Circular Polymers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

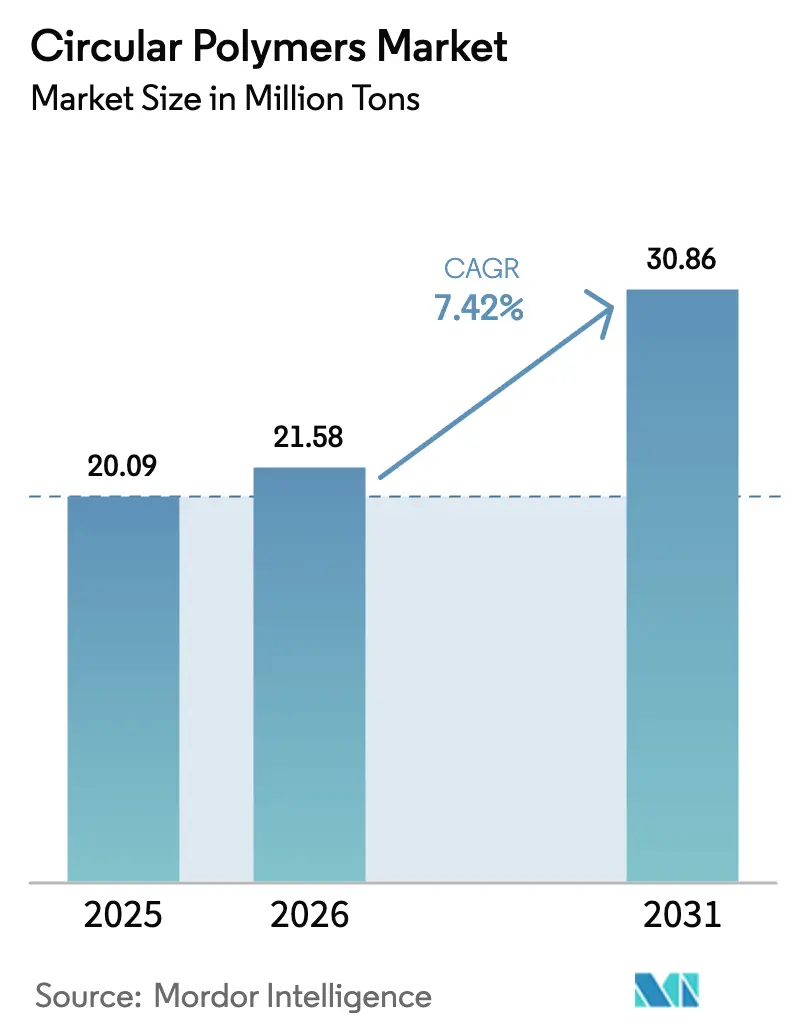

| Market Volume (2026) | 21.58 Million tons |

| Market Volume (2031) | 30.86 Million tons |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

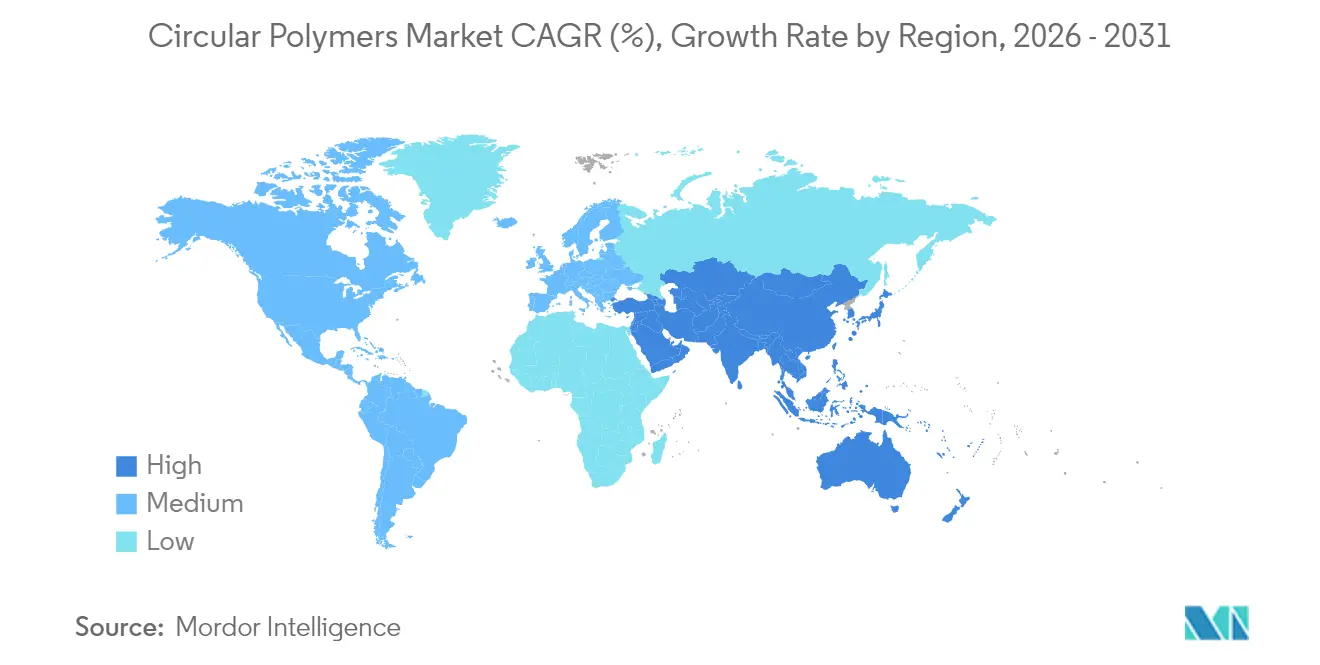

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circular Polymers Market Analysis by Mordor Intelligence

The circular polymers market size is expected to grow from 20.09 million tons in 2025 to 21.58 million tons in 2026 and is forecast to reach 30.86 million tons by 2031 at 7.42% CAGR over 2026-2031. The expansion reflects a global pivot from linear disposal models toward closed-loop value chains that reclaim polymers through mechanical and chemical recycling. Mandatory recycled-content thresholds, especially the European Union requirement for 30% recycled PET in beverage bottles by 2030, are reshaping procurement strategies. Advanced recycling that converts previously non-recyclable streams into near-virgin feedstock is narrowing the cost gap with primary resins. Investment surges, such as TotalEnergies’ Grandpuits platform and LyondellBasell’s Knapsack hub, signal mounting confidence in the circular polymers market. Asia-Pacific’s accelerating capacity build-out complements Europe’s mature infrastructure, ensuring feedstock availability and diversified growth pathways for the circular polymers market.

Key Report Takeaways

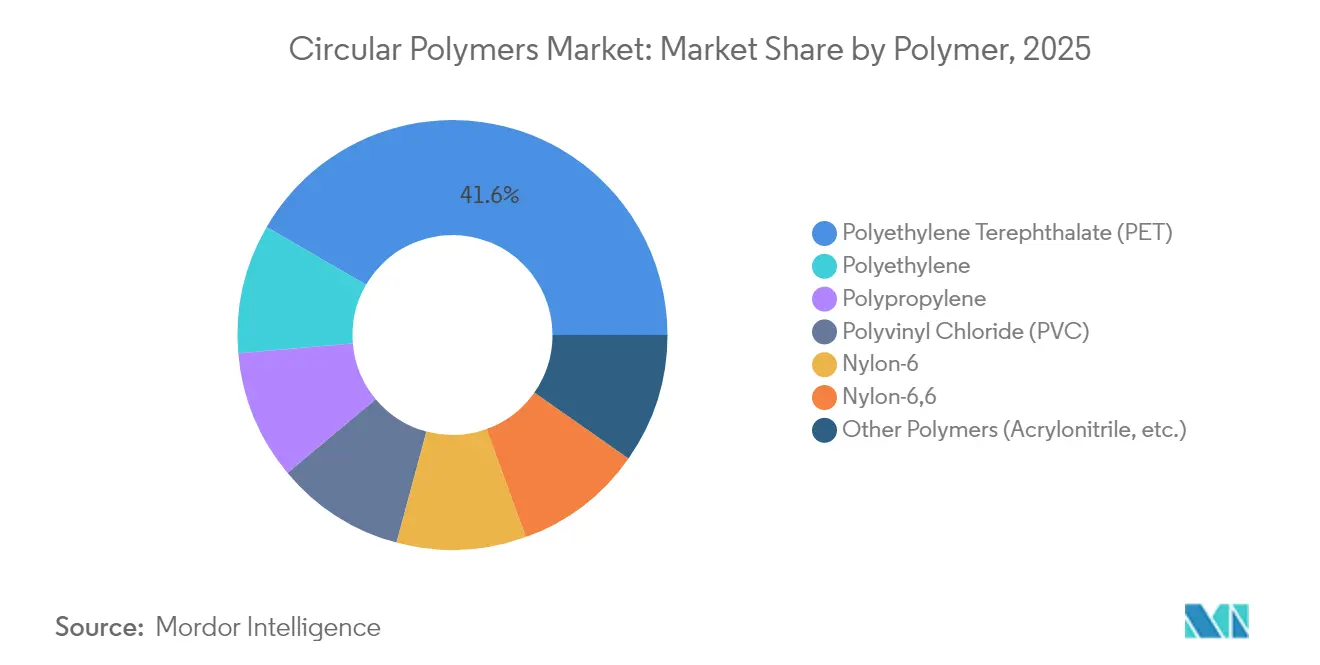

- By polymer, PET led with 41.62% of the circular polymers market share in 2025, while Nylon-6 is projected to expand at an 8.37% CAGR to 2031.

- By recycling technology, mechanical recycling held 64.35% of the circular polymers market share in 2025, whereas chemical recycling is forecast to rise at an 8.29% CAGR to 2031.

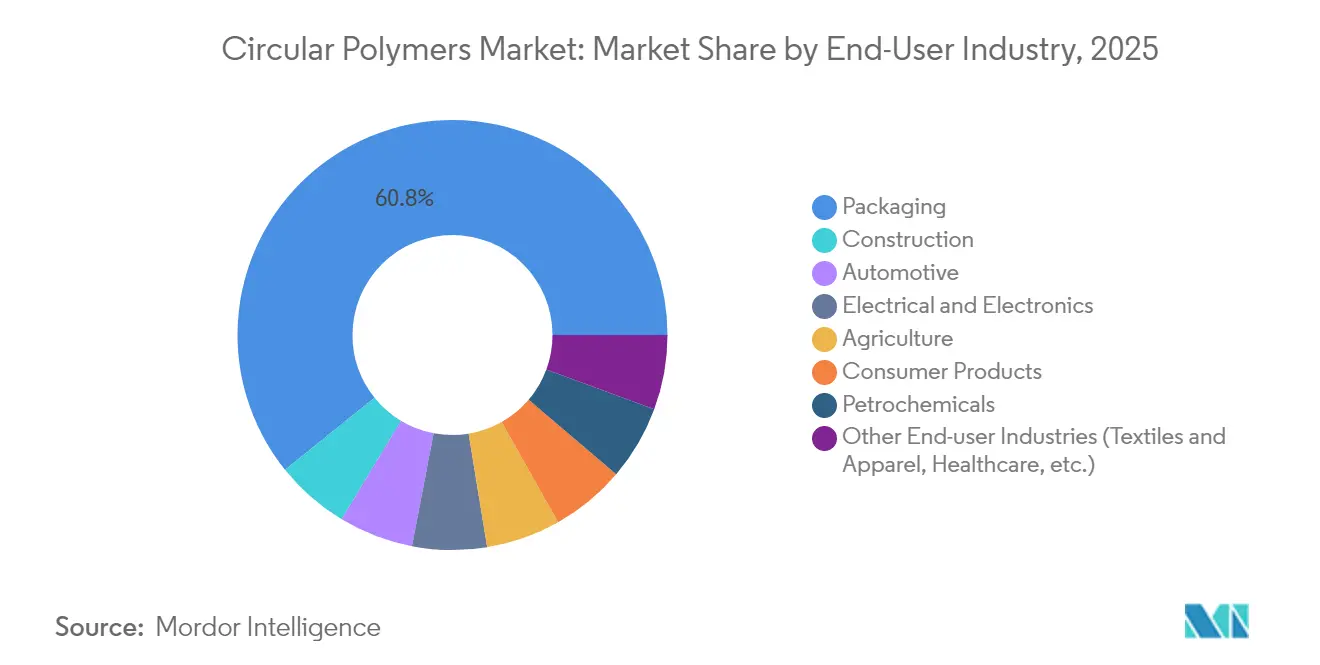

- By end-user industry, packaging commanded 60.78% share of the circular polymers market size in 2025; the other end-user industries cluster is advancing at a 8.61% CAGR through 2031.

- By region, Europe accounted for 31.22% of the circular polymers market size in 2025; Asia-Pacific records the fastest regional CAGR at 8.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Circular Polymers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Use of Recycled Polymers in Packaging Application | +2.1% | Global, with EU and North America leading adoption | Medium term (2-4 years) |

| The Growing Awareness and Regulations Promoting Circular Economy Practices | +1.8% | EU core, expanding to APAC and North America | Long term (≥ 4 years) |

| Massive investments in recycling infrastructure | +1.5% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Growing demand from the automotive sector | +1.2% | Global, with APAC and Europe leading | Medium term (2-4 years) |

| Increasing demand in construction sector for insulation, wires and carpeting | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Use of Recycled Polymers in Packaging Application

Brand-owner commitments to 50% recycled content in packaging are amplifying demand, while the EU Decision 2023/2683 enforces 25% recycled plastic in PET bottles by 2025 and 30% in all beverage bottles by 2030[1]European Commission, “Directive (EU) 2019/904 on reducing the impact of certain plastic products on the environment,” europa.eu. Companies such as Berry Global reported a 43% jump in post-consumer resin consumption under its Impact 2025 roadmap. Digital watermarks and AI-enabled sorters are improving bale purity, helping converters meet food-grade safety criteria. Mono-material flexible packs further unlock mechanical routes that were previously uneconomic. These developments enhance volume certainty for the circular polymers market and nurture long-range contracts between waste managers and resin buyers.

The Growing Awareness and Regulations Promoting Circular Economy Practices

Extended producer responsibility schemes and recycled-content mandates are embedding circularity into procurement decisions. The European Regulation (EU) 2025/351 tightens purity limits and introduces traceability protocols for recycled food-contact plastics. China’s National Center for Food Safety Risk Assessment is driving regulatory convergence with US and EU standards, paving the way for formal food-contact rules in 2025. In the United States, H.R. 9676 proposes national recycling standards targeting 50% plastics recycling by 2030[2]United States Congress, “H.R. 9676 Accelerating a Circular Economy for Plastics and Recycling Innovation Act of 2024,” govtrack.us . Such harmonization provides clearer incentives for capital allocation into next-generation recycling assets.

Massive Investments in Recycling Infrastructure

Global recycling-infrastructure investment totaled USD 160 billion between 2018 and mid-2023, focusing on collection, sorting, and advanced recycling capacity. LyondellBasell’s integrated hub in Knapsack and its EUR 40 million chemical recycling plant in Germany exemplify large-scale European projects. TotalEnergies transformed Grandpuits into France’s first zero-crude platform, complete with a 15 kiloton-per-year advanced recycling unit. Indorama Ventures’ joint ventures in India add 100 kilotons of rPET capacity annually. These projects collectively broaden feedstock coverage and underpin forecast growth in the circular polymers market.

Growing Demand from the Automotive Sector

Automakers embed secondary polymers to reduce weight and meet carbon goals. BMW plans up to 50% secondary content in its Neue Klasse vehicles while its Munich site moves to all-EV production by 2027. RadiciGroup produced an air-intake manifold from 100% recycled polyamide, cutting lifecycle CO₂ by 70%. Ford integrates post-consumer plastics into interior parts as part of its closed-loop strategy. The revised 2023 EU End-of-Life Vehicles Directive embeds recycled-plastic thresholds, supporting polymer demand beyond packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed-stock contamination variability | -1.4% | Global, particularly affecting food-grade applications | Short term (≤ 2 years) |

| Low-oil-price cost disadvantage | -0.8% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| High initial capital expenditure (CAPEX) | -0.6% | Emerging markets and smaller players | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Contamination Variability

Analytical studies found 191 pesticides and 107 pharmaceuticals in recycled pellets from multiple countries, underscoring persistent contamination risks that can breach food-contact limits. Separate collection of HDPE milk bottles mitigates cross-contamination, yet seven contamination pathways remain during mechanical reprocessing. AI-enabled sorters and digital watermarks improve homogeneity but raise CAPEX for small recyclers. These challenges add qualification costs for converters pursuing food-grade approvals, tempering near-term growth in the circular polymers market.

Low-Oil-Price Cost Disadvantage

Virgin-polymer spot prices periodically undercut recycled resin when crude prices decline, eroding recycling margins. Pyrolysis oil trades at USD 600-900 per ton while syngas delivers lower revenue streams, making profitability sensitive to fossil-fuel benchmarks. The Institute for Energy Economics and Financial Analysis reported that US virgin polypropylene prices were below recycled equivalents during most of 2024[3]Institute for Energy Economics and Financial Analysis, “Price Volatility in Plastic Markets,” ieefa.org . Policy options such as production caps on virgin plastics are under discussion to stabilize economics for the circular polymers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer: PET Dominance Meets Nylon Innovation

PET accounted for 41.62% of the circular polymers market in 2025 owing to established bottle-to-bottle loops and global brand adoption. India reached a 95% PET-bottle recycling rate with 500,000 tons annual capability. PET also benefits from clear food-grade approval pathways, positioning it for incremental gains as beverage producers ramp up recycled content. Mechanical flake pricing remained within 4% of virgin resin during late 2024, narrowing the cost hurdle.

Nylon-6 represents the fastest-growing polymer at an 8.37% CAGR through 2031. Catalyst-driven depolymerization fields high-purity caprolactam in seconds without solvents and achieves over 90% monomer recovery. Automotive lightweighting and high-performance textiles favor nylon recyclates with verified mechanical parity. Continuous-loop pilot plants in Germany and Japan plan commercial output by 2026, adding depth to the circular polymers market.

Polyolefins leverage mechanical upgrades that slash mPP recyclate costs by 30%, but food-grade compliance remains challenging. Dissolution processes evacuate pigments and odorous compounds from polypropylene at 0.32 kg CO2-equivalent emissions per kg recycled PP, opening high-value packaging uses. PVC recycling requires dechlorination, elevating processing complexity. Specialty resins such as ABS and polycarbonate register slower growth yet gain traction in consumer-electronics take-back schemes.

By Recycling Technology: Mechanical Dominance Challenged by Chemical Innovation

Mechanical recycling controlled 64.35% of the circular polymers market in 2025 thanks to incumbency and lower cost. Design-for-recycling guidelines and circuit-board grade sorters trimmed polypropylene recyclate production costs by nearly one-third, lifting margins. However, mechanical pathways still struggle with multilayer films and contaminated oceanside collections.

Chemical recycling expands at an 8.29% CAGR as pyrolysis, gasification, and solvent-based recovery unlock complex feedstocks. TotalEnergies’ Grandpuits unit produces 10,000 tons of pyrolysis oil yearly that is re-polymerized into certified circular polymers. Dissolution processes separate nylon from cotton in textile blends without compromising fiber strength. Energy-recovery plants with heat capture remain the lowest-value outlet, and critics argue they may divert feedstock from higher-value loops, an ongoing policy debate in the circular polymers market.

By End-user Industry: Packaging Leadership Drives Innovation

Packaging retained 60.78% share of the circular polymers market in 2025 under the combined force of regulation and brand commitments. Tetra Pak and Lactalis progressed mono-material cartons, and Braskem launched bio-circular polypropylene sourced from used-cooking oil for food packaging. Sorting technologies with near-infrared spectroscopy and robotics increased food-grade yields, meeting stricter migration limits under EU Regulation 2025/351.

The other end-user industries cluster grows at a 8.61% CAGR, reflecting momentum in apparel, healthcare, and household goods. Study data show recycled-plastic concrete mixes raising compressive strength by 15% while saving embedded emissions. In mobility, fishing-net-derived PA6 composites delivered 23% higher tensile strength, aligning with automaker CO2 targets. Electrical components adopt flame-retardant recyclates that meet UL 94 V-0 standards, broadening addressable market volume.

Geography Analysis

Europe held 31.22% of the circular polymers market share in 2025, anchored by stringent circular-economy directives and robust collection networks. The EU Packaging and Packaging Waste Regulation imposes staged recycled-content mandates, while the General Product Safety Regulation tightens product labeling and safety standards. Supply-demand imbalances for high-quality recyclate create premiums of up to USD 250 per ton over conventional grades, intensifying intra-EU trade in secondary polymers. Investments like LyondellBasell’s EUR 40 million chemical-recycling plant and Borealis’ Borcycle M compounding line in Belgium shore up local supply. Circularity gaps remain, prompting import partnerships with Asia-based suppliers.

Asia-Pacific records a 8.46% CAGR through 2031, the fastest among regions. China achieves a 96.48% PET-bottle recycling rate, yet only 30% of an estimated 63 million tons of overall plastic waste is recycled, leaving scope for rapid growth. India mandates 30% recycled content by 2025-2026, rising to 60% by 2028-2029, catalyzing capital inflow. Indorama Ventures’ joint platform with Dhunseri and Varun Beverages adds 100 kilotons annual rPET capacity, and Ganesha Ecopet targets 42,000 tons yearly by 2026.

North America benefits from mature mechanical lines and expanding chemical-recycling pilots. The US H.R. 9676 bill seeks 50% plastics-recycling rates by 2030, establishing unified national standards that could streamline feedstock flows. Mexico and Canada adopt compatible labeling schemes, easing regional trade in recycled flakes and pellets.

South America and the Middle East & Africa form emerging growth pockets. Brazil’s PET-bottle recycling rate rose to 56.4% by 2024 under ANVISA’s food-safety oversight. Saudi Arabia’s Vision 2030 tasks the Saudi Investment Recycling Company with achieving 95% waste recycling, eyeing SAR 120 billion GDP contribution. Project pipelines across the Gulf Cooperation Council include solvent-based recovery plants positioned to serve Asian converters.

Competitive Landscape

The circular polymers market is moderately fragmented, with traditional petrochemical firms leveraging scale and integrated feedstock networks, while specialist recyclers drive innovation. LyondellBasell acquired a 25% stake in the Cyclyx joint venture with Agilyx and ExxonMobil, gaining access to waste-sorting capacity and pyrolysis technology. Agilyx operates Circularity Centers with 20 patents on waste optimization and depolymerization. SABIC’s TRUCIRCLE program commercialized mixed-plastic recycling and established traceable downstream partnerships. TotalEnergies, in collaboration with Plastic Energy, targets 1 million tons of circular output by 2030. Patent filings focus on catalyst advancements and sensor-assisted sorting technologies. High CAPEX for chemical-recycling plants and stringent food-grade qualification protocols remain key entry barriers. Midsize recyclers mitigate risks through toll-processing contracts, ensuring closed-loop traceability.

Circular Polymers Industry Leaders

SABIC

Borealis GmbH

LyondellBasell Industries Holdings B.V.

Plastic Energy

Veolia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TotalEnergies and Plastic Energy began operations at an advanced recycling unit in Grandpuits, France, supplying 15 kilotons of feedstock annually toward a goal of 1 million tons of circular polymers by 2030.

- February 2024: TotalEnergies converted plastic-waste feedstocks into circular polypropylene at its La Porte, Texas plant, producing certified grades for food packaging.

Global Circular Polymers Market Report Scope

Circular polymers are made from plastics gathered from diverse sources, such as municipal and industrial trash. The plastic circular economy is a paradigm of closed systems that encourages polymer reuse and recycling. This concept produces value from trash and discourages the disposal of recovered plastics in landfills. The global plastics sector is looking for ways to replace fossil fuels with renewable resources. As the circular economy converts more plastic waste into recycling, sales of circular polymers are likely to expand in the coming years.

The circular polymers market is segmented by polymer, form, end-user industry, and geography. By polymer, the market is segmented into polyethylene terephthalate (PET), polyethylene, polypropylene, polyvinyl chloride (PVC), nylon 6, nylon 6,6, and other polymers (acrylonitrile). By end-user industry, the market is segmented into packaging, construction, automotive, electrical and electronics, agriculture, consumer products (household), petrochemicals, and other end-user industries (textiles, healthcare, and others). The report also offers market sizes and forecasts for 27 countries across major regions. For each segment, market sizing and forecasts were made based on volume (tons).

| Polyethylene Terephthalate (PET) |

| Polyethylene |

| Polypropylene |

| Polyvinyl Chloride (PVC) |

| Nylon-6 |

| Nylon-6,6 |

| Other Polymers (Acrylonitrile, etc.) |

| Mechanical Recycling |

| Chemical Recycling |

| Dissolution / Solvent-based |

| Pyrolysis & Gasification (Feedstock) |

| Energy Recovery (Incineration with Heat Capture) |

| Packaging |

| Construction |

| Automotive |

| Electrical and Electronics |

| Agriculture |

| Consumer Products |

| Petrochemicals |

| Other End-user Industries (Textiles and Apparel, Healthcare, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Polymer | Polyethylene Terephthalate (PET) | |

| Polyethylene | ||

| Polypropylene | ||

| Polyvinyl Chloride (PVC) | ||

| Nylon-6 | ||

| Nylon-6,6 | ||

| Other Polymers (Acrylonitrile, etc.) | ||

| By Recycling Technology | Mechanical Recycling | |

| Chemical Recycling | ||

| Dissolution / Solvent-based | ||

| Pyrolysis & Gasification (Feedstock) | ||

| Energy Recovery (Incineration with Heat Capture) | ||

| By End-user Industry | Packaging | |

| Construction | ||

| Automotive | ||

| Electrical and Electronics | ||

| Agriculture | ||

| Consumer Products | ||

| Petrochemicals | ||

| Other End-user Industries (Textiles and Apparel, Healthcare, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the circular polymers market by 2031?

The circular polymers market size is expected to reach 30.86 million tons by 2031, reflecting a 7.42% CAGR over the 2026-2031 forecast period.

Which region leads the circular polymers market today?

Europe holds the largest regional position with 31.22% of the circular polymers market share in 2025, driven by stringent recycled-content mandates.

Which polymer dominates recycled volumes?

PET leads with 41.62% share in 2025 due to well-established bottle-to-bottle loops and regulatory support for food-grade applications.

What technology currently processes most feedstock?

Mechanical recycling maintains 64.35% of circular polymers market share in 2025 thanks to mature infrastructure and favorable economics.

Page last updated on: