Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

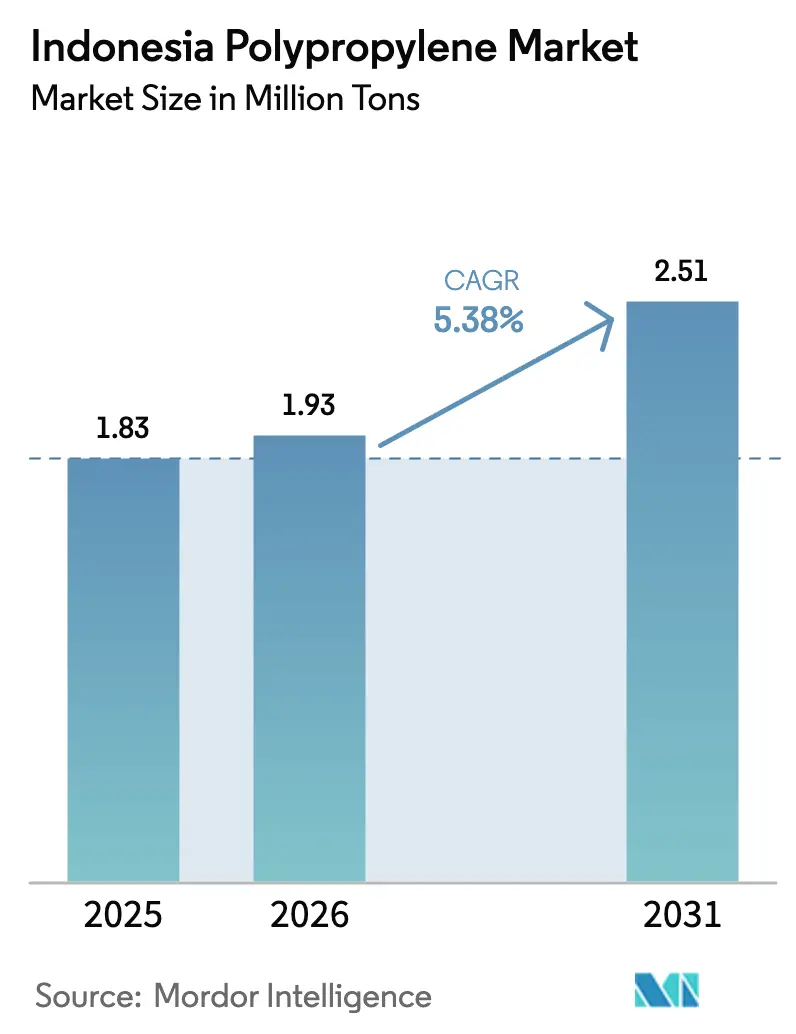

| Base Year Market Size (2025) | 1.83 Million tons |

| Market Volume (2026) | 1.93 Million tons |

| Market Volume (2031) | 2.51 Million tons |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Polypropylene Market Analysis by Mordor Intelligence

Indonesia Polypropylene Market size in 2026 is estimated at 1.93 million tons, growing from 2025 value of 1.83 million tons with 2031 projections showing 2.51 million tons, growing at 5.38% CAGR over 2026-2031. Population growth, widening middle-class purchasing power, new domestic capacity led by Lotte Chemical Indonesia’s 350 kiloton-per-year line, and rising sustainability mandates collectively sustain this trajectory. The Indonesia polypropylene market is transforming from a heavily import-dependent arena toward integrated local production as anti-dumping measures, refinery-to-polymer integration at Balikpapan, and extended-producer-responsibility rules steer resin buyers toward domestic supply. Flexible-packaging demand from snack, beverage, and personal-care brands is shifting rapidly toward recyclable mono-material films, while automotive lightweighting, under 40% TKDN local-content rules, is lifting demand for glass-fiber-reinforced grades. At the same time, e-commerce parcel volumes are accelerating the use of film and woven bags, and integrated producers such as Chandra Asri Petrochemical are leveraging feedstock control to compete on cost and reliability.

Key Report Takeaways

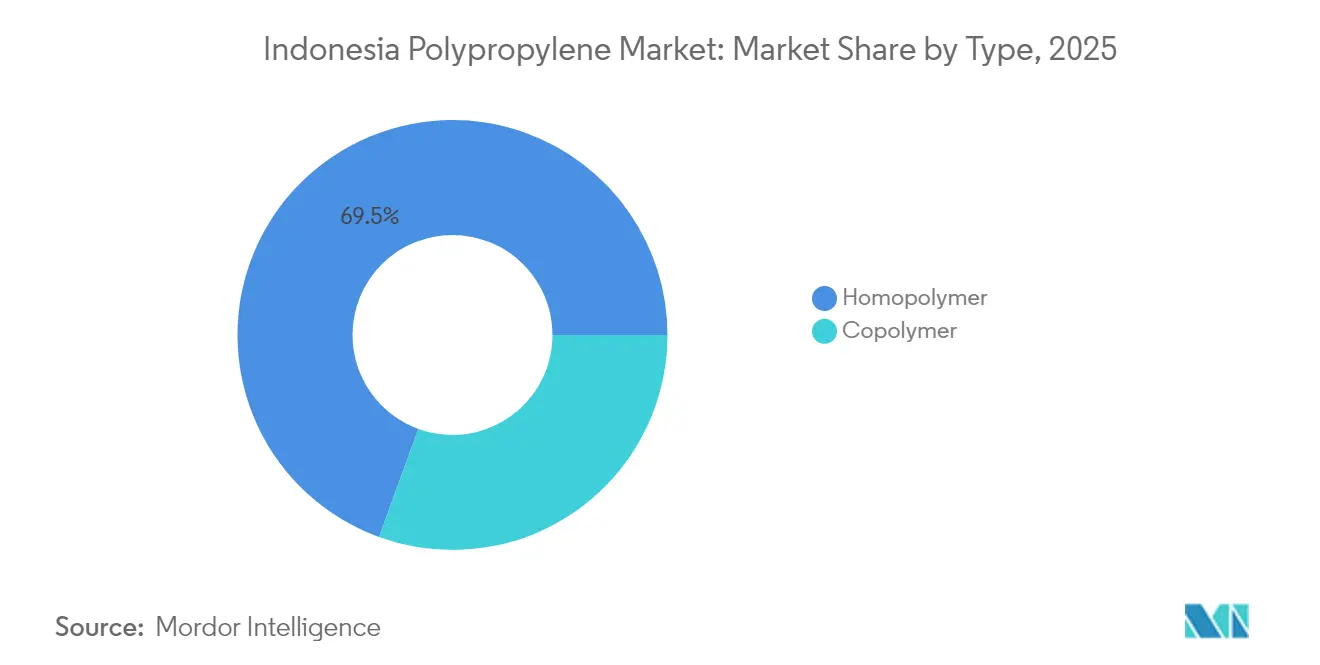

- By type, homopolymer captured 69.45% of the Indonesia polypropylene market share in 2025. The market share of homopolymer is expected to grow with a CAGR of 5.59% during the forecast period (2026-2031).

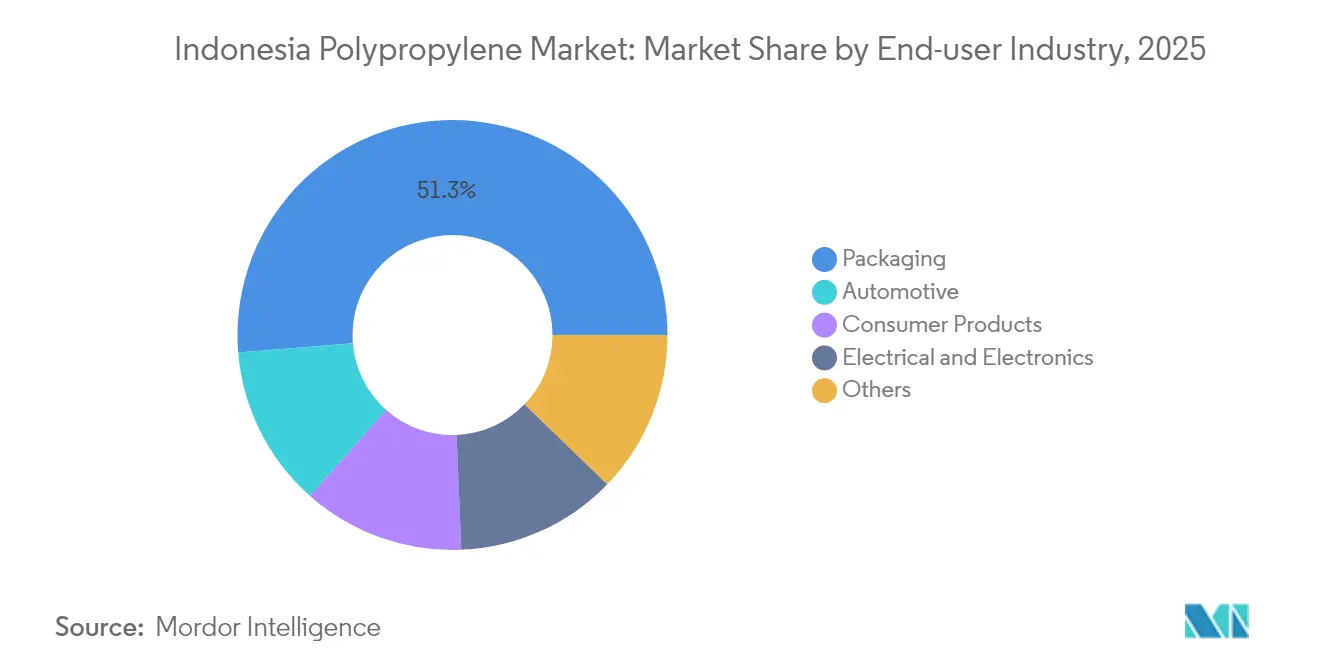

- By end-user industry, packaging accounted for 51.30% of the market in 2025. The market share of the automotive industry is expected to increase at a CAGR of 5.74% during the forecast period (2026-2031).

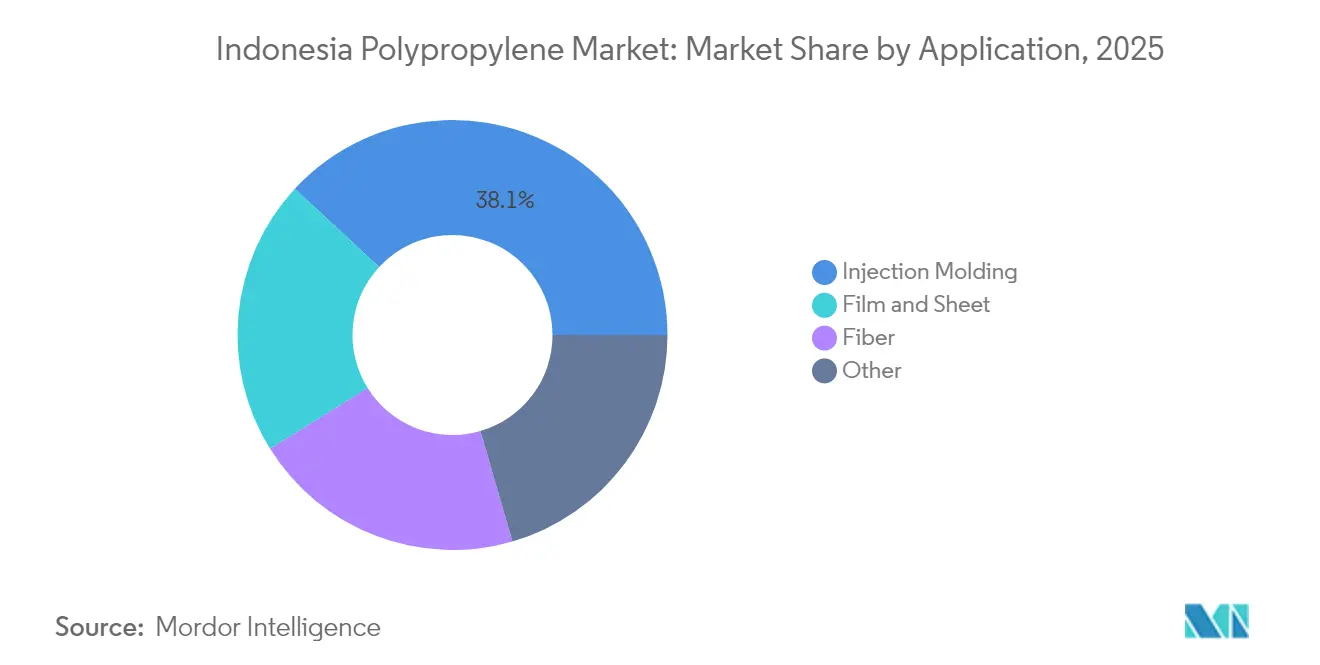

- By application, the market share of injection molding was 38.10% in 2025, and the share of film and sheet is expected to increase with a CAGR of 5.88% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Polypropylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in flexible-packaging demand from Indonesia's booming snack and FMCG sectors | +1.2% | National, concentrated in Java (Jakarta, Surabaya, Bandung) and Sumatra | Medium term (2-4 years) |

| Lightweighting push in domestic automotive OEM supply chains | +0.9% | National, with manufacturing clusters in Greater Jakarta, Karawang, and Bekasi | Long term (≥ 4 years) |

| Rapid build-out of e-commerce fulfillment networks needing durable tote and film solutions | +0.8% | National, early gains in Jakarta, Surabaya, Medan, and Makassar | Short term (≤ 2 years) |

| Local anti-dumping duties favoring domestic PP versus imports | +0.7% | National, affecting import flows from Korea, Vietnam, UAE, Malaysia, Singapore | Medium term (2-4 years) |

| Petrochemical integration at new Balikpapan refinery-to-PP complex | +1.1% | National, with supply-chain spillover to East Kalimantan and Sulawesi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Flexible-Packaging Demand

Snack and FMCG producers are redesigning multilayer sachets into recyclable mono-material films to comply with Regulation 75/2019 that mandates 100% recyclable packaging by 2029. Twenty-one food and beverage companies filed official roadmaps in 2024, and converters such as Dai Nippon Printing Indonesia launched mono-material polypropylene formats that replace 40 kilotons of difficult-to-recycle instant-noodle wrap each year[1]ChemOrbis Editorial Team, “Indonesia’s PP Market Dynamics Post-LINE Project,” chemorbis.com. Middle-class demand for convenient single-serve packs accelerates volume, and polypropylene’s balance of sealability, stiffness, and clarity makes it the preferred candidate over multilayer laminates. The Indonesia polypropylene market benefits as brand owners shift volumes to domestically produced homopolymer and random-copolymer film grades. New capacity in Cilegon shortens lead times for converters and tempers raw-material price risk.

Lightweighting Push in Domestic Automotive OEM Supply Chains

Vehicle assemblers produced 551,082 units in H1 2025 under a policy that requires 40% local content on finished vehicles. Polypropylene compounds reinforced with 30%–40% glass fiber deliver up to 40% weight savings over steel for liftgates and front-end modules while meeting crash standards. The Indonesia polypropylene market gains from this substitution because the material is sourced locally, reducing imported assemblies. Electric-vehicle incentives raise the value of mass reduction, and capacity expansions at Chandra Asri and Polytama Propindo supply homopolymer feedstock for compounding. OEM validation cycles indicate steady demand visibility for at least four model years.

Rapid Build-Out of E-Commerce Fulfillment Networks

Tokopedia data show that 68% of fashion SMEs adopted polyethylene or polypropylene polymailers in 2024 to cut shipping weight and improve parcel protection[2]Tokopedia Insights, “SME Fulfillment Survey 2024,” goodstats.id. Warehousing expansion in Jakarta, Surabaya, Medan, and Makassar requires millions of reusable totes, stretch-wrap, and woven sacks, all of which are polypropylene-intensive. The Indonesia polypropylene market therefore captures logistics-linked growth ahead of regional rivals. Superior tensile strength enables higher load factors compared to polyethylene, and domestic film extruders are scaling their co-extrusion lines to meet demand. Short delivery windows give a tactical edge to resin produced within the archipelago.

Local Anti-Dumping Duties Favoring Domestic PP Versus Imports

The Ministry of Trade imposed anti-dumping duties on imports of copolymers from South Korea, Vietnam, the UAE, Malaysia, and Singapore in 2024. Duties align with the October 2025 start-up of Lotte Chemical’s 350 kiloton line, redirecting procurement toward domestic sellers and narrowing historical reliance on imports that once met 65% of demand. International producers now face squeezed margins, while converters secure stable volumes without foreign-exchange risk. The Indonesia polypropylene market thus pivots to local feedstock, reinforcing recent investment cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from PET and rPET in beverage and pouch formats | -0.6% | National, particularly Java and Bali where beverage consumption is highest | Medium term (2-4 years) |

| Volatile naphtha feedstock costs versus ethane-advantaged imports | -0.8% | National, affecting all naphtha-fed crackers and import economics | Short term (≤ 2 years) |

| Intensifying plastics-waste regulation in Jakarta and Bali provinces | -0.5% | Regional, with Jakarta and Bali enforcement leading national rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from PET and rPET in Beverage and Pouch Formats

Indonesia consumed 1 million tons of PET in 2024, and leading beverage brands committed to using 100% recycled PET bottles, reinforcing PET’s dominance in transparent applications. Higher collection rates and a 2.5 million-ton recycling infrastructure favor PET when producers must hit 50% recycled-content targets by 2029. For the Indonesia polypropylene market, this trend reduces penetration in premium beverage and high-barrier pouch categories. Converters are forced to differentiate based on rigidity and heat performance rather than clarity.

Volatile Naphtha Feedstock Costs Versus Ethane-Advantaged Imports

Asian naphtha traded USD 17 per barrel higher in April 2025 than a year earlier, widening the cost gap with ethane-rich producers in the Middle East and North America. Domestic crackers in Cilegon and Anyer rely on naphtha, so local resin pricing mirrors crude swings. Elevated feedstock costs tighten margins just as the Indonesia polypropylene market adds capacity. Although refinery integration at Balikpapan will cut propylene import bills, near-term volatility challenges profitability and may delay specialty-grade upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Homopolymer Dominates on Cost-Performance Balance

Homopolymer captured 69.45% of the Indonesia polypropylene market share in 2025 and is forecast to grow at a 5.59% CAGR through 2031, reflecting its low cost and high stiffness in injection-molded automotive and rigid-packaging parts. The Indonesia polypropylene market size for homopolymer is predicted to reach 1.76 million tons by 2031, aided by Lotte Chemical’s new line that mainly targets general-purpose grades. Domestic converters gain security of supply and faster order cycles, aligning with TKDN local-content rules.

Copolymer serves caps, closures, and impact-modified films that require flexibility or clarity. Anti-dumping duties on copolymer imports have curtailed volume growth; however, the adoption of mono-material film under EPR rules is reviving interest. In the medium term, success depends on local producers upgrading reactors to random- and impact-copolymer capability.

By End-User Industry: Automotive Outpaces Packaging Growth

Packaging retained 51.30% demand in 2025, powered by snacks, beverages, and household-care goods that favor polypropylene containers and films. The Indonesia polypropylene market size for packaging is expected to rise as mono-material films replace multilayer laminates.

Automotive demand, however, is projected to post the fastest 5.74% CAGR to 2031. The polypropylene content per vehicle increases as OEMs substitute metal with glass-fiber-reinforced compounds to meet efficiency targets. Domestic resin advances enhance supply transparency, providing Tier-1 molders with the confidence to localize parts that were previously assembled in Thailand or China.

By Application: Film and Sheet Gains on E-Commerce Logistics

Injection molding contributed 38.10% in 2025. Film and sheet are set to overtake it by 2031 as polymailers, stretch-wrap, and mono-material food films proliferate across fulfillment and retail channels. The Indonesia polypropylene market size for film and sheet is projected to reach 522 kilotons in 2031.

Fiber applications in woven sacks, geotextiles, and non-woven fabrics show steady uptake alongside infrastructure expansion in Kalimantan and Sumatra. Government road-building and coastal-protection projects specify polypropylene geotextiles for durability and chemical resistance, supporting specialized fiber lines in Java.

Geography Analysis

Java remains the consumption epicenter, anchored by automotive assembly plants in Greater Jakarta and large FMCG processing zones in Surabaya and Bandung. Cilegon’s integrated complex supplies resin by pipeline, cutting transport costs that once burdened import-dependent processors. The Indonesia polypropylene market benefits from just-in-time deliveries that reduce converter working capital.

Sumatra and Kalimantan are next-wave growth fronts. Plantation agriculture and mining increase demand for woven sacks, geomembranes, and heavy-duty films. Pertamina’s USD 7.4 billion Balikpapan integration promises 225 kilotons of propylene, re-balancing supply away from Java and shortening lead times in eastern provinces.

Bali and Nusa Tenggara consume less resin but enact the toughest single-use-plastic bans, spurring rapid converter innovation. Compliance pressure creates an incubator for mono-material solutions that later scale nationwide. Overall, regional diversification mitigates logistics risk and encourages investment in satellite compounding and recycling hubs, deepening the Indonesia polypropylene market.

Competitive Landscape

The Indonesia Polypropylene Market is highly concentrated. PT Chandra Asri Petrochemical, Lotte Chemical Indonesia, and Polytama Propindo collectively control the majority of domestic capacity, yet international firms maintain a strong foothold in specialty resins. Chandra Asri’s acquisition of Shell’s Singapore cracker secures upstream feedstock and positions the firm to capture value-chain margins. Lotte Chemical’s Cilegon complex pushes Indonesia toward 90% ethylene self-sufficiency, underpinning polypropylene cost competitiveness.

Indonesia Polypropylene Industry Leaders

Exxon Mobil Corporation

LG Chem

Chandra Asri Group

PT Polytama Propindo

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: LOTTE Chemical inaugurated its new facility, LOTTE Chemical Indonesia (LCI), located in Cilegon, Indonesia. This petrochemical complex is expected to produce various products annually, including 520,000 tons of propylene and 350,000 tons of polypropylene, among others.

- February 2025: The Indonesian Anti-Dumping Committee (KADI) proposed the imposition of anti-dumping duties (ADDs) on the imports of polypropylene (PP) copolymer from five origins. The affected exporters are from South Korea, Singapore, Malaysia, Vietnam, and the United Arab Emirates. This could boost the local Indonesian Polypropylene market.

Indonesia Polypropylene Market Report Scope

Polypropylene (PP) is a tough, rigid, crystalline thermoplastic made by polymerizing propylene. It is made from propene (or propylene) monomer. Polypropylene is often classified as a commodity plastic because its primary use is in packaging products such as bags and bottles.

The Indonesian polypropylene market is segmented by type, end-user industry, and application. By type, the market is segmented into homopolymer and copolymer. By end-user industry, the market is segmented into packaging, electrical and electronics, automotive, consumer products, and others. By application, the market is segmented into injection molding, fiber, film and sheet, and others.

By Type

| Homopolymer |

| Copolymer |

By End-user Industry

| Packaging |

| Automotive |

| Consumer Products |

| Electrical and Electronics |

| Others |

By Application

| Injection Molding |

| Fiber |

| Film and Sheet |

| Other |

| By Type | Homopolymer |

| Copolymer | |

| By End-user Industry | Packaging |

| Automotive | |

| Consumer Products | |

| Electrical and Electronics | |

| Others | |

| By Application | Injection Molding |

| Fiber | |

| Film and Sheet | |

| Other |

Key Questions Answered in the Report

How large is the Indonesia polypropylene market today?

The Indonesia polypropylene market size reached 1.93 million tons in 2026 and is forecast at 2.51 million tons by 2031.

What is the expected CAGR for polypropylene demand in Indonesia?

Total demand is projected to grow at a 5.38% CAGR between 2026 and 2031.

How are anti-dumping duties affecting domestic supply?

Duties on copolymer imports from five countries redirect procurement toward local resin and strengthen domestic producers’ pricing power.

What role does automotive lightweighting play in polypropylene demand?

Automotive parts built with glass-fiber-reinforced polypropylene are growing at 5.74% CAGR as OEMs chase weight reduction and TKDN compliance.

Page last updated on: