Bio-based Polypropylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

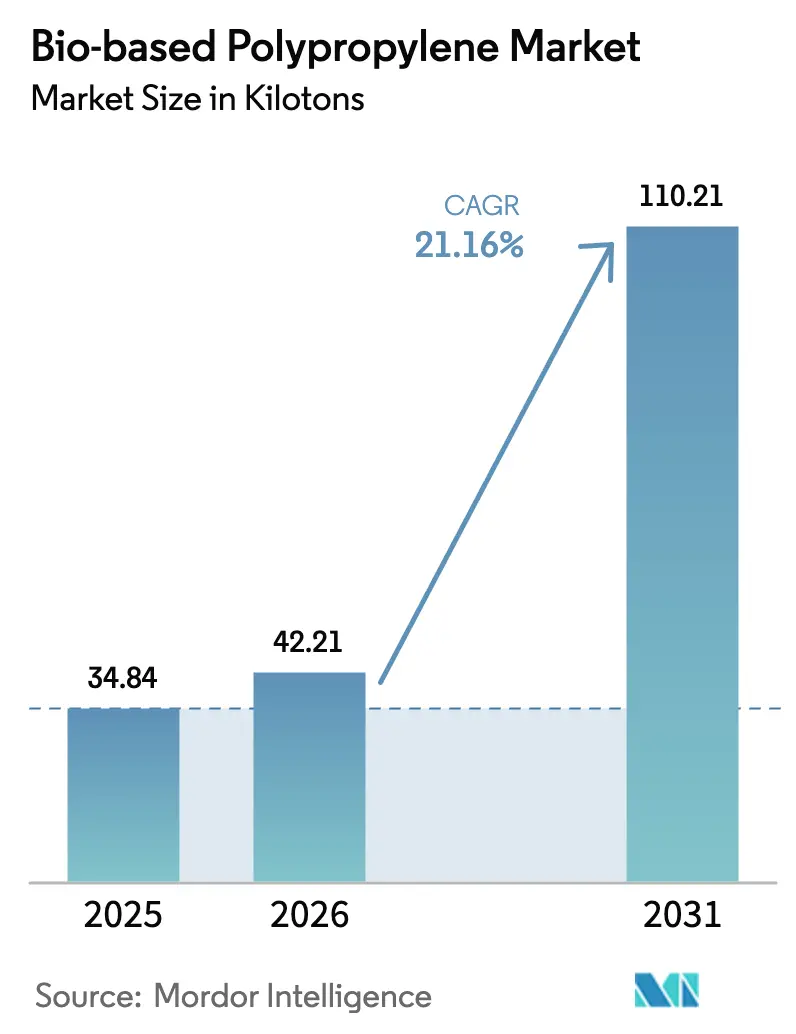

| Market Volume (2026) | 42.21 kilotons |

| Market Volume (2031) | 110.21 kilotons |

| Growth Rate (2026 - 2031) | 21.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-based Polypropylene Market Analysis by Mordor Intelligence

The Bio-based Polypropylene Market size was valued at 34.84 kilotons in 2025 and is estimated to grow from 42.21 kilotons in 2026 to reach 110.21 kilotons by 2031, at a CAGR of 21.16% during the forecast period (2026-2031). This expansion is propelled by mandatory recycled-content rules in the European Union, a global pivot toward mass-balance certification, and rapid adoption by automotive OEMs seeking lightweight solutions that dovetail with net-zero pathways. Brand owners value the seamless integration of renewable feedstock into existing conversion assets, which eliminates retooling downtime while still delivering compelling carbon-footprint improvements. Automotive firms such as BMW and Volvo are piloting bio-based grades to satisfy stringent Scope 3 emissions metrics, while polymer producers leverage cracker networks and ISCC Plus allocation to scale volumes without the capital intensity of dedicated bio-monomer plants. Synergistic demand also flows from fast-moving consumer goods (FMCG) companies that are harmonizing flexible-packaging designs around mono-material structures to boost recyclability and unlock compliance credits.

Key Report Takeaways

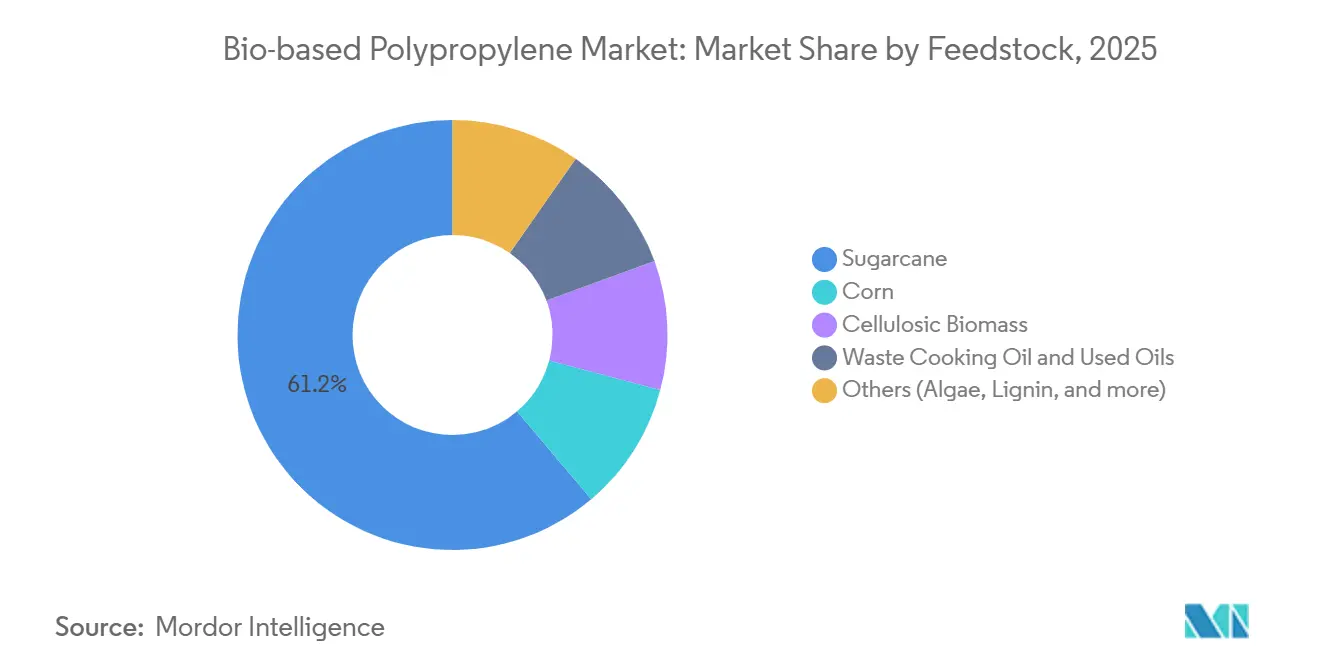

- By feedstock, sugarcane contributed 61.17% share of the bio-based polypropylene market size in 2025, whereas cellulosic biomass is set to expand at 25.21% CAGR between 2026-2031.

- By product type, homopolymer commanded 57.89% share in 2025, yet impact copolymer is poised for 23.78% CAGR growth through 2031.

- By application, injection molding held 66.12% of the bio-based polypropylene market share in 2025 and is forecast to grow at a 22.89% CAGR through 2031.

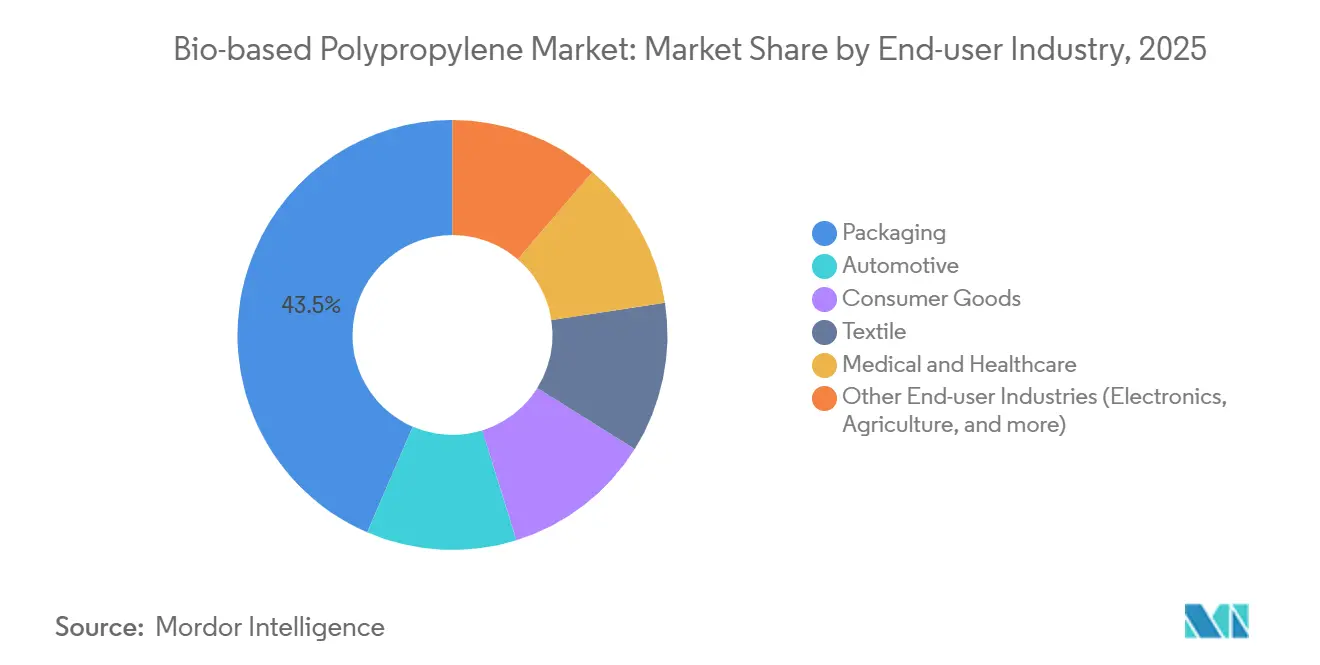

- By end-user industry, packaging accounted for 43.51% revenue share in 2025, while automotive is projected to advance at 23.45% CAGR to 2031.

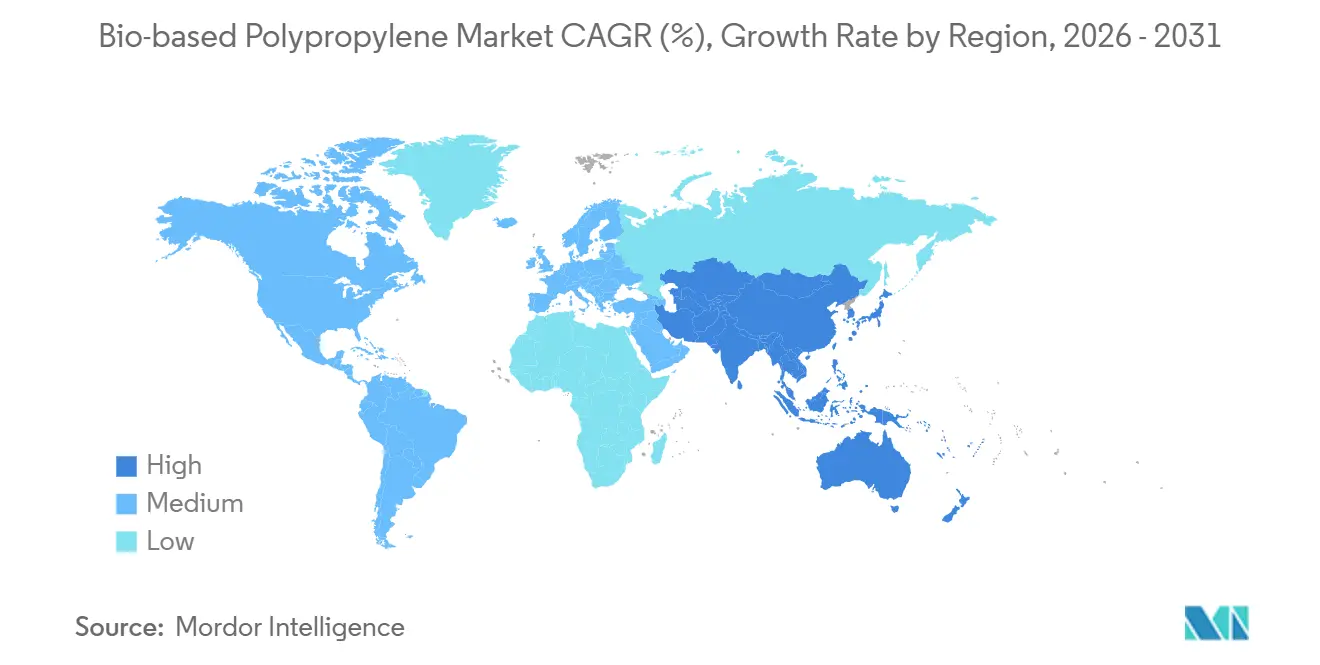

- By geography, Asia-Pacific led with 41.28% market share in 2025 and is expected to post the fastest regional CAGR of 24.71% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bio-based Polypropylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU recycled-content mandates | +4.8% | Europe, spillover to North America | Medium term (2-4 years) |

| Automotive lightweighting & net-zero targets | +5.2% | Global, focus on Europe, North America, Japan, South Korea | Medium term (2-4 years) |

| FMCG migration to mono-PP flexible films | +3.9% | Global | Short term (≤ 2 years) |

| 3-D printing for medical prototypes | +2.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| ISCC-Plus pallets in shipping | +1.7% | Global, early Europe & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

European Union Strict Packaging Recycled-Content Mandates Spur Rigid Bio-PP Demand

The Packaging and Packaging Waste Regulation that came into force in February 2025 obligates all plastic packaging sold in the bloc to achieve 30% recycled content by 2030 and 50%-65% by 2040[1]Packaging and Packaging Waste Regulation, “Regulation (EU) 2024/825,” EUROPARL.EUROPA.EU. A carve-out enables bio-based feedstock to count toward these thresholds until viable food-grade recycling technology is commercialized, a clause that the Commission will review by February 2028. Rigid polypropylene tubs, caps, and crates, therefore, gain a regulatory “insurance policy,” prompting retailers to line up mass-balance-certified supply ahead of enforcement. The Regulation simultaneously bans PFAS in food-contact formats, nudging grease-resistant use-cases formerly dominated by fluorinated coatings toward bio-attributed polypropylene grades. Multinationals are thus front-loading procurement contracts to hedge against compliance risk.

Automotive OEM Lightweighting and Net-Zero Commitments

BMW targets 40% recycled content in thermoplastics by 2030 and is piloting bio-based polypropylene door panels and instrument clusters that slot into extant molds without requalification[2]BMW Group, “Sustainability Report 2025,” BMWGROUP.COM. Volvo plans 30% recycled plastics across its fleet by 2030, assigning renewable polypropylene to interior trim parts to preserve crash-worthiness. Ford received a USD 2.5 million US DOE grant to advance CO₂-to-polyol chemistry that could dovetail with bio-attributed propylene derivatives. Borealis counters with Bornewables compounds that deliver up to 100% renewable content via ISCC Plus allocation, while Lignin Industries’ Renol nucleating agent trims part weight by 10% and cycle time by 30% in injection-molded copolymers.

Global FMCG Shift to Mono-PP Flexible Films

Nestlé invested GBP 1.5 billion to secure food-grade recycled polypropylene and is concurrently developing bio-based wrappers for confectionery and pet food. Unilever trimmed virgin-plastic use by 21.3% as of 2024 and is redesigning pouches and sachets into mono-polypropylene laminates that meet recyclability benchmarks. These packs require higher heat-seal strength and barrier attributes, opening headroom for premium bio-attributed resin grades that can command a modest price lift where consumer willingness to pay remains robust. Because mechanical recycling of multi-layer films still lags, brand owners view renewable feedstock as a stop-gap lever that offers tangible carbon savings independent of post-consumer collection rates.

Rapid Growth of 3-D Printing in Medical Prototyping (Bio-PP Filaments)

Medical-device engineers increasingly specify bio-based polypropylene filaments for iterative prototyping of syringe hubs, inhaler bodies, and diagnostic housings that must survive autoclave sterilization cycles above 121°C. Polypropylene’s chemical resistance outperforms PLA or ABS in harsh cleaning regimens, and its documented biocompatibility streamlines US FDA 510(k) clearances when material properties mirror predicate devices. Japan’s Green Innovation Fund specifically earmarks grants for medical polymers, underscoring long-term demand traction. Although filament prices sit 20%-50% above fossil equivalents, cost sensitivity is muted in concept stages where material volumes remain modest.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Production cost premium vs. fossil PP | -3.4% | Global | Short term (≤ 2 years) |

| Lower heat-deflection temperature | -1.8% | Europe, North America, Japan | Medium term (2-4 years) |

| Absence of unified certification in MENA | -1.2% | Middle-East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Production Cost Premium vs. Fossil PP

Bio-based polypropylene trades at a 20%-50% premium because feedstock logistics, hydro-processing, and small-scale dehydration units add fixed costs that legacy naphtha crackers amortized decades ago. Neste’s Singapore complex produces 1.3 million t/y renewable hydrocarbons from waste cooking oil, yet collection and pre-treatment inflate delivered cost relative to fossil naphtha. LyondellBasell passes these differentials through its Circulen Plus line, limiting penetration to customers who can book carbon savings against corporate targets. Cellulosic pathways require enzymatic hydrolysis and multi-step catalysis, pushing capex 40% above first-generation sugarcane ethanol. Consequently, bio-attributed grades concentrate in high-value applications where sustainability differentiation outweighs margin erosion.

Lower Heat-Deflection Temperature Limits Under-Hood Use

Unfilled bio-based homopolymers soften at 90°C-110°C, below the 150°C benchmark for coolant reservoirs and air-intake manifolds. Glass-fiber reinforcement can lift thresholds to 160°C, but higher density offsets weight savings. Renol nucleators add 5°C-8°C, yet even that leaves a performance gap. As a result, OEM adoption focuses on interior panels, consoles, and trim where peak temperatures remain under 100°C. Borealis Fibremod grades meet the thermal targets when reinforcement is above 30 wt%, although biomass fraction declines accordingly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Cellulosic Pathways Challenge Sugarcane Dominance

Sugarcane accounted for 61.17% of the bio-based polypropylene market in 2025, owing to Brazil’s mature ethanol chain, but cellulosic inputs are forecast to register a 25.21% CAGR as enzyme economics improve. Sugarcane mills supply monohydrate ethanol that is dehydrated to ethylene and oligomerized to propylene in Europe under ISCC Plus allocation. The bio-based polypropylene market size derived from sugarcane is therefore expected to rise steadily, yet its overall proportional share will erode as agricultural residues scale.

Cellulosic residues such as corn stover, wheat straw, and bagasse lower indirect land-use change risk and qualify for additional sustainability credits, positioning them to capture incremental volume in North America and China. LanzaTech blends gas-fermentation ethanol with catalytic upgrading, while Neste processes waste oils and fats that bypass fermentation altogether. Feedstock diversification de-risks supply shocks and stabilizes the bio-based polypropylene market, yet long-haul transport of low-density residues still taxes delivered cost outside integrated agro-industrial hubs.

By Product Type: Impact Copolymers Gain in Automotive

Homopolymers held a 57.89% share of the bio-based polypropylene market size in 2025, favored for rigid containers and closures requiring stiffness and clarity. Impact copolymers are expected to grow at a 23.78% CAGR through 2031 because automotive door panels, glove boxes, and side-claddings demand high toughness at sub-zero temperatures. The bio-based polypropylene market share attributed to impact copolymers will thus widen as OEMs integrate Scope 3 metrics in design briefs.

Random copolymers trail owing to head-to-head competition with polyethylene in films, yet FMCG brand owners are shifting confectionery wrappers to mono-polypropylene structures, which could resurrect demand. Borealis, SABIC, and LyondellBasell have launched random-copolymer grades with tailored seal-initiation temperatures that align with high-speed horizontal form-fill-seal equipment. Medical-device housings now specify random-copolymer bio-based polypropylene to pair clarity with autoclave resistance, a niche that commands price premiums sufficient to absorb feedstock surcharges.

By Application: Injection Molding Dominates, Films Lag Polyethylene

Injection molding represented 66.12% of the bio-based polypropylene market volume in 2025, and the segment is forecast at 22.89% CAGR to 2031. Lightweight crates, beverage caps, and instrument clusters continue to underpin volume as processors retrofit nozzles and hot runners to accommodate marginally lower melt-flow indices. Films lag because polyethylene still owns commodity flexible packaging; however, confectionery liners and retort pouches that need elevated barrier properties are adopting random-copolymer bio-grades.

The bio-based polypropylene market size captured by textiles remains modest, yet nonwoven diaper backsheets and geotextiles offer steady pull-through as retailers push for lower-carbon labeling. Extrusion blow-molding of canisters and drums benefits from drop-in substitution at par processing pressures, though lower impact strength in unfilled bio-homopolymers tempers broader penetration. Brand owners balance mechanical performance against storytelling value, selectively applying bio-attribution to hero SKUs to maximize marketing reach.

By End-User Industry: Automotive Overtakes Packaging Growth

Packaging contributed 43.51% of demand in 2025 and will continue to generate the largest absolute volume through 2031. Nevertheless, automotive is projected to outpace all end uses with a 23.45% CAGR, lifting its share of the bio-based polypropylene market as cabin components undergo renewable content audits. OEMs favor mass-balance allocation because it avoids tooling upheaval and keeps color-matching within acceptable tolerances.

Consumer-goods manufacturers adopt bio-attributed polypropylene for durable housewares and personal-care packaging that require chemical resistance superior to PET. Textiles and hygiene absorb moderate tonnage through nonwoven backsheet fabrics, yet full commercial scale hinges on cost parity with fossil sources. Medical and healthcare applications gain from identical sterilization cycles and regulatory familiarity, but adoption cadence remains tied to 510(k) review queues at the FDA.

Geography Analysis

Asia-Pacific contributed 41.28% of the global bio-based polypropylene market volume in 2025 and is forecast to climb at a 24.71% CAGR to 2031. China’s 14th Five-Year Plan earmarks bio-based materials as a strategic pillar, while India’s single-use plastic ban seeds domestic demand for renewable polymers. Japan’s Green Innovation Fund and South Korea’s K-Circular Economy Plan inject grant capital across pilot plants, expanding regional feedstock diversity.

Europe remains the compliance bellwether. The Packaging and Packaging Waste Regulation codifies 30% recycled content by 2030 but explicitly allows bio-based substitution, ensuring continued import demand for ISCC-Plus grades. North America benefits from the Inflation Reduction Act and Clean Fuel Regulations, underwriting automotive trials and cradle-to-gate carbon tracking. South America leverages Brazil’s sugarcane-ethanol backbone yet lacks the demand breadth seen in Asia. The Middle East and Africa add incremental supply but confront certification barriers that impede entry into premium import markets.

Regulatory Landscape

In the European Union, the Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40) entered into force on 11 February 2025 and applies generally from 12 August 2026. It tightens compliance expectations for packaging placed on the EU market and raises the bar for auditable claims around renewable and circular inputs. PPWR also sets a framework for harmonized presentation of bio-based content information when companies choose to communicate it, while the European Commission is tasked to assess whether EU-wide definitions can support certification and scaling of bio-based polymers, keeping policy attention on standardized substantiation rather than marketing language.

Globally, verification is supported by recognized test and calculation standards, including ASTM D6866 (updated 1 May 2026) for radiocarbon-based measurement of bio-based carbon content and ISO 16620 (parts 1 and 2) for determining and reporting bio-based content in plastics. Alongside PPWR, the European Commission scheduled adoption of a Circular Economy Act for 2026 and launched pilot actions in January 2026 aimed at accelerating circular economy measures in plastics, including work on end-of-waste implementing acts and market monitoring. Together, these steps underpin broader uptake of traceable, certified supply chains for bio-attributed polypropylene.

Value Chain Analysis

The bio-based polypropylene value chain begins with renewable feedstock sourcing and recovery, such as corn-based ethanol, green methanol, and used cooking oils. It then moves through precursor conversion into olefins (ethanol-to-olefins or methanol-to-olefins routes) and polymerization into drop-in PP resins, with mass-balance certification commonly used to allocate renewable content through existing petrochemical assets. Downstream, resin distribution runs through traders and compounders to converters, including injection molders, film extruders, and nonwovens producers, before reaching brand owners and OEMs in packaging, automotive interiors, and consumer goods.

Key bottlenecks involve synchronizing regional feedstock availability, conversion capacity, and committed demand, since projects require coordinated build-out across multiple stages. Recent announcements show participants reducing chain risk through long-term commercial commitments and technology selection: Citroniq announced a 15-year binding offtake with Premier Product Marketing (a Vinmar company) covering 50% of planned output for its Nebraska facility, while Vioneo selected Lummus Technology Novolen PP technology for a green-methanol-based plant in Antwerp. Blue Circle Olefins also partnered with Ducor Petrochemicals to establish a methanol-to-olefins-based circular PP value chain at the Port of Rotterdam.

Competitive Landscape

The Bio-based Polypropylene market is highly concentrated. Borealis, SABIC, and LyondellBasell combine cracker infrastructure with ISCC Plus accounting, yielding integrated cost advantages and swift commercial turnarounds. TotalEnergies and Braskem pursue dual tracks of circular and bio-based polymers, diversifying portfolios to hedge regulatory outcomes. Strategic moves in 2025 included Borealis extending Bornewables up to 100% renewable content, LyondellBasell scaling Circulen Plus grades with Neste hydrocarbons.

Bio-based Polypropylene Industry Leaders

Braskem

SABIC

LyondellBasell Industries Holdings B.V.

Borealis GmbH

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The main opportunity is scaling certified, drop-in bio-attributed polypropylene that can fit existing converting lines for packaging and automotive interiors. Customers are looking for defensible renewable-content and carbon-accounting attributes without retooling. This direction is supported by active industrial investments and commercialization steps, including Borealis producing certified renewable polypropylene at its Kallo and Beringen sites in Belgium using ISCC Plus certified renewable feedstock from Neste, which supports volume growth via existing assets rather than dedicated bio-monomer plants.

Greenfield and non-fossil carbon routes also create whitespace for new supply hubs tied to long-term offtake and technology partners, especially in regions seeking domestic supply security for sustainable polymers. Examples include Citroniq's Nebraska project using corn-based ethanol, paired with a 15-year binding offtake with Premier Product Marketing (Vinmar) covering half of planned capacity, and Vioneo's selection of Lummus Novolen technology for a large-scale green-methanol-to-polypropylene project in Antwerp. These developments broaden procurement options for brand owners and OEMs that are standardizing on mass-balance certification and mono-material PP designs, reinforcing demand for consistent, auditable renewable feedstock allocation across global supply chains.

Recent Industry Developments

- June 2026: Borouge International introduced bio-based versions of polypropylene grades for drinking water and irrigation, including grade BA160E-8229-01 with 10% certified bio-based feedstock. This extends renewable-attributed PP beyond packaging into infrastructure-linked applications that require reliability and compliance documentation. The launch also signals broader commercialization of certified feedstock allocation for application-specific PP grades.

- September 2025: LyondellBasell partnered with Futamura Chemical and Iwatani to integrate its bio-based polypropylene into packaging for Shiseido in Japan. The collaboration connects certified renewable resin supply with high-visibility consumer packaging, supporting brand-owner sustainability targets without changing converting equipment. It also strengthens demand pull for mass-balance-certified PP in Asia-Pacific premium packaging value chains.

- September 2024: Braskem America launched WENEW bio-circular polypropylene derived from used cooking oil for restaurant and snack food packaging. The product positioned UCO as a scalable circular feedstock route for PP applications that need food-service performance attributes. It also widened the competitive set of renewable/circular PP offerings available to packaging converters seeking drop-in materials.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the bio-based polypropylene market covers virgin bio-PP resin produced from renewable feedstocks and sold as a drop-in alternative to conventional polypropylene across common converting routes and end uses.

Scope exclusions: We exclude pilot-scale material and blends where bio-PP is mixed with fossil polymers and sold as a compounded or hybrid product.

Segmentation Overview

- By Feedstock

- Sugarcane

- Corn

- Cellulosic Biomass

- Waste Cooking Oil and Used Oils

- Others (Algae, Lignin, etc.)

- By Product Type

- Homopolymer

- Random Copolymer

- Impact Copolymer

- By Application

- Injection Molding

- Films

- Textiles

- Other Applications (Foams, Blow Molding, Extrusion Coating)

- By End-user Industry

- Packaging

- Automotive

- Consumer Goods

- Textile

- Medical and Healthcare

- Other End-user Industries (Electronics, Building and Construction, Agriculture)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a clear fact base on bio-based feedstocks, polymer certification, and the broader polypropylene demand backdrop before the model was finalized. We referenced public sources such as trade and production statistics from agencies like the US International Trade Commission, Eurostat, and UN Comtrade, along with sustainability and certification guidance published by bodies such as ISO and recognized mass-balance programs.

To keep the assumptions realistic, we also reviewed sources such as SEC filings and investor presentations, technical papers in polymer journals, and association or conference publications that discuss resin pricing and adoption constraints. In a few places, paid subscriptions for company financials and patent databases were used to cross-check capacity announcements and technology claims. The sources listed here are illustrative, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where bio-PP is actually being adopted, what premium levels are being accepted, and how certification rules affect what is counted as bio-based material in commercial trade. We spoke with a mix of resin producers, converters, brand-side sustainability teams, and distribution participants across APAC, EMEA, and the Americas to pressure-test demand signals and close gaps that desk research could not cover directly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 19% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where polypropylene demand signals and bio-based penetration assumptions were used to reconstruct the bio-PP demand pool by region, followed by checks against supply-side realities. To keep the totals practical, we corroborated outputs with selective bottom-up approximations such as sampled volume by application, typical price premiums, and channel feedback on available grades, and then adjusted the model where the pieces did not align.

Key inputs included announced and effective nameplate capacity for bio-PP, certification-related allocation practices that influence what can be marketed as bio-attributed, adoption rates in packaging and durable goods, the spread between bio-PP and fossil PP prices, and regional trade flows for relevant intermediates and resins where these were visible in official datasets. Forecasting leaned on scenario analysis supported by expert consensus, since policy moves, corporate commitments, and feedstock economics can shift adoption faster than a simple time series would suggest. Where direct volume visibility was limited, we used bounded ranges tied to capacity utilization and realistic ramp-up curves, and then narrowed them through interview feedback.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including capacity timelines, import and export patterns, and observed premium ranges, and then outliers were reviewed before internal sign-off. When a number did not fit the surrounding evidence, we revisited the assumptions and, where needed, re-contacted respondents to confirm what changed.

Reports are refreshed annually, and interim updates are made when material events occur such as major capacity starts, policy changes, or certification rule updates. Before delivery, an analyst performs a final pass to make sure the latest publicly available information is reflected consistently in the model.

Mordor Intelligence's Bio Based Polypropylene Market Size Measured Against Other Published Estimates

Published market sizes for bio-based polypropylene often differ because authors pick different counting rules, units, and conversion choices, and those decisions can move the final number even when the growth story is similar. The spread is also influenced by how quickly assumptions are refreshed when new capacity starts, price premiums change, or certification practices shift.

A common gap driver is whether the estimate is presented in volume or converted into USD using a fixed average selling price, since early-stage bio-PP pricing can swing with feedstock costs and fossil PP reference prices. Currency timing matters too, because an average annual rate versus a spot conversion can change the headline value, especially when the base year is close to a volatile period. Because the 2025 and 2026 volumes are updated with data as of January 2026 and then translated with current-year pricing checks, the conversion step is handled more tightly by Mordor Intelligence than in approaches that rely on older ASP ladders or broad polymer price baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.17 B (2025) | |

| Global Consultancy A | USD 0.17 B (2025) | Reports a value figure without making the volume-to-USD conversion logic fully transparent, so differences can arise from the assumed bio-PP premium and the PP reference price series used. |

| Industry Publisher B | USD 0.06 B (2025) | Uses a narrower commercialization view that can undercount certified mass-balance volumes and may apply conservative ramp-up and pricing assumptions for early-stage supply. |

The table shows that the biggest differences come from conversion choices and what is treated as commercially countable bio-PP in the base year. By keeping the sizing traceable to demand signals, capacity reality checks, and explicitly refreshed pricing inputs, our estimate stays easier to reconcile when buyers compare numbers across sources.

Key Questions Answered in the Report

What volume growth is bio-based polypropylene expected to record between 2026 and 2031?

Global demand is projected to rise from 42.21 kilotons in 2026 to 110.21 kilotons by 2031, a 21.16% CAGR.

Which region is predicted to add the most incremental bio-based polypropylene tonnage by 2031?

Asia-Pacific, supported by China’s 14th Five-Year Plan and India’s single-use plastic ban, is forecast as the largest contributor.

How does the European Union regulation affect rigid bio-based polypropylene packaging

How does the European Union regulation affect rigid bio-based polypropylene packaging?

Why are automotive original equipment manufacturers adopting renewable polypropylene in interior components

Why are automotive original equipment manufacturers adopting renewable polypropylene in interior components?

What is the most significant technical restraint for under-hood automotive applications

Unfilled bio-based homopolymers soften below 110°C, necessitating reinforcement or nucleation to reach the 150°C threshold typical for engine-bay parts.

Page last updated on: