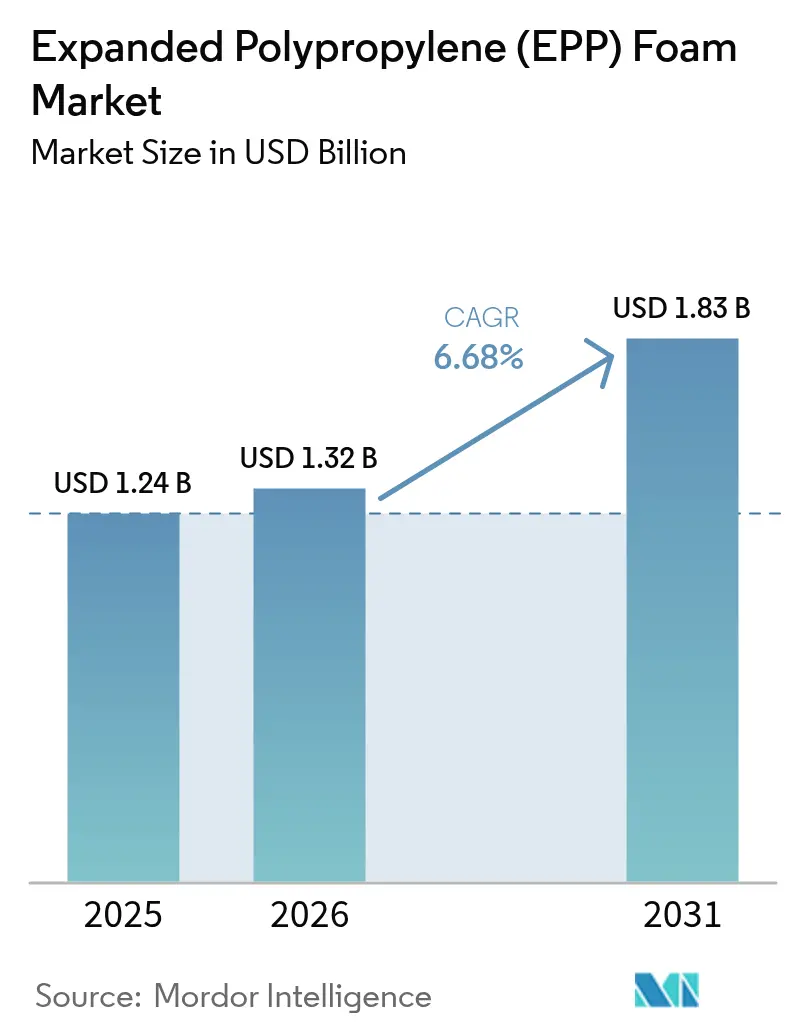

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Expanded Polypropylene (EPP) Foam Market Analysis by Mordor Intelligence

The Expanded Polypropylene Foam Market size is expected to grow from USD 1.24 billion in 2025 to USD 1.32 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at a 6.68% CAGR over 2026-2031. Rapid automotive lightweighting, the boom in reusable e-commerce packaging, and the need for thermal barriers in electric-vehicle (EV) batteries are the principal forces shaping demand. Synthetic polypropylene maintained price leadership in 2025, helping converters limit resin-cost volatility. Concurrently, 3D steam-chest molding is reducing part counts in complex HVAC ducts and battery enclosures, trimming assembly labor, and reinforcing the expanded polypropylene foam market’s pull with OEM engineers. Regulatory tightening on microplastic pellet loss in Europe and California is adding 8-12% to compliance costs, yet large fabricators are absorbing these outlays through scale efficiencies. Asia-Pacific’s 15-20% landed-cost advantage keeps the region on top, although new capacity coming onstream in Ohio and Thailand signals a gradual rebalance.

Key Report Takeaways

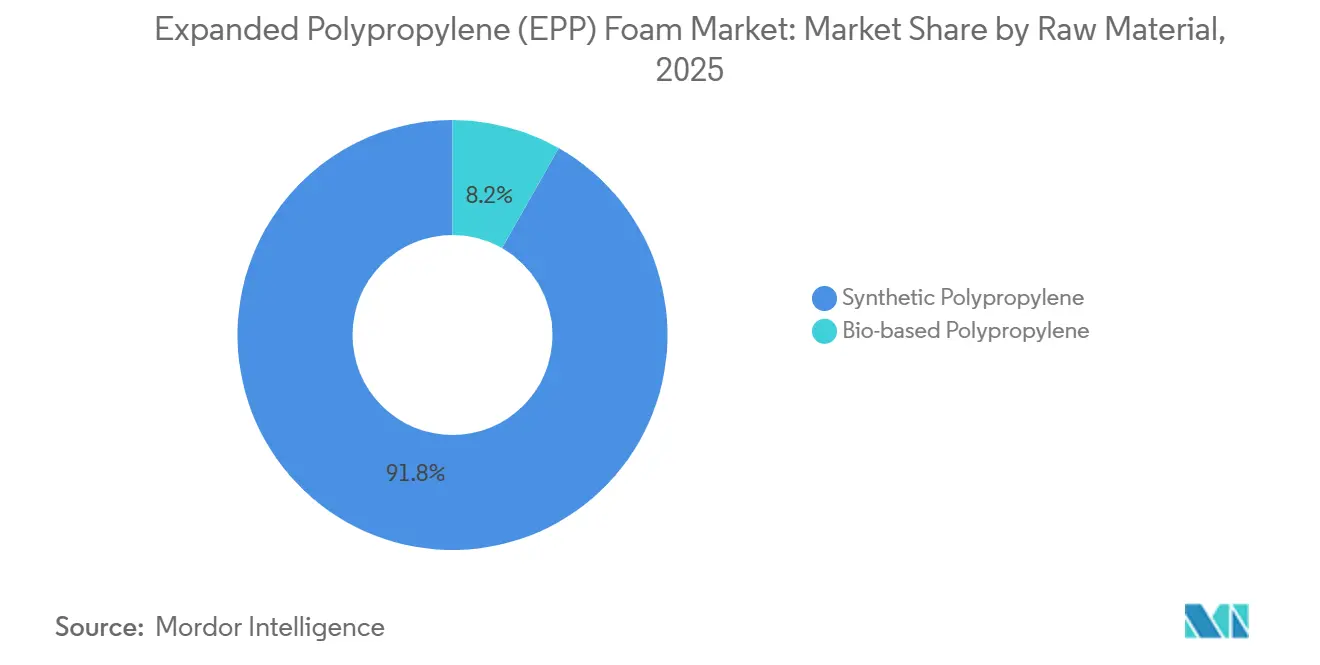

- By raw material, synthetic polypropylene held 91.78% of the Expanded Polypropylene (EPP) Foam market share in 2025 and is expected to retain its leadership by growing at a CAGR of 6.89% during the forecast period (2026-2031).

- By foam type, molded EPP captured 70.88% of the Expanded Polypropylene (EPP) Foam market share in 2025 and is forecasted to grow at a 6.80% CAGR during the forecast period (2026-2031), due to rising demand for complex geometries in automotive interiors.

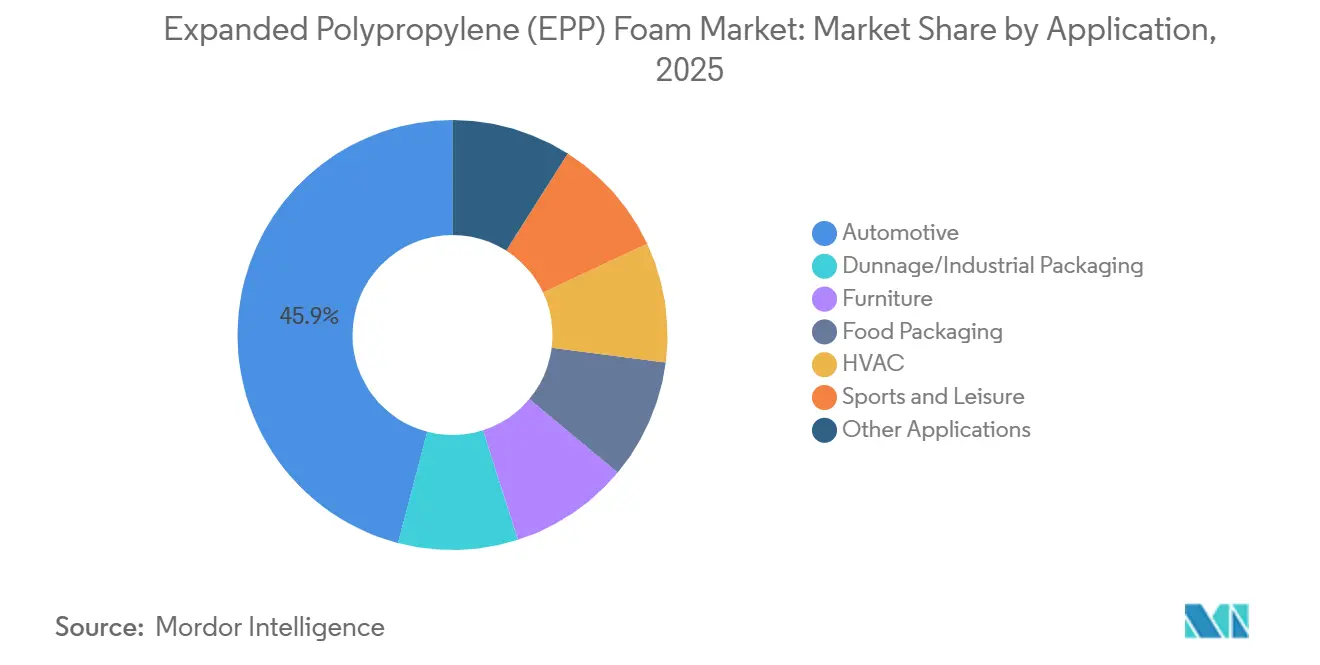

- By application, the automotive sector led with a 45.92% revenue share in 2025, while the dunnage/industrial packaging segment is expected to expand at a 7.02% CAGR through 2031 as e-commerce platforms adopt reusable crate systems.

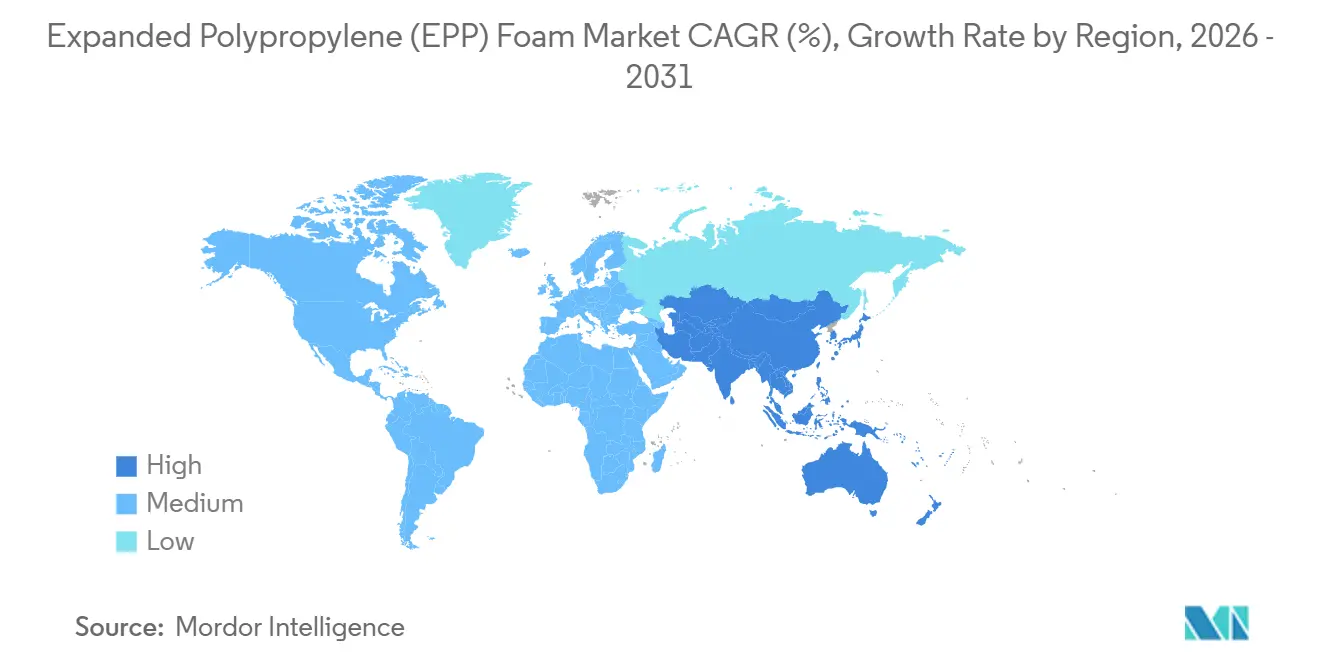

- By geography, the Asia-Pacific region commanded 42.22% of 2025 revenue and is advancing at a 7.15% CAGR during the forecast period (2026-2031), driven by new JSP capacity in India and Mexico, serving regional automotive transplants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Expanded Polypropylene (EPP) Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting and safety demand | +1.8% | Global, with concentration in APAC (China, Japan, South Korea) and Europe (Germany, France) | Medium term (2-4 years) |

| Boom in e-commerce protective packaging | +1.5% | Global, led by North America and APAC, spill-over to Europe and MEA | Short term (≤ 2 years) |

| 3D steam-chest molding enables complex auto parts | +1.2% | APAC core (Japan, South Korea), expanding to North America and Europe | Long term (≥ 4 years) |

| Adoption in electric vehicle battery thermal management packs | +1.0% | APAC (China, South Korea), North America (United States), Europe (Germany) | Medium term (2-4 years) |

| Net-zero buildings using EPP geo-foam insulation | +0.6% | Europe (Nordics, Germany), MEA (Saudi Arabia, UAE), North America (Canada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting and Safety Demand

Vehicle makers target 10-20% mass reduction by 2030 and have specified expanded polypropylene foam in 65% of the Japanese passenger-car platforms launched since 2024. Europe’s 2025 update to UN ECE R94 side-impact rules raised energy-absorption thresholds by 15%, accelerating foam substitution for heavier polyurethane in B-pillar reinforcements[1]Knauf Industries, “Automotive Applications of EPP,” knaufindustries.com. EV programs intensify this pull; EPP combines impact protection with thermal insulation, so it increasingly lines lithium-ion packs where weight offsets are scarce.

Boom in E-commerce Protective Packaging

Cross-border parcels doubled between 2024 and 2025, and reusable EPP dunnage lowers damage rates by 30-50% versus fiberboard, making the expanded polypropylene foam market indispensable to fulfillment centers[2]European Bioplastics, “Bioplastics Market Data 2025,” europeanbioplastics.org. Sonoco’s 2024 EnviroFlex trays nest for return shipping, cutting reverse-logistics costs 20% while surviving 10-15 trips. Cost remains the friction point: units are 20-30% pricier than EPS, limiting uptake to high-value electronics.

3D Steam-chest Molding Enables Complex Auto Parts

One-piece HVAC ducts and battery trays, molded with independent steam zones, trim component weight by 18% and assembly labor by 60%. Capital outlays of USD 0.5-1.5 million per tool confine most lines to Japan, South Korea, and China. Sekisui Plastics broke this pattern with a USD 25 million Ohio plant due online in 2026, promising 12,000 t/y of domestic capacity.

Adoption in Electric-Vehicle Battery Thermal Management Packs

Chinese EV makers integrated EPP thermal barriers in 45% of 2025 battery designs, up from 20% in 2024, complying with flame-spread ratings below 25. Hanwha Solutions supplies spacers to LG Energy Solution and Samsung SDI, shipping 2.3 million packs in 2025. Foam maintains cell spacing during vibration and muffles 200-400 Hz inverter hum, improving cabin acoustics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from cheaper EPS and other foams | -1.2% | Global, most acute in price-sensitive segments (food packaging, furniture) | Short term (≤ 2 years) |

| Limited steam-chest molding capacity ex-Asia | -0.8% | North America, Europe, South America | Medium term (2-4 years) |

| Microplastics pellet-loss regulations tightening | -0.5% | Europe (EU-27), North America (California, Canada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Cheaper EPS and Other Foams

Expanded polystyrene maintains a 20-30% cost advantage over EPP in commodity applications, and food packaging and furniture segments remain price-sensitive enough to resist switching despite EPP's superior reusability. Cold-chain food packaging illustrates the trade-off: EPP insulated containers survive 10-15 reuse cycles versus 2-3 for EPS, but the initial unit cost of USD 8-12 for EPP versus USD 3-5 for EPS deters small-scale distributors with limited reverse-logistics infrastructure. The prototype remains pre-commercial, yet it underscores the risk that adjacent materials will erode EPP's sustainability positioning if bio-based polypropylene feedstock scales slowly.

Limited Steam-chest Molding Capacity Ex-Asia

North America and Europe collectively held under 25% of global steam-chest molding capacity in 2025, constraining local automotive OEMs' ability to source complex EPP components with just-in-time delivery. European molders face additional constraints from natural gas price volatility; steam generation accounts for 40-50% of EPP molding energy costs, and gas prices that spiked 60% in early 2025 compressed margins by 8-12 percentage points. Asian competitors benefit from coal-fired steam generation and vertically integrated polypropylene supply chains, creating a structural cost disadvantage that limits Western capacity expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Synthetic Dominance Persists Despite Bio-push

Synthetic polypropylene accounted for 91.78% of the expanded polypropylene foam market size for raw materials in 2025, expanding at a 6.89% CAGR to 2031. Bio-based content remains very low but is forecast to reach a decent share of global bioplastics capacity by 2029 as Neste and LyondellBasell scale renewable feedstocks. Cost discipline and tight crystallinity tolerances keep synthetic grades in pole position for automotive and dunnage. Consumer-facing goods such as sports helmets accept the 15-20% premium for bio-EPP, underpinning slower CAGR growth.

Brand owners seeking lower carbon footprints are piloting bio-PP EPP in food-contact trials pending regulatory clearance in the United States and Europe. The expanded polypropylene foam market, therefore, balances secure fossil-based supply chains against sustainability branding in high-margin niches.

By Foam Type: Molded EPP Leads on Automotive Demand

Molded grades captured 70.88% of the expanded polypropylene foam market share by foam type in 2025, posting a 6.80% forecast CAGR for the period between 2026 to 2031. Steam-chest molding generates net-shape parts with density gradients, saving 15-20% material versus fabricated sheet. Fabricated foam retains relevance in low-volume HVAC ducting thanks to simpler tooling and shorter lead times.

Growth in 3D steam-chest technology amplifies molded foam’s leadership by integrating clips and fasteners directly into bumper cores and door inserts. Extruded polypropylene and bead-molded variants together hold a small share, targeting aerospace interiors where Zotefoams’ autoclave route meets FAA flame limits.

By Application: Dunnage Outpaces Automotive Growth

Automotive remained the largest slice at 45.92% in 2025, yet dunnage and industrial packaging will outstrip it with a 7.02% CAGR during the forecast period (2026-2031) as the expanded polypropylene foam market follows e-commerce’s logistics expansion. Reusable inserts show 20% reverse-logistics savings and reduced breakage, lining up with Amazon and Alibaba sustainability pledges.

Automotive will still advance by extending into EV battery covers, while food packaging leverages cold-chain growth for biologics and specialty groceries. Sports and leisure rely on multi-impact helmets that outperform EPS in low-energy events.

Geography Analysis

Asia-Pacific held 42.22% of the expanded polypropylene foam market in 2025 and will increase at a 7.15% CAGR. China produced 28 million vehicles and specified EPP in 55% of new car platforms. Japan’s JSP, Kaneka, and Sekisui ship 60% of output overseas, proving that vertically integrated resin supply plus low steam energy costs confer a 15-20% cost advantage.

North America’s market share is poised for decent growth, as EPA mileage rules force lightweighting. Sekisui Plastics’ Ohio plant goes live in 2026, trimming Detroit lead times 40%. Canada’s single-use plastics ban drives reusable dunnage, and Mexico’s 3.5-million-unit auto output boosts local molding.

Europe’s market share is about experience nominal growth, checked by energy volatility and microplastics rules. Net-zero building codes in the Nordics lifted geo-foam insulation demand 35% for BEWi in 2025. South America and the Middle East-Africa together form an emerging 8% slice, stimulated by Brazil’s and Saudi Arabia’s green-building ordinances.

Regulatory Landscape

Regulation affecting expanded polypropylene (EPP) foam is tightening most visibly around packaging circularity, pellet-loss prevention, and chemical compliance. In the European Union, Regulation (EU) 2025/40 entered into force on 11 February 2025 and begins application on 12 August 2026, pushing minimum recycled content and harmonized labeling requirements that affect EPP packaging formats and traceability practices across EU-27 supply chains.

Region-specific restrictions also influence end-use suitability and portfolio design. Western Australia implemented a ban on expanded plastic packaging (including EPP) effective 1 July 2025 for products manufactured on or after 1 March 2025, reducing addressable packaging demand in that jurisdiction. In North America, California SB 54 final regulations (2026) set circular-economy compliance obligations for producers of covered material, reinforcing requirements for documented recycling performance; alongside this, EPP producers continue to operate under broad chemical substance frameworks such as EU REACH for upstream substance registration and safe-use requirements.

Value Chain Analysis

The EPP foam value chain runs from upstream propylene and polypropylene resin production through bead production and conversion into molded or fabricated parts, then to distribution and end-use integration. Upstream feedstocks are tied to crude oil and natural gas markets, with polypropylene suppliers including large global resin producers; the midstream is led by EPP bead and foam producers such as JSP, BASF, Kaneka, Hanwha Solutions, Knauf Industries, and BEWi, which supply beads, technical grades, and application-specific compounds to converters and OEM-aligned molders.

Conversion is energy and process intensive, centered on steam-based pre-expansion, conditioning/maturation, and steam-chest molding, where tooling and steam generation shape both cost and throughput. Downstream demand concentrates in automotive (impact management, lightweighting, interior and battery-related components) and protective dunnage/industrial packaging that depends on reverse-logistics systems for reuse. Circularity is increasingly embedded in the chain via recycled polypropylene sourcing and closed-loop programs, with partnerships and initiatives that secure recycled feedstock and improve traceability becoming operational differentiators for bead suppliers and large converters.

Competitive Landscape

The Expanded Polypropylene (EPP) Foam market is moderately consolidated. Niche converters target sports helmets, cold-chain boxes, and HVAC ducts where closed-cell durability commands a 20-30% price premium over EPS. Patent portfolios defend incumbents; JSP holds 120+ filings covering bead pre-expansion and mold filling, and ISO 14001 environmental certification is now table stakes with automakers policing pellet handling. Bio-based EPP pioneers cultivate brand alignment, but cellulose-foam prototypes signal eventual adjacent-material competition.

Expanded Polypropylene (EPP) Foam Industry Leaders

JSP

BASF

Kaneka Corporation

Hanwha Solutions

BEWI

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits in regionalizing EPP part supply for automotive and industrial packaging customers that need short lead times and consistent quality outside Asia-Pacific. North American converters are allocating capital to add local EPP capacity: Engineered Foam Packaging (EFP) announced a USD 31.5 million expansion of its Bishopville, South Carolina facility (200,000 square feet) to increase EPP and EPS production capacity, with operations targeted to be fully functional by April 2026. This expansion supports nearer-to-OEM sourcing and reduces the logistics burden for reusable packaging loops where return economics depend on cycle time and damage-rate reduction.

Technology and materials choices also open opportunities in thinner-wall, tighter-tolerance molded parts and in more recyclable, design-aligned packaging formats under new rules. JSP published SAE technical work in April 2026 describing new EPP grades aimed at tighter dimensional tolerances at thinner cross-sections, aligning with component consolidation trends in complex automotive parts that favor one-piece molded solutions. On the resin side, Borealis announced an investment of over EUR 100 million to add a new production line at Burghausen, Germany, with start-up planned for the second half of 2026 to triple capacity for High Melt Strength polypropylene used in lightweight foam solutions, supporting broader availability of foam-optimized PP inputs as packaging and product designers adopt design-for-recycling guidance and recycled-content requirements.

Recent Industry Developments

- June 2026: Borealis announces EUR 100 million investment to add a new production line at Burghausen, Germany, with start-up planned for the second half of 2026 to triple capacity for High Melt Strength polypropylene used in lightweight foam solutions.

- October 2025: JSP partnered with Alessiohitech to validate ZERO tooling for EPP molding, reporting cycle-time reductions of about 30 percent and steam-use reductions of over 50 percent.

- November 2024: JSP inaugurated manufacturing operations in Pune, India, to produce ARPRO (EPP) for domestic automotive and packaging customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the value of expanded polypropylene (EPP) foam materials sold as beads and converted foams used in end applications such as cushioning, impact protection, and lightweight parts across industries.

Scope exclusions: We exclude non-EPP polymer foams (such as EPS, XPS, PU, and PE foams) and fully assembled finished goods where EPP is only one input.

Segmentation Overview

- By Raw Material

- Synthetic Polypropylene

- Bio-based Polypropylene

- By Foam Type

- Fabricated EPP

- Molded EPP

- Other Foams

- By Application

- Automotive

- Dunnage/Industrial Packaging

- Furniture

- Food Packaging

- HVAC

- Sports and Leisure

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi-Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the EPP foam value chain and the demand pool in the most material end uses, which helps us avoid mixing EPP with wider polymer foam categories. We use public sources such as UN Comtrade trade statistics for polymer articles, USITC and EU trade portals for tariff line context, and national statistics offices for industrial output and automotive production indicators.

We also review technical and market signals from sources such as USPTO and EPO patent databases to see where material and processing innovation is clustering, peer reviewed polymer science journals for density and performance benchmarks, and trade association publications for packaging and automotive material trends. This is then complemented with company annual reports, investor presentations, and reputable press for capacity additions, plant locations, and product mix cues, along with selective use of paid subscriptions for company financials and intelligence, patent analytics, and shipment-level import and export checks where available. These examples are not exhaustive, and many other public sources were used to collect, validate, and clarify the final dataset.

Primary Interviews and Surveys

Primary work focuses on validating what is actually sold as EPP foam revenue, how pricing moves by density and form, and how demand changes across automotive, packaging, and industrial uses. We spoke with a mix of material suppliers, foam converters, distributors, and procurement and engineering respondents from key end-use industries, and then used that input to confirm assumptions and adjust outliers across regions.

Because application and processing choices vary by geography, inputs were cross-checked with respondents covering APAC, EMEA, and the Americas so we could align penetration and price logic to local realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | APAC: 41% |

| Mid tier: 44% | Functional/Unit leaders: 26% | EMEA: 36% |

| Smaller Players: 22% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, where demand is reconstructed from end-use activity and then cross-checked with supplier and converter reality checks. On the top-down side, we translate indicators such as light vehicle production, use-rate of EPP in safety and interior parts, packaging volumes for durable and returnable transport, and industrial dunnage usage into an addressable EPP foam demand pool, which is then priced using typical regional ASP ranges.

Bottom-up checks are applied selectively by rolling up a sample of supplier and converter revenue splits, validating capacity and utilization ranges, and testing ASP x volume for common density bands and forms (beads, molded parts, and fabricated shapes). Where company disclosures are limited, gaps are handled with conservative interpolation using nearby peers, trade flow signals, and interview-based channel checks.

For forecasting, we rely on scenario analysis supported by a simple multivariate regression view, using drivers like automotive lightweighting intensity, EV-related thermal and protection needs, industrial production cycles, and resin price direction as explanatory inputs. Assumptions are reviewed with primary respondents so the forecast reflects practical adoption pace rather than purely smooth trend lines.

Data Validation & Update Cycle

Model outputs are triangulated against independent signals such as regional production trends, trade movement direction, and implied consumption per end-use unit, and then the biggest variances are reworked until the logic is consistent. Anomaly checks are done at the country and application level so sudden jumps in pricing, penetration, or volumes are questioned and corrected before sign-off.

A multi-step review is followed where another analyst rechecks calculations, units, currency conversion timing, and the linkage between drivers and outputs. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity announcements, sharp resin cost swings, or demand shocks. Before delivery, we run a final update pass so the client receives the most current view possible.

Mordor Intelligence's Expanded Polypropylene Epp Foam Market Sizing Compared With Other Published Estimates

Published market sizes for EPP foam can look far apart because the scope line is drawn differently across sources, and because pricing and end-use penetration assumptions are updated at different times. The table makes this visible right away, since each estimate reflects its own choices on what gets counted and how current-year pricing is carried forward.

Key gap drivers here usually come from whether pre-expanded bead intermediates and converted forms are both counted, how automotive content per vehicle is treated, and whether packaging demand is tied to returnable transport versus broader protective packaging. The table shows part of the spread, and in Mordor Intelligence's model the 2025 value is aligned to EPP foam revenue across beads and converted products, while excluding other polymer foams and fully assembled finished goods that only contain EPP as a component.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.24 B (2025) | |

| Global Consultancy A | USD 1.26 B (2025) | Often includes a wider product mapping and may blend revenue and volume views, which can shift totals when density mix and conversion yield assumptions are not made explicit. |

| Industry Publisher B | USD 1.80 B (2025) | Tends to use broader inclusion choices around what counts as EPP-related value and can apply higher assumed pricing or content per end-use unit, which lifts the stated market size for the same year. |

Taken together, the comparison suggests that the tightest way to reduce variance is to keep the counted product set clear and then anchor volumes to observable end-use activity, before applying pricing logic that is checked with real market participants. This approach produces a balanced number that can be traced back to practical drivers like vehicle output, packaging use intensity, density mix, and region-level ASP movement.

Key Questions Answered in the Report

What CAGR is forecast for expanded polypropylene foam through 2031?

The expanded polypropylene foam market is forecast to post a 6.68% CAGR from 2026 to 2031.

Which region leads demand?

Asia-Pacific held 42.22% in 2025 and will grow at a 7.15% CAGR, driven by China, Japan, and South Korea.

Why is dunnage growing faster than automotive?

Cross-border e-commerce doubled in 2024-2025, and reusable EPP dunnage cuts breakage and reverse-logistics costs, supporting a 7.02% CAGR to 2031.

What is the main technical advance in molding?

3D steam-chest molding creates complex one-piece parts, trimming part count and reducing assembly labor by up to 60%.

How do microplastics rules affect producers?

EU and Californian regulations add 8-12% compliance costs by mandating closed-loop pellet handling and audits, pressuring smaller converters.

What is the current market size of expanded polypropylene foam market?

The Expanded Polypropylene Foam Market size is expected to grow from USD 1.24 billion in 2025 to USD 1.32 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at a 6.68% CAGR over 2026-2031.

Page last updated on: