Chlorinated Polyethylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

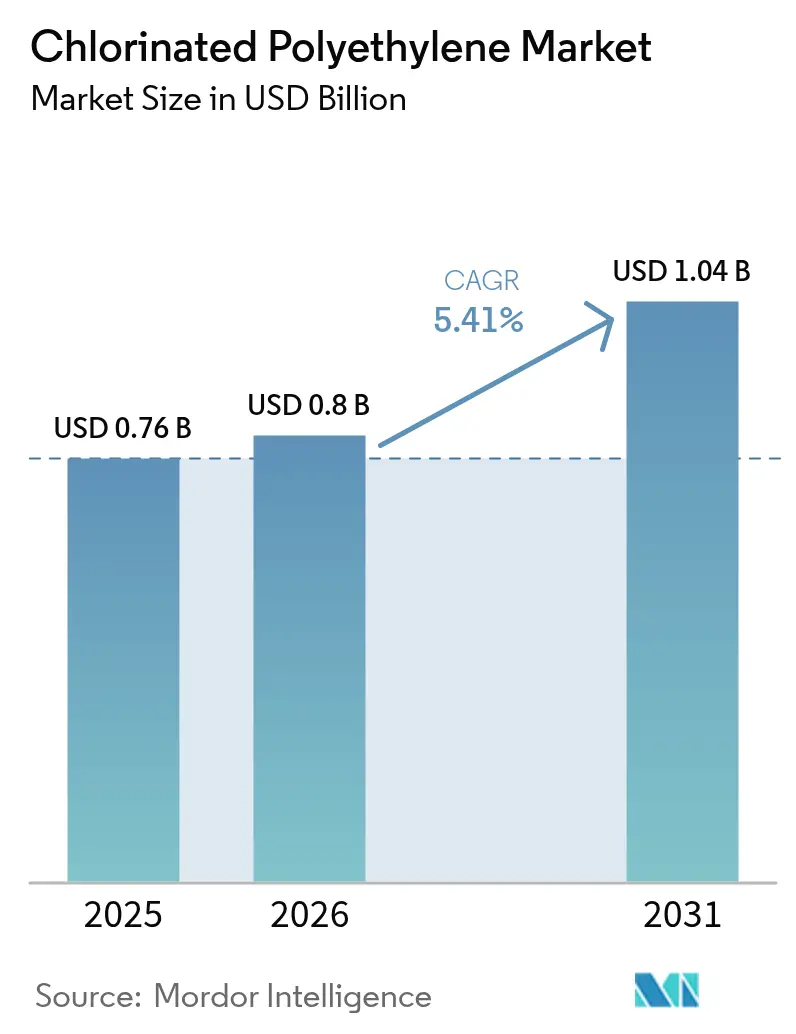

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

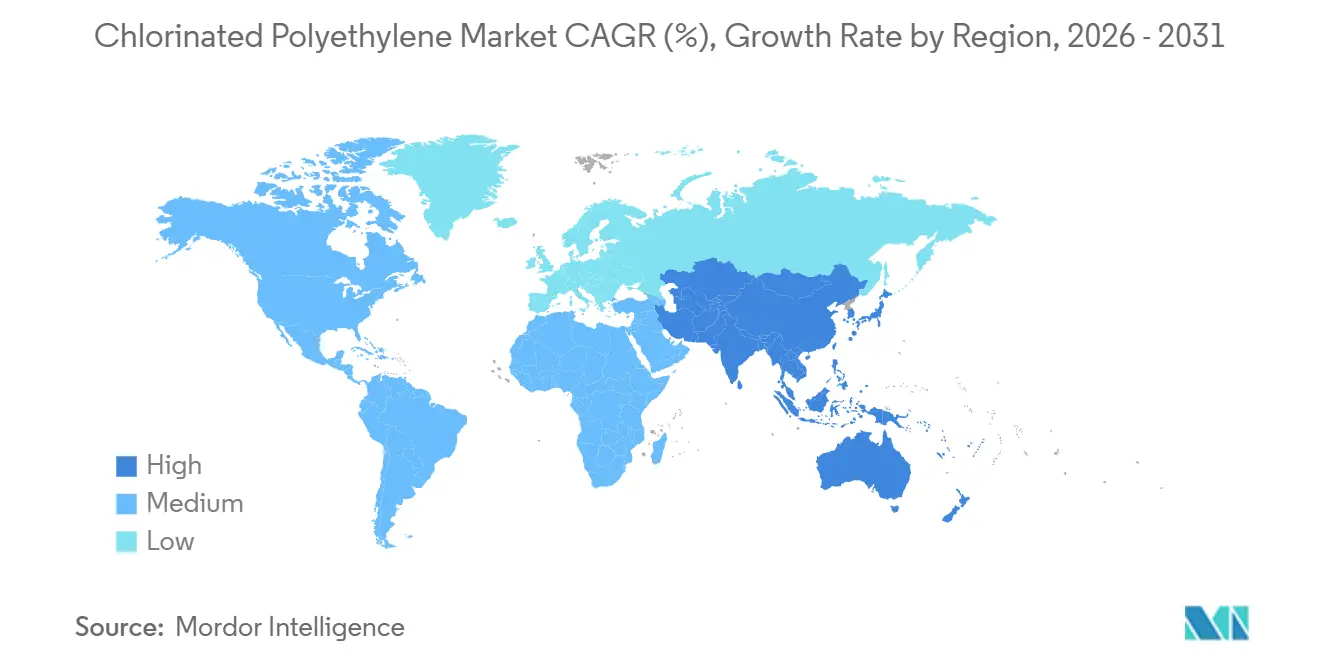

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chlorinated Polyethylene Market Analysis by Mordor Intelligence

The Chlorinated Polyethylene Market size is expected to increase from USD 0.76 billion in 2025 to USD 0.8 billion in 2026 and reach USD 1.04 billion by 2031, growing at a CAGR of 5.41% over 2026-2031. Momentum stems from the polymer’s entrenched use as a PVC impact modifier, its widening role in wire and cable jacketing, and its rising adoption in hose compounds and three-layer roofing membranes. High chlorine compatibility enables CPE to deliver cost-efficient oil resistance, flame performance, and weatherability, features that remain hard for thermoplastic polyolefins to match without expensive additives. Asia-Pacific’s dominance solidifies price leadership for the chlorinated polyethylene market: regional producers benefit from integrated chlor-alkali chains, low-cost coal or renewable electricity, and proximity to downstream PVC extrusion hubs. Halogen-free regulations in Europe and parts of North America do press formulators to partially replace CPE with TPV, SEBS, or EVA blends, yet CPE retains a defendable cost-performance niche wherever continuous oil exposure, high sunlight intensity, or tight bend radii prevail. Competitive intensity is moderate; the top five producers capture about 55–60% revenue but no firm unilaterally sets contract pricing or innovation pace.

Key Report Takeaways

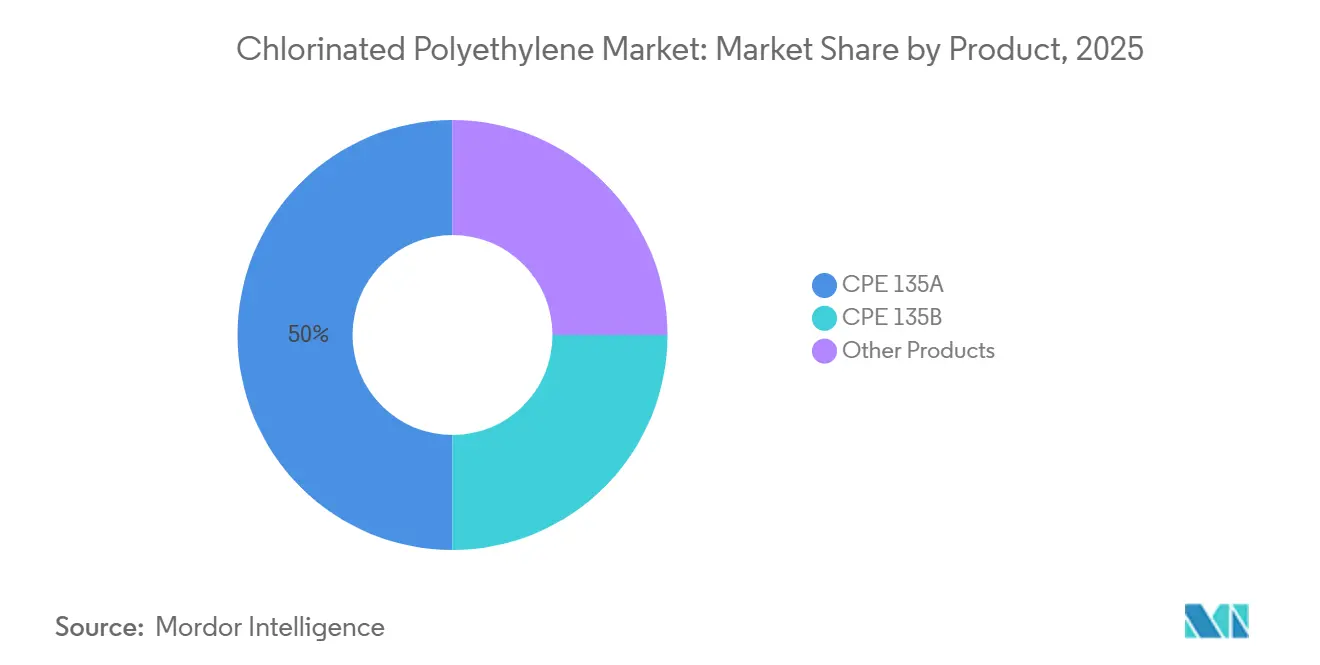

- By product grade, CPE 135A led with 52.94% revenue in 2025, while the higher-viscosity CPE 135B grade is projected to expand at a 5.51% CAGR through 2031.

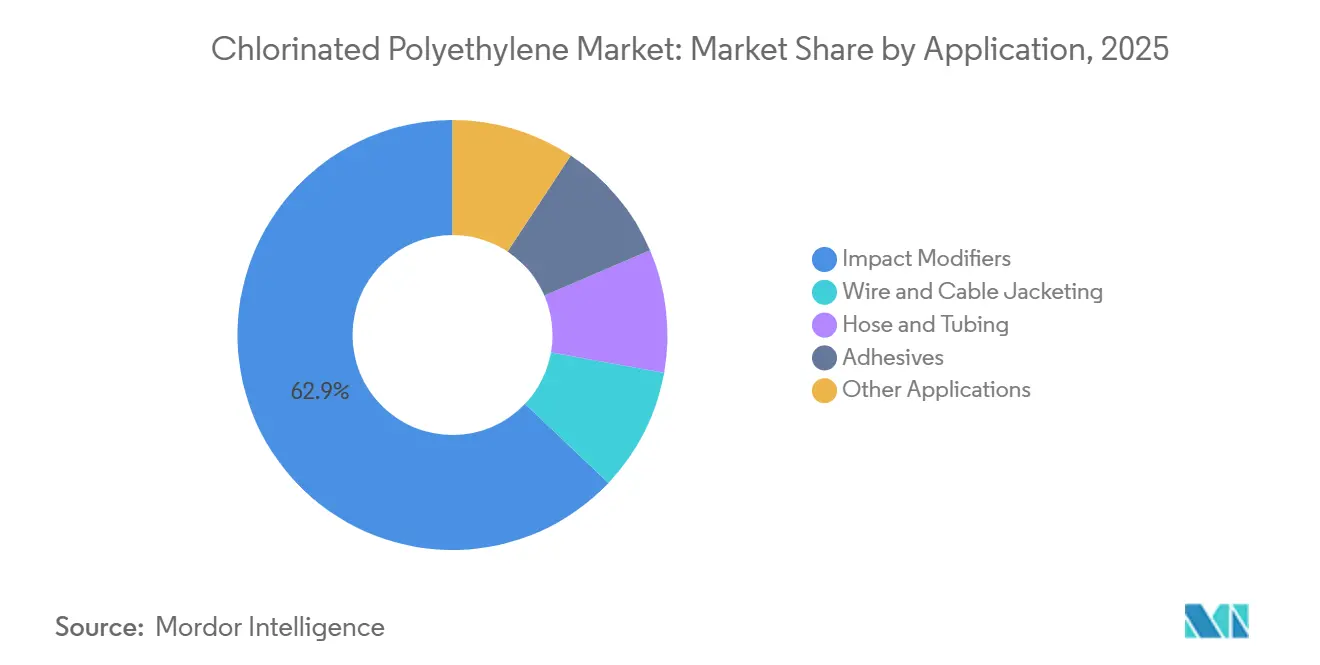

- By application, impact modifiers commanded 62.91% of the global chlorinated polyethylene market share in 2025, whereas hose and tubing is the fastest-growing end-use, advancing at 5.97% CAGR to 2031.

- By geography, Asia-Pacific accounted for 72.15% of worldwide consumption in 2025 and is set to register a 5.78% CAGR between 2026 and 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chlorinated Polyethylene Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward halogen-free flame-retardant CPE hybrids | +0.8% | North America and EU, spill-over to APAC electronics hubs | Medium term (2–4 years) |

| Chinese supply-side expansion enhancing price competitiveness | +1.2% | Global, with strongest effect in APAC and Middle East | Short term (≤ 2 years) |

| Oil-resistant hoses for hydrogen refueling infrastructure | +0.6% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Growth of 3-layer smart roofing membranes in tropical regions | +0.5% | ASEAN, Middle East, Latin America (Brazil, Mexico) | Medium term (2–4 years) |

| On-site chlorination tech cutting Scope-3 emissions in Europe | +0.4% | EU core (Netherlands, Germany, France) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Halogen-Free Flame-Retardant CPE Hybrids

Formulators are lowering total halogen content by blending CPE with phosphorus–nitrogen intumescent systems, reaching UL-94 V-0 ratings while meeting IEC 60754-2 thresholds. A 2025 study showed that adding micro-encapsulated red phosphorus and melamine cyanurate delivers limiting oxygen index values above 34% and smoke density below 80 Ds, allowing 40% less mineral hydroxide filler. North American and EU cable plants serving data centers and rail transit are early adopters because local codes mandate low-smoke performance without banning all halogens. Such “reduced-halogen” compounds lengthen the product life cycle for the chlorinated polyethylene market, though precise dispersion and moisture-resistant packaging raise formulation complexity and cost.

Chinese Supply-Side Expansion Enhancing Price Competitiveness

Integrated ethylene and chlor-alkali assets in Shandong province drove average CPE cash costs below USD 1,200 per tonne in 2025, undercutting Western producers by 20–30%[1]China Petroleum & Chemical Industry Federation, “Annual Petrochemical Capacity Report 2025,” cpcif.org.cn. Weifang Yaxing alone lifted capacity to 80,000 tpa yet saw margins narrow when export demand cooled, prompting a pivot toward greenhouse-film and specialty hose grades. Price softness benefits compounders across India, Vietnam, and Indonesia that feed cost-sensitive PVC and cable segments, although quality variability among smaller Shandong facilities stokes anti-dumping inquiries and undermines brand confidence.

Oil-Resistant Hoses for Hydrogen Refueling Infrastructure

Hydrogen hoses require outer jackets that resist mineral oil, abrasion, and sunlight. Southwire’s 2025 specifications for EV charging and oil-gas cables cite thermoset CPE jackets qualified to UL 44 and IEEE 1202 FT4 with 90 °C continuous rating[2]Southwire Company, “SPEC 45005 Thermoset CPE EV Cable,” southwire.com . While inner liners favor HNBR or FKM for permeation control, CPE captures 15–20% of the volume in external layers because polyolefins struggle to hit the same flame-oil balance without cost-intensive additives. Planned station rollouts in California, Germany, Japan, and South Korea underpin the long-term tailwind for the chlorinated polyethylene market.

Growth of 3-Layer Smart Roofing Membranes

CPE-based base sheets bonded to reflective mid-layers and UV-stabilized topcoats are gaining share in tropical climates. Their flexibility, ozone resistance, and compatibility with bitumen adhesives align with ASTM D4068 and mitigate seam failures common in thermoplastic polyolefin membranes. Embedded leak-detection sensors push initial system costs 25–35% higher but deliver lifecycle payback via lower cooling loads and rapid leak localization. Adoption is strongest in Singapore, Dubai, and metropolitan Brazil, advancing regional penetration for the chlorinated polyethylene market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU public-procurement bans on chlorinated plastics | -0.7% | EU member states, potential adoption in UK and Norway | Short term (≤ 2 years) |

| TPV and SEBS elastomer performance advances | -0.9% | Global, led by automotive OEMs in North America, EU, Japan | Medium term (2–4 years) |

| Emerging carbon-border tariffs on halogenated polymers | -0.6% | EU (CBAM), potential extensions to UK and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Public-Procurement Bans on Chlorinated Plastics

Germany, France, and the Netherlands now prioritize LSZH materials in publicly funded projects. Although REACH and CPR stop short of an outright ban, procurement guidelines cap halogen acid gas at ≤ 0.5% under IEC 60754-1. Cable and roofing suppliers must keep dual inventories, diverting CPE toward industrial markets while downtown fire codes tighten. The chlorinated polyethylene market therefore faces near-term European volume erosion and margin compression.

TPV and SEBS Elastomer Performance Advances

Dynamic vulcanizates of EPDM–PP and high-molecular SEBS systems now match CPE 135A for oil resistance and far exceed it for low-temperature flexibility, all without halogen content. Automotive wire harness and coolant hose buyers view halogen-free status as critical for recycling mandates under EU ELV directives. As TPV scaling lowers cost, the substitution pressure against the chlorinated polyethylene industry intensifies, particularly in automotive interiors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Semi-Crystalline Grades Hold Sway, Specialty Formulations Scale

The chlorinated polyethylene market size for CPE 135A accounted for 52.94% of revenue share in 2025. This semi-crystalline grade balances 35±2% chlorine with Mooney viscosity around 50, generating Shore A 60 hardness and elongation above 600%, metrics prized for rigid PVC impact modification and wire jackets. Higher-viscosity CPE 135B offers extra melt strength, unlocking blown-film and flame-retardant filler loading that underpins a forecast 5.51% CAGR through 2031. Specialty variants. high-chlorine (>40% Cl) for UL-94 V-0 cable compounds, modified molecular-weight grades for rubber magnets, and heat-stable versions for under-hood hoses, collectively broaden value pools beyond commodity resin.

Competition intensifies as producers migrate upstream: Dow, Resonac, and leading Shandong firms supply co-processed CPE-phosphorus masterbatches, enabling compounders to offer turnkey low-smoke solutions. This vertical move shields margin amid flat commodity pricing and embeds long-term customers within integrated supply contracts, reinforcing stickiness across the chlorinated polyethylene market.

By Application: Impact Modifiers Dominate, Hose and Tubing Accelerate

Impact modifiers absorbed 62.91% of 2025 demand, reflecting CPE’s ability to triple Izod impact strength of rigid PVC profiles at 5–10 phr loadings without impairing gloss or printability. The chlorinated polyethylene market share for impact-modifier use is forecast to decline modestly as TPV and ASA alloys nibble into window-frame and pipe specifications in Europe, yet absolute tonnage still rises with construction in India and ASEAN regions.

Hose and tubing will expand at a 5.97% CAGR, lifting the chlorinated polyethylene market size for this end-use toward USD 0.13 billion by 2031. Southwire’s SPEC 44122 sets jacket thickness between 3.7 mm and 8.3 mm, numbers difficult for polyolefins to hit under identical abrasion-oil-flame tests without premium ingredients. Growth stems from offshore oil hose refurbishment, hydrogen fueling lines, and high-flex mining cables in Latin America and Africa.

Geography Analysis

Asia-Pacific anchored 72.15% of 2025 global demand for the chlorinated polyethylene market and is projected to grow at a 5.78% CAGR through 2031. China harbors integrated ethylene (62 Mt y) and polyethylene (45 Mt y) assets that flow chlorine feedstock cheaply into CPE reactors. Shandong clusters deliver ex-works prices under USD 1,200 t, spurring compounders in India and Vietnam to capture share versus XLPE and TPO. Overcapacity, however, trims producer margins and invites periodic anti-dumping probes from Turkey and Brazil.

North American market growth is buoyed by EV charging cables, data-center power cords, and oil-patch hoses. Federal codes allow CPE in industrial wiring; state procurements in California increasingly request LSZH for high-occupancy transit. Southwire’s 2025 EV charge-station spec (SPEC 45005) calls for thermoset CPE jackets to assure 90 °C continuous rating and FT4 flame compliance. Such documents validate CPE’s staying power despite halogen scrutiny.

European market faces dual headwinds: national procurement bans shrink building-wire tonnage, and CBAM may raise landed costs for high-carbon imports. Local producers, led by Nobian in the Netherlands, retrofit membrane electrolysers paired with renewable electricity to cut embedded carbon and sustain domestic CPE competitiveness.

South America, the Middle East, and Africa are witnessing rising demand for chlorinated polyethylene. Brazil and Mexico deploy CPE-based three-layer roofing in tropical industrial zones; Saudi Arabia and the UAE specify CPE jackets in offshore drilling cables where 90°C oil immersion is routine. Lower regulatory pressure on halogens and heavy sunlight drive incremental uptake, supporting diversified growth across the chlorinated polyethylene market.

Competitive Landscape

The chlorinated polyethylene market is moderately consolidated. Cost-centric producers in Shandong maintain aggressive capacity ramp-ups. Weifang Yaxing’s 80 kiloton per annum plant illustrates scale economics but endures margin dilution when export pullbacks collide with domestic oversupply, leading management to channel output into film-grade CPE and specialty hose compounds.

Value-added players such as Dow and Resonac pivot toward specialty CPE. Resonac’s 2024 ELASLEN catalog lists low-chlorine grades for adhesive rubber alloys, mid-range for PVC modifiers, and high-chlorine for V-0 flame systems, bundled with formulation services to embed itself in semiconductor-equipment plates and EMI-shielding magnets. This shift lifts average selling prices and buffers against halogen-free substitution.

Emerging disruptors blend CPE with phosphorus–nitrogen synergists or pre-compound CPE-EPDM to address LSZH mandates. Their downstream integration captures margin and keeps entry barriers high. Competitive risk revolves around regulation: EU public-procurement bans and CBAM carbon factors fracture markets into compliance-premium and low-cost tiers, forcing multinationals to juggle split inventories and tailor certification pathways.

Chlorinated Polyethylene Industry Leaders

Weifang Yaxing Chemical Co. Ltd

Sundow Polymers Co. Ltd

Shandong Gaoxin Chemical Co. Ltd

Dow

Hangzhou Keli Chemical Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Weifang Yaxing completed the second debottlenecking at its 80 kiloton per annum Shouguang facility to raise specialty film-grade output by 15%.

- February 2024: Resonac released an expanded ELASLEN catalog detailing 20–45% chlorine grades positioned for semiconductor-equipment PVC plates and magnetic rubber alloys.

Global Chlorinated Polyethylene Market Report Scope

Chlorinated polyethylene (CPE) is a thermoplastic elastomer produced by chlorinating high-density polyethylene. CPE exhibits high flexibility, impact resistance, chemical resistance, weatherability, and thermal stability, which makes it a superior alternative to standard-grade polyethylene. The product is used in applications in critical industrial functions such as impact modifiers, wire and cable jacketing, adhesives, hose and tubing, and infrared absorption.

The chlorinated polyethylene market is segmented by product, application, and geography. By product type, the market is segmented into CPE 135A, CPA 135B, and other products. By application, the market is segmented into impact modifiers, wire and cable jacketing, hose and tubing, adhesives, and other applications. The report also covers the market sizes and forecasts for chlorinated polyethylene in 16 countries across major regions. For each segment, the market size and forecasts have been done on the basis of value (USD).

| CPE 135A |

| CPE 135B |

| Other Products |

| Impact Modifiers |

| Wire and Cable Jacketing |

| Hose and Tubing |

| Adhesives |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product | CPE 135A | |

| CPE 135B | ||

| Other Products | ||

| By Application | Impact Modifiers | |

| Wire and Cable Jacketing | ||

| Hose and Tubing | ||

| Adhesives | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current market size for the chlorinated polyethylene market?

The Chlorinated Polyethylene Market size is expected to increase from USD 0.76 billion in 2025 to USD 0.8 billion in 2026 and reach USD 1.04 billion by 2031, growing at a CAGR of 5.41% over 2026-2031.

Which product grade currently generates the highest revenue?

Semi-crystalline CPE 135A led with 52.94% of 2025 revenue because its 35% chlorine content optimizes PVC impact modification and wire jacketing.

Why does Asia-Pacific contribute the bulk of global demand?

Integrated chlor-alkali and PVC extrusion chains in China, India, and Southeast Asia deliver low-cost feedstock and proximity to cable and construction end-users, giving the region about 72% share in 2025.

How quickly will hose and tubing applications expand through 2031?

They are projected to post a 5.97% CAGR, propelled by hydrogen refueling, offshore hose replacement, and EV charging infrastructure.

What cost impact could the EU Carbon Border Adjustment Mechanism have on imports?

Certificates tied to embedded emissions could add EUR 50–100 per tonne for coal-powered Chinese grades once polymers enter the scheme after 2028.

How concentrated is the competitive landscape?

The top five producers control roughly 55–60% of global revenue, yielding a moderate concentration score of 6 / 10.

Page last updated on: